business accounts tutor pack - osbornebooks.co.uk · osborne books is grateful to roger petheram...

TRANSCRIPT

Business Accounts Tutor Packanswers to chapter questions

The answers shown here are to the questions which are not answered at the back of the main text.

chapter chapter answersnumber page

1 12 13 34 55 76 87 108 109 1110 1411 1512 1513 1714 1915 2016 2217 2318 2419 2520 2721 2822 3023 3224 3425 3526 3627 3828 40

29 - 32 41

© Osborne Books Limited 2012

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmittedin any form or by any means, electronic, mechanical, photo-copying, recording or otherwise, without the priorconsent of the publishers, or in accordance with the provisions of the Copyright, Designs and Patents Act 1988,or under the terms of any licence permitting limited copying issued by the Copyright Licensing Agency, 90Tottenham Court Road, London W1P 9HE.

Osborne Books is grateful to Roger Petheram for checking the answers. All answers are the responsibility of the publisher.

Published by Osborne Books Limited Tel 01905 748071Email [email protected]

1.2 • documentsprocessing of prime documents relating to financial transactions

• initial recording of transactionsrecording financial transactions in primary accounting records, or books of prime entry

• double-entry accounts systemtransfer from primary accounting records into the double-entry book-keeping system of accounts inthe ledger

• trial balanceextraction of figures from all the double-entry accounts to check their accuracy

• final accountsproduction of a profit and loss account and a balance sheet

Information from the accounting system includes:• purchases to date• sales to date• expenses to date• debtors – total amount owed to the business, and individual debtors• creditors – total amount owed by the business, and individual creditors• assets owned• liabilities owed• profit during a particular period

1.3 • financial accountant– preparation of final accounts– negotiation with Inland Revenue on taxation matters– for a limited company, preparation of final accounts which comply with the Companies Act 1985

• cost and management accountant– obtains information about recent costs of the business, and costs of products/services– estimates costs for the future, and prepares budgets– prepares reports and makes recommendations to the owner(s)/managers

• auditors – externalstatutory audit addressed to the shareholders of a limited company certifying that the accounts showa 'true and fair view' of the business and comply with the legal requirements of the Companies Act1985

• auditors – internalinternal checking and control procedures of the business in which they are employed

In addition, there are likely to be advertisements for book-keepers to carry out various aspects of businessaccounting.

1.4 (a) Business entity – the accounts record and report on the financial transactions of a particularbusiness, and not the owner's personal financial transactions.

(b) Money measurement – the accounting system uses money as the common denominator in recordingand reporting all business transactions; thus the loyalty of a firm's workforce or the quality of a productcannot be recorded because these cannot be reported in money terms.

1.5 • assets – items owned by a business; liabilities – items owed by a business• debtors – individuals or businesses who owe money in respect of goods or services supplied by the

business; creditors – individuals or businesses to whom money is owed by the business• purchases – goods bought, either on credit or for cash, which are intended to be resold later; sales –

the sale of goods, whether on credit or for cash, in which the business trades• credit purchases – goods bought, with payment to be made at a later date; cash purchases – goods

bought and paid for immediately

1.6 • asset of bank increases by £8,000capital increases by £8,000asset £8,000 – liability £0 = capital £8,000

• asset of computer increases by £4,000asset of bank decreases by £4,000asset £8,000 – liability £0 = capital £8,000

• asset of bank increases by £3,000liability of loan increases by £3,000asset £11,000 – liability £3,000 = capital £8,000

• asset of van increases by £6,000asset of bank decreases by £6,000asset £11,000 – liability £3,000 = capital £8,000

2.1 Dr Capital Account Cr20-1 £ 20-1 £

1 Feb Bank 7,500

Dr Computer Account Cr20-1 £ 20-1 £6 Feb Bank 2,000

Dr Rent Paid Account Cr20-1 £ 20-1 £8 Feb Bank 750

Dr Wages Account Cr20-1 £ 20-1 £12 Feb Bank 42525 Feb Bank 380

Dr Bank Loan Account Cr20-1 £ 20-1 £

14 Feb Bank 2,500

Dr Commission Received Account Cr20-1 £ 20-1 £

20 Feb Bank 145

Dr Drawings Account Cr20-1 £ 20-1 £23 Feb Bank 200

1

CHAPTER 1 What are Business Accounts?

CHAPTER 2 Double-entry Book-keeping: First Principles

Dr Van Account Cr20-1 £ 20-1 £28 Feb Bank 6,000

2.3 Dr Bank Account Cr20-5 £ 20-5 £1 Aug Capital 5,000 3 Aug Computer 1,80015 Aug S Orton: loan 1,000 7 Aug Rent paid 10020 Aug Office fittings 250 12 Aug Office fittings 2,00025 Aug Commission received 150 27 Aug S Orton: loan 150

Dr Capital Account Cr20-5 £ 20-5 £

1 Aug Bank 5,000

Dr Computer Account Cr20-5 £ 20-5 £3 Aug Bank 1,800

Dr Rent Paid Account Cr20-5 £ 20-5 £7 Aug Bank 100

Dr Commission Received Account Cr20-5 £ 20-5 £

10 Aug Cash 20025 Aug Bank 150

Dr Cash Account Cr20-5 £ 20-5 £10 Aug Commission received 200 17 Aug Drawings 100

Dr Office Fittings Account Cr20-5 £ 20-5 £12 Aug Bank 2,000 20 Aug Bank 250

Dr Sally Orton: Loan Account Cr20-5 £ 20-5 £27 Aug Bank 150 15 Aug Bank 1,000

Dr Drawings Account Cr20-5 £ 20-5 £17 Aug Cash 100

2.5 Dr Bank Account Cr20-7 £ 20-7 £1 Nov Capital 75,000 3 Nov Photocopier 2,5007 Nov Bank loan 70,000 10 Nov Office premises 130,00023 Nov Cash 100 12 Nov Business rates 3,00025 Nov Office fittings 200 14 Nov Office fittings 1,50028 Nov Commission received 200 20 Nov Wages 250

Dr Capital Account Cr20-7 £ 20-7 £

1 Nov Bank 75,000

Dr Photocopier Account Cr20-7 £ 20-7 £3 Nov Bank 2,500

Dr Bank Loan Account Cr20-7 £ 20-7 £

7 Nov Bank 70,000

Dr Office Premises Account Cr20-7 £ 20-7 £10 Nov Bank 130,000

Dr Rates Account Cr20-7 £ 20-7 £12 Nov Bank 3,000

Dr Office Fittings Account Cr20-7 £ 20-7 £14 Nov Bank 1,500 25 Nov Bank 200

Dr Cash Account Cr20-7 £ 20-7 £15 Nov Commission received 300 18 Nov Drawings 125

