business cycle of a fixed asset - william quam. santee cooper moncks corner, sc the state's...

TRANSCRIPT

Business Cycle of a Business Cycle of a Fixed AssetFixed Asset

-William Quam

Santee CooperSantee Cooper

Moncks Corner, SC

The state's leading resource for improving the quality of life for the people of South Carolina

Santee Cooper Headquarters, One Riverwood Dr.

About UsAbout Us

Total Revenue: $1.60 Billion

Customers:

Retail 162,657

Industrial 31

Wholesale (Co-op) 4

Plant in service: $6.4 Billion

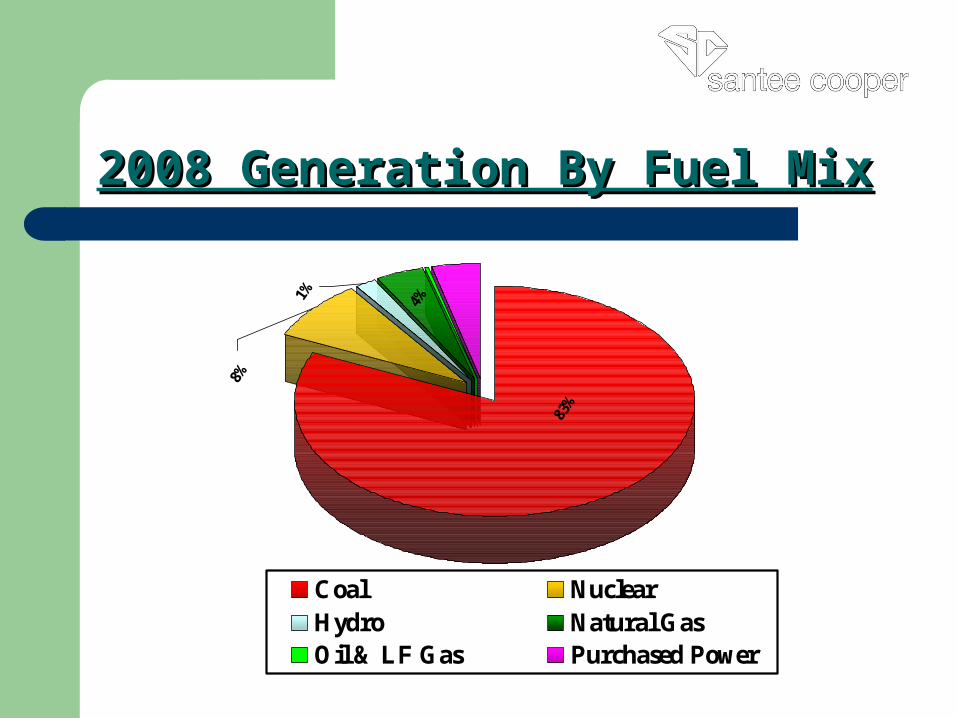

2008 Generation By Fuel Mix2008 Generation By Fuel Mix8%

1% 4%

83%

Coal NuclearHydro Natural GasOil & LF Gas Purchased Power

What is a Fixed Asset?What is a Fixed Asset?

Plant, Property, and Plant, Property, and

EquipmentEquipment

For use in operations and not For use in operations and not

for resalefor resale Long-term in nature and usually Long-term in nature and usually

subject to depreciationsubject to depreciation Possess physical substancePossess physical substance

Grainger Generating Station - Steam

Capitalization PolicyCapitalization Policy

Capitalization policy for capital assets: Guidelines to follow GAAP and Federal accounting regulations for electric utilities

provide a guide for the

future replacement

establish a basis for the amount

of insurance coverage required.

Capitalization PolicyCapitalization Policy

Suggestion #1 from Engineering

“At such time that your capital budget has been 100% spent, all future charges shall be classified as operations and maintenance expense”

Capitalization PolicyCapitalization Policy

Suggestion #2 from Engineering

“At such time that your operations and maintenance expense budget has been 100% spent, all future charges shall be classified as capital costs”

Capitalization PolicyCapitalization Policy

Engineering’s pet names for Accountants:

1) FERC Boy

2) Bean Counter

3) Horse’s Asset

4) Number Geek

5) That Simon Guy from American Idol

Capitalization PolicyCapitalization Policy

Retirement Unit: Term used to identify items of electric plant

The installation of a new addition or complete replacement of a retirement unit is always classified as a capital cost

Includes installed cost plus sales tax and overhead

Capitalization Policy (cont.)Capitalization Policy (cont.)

Minor Item: A component part of a retirement unit.

When a minor item is replaced independently with a like minor item, the cost is charged to maintenance regardless of $ value.

Different rules for addition of minor items which did not previously exist.

Capitalization Policy (cont.)Capitalization Policy (cont.)

Substantial Betterment: Addition of unlike minor items adds years of useful life and/or increased output / efficiency

Measurement: Installment cost of unlike minor items exceeds cost of like minor items by at least 35%

Retirement UnitsRetirement Units

Major

Examples:

Building – Warehouse

Conveyor System

Transformer

Minor

Examples:

Ceiling Fans

Individual Bucket

Replace & Rewind Inner Coil

Dress Pole PolicyDress Pole Policy

The first installation of a pole and components shall be charged to construction. The retirement unit will be pole and fixtures.

