business perspectives on emerging markets 2012 … to the findings in gia’s business perspectives...

TRANSCRIPT

www.globalintelligence.com All Rights Reserved ©2012

Business Perspectives on Emerging Markets 2012-2017

Global survey (South Africa results) June 2012 June 2012

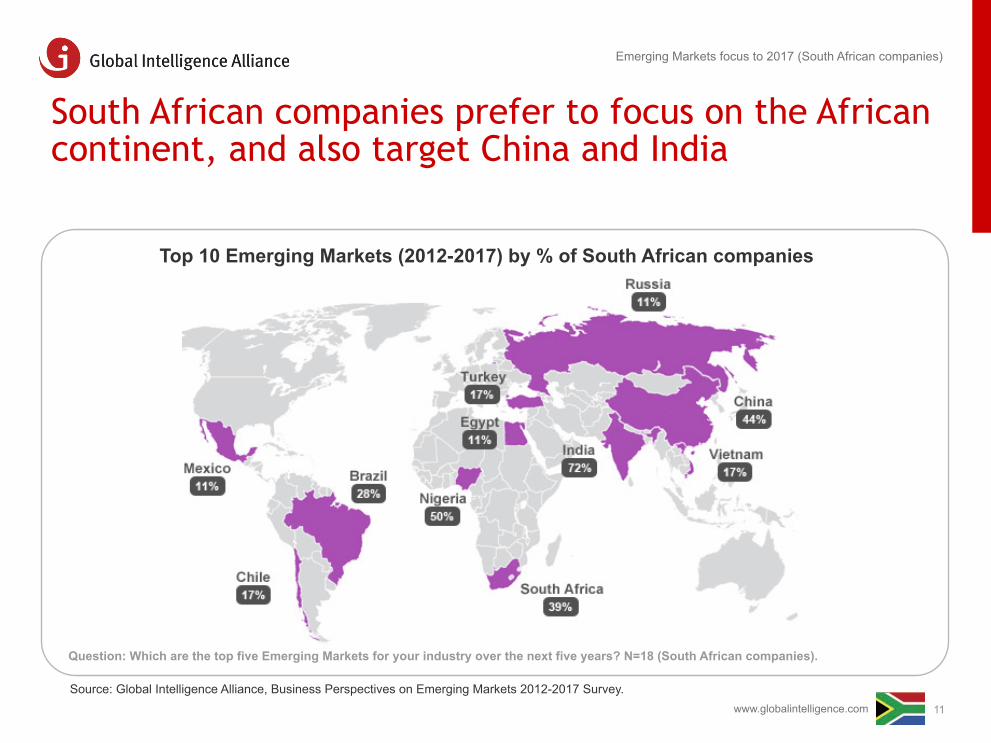

According to the findings in GIA’s Business Perspectives on Emerging Markets 2012-2017 Report, South African companies prefer to focus on the African continent when investing in Emerging Markets - 39% picked South Africa while over 50% listed Nigeria as their target markets. Twenty-two percent of the global companies surveyed said that South Africa is also one of their top target markets to 2017, promising more competition from foreign players on South African turf.

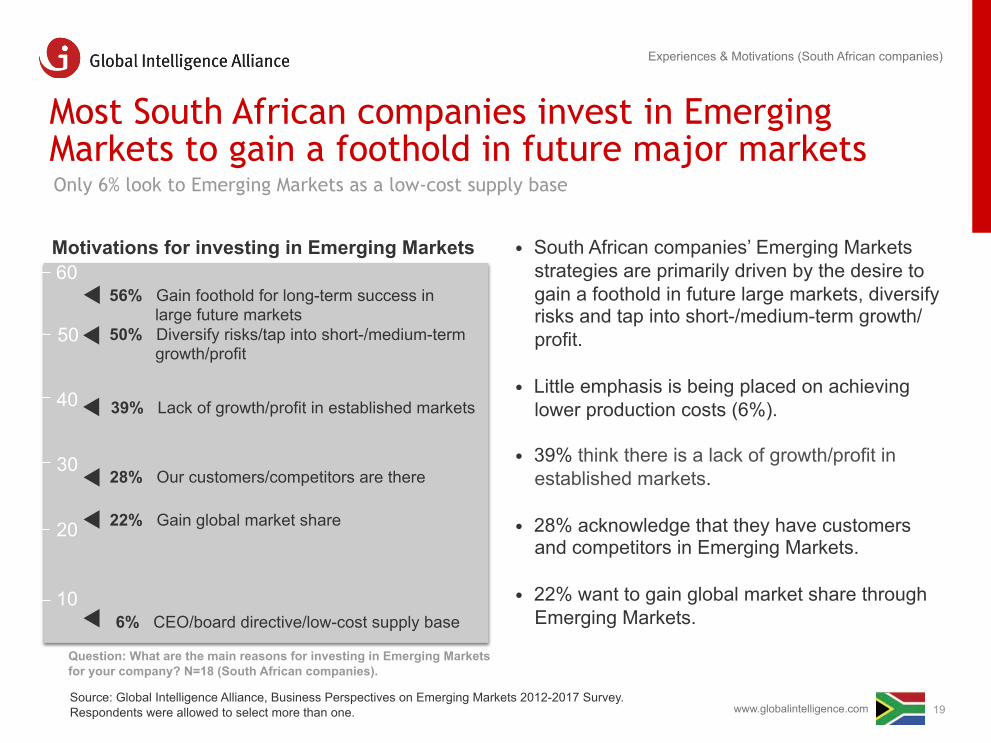

South African companies’ Emerging Markets strategies are primarily driven by the desire to gain a foothold in future large markets, diversify risks, and tap into short to medium-term growth/profit. Thirty-nine percent believe there is a lack of growth/profit in established markets while 28% acknowledge that they have customers and competitors in Emerging Markets.

With this study, we share the strategic ambitions, concerns and challenges facing South African companies in other fast-moving markets. I wish you an insightful read, and welcome any thoughts you might want to share with me and my colleagues around the world. Our mission is to help companies understand, compete and grow in international markets.

For the global findings or other country reports, please visit http://bit.ly/GIA2012 www.globalintelligence.com | [email protected]

Business Perspectives on Emerging Markets 2012-2017 Why this study is important

Stuart Maclachlan Managing Director, GIA Member South Africa Global Intelligence Alliance

www.globalintelligence.com 2

Summary: South African companies prefer to invest in Emerging Markets in Africa They lag behind global peers in using market intelligence, resulting in delays in decision making

3

Emerging Markets focus and expectations

• Nigeria, India and China are the three most important Emerging Markets for South African companies to 2017, with South Africa coming in fourth.

• South African companies’ Emerging Markets strategies are primarily driven by the desire to gain a foothold in future large markets and increase market share. Access to customers is the biggest single Emerging Markets success factor across industries.

• Most of the secondary Emerging Markets that South African companies plan to target in 2012-2017 are in developing economies. South African companies will choose more Asian countries as their Emerging Markets in the next five years.

• India and China are amongst most important Emerging Markets for South African companies to 2017.

Motivations and concerns

• All the South African companies surveyed said they should have entered Emerging Markets more quickly, and almost 40% said they would have made greater efforts to conduct intelligence/due diligence better.

• The Technology sector expects the most growth in Emerging Markets, followed by the Logistics and Chemicals sectors.

• The top industries for Emerging Markets include Chemicals (27% of respondents list South Africa as a destination of choice), followed by Financial Services (18%) and Automotive (19%).

