business outlook global electronics industry

TRANSCRIPT

Business OutlookGlobal Electronics

Industry(with emphasis on Europe)

Custer Consulting Groupwww.custerconsulting.comJune 2018

2018 SituationAfter strong growth in 2017, expansion has now slowed.

Exchange rates distort global growth calculation. U.S. dollar denominated growth far exceeds Euro denominated growth.

Passive component shortages remain a big problem

Automotive, industrial and Internet of Things are growth drivers.

5G and other disruptive technologies are emerging.

Geopolitical unrest remains very significant.

Trade wars could do major damage.

Industrial Production – World% Change vs. One Year Earlier

Britain + 1.8 AprCzech Republic + 5.5 AprFrance + 2.1 AprGermany + 2.0 AprItaly + 1.9 AprNetherlands + 5.0 AprRussia + 1.0 AprSpain +11.0 AprEuro Area + 1.7 Apr

Canada + 4.9 MarUSA + 3.5 AprChina + 6.8 MayIndia + 4.9 AprMalaysia + 4.5 AprVietnam + 7.1 May Singapore + 9.1 AprS Korea + 0.9 AprTaiwan + 3.1 MarThailand + 4.0 AprJapan + 2.5 Apr

www.economist.com + Eurostat

20180620

Industrial Production – Europe Manufacturing Index (2015 Avg. Month = 100, Seasonally Adjusted)

70

80

90

100

110

120

130

140

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Jul-1

7

Jan-

18

Eur28 Germany France Italy UK

Eurostat

2018061b3

Index

LeadingIndicators

Global "Purchasing Managers" IndexDiffusion Index, >50 = Growth

Markit Economics

30

35

40

45

50

55

60

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

n

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

PMI

20180601

Expansion

Contraction

49.8

56.5

55.8

53.4

52.7

54.4

54.4

56.9

55.5

51.3

57.2

54.5

54.4

53.5

53.8

53.9

58.1

56.2

48.0 50.0 52.0 54.0 56.0 58.0 60.0 62.0

Russia

Czech

Sweden

Spain

Italy

France

UK

Germany

Europe

PMI

April

May

European Purchasing Managers' Indices May vs April 2018

Markit Economics

Above 50 = GrowthBelow 50 = Contraction

20180601

Eurozone Manufacturing "Purchasing Managers" Index

Diffusion Index, >50 = Growth

Markit Economics

30

35

40

45

50

55

60

65

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

1997199819992000200120022003200420052006200720082009201020112012201320142015201620172018

PMI

20180601

Germany Manufacturing "Purchasing Managers" Index

Diffusion Index, >50 = Growth

Markit Economics

30

35

40

45

50

55

60

65

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

PMI

20180601

Electronic Equipment

World

World Electronic Equipment ProductionBy Type20180612

0

500

1000

1500

2000

2500

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

industr+instrugov/milComputer & PeripheralsautomotiveconsumerTelecom/DatacomBusiness

1Q’18Weighted avg

For total El Eq +10.8%Annual Rate $B (converted @ fluctuating exchange rates)

Electronic Equipment SuppliersEuro vs. Dollar Growth

20180610

-20-15-10-505

1015202530

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

% G

row

th

US $ Euro

US$ & Euro converted @ fluctuating exchange rate

Exchange Rate Impact on US$ Denominated Consolidated World Electronic Equipment Sales

Quarterly Revenue Growth Converted to US$ @ Fixed 2017 vs Fluctuating Exchange

Global model based on regional shipment indices

20180525

-10

-5

0

5

10

15

20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2014 2015 2016 2017 2018

% G

row

th

Fixed Fluctuating

Impact of weakening US$Global growth 7.9% stronger when calculated at fluctuating exchange

Regional DataU.S.

Europe (Eurostat)

JapanChina/Taiwan

S Korea

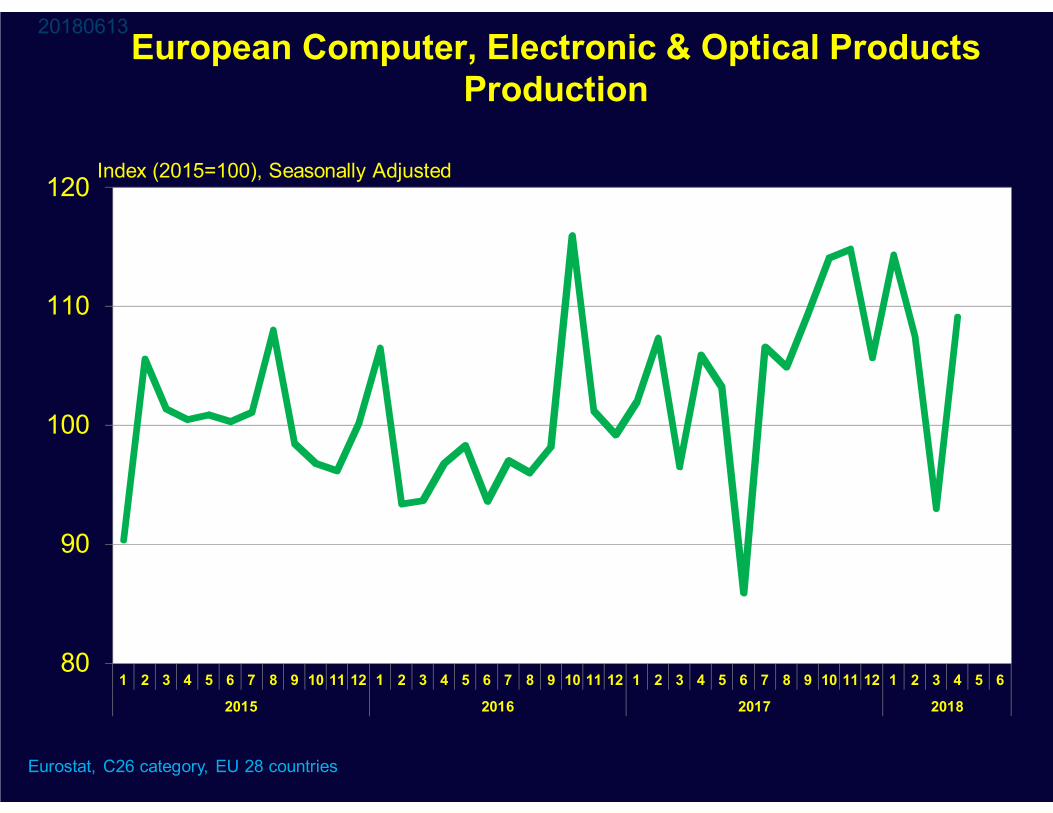

European Computer, Electronic & Optical Products Production

Eurostat, C26 category, EU 28 countries

20180619

40

50

60

70

80

90

100

110

120

1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

???

