butterfly gandhimathi appliances€¦ · butterfly gandhimathi appliances limited q4 & fy16 ...

TRANSCRIPT

BUTTERFLY GANDHIMATHI APPLIANCES LIMITED

Q4 & FY16 www.butterflyindia.com

RESULTS PRESENTATION

www.butterflyindia.com

Safe Harbour

Certain statements in this presentation concerning our future growth prospects are forward

looking statements, which involve a number of risks and uncertainties that could cause actual

results to differ materially from those in such forward-looking statements. The risks and

uncertainties relating to these statements include, but are not limited to, fluctuations in earnings,

our ability to manage growth, competitive intensity in our industry of operations including those

factors which may affect our cost advantage, wage increases, our ability to attract and retain

highly skilled professionals, sufficient availability of raw materials, our ability to successfully

complete and integrate potential acquisitions, liability for damages on our contracts to supply

products, the success of the companies in which Butterfly Gandhimathi Appliances Ltd has made

strategic investments, withdrawal of governmental fiscal incentives, political instability, legal

restrictions on raising capital or acquiring companies outside India, and unauthorized use of our

intellectual property and general economic conditions affecting our industry. Butterfly

Gandhimathi Appliances Ltd may, from time to time, make additional written and oral forward-

looking statements, including our reports to shareholders. The Company does not undertake to

update any forward-looking statement that may be made from time to time by or on behalf of the

company

3

www.butterflyindia.com

Contents

4

Company Overview 1

Financial Overview

Q4 & FY16 Operating Performance & Highlights

2

3

Outlook 4

www.butterflyindia.com

Company Overview 1

www.butterflyindia.com

About Us..

6

Leading manufacturer of Kitchen and Electrical Appliances

The „Butterfly‟ brand is a highly respected brand synonymous with quality

Headquartered in Tamil Nadu with Pan India presence

Strong R&D focus which has led to several pioneering initiatives and continues to drive in-house development of new products

Healthy Balance Sheet with continuously improving Financial Indicators

Mix of industry growth and Company initiatives has led to traction in Revenues in last few years

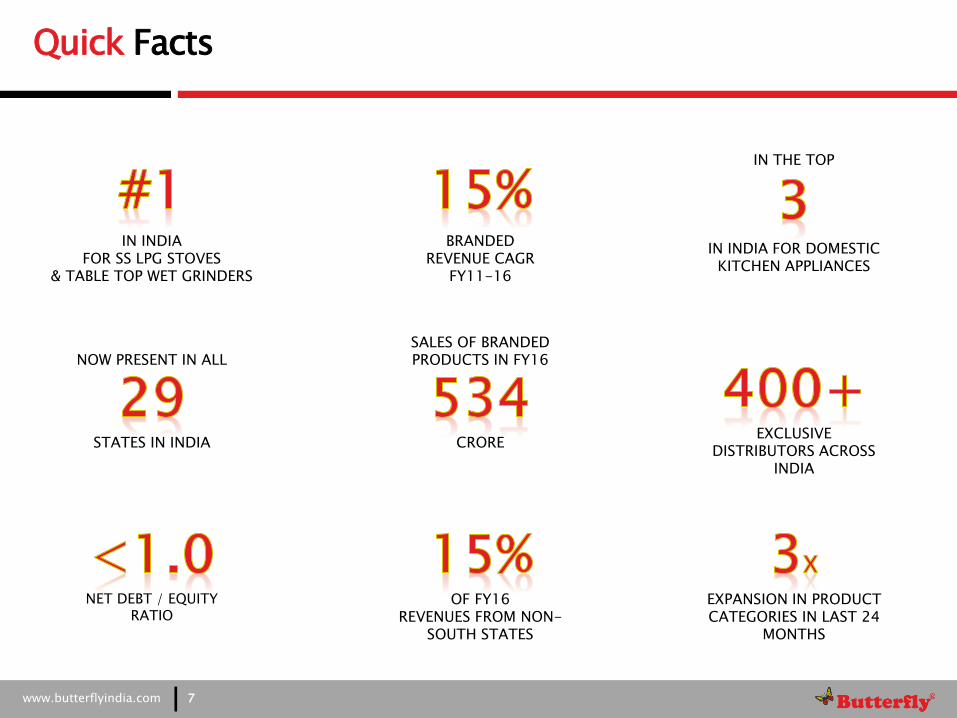

Market Leader in India for SS LPG Stoves & Table Top Wet Grinders and major supplier of Mixer Grinders & Pressure Cookers

Established in 1986 by Shri V. Murugesa Chettiar - currently helmed by 2nd and 3rd generation of promoter family