23 Nov Bank 100

Dr Commission Received Account Cr20-7 £ 20-7 £

15 Nov Cash 30028 Nov Bank 200

Dr Drawings Account Cr20-7 £ 20-7 £18 Nov Cash 125

Dr Wages Account Cr20-7 £ 20-7 £20 Nov Bank 250

2

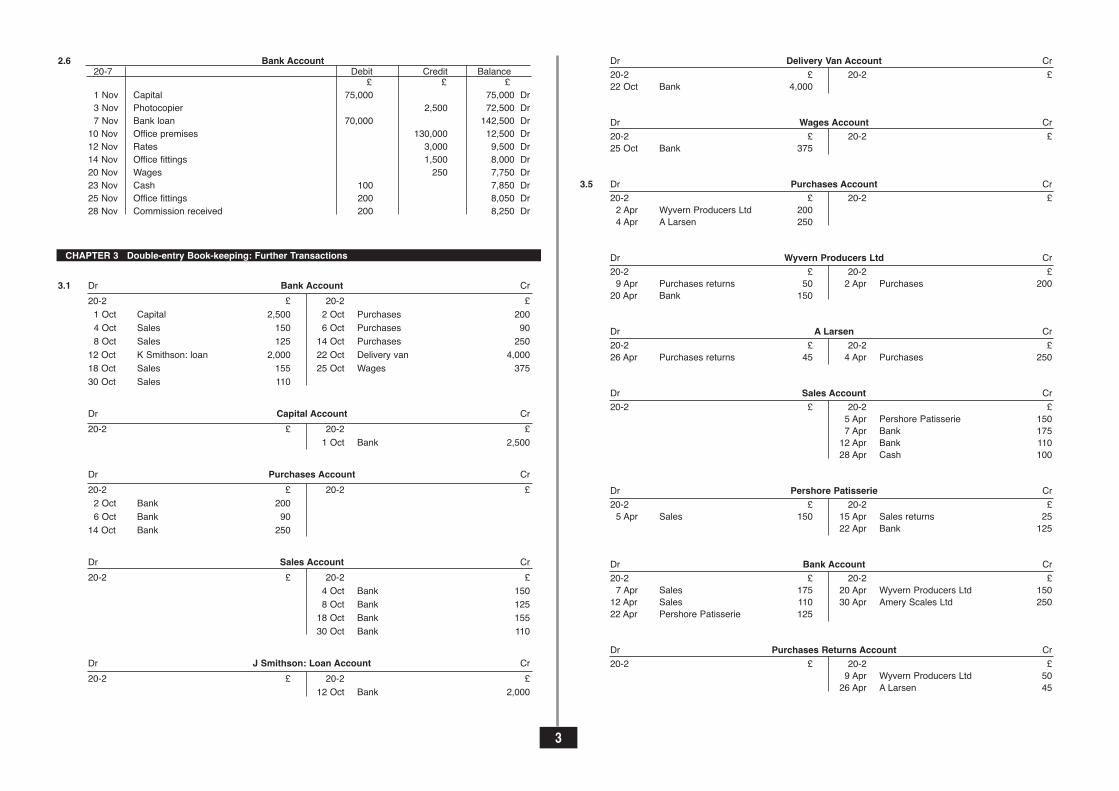

2.6 Bank Account 20-7 Debit Credit Balance

£ £ £ 1 Nov Capital 75,000 75,000 Dr3 Nov Photocopier 2,500 72,500 Dr7 Nov Bank loan 70,000 142,500 Dr10 Nov Office premises 130,000 12,500 Dr12 Nov Rates 3,000 9,500 Dr14 Nov Office fittings 1,500 8,000 Dr20 Nov Wages 250 7,750 Dr23 Nov Cash 100 7,850 Dr25 Nov Office fittings 200 8,050 Dr28 Nov Commission received 200 8,250 Dr

3.1 Dr Bank Account Cr20-2 £ 20-2 £1 Oct Capital 2,500 2 Oct Purchases 2004 Oct Sales 150 6 Oct Purchases 908 Oct Sales 125 14 Oct Purchases 25012 Oct K Smithson: loan 2,000 22 Oct Delivery van 4,00018 Oct Sales 155 25 Oct Wages 37530 Oct Sales 110

Dr Capital Account Cr20-2 £ 20-2 £

1 Oct Bank 2,500

Dr Purchases Account Cr20-2 £ 20-2 £2 Oct Bank 2006 Oct Bank 9014 Oct Bank 250

Dr Sales Account Cr20-2 £ 20-2 £

4 Oct Bank 1508 Oct Bank 12518 Oct Bank 15530 Oct Bank 110

Dr J Smithson: Loan Account Cr20-2 £ 20-2 £

12 Oct Bank 2,000

Dr Delivery Van Account Cr20-2 £ 20-2 £22 Oct Bank 4,000

Dr Wages Account Cr20-2 £ 20-2 £25 Oct Bank 375

3.5 Dr Purchases Account Cr20-2 £ 20-2 £2 Apr Wyvern Producers Ltd 2004 Apr A Larsen 250

Dr Wyvern Producers Ltd Cr20-2 £ 20-2 £9 Apr Purchases returns 50 2 Apr Purchases 20020 Apr Bank 150

Dr A Larsen Cr20-2 £ 20-2 £26 Apr Purchases returns 45 4 Apr Purchases 250

Dr Sales Account Cr20-2 £ 20-2 £

5 Apr Pershore Patisserie 1507 Apr Bank 17512 Apr Bank 11028 Apr Cash 100

Dr Pershore Patisserie Cr20-2 £ 20-2 £5 Apr Sales 150 15 Apr Sales returns 25

22 Apr Bank 125

Dr Bank Account Cr20-2 £ 20-2 £7 Apr Sales 175 20 Apr Wyvern Producers Ltd 15012 Apr Sales 110 30 Apr Amery Scales Ltd 25022 Apr Pershore Patisserie 125