Index (2010=100), Seasonally Adjusted

Eurostat dataproblem

European Computer, Electronic & Optical Products Production

Eurostat, C26 category, EU 28 countries

20180613

80

90

100

110

120

1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6

2015 2016 2017 2018

Index (2015=100), Seasonally Adjusted

Taiwan/China Electronic Equipment ProducersComposite of 101 Manufacturers

Consolidated Revenue

Taiwan listed companies, often with significant manufacturing in China

0

200

400

600

800

1000

1200

1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

May 2018 up 13.7% compared to May 2017 and up 6.7% sequentially compared to April 2018

Total 2017 down 9.2% compared to total 2016

NT$ Billions

S Korea Electronic Equipment ProducersComposite of 7 Manufacturers20170619

40

50

60

70

80

90

100

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

+18.1%

KRW Trillions

Samsung Electronics, LG Electronics, Daewoo Electronic Components, Samsung SDI, Dongbu Hitek, SK Hynix, KEC Corp

U.S. Electronic Equipment Orders & ShipmentsComputer, Communications, Measurement & Control and Military

www.census.gov/indicator/www/m3/

20180604

1416182022242628303234

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

n

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Orders

Shipments

$ Billions (monthly, seasonally adjusted)

2016 World Electronic Equipment Production by Type@2016 Exchange Rates

Henderson Ventures 9/2017

2.1%

21.6 %

11.8%

9.4%23.5%

8.3%

10.3%

13.0%BusinessCommunicationConsumerAutoComputerMilitaryIndustrialInstrument

20171108

World Electronic Equipment Monthly Shipments

Converted @ Fluctuating Exchange Rates

Source: Custer Consulting Group

0

20

40

60

80

100

120

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

USAEuropeJapanChinaTaiwanKoreaROAROW

US$ B

20180612

World Electronic Equipment Monthly Shipments

Converted @ Fluctuating Exchange Rates

Source: Custer Consulting Group

20180525

80

100

120

140

160

180

200

220

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

April 2018 up 14.0% vs April 2017and down 6.4% sequentially vs. March 2018

US$ M

Electronic Equipment

Growth

Europe & World

Global Electronic Supply Chain Growth 1Q'18 vs. 1Q'17

1110

212

714

310

617

-128

2025

711

61616

8

-10 0 10 20 30Electronic Equipment

MilitaryBusiness & Office

Instruments & ControlsMedical

CommunicationInternet (Datacom)

ComputerData Storage

AutomotiveConsumer

SEMI Equip (SEMI)Semiconductors (SIA)Passive Components

PCBsLarge EMS (excl Foxconn)

ODMProcess Equipment

MaterialsRigid & Flex Laminate

Equip Tot=Weighted avgby product sector

% US$ Change

20180619

US$ equivalent at fluctuating exchange; based upon industry composites including acquisitions

European Electronic Supply Chain Growth 1Q’17 vs 1Q’18

28

-64

-13

45

32

46

-8 -6 -4 -2 0 2 4 6 8 10

Electronic EquipmentInstruments & Controls

Medical electronicsCommunication Equipment

Domestic Electric AppliancesMotor Vehicles

Airplane/AerospaceSemiconductors (SIA in euros)

Electronic componentsElectronic components & boards

Loaded electronic boardsWiring devices

% Change

20180515

Euro denominated growth rates; Eurostat, SIA & Custer Consulting Group

Markets of European Focus

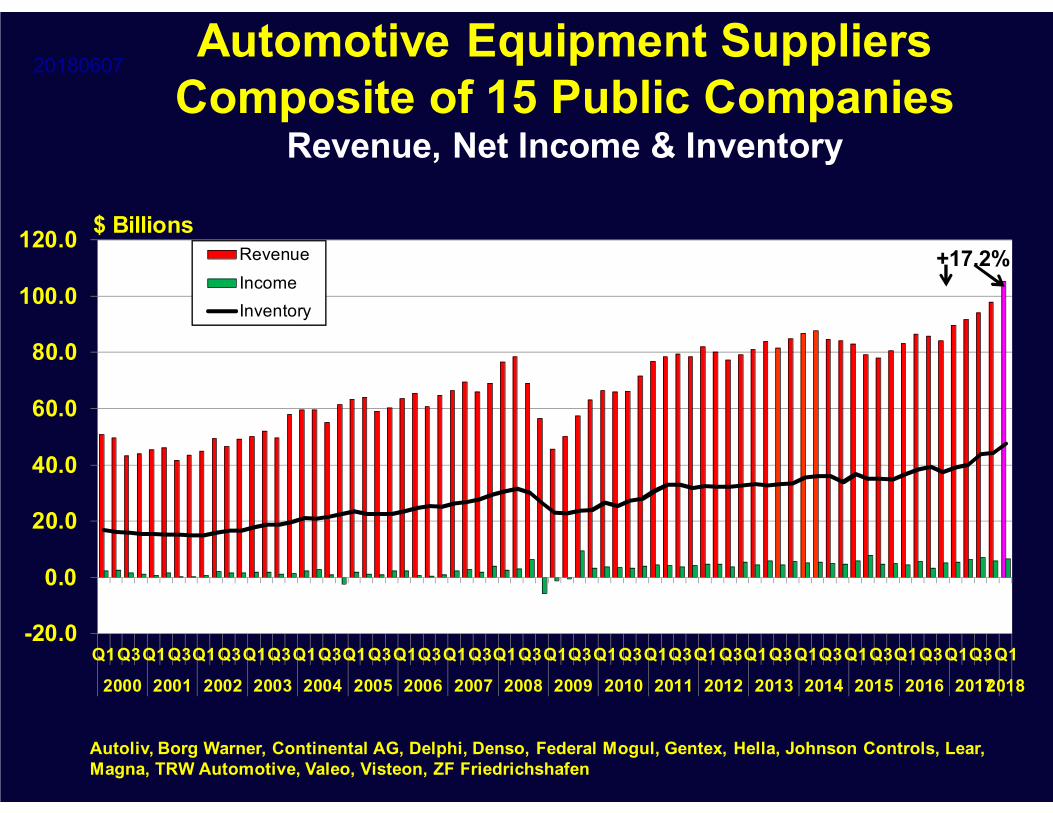

Automotive Equipment SuppliersComposite of 15 Public Companies

Revenue, Net Income & Inventory

Autoliv, Borg Warner, Continental AG, Delphi, Denso, Federal Mogul, Gentex, Hella, Johnson Controls, Lear, Magna, TRW Automotive, Valeo, Visteon, ZF Friedrichshafen

20180607

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ BillionsRevenueIncomeInventory

+17.2%

European Motor Vehicle Production

Eurostat, C291 category, EU 27 countries

20180613

40

50

60

70

80

90

100

110

120

1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

Index (2015=100), Seasonally Adjusted

Robert Bosch GmbhMobility Solutions Revenue

(formerly Automotive Technology sector)

CY

20180606

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Euros (Millions)