www.butterflyindia.com

Quick Facts

7

BRANDED

REVENUE CAGR FY11-16

EXCLUSIVE DISTRIBUTORS ACROSS

INDIA

STATES IN INDIA

CRORE

IN INDIA FOR SS LPG STOVES

& TABLE TOP WET GRINDERS

NET DEBT / EQUITY

RATIO

OF FY16

REVENUES FROM NON-SOUTH STATES

IN INDIA FOR DOMESTIC KITCHEN APPLIANCES

IN THE TOP

NOW PRESENT IN ALL

EXPANSION IN PRODUCT CATEGORIES IN LAST 24

MONTHS

SALES OF BRANDED PRODUCTS IN FY16

www.butterflyindia.com

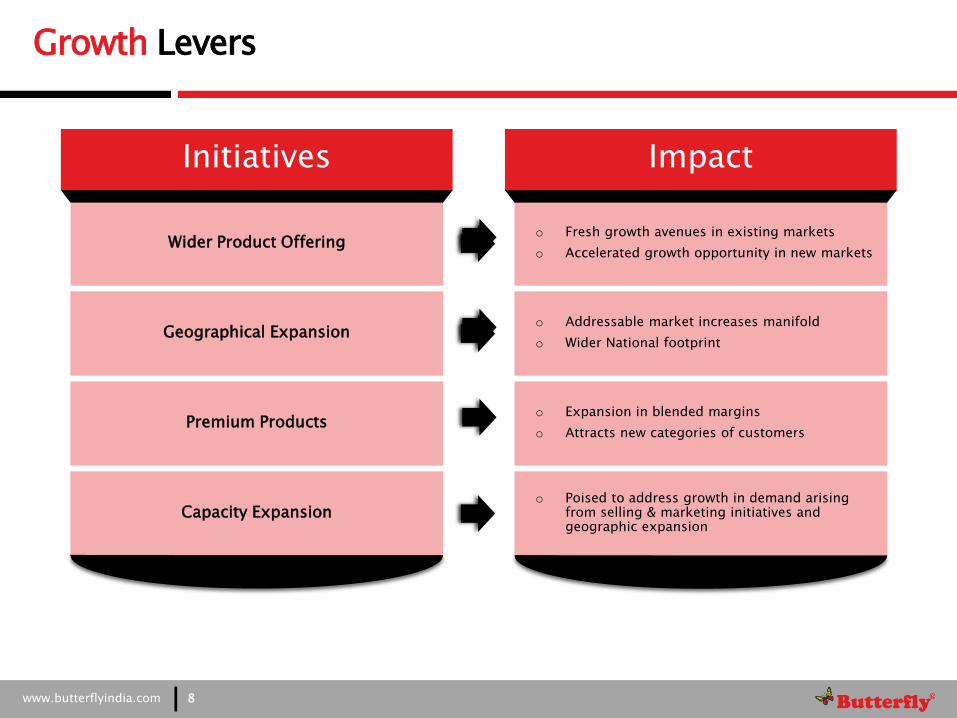

Capacity Expansion

Premium Products o Expansion in blended margins

o Attracts new categories of customers

o Poised to address growth in demand arising from selling & marketing initiatives and geographic expansion

Initiatives

Wider Product Offering

Impact

o Fresh growth avenues in existing markets

o Accelerated growth opportunity in new markets

o Addressable market increases manifold

o Wider National footprint Geographical Expansion

Growth Levers

8

www.butterflyindia.com

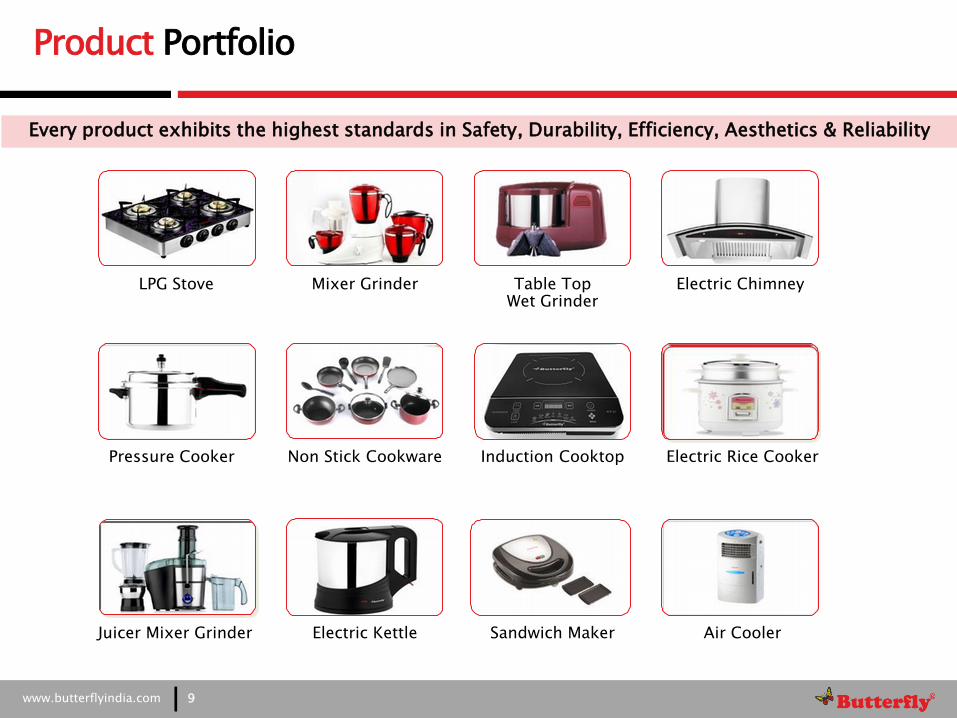

Product Portfolio

9

LPG Stove Table Top Wet Grinder

Pressure Cooker Non Stick Cookware

Mixer Grinder

Induction Cooktop

Electric Kettle Sandwich Maker Juicer Mixer Grinder

Every product exhibits the highest standards in Safety, Durability, Efficiency, Aesthetics & Reliability

Electric Chimney

Electric Rice Cooker

Air Cooler

www.butterflyindia.com

Product Portfolio

10

Other Pioneering Products

Electric Iron Pop-up Toaster

Juicer Hand Blender Washer Water Heater

www.butterflyindia.com

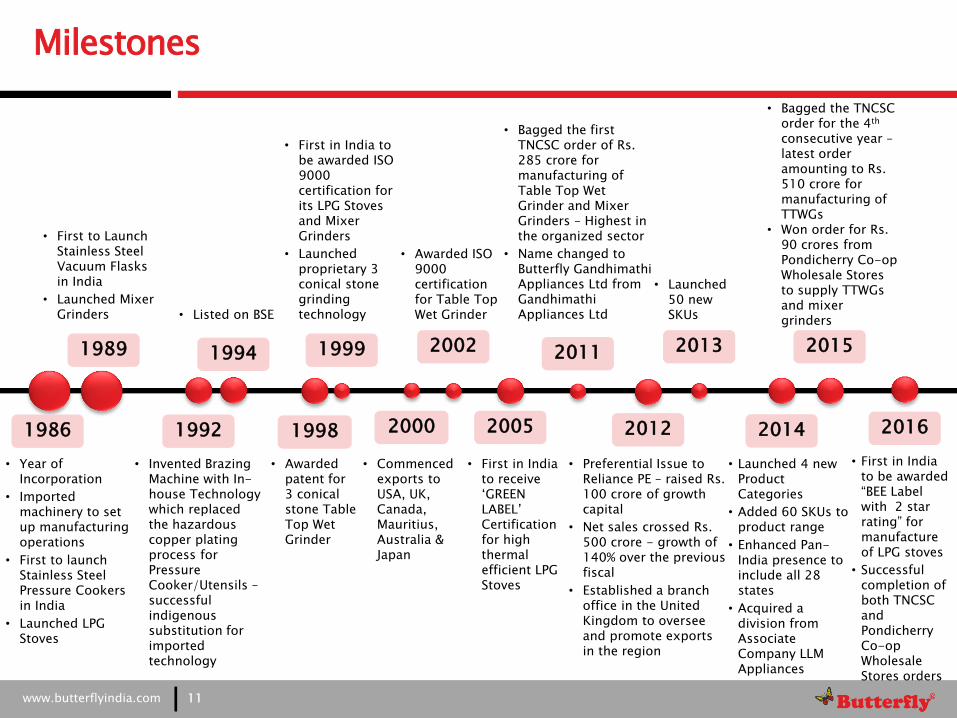

Milestones

11

1986

1999 2011 1989

1992 2000 2012

2013

• Preferential Issue to Reliance PE – raised Rs. 100 crore of growth capital

• Net sales crossed Rs. 500 crore - growth of 140% over the previous fiscal

• Established a branch office in the United Kingdom to oversee and promote exports in the region