• South African companies appreciate the value of market intelligence. 94% said that accurate market sizing and growth estimates are critical to their Emerging Markets strategies. However, only 39% use market intelligence to support their decisions regarding Emerging Markets, versus a global average of 55%.

www.globalintelligence.com

www.globalintelligence.com

How can South African companies succeed in Emerging Markets in 2012-2017?

• In April-May 2012, GIA conducted an online survey of business managers at 431 large and mid-sized companies around the world, 18 of which were headquartered in South Africa.

• We asked them questions such as: • How do you define Emerging Markets in your company? • Which are the top Emerging Markets for your industry over the next five years? • What key factors will determine whether foreign companies succeed in Emerging Markets? • What are the biggest barriers to succeeding in Emerging Markets? • What are your company’s main reasons for investing in Emerging Markets? • What share of your company’s global revenue do you expect to come from Emerging Markets? • Which single aspect of your Emerging Markets strategy would you revisit and change if you could?

• The South African respondents’ primary job functions included senior management/market or competitive intelligence (33%); research and development/product management (11%); strategic planning/business development/sales and marketing (6%) and others.

• Forty-four percent of the South African companies in the survey earned more than R10.6 billion ($1.3 billion) in annual revenue, and over 50% have more than 1 000 employees each.

• See Appendix for more details about the survey sample.

18 South African companies revealed what drives their strategy How do companies target different Emerging Markets and have they been successful so far?

5 www.globalintelligence.com

• Manufacturing & Industrial

• Telecommunication, Technology & Media

• Professional & Business Services

• Financial Services

• Consumer & Retail

• Pharmaceuticals & Healthcare

• Energy, Resources & Environment

• Automotive

• Chemicals

• Logistics & Transportation

Ten industries are represented in this report The industries are represented by the following symbols

6 www.globalintelligence.com

• GIA took the opportunity to donate R52 for every completed survey.

• The total donation came close to R2,298 and was distributed across the following local charities:

This study also aided those living in Emerging Markets Donations from this study went to four charities that assist poor communities in Emerging Markets

7 www.globalintelligence.com

• Cambodia: Tabitha (NGO that runs self-help programmes on personal and financial development for the poorest people).

• Brazil: VidaBela (NGO that awards university scholarships to talented candidates from highly-disadvantaged socio-economic backgrounds).

• Russia: Gift of Life/Podari Zhizn (charity that funds vital medicine for leukemia treatment and searches for potential bone marrow donors for children).

• South Africa: CANSA (NGO that provides holistic cancer care and support to those affected by the disease).

www.globalintelligence.com

Emerging Markets focus for South African companies to 2017

www.globalintelligence.com 9

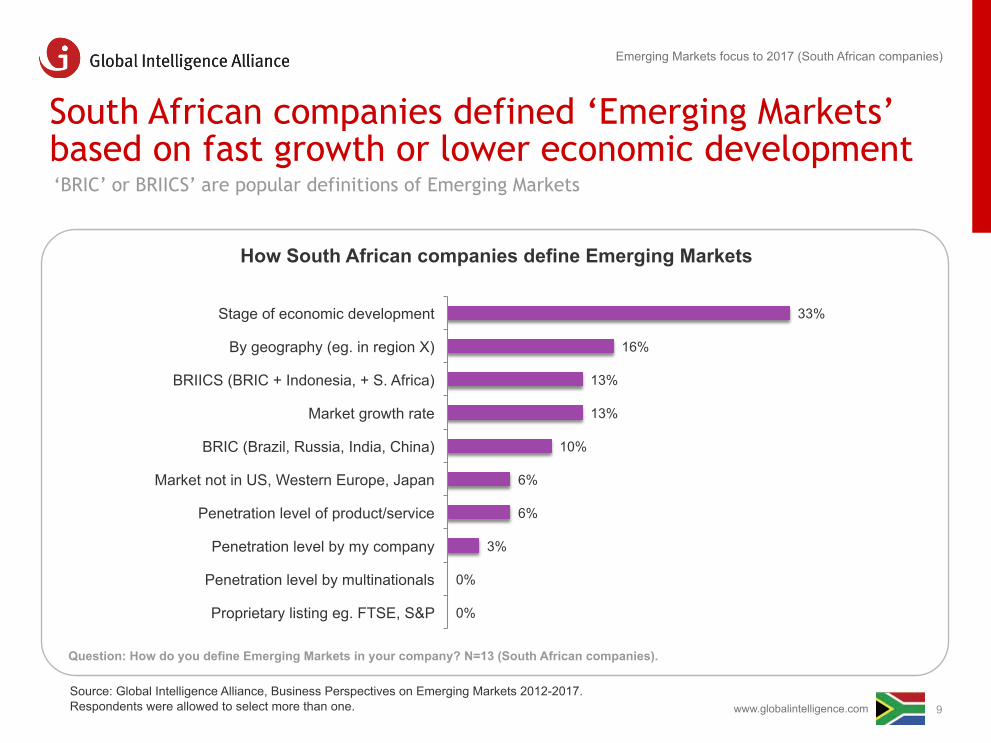

South African companies defined ‘Emerging Markets’ based on fast growth or lower economic development ‘BRIC’ or BRIICS’ are popular definitions of Emerging Markets

How South African companies define Emerging Markets

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017. Respondents were allowed to select more than one.

Question: How do you define Emerging Markets in your company? N=13 (South African companies).

33%

16%

13%

13%

10%

6%

6%

3%

0%

0%

Stage of economic development

By geography (eg. in region X)

BRIICS (BRIC + Indonesia, + S. Africa)

Market growth rate

BRIC (Brazil, Russia, India, China)

Market not in US, Western Europe, Japan

Penetration level of product/service

Penetration level by my company

Penetration level by multinationals

Proprietary listing eg. FTSE, S&P

Emerging Markets focus to 2017 (South African companies)

www.globalintelligence.com

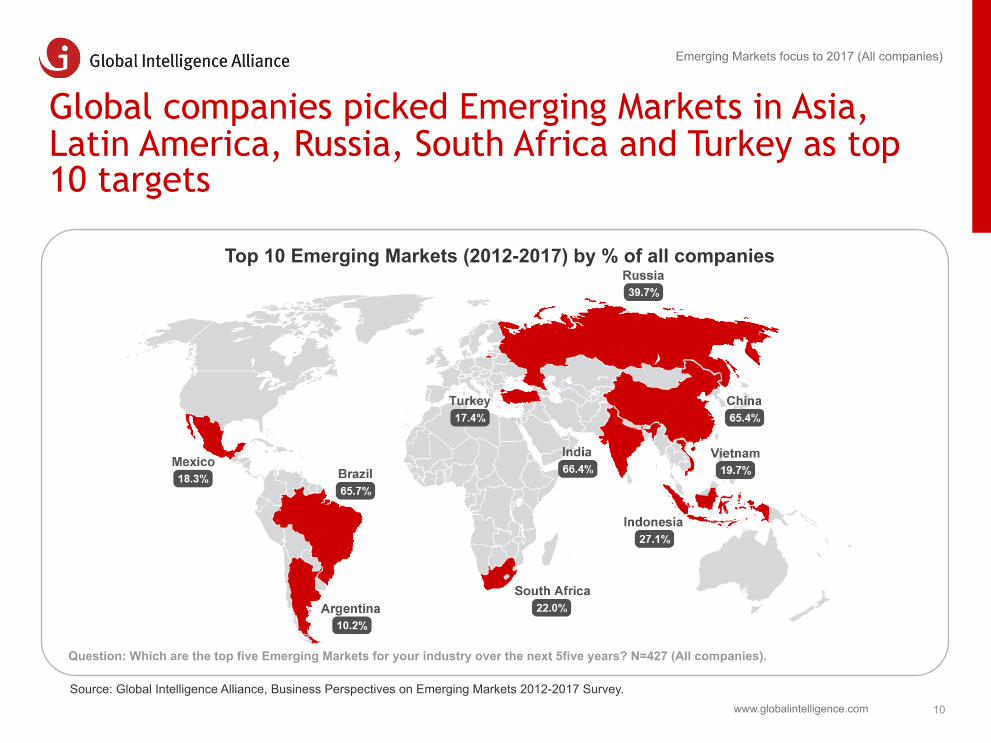

Global companies picked Emerging Markets in Asia, Latin America, Russia, South Africa and Turkey as top 10 targets

10

Top 10 Emerging Markets (2012-2017) by % of all companies

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey.

