business optimism index - boi asean q1 2016

TRANSCRIPT

D U N & B R A D S T R E E T

ASEANBusiness Optimism IndexQuarter 1 2016

GROWING RELATIONSHIPS THROUGH DATA

MeasuringConfidence

MeasuredDecisions

BUSINESS OPTIMISM INDEXThe Dun & Bradstreet Business Optimism Index (BOI) report is a measure of business confidence in the economy. Released quarterly, it measures the pulse of the business community and is one of the most effective ways to track how the business community perceives the business environment, and where they think it is going. Over time, this quarterly survey has emerged as a leading indicator of turning points in economic activity in countries which it is published.

SURVEY METHODOLOGYFor the purpose of conducting the survey, a sample is randomly selected from Dun & Bradstreet database, consisting of companies belonging to the following sectors including Agriculture, Construction, Utilities, Finance, Manufacturing, Mining, Services, Transportation, Wholesale, and Real Estate.

All the respondents in the survey are asked six standard questions regarding their expectations as to whether the following critical parameters pertaining to their respective companies will register an increase ( ), decline ( ) or show no change ( ) in the ensuing quarter as compared to the same quarter in the prior year: Volume of Sales, Net Profits, Selling Prices, New Orders, Inventory Levels, and Employees.

The individual indices are then calculated by subtracting the percentage of respondents expecting decreases from those expecting increases. Unless otherwise stated, increases and decreases in indices represent changes from the previous quarter.

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION WHOLESALERSSERVICESMININGUTILITIES FINANCE

SALES VOLUME

NETPROFIT

NEW ORDERS

SELLING PRICE

INVENTORY EMPLOYMENT

REAL ESTATE

ASEAN Business Optimism Index

7th 3rd&largest in the world

largest in Asia

The leading indicator of business confidence for Southeast Asia region

| QUARTER 1, 2016

In 2014, ASEAN economy was

the the

SALES VOLUME

NETPROFIT

SELLING PRICE

INVENTORY EMPLOYMENT

Businesses are asked to give their outlook on six key indicators

ASEAN-6INDONESIA

MALAYSIA

PHILIPPINES

SINGAPORE

THAILAND

VIETNAM

SALES VOLUME

NET PROFIT

SELLING PRICE

NEW ORDERS

INVENTORY

EMPLOYMENT

NEW ORDERS

Source: ASEAN Secretariat

SUMMARYBusiness sentiment starts off the year in a positive note for almost all of the 6 ASEAN member states surveyed by Dun & Bradstreet for its quarterly Business Optimism Index (BOI). The Philippines extends its gains healthily while Vietnam takes a seasonal correction from its fast-paced growth. Things may have finally bottomed out in Malaysia and Indonesia as confidence bounces back in the first quarter, after a prolonged period of decline. Thailand is also seeing bright spots across the economy with stimulus measures in place. The lone exception is Singapore, where weakness in its manufacturing industries push business expectations down to a multi-year low.

The Dun & Bradstreet ASEAN BOI is the first and leading business optimism metric for Southeast Asia, one of the world’s largest trade regions which officially established the ASEAN Economic Community (AEC) in December 2015.

INDEX

INDONESIA Hands on Deck for a Better Outlook 05

MALAYSIA Too Early for Signs of Green Shoots? 08

PHILIPPINES Spring Fever for Filipino Businesses 11

SINGAPORE Chips Stay Down for Manufacturing 14

THAILAND Economic Stimulus Starts to Bear Fruit 17

VIETNAM Fast-Track Growth Takes a Pit Stop 20

Hands on Deck for a Better Outlook

The government has put their hands on deck with stronger reform momentum. One of its efforts in maintaining purchasing power is realized through the non-taxable income policy. Investment is also expected to exceed household consumption as the backbone of economic growth. The government targets investment growth to reach 8.6% to 9% in 2016. In addition, it will coordinate with the central bank to extend the coverage of social welfare programs throughout local governments to rein in the national inflation target at 4.7% in 2016.

The Indonesian Employers Association (Apindo) also agrees that economic prospects will be brighter. One trigger is the economic policy package comprising volumes 1-7 (issued by the government since mid-2015), which is expected to bring positive stimulus to the market in the near future. Another optimism-friendly measure is the establishment of One Stop Services (OSS) to accelerate business licensing services through the Investment Coordinating Board (BKPM). This effort has succeeded in improving Indonesia’s ranking from 120 to 109, in the Ease of Doing Business survey released by World Bank Group.