• Launched 50 new SKUs

• Bagged the first TNCSC order of Rs. 285 crore for manufacturing of Table Top Wet Grinder and Mixer Grinders – Highest in the organized sector

• Name changed to Butterfly Gandhimathi Appliances Ltd from Gandhimathi Appliances Ltd

• First in India to be awarded ISO 9000 certification for its LPG Stoves and Mixer Grinders

• Launched proprietary 3 conical stone grinding technology

• Year of Incorporation

• Imported machinery to set up manufacturing operations

• First to launch Stainless Steel Pressure Cookers in India

• Launched LPG Stoves

• Listed on BSE

• Invented Brazing Machine with In-house Technology which replaced the hazardous copper plating process for Pressure Cooker/Utensils – successful indigenous substitution for imported technology

• First to Launch Stainless Steel Vacuum Flasks in India

• Launched Mixer Grinders

2014

• Launched 4 new Product Categories

• Added 60 SKUs to product range

• Enhanced Pan-India presence to include all 28 states

• Acquired a division from Associate Company LLM Appliances

2002

• Awarded ISO 9000 certification for Table Top Wet Grinder

2005

• First in India to receive „GREEN LABEL‟ Certification for high thermal efficient LPG Stoves

1994

• Commenced exports to USA, UK, Canada, Mauritius, Australia & Japan

1998

• Awarded patent for 3 conical stone Table Top Wet Grinder

2015

• Bagged the TNCSC order for the 4th consecutive year – latest order amounting to Rs. 510 crore for manufacturing of TTWGs

• Won order for Rs. 90 crores from Pondicherry Co-op Wholesale Stores to supply TTWGs and mixer grinders

2016

• First in India to be awarded “BEE Label with 2 star rating” for manufacture of LPG stoves

• Successful completion of both TNCSC and Pondicherry Co-op Wholesale Stores orders

www.butterflyindia.com

Revenue Profile

12

100% 56%

54% 61% 84% 54%

44%

46% 39%

16%

46%

FY11 FY12 FY13 FY14 FY15 FY16

Branded Sales Govt Order

Annual Revenue (Rs. crore)

807

642

267

839

577

CAGR: 30%

Note: FY15 Government Tender was deferred and combined with FY16 tender which resulted in increased Govt. revenues in FY16

995

www.butterflyindia.com

Government Orders

13

369 331

92

461

FY13 FY14 FY15* FY16

Government Order Sales (Rs. crore)

For the last 4 years in succession, BGMAL won orders in the annual tender of Tamil Nadu Civil Supplies Corporation (TNCSC). In January 2015, the Company bagged orders worth Rs. 510 crore* for supply of Table Top Wet Grinders from TN Govt in CY2016. This order marked the completion of the TN Govt order under the current regime

In August 2015, the Company also bagged orders worth Rs. 90 crore for supply of Table Top Wet Grinders and Mixer Grinders from Pondicherry Co-Op. Wholesale Stores (PCWS)

16.1 15.9

4.5

21.3

3.0 0.7 0.0 3.0

FY13 FY14 FY15 FY16

Products supplied (in lakh units)

TTWG Mixer Grinder

Benefits to BGMAL

• Incremental contribution to profitability, favorable payment terms enabling a positive cash flow business

• Increase in volumes have elevated BGMAL‟s manufacturing and delivery capabilities

• Increased number of users of the Company‟s products has led to an increase in the potential market for the Company

• Creates ready customer base which will materialize at the time of product replacement or upgradation

• Delivery experience has led to innovation and launch of economy models which have aided growth in Branded Sales

Note: Govt. Order for FY15 was received only in Jan, 2015 hence the revenues accrued primarily in FY16.

* The order size for TNCSC has been revised from Rs. 510 crore to Rs. 463 crore

Orders received from

Order size (Rs. Crore)

Completed till-date

(Rs. Crore)

Balance (Rs. Crore)

TNCSC* 463 463 0

PCWS 90 90 0

TOTAL 553 553 0

www.butterflyindia.com

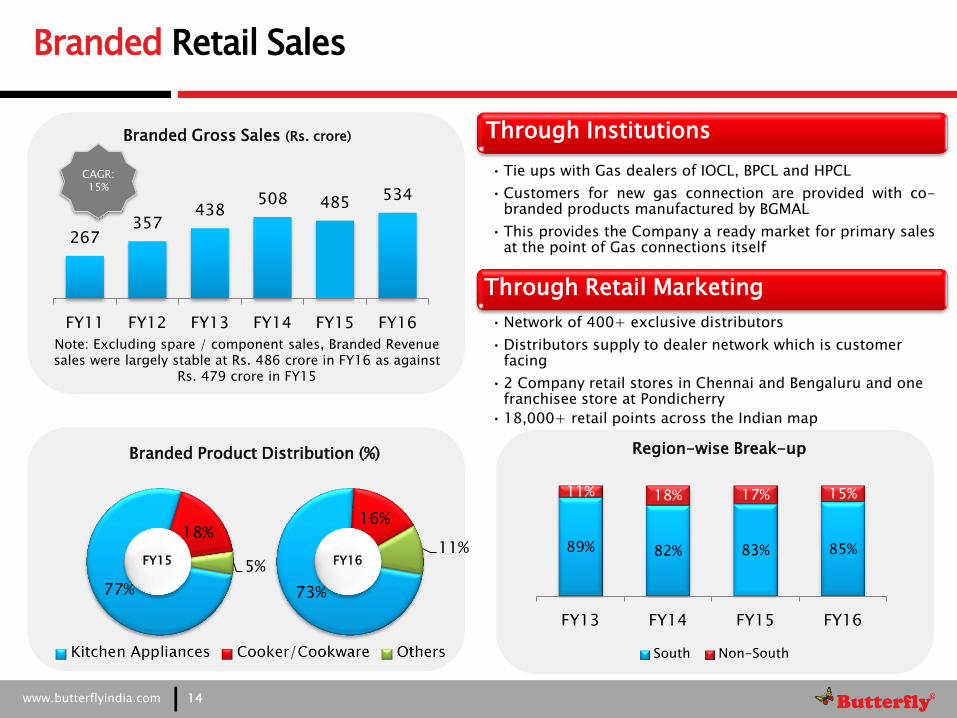

Branded Retail Sales

14

267 357

438 508 485

534

FY11 FY12 FY13 FY14 FY15 FY16

Branded Gross Sales (Rs. crore) Through Institutions

• Tie ups with Gas dealers of IOCL, BPCL and HPCL

• Customers for new gas connection are provided with co-branded products manufactured by BGMAL

• This provides the Company a ready market for primary sales at the point of Gas connections itself

77%

18%

5%

Through Retail Marketing

• Network of 400+ exclusive distributors

• Distributors supply to dealer network which is customer facing

• 2 Company retail stores in Chennai and Bengaluru and one franchisee store at Pondicherry

• 18,000+ retail points across the Indian map

73%

16%

11% FY15 FY16

89% 82% 83% 85%

11% 18% 17% 15%

FY13 FY14 FY15 FY16

Region-wise Break-up

South Non-South

CAGR: 15%

Branded Product Distribution (%)

Note: Excluding spare / component sales, Branded Revenue sales were largely stable at Rs. 486 crore in FY16 as against

Rs. 479 crore in FY15

www.butterflyindia.com

Enhancing Sales and Marketing Efficiency For Better Penetration And Brand Development

Increased Product Categories For Wider Product Portfolio And Higher Market Share

Augmenting Organic Growth

15

6 6 6

20+ 20+ 20+

2011 2012 2013 2014 2015 2016

Product Categories (Nos.)