Question: Which are the top five Emerging Markets for your industry over the next 5five years? N=427 (All companies).

Emerging Markets focus to 2017 (All companies)

www.globalintelligence.com

South African companies prefer to focus on the African continent, and also target China and India

11

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey.

Question: Which are the top five Emerging Markets for your industry over the next five years? N=18 (South African companies).

Top 10 Emerging Markets (2012-2017) by % of South African companies

Emerging Markets focus to 2017 (South African companies)

www.globalintelligence.com

Not all BRIC countries are favored as top Emerging Markets by South African respondents

12

South African companies would like to place more emphasis on African markets than global peers

Top-four Emerging Markets (2012-2017)

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017. Respondents were allowed to select more than one. * Figures based on 2012, 2013 and 2017 average from IMF World Economy Outlook: Growth Resuming, Dangers Remain

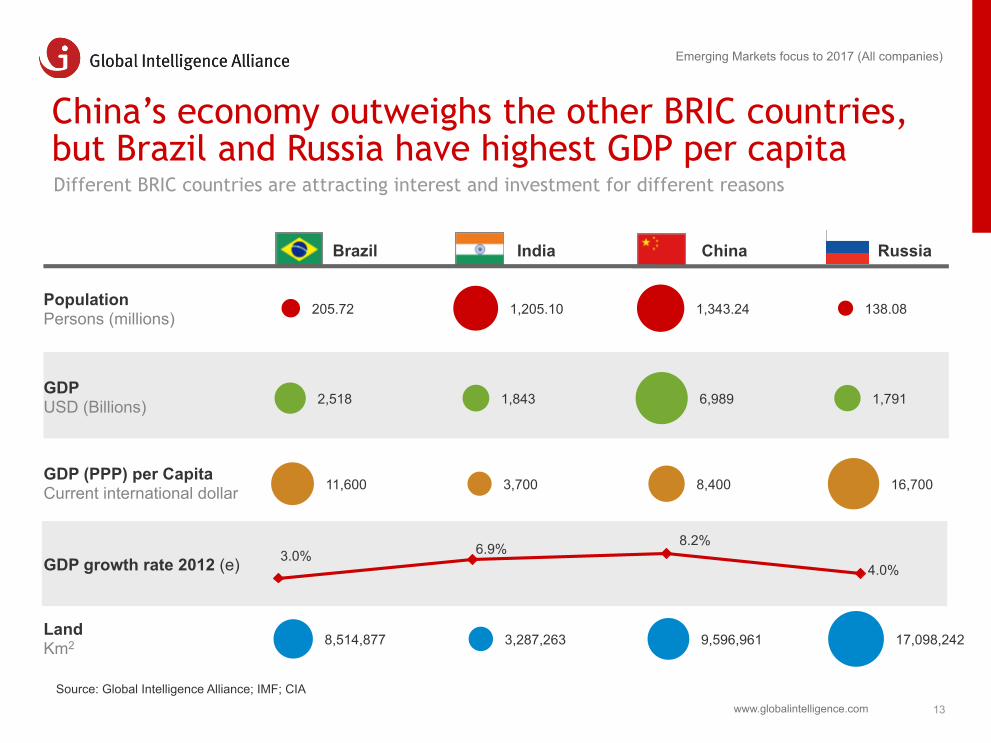

• Unlike global companies which choose BRIC as their top four markets, South African companies pick only India and China to be amongst their four most important Emerging Markets to 2017.

• Instead, Nigeria and South Africa are part of the top four Emerging Markets for South African companies.

• According to the IMF, average growth rates for 2012-2017* are 7.4% for India, 6.6% for Nigeria, 8.5% for China and 3.3% for South Africa. South Africa seems to be finding favour for reasons other than its growth rates.

Question: Which are the top five Emerging Markets for your industry over the next five years? N=18 (S. African companies).

72.2%

50.0%

44.4%

38.9%

India

Nigeria

China

South Africa

All respondents South African respondents

India 67.0%

Nigeria 7.7%

China 66.0%

S. Africa 22.0%

Emerging Markets focus to 2017 (South African companies)

www.globalintelligence.com

205.72 1,205.10 1,343.24 138.08

China’s economy outweighs the other BRIC countries, but Brazil and Russia have highest GDP per capita

13

Different BRIC countries are attracting interest and investment for different reasons

Source: Global Intelligence Alliance; IMF; CIA

Population Persons (millions)

GDP USD (Billions)

GDP (PPP) per Capita Current international dollar

GDP growth rate 2012 (e)

Land Km2

Brazil India China Russia

11,600 3,700 8,400 16,700

2,518 1,843 6,989 1,791

3.0% 6.9% 8.2%

4.0%

8,514,877 3,287,263 9,596,961 17,098,242

Emerging Markets focus to 2017 (All companies)

www.globalintelligence.com

303 286 1,312 375

It is easiest to do business in China, and Brazil is becoming more competitive in the global context

14

Levels of development and opportunities vary across the different BRIC countries

Source: Global Intelligence Alliance; MIIT China, TRAI India, Anatel Brazil, Deloitte

Brazil India China Russia

Mobile subscribers Q1, 2012

Teledensity (wireless) Q1, 2012

1.01 billion 919 million 250 million

No. of millionaire households 2011, thousands

Ease of doing business index (World Bank) 2011, ranking

91 132 126

Global Competitiveness Index (WEO) 2010/11 to 2011/12, ranking

120

227 million

74% 76% 126% 160%

26 53

58

51

27 66

63

Emerging Markets focus to 2017 (All companies)