After registering four consecutive quarters of decline throughout 2015, the new Business Optimism Index (BOI) opens Q1 2016 with an improved optimistic outlook from surveyed companies. The overall BOI score rose from 27.8% in previous quarter to 34.6% in Q1. Besides Selling Price, all parameters are expansionary on q-o-q basis. A net weighted 15.3% of respondents expect the market to grow better than last year. Meanwhile, the proportion holding a pessimistic outlook stayed low at only 2.9%.

– Volume of Sales and New Orders registered the largest improvement by 19% and 18% q-o-q respectively. Wholesale is the most optimistic sector in both instances, followed by Mining and Services.

– Net Profit experienced the third largest improvement among all parameters with 16.7% from -0.3% to 17% in Q1 2016.

– Inventory and Employment also increased, by 4% and -3.3% respectively. Agriculture, Wholesale, and Mining are the most optimistic sectors for this parameter.

– Selling Price is the only parameter that posted a decrease (-0.7%) from 10% to 9.3% in Q1 2016. This is as most respondents have increased prices in the last quarter, due to the weakening rupiah against US dollar.

While still overshadowed by global economic challenges such as China slowdown, Fed rate hike, and plunging commodity prices, Indonesia is expected to recover in 2016. Both the government and business community share the same optimistic outlook that economic performance will be better than last year, bolstered by household consumption rebound and robust investment. Bank Indonesia forecasted GDP in 2016 in a range of 5.2% to 5.6% or higher than 2015 (at 4.7%-5.1%).

Business Optimism IndexINDONESIA

Quarter 1 2016

Q3

90 7

70

80

5

6

60

450

340

302

0 0

20

10 1

Q3

Q2

Q2

Q1

Q4

Q3

Q3

Q4

Q4

Q4

Q1

Q1

Q1

Q2

2015 20162013 20142012

OVERALL BOI SCORE CHART (Q3 2012 – Q1 2016)

BO

I

SC

OR

E

GD

P

GR

OW

TH

(

%)

Composite BOI GDP Growth (y-o-y %)