250 250 320

500 552 554

2011 2012 2013 2014 2015 2016

SKUs (Nos.)

180 180 240

425 359

310

2011 2012 2013 2014 2015 2016

Sales Team (Personnel)

16

46 49 49 37

68

2011 2012 2013 2014 2015 2016

Marketing Spend (Rs. Cr)

www.butterflyindia.com

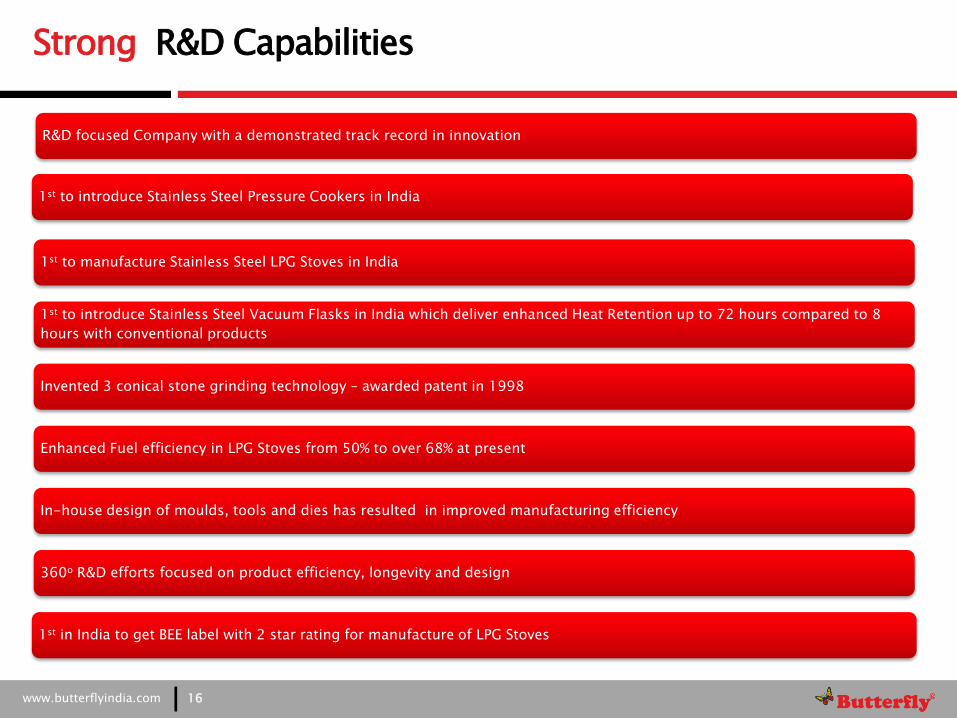

Strong R&D Capabilities

R&D focused Company with a demonstrated track record in innovation

1st to introduce Stainless Steel Pressure Cookers in India

1st to manufacture Stainless Steel LPG Stoves in India

1st to introduce Stainless Steel Vacuum Flasks in India which deliver enhanced Heat Retention up to 72 hours compared to 8

hours with conventional products

Invented 3 conical stone grinding technology – awarded patent in 1998

Enhanced Fuel efficiency in LPG Stoves from 50% to over 68% at present

In-house design of moulds, tools and dies has resulted in improved manufacturing efficiency

360o R&D efforts focused on product efficiency, longevity and design

1st in India to get BEE label with 2 star rating for manufacture of LPG Stoves

16

www.butterflyindia.com

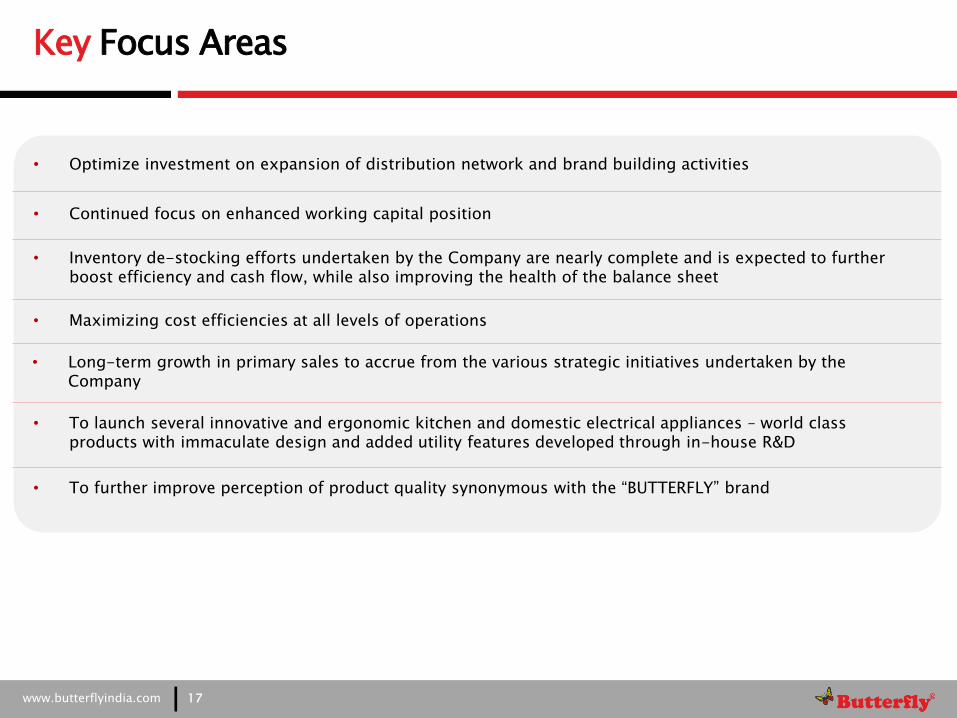

Key Focus Areas

17

• Optimize investment on expansion of distribution network and brand building activities

• Continued focus on enhanced working capital position

• Maximizing cost efficiencies at all levels of operations

• To launch several innovative and ergonomic kitchen and domestic electrical appliances – world class products with immaculate design and added utility features developed through in-house R&D