Any additions to pole, charge to O&M Replacement of pole, with or without components,

charge to capital Replacement of any components, charge to O&M

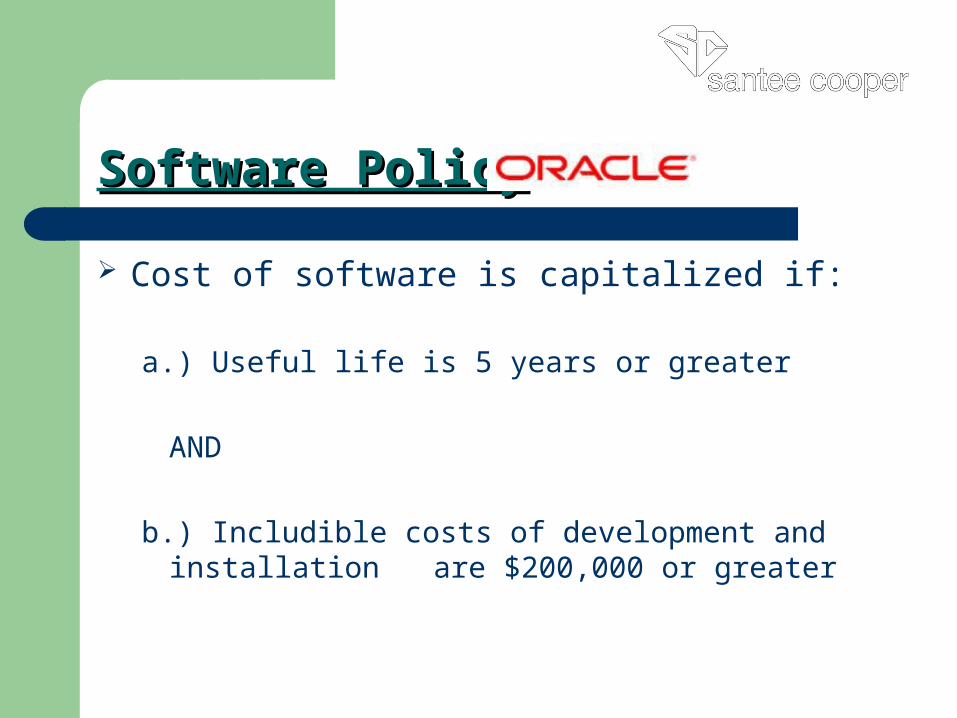

Software PolicySoftware Policy

Cost of software is capitalized if:

a.) Useful life is 5 years or greater

AND

b.) Includible costs of development and installation are $200,000 or greater

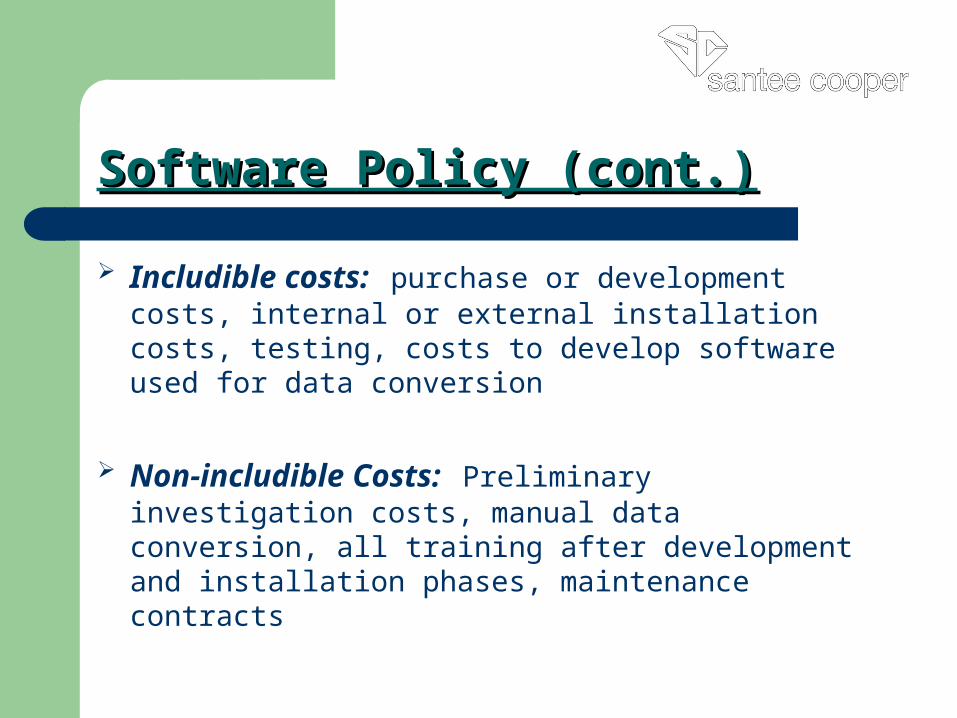

Software Policy (cont.)Software Policy (cont.)