Revenue

www.bosch.com

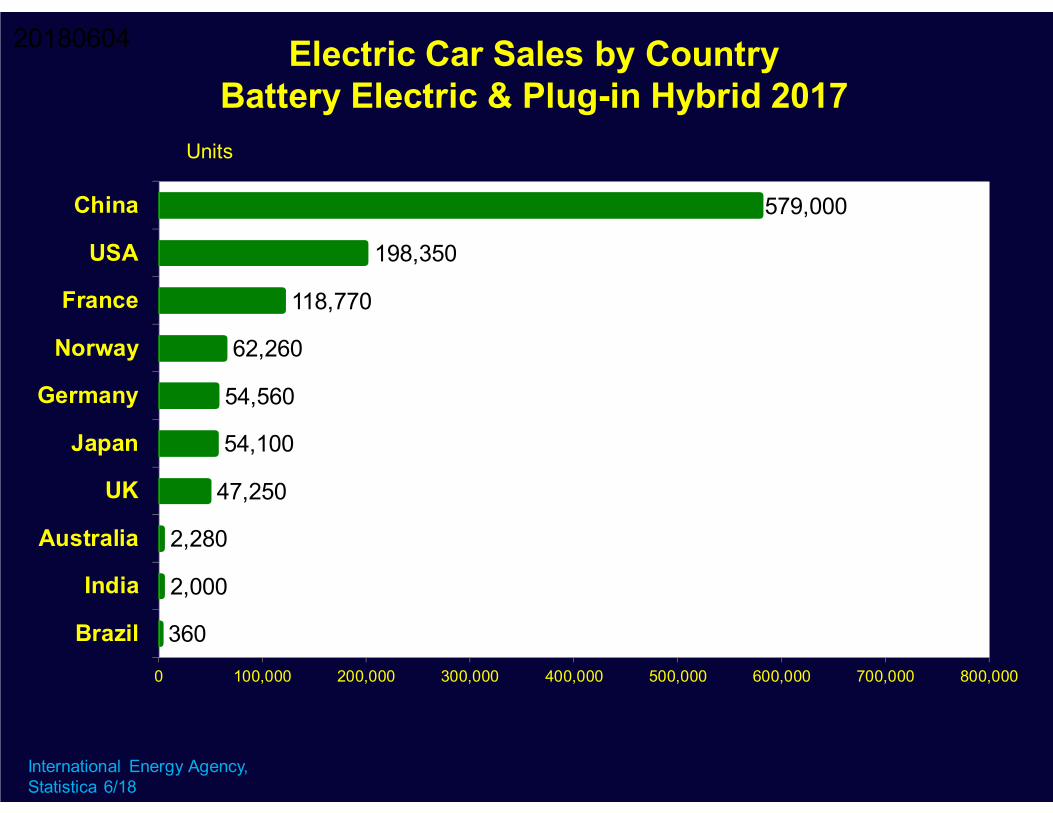

Electric Car Sales by CountryBattery Electric & Plug-in Hybrid 2017

International Energy Agency, Statistica 6/18

20180604

360

2,000

2,280

47,250

54,100

54,560

62,260

118,770

198,350

579,000

0 100,000 200,000 300,000 400,000 500,000 600,000 700,000 800,000

Brazil

India

Australia

UK

Japan

Germany

Norway

France

USA

China

Units

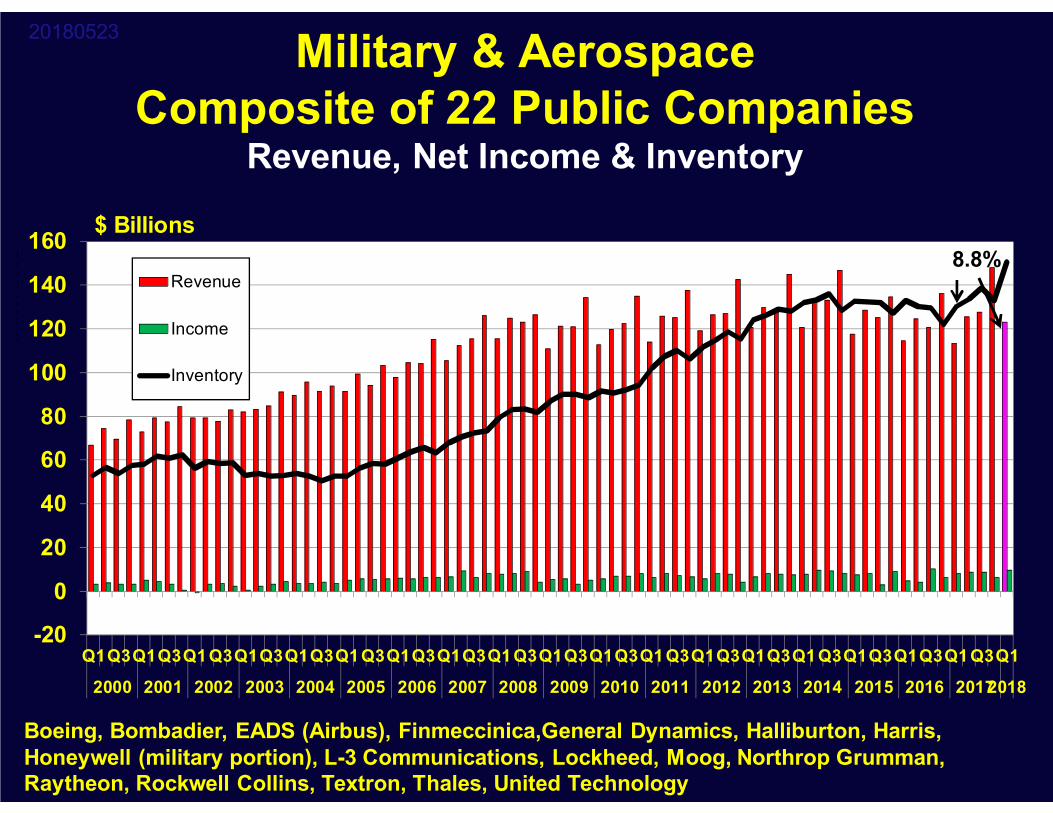

Military & AerospaceComposite of 22 Public Companies

Revenue, Net Income & Inventory

Boeing, Bombadier, EADS (Airbus), Finmeccinica,General Dynamics, Halliburton, Harris, Honeywell (military portion), L-3 Communications, Lockheed, Moog, Northrop Grumman, Raytheon, Rockwell Collins, Textron, Thales, United Technology

20180523

-20

0

20

40

60

80

100

120

140

160

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ Billions

Mill

ions Revenue

Income

Inventory

8.8%

European Production - Aircraft, Spacecraft & Related Equipment

Eurostat, C303 category, EU 27 countries

20180613

40

50

60

70

80

90

100

110

120

1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Index (2015=100), Seasonally Adjusted

Instruments & Control EquipmentComposite of 16 Public Companies

Revenue, Net Income & Inventory

ABB, Agilent, Ametek, Emerson, Itron, Keysight, National Instruments, PerkinElmer, Rockwell Automation, Rotork, Teledyne, ThermoFisher, Woodward Govenor

20180607

-10

0

10

20

30

40

50

60

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ Billions

Mill

ions

Revenue

Income

Inventory

+12.2%

European Production - Instruments & Appliances for Measuring, Testing & Navigation

Eurostat, C2651 category, EU 27 countries

20180613

60

70

80

90

100

110

120

1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6 11 4 9 2 7 12 5 10 3 8 1 6

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Index (2015=100), Seasonally Adjusted

VolumeConsumer-driven

Products

Volume Markets

0

50

100

150

200

250

300

350

400

450

Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Thou

sand

s Smartphones PCs Tablets Digital Still CamerasWorld Units (Millions)

20180619

www.gartner.com; www.cipa.jp/; www.icinsights.com; www.idc.com; www.digitimes.com

1Q’18 Computer GrowthServers +33.4%Higher PC performance & pricesUS$ value inflated by Exchange rateGamingCrypto mining

World Server Shipment Revenue

Gartner 6/18 & prior reports

02468

101214161820

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

US$ Billions

20180612

+33.4%

Autonomous carsInternet of Things (IoT)Industrial Internet of Things (IIoT)Cloud storage5G Handsets & InfrastructureVirtual & Augmented RealityAI/Machine LearningSmart Cities, Smart AgricultureDronesRobotsWearables3D PrintingHealth Care

Emerging Volume Markets

Things Connected to Internet

Visual Capitalist 11/17CISCO IBSGFusion

20151219

Semiconductors

World Semiconductor SalesMemory & non Memory

Gartner 1/18

20180116

16.6% -1.3% 1.1%64.3% 13.7% -12.9% -10.2% 10.2%

342.4 334.9 343.5

419.7 451.0 444.0 448.9 477.7

0

100

200

300

400

500

2014 2015 2016 2017 2018 2019 2020 2021

non MemoryMemory

Revenues & Growth ($ Billions)