Dr Purchases Returns Account Cr20-2 £ 20-2 £

9 Apr Wyvern Producers Ltd 5026 Apr A Larsen 45

3

CHAPTER 3 Double-entry Book-keeping: Further Transactions

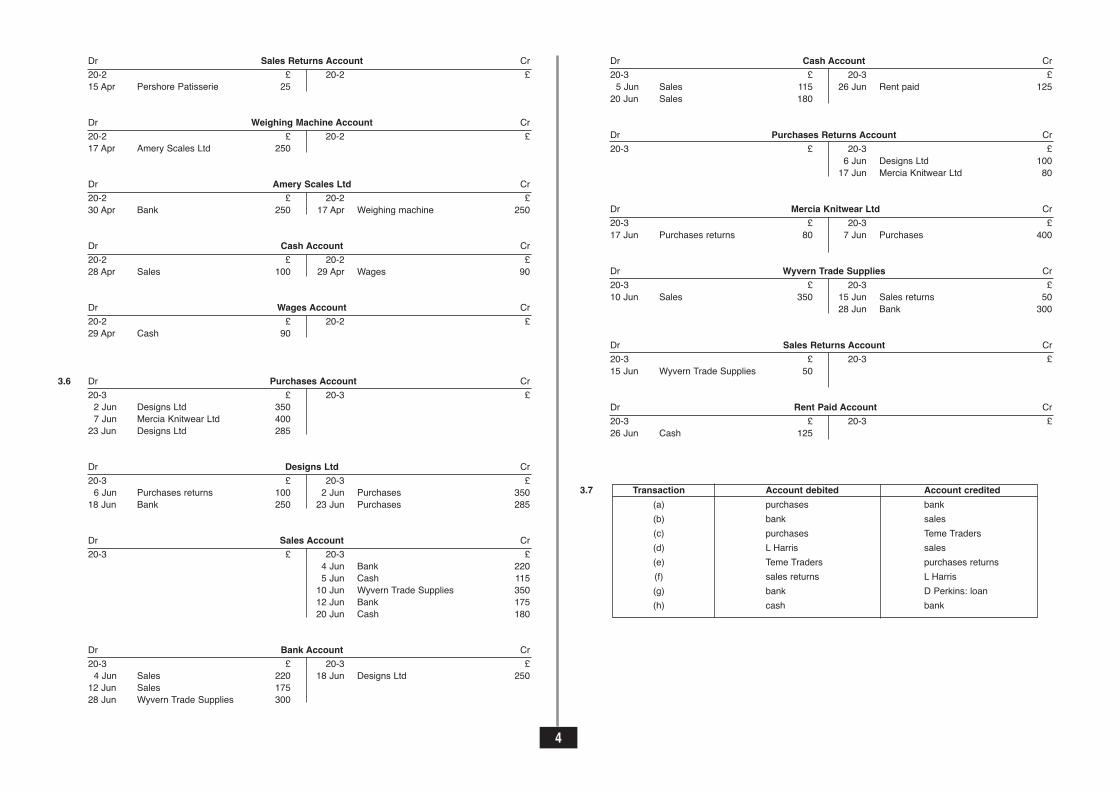

Dr Sales Returns Account Cr20-2 £ 20-2 £15 Apr Pershore Patisserie 25

Dr Weighing Machine Account Cr20-2 £ 20-2 £17 Apr Amery Scales Ltd 250

Dr Amery Scales Ltd Cr20-2 £ 20-2 £30 Apr Bank 250 17 Apr Weighing machine 250

Dr Cash Account Cr20-2 £ 20-2 £28 Apr Sales 100 29 Apr Wages 90

Dr Wages Account Cr20-2 £ 20-2 £29 Apr Cash 90

3.6 Dr Purchases Account Cr20-3 £ 20-3 £2 Jun Designs Ltd 3507 Jun Mercia Knitwear Ltd 40023 Jun Designs Ltd 285

Dr Designs Ltd Cr20-3 £ 20-3 £6 Jun Purchases returns 100 2 Jun Purchases 35018 Jun Bank 250 23 Jun Purchases 285

Dr Sales Account Cr20-3 £ 20-3 £

4 Jun Bank 2205 Jun Cash 11510 Jun Wyvern Trade Supplies 35012 Jun Bank 17520 Jun Cash 180

Dr Bank Account Cr20-3 £ 20-3 £4 Jun Sales 220 18 Jun Designs Ltd 25012 Jun Sales 17528 Jun Wyvern Trade Supplies 300

Dr Cash Account Cr20-3 £ 20-3 £5 Jun Sales 115 26 Jun Rent paid 12520 Jun Sales 180

Dr Purchases Returns Account Cr20-3 £ 20-3 £

6 Jun Designs Ltd 10017 Jun Mercia Knitwear Ltd 80

Dr Mercia Knitwear Ltd Cr20-3 £ 20-3 £17 Jun Purchases returns 80 7 Jun Purchases 400

Dr Wyvern Trade Supplies Cr20-3 £ 20-3 £10 Jun Sales 350 15 Jun Sales returns 50

28 Jun Bank 300

Dr Sales Returns Account Cr20-3 £ 20-3 £15 Jun Wyvern Trade Supplies 50

Dr Rent Paid Account Cr20-3 £ 20-3 £26 Jun Cash 125

3.7 Transaction Account debited Account credited(a) purchases bank(b) bank sales(c) purchases Teme Traders(d) L Harris sales(e) Teme Traders purchases returns(f) sales returns L Harris(g) bank D Perkins: loan(h) cash bank

4

4.3

* £492.50 x 97.5% x 20% = £96.03 VATNote: Students can complete details for telephone, fax, VAT registration number and order number

4.4

* £190.00 x 97.5% x 20% = £37.05 VATNote: Students can complete details for telephone, fax, VAT registration number and order number

5

invoice to

deliver to

invoice no 2451account your reference

date/tax point todayas above

quantity description price unit total discount net %

5 Dresses 30.00 each 150.00 0.00 150.00 3 Suits 45.50 each 136.50 0.00 136.50 4 Coats 51.50 each 206.00 0.00 206.00

terms2.5% cash discount for full settlementwithin 14 daysNet 30 daysCarriage paidE & OE

Excel Fashions49 Highland StreetLongtonMercia LT3 2XL

INVOICE

JANE SMITH, FASHION WHOLESALERUnit 21, Eastern Industrial Estate, Wyvern, Wyvernshire, WY1 3XJ

Tel 01927 354172 Fax 01927 354173VAT REG GB 0745 4731 41

GOODS TOTAL 492.50

VAT 96.03*

TOTAL 588.53

invoice to

deliver to

invoice no 8234account your reference

date/tax point todayas above

quantity description price unit total discount net %

5 Assorted rubbers 5.00 box 25.00 0.00 25.00 100 Shorthand notebooks 4.00 10 40.00 0.00 40.00 250 Ring Binders 0.50 each 125.00 0.00 125.00

terms2.5% cash discount for full settlementwithin 14 daysNet 30 daysCarriage paidE & OE

The Card Shop126 The CornbowTeamington SpaWyvernshire WY33 0EG

INVOICE

DEANSWAY TRADING COMPANYThe Model Office, Deansway, Rowcester, RW1 2EJ

Tel 01908 765314 Fax 01908 765951VAT REG GB 0745 4672 76

GOODS TOTAL 190.00

VAT 37.05*

TOTAL 227.05

CHAPTER 4 Business Documents

4.5

4.6 Dr Purchases Account Cr20-4 £ 20-4 £2 Feb G Lewis 20016 Feb G Lewis 160

Dr Sales Account Cr20-4 £ 20-4 £

4 Feb L Jarvis 1507 Feb G Patel 240

Dr G Lewis Cr20-4 £ 20-4 £10 Feb Bank 190 2 Feb Purchases 20010 Feb Discount received 10 16 Feb Purchases 16024 Feb Bank 15224 Feb Discount received 8

360 360

Dr L Jarvis Cr20-4 £ 20-4 £4 Feb Sales 150 12 Feb Bank 147

12 Feb Discount allowed 3150 150

Dr G Patel Cr20-4 £ 20-4 £7 Feb Sales 240 20 Feb Bank 234

20 Feb Discount allowed 6240 240

Dr Bank Account Cr20-4 £ 20-4 £12 Feb L Jarvis 147 10 Feb G Lewis 19020 Feb G Patel 234 24 Feb G Lewis 152

Dr Discount Received Account Cr20-4 £ 20-4 £

10 Feb G Lewis 1024 Feb G Lewis 8

Dr Discount Allowed Account Cr20-4 £ 20-4 £12 Feb L Jarvis 320 Feb G Patel 6

6

STATEMENT OF ACCOUNT

account 3993

date 31 March 20--

TOJ Wilson

AMOUNT NOW DUE 340.00

date no. details debit credit balance £ £ £ 20-- 1 Mar Balance b/d 145.00 Dr 3 Mar 8119 Invoice 210.00 355.00 Dr10 Mar Cheque 145.00 210.00 Dr23 Mar CN345 Credit Note 50.00 160.00 Dr28 Mar 8245 Invoice 180.00 340.00 Dr

5.1 (a) and (c)

Dr Bank Account Cr20-9 £ 20-9 £1 Jan Capital 10,000 4 Jan Rent paid 50011 Jan Sales 1,000 5 Jan Shop fittings 1,50012 Jan Sales 1,250 20 Jan Comp Supplies Ltd 5,00022 Jan Sales 1,450 31 Jan Balance c/d 6,700

13,700 13,7001 Feb Balance b/d 6,700 2 Feb Rent paid 5004 Feb Sales 1,550 15 Feb Shop fittings 85010 Feb Sales 1,300 27 Feb Comp Supplies Ltd 6,35012 Feb Rowcester College 750 28 Feb Balance c/d 5,30019 Feb Sales 1,60025 Feb Sales 1,100

13,000 13,0001 Mar Balance b/d 5,300

Dr Capital Account Cr20-9 £ 20-9 £

1 Jan Bank 10,000

Dr Rent Paid Account Cr20-9 £ 20-9 £4 Jan Bank 500 28 Feb Balance c/d 1,0002 Feb Bank 500

1,000 1,0001 Mar Balance b/d 1,000

Dr Shop Fittings Account Cr20-9 £ 20-9 £5 Jan Bank 1,500 28 Feb Balance c/d 2,35015 Feb Bank 850