NET PROFIT

SELLING PRICE

17.3Q-O-Q

0.7Q-O-Q

19.0

VOLUME OF SALES

Q-O-Q

2016 Q12015 Q42015 Q32015 Q22015 Q1

80

40

-20

60

0

20

-40

%

MANUFACTURING TRANSPORTATION ALLSERVICES UTILITIESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTION

80

40

-20

60

0

20

-40

%

80

40

50

-10

60

70

0

20

10

30

-20

%

Business Optimism IndexINDONESIA

Quarter 1 2016

MANUFACTURING TRANSPORTATION ALLSERVICES UTILITIESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTION

MANUFACTURING TRANSPORTATION ALLSERVICES UTILITIESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTION

ALL

NEW ORDERS

INVENTORY

EMPLOYMENT

4.7Q-O-Q

80

40

-20

60

0

20

-40

%

40

30

0

-30

20

10

-20

-10

-40

%

40

10

-5

15

20

25

30

35

0

5

-15

-10

%

Business Optimism IndexINDONESIA

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1

MANUFACTURING TRANSPORTATION ALLSERVICES UTILITIESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTION

MANUFACTURING TRANSPORTATION ALLSERVICES UTILITIESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTION

MANUFACTURING TRANSPORTATION ALLSERVICES UTILITIESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTION

6.7Q-O-Q

18.7Q-O-Q

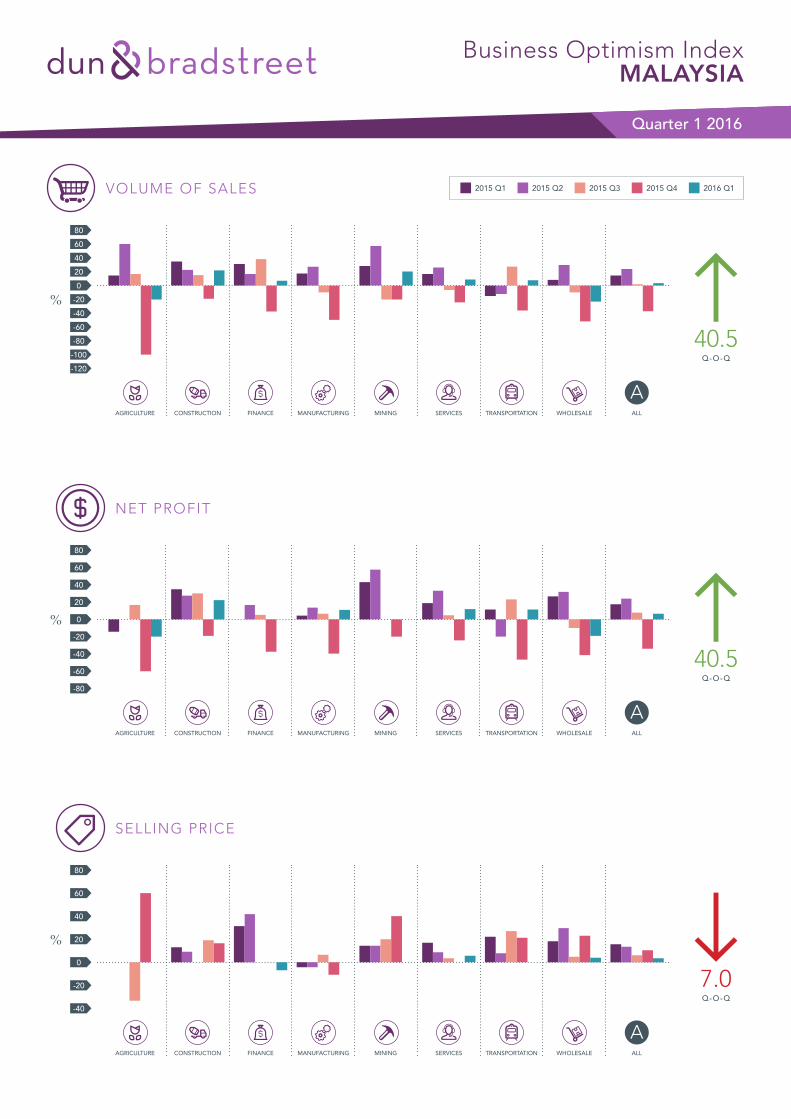

Too Early for Signs of Green Shoots?

under strain, as both residential and non-residential building activities have plateaued in recent months. Wholesale is the least optimistic given that export growth continues to be anemic.

Corruption scandals, alarmist reports of capital outflows, the persistently low oil price, the deteriorating inflation outlook, and disappointing growth in China have all conspired to depress consumer sentiment. The fiscal stimulus in 2016 will be limited. Taxes for high-income earners will be raised, and the overall budget deficit is scheduled to decline, but infrastructure spending will be more frontloaded than previously announced.

On the foreign exchange front, Malaysia’s fragile short-term liquidity profile makes the currency very vulnerable to any events that increase global risk-aversion. The currency is unlikely to strengthen under any scenario other than a sustained oil price recovery (which is improbable at the moment). Inflation is above target (and increasing), but the central bank is not in a position to raise rates, given the softening growth pattern. We have maintained our growth forecast of 4.5% for 2015, but lowered 2016 forecast to 4.7% (down from 5.2%).

Following a historic trough in confidence, Malaysian firms rebounded into the expansionary zone for the new quarter. According to Dun & Bradstreet Malaysia’s latest Business Optimism Index (BOI), all six indicators have sprung into positive territory for Q1 2016. The overall index rose from -14.5% to +4.8% for Q1 on a q-o-q basis, though markedly lower than the level seen last year at +13.1%.

– Both Volume of Sales and Net Profit experienced the largest q-o-q increases. As encouraging as this is, sentiments could be seasonal with Chinese New Year around the corner. The numbers are still significantly off the mark set a year ago, which suggests that broader weakness will be carried over to 2016.

– Meanwhile, Selling Price eased from +10.5% in Q4 to +3.5% in Q1 2016. Most respondents do not expect to raise prices, as consumers are already grappling with reduced purchasing power due to the weak ringgit, higher taxes, and higher inflation.

– New Orders for manufacturers reversed fortunes from -10.7% in Q4 to +8.1% in Q1 2016. Inventory finally edged above water after languishing for three consecutive quarters, rising from -8.0% in Q4 +0.5% in Q1 2016.

– Employment is positive again, from -4.5% in Q4 to +2.0% in Q1 2016. Most sectors remain unchanged from last quarter, with Construction recording the steepest decline.