6.3%-2.2% 3.0%

9.4%

4.6% 4.1% 5.8%5.1%

8.5% -2.2% 2.6%

22.2%7.5% -1.6% 1.1%

6.4%

Total Semiconductor Shipments to an AreaMonthly Shipments - Reporting Firms

www.wsts.org,www.sia-online.org/

20180606

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Japan

N America

Europe

Asia-Pac

$ Billions Asia Pacific

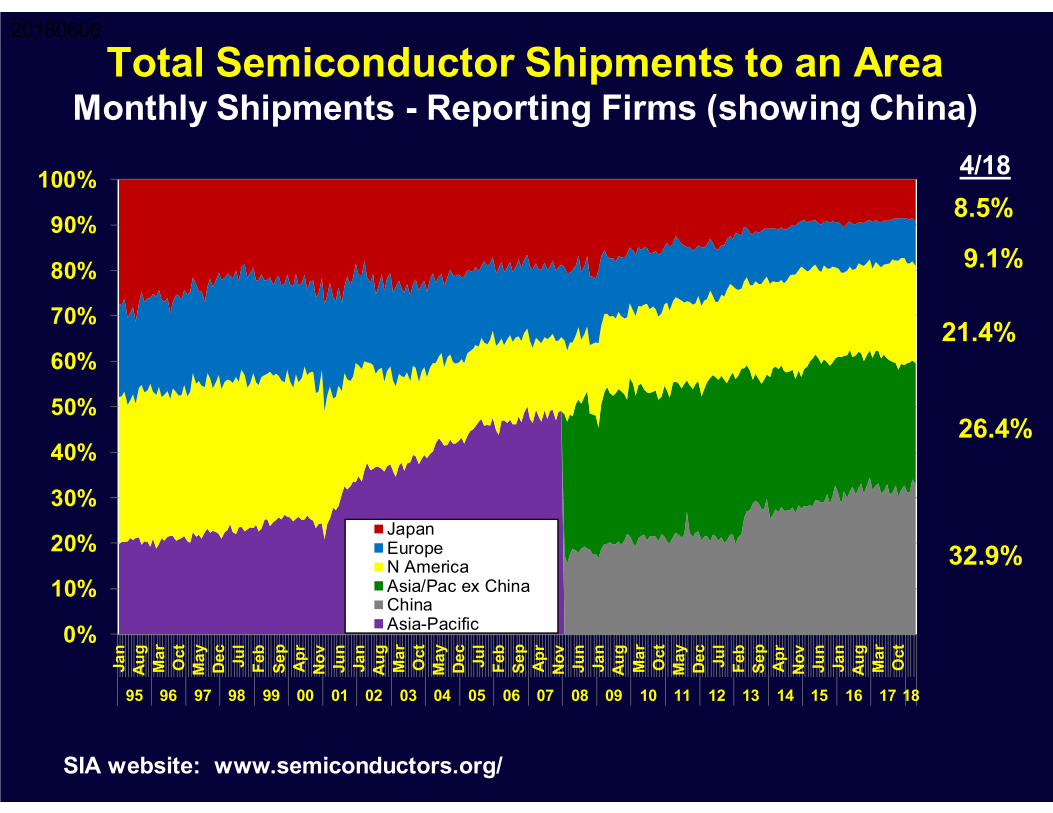

Total Semiconductor Shipments to an AreaMonthly Shipments - Reporting Firms (showing China)

SIA website: www.semiconductors.org/

20180606

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan

Aug

Mar Oct

May De

cJu

lFe

bSe

pAp

rNo

vJu

nJa

nAu

gM

ar Oct

May De

cJu

lFe

bSe

pAp

rNo

vJu

nJa

nAu

gM

ar Oct

May De

cJu

lFe

bSe

pAp

rNo

vJu

nJa

nAu

gM

ar Oct

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

JapanEuropeN AmericaAsia/Pac ex ChinaChinaAsia-Pacific

4/18

9.1%

8.5%

21.4%

32.9%

26.4%

SemiconductorCapital

Equipment

Semiconductor Capital Equipment Shipments by Area

SEMI

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

ROWChinaTaiwanS KoreaN AmericaJapanEurope

$ Billions

+28%

EuropeSupply Chain

European Computer, Electronic and Optical Products, Semiconductors, & SEMI Equipment Shipments

Total $ Semiconductor Shipments from All Countries to Europe www.sia-online.org/, Eurostat class C26 & SEMI, CCG Extrapolation of SEMI growth

20180515

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

Jan

Jul

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Semiconductor shipments to Europe

Computer, electronic and optical products

SEMI equipment shipments to Europe

DMASS-electronic component distribution

Zero growth

Euro 3/12 Rate of Change

ShortagesDrive Component

Sales

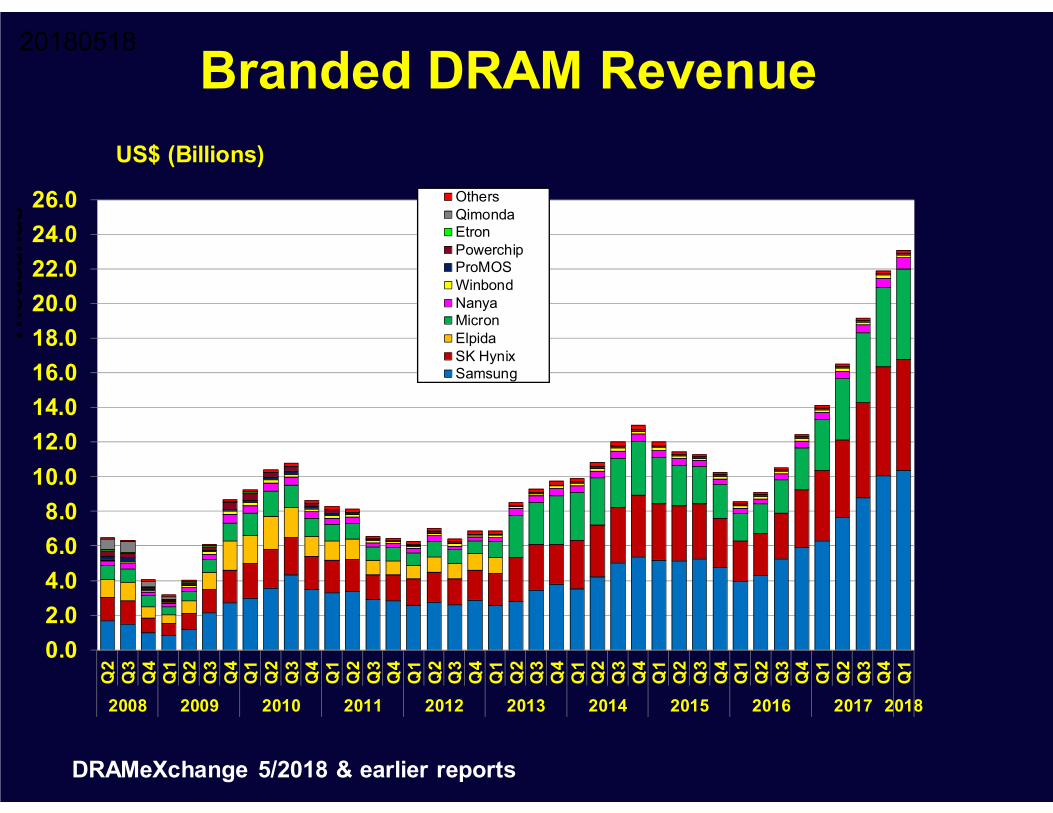

Branded DRAM Revenue

DRAMeXchange 5/2018 & earlier reports

20180518

0.02.04.06.08.0

10.012.014.016.018.020.022.024.026.0

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Thou

sand

s

OthersQimondaEtronPowerchipProMOSWinbondNanyaMicronElpidaSK HynixSamsung

US$ (Billions)

Passive ComponentsComposite of 14 Companies

Revenue, Net Income & Inventory

ALPS, AVX, Bel Fuse, Diodes, International Rectifier, Kemet, Knowles, Littlefuse, Murata, RF Micro, Rohm, Vishay, TDK, Yageo;Euro, Yen & NT$ converted to US$ at fluctuating exchange rates