2,350 2,3501 Mar Balance b/d 2,350

Dr Purchases Account Cr 20-9 £ 20-9 £7 Jan Comp Supplies Ltd 5,000 31 Jan Balance c/d 11,50025 Jan Comp Supplies Ltd 6,500

11,500 11,500

1 Feb Balance b/d 11,500 28 Feb Balance c/d 17,00024 Feb Comp Supplies Ltd 5,500

17,000 17,0001 Mar Balance b/d 17,000

Dr Comp Supplies Limited Cr20-9 £ 20-9 £20 Jan Bank 5,000 7 Jan Purchases 5,00031 Jan Balance c/d 6,500 25 Jan Purchases 6,500

11,500 11,5005 Feb Purchases returns 150 1 Feb Balance b/d 6,50027 Feb Bank 6,350 24 Feb Purchases 5,50028 Feb Balance c/d 5,500

12,000 12,0001 Mar Balance b/d 5,500

Dr Sales Account Cr20-9 £ 20-9 £31 Jan Balance c/d 4,550 11 Jan Bank 1,000

12 Jan Bank 1,25016 Jan Rowcester College 85022 Jan Bank 1,450

4,550 4,55028 Feb Balance c/d 11,150 1 Feb Balance b/d 4,550

4 Feb Bank 1,55010 Feb Bank 1,30019 Feb Bank 1,60025 Feb Bank 1,10026 Feb Rowcester College 1,050

11,150 11,1501 Mar Balance b/d 11,150

Dr Rowcester College Cr20-9 £ 20-9 £16 Jan Sales 850 27 Jan Sales returns 100

31 Jan Balance c/d 750850 850

1 Feb Balance b/d 750 12 Feb Bank 75026 Feb Sales 1,050 28 Feb Balance c/d 1,050

1,800 1,8001 Mar Balance b/d 1,050

Dr Sales Returns Account Cr20-9 £ 20-9 £27 Jan Rowcester College 100

Dr Purchases Returns Account Cr20-9 £ 20-9 £

5 Feb Comp Supplies Ltd 150

7

CHAPTER 5 Balancing Accounts – the Trial Balance

(b) Trial balance as at 31 January 20-9Dr Cr

Name of Account £ £Bank 6,700Capital 10,000Rent paid 500Shop fittings 1,500Purchases 11,500Comp Supplies Limited 6,500Sales 4,550Rowcester College 750Sales returns 100

21,050 21,050

(d) Trial balance as at 28 February 20-9Dr Cr

Name of Account £ £Bank 5,300Capital 10,000Rent paid 1,000Shop fittings 2,350Purchases 17,000Comp Supplies Limited 5,500Sales 11,150Rowcester College 1,050Sales returns 100Purchases returns 150

26,800 26,800

5.2 Trial balance of Jane Greenwell as at 28 February 20-1Dr Cr£ £

Name of accountBank 1,250Purchases 850Cash 48Sales 730Purchases returns 144Creditors 1,442Equipment 2,704Van 3,200Sales returns 90Debtors 1,174Wages 1,500Capital (missing figure) 6,000

9,566 9,566

5.5 Four from:• Error of omission

Business transaction completely omitted from the accounting records. For example, cash sale omittedfrom both cash account and sales account.

• Reversal of entriesDebit and credit entries on the wrong side of the two accounts concerned. For example, cash saleentered wrongly as debit sales account, credit cash account.

• Mispost/error of commissionTransaction entered to the wrong person's account. For example, a sale of goods on credit to A THughes has been entered as debit A J Hughes' account, credit sales account.

• Error of principleTransaction entered in the wrong type of account. For example, cost of petrol for vehicles has beenentered as debit motor vehicles account, credit bank account.

• Error of original entry (or transcription)Amount entered incorrectly in both accounts. For example, sale of £45 entered in both sales accountand the debtor's account as £54.

• Compensating errorTwo errors cancel each other out. For example, balance of purchases account calculated wrongly at£10 too much, compensated by the same error in sales account.

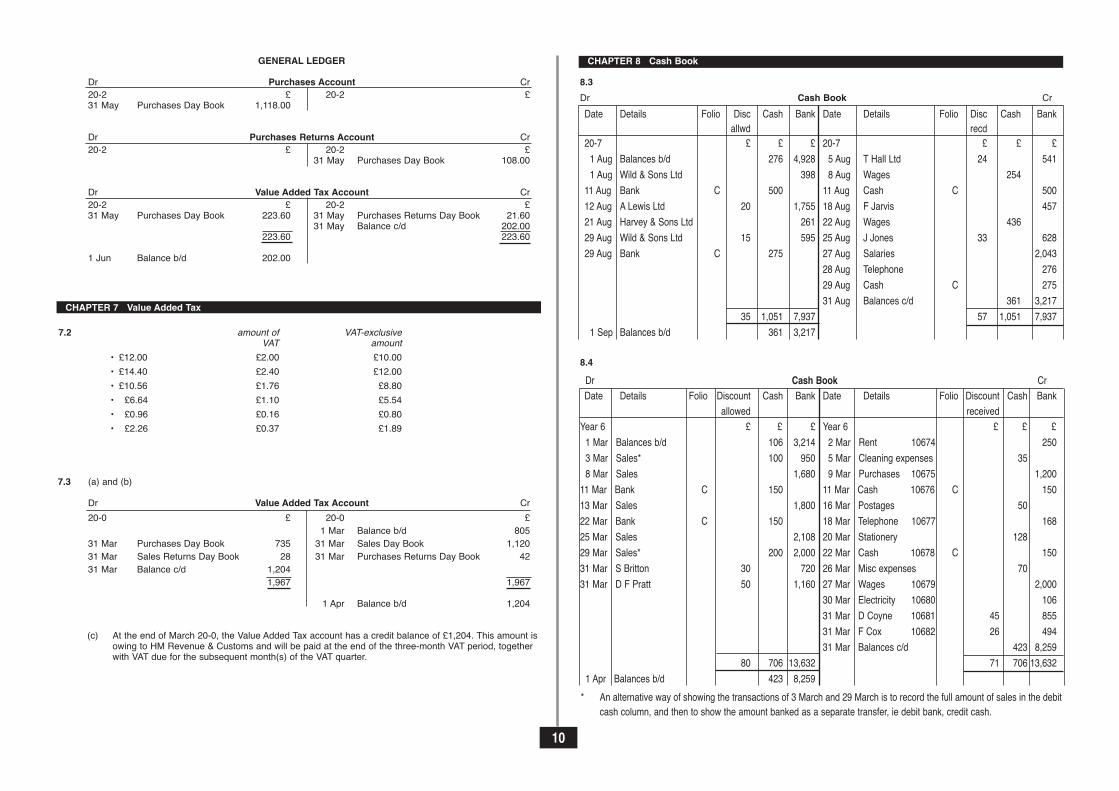

6.2 Purchases Day Book

Date Details Invoice Folio Net VAT Gross 20-2 £ £ £1 Feb Softseat Ltd 961 320 64 3842 Feb PRK Ltd 068 80 16 9615 Feb Quality Furnishings 529 160 32 19219 Feb Softseat Ltd 984 160 32 192

28 Feb Totals for month 720 144 864

Sales Day Book

Date Details Invoice Folio Net VAT Gross 20-2 £ £ £8 Feb High Street Stores 001 440 88 52814 Feb Peter Lounds Ltd 002 120 24 14418 Feb Carpminster College 003 320 64 38425 Feb High Street Stores 004 200 40 240