Includible costs: purchase or development costs, internal or external installation costs, testing, costs to develop software used for data conversion

Non-includible Costs: Preliminary investigation costs, manual data conversion, all training after development and installation phases, maintenance contracts

Capital EquipmentCapital Equipment

Defined as a retirement unit costing $3,000 or

more (including sales tax)

and does not require labor

or travel to be operational

Ex: vehicle, copier, stuffed bear

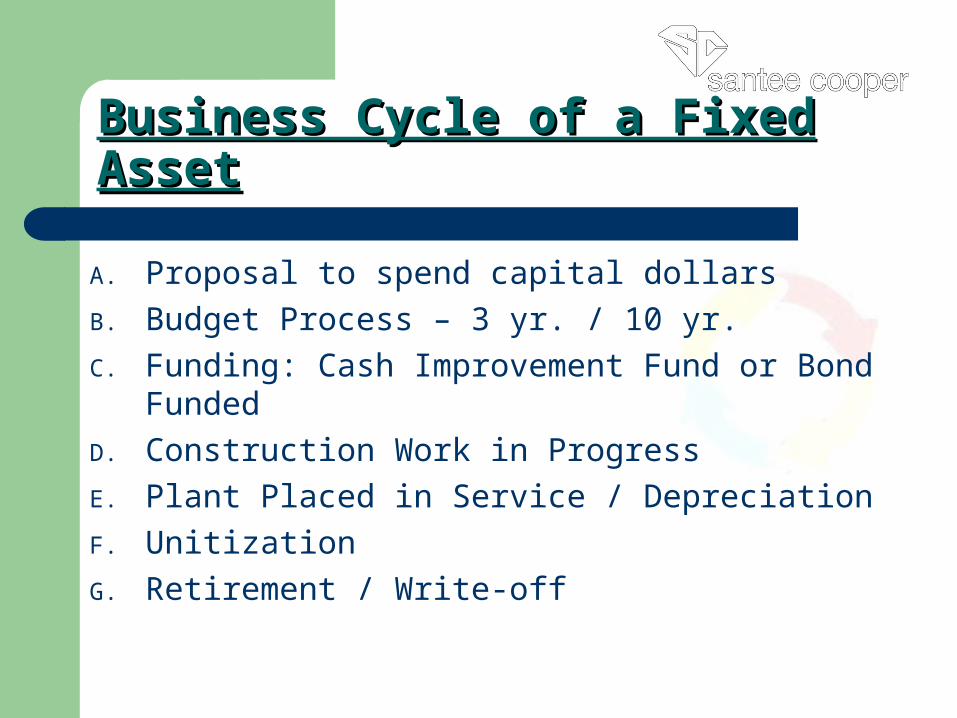

Business Cycle of a Fixed AssetBusiness Cycle of a Fixed Asset

A. Proposal to spend capital dollars

B. Budget Process – 3 yr. / 10 yr.

C. Funding: Cash Improvement Fund or Bond Funded

D. Construction Work in Progress

E. Plant Placed in Service / Depreciation

F. Unitization

G. Retirement / Write-off

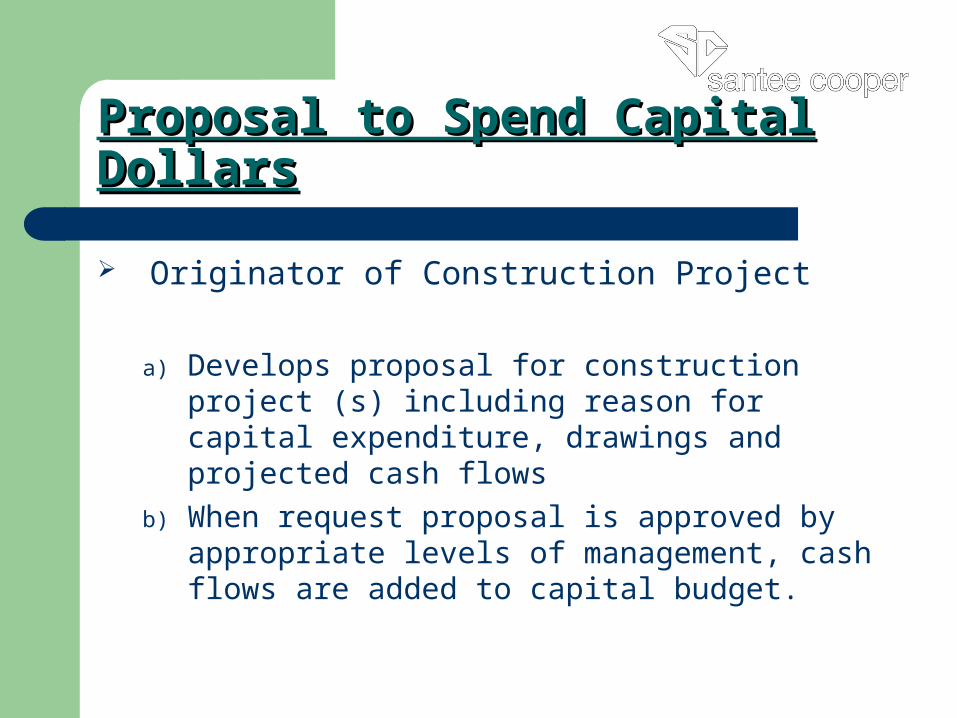

Proposal to Spend Capital DollarsProposal to Spend Capital Dollars

Originator of Construction Project

a) Develops proposal for construction project (s) including reason for capital expenditure, drawings and projected cash flows

b) When request proposal is approved by appropriate levels of management, cash flows are added to capital budget.