It may be premature to ascertain that things will actually turn around for good as businesses tend to rake in more sales during the festive season. Services are expected to remain the strong pillar of the Malaysian economy while the once-rosy Construction sector is

Q2

40

30

20

10

0

-20

-10

Q3

Q1

Q1

Q4

Q2

Q3

Q3

Q4

Q4

Q1

Q2

2015 20162013 2014

OVERALL BOI SCORE CHART (Q2 2013 – Q1 2016)

BO

I

SC

OR

E

Business Optimism IndexMALAYSIA

Quarter 1 2016

VOLUME OF SALES

NET PROFIT

SELLING PRICE

80

0

40

-40

-100

60

-20

-80

20

-60

-120

80

40

-20

60

0

20

-40

80

0

40

-40

60

-20

20

-60

-80

%

%

%

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

Business Optimism IndexMALAYSIA

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1

40.5Q-O-Q

40.5Q-O-Q

7.0Q-O-Q

NEW ORDERS

15

10

0

-10

5

-5

-15

%

INVENTORY

%

EMPLOYMENT

40

30

10

-20

20

-10

0

-30

25

0

10

-10

-25

15

20

-5

-20

5

-15

-30

%

8.5Q-O-Q

MINING

Business Optimism IndexMALAYSIA

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

6.5Q-O-Q

18.8Q-O-Q

Spring Fever for Filipino Businesses

Expectations Survey revealed that business sentiment hit a two-year high in Q4, supported by a range of factors including rising sales and orders. Confidence was highest among businesses in the Wholesale & Retail trade sector.

The Philippines remains one of the fastest growing countries in the region. Overall, D&B maintains a broadly upbeat view of the economy and continue to expect full-year growth of 5.8% in 2015, followed by a slightly stronger expansion of 6.2% in 2016. While uncertainty over who will succeed current president Benigno Aquino could dampen investor sentiment to some degree in the short term, we expect improvements to the business environment will continue to be made after he leaves office. Indeed, all of the major candidates have indicated their intention to pursue further liberalisation should they win the election. While consumer price growth remains below the central bank’s 2-4% target range, the central bank has sufficient room to tighten monetary policy should inflation accelerate rapidly, as interest rates are at close to historic lows and the economy is growing at a healthy pace.

Businesses are upbeat for the coming spring. They bounced back from Q4 and rose 14% for the first quarter of 2016. The Business Optimism Index (BOI) stands at 66%, the highest in the ASEAN region for all key markets surveyed by Dun & Bradstreet. Almost 70% of respondents have increased expectations while only 3% decreased. The rest were unchanged. All the parameters grew convincingly in Q1 from the preceding quarter; four of them by double digits.

– Volume of Sales inched up by 0.7 to a high 81%. Net Profit rose by 7 percentage points to 80%. Wholesale, Construction and Services are riding on the wave of optimism.

– Selling Price went up by 17%. Higher food prices are largely responsible for driving the rise in inflation. Consumer prices rose at the fastest pace so far this year, indicating that inflationary pressures are gradually building.

– New Orders climbed 16 percentage points to 77% in Q1, led by Wholesale and Services. Inventory jumped 23 percentage points, with strong upticks in Mining, Wholesale and Manufacturing.

– Employment hit above 50% confidence level for the first time, reaching 59%. This is an increase of 22% from the previous quarter, with almost all sectors showing expansion. On y-o-y basis, it is an increase of 35%.

Two other surveys corroborated the findings above. According to the central bank’s Q4 Consumer Expectations Survey, consumer confidence has hit its highest level since the third quarter of 2013. Lower unemployment and an improving economy are two key factors that are supporting sentiment. Meanwhile, the central bank’s Business

80

60

40

20

0

Q2

Q4

Q1

Q3

Q1

2015 2016

OVERALL BOI SCORE CHART (Q1 2015 – Q1 2016)

BO

I

SC

OR

E

Business Optimism IndexPHILIPPINES

Quarter 1 2016

6.5

6

5.5

4.5

5

GD

P

GR

OW

TH

(

%)

Composite BOI GDP Growth (y-o-y %)

120

80

40

100

60

20

0

120

80

40

100

60

20

0

80

40

60

0

-60

20

-40

-20

-80

%

%

%

Business Optimism IndexPHILIPPINES

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1VOLUME OF SALES

NET PROFIT

SELLING PRICE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

17.3Q-O-Q

7.0Q-O-Q

0.7Q-O-Q

%

150

0

-100

100

50

-50

-150

%

120

80

40

100

60

20

0

%

120

80

100

40

-20

60

0

20

-40

Business Optimism IndexPHILIPPINES

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

NEW ORDERS

INVENTORY

EMPLOYMENT

22.0Q-O-Q

22.5Q-O-Q

16.0Q-O-Q

Chips Stay Down for Manufacturing

term. Our previous Q4 2015 report had forecasted hard knocks for the sector. It is the least optimistic sector with all six parameters in contraction, due to a sustained decline in output, most notably in the transport engineering, electronics and precision engineering segments. Survey findings also reveal that the outlook of construction firms has dampened for Q1 2016. Given that global risks are likely to be skewed downside, optimism levels could remain muted in the months ahead.