28 Feb Totals for month 1,080 216 1,296

8

CHAPTER 6 Division of the Ledger – Primary Accounting Records

PURCHASES LEDGER

Dr Softseat Ltd Cr20-2 £ 20-2 £28 Feb Balance c/d 576 1 Feb Purchases 384

19 Feb Purchases 192576 576

1 Mar Balance b/d 576

Dr PRK Ltd Cr20-2 £ 20-2 £

2 Feb Purchases 96

Dr Quality Furnishings Cr20-2 £ 20-2 £

15 Feb Purchases 192

SALES LEDGER

Dr High Street Stores Cr20-2 £ 20-2 £8 Feb Sales 528 28 Feb Balance c/d 76825 Feb Sales 240

768 768

1 Mar Balance b/d 768

Dr Peter Lounds Ltd Cr20-2 £ 20-2 £14 Feb Sales 144

Dr Carpminster College Cr20-2 £ 20-2 £18 Feb Sales 384

GENERAL LEDGER

Dr Purchases Account Cr20-2 £ 20-2 £28 Feb Purchases Day Book 720

Dr Sales Account Cr20-2 £ 20-2 £

28 Feb Sales Day Book 1,080

Dr Value Added Tax Account Cr20-2 £ 20-2 £28 Feb Purchases Day Book 144 28 Feb Sales Day Book 21628 Feb Balance c/d 72

216 216

1 Mar Balance b /d 72

6.3 Purchases Day Book

Date Details Invoice Folio Net VAT Gross 20-2 £ £ £2 May M Roper & Sons 562 PL 302 190.00 38.00 228.004 May Wyper Ltd 82 PL 301 200.00 40.00 240.0010 May Wyper Ltd 86 PL 301 210.00 42.00 252.0018 May M Roper & Sons 580 PL 302 180.00 36.00 216.0021 May Wyper Ltd 91 PL 301 240.00 48.00 288.0025 May M Roper & Sons 589 PL 302 98.00 19.60 117.60

31 May Totals for month 1,118.00 223.60 1,341.60

Purchases Returns Day Book

Date Details Credit Folio Net VAT Gross Note

20-2 £ £ £18 May M Roper & Sons 82 PL 302 30.00 6.00 36.0023 May Wyper Ltd 6 PL 301 40.00 8.00 48.0028 May M Roper & Sons 84 PL 302 38.00 7.60 45.60

31 May Totals for month 108.00 21.60 129.60

PURCHASES LEDGER

Dr Wyper Ltd (account no 301) Cr20-2 £ 20-2 £23 May Purchases Returns 48.00 1 May Balance b/d 100.0031 May Balance c/d 832.00 4 May Purchases 240.00

10 May Purchases 252.0021 May Purchases 288.00

880.00 880.00

1 Jun Balance b/d 880.00

Dr M Roper & Sons (account no 302) Cr20-2 £ 20-2 £18 May Purchases Returns 36.00 1 May Balance b/d 85.0028 May Purchases Returns 45.60 2 May Purchases 228.0031 May Balance c/d 565.00 18 May Purchases 216.00

25 May Purchases 117.60646.60 646.60

1 Jun Balance b/d 565.00

9

GENERAL LEDGER

Dr Purchases Account Cr20-2 £ 20-2 £31 May Purchases Day Book 1,118.00

Dr Purchases Returns Account Cr20-2 £ 20-2 £

31 May Purchases Day Book 108.00

Dr Value Added Tax Account Cr20-2 £ 20-2 £31 May Purchases Day Book 223.60 31 May Purchases Returns Day Book 21.60

31 May Balance c/d 202.00223.60 223.60

1 Jun Balance b/d 202.00

7.2 amount of VAT-exclusiveVAT amount

• £12.00 £2.00 £10.00• £14.40 £2.40 £12.00• £10.56 £1.76 £8.80• £6.64 £1.10 £5.54• £0.96 £0.16 £0.80• £2.26 £0.37 £1.89

7.3 (a) and (b)

Dr Value Added Tax Account Cr20-0 £ 20-0 £

1 Mar Balance b/d 80531 Mar Purchases Day Book 735 31 Mar Sales Day Book 1,12031 Mar Sales Returns Day Book 28 31 Mar Purchases Returns Day Book 4231 Mar Balance c/d 1,204

1,967 1,967

1 Apr Balance b/d 1,204

(c) At the end of March 20-0, the Value Added Tax account has a credit balance of £1,204. This amount isowing to HM Revenue & Customs and will be paid at the end of the three-month VAT period, togetherwith VAT due for the subsequent month(s) of the VAT quarter.

8.3Dr Cash Book CrDate Details Folio Disc Cash Bank Date Details Folio Disc Cash Bank

allwd recd20-7 £ £ £ 20-7 £ £ £1 Aug Balances b/d 276 4,928 5 Aug T Hall Ltd 24 5411 Aug Wild & Sons Ltd 398 8 Aug Wages 25411 Aug Bank C 500 11 Aug Cash C 50012 Aug A Lewis Ltd 20 1,755 18 Aug F Jarvis 45721 Aug Harvey & Sons Ltd 261 22 Aug Wages 43629 Aug Wild & Sons Ltd 15 595 25 Aug J Jones 33 62829 Aug Bank C 275 27 Aug Salaries 2,043

28 Aug Telephone 27629 Aug Cash C 27531 Aug Balances c/d 361 3,217

35 1,051 7,937 57 1,051 7,9371 Sep Balances b/d 361 3,217

8.4

Dr Cash Book CrDate Details Folio Discount Cash Bank Date Details Folio Discount Cash Bank

allowed receivedYear 6 £ £ £ Year 6 £ £ £ 1 Mar Balances b/d 106 3,214 2 Mar Rent 10674 2503 Mar Sales* 100 950 5 Mar Cleaning expenses 358 Mar Sales 1,680 9 Mar Purchases 10675 1,20011 Mar Bank C 150 11 Mar Cash 10676 C 15013 Mar Sales 1,800 16 Mar Postages 5022 Mar Bank C 150 18 Mar Telephone 10677 16825 Mar Sales 2,108 20 Mar Stationery 12829 Mar Sales* 200 2,000 22 Mar Cash 10678 C 15031 Mar S Britton 30 720 26 Mar Misc expenses 7031 Mar D F Pratt 50 1,160 27 Mar Wages 10679 2,000

30 Mar Electricity 10680 10631 Mar D Coyne 10681 45 85531 Mar F Cox 10682 26 49431 Mar Balances c/d 423 8,259

80 706 13,632 71 706 13,6321 Apr Balances b/d 423 8,259

* An alternative way of showing the transactions of 3 March and 29 March is to record the full amount of sales in the debitcash column, and then to show the amount banked as a separate transfer, ie debit bank, credit cash.