20180518

-6.0-4.0-2.00.02.04.06.08.0

10.012.014.0

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ Billions

Revenue

Income

Inventory

24.6%

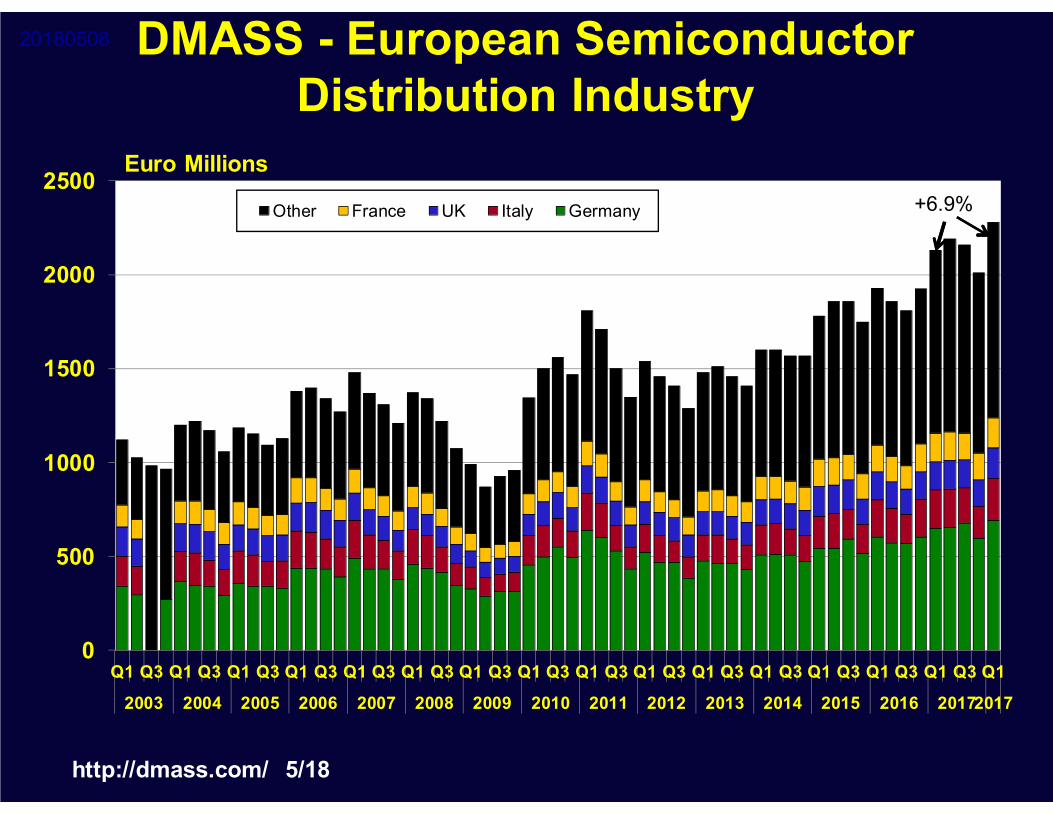

EuropeanComponent Shipments by Country

DMASS - European Semiconductor Distribution Industry

http://dmass.com/ 5/18

20180508

0

500

1000

1500

2000

2500

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172017

Other France UK Italy Germany

Euro Millions+6.9%

DMASSEuropean Semiconductor Distribution Industry

20180508

653695

201 220156 166152 157177 187

327366

467 489

0

100

200

300

400

500

600

700

800

900

1,000

1Q'17 1Q'18

Euros (Millions)

GermanyItalyUKFranceNordicE EuropeOther

DMASS 5/18; http://dmass.com/

“ Looking at the market by product, we cannot see a very consistent picture in Q1, some of the below-average increases in big product categories may be driven by allocation or channel shifts. However, one quarter does not really tell a story. After the dust of various market effects has settled, the situation may become clearer(and so far the weight of the big product groups has not really changed dramatically)."

Georg Steinberger, chairman of DMASS: "As we face peak demand in many industries and long lead-times for many semiconductor products, the growth is no surprise. It could have been even higher, considering channel shifts back to some manufacturers and the negative exchange rate effects from a weak US-Dollar. It remains to be seen how sustainable this is, considering that customers have to push out production in many instances due to hard allocation in other component segments. Nevertheless, at the moment outlook is solid."

EMS & ODM Companies

Global EMS & ODM Companies Composite of 52 Public Companies

Revenue

0

20

40

60

80

100

120

140

Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1Q3Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

US$ Sales @ fluctuating exchangeM

illio

ns +12.7%

20180518

US $ Billions

European EMS MarketWestern Europe and Eastern Europe

Source: In4ma [email protected]

20180125

16.4 17.0 17.2 17.9 18.515.5 16.9 17.1 18.2 19.3

31.933.9 34.3

36.137.8

0

5

10

15

20

25

30

35

40

45

2014 2015 2016 2017F 2018F

W Europe E Europe Total Europe

Euros B

Summary of 1,576 individual EMS entities plus 2.9%added to estimate to bring Europe 35.5 billion Euro for 2016.MENA not included

European Loaded Electronic Board Production

40

50

60

70

80

90

100

110

120

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 2015 2016 2017 2018

Index (2015=100); Seasonally Adjusted

Calendar YearEurostat, C2612

2017/20162017 2016 Growth %

Hon Hai (Foxconn) Taiwan 155,078 137,648 +12.7%Flextronics Singapore 24,893 24,419 +1.9%Jabil Circuit USA 19,544 18,651 +4.8%Sanmina USA 6,893 6,322 +9.0%Celestica Canada 6,110 5,604 +7.3%Venture Mfg Singapore 2,906 1,933 +52.7%Plexus USA 2,570 2,574 -0.1%Benchmark Elec USA 2,467 2,469 -0.1%

Total 220,544 199,844 +10.4%

Large Global EMS Providers20180303

Sources: Company data; 4Q’17 estimates for Benchmark, VentureLocal currency converted at fluctuating exchange

2017 vs. 2016 Sales ($M)