56

www.globalintelligence.com

26%

28%

21%

33%

29%

25%

24%

32%

17%

19%

15%

13%

28%

28%

40%

22%

US headquarters

European headquarters

Latin American headquarters

Asian headquarters

Brazil Russia India China

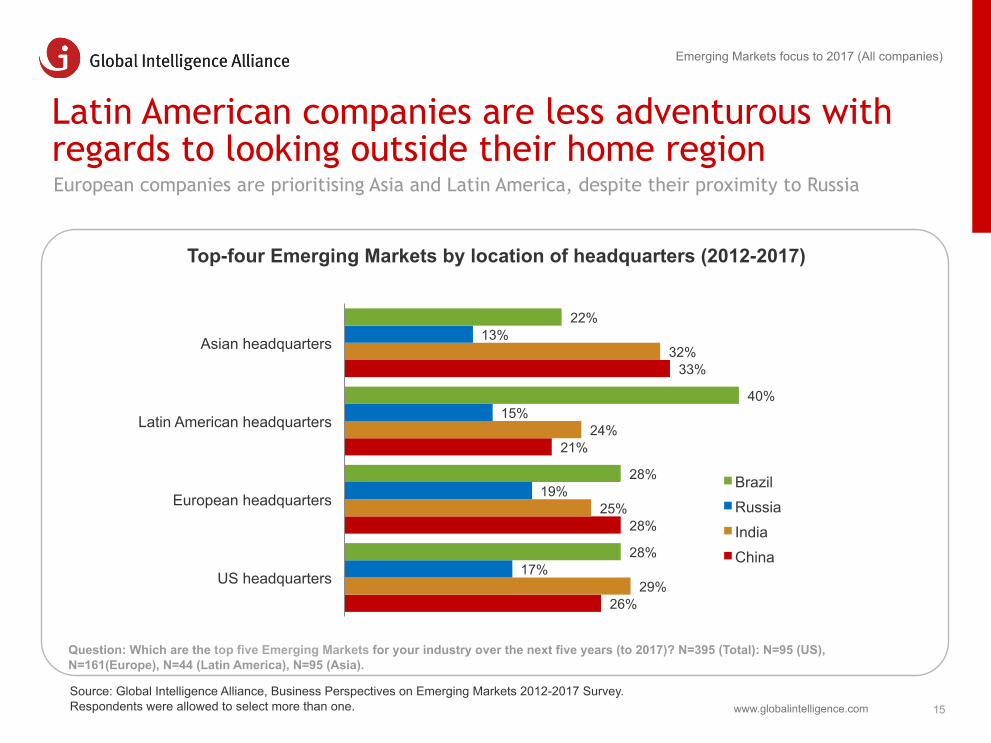

Latin American companies are less adventurous with regards to looking outside their home region

15

European companies are prioritising Asia and Latin America, despite their proximity to Russia

Top-four Emerging Markets by location of headquarters (2012-2017)

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey. Respondents were allowed to select more than one.

Question: Which are the top five Emerging Markets for your industry over the next five years (to 2017)? N=395 (Total): N=95 (US), N=161(Europe), N=44 (Latin America), N=95 (Asia).

Emerging Markets focus to 2017 (All companies)

www.globalintelligence.com

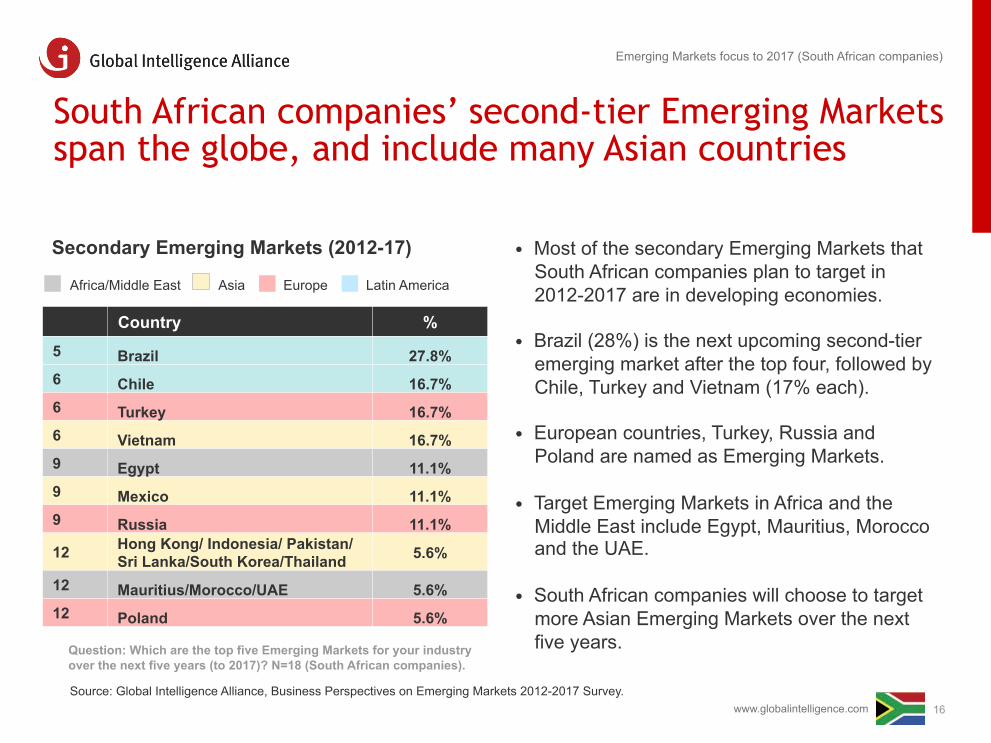

South African companies’ second-tier Emerging Markets span the globe, and include many Asian countries

16

Secondary Emerging Markets (2012-17)

Emerging Markets focus to 2017 (South African companies)

Africa/Middle East Asia Europe Latin America

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey.

• Most of the secondary Emerging Markets that South African companies plan to target in 2012-2017 are in developing economies.

• Brazil (28%) is the next upcoming second-tier emerging market after the top four, followed by Chile, Turkey and Vietnam (17% each).

• European countries, Turkey, Russia and Poland are named as Emerging Markets.

• Target Emerging Markets in Africa and the Middle East include Egypt, Mauritius, Morocco and the UAE.

• South African companies will choose to target more Asian Emerging Markets over the next five years. Question: Which are the top five Emerging Markets for your industry

over the next five years (to 2017)? N=18 (South African companies).

Country % 5 Brazil 27.8% 6 Chile 16.7% 6 Turkey 16.7% 6 Vietnam 16.7% 9 Egypt 11.1% 9 Mexico 11.1% 9 Russia 11.1%

12 Hong Kong/ Indonesia/ Pakistan/ Sri Lanka/South Korea/Thailand 5.6%

12 Mauritius/Morocco/UAE 5.6% 12 Poland 5.6%

www.globalintelligence.com

15% 18% 4%

26%

15% 17%

11%

11% 10%

11%

3%

22% 15% 10%

29%

6% 14% 17%

7%

6% 10% 4%

20%

2%

5% 7% 1%

10%

6% 3% 20% 3%

6% 6%

4%

6%

4% 7%

1%

8%

US HQ European HQ Latin American HQ Asian HQ

Malaysia

South Korea

Chile

Thailand

Argentina

Turkey

Mexico

Vietnam

South Africa

Indonesia

After Indonesia and South Africa, US and European companies are most interested in Turkey and Mexico

17

Latin American companies focus more on their own home region; while Asian companies favour Vietnam

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey.

Question: Which are the top five Emerging Markets for your industry over the next five years (to 2017)? N=395 (Total): N=95 (US), N=161 (Europe), N=44 (Latin America), N=95 (Asia).

Top-10 secondary Emerging Markets by location of headquarters (2012-2017)

Emerging Markets focus to 2017 (All companies)

www.globalintelligence.com

Emerging Markets investment experiences and motivations

(South African companies)

www.globalintelligence.com

50

60

30

40

10

56% Gain foothold for long-term success in large future markets

39% Lack of growth/profit in established markets

28% Our customers/competitors are there

22% Gain global market share

6% CEO/board directive/low-cost supply base

Most South African companies invest in Emerging Markets to gain a foothold in future major markets

19

Only 6% look to Emerging Markets as a low-cost supply base

Motivations for investing in Emerging Markets

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey. Respondents were allowed to select more than one.

• South African companies’ Emerging Markets strategies are primarily driven by the desire to gain a foothold in future large markets, diversify risks and tap into short-/medium-term growth/profit.

• Little emphasis is being placed on achieving lower production costs (6%).

• 39% think there is a lack of growth/profit in established markets.

• 28% acknowledge that they have customers and competitors in Emerging Markets.

• 22% want to gain global market share through Emerging Markets.