Dun & Bradstreet takes the view that the resiliency of the Singapore consumer will help to support near-term growth and absorb some of the weakness in the Manufacturing segment. In addition, the Monetary Authority of Singapore has shifted the main policy band in October by reducing the slope of the Singapore dollar’s appreciation. This movement toward a more accommodative policy measure will help to stimulate Singapore’s export market. A movement toward further accommodation remains likely given the current deflationary environment. The current weakness in Singapore’s real GDP should be considered a blip and growth will return to 2.3% in 2016.

Greater pessimism is felt across local businesses due primarily to constrained global demand as well as prolonged weakness and flat growth in the Manufacturing and Wholesale sectors. According to Singapore Commercial Credit Bureau (SCCB), which operates under Dun & Bradstreet Singapore, the overall index hit a historic multi-year low as it fell into negative territory from 0.14% in Q4 2015 to -2.93% in Q1 2016. On a y-o-y basis, the index slid 4.04% from the corresponding quarter last year.

– Both Volume of Sales and Net Profits deteriorated further in Q1 2016, by 2.75% and 4.92% respectively. Local firms are treading cautiously into 2016. Merely 6% of those surveyed expects to increase investment for business expansion while the vast majority stays unchanged.

– Selling Price is the only parameter which is expansionary, climbing from -6.43% in Q4 to +4.93% in Q1 2016. There is also a marginal improvement on y-o-y basis of 0.64%.

– Two other parameters fell into the red. New Orders for manufacturers remain contractionary, plunging from -22.22% in Q4 to a new depth of -56.0% in Q1 2016. Overall new orders for all sectors also lost ground, at -2.11%. Inventory slipped by 4.25% in Q1 2016.

– Employment took a large hit of almost 20%. Nevertheless the survey also found that 38% of respondents cited skills upgrading of employees as the most important area of investment for 2016, slightly above machinery and capital equipment (37%).

Manufacturing, which accounts for between 18-20% of annual GDP, will continue to be a drag over the near

Q1

40

30

35

25

20

10

15

-5

0

5

Q3

Q1

Q1

Q4

Q2

Q3

Q2

Q3

Q4

Q4

Q1

Q2

2015 20162013 2014

OVERALL BOI SCORE CHART (Q1 2013 – Q1 2016)

BO

I

SC

OR

E

Business Optimism IndexSINGAPORE

Quarter 1 2016

60

-20

20

-60

40

-40

0

-80

80

40

0

-60

20

-40

60

-20

-80

100

20

60

20

-80

80

0

-60

40

-40

-100

%

%

%

Business Optimism IndexSINGAPORE

Quarter 1 2016

VOLUME OF SALES

NET PROFIT

SELLING PRICE

2016 Q12015 Q42015 Q32015 Q22015 Q1

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

4.9Q-O-Q

2.7Q-O-Q

11.4Q-O-Q

20

-10

10

-30

-20

-50

0

-40

-60

%

80

40

0

20

60

-20

-40

%

80

0

40

-40

60

-20

20

-60

%

MINING

Business Optimism IndexSINGAPORE

Quarter 1 2016

NEW ORDERS

INVENTORY

EMPLOYMENT

2016 Q12015 Q42015 Q32015 Q22015 Q1

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

AGRICULTURE CONSTRUCTION MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALE

19.9Q-O-Q

4.2Q-O-Q

33.8Q-O-Q

Economic Stimulus Starts to Bear Fruit

Stimulus measures focusing on SMEs and low income earners are showing more concrete outcome, such as the development of government-sector infrastructure (1.7 trillion baht), assistance for IT retail businesses like 4G services, and the 10 Clusters Support policy. Consequently, the Government is aiming to reduce logistics costs per GDP by not less than 2% in all modes of transportation: railways, elevated trains, motorways, and Phase 2 of Suvarnabhumi Airport. Pump priming and 20% increase in the investment budget will spur private-sector investment and consumption.

Nonetheless, household incomes in the Agriculture sector are still low due to weak commodity prices. The ratio of household debts remains high, and the drought problem persists. Terrorism has affected the trade atmosphere, and international investment has stagnated. On the other hand, Tourism is set to welcome about 32.2 million foreign tourists, with those from China, continuing to rise satisfactorily. Construction should expand by 10% this year. Oil prices mired below US$40 per barrel will stabilize the price of raw materials, especially steel bars. The steadily weakening baht should also help baht-designated exports.