• To further improve perception of product quality synonymous with the “BUTTERFLY” brand

• Inventory de-stocking efforts undertaken by the Company are nearly complete and is expected to further boost efficiency and cash flow, while also improving the health of the balance sheet

• Long-term growth in primary sales to accrue from the various strategic initiatives undertaken by the Company

www.butterflyindia.com

Financial Overview 2

www.butterflyindia.com

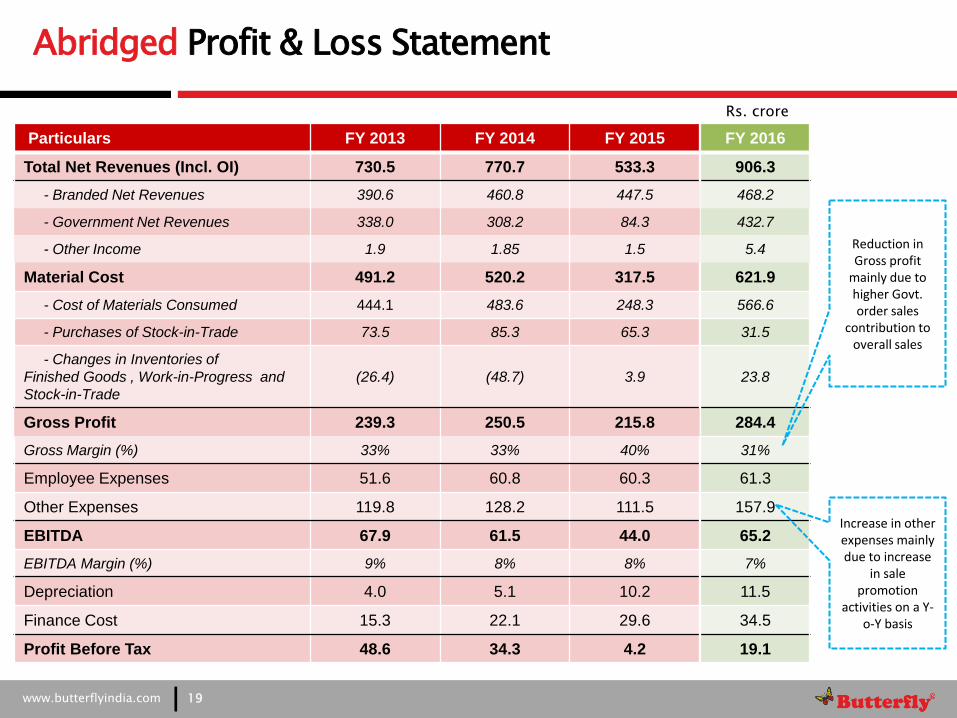

Abridged Profit & Loss Statement

19

Particulars FY 2013 FY 2014 FY 2015

Total Net Revenues (Incl. OI) 730.5 770.7 533.3

- Branded Net Revenues 390.6 460.8 447.5

- Government Net Revenues 338.0 308.2 84.3

- Other Income 1.9 1.85 1.5

Material Cost 491.2 520.2 317.5

- Cost of Materials Consumed 444.1 483.6 248.3

- Purchases of Stock-in-Trade 73.5 85.3 65.3

- Changes in Inventories of

Finished Goods , Work-in-Progress and

Stock-in-Trade

(26.4) (48.7) 3.9

Gross Profit 239.3 250.5 215.8

Gross Margin (%) 33% 33% 40%

Employee Expenses 51.6 60.8 60.3

Other Expenses 119.8 128.2 111.5

EBITDA 67.9 61.5 44.0

EBITDA Margin (%) 9% 8% 8%

Depreciation 4.0 5.1 10.2

Finance Cost 15.3 22.1 29.6

Profit Before Tax 48.6 34.3 4.2

Rs. crore

FY 2016

906.3

468.2

432.7

5.4

621.9

566.6

31.5

23.8

284.4

31%

61.3

157.9

65.2

7%

11.5

34.5

19.1

Increase in other expenses mainly due to increase

in sale promotion

activities on a Y-o-Y basis

Reduction in Gross profit

mainly due to higher Govt. order sales

contribution to overall sales

www.butterflyindia.com

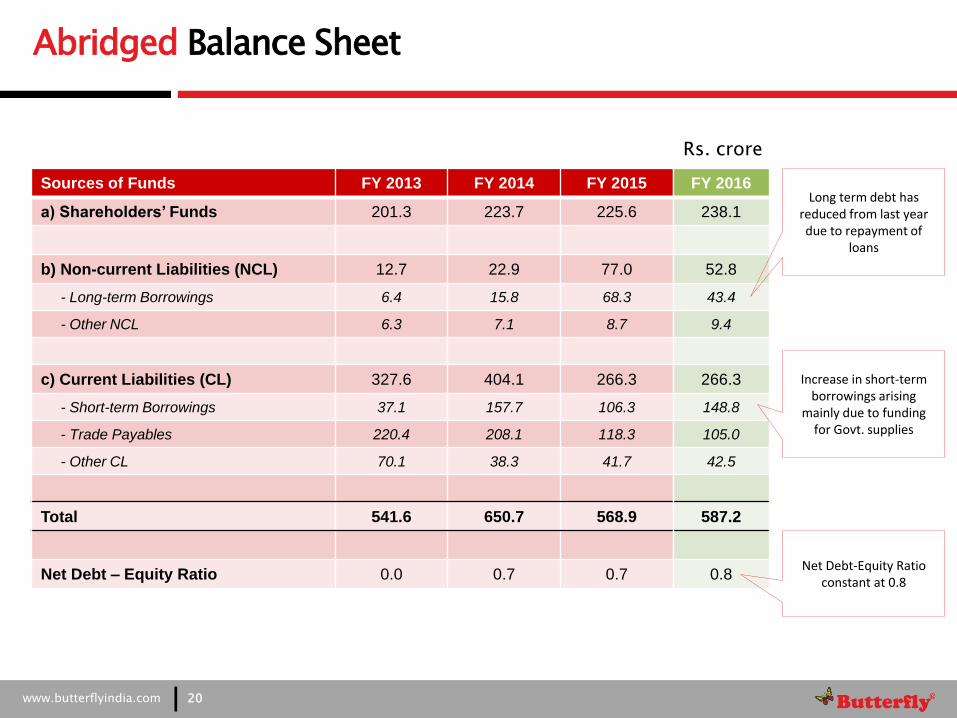

Abridged Balance Sheet

20

Sources of Funds FY 2013 FY 2014 FY 2015

a) Shareholders’ Funds 201.3 223.7 225.6

b) Non-current Liabilities (NCL) 12.7 22.9 77.0

- Long-term Borrowings 6.4 15.8 68.3

- Other NCL 6.3 7.1 8.7

c) Current Liabilities (CL) 327.6 404.1 266.3

- Short-term Borrowings 37.1 157.7 106.3

- Trade Payables 220.4 208.1 118.3

- Other CL 70.1 38.3 41.7

Total 541.6 650.7 568.9

Net Debt – Equity Ratio 0.0 0.7 0.7

Rs. crore

FY 2016

238.1

52.8

43.4

9.4

266.3

148.8

105.0

42.5

587.2

0.8

Long term debt has reduced from last year due to repayment of

loans

Increase in short-term borrowings arising

mainly due to funding for Govt. supplies

Net Debt-Equity Ratio constant at 0.8

www.butterflyindia.com

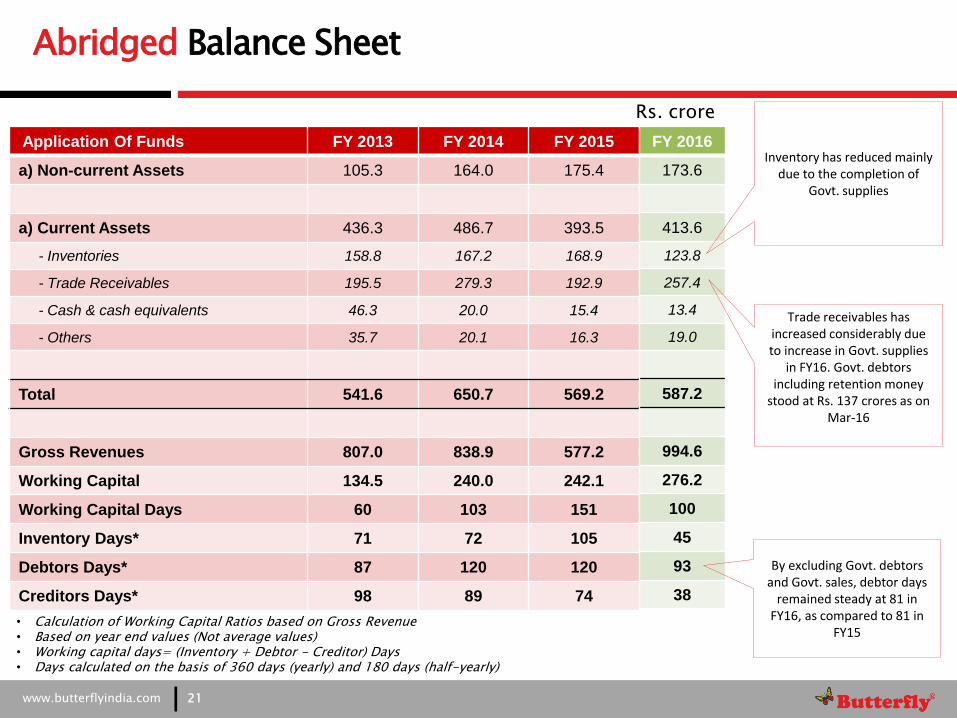

Abridged Balance Sheet

21

Application Of Funds FY 2013 FY 2014 FY 2015

a) Non-current Assets 105.3 164.0 175.4

a) Current Assets 436.3 486.7 393.5

- Inventories 158.8 167.2 168.9

- Trade Receivables 195.5 279.3 192.9