10

CHAPTER 7 Value Added Tax

CHAPTER 8 Cash Book

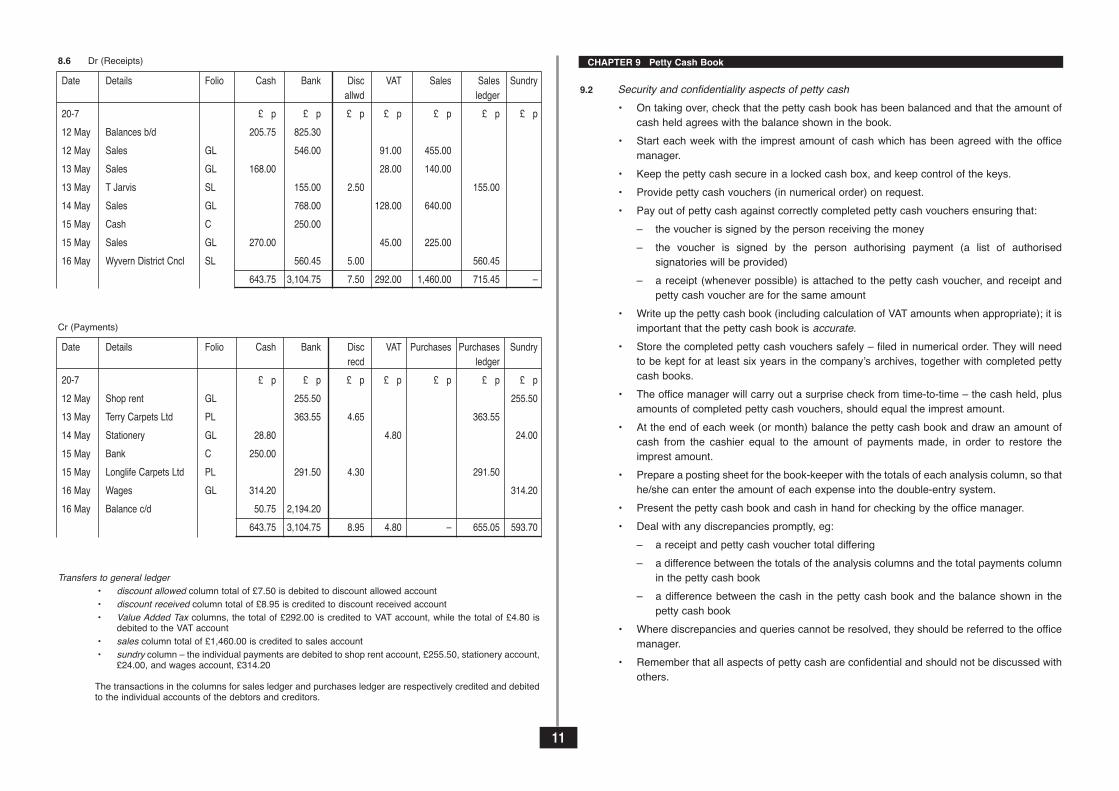

8.6 Dr (Receipts)

Date Details Folio Cash Bank Disc VAT Sales Sales Sundryallwd ledger

20-7 £ p £ p £ p £ p £ p £ p £ p

12 May Balances b/d 205.75 825.30

12 May Sales GL 546.00 91.00 455.00

13 May Sales GL 168.00 28.00 140.00

13 May T Jarvis SL 155.00 2.50 155.00

14 May Sales GL 768.00 128.00 640.00

15 May Cash C 250.00

15 May Sales GL 270.00 45.00 225.00

16 May Wyvern District Cncl SL 560.45 5.00 560.45

643.75 3,104.75 7.50 292.00 1,460.00 715.45 –

Cr (Payments)

Date Details Folio Cash Bank Disc VAT Purchases Purchases Sundryrecd ledger

20-7 £ p £ p £ p £ p £ p £ p £ p

12 May Shop rent GL 255.50 255.50

13 May Terry Carpets Ltd PL 363.55 4.65 363.55

14 May Stationery GL 28.80 4.80 24.00

15 May Bank C 250.00

15 May Longlife Carpets Ltd PL 291.50 4.30 291.50

16 May Wages GL 314.20 314.20

16 May Balance c/d 50.75 2,194.20

643.75 3,104.75 8.95 4.80 – 655.05 593.70

Transfers to general ledger• discount allowed column total of £7.50 is debited to discount allowed account• discount received column total of £8.95 is credited to discount received account• Value Added Tax columns, the total of £292.00 is credited to VAT account, while the total of £4.80 is

debited to the VAT account• sales column total of £1,460.00 is credited to sales account• sundry column – the individual payments are debited to shop rent account, £255.50, stationery account,

£24.00, and wages account, £314.20

The transactions in the columns for sales ledger and purchases ledger are respectively credited and debitedto the individual accounts of the debtors and creditors.

9.2 Security and confidentiality aspects of petty cash• On taking over, check that the petty cash book has been balanced and that the amount of

cash held agrees with the balance shown in the book.• Start each week with the imprest amount of cash which has been agreed with the office

manager.• Keep the petty cash secure in a locked cash box, and keep control of the keys.• Provide petty cash vouchers (in numerical order) on request.• Pay out of petty cash against correctly completed petty cash vouchers ensuring that:

– the voucher is signed by the person receiving the money– the voucher is signed by the person authorising payment (a list of authorised

signatories will be provided)– a receipt (whenever possible) is attached to the petty cash voucher, and receipt and

petty cash voucher are for the same amount• Write up the petty cash book (including calculation of VAT amounts when appropriate); it is

important that the petty cash book is accurate.• Store the completed petty cash vouchers safely – filed in numerical order. They will need

to be kept for at least six years in the company’s archives, together with completed pettycash books.

• The office manager will carry out a surprise check from time-to-time – the cash held, plusamounts of completed petty cash vouchers, should equal the imprest amount.

• At the end of each week (or month) balance the petty cash book and draw an amount ofcash from the cashier equal to the amount of payments made, in order to restore theimprest amount.

• Prepare a posting sheet for the book-keeper with the totals of each analysis column, so thathe/she can enter the amount of each expense into the double-entry system.

• Present the petty cash book and cash in hand for checking by the office manager.• Deal with any discrepancies promptly, eg:

– a receipt and petty cash voucher total differing– a difference between the totals of the analysis columns and the total payments column

in the petty cash book– a difference between the cash in the petty cash book and the balance shown in the

petty cash book• Where discrepancies and queries cannot be resolved, they should be referred to the office

manager.• Remember that all aspects of petty cash are confidential and should not be discussed with

others.

11

CHAPTER 9 Petty Cash Book

9.3

Documentation will be a post office receipt for £4.45, being the amount of postages paid.

Documentation will be a till receipt (or handwritten receipt) from the stationery shop for £2.40.

9.4

Receipts Date Details Voucher Total ANALYSIS COLUMNS

number payment Postage Travelling Vehicle Cleaning Ledger

£ Year 8 £ £ £ £ £ £

120.00 1 Jun Balance b/d

80.00 1 Jun Bank

2 Jun Postage 5.20 5.20

6 Jun Rail fare 12.70 12.70

9 Jun Petrol 8.50 8.50

14 Jun Cleaning materials 10.00 10.00

16 Jun S Lancaster 18.30 18.30

18 Jun Petrol 14.30 14.30

20 Jun Postage 6.70 6.70

24 Jun Petrol 12.40 12.40

25 Jun Rail fare 13.20 13.20

27 Jun Postage 7.70 7.70

28 Jun W Rose 19.20 19.20

30 Jun Petrol 14.80 14.80

143.00 19.60 25.90 50.00 10.00 37.50

30 Jun Balance c/d 57.00

200.00 200.00

57.00 1 Jul Balance b/d

143.00 1 Jul Bank

12

petty cash voucher No. 851date today

description amount (£)

Postage on urgent parcel of spare parts toEvelode Supplies Ltd 4 45

4 45VAT

4 45

signature Jayne Smith

authorised A Student

petty cash voucher No. 852date today

description amount (£)