Budget ProcessBudget Process

3 year Budget Cycle

O&M and Capital Budget

Only spend Capital dollars

if your capital project is

approved as part of your capital budget

Board of Directors and Exec. Management approve budget

FundingFunding

A. O&M expenses paid by Revenue Fund

B. Capital replacements and improvements paid by Capital Improvement Fund. 8.5% added to every $1 of revenue

C. Large construction projects (generating stations) funded by revenue bonds

Budget VarianceBudget Variance

If Project Manager exceeds the approved capital budget item request amount

a) Director of Plant Accounting can place a hold on additionalcharges to construction projects in Oracle system

b) Executive Management approval needed to complete construction project that is over budget.

c) Board of Directors approval to increase budget is required on revenue bond funded projects

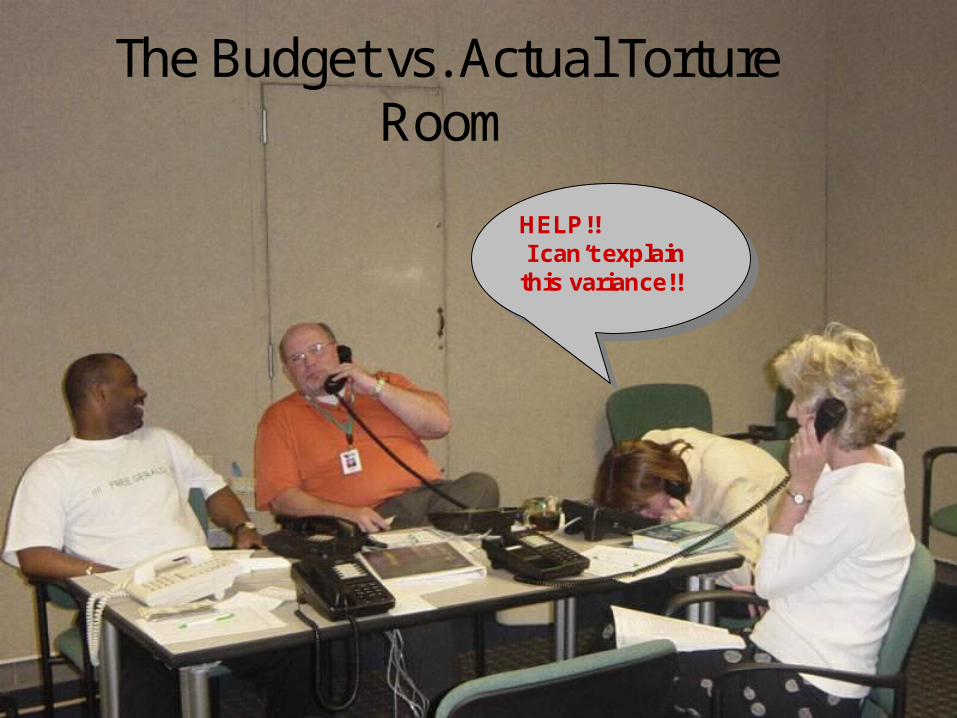

What happens to folks who don’t follow the Accounting Rules

The Budget vs. Actual Torture Room

HELP!!I can’t explain

this variance!!

HELP!!I can’t explain

this variance!!

Construction Work in ProgressConstruction Work in Progress

A. What costs should be included in Electric Plant and CWIP?

1) Code of Federal Regulations Subchapter C, Part 101 Electric Plant Instructions

Construction Work in ProgressConstruction Work in Progress

A. What costs should be included in Electric Plant and CWIP?

Overhead or Burden CostsShare of management and administrative expenses that indirectly benefit construction

Construction’s share of the cost of systems (Inventory, Purchasing) and employee benefits and leave.

Construction Work in ProgressConstruction Work in Progress

2. Overhead or Burden CostsAdded per $1 of labor

-General A&G-Leave Allocation-Fringe Benefits

Added per $1 of Inventory Stock charges-Materials overhead

Added per $1 of invoiced charges-Accounts Payable/Purchasing System

Construction Work in ProgressConstruction Work in Progress

A. What costs should be included in Electric Plant and CWIP?

– Contribution in Aid of Construction (CIAC)– Preliminary Studies – Deferred Debits