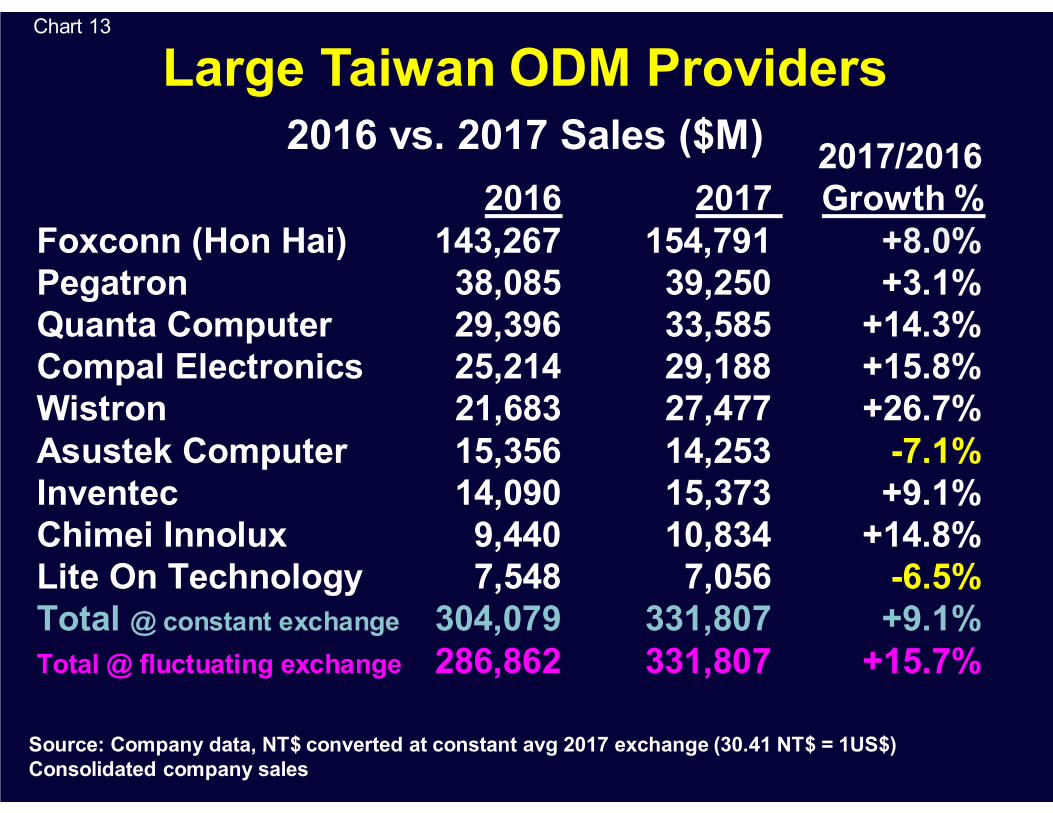

2017/20162016 2017 Growth %

Foxconn (Hon Hai) 143,267 154,791 +8.0%Pegatron 38,085 39,250 +3.1%Quanta Computer 29,396 33,585 +14.3%Compal Electronics 25,214 29,188 +15.8%Wistron 21,683 27,477 +26.7%Asustek Computer 15,356 14,253 -7.1%Inventec 14,090 15,373 +9.1%Chimei Innolux 9,440 10,834 +14.8%Lite On Technology 7,548 7,056 -6.5%Total @ constant exchange 304,079 331,807 +9.1%Total @ fluctuating exchange 286,862 331,807 +15.7%

Large Taiwan ODM ProvidersChart 13

Source: Company data, NT$ converted at constant avg 2017 exchange (30.41 NT$ = 1US$)Consolidated company sales

2016 vs. 2017 Sales ($M)

Taiwan ODM CompaniesComposite Sales of 11 Large Manufacturers

0

200

400

600

800

1,000

1,200

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

n

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

May 2018 up 13.4% vs. May 2017 and up 3.5%sequentially from April 2018

Total 2017 up 9.1% in NT$ vs. total 2016Up 15.7% in fluctuating exchange 2017 vs 2016 US$

NT$ (Billions)

Asustek Computer, Chei Mei, Compal Electronics, Foxconn, Chimei Innolux , Inventec, Inventec Appliance, Lite On Technology, Mitac International, Pegatron, Quanta Computer, Wistron, Chei Mei Display replacing Chei Mei & Innolux Display 3/10 & later

Calendar YearCompany Financial Releases

U.S. tariffs coulddrive assembly

fromChina to SE Asia

PCB Fabrication

World PCB Production 1980-2018

IPC: World PCB Production Report 2016 + Custer estimates for 2017 & 2018

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Thou

sand

s

US$

Calendar Year

Note: Each year was calculated independently using exchange rates for that year.

Because each year involved an independent evaluation and because exchange rates can fluctuate significantly, year-to-year growth rates may not be meaningful.

"Fluctuating exchange" growth rates can be significantly different vs. those calculated using constant exchange rates.

2016 World Total PCB Production by Geographical Area

IPC 9/17

4.9%

3.6%

8.9%

50.2%

12.4%

11.3% 8.3% 0.3%

N AmericaEuropeJapanChina/HKTaiwanS KoreaRest of AsiaROW

20170923

Total: $58.2 Billion

(US$ M @ Average 2016 Exchange)

Japan PCB Production20180525

0

10

20

30

40

50

60

70

80

90

100

Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

Sep

May Jan

82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Yen (Billions)

Calendar YearJEITA

2017/2016+1.6%

Taiwan Shipments42 Rigid PCB & 8 Laminate Manufacturers

20180609

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

5

10

15

20

25

30

35

40

45

50

55

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

PCB

Laminate

PCB – NT$ (Billions)

Calendar YearCompany Financial Releases

Laminate – NT$ (Millions)

S Korean Companies’ Global PCB Production

Private communication from industry source

20180523

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12015 2016 2017 2018

Total 1,980 1,890 2,035 2,000 1,937 1,844 1,972 1,961 1,939 1,965 2,206 2,634 2,043IC Substrate 530 510 540 530 518 504 545 537 512 496 541 538 533Flex 440 410 470 460 401 364 420 425 421 489 650 1138 529Rigid 1010 970 1025 1010 1018 976 1007 999 1006 980 1015 958 981

1,980 1,8902,035 2,000 1,937 1,844 1,972 1,961 1,939 1,965

2,206

2,634

2,043

0

500

1,000

1,500

2,000

2,500

3,000

3,500US$ millions (converted at 1150 won/$)

• Overseas production was about 12% of total PCB production last year• While FPCB makers are active in overseas expansion, none of substrate factories are outside Korea• The overseas portion will be increased this year due to rigid-flex PCB production at Samsung Electro-mechanics’

Vietnam site• With decrease in iPhone X sales as well as struggling Galaxy S9, the FPCB production of Q1 was less than

half of that of the last quarter. However it was still better than that of last year.• Others sectors were flat during the quarter

N American Rigid & Flexible PCB Shipments & Orders

0

50

100

150

200

250

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Shipments

Orders

2017/2016 Rigid & Flex PCB Shipments -1.8%, Orders +7.9%

Note: IPC survey captures "market" not domestic production. About 15% of the above represents imported boards resold by N American PCB producers in survey.

$M (statistical sample of about 50% of producers)

IPC

European Electronic Wiring Devices20180614

70

80

90

100

110

120

130

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Index (2015=100); Seasonally Adjusted