Question: What are the main reasons for investing in Emerging Markets for your company? N=18 (South African companies).

20

50% Diversify risks/tap into short-/medium-term growth/profit

Experiences & Motivations (South African companies)

www.globalintelligence.com

66%

42%

9%

17%

25%

27%

17%

33%

46% 18%

2012

2014

2017

0%-10% 11%-20% 21%-30% 31%-50% 51%-60% 61%-80% 81%-100%

Proportion of global revenues from Emerging Markets will continue to grow to 2017

20

All the South African companies surveyed would have entered Emerging Markets by 2014

% global revenue from Emerging Markets (2012-2017)

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017.

Question: What % of your company's global revenue do you expect to come from Emerging Markets? N=13 (2012), N=13 (2014), N=13 (2017).

Zero global revenue from Emerging Markets

(2012-2017)

7.69%

0.00%

0.00%

Experiences & Motivations (South African companies)

www.globalintelligence.com

South African companies would have done some things differently with their Emerging Markets strategies

21

Almost 40% struggle to have conducted intelligence/due diligence better

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey,

• None of South African companies are satisfied with their Emerging Markets strategy, compared to the global average satisfaction rate of 9%.

• All of the South African companies surveyed would have done things differently with regards to their Emerging Markets strategy.

• South African companies primarily have two main regrets: almost 40% would have made greater efforts to conduct intelligence/due diligence better, and more than 30% said they would have entered Emerging Markets earlier.

Emerging Markets strategy as of 2012

100% would have done things differently

Question: Which one aspect of your Emerging Markets strategy would you change if you could go back in time, and how? N=16 (South African companies)

Experiences & Motivations (South African companies)

www.globalintelligence.com

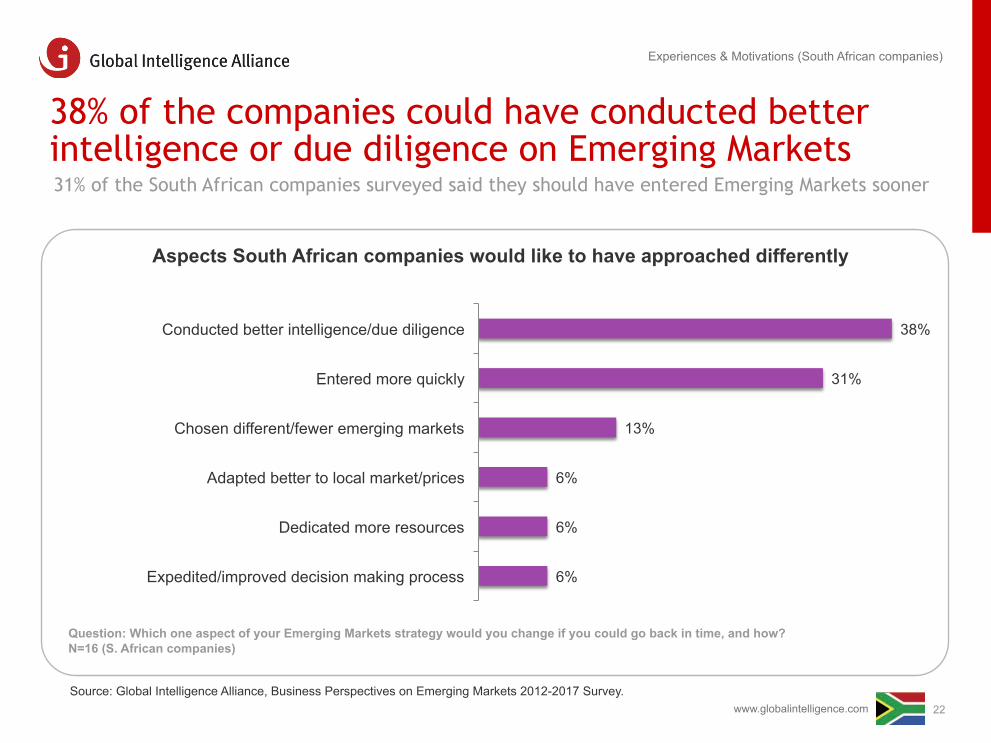

38% of the companies could have conducted better intelligence or due diligence on Emerging Markets

22

Experiences & Motivations (South African companies)

Aspects South African companies would like to have approached differently

31% of the South African companies surveyed said they should have entered Emerging Markets sooner

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey.

Question: Which one aspect of your Emerging Markets strategy would you change if you could go back in time, and how? N=16 (S. African companies)

38%

31%

13%

6%

6%

6%

Conducted better intelligence/due diligence

Entered more quickly

Chosen different/fewer emerging markets

Adapted better to local market/prices

Dedicated more resources

Expedited/improved decision making process

www.globalintelligence.com

Emerging Markets investment experiences and motivations

(Global companies)

Technology sector expects the most growth in Emerging Markets, followed by Logistics and Chemical

24

The Resources sector will source the most revenue from Emerging markets; Consumer, Finance and Healthcare the least

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017

Experiences & Motivations (All companies)

17%

19%

19%

35%

15%

15%

13%

18%

20%

24%

24%

29%

25%

45%

18%

21%

19%

27%

32%

30%

36%

38%

37%

53%

26%

28%

27%

37%

48%

41%

2017 2014 2012

Question: What share of your company's global revenue do you expect to come from Emerging Markets? N=277 (2012), N=268 (2014), N=263 (2017).

% Average Global Revenue from Emerging Markets by Industry (2012-2017)

US companies are slightly behind the curve on tapping into Emerging Markets revenues

25

Smaller companies are expecting a greater share of revenue from Emerging Markets than larger ones

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017

Experiences & Motivations (All companies)

Question: What share of your company's global revenue do you expect to come from Emerging Markets? N=256 (Total of 2017): N=86(<0.1 bil Euro), N=62 (0.1 bil-<1 bil Euro), N=108 (=/>1 bil Euro). .

% Average Expected Global Revenue from Emerging Markets (2017)

33%

38%

42%

=/> 1bil Euro

0.1 bil - < 1bil Euro

<0.1 bil Euro

By size of annual revenue

34%

36%

37%

38%

US HQ

Latin American HQ

European HQ

Asian HQ

By location of headquarters

Question: What share of your company's global revenue do you expect to come from Emerging Markets? N=245 (Total of 2017): N=63 (US), N=94 (Europe), N=27 (Latin America), N=61 (Asia).