- Cash & cash equivalents 46.3 20.0 15.4

- Others 35.7 20.1 16.3

Total 541.6 650.7 569.2

Gross Revenues 807.0 838.9 577.2

Working Capital 134.5 240.0 242.1

Working Capital Days 60 103 151

Inventory Days* 71 72 105

Debtors Days* 87 120 120

Creditors Days* 98 89 74

• Calculation of Working Capital Ratios based on Gross Revenue • Based on year end values (Not average values) • Working capital days= (Inventory + Debtor - Creditor) Days • Days calculated on the basis of 360 days (yearly) and 180 days (half-yearly)

Rs. crore

FY 2016

173.6

413.6

123.8

257.4

13.4

19.0

587.2

994.6

276.2

100

45

93

38

Inventory has reduced mainly due to the completion of

Govt. supplies

Trade receivables has increased considerably due to increase in Govt. supplies

in FY16. Govt. debtors including retention money

stood at Rs. 137 crores as on Mar-16

By excluding Govt. debtors and Govt. sales, debtor days

remained steady at 81 in FY16, as compared to 81 in

FY15

www.butterflyindia.com

Performance Track Record - Annualized

22

267

642 807 839

577

995

FY11* FY12 FY13 FY14 FY15 FY16

Total Revenue (Rs crore)

27

63 73

62

44

65

FY11* FY12 FY13 FY14 FY15 FY16

EBITDA (Rs crore)

18

44 48

34

4

19

FY11* FY12 FY13 FY14 FY15 FY16

Profit Before Tax (Rs crore)

19

30 33

22

3

12

FY11* FY12 FY13 FY14 FY15 FY16

Profit After Tax (Rs crore)

CAGR: 30%

CAGR: 19%

NOTE : * FY11 was for period of 9 months ended on 31.03.2011. The figures above represent the annualized numbers in order to facilitate a comparison.

www.butterflyindia.com

Key Financials

23

20 20 19

13

2

7

FY11 @ FY12 FY13 FY14 FY15 FY16

Earning Per Share (Rs) - Annualized

43 49

113 125 126

133

FY11 FY12 FY13 FY14 FY15 FY16

Book value per share (Rs)

@ FY11 was for period of 9 months ending 31.03.2011. The figures above represent the annualized numbers in order to facilitate a comparison.

www.butterflyindia.com

Key Financials

24

41 76

201 224 226 239

FY11 FY12 FY13 FY14 FY15 FY16

Net Worth (Rs crore)

68 84

1

154 159 177

FY11 FY12 FY13 FY14 FY15 FY16

Net Debt (Rs crore)

1.6

1.1

0.0

0.7 0.7 0.8

FY11 FY12 FY13 FY14 FY15 FY16

Net Debt - Equity Ratio

140

587 492 523

343 298

FY11 FY12 FY13 FY14 FY15 FY16

Market Cap (Rs crore)

• *Increase in Net debt in FY2016 is mainly due to the funding for Govt. orders in FY16

www.butterflyindia.com

Q4 & FY16 Operating Performance & Highlights 3

www.butterflyindia.com

• Total Income (Net) during Q4 FY16 stood at Rs. 156.8 crore,

registering a growth of 4.6% Y-o-Y

• Branded sales grew by 58.5% on a Y-o-Y basis to Rs.