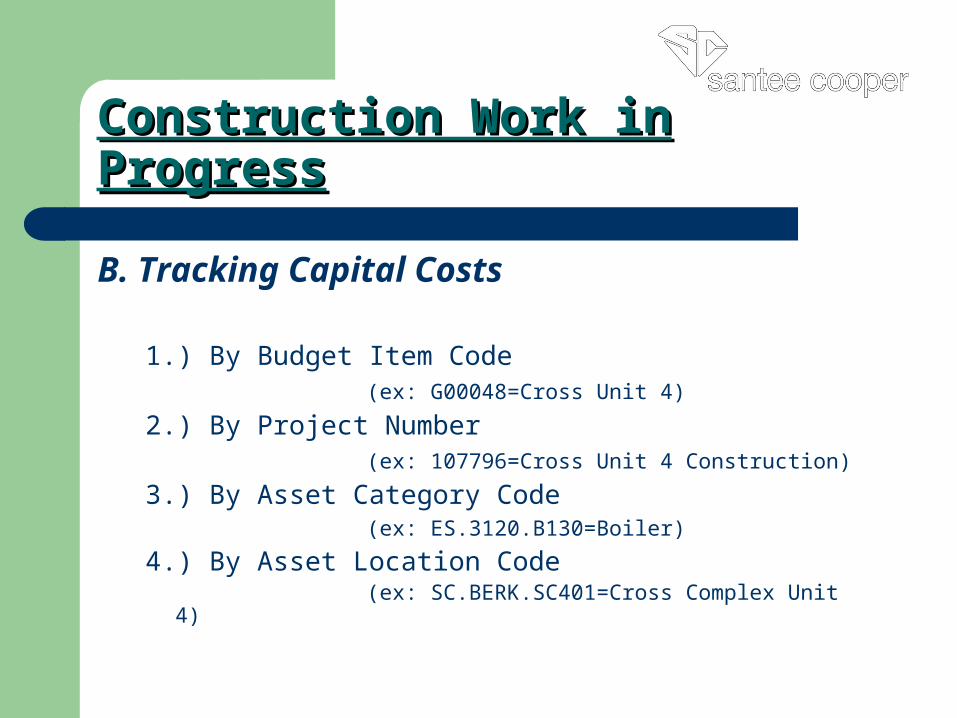

Construction Work in ProgressConstruction Work in Progress

B. Tracking Capital Costs

1.) By Budget Item Code(ex: G00048=Cross Unit 4)

2.) By Project Number(ex: 107796=Cross Unit 4 Construction)

3.) By Asset Category Code(ex: ES.3120.B130=Boiler)

4.) By Asset Location Code(ex: SC.BERK.SC401=Cross Complex Unit 4)

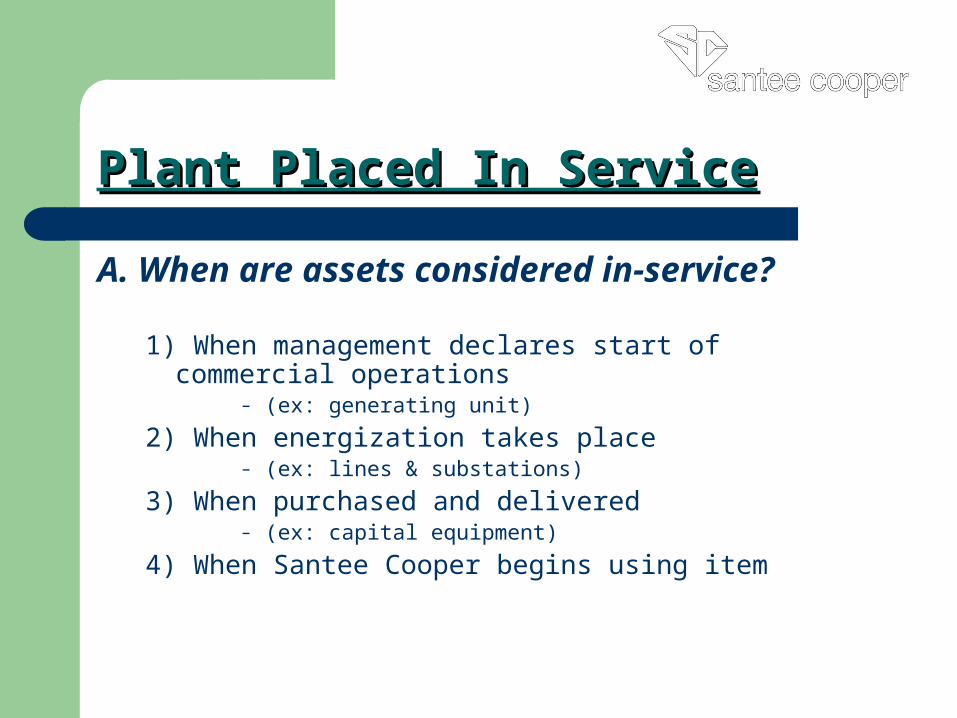

Plant Placed In ServicePlant Placed In Service

A. When are assets considered in-service?

1) When management declares start of commercial operations

– (ex: generating unit)

2) When energization takes place– (ex: lines & substations)

3) When purchased and delivered– (ex: capital equipment)

4) When Santee Cooper begins using item

Plant Placed In-ServicePlant Placed In-Service

B. Accounting Treatment

1) In the month that asset is placed in service:

Asset cost transferred from CWIP-1070 to Utility Plant in service-1060

Depreciation of asset begins

Plant Placed In-ServicePlant Placed In-Service

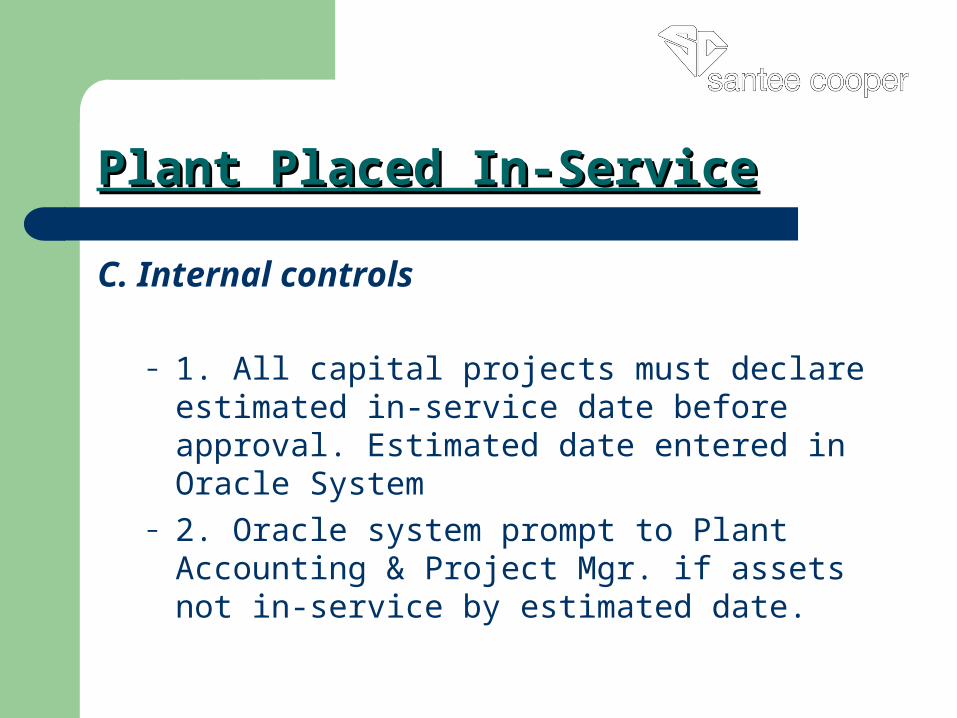

C. Internal controls

– 1. All capital projects must declare estimated in-service date before approval. Estimated date entered in Oracle System

– 2. Oracle system prompt to Plant Accounting & Project Mgr. if assets not in-service by estimated date.

DepreciationDepreciation

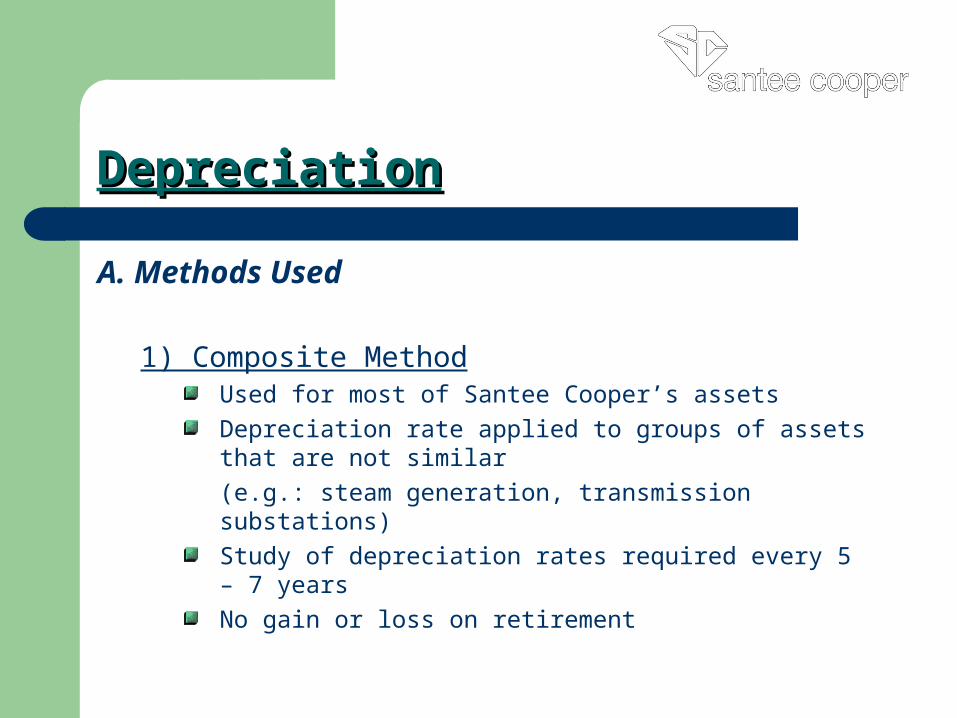

A. Methods Used

1) Composite MethodUsed for most of Santee Cooper’s assets

Depreciation rate applied to groups of assets that are not similar

(e.g.: steam generation, transmission substations)