According to Dun & Bradstreet, almost all business confidence parameters went up compared to the last quarter, though they are still shy of the levels last year. Utilities and Wholesale & Retail sectors had the brightest outlook, showing sizable increases in most categories. Mining and Agriculture & Fishing suffered heavy fall in almost all indices.

– Both Volume of Sales and Net Profits moved in tandem, and increased from -12% last quarter to 7% in Q1 2016. But on y-o-y basis, both declined by 21% and 20% respectively. Respondents in Utilities had the best outlook, forecasting a net increase of 33%, followed by Wholesale & Retail. Mining fared the worst followed by Agriculture & Fishing.

– Selling Price held on to its position, budging by merely 1% from last quarter. On y-o-y basis, it had plunged by 14%. Services had the most positive direction, followed by Wholesale & Retail. Mining projected a net fall of 15% in Q1, followed by construction (-10%).

– New Orders is back to black after a contractionary quarter, and increased by 10%. On y-o-y basis, it had dropped by 18%. Services is the most favorable sector, expecting a net gain of 25%. This is followed by Utilities (+22%). Inventory improved from -10% last quarter to -2% in Q1 2016, and also performed better by 2% on y-o-y basis.

– Employment enjoyed a quarterly gain of 9% in Q1 2016, with 19% of respondents predicting an increase, 12% decrease and 68% foreseeing no change. Utilities is the most optimistic, with net growth of 44% followed by Construction (40%), in contrast with Agriculture & Fishing (-8%).

20

15

10

5

0

-10

-5

Q3

Q1

Q4

Q4

Q1

Q2

2015 20162014

OVERALL BOI SCORE CHART (Q4 2014 – Q1 2016)