104.0 crore in Q4 FY16 due to lower base effect

• EBITDA improved by 17.6% and stood at Rs. 14 crore in Q4

FY16 as against Rs. 11.9 crore in Q4 FY15

• PAT stood at Rs. 0.6 crore in Q4 FY16, translating into an

EPS of Rs. 0.3

Q4 FY16 – Performance highlights

26

65.6 104.0

84.3 52.8

Q4FY15 Q4FY16Branded Sales Govt Order Sales

Total Income (Net) (Rs. crore)

Detailed Performance Overview discussed on Slide 29

0.9

0.6

Q4FY15 Q4FY16

PAT (Rs crore)

11.9

14.0

Q4FY15 Q4FY16

EBITDA (Rs. crore)

149.9 156.8

www.butterflyindia.com

• Total Income (Net) during FY16 stood at Rs. 906 crore

• Within total revenues, Branded Sales was higher by

5.5% on a Y-o-Y basis to Rs. 473.6 crore in FY16

• EBITDA stood at Rs. 65.2 crore in FY16 as against Rs. 44

crore in FY15, registering a growth of 48%

• PAT stood at Rs. 12.4 crore in FY16, translating into an EPS

of Rs. 6.9

• Dividend has been declared at Rs. 1.25 per share

FY16 – Performance highlights

27

449.0 473.6

84.3

432.7

FY15 FY16Branded Sales Govt Order Sales

Total Income (Net) (Rs. crore)

Detailed Performance Overview discussed on Slide 29

2.8

12.4

FY15 FY16

PAT (Rs crore)

44.0

65.2

FY15 FY16

EBITDA (Rs. crore)

533.3

906.3

www.butterflyindia.com

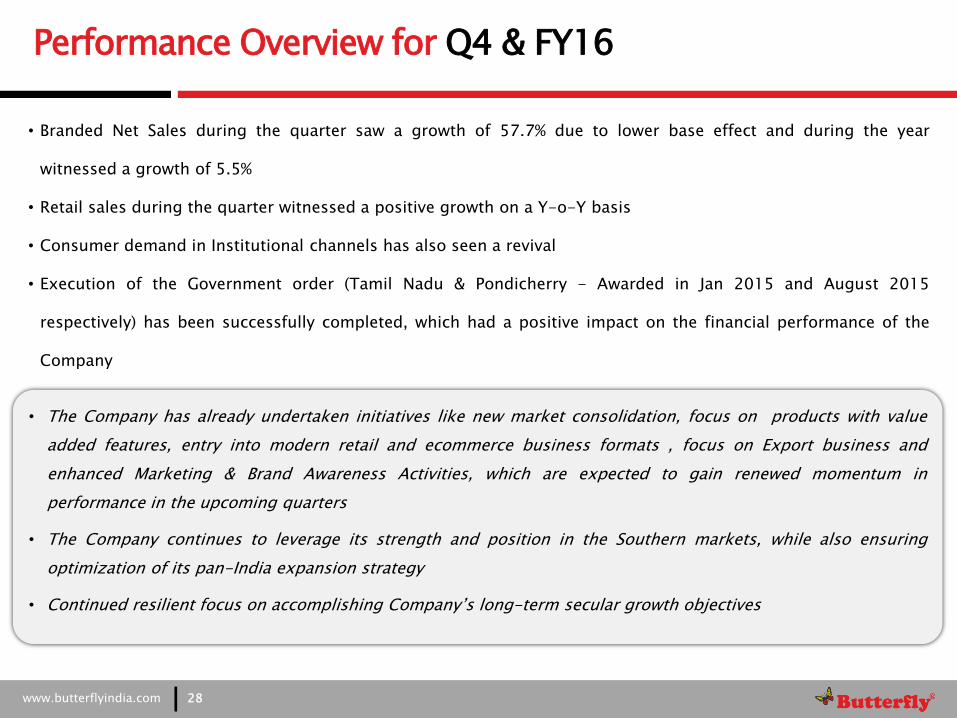

Performance Overview for Q4 & FY16

28

• The Company has already undertaken initiatives like new market consolidation, focus on products with value

added features, entry into modern retail and ecommerce business formats , focus on Export business and

enhanced Marketing & Brand Awareness Activities, which are expected to gain renewed momentum in

performance in the upcoming quarters

• The Company continues to leverage its strength and position in the Southern markets, while also ensuring

optimization of its pan-India expansion strategy

• Continued resilient focus on accomplishing Company‟s long-term secular growth objectives

• Branded Net Sales during the quarter saw a growth of 57.7% due to lower base effect and during the year

witnessed a growth of 5.5%

• Retail sales during the quarter witnessed a positive growth on a Y-o-Y basis

• Consumer demand in Institutional channels has also seen a revival

• Execution of the Government order (Tamil Nadu & Pondicherry - Awarded in Jan 2015 and August 2015

respectively) has been successfully completed, which had a positive impact on the financial performance of the

Company

www.butterflyindia.com

Product Categories

29

Kitchen Appliances

•LPG Stove

•Mixer Grinder

•Table Top Wet Grinder

•Electric Chimney

•Hand Blender

•Induction Cooktop

•Electric Kettle

•Juicer

•Juicer Mixer Grinder

•Slice Toaster

•Sandwich Maker

Cookers/Cookware

•Pressure Cooker

•Non-Stick Cookware

•Electric Rice Cooker

Others

•Air Cooler

•Water Heater (Geyser)

•Other Trading Goods

•Electric Iron

www.butterflyindia.com

Key Highlights

30

• The Retail market demand was subdued for most part of the year. Given the lower base in FY15, the growth is substantial

• Institutional demand witnessed a positive growth

• Fan category has been discontinued from FY16, which contributed to the reduction in Others product category sales on a Y-o-Y basis

Product Q4 FY16 Q3 FY16 Q4 FY15 Y-o-Y Growth

FY16 FY15 Y-o-Y Growth

Branded Market

Kitchen Appliances 85.3 99.0 45.6 87.1% 387.7 367.4 5.5%

Cooker/Cookware 19.4 26.1 11.7 65.8% 86.7 86.5 0.2%

Others 4.4 2.8 8.2 -46.3% 13.1 24.0 -45.4%

Total-Branded 109.1 127.9 65.5 66.6% 487.5 477.9 2.0%

Others (Components / Spares) 4.9 7.3 6.0 -18.3% 46.5 7.1 554.9%

Grand Total 114.0 135.2 71.5 59.4% 534.0 485.0 10.1%

Branded Gross Sales (including excise) (Rs crore)