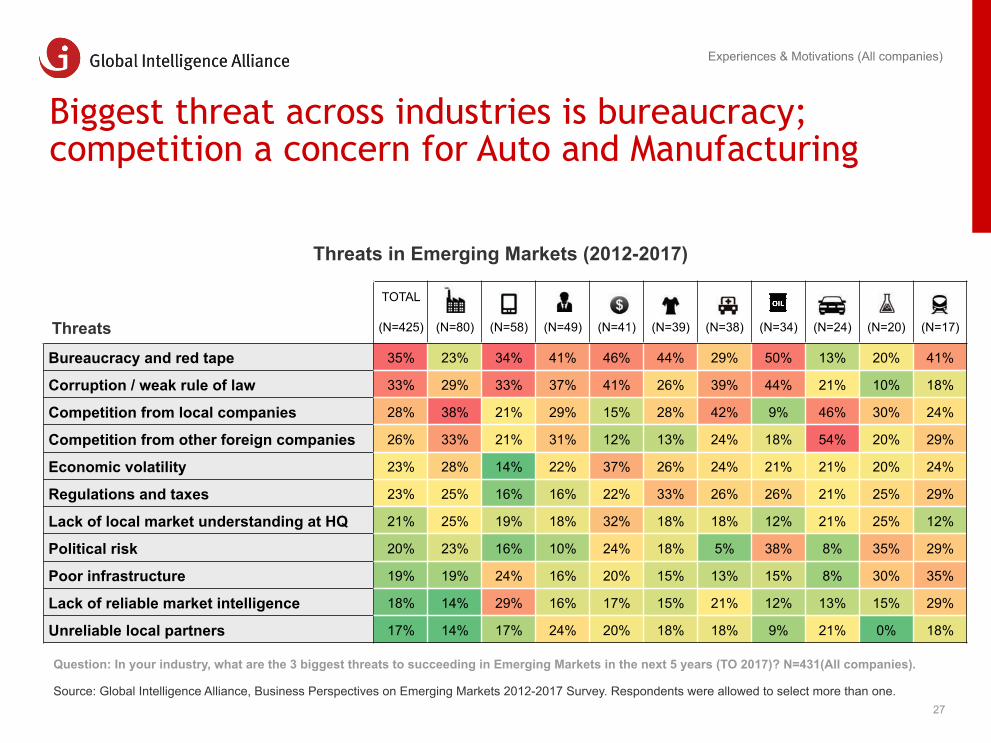

TOTAL

(N=425) (N=80) (N=58) (N=49) (N=41) (N=39) (N=38) (N=34) (N=24) (N=20) (N=17)

Distribution / access to customers 35% 41% 36% 22% 37% 49% 37% 15% 21% 50% 29%

Adapting to local culture 28% 25% 34% 37% 24% 26% 11% 29% 17% 25% 24%

Building a strong brand 24% 18% 26% 33% 24% 44% 26% 9% 25% 20% 12%

Local partner(s) 24% 20% 19% 37% 32% 15% 29% 21% 21% 15% 12%

Government relations 23% 13% 21% 33% 32% 13% 24% 32% 21% 5% 24%

Pricing 23% 24% 22% 16% 12% 31% 34% 15% 38% 30% 24%

Localized competitive positioning 22% 21% 28% 20% 2% 10% 32% 18% 38% 35% 35%

Product/service quality 21% 21% 21% 20% 27% 21% 24% 12% 4% 35% 29%

Flexibility as the market develops 20% 19% 22% 18% 17% 15% 8% 21% 25% 10% 18%

Localization of products/services 18% 26% 26% 8% 7% 18% 13% 6% 38% 20% 18%

Finding the right talent 18% 16% 16% 18% 12% 13% 18% 24% 21% 15% 12%

Local business relationships/lobbying 17% 16% 12% 22% 17% 13% 11% 21% 13% 20% 18%

Access to customers is the biggest single Emerging Markets success factor across industries

26

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey. Respondents were allowed to select more than one.

Question: In your industry, what 3 key factors will determine which foreign companies succeed in Emerging Markets to 2017? N=425(All companies).

Experiences & Motivations (All companies)

Success Factors for Emerging Markets (2012-2017)

Success Factors

Brand is very important for the Consumer sector; localization least important for the Finance sector

TOTAL

(N=425) (N=80) (N=58) (N=49) (N=41) (N=39) (N=38) (N=34) (N=24) (N=20) (N=17)

Bureaucracy and red tape 35% 23% 34% 41% 46% 44% 29% 50% 13% 20% 41%

Corruption / weak rule of law 33% 29% 33% 37% 41% 26% 39% 44% 21% 10% 18%

Competition from local companies 28% 38% 21% 29% 15% 28% 42% 9% 46% 30% 24%

Competition from other foreign companies 26% 33% 21% 31% 12% 13% 24% 18% 54% 20% 29%

Economic volatility 23% 28% 14% 22% 37% 26% 24% 21% 21% 20% 24%

Regulations and taxes 23% 25% 16% 16% 22% 33% 26% 26% 21% 25% 29%

Lack of local market understanding at HQ 21% 25% 19% 18% 32% 18% 18% 12% 21% 25% 12%

Political risk 20% 23% 16% 10% 24% 18% 5% 38% 8% 35% 29%

Poor infrastructure 19% 19% 24% 16% 20% 15% 13% 15% 8% 30% 35%

Lack of reliable market intelligence 18% 14% 29% 16% 17% 15% 21% 12% 13% 15% 29%

Unreliable local partners 17% 14% 17% 24% 20% 18% 18% 9% 21% 0% 18%

27 Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey. Respondents were allowed to select more than one.

Experiences & Motivations (All companies)

Question: In your industry, what are the 3 biggest threats to succeeding in Emerging Markets in the next 5 years (TO 2017)? N=431(All companies).

Threats in Emerging Markets (2012-2017)

Biggest threat across industries is bureaucracy; competition a concern for Auto and Manufacturing

Threats

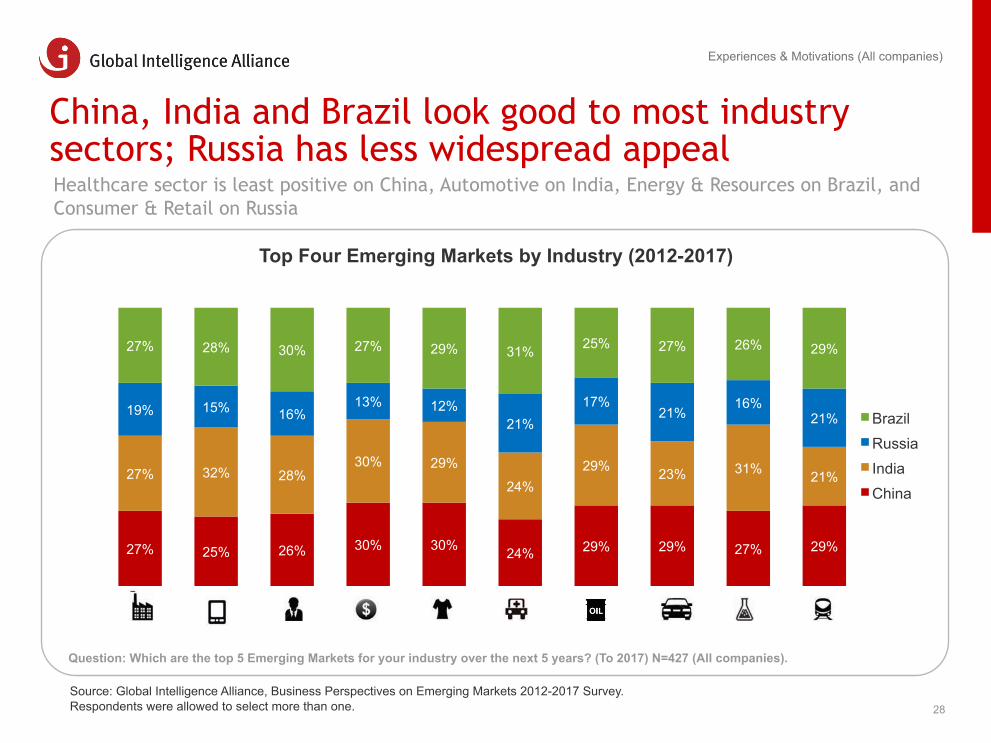

China, India and Brazil look good to most industry sectors; Russia has less widespread appeal

28

Healthcare sector is least positive on China, Automotive on India, Energy & Resources on Brazil, and Consumer & Retail on Russia

Top Four Emerging Markets by Industry (2012-2017)

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey. Respondents were allowed to select more than one.