Airmail envelopes 2 00

2 00VAT 0 40

2 40

signature Tanya Howard

authorised A Student

9.7 Petty Cash Book

Receipts Date Details Voucher Total Analysis columns

No Payment VAT Postages Travel Meals SundryOffice

£ 20-7 £ £ £ £ £ £

125.00 2 Jun Balance b/d

2 Jun Postages 123 6.35 6.35

3 Jun Travel expenses 124 13.25 13.25

3 Jun Postages 125 3.25 3.25

4 Jun Envelopes 126 4.64 0.77 3.87

4 Jun Window cleaning 127 12.00 2.00 10.00

5 Jun Taxi fare/meals 128 24.00 4.00 8.00 12.00

5 Jun Post/packing 129 12.10 0.60 8.50 3.00

5 Jun Taxi fare/meals 130 21.60 3.60 10.00 8.00

6 Jun Pens/envelopes 131 6.49 1.08 5.41

103.68 12.05 18.10 31.25 20.00 22.28

103.68 6 Jun Cash received

6 Jun Balance c/d 125.00

228.68 228.68

125.00 7 Jun Balance b/d

GENERAL LEDGER

Dr Value Added Tax Account Cr20-7 £ p 20-7 £ p6 Jun Petty Cash Book 12.05

Dr Postages Account Cr20-7 £ p 20-7 £ p6 Jun Petty Cash Book 18.10

Dr Travel Expenses Account Cr20-7 £ p 20-7 £ p6 Jun Petty Cash Book 31.25

Dr Meals Account Cr20-7 £ p 20-7 £ p6 Jun Petty Cash Book 20.00

Dr Sundry Office Expenses Account Cr20-7 £ p 20-7 £ p6 Jun Petty Cash Book 22.28

CASH BOOKDr Cash book Cr

Cash Bank Cash Bank20-7 £ p £ p 20-7 £ p £ p

6 Jun Petty Cash Book 103.68

9.9

Dr Cash Book Cr

Date Details Folio Discount Cash Bank Date Details Folio Discount Cash Bankallowed received

20-8 £ £ £ 20-8 £ £ £

5 Feb S Kahn 3,250.60 1 Feb Balance b/d 1,598.55

10 Feb Cash sales 88.25 1 Feb Petty cash 169.60

12 Feb B Shean 5.00 140.00 5 Feb Insurance 120.50

12 Feb H Shanks 335.85 5 Feb Rent 240.00

16 Feb S Groves 60.00 1,140.00 16 Feb Motor expenses 120.00

26 Feb Cash sales 220.00 16 Feb Purchases 390.55

26 Feb C Bentley 435.55 19 Feb Drawings 50.00

26 Feb Purchases 990.50

28 Feb Balance c/d 1,930.55

65.00 5,610.25 – 5,610.25

1 Mar Balance b/d 1,930.55

13

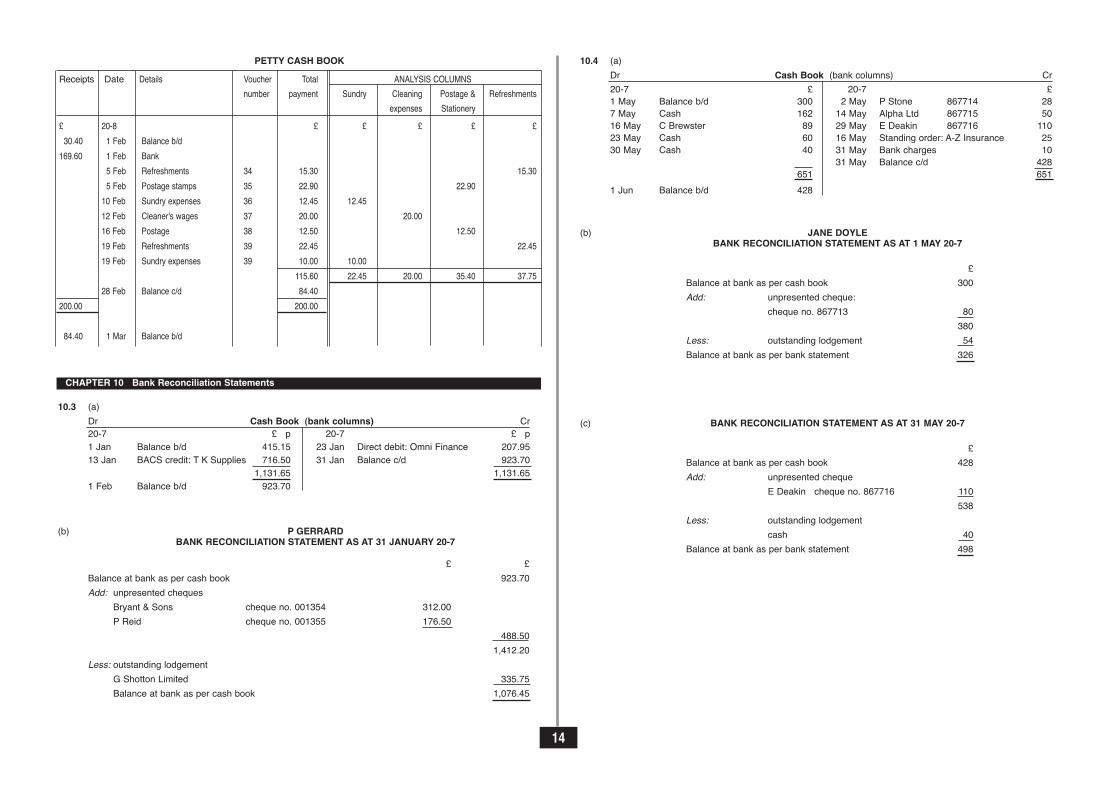

PETTY CASH BOOK

Receipts Date Details Voucher Total ANALYSIS COLUMNS

number payment Sundry Cleaning Postage & Refreshments

expenses Stationery

£ 20-8 £ £ £ £ £

30.40 1 Feb Balance b/d

169.60 1 Feb Bank

5 Feb Refreshments 34 15.30 15.30

5 Feb Postage stamps 35 22.90 22.90

10 Feb Sundry expenses 36 12.45 12.45

12 Feb Cleaner's wages 37 20.00 20.00

16 Feb Postage 38 12.50 12.50

19 Feb Refreshments 39 22.45 22.45

19 Feb Sundry expenses 39 10.00 10.00

115.60 22.45 20.00 35.40 37.75

28 Feb Balance c/d 84.40

200.00 200.00

84.40 1 Mar Balance b/d

10.3 (a)Dr Cash Book (bank columns) Cr20-7 £ p 20-7 £ p1 Jan Balance b/d 415.15 23 Jan Direct debit: Omni Finance 207.9513 Jan BACS credit: T K Supplies 716.50 31 Jan Balance c/d 923.70

1,131.65 1,131.651 Feb Balance b/d 923.70

(b) P GERRARDBANK RECONCILIATION STATEMENT AS AT 31 JANUARY 20-7

£ £Balance at bank as per cash book 923.70Add: unpresented cheques

Bryant & Sons cheque no. 001354 312.00P Reid cheque no. 001355 176.50

488.501,412.20

Less: outstanding lodgementG Shotton Limited 335.75Balance at bank as per cash book 1,076.45

10.4 (a)Dr Cash Book (bank columns) Cr20-7 £ 20-7 £1 May Balance b/d 300 2 May P Stone 867714 287 May Cash 162 14 May Alpha Ltd 867715 5016 May C Brewster 89 29 May E Deakin 867716 11023 May Cash 60 16 May Standing order: A-Z Insurance 2530 May Cash 40 31 May Bank charges 10

31 May Balance c/d 428651 651

1 Jun Balance b/d 428

(b) JANE DOYLEBANK RECONCILIATION STATEMENT AS AT 1 MAY 20-7

£Balance at bank as per cash book 300Add: unpresented cheque:

cheque no. 867713 80380

Less: outstanding lodgement 54Balance at bank as per bank statement 326

(c) BANK RECONCILIATION STATEMENT AS AT 31 MAY 20-7

£Balance at bank as per cash book 428Add: unpresented cheque

E Deakin cheque no. 867716 110538

Less: outstanding lodgementcash 40

Balance at bank as per bank statement 498

14

CHAPTER 10 Bank Reconciliation Statements

10.511.5 (a) Objections:

• jobs may be threatened and redundancies may occur

• the need for retraining

• possible bad effects to health caused by sitting in front of a computer all day: RSI (Repetitive Strain Injury), back problems, radiation and eye damage from computer screens

(b) Potential benefits:

• potential for updating IT skills through training

• possible increase in pay for skilled work

• better career prospects

• job satisfaction through automation of manual processes

12.2

15

MEMORANDUMTO: ........................................