www.butterflyindia.com

Outlook 4

www.butterflyindia.com

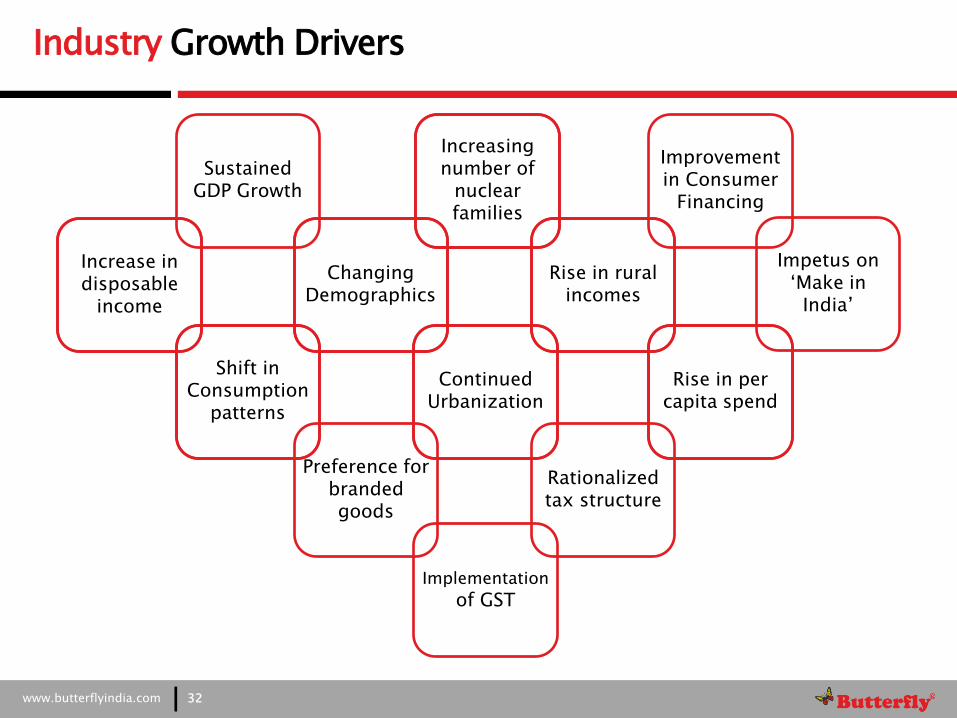

Industry Growth Drivers

32

Increasing number of

nuclear families

Improvement in Consumer

Financing

Sustained GDP Growth

Changing Demographics

Rise in rural incomes

Continued Urbanization

Rise in per capita spend

Rationalized tax structure

Increase in disposable

income

Shift in Consumption

patterns

Preference for branded goods

Impetus on „Make in

India‟

Implementation of GST

www.butterflyindia.com

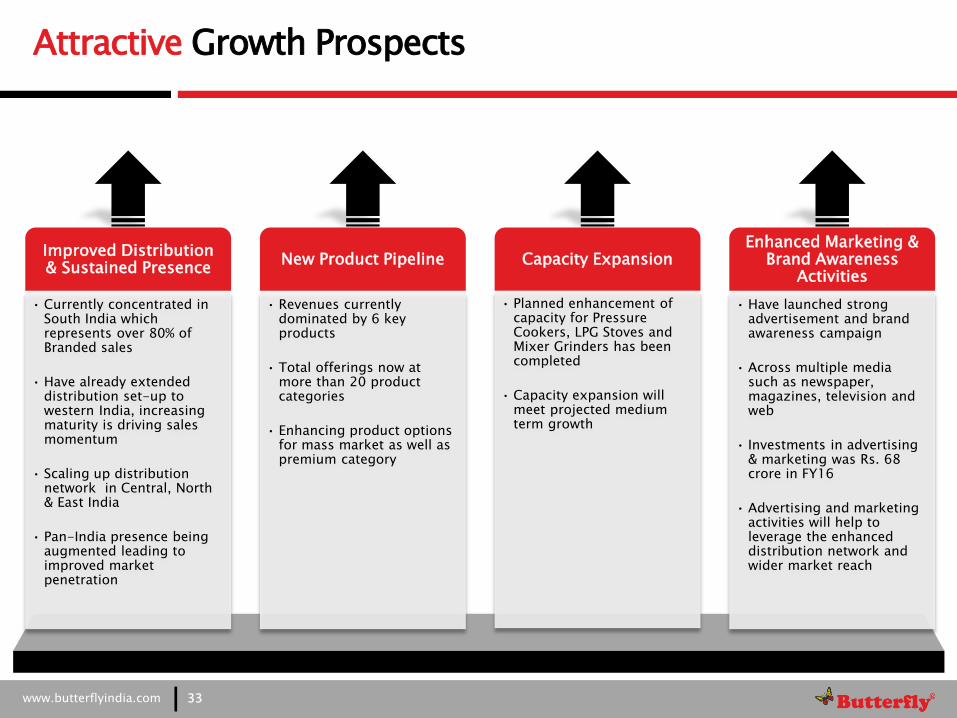

Attractive Growth Prospects

Improved Distribution & Sustained Presence

• Currently concentrated in South India which represents over 80% of Branded sales

• Have already extended distribution set-up to western India, increasing maturity is driving sales momentum

• Scaling up distribution network in Central, North & East India

• Pan-India presence being augmented leading to improved market penetration

New Product Pipeline

• Revenues currently dominated by 6 key products

• Total offerings now at more than 20 product categories

• Enhancing product options for mass market as well as premium category

Capacity Expansion

• Planned enhancement of capacity for Pressure Cookers, LPG Stoves and Mixer Grinders has been completed

• Capacity expansion will meet projected medium term growth

Enhanced Marketing & Brand Awareness

Activities

• Have launched strong advertisement and brand awareness campaign

• Across multiple media such as newspaper, magazines, television and web

• Investments in advertising & marketing was Rs. 68 crore in FY16

• Advertising and marketing activities will help to leverage the enhanced distribution network and wider market reach

33

www.butterflyindia.com

Outlook

34

Retail Channel Sales • The market scenario remained subdued for

most part of the year, especially in Southern markets

• Institutional sales is dependent on release of new LPG gas connections

• Issuance of new LPG gas connections has improved resulting in good growth

Government Order Sales

• As of Q4 FY16, both TNCSC and Pondicherry Co-Op. Wholesale Stores orders has been successfully completed

Institutional Channel Sales

70-75% of Branded Sales in FY16

Retail channel demand will continue to be subdued in the first half of the year and recovery is expected from the second half of FY17

Consumer demand is expected to improve in the coming quarters

Rs. 461 crore No new orders are expected in the near future

25-30% of Branded Sales in FY16

CATEGORY MARKET ENVIRONMENT FY16

CONTRIBUTION OUTLOOK

TOTAL BRANDED SALES

Rs. 488 crore

GROSS REVENUES

Rs. 995 crore

• Component/Spare sales are done only when we have Govt. orders

Component/Spare Sales

No new sales are expected in coming year

Rs. 46 crore

Thank you