BO

I

SC

OR

E

Business Optimism IndexTHAILAND

Quarter 1 2016

120

100

40

20

-40

80

60

-20

0

-60

%

ALLSERVICESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTIONUTILITIESMANUFACTURING TRANSPORTATION REAL ESTATE

ALLSERVICESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTIONUTILITIESMANUFACTURING TRANSPORTATION REAL ESTATE

ALLSERVICESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTIONUTILITIESMANUFACTURING TRANSPORTATION REAL ESTATE

120

100

40

20

-40

80

60

-20

0

-60

%

100

80

60

0

20

40

-20

%

Business Optimism IndexTHAILAND

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1VOLUME OF SALES

NET PROFIT

SELLING PRICE

1.0Q-O-Q

19.0Q-O-Q

19.0Q-O-Q

100

80

20

0

-60

60

40

-40

-20

-80

%

40

30

20

-10

-20

-50

10

0

-40

-30

-60

%

120

100

40

20

-40

80

60

-20

0

-60

%

Business Optimism IndexTHAILAND

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1NEW ORDERS

INVENTORY

EMPLOYMENT

ALLSERVICESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTIONUTILITIESMANUFACTURING TRANSPORTATION REAL ESTATE

ALLSERVICESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTIONUTILITIESMANUFACTURING TRANSPORTATION REAL ESTATE

ALLSERVICESMININGAGRICULTURE FINANCEWHOLESALECONSTRUCTIONUTILITIESMANUFACTURING TRANSPORTATION REAL ESTATE

9.0Q-O-Q

8.0Q-O-Q

10.0Q-O-Q

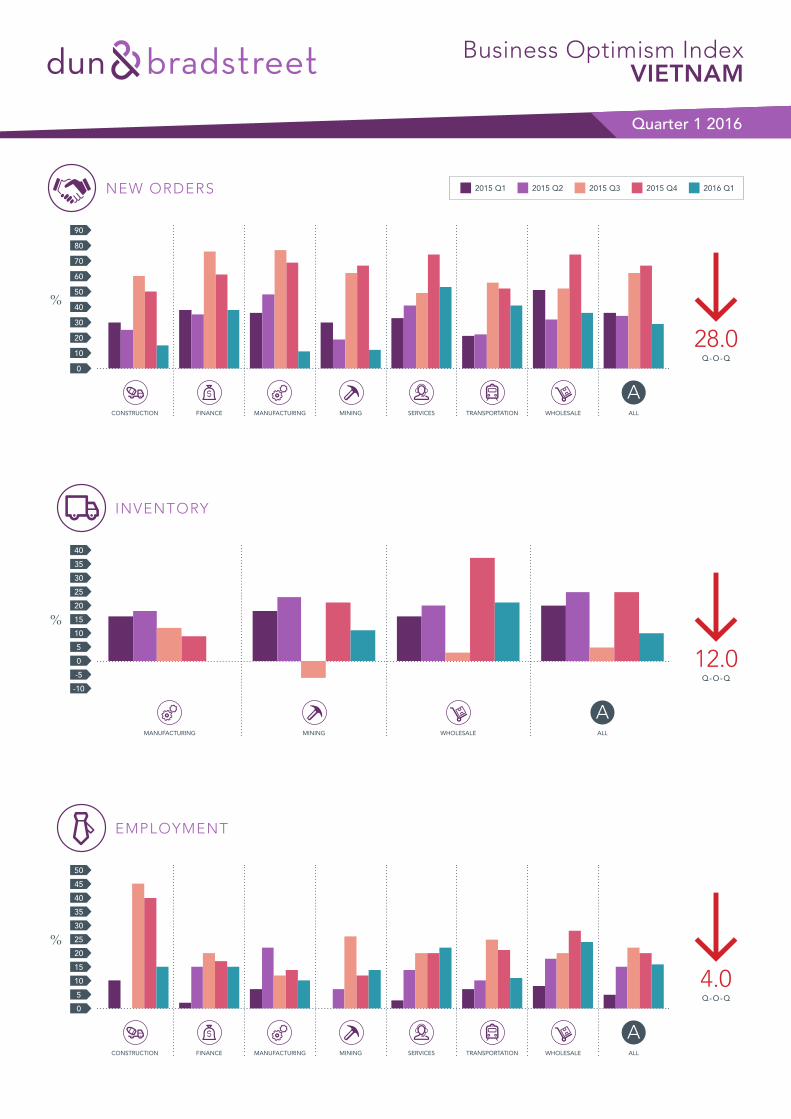

Fast-Track Growth Takes a Pit Stop

(see chart below). Therefore we view this as cyclical in nature and expect the readings to pick up in Q2. Recent fluctuations in the exchange rate may also have cast shadows on the business environment, specifically for Manufacturing.

Overall, Vietnam’s economic performance is on the acceleration track. Growth is estimated about 6.5% at least, with Industry & Construction projected to grow at 10%. D&B sees a number of factors supporting growth over the next few years. The first is strong exports, amid the continued relocation of low-end manufacturing from China to lower-cost regional locations. Even though exports from most emerging markets contracted in 2015, Vietnamese exports have still grown at close to double-digit pace. The other factor is loose monetary policy. Low inflation has given the central bank scope to keep interest rates low. Meanwhile, the banking sector is showing gradual signs of recovery. Credit growth is accelerating while the level of non-performing loans is down sharply.

From the outset, there does not seem to be much to cheer from the latest business confidence numbers released by Dun & Bradstreet Vietnam, as all six parameters fell and across all sectors. But at a closer look, the slump is most likely a seasonal correction which will rebound next quarter. The overall index was slashed by half from 45% to 22% in Q1 2016, after hovering above 40% for two consecutive quarters.

– Net Profit suffered the largest drop from 88% to 43% in Q1 2016. Volume of Sales moved in the same direction but in a slightly lesser range, from 71% to 36%. Deep cuts are felt in Construction, Mining, and Manufacturing.

– Selling Price kept to almost the same level at 2%, compared to 3% last quarter. This is the largest drop among the parameters on y-o-y basis (10 percentage points), and is rather obvious given the very low inflation this year (estimated to be less than 1%).

– New Orders plunged from 67% to 29% in Q1 2016, though it should be noted that Services, Transportation, Communication and Utilities held up fairly well. Change in Inventory level is milder with 12 percentage points down (from 20% to 8%).

– Employment recorded a 4 percentage point downward adjustment, from 20% to 16%. In y-o-y terms, this is actually the largest increase (11 percentage points), buttressed by stable and positive economic outlook for the year.