Study of depreciation rates required every 5 – 7 years

No gain or loss on retirement

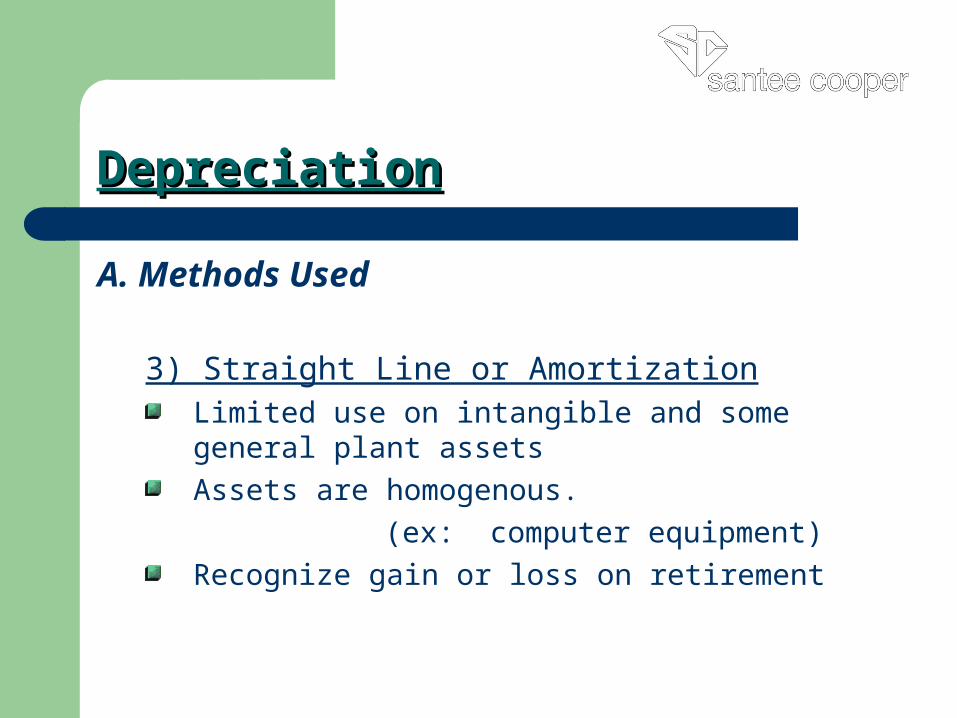

DepreciationDepreciation

A. Methods Used

2) Composite RatesOne depreciation rate for each production category

(ex: steam, hydro, nuclear, other power)

Individual depreciation rate for each FERC regulatory acct.

(Transmission, distribution, generation plant)

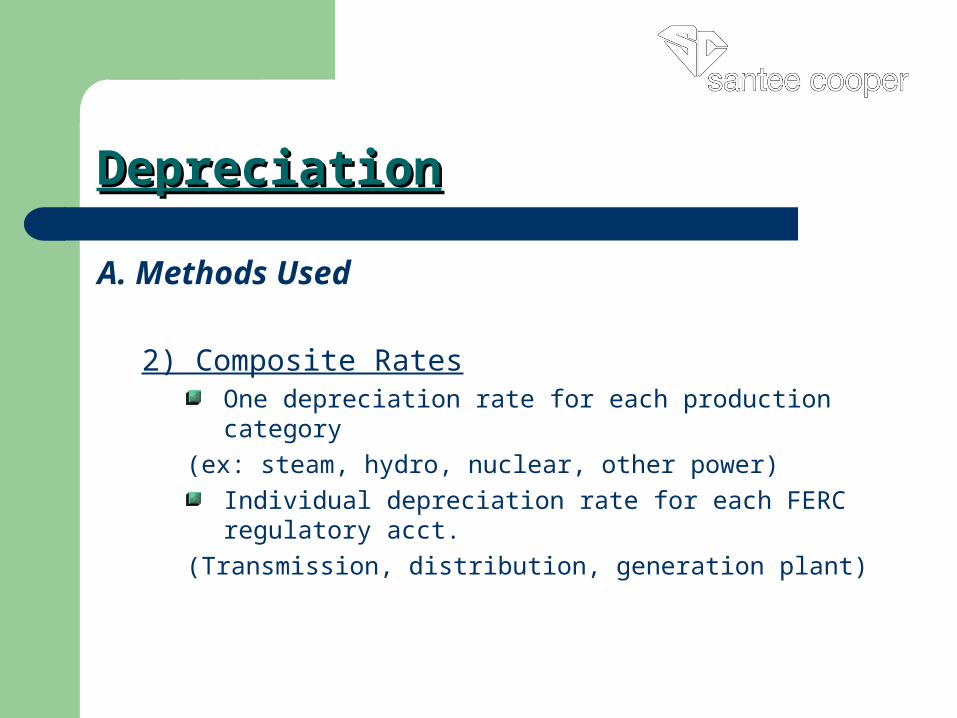

DepreciationDepreciation

A. Methods Used

3) Straight Line or AmortizationLimited use on intangible and some general plant assets

Assets are homogenous.