Question: Which are the top 5 Emerging Markets for your industry over the next 5 years? (To 2017) N=427 (All companies).

27% 25% 26% 30% 30% 24% 29% 29% 27% 29%

27% 32% 28% 30% 29%

24% 29% 23% 31% 21%

19% 15% 16% 13% 12%

21% 17%

21% 16%

21%

27% 28% 30% 27% 29% 31% 25% 27% 26% 29%

Brazil Russia India China

Experiences & Motivations (All companies)

Vietnam stands out for Consumer, Logistics and Resources sectors, Mexico for Healthcare

29

Chemical sector very focused on Indonesia and South Africa, Consumer & Retail on SE Asia

Experiences & Motivations (All companies)

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey.

Question: Which are the top 5 Emerging Markets for your industry over the next 5 years (TO 2017)? N=427 (All companies).

Top 10 Secondary Emerging Markets by industry (2012-2017)

21% 18% 16% 20% 21% 12% 16% 16%

27% 21%

18% 15%

12%

20% 6%

14% 18% 19%

27%

8%

14% 15%

14%

7% 20%

3%

18% 6%

14%

21%

10% 15% 14%

10% 12%

20%

12%

13%

4%

4%

14% 8%

10% 12% 11%

17%

6% 16%

8%

8%

5% 8%

8% 6% 3% 14% 6% 3%

5%

8%

4% 5% 9% 6%

3%

8% 8%

6%

5%

14%

6% 8% 2% 6%

8%

4% 6%

9%

5% 8%

3% 6% 9% 3% 12% 1% 6% 6%

4% 5% 2% 6% 10%

4% 7% 4% 6% 5% 4%

South Korea Malaysia Thailand Chile Argentina Turkey Mexico Vietnam South Africa Indonesia

www.globalintelligence.com

Emerging Markets intelligence

www.globalintelligence.com

Availability, accuracy and comprehensiveness of intelligence on Emerging Markets are issues for many

31

45% South African companies find decision making is delayed due to a lack of information.

Emerging Markets intelligence

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey, N=18 (S. African companies).

• South African companies appreciate the value of market intelligence, with 94% saying that accurate market sizing and growth estimates are critical to their Emerging Markets strategy. However, only 39% use market intelligence to support their decisions on Emerging Markets, compared with a global average of 55%.

• Meanwhile, South African companies appear to lack readily-available Emerging Markets information more than their global peers. 61% of the former said that information on Emerging Markets is not readily available in their organisations, compared to the global average of 53%.

• 45% of the South African companies respondents said the lack of intelligence regarding Emerging Markets delays their decision making, which is lower than the global average of 48%.

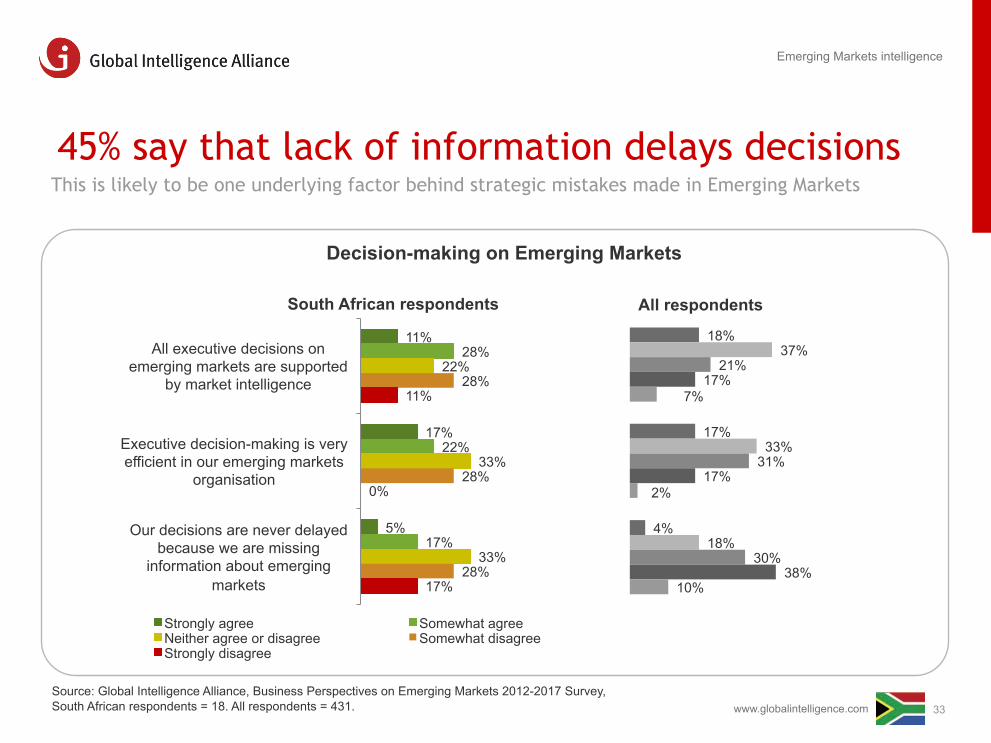

• One third of the South African companies surveyed were unable to say if decision-making on Emerging Markets in their organisations is efficient or not.

• Moreover, 83% doubt the accuracy and completeness of the information they have on Emerging Markets.

www.globalintelligence.com

42%

6%

3%

6%

44%

18%

10%

22%

9%

23%

12%

24%

4%

38%

40%

34%

1%

15%

35%

14%

61%

17%

6%

6%

33%

11%

11%

6%

0%

11%

0%

22%

6%

33%

33%

44%

0%

28%

50%

22%

Accurate market-sizing and growth estimates are critical for our emerging markets strategy

Information on emerging markets is always readily

available in our organization

Inaccurate or incomplete information about emerging markets is never a problem

Large volumes or overflow of information about emerging markets is never a problem

Strongly agree Somewhat agree Neither agree or disagree Somewhat disagree Strongly disagree

32

Information on Emerging Markets

South African respondents All respondents

Emerging Markets intelligence

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey, South African respondents = 18. All respondents = 431.

South African companies lack readily-available Emerging Markets information more than global peers 61% say such information is lacking, compared to a global average of 53%

www.globalintelligence.com

18%

17%

4%

37%

33%

18%

21%

31%

30%

17%

17%

38%

7%

2%

10%

11%

17%

5%

28%

22%

17%

22%

33%

33%

28%

28%

28%

11%

0%

17%

All executive decisions on emerging markets are supported

by market intelligence

Executive decision-making is very efficient in our emerging markets

organisation

Our decisions are never delayed because we are missing

information about emerging markets

Strongly agree Somewhat agree Neither agree or disagree Somewhat disagree Strongly disagree

33

Decision-making on Emerging Markets

All respondents

Emerging Markets intelligence

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey, South African respondents = 18. All respondents = 431.

45% say that lack of information delays decisions This is likely to be one underlying factor behind strategic mistakes made in Emerging Markets

South African respondents

www.globalintelligence.com

Appendix: Survey respondents

18 large and mid-sized South African companies participated in the survey 56% have at least 1,000 employees

35 Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey, N=18.