When compared y-o-y, these changes are rather mild, within +/- 10 percentage points or less in most cases. Even the overall score is similar to Q1 2015. In fact, similar drops are observed for Q1 in the last two years

Q4

50

40

30

20

0

10

Q3

Q3

Q1

Q4

Q1

Q4

Q1

Q2

Q2

2015 201620142013

OVERALL BOI SCORE CHART (Q4 2013 – Q1 2016)

BO

I

SC

OR

E

8

5

7

6

4

3

2

0

1

GD

P

GR

OW

TH

(

%)

Composite BOI GDP Growth (y-o-y %)

Business Optimism IndexVIETNAM

Quarter 1 2016

100

60

80

40

10

90

50

20

70

30

0

%

MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALECONSTRUCTION

MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALECONSTRUCTION

MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALECONSTRUCTION

100

60

80

40

10

90

50

20

70

30

0

%

25

15

5

-10

10

-5

20

0

-15

%

Business Optimism IndexVIETNAM

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1VOLUME OF SALES

NET PROFIT

SELLING PRICE

1.0Q-O-Q

41.0Q-O-Q

35.0Q-O-Q

MANUFACTURING ALLMINING WHOLESALE

90

60

80

40

10

50

20

70

30

0

%

50

30

40

20

5

45

25

10

35

15

0

%

40

20

10

-5

30

15

0

25

5

-10

%

Business Optimism IndexVIETNAM

Quarter 1 2016

2016 Q12015 Q42015 Q32015 Q22015 Q1NEW ORDERS

INVENTORY

EMPLOYMENT

MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALECONSTRUCTION

MANUFACTURING TRANSPORTATION ALLSERVICESMININGFINANCE WHOLESALECONSTRUCTION

35

4.0Q-O-Q

12.0Q-O-Q

28.0Q-O-Q

ABOUT DUN & BRADSTREET® (D&B)Dun & Bradstreet (NYSE: DNB) grows the most valuable relationships in business. By uncovering truth and meaning from data, we connect customers with the prospects, suppliers, clients and partners that matter most, and have since 1841. Nearly ninety percent of the Fortune 500, and companies of every size around the world, rely on our data, insights and analytics. For more about Dun & Bradstreet, visit DNB.com.

© Dun & Bradstreet, Inc. 2016. All rights reserved.

D&B BUSINESS OPTIMISM INDEX (BOI)

INDONESIA Analysis and commentary by Bayu Krisna Setyadi, Dun & Bradstreet Indonesia.

For more information, please visit www.dnb.co.id, or contact our Customer Service Center at +62 21 5790 0979, or email us [email protected].

MALAYSIA Analysis and commentary by Matthias Chen, Dun & Bradstreet Malaysia, with reference to D&B Country Insight Services.

For more information, please visit www.dnb.com.sg, or contact Matthias Chen at +65 6439 6670, or email [email protected].

PHILIPPINES Analysis and commentary by Ian Velasco, Dun & Bradstreet Philippines, with reference to D&B Country Insight Services.

For more information, please visit www.dnb.com.ph, or contact our Customer Service Center at +632 907 6080, or email us [email protected].

SINGAPORE Analysis and commentary by Singapore Commercial Credit Bureau.

Established in 2005, Singapore Commercial Credit Bureau (SCCB) operates a database of local enterprises and their credit history to provide clients with the insight needed to build trust and improve the quality of business relationships with their customers, suppliers and business partners. SCCB operates under Dun & Bradstreet Singapore. For more information, please visit www.dnb.com.sg, or contact Matthias Chen at +65 6439 6670, or email [email protected].

THAILAND Analysis by Dun & Bradstreet Thailand. Commentary by Asst. Prof. Pannarai Sangvichien, Ms. Nitaya Limphaisa, Mr. Somnuk Assadornviseth, Ms Sariya Nuchanong, Ms. Banjertsak SanhaPuckdee, Huachiew Chalermprakiet University.

For more information, please visit www.dnb.co.th, or contact our Customer Service Center at +662 657 3999 ext. 4200, or email us [email protected].

VIETNAM Analysis by Dun & Bradstreet Vietnam. Commentary by Assoc. Prof. Dr. Nguyen Minh Ha, Dean of Post Graduate School, HCMC Open University, Vietnam.

For more information, please visit www.dnbvietnam.com, or contact our Customer Service Center at +848 3911 7288, or email [email protected].

Market Intelligence to Navigate Market RiskD&B’s Country Insight Solutions monitor changes in the business environment of individual countries and forecast country-wide developments which may affect the level of risk or provide opportunities in the short to medium term.

If your business trades overseas and needs up-to-date Credit, Political, Supply Chain risk, or Commercial insight, D&B’s country level solutions let you integrate our leading country data, predictive analysis and commercially relevant insight in your business processes to help you deliver a competitive advantage. Click here to see how you can benefit.

Your VisionYour Vision Our Insight

GROWING RELATIONSHIPS THROUGH DATA