Calendar YearEurostat, C2733

Europe PMI Leading Indicator vs. Europe Wiring Devices

20180601

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan

Apr Ju

lO

ctJa

nA

pr Jul

Oct

Jan

Apr Ju

lO

ctJa

nA

pr Jul

Oct

Jan

Apr Ju

lO

ctJa

nA

pr Jul

Oct

Jan

Apr Ju

lO

ctJa

nA

pr Jul

Oct

Jan

Apr Ju

lO

ctJa

nA

pr Jul

Oct

Jan

Apr Ju

lO

ctJa

nA

pr Jul

Oct

Jan

Apr Ju

lO

ctJa

nA

pr Jul

05 06 07 08 09 10 11 12 13 14 15 16 17 18

Eurostat Wiring Devices

PCB Leading Indicator

Zero Growth

Source: Custer Consulting Group

3/12 Rate of Change

Calendar Year

FromMichael Gasch

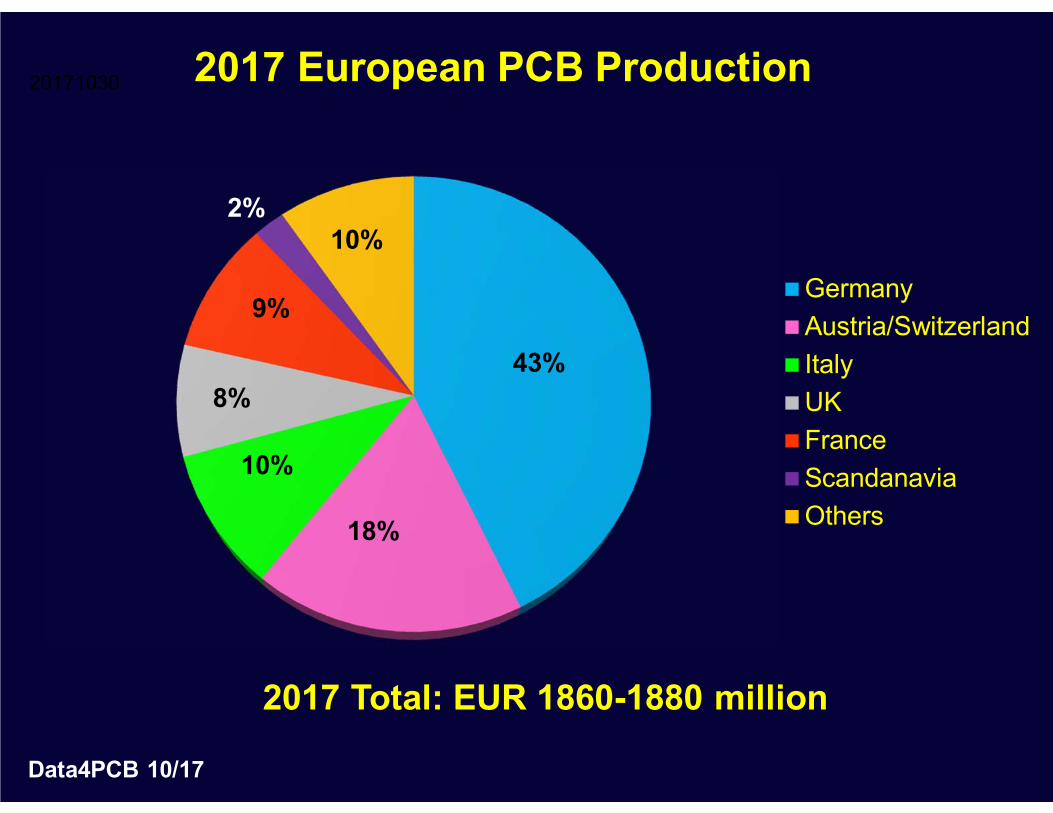

2017 European PCB Production

Data4PCB 10/17

2017 Total: EUR 1860-1880 million

43%

18%

10%

8%

9%

2%10%

GermanyAustria/SwitzerlandItalyUKFranceScandanaviaOthers

20171030

European PCB Production

Data4PCB 4/18 & prior

20171030

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017Other 601 577 422 408 410 346 309 264 221 169 170 155 157 151 158 170 172 202UK 641 478 368 340 330 278 252 197 177 137 165 161 158 153 165 173 163 149Scandanavia 351 309 260 201 200 198 169 137 103 64 64 64 50 40 42 40 40Austria/Switzerland 561 575 463 447 427 427 447 427 378 258 341 343 325 323 312 315 299 332Italy 619 530 444 338 324 281 284 248 212 156 181 186 174 168 174 181 188 206France 541 465 287 244 266 240 234 231 206 165 170 166 147 148 148 157 168 156Germany 1461 1300 1006 1027 1044 981 1054 1039 970 676 883 902 835 828 825 796 740 788

0

1000

2000

3000

4000

5000

6000Euros (Millions)

Russia & FSU not included

+5%

4.8 4.8 5.4 4.4 3.8 3.9 3.1 3.3

22.9 22.1 21.2 20.6 20.2 21.1 19.7 18.6

47.5 45.0 44.341.1 42.3 42.9

41.1 41.0

9.0 10.4 9.311.0 11.6 11.5

12.4 12.6

6.9 7.9 10.1 11.3 9.5 9.3 10.5 10.7

5.2 6.1 5.6 6.9 7.7 7.9 7.9 8.1

3.6 3.7 4.1 4.8 4.9 3.4 5.3 5.7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017

OthersFlex-RigidFlexHDIMLPTHn-PTH

European PCB Production by Technology

Data4PCB 4/18

20180426

18.3 17.6 17.7 16.7 19.4 20.4 21.0 21.8

2.6 2.5 2.0 2.1 1.7 1.5 1.6 1.410.9 8.4 10.4 8.2 7.0 6.9 5.6 5.2

3.32.8 1.9 3.0 2.9 2.9 2.6 2.1

8.2 9.7 6.7 7.1 7.3 7.8 7.9 8.23.9 4.2 4.4 4.8 5.3 5.6

37.5 41.8 43.2 43.8 42.9 40.8 40.3 39.8

7.6 7.2 7.1 7.8 8.2 8.8 9.6 8.311.6 9.9 7.1 7.1 6.2 6.1 6.1 7.5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016 2017

OtherMedicalIndustrialAeronauticsDefenseConsumerCommunicationComputerAutomotive

European PCB Production by End Market

Data4PCB 4/18

20180426

PCB industry in Europe 2000 – 2017revenues and number of manufacturers

4,77

54,

233

3,25

02,

937

3,00

43,

001

2,75

02,

748

2,54

32,

267

1,62

51,

969

1,97

21,

846

1,80

71,

831

1,81

51,

747

1,83

3

555

488457

405

478426

379 374359

333

314 304 299284

272252 247

230 223

0

100

200

300

400

500

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2000 2002 2003+ 2005 2007 2009 2011 2013 2015 2017

Revenues in million EUR Number of

manufacturers

* 2003+ = incl. Central Europe

Data4PCB 4/18 & earlier

Europe’s Top 41 PCB Companies Ranked by 2017 Revenues20160502

Rank Company Rank Company 1 AT&S / A 22 Cicor Group / CH

2 Würth Gruppe / D 23 Schaltungsdruck Storz / D

3 Schweizer Electronic / D 24 Aspocomp Oy –Gruppe / Fin4 KSG GmbH + Co KG / D 25 ACB N.V. / B

5 Elvia Group / F 26 Eleprint srl / I

6 Mektec Europa / D 27 Europrint Eger Kft / B

7 Unimicron Germany / D 28 Tecnomaster SpA / I

8 SoMaCis / I 29 Graphic plc / GB

9 hmp Macroprint / D 30 Spirit Group / GB

10 Elco Group / I + NL 31 Silga SpA / I11 European Electronic Systems / D 32 TW Elektronik Horst Muller / D

12 GS SwissPCB AG /CH 33 Ilfa / D

13 Dyconex AG / CH 34 Elekonta Marek GmbH / D

14 Varioprint AG Electronic / CH 35 OMR Italia SpA / I

15 Hausermann GmbH / A 36 Merlin (Falcon) Group / GB

16 Amphenol-Invotec /GB 37 Precoplat / D

17 Cimulec Group / F 38 Asetronic AG / CH

18 Optiprint AG / CH 39 Jenaer Leiterplatten / D

19 Cistelaier-Group / I 40 LAB Circuits S.A. / E

20 Polytron Print GmbH / D 41 Techno Service / PL

21 Rohde & SchwarzData4PCB

4/17

2017 European PCB Production

Data4PCB 4/18

EUR 1832 million

43.0%

18.1%

11.2%

8.5%

8.2%

6.9% 4.1%

GermanyAustria/SwitzerlandItalyFranceUKBelgium/Netherlands/ScandanaviaCentral Europe

20160502

Michael Gasch Comments 6/18Up to April sales of the ZVEI-group have been 7% better than in the years 2015 to 2017 for the same 4 months.

This good result is shared by all participants (small to big) and I can't pinpoint it to a certain industry. Plausible explanations might be that during the shortage of copper foil several new projects were not (yet) transferred to Asia and are still remaining to a certain extent in Europe and Asia no longer is the cheap-cheap working bench for Europe as wages are rising.

France had poorer sales during the first quarter than last year, apparently a big project for defense and/or aeronautics came to an end last year and there is no replacement in the same volume.

UK is again reporting to the B2B statistics, however, with a different group of companies. Therefore, all previous results had to be corrected. During the 1st quarter sales in GBP rose 7.3%. As export sales account for just about 20-25% and most of the business is transacted within the own country the consequences of the coming Brexit are not (yet) felt.