37%

19%

6%

19%

19%

< $0.13 bil/0.1 bil Euro

$0.13-<$1.3 bil/0.1-<1 bil Euro

$1.3-<$6.5 bil/1–<5 bil Euro

$6.5-<$13 bil/5-<10 bil Euro

=/> $13 bil/10 bil Euro

% of respondents by annual revenue

www.globalintelligence.com

36

South African companies in the survey represented financial services and a range of other industries

44%

11%

11%

10%

6%

6%

6%

6%

Financial Services

Manufacturing & Industrial

Telecommunication, Technology & Media

Other

Construction & Property Development

Energy, Resources & Environment

Private Equity

Professional & Business Services

% of respondents by industry

Source: Global Intelligence Alliance, Business Perspectives on Emerging Markets 2012-2017 Survey, N=18. www.globalintelligence.com

www.globalintelligence.com

About GIA

GIA is a strategic market intelligence and advisory group

Global Intelligence Alliance (GIA) is the preferred partner for organizations seeking to understand, compete and grow in international markets.

Our industry expertise and coverage of over 100 countries enables our customers to make better informed decisions worldwide.

GIA Group has 11 offices on 4 continents. Together with affiliated GIA Member companies, certified GIA Research Partners and consultants, GIA provides access to local knowledge in over 100 countries.

All GIA Network companies adhere to GIA’s Research and Analysis Quality System as well as the SCIP Code of Ethics.

www.globalintelligence.com | [email protected]

www.globalintelligence.com 38

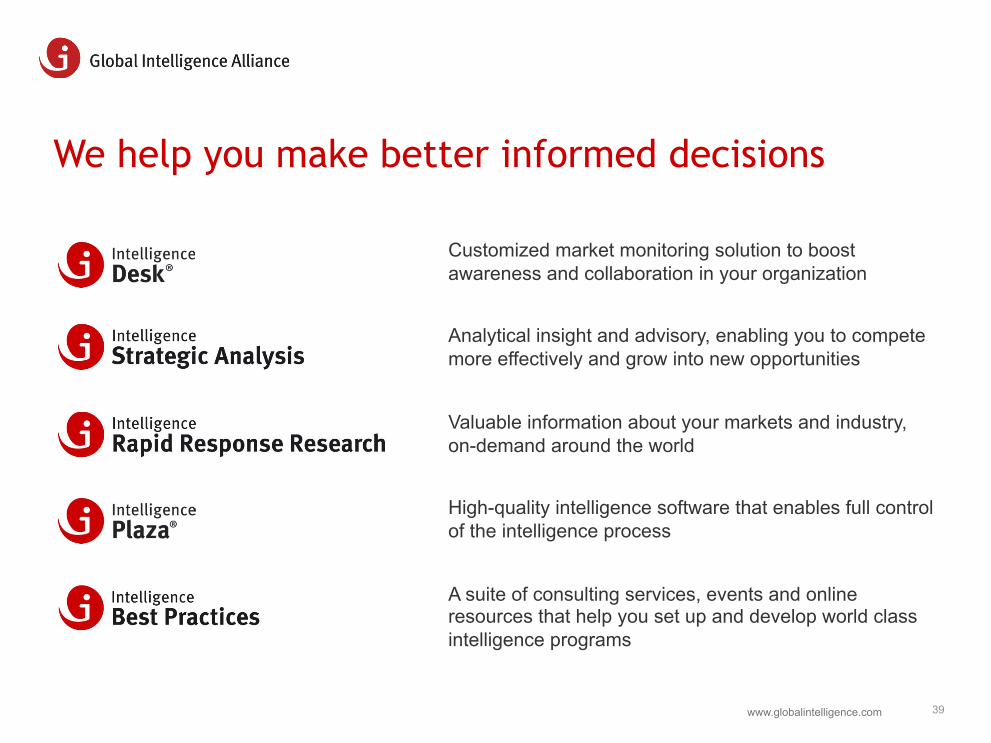

We help you make better informed decisions

Customized market monitoring solution to boost awareness and collaboration in your organization

Analytical insight and advisory, enabling you to compete more effectively and grow into new opportunities

Valuable information about your markets and industry, on-demand around the world

High-quality intelligence software that enables full control of the intelligence process

A suite of consulting services, events and online resources that help you set up and develop world class intelligence programs

39 www.globalintelligence.com

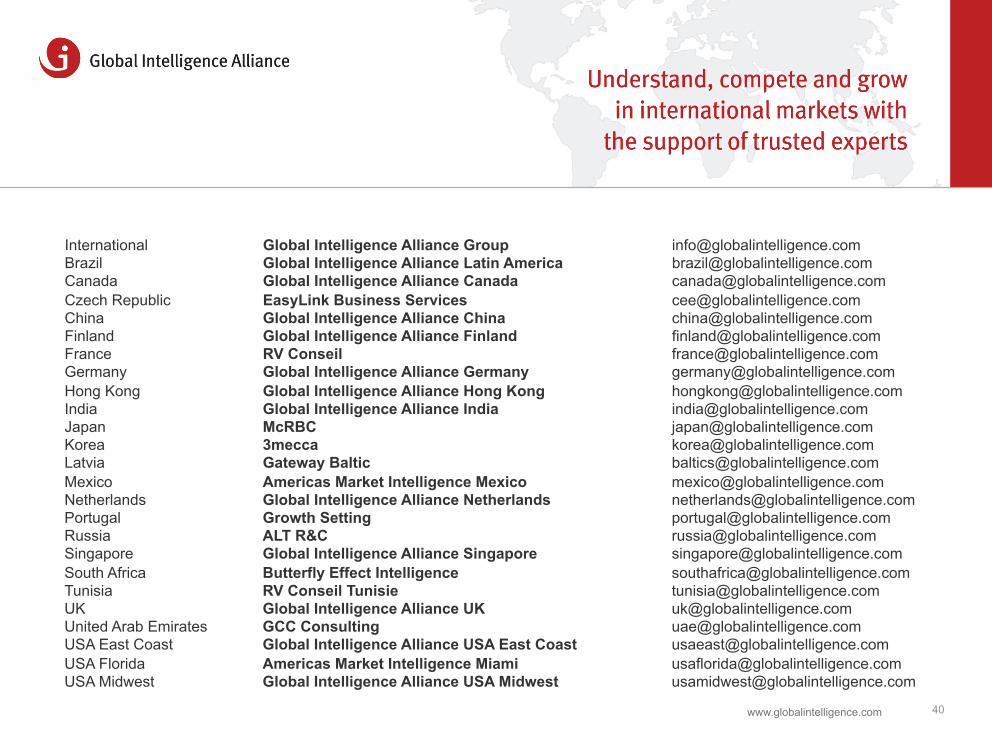

International Global Intelligence Alliance Group [email protected] Brazil Global Intelligence Alliance Latin America [email protected] Canada Global Intelligence Alliance Canada [email protected] Czech Republic EasyLink Business Services [email protected] China Global Intelligence Alliance China [email protected] Finland Global Intelligence Alliance Finland [email protected] France RV Conseil [email protected] Germany Global Intelligence Alliance Germany [email protected] Hong Kong Global Intelligence Alliance Hong Kong [email protected] India Global Intelligence Alliance India [email protected] Japan McRBC [email protected] Korea 3mecca [email protected] Latvia Gateway Baltic [email protected] Mexico Americas Market Intelligence Mexico [email protected] Netherlands Global Intelligence Alliance Netherlands [email protected] Portugal Growth Setting [email protected] Russia ALT R&C [email protected] Singapore Global Intelligence Alliance Singapore [email protected] South Africa Butterfly Effect Intelligence [email protected] Tunisia RV Conseil Tunisie [email protected] UK Global Intelligence Alliance UK [email protected] United Arab Emirates GCC Consulting [email protected] USA East Coast Global Intelligence Alliance USA East Coast [email protected] USA Florida Americas Market Intelligence Miami [email protected] USA Midwest Global Intelligence Alliance USA Midwest [email protected]

www.globalintelligence.com 40