(ex: computer equipment)

Recognize gain or loss on retirement

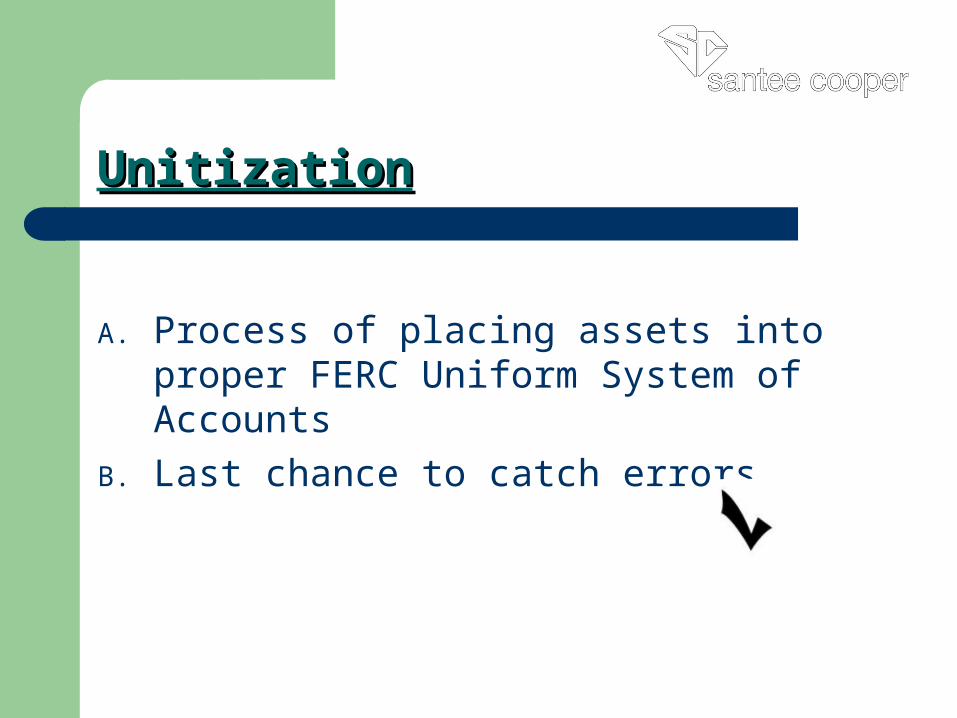

UnitizationUnitization

A. Process of placing assets into proper FERC Uniform System of Accounts

B. Last chance to catch errors

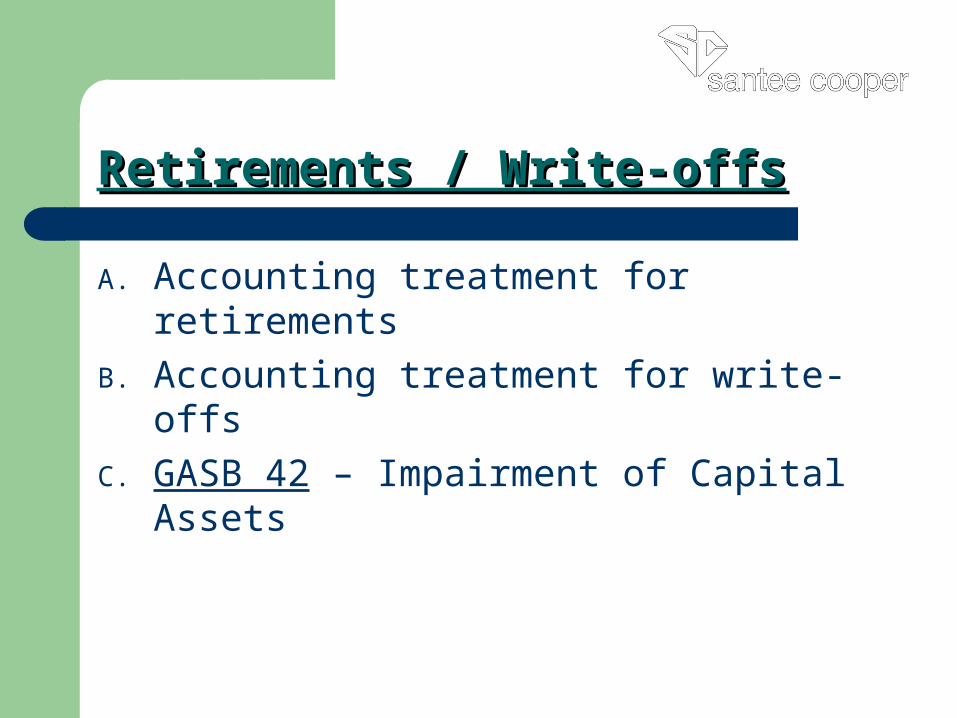

Retirements / Write-offsRetirements / Write-offs

A. Accounting treatment for retirements

B. Accounting treatment for write-offs

C. GASB 42 – Impairment of Capital Assets