Michael Gasch Comments 6/18

A much greater concern, however, is the erratic behavior of the US president. The longer he is in office the more multinational treaties and agreements are no longer valid. I wonder what the North Koreans are thinking regarding how long any promises will be valid. This can't be explained any longer with "America first".

Everything is just at the whim of the day. And this has effects on the business confidence in the PCB (and the electronic) industry in Europe. I wonder as well how long it will take China to put an export ban on PCBs or electronic components for people like Apple and Google and Facebook ("as it is against the national security") and without those components servers in the USA will run on a "flat tire"...

Process Equipment, Laminate &

Materials Suppliers

Process Equipment Related SuppliersComposite of 12 Companies

Revenue

C-Sun,Tailing Technology, Camtek, Cadence, ESI, GSI Group, Mentor Graphics, Nordson, Rofin-Sinar, Coherent, Orbotech, Data I/O

20180523

0

500

1000

1500

2000

2500

3000

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ Millions

+15.8%PCBFlat Panel DisplaysTouch ScreensPhotovoltaic

Material Suppliers (excluding laminate)Composite of 14 Companies

Revenue

Momentive, OM Group, Taiwan Glass, Baotech, Glotech, Shenmao, Wahlee,Topoint, Cabot Micro, Cookson Elec, Eternal Chemical, Hexcel, Chang Wah, Platform Specialty Products

NT$ & GBP converted to US$ at fluctuating exchange

201805184

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ Millions

+15.5%

Rigid & Flex Laminate SuppliersComposite of 13 Companies

Revenue

Arisawa, Arlon Electronic Materials, Elite Materials, Hwa Woei, Iteq, Microcosm,Park Electrochemical, Rogers, Shinemore, Taiflex, Thinflex, Top Union, Uniplus

NT$ converted at fluctuating exchange

20180518

0100200300400500600700800900

1000

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

$ Millions+8.4%

Global Growth RatesProcess Equipment, Materials & Laminate

20180523

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Process Eq

Materials

Laminate

Zero Growth

3/12 Rate of Change

Company Financials of 12 Laminate suppliers, 13 material suppliers & 8 Process Equipment Suppliers

Calendar Year

World PCB Model

Regional PCB Shipment Growth20180614

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

Taiwan/China

S Korea

Japan

N America

Europe

Zero Growth

3/12 Rate of Growth (in local currency)

Sources: IPC, JPCA, Taiwan/China composite; Eurostat "wiring devices" for Europe

Calendar Year

2016 World Total PCB Production by Geographical Area

IPC 9/17

4.9%

3.6%

8.9%

50.2%

12.4%

11.3% 8.3% 0.3%

N AmericaEuropeJapanChina/HKTaiwanS KoreaRest of AsiaROW

20170923

Total: $58.2 Billion

(US$ M @ Average 2016 Exchange)

World PCB Monthly ShipmentsConverted @ Fluctuating Exchange Rates

20180614

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18

N AmericaEuropeJapanTaiwan/ChinaRest of AsiaKorea

$ Billions

Source: Custer Consulting GroupCalendar Year

Note:harmonization with 2016 IPC World Market report

Forecasts

6.3

4.7

0.8

1.7

2.0

3.0

6.5

4.5

1.0

2.1

2.2

3.1

6.9

4.3

1.7

2.4

2.3

3.1

0 2 4 6 8

China

Emerging Markets

Japan

Euro area

USA

World

% Annual Growth

2017 2018F 2019F

Real GDP GrowthGrowth rates calculated using constant 2010 US$ weights

World Bank 6/18, www.worldbank.org

20180609

Asked if there was a risk for the global economy, WTO Director-General Roberto Azevedo stated: "Absolutely. If the trade dispute escalates, there's the risk of a global downturn and we're already seeing signs that this downward process has already started." He said it was crucial to maintain dialogue to avoid an escalation.

Worldwide Semiconductor Market by GeographyWSTS Forecast

WSTS 6/18

20180606

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019Total 149.4 204.4 138.9 140.8 166.3 213.1 227.4 247.7 255.6 248.6 226.3 298.3 299.5 291.6 305.6 335.8 335.2 338.9 412.2 463.4 483.7Asia Pacific 37.2 51.3 39.8 51.2 62.8 88.8 103.5 116.5 123.5 124.0 119.6 160.0 164.0 163.0 174.4 194.2 201.1 208.4 248.8 279.4 291.3Japan 32.8 46.7 33.1 30.5 38.9 45.8 44.1 46.4 48.8 48.5 38.3 46.6 42.9 41.1 34.8 34.8 31.1 32.3 36.6 39.8 41.4Europe 31.9 42.3 30.2 27.8 32.3 39.4 39.1 39.9 41.0 38.2 29.9 38.1 37.4 33.2 34.9 37.5 34.3 32.7 38.3 43.4 45.5Americas 47.5 64.1 35.8 31.3 32.3 39.1 40.7 44.9 42.3 37.9 38.5 53.7 55.2 54.4 61.5 69.3 68.7 65.5 88.5 100.9 105.5

149

204

139 141166

213 227248 256 249

226

298 300 292 306336 335 339

412

463484

0

100

200

300

400

500

+21.6% +12.4% +4.4%$ B

Worldwide Semiconductor Market by TypeWSTS Forecast

WSTS 6/18

20180606

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019Total 255646 248604 226314 298316 299522 291561 305582 335842 335168 338931 412222 463411 483719IC-Memory 57854 46348 44797 69614 60749 56995 67043 79232 77205 76767 123974 156786 162545IC-Logic 67292 73531 65215 77377 78782 81703 85928 91633 90753 91498 102209 109476 114747IC-Micro 56211 53140 48330 60633 65204 60238 58686 62072 61298 60585 63934 66152 68582IC-Analog 36453 35637 32001 42285 42338 39303 40117 44365 45228 47848 53070 58095 61044Sensors 5126 5111 4753 6903 7970 8009 8036 8502 8816 10821 12571 13306 14118Optoelectronics 15901 17902 17043 21702 23092 26175 27571 29868 33256 31994 34813 35986 38024Discrete 16809 16935 14175 19802 21387 19138 18201 20170 18612 19418 21651 23610 24659

256 249 226

298 300 292 306336 335 339

412463 484

-50

50

150

250

350

450

550$ Billions

World PCB Shipments (with forecast)Converted @ Fluctuating Exchange Rates

20180614

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Jan

Jun

Nov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

nJu

nN

ov Apr

Sep

Feb

Jul

Dec

May Oct

Mar

Aug Ja

n

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19

ActualForecast

-2.8%

$ Billions

Source: Custer Consulting Group - 2010 base year expanded by monthly growth of N. American, European, Japanese, Korean & Taiwan/China monthly PCB shipments

Calendar Year

Growth calculations:Europe = Eurostat “Wiring Device”Japan & N. America from JPCA & IPC dataTaiwan/China:46 rigid & flex company compositeS Korea from NT Information, company composites & KPCA

+.2%

Note:Historical data harmonized with IPC World Market reports 10/30/17

+6.8%+5.3%

Summary

Expect slowing growth due to trade disputes

Long standing regional alliances are now in question

Electronic assembly may shift to countries less affected by tariffs

Many exciting new electronic products are on the horizon but without attitude changes growth may be limited.

20111007

Custer Consulting Group Products

Daily News Services (6 days/week)- Global electronics supply chain- Solar/Photovoltaic supply chain- Automotive supply chain

Business Outlook- Market charts & data

Global marketOEMsComponents, EMS, ODM, materials & process equipSolar/Photovoltaic

- Weekly Market Comments with latest charts

20111007

Looking forward to Session 2

And thank youMichael Weinhold

for all that you have done for the EIPC and the industry

For a copy of my updated charts

Give me your business card

Ask about our newAutomotive News Service