FROM: Accounts Clerk

DATE: .........................................

SUBJECT: Bank Reconciliation Statements

Reconciliation of the bank statement balance with that shown in the cash book is carried out atthe month-end as follows:

1. From the bank columns of the cash book tick off, in both cash book and bank statement:

• the receipts that appear in both

• the payments that appear in both

2. Identify the items that are unticked on the bank statement and enter them in the cash bookon the debit or credit side as appropriate. These will be things such as BACS receipts,standing order and direct debit payments, bank charges and interest, unpaid chequesdebited by the bank. However, if the bank has made a mistake by debiting or crediting ouraccount in error, don’t enter them in the cash book; instead, notify the bank for them tomake the correction.

3. Balance the bank columns of the cash book to find the up-to-date balance.

4. Start the bank reconciliation statement with the balance brought down figure shown in thecash book.

5. In the bank reconciliation statement:

• add the unticked payments shown in the cash book – these are unpresented cheques

• deduct the unticked receipts shown in the cash book – these are outstanding lodgements

6. The resultant money amount on the bank reconciliation statement is the balance of thebank statement.

7. Date the reconciliation statement and file it away for future reference. Note that, if thebalances of the cash book (bank columns) and the bank statement were not identical at thebeginning of the month, then you will need to refer to the previous bank reconciliationstatement prepared at the end of last month. Items appearing on that bank reconciliationstatement must also be ticked off at step 1. Anything remaining unticked will be included inthis month’s reconciliation statement (step 5).

A Student

CHAPTER 11 An Introduction to Computer Accounting

CHAPTER 12 Final Accounts

Vehicle

12.5CLARE LEWIS

TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 20-4

£ £Sales 144,810Opening stock 16,010Purchases 96,318

112,328Less Closing stock 13,735Cost of Goods Sold 98,593Gross profit 46,217Less expenses:Salaries 18,465Heating and lighting 1,820Rent and rates 5,647Sundry expenses 845Vehicle expenses 1,684

28,461Net profit 17,756

BALANCE SHEET AS AT 31 DECEMBER 20-4

£ £ £Fixed AssetsVehicles 9,820Office equipment 5,500

15,320Current AssetsStock 13,735Debtors 18,600

32,335Less Current LiabilitiesCreditors 12,140Value Added Tax 1,210Bank overdraft 4,610

17,960Working Capital 14,375NET ASSETS 29,695

FINANCED BYCapitalOpening capital 25,250Add Net profit 17,756

43,006Less Drawings 13,311

29,695

12.6 capital revenueexpenditure expenditure

(a) purchase of vehicles �

(b) rent paid on premises �

(c) wages and salaries �

(d) legal fees relating to the purchase �

of property

(e) re-decoration of office �

(f) installation of air-conditioning in office �

(g) wages of own employees used to build �

extension to the stockroom

(h) installation and setting up of a new �

machine

12.7(a) (i) Capital expenditure

• Weighing equipment for business use• Extension to business premises• Legal fees relating to extension

(ii) Revenue expenditure• Payment of local authority rates• Sales assistants' wages

(iii) Revenue receipt• Rent received from sub-letting office space

(b) (i) Trading account• Sales assistants' wages (shown here in trading account because it is a direct selling expense,

rather than a general profit and loss account expense)

(ii) Profit and loss account• Rent received from sub-letting office space• Payment of local authority rates

(iii) Balance sheet• Weighing equipment for business use• Extension to business premises (added to the cost of the premises)• Legal fees relating to extension (shown in balance sheet, and added to the cost of the premises,

because it is an expense which relates to the improvement of fixed assets, rather than a generalprofit and loss account expense)

16

13.1 (a) Expense in profit and loss account of £56,760; balance sheet shows wages and salaries accrued(current liability) of £1,120.

(b) Expense in profit and loss account of £2,852; balance sheet shows rates prepaid (current asset) of£713.

(c) Expense in profit and loss account of £1,800; balance sheet shows computer rental prepaid (currentasset) of £150.

13.2SOUTHTOWN SUPPLIES

TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 20-9

£ £

Sales 420,000

Opening stock 70,000

Purchases 280,000

350,000

Less Closing stock 60,000

Cost of Goods Sold 290,000

Gross profit 130,000

Less expenses:

Rent and rates £10,250 – £550 9,700

Electricity 3,100

Telephone 1,820

Salaries £35,600 + £450 36,050

Vehicle expenses 13,750

64,420

Net profit 65,580

13.4 (a)H EGGLETON

BALANCE SHEET AS AT 28 FEBRUARY 20-8

£ £ £Fixed AssetsFreehold property 50,000Motor vehicles 12,600Machinery 2,500Fixtures and fittings 1,250

66,350

Current AssetsStock 4,760Debtors 540Prepayment (insurance) 380Cash 390

6,070

Less Current LiabilitiesCreditors 550Bank 3,250Accrual (wages) 900

4,700Working Capital 1,370

67,720

Less Long-term LiabilitiesMortgage 10,000NET ASSETS 57,720

FINANCED BY:CapitalOpening capital (missing figure) 45,750Add net profit 13,970

59,720Less drawings 2,000

57,720

(b)

Dr Drawings Account Cr

20-7/20-8 £ 20-7/20-8 £2 Jun Bank 500 28 Feb Capital 2,00028 Aug Bank 5001 Dec Bank 50010 Feb Bank 500

2,000 2,000

17

CHAPTER 13 Accruals and Prepayments

Dr Capital Account Cr20-7/20-8 £ 20-7/20-8 £28 Feb Drawings 2,000 1 Mar Balance b/d 45,75028 Feb Balance c/d 57,720 28 Feb Profit and loss account 13,970

59,720 59,7201 Mar Balance b/d 57,720

13.6JOHN BARCLAY

TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 30 JUNE 20-9

£ £ £Sales 864,321Less Sales returns 2,746Net sales 861,575Opening stock (1 July 20-8) 63,084Purchases (less £250 goods for own use) 599,878Less Purchase returns 3,894Net purchases 595,984

659,068Less Closing stock (30 June 20-9) 66,941Cost of Goods Sold 592,127Gross profit 269,448Add Discount received 4,951

274,399

Less expenses:Office expenses 33,601Salaries 122,611Vehicle expenses 38,144Discount allowed 3,187

197,543Net profit 76,856

BALANCE SHEET AS AT 30 JUNE 20-9

£ £ £Fixed AssetsLand and buildings 100,000Vehicles 83,500Office equipment 23,250

206,750

Current AsetsStock 66,941Debtors 74,328Prepayment 346Bank 1,197

142,812

Less Current LiabilitiesCreditors 52,919Value Added Tax 10,497Accrual 1,250

64,666Working Capital 78,146

284,896

Less Long-term LiabilitiesBank loan 75,000NET ASSETS 209,896

FINANCED BY:

CapitalOpening capital 155,000Add net profit 76,856

231,856Less drawings (plus £250 goods for own use) 21,960

209,896

18

14.3 (a)Dr Vehicles Account Cr20-8 £ 20-8 £1 Jan Balance b/d 12,000 1 Oct Disposals account 12,0001 Oct Disposals account 5,500 31 Dec Balance c/d 15,000

(part-exchange allowance)1 Oct Bank 9,500

(balance paid by cheque)27,000 27,000

20-9 £ 20-9 £1 Jan Balance b/d 15,000

(b)

Dr Provision for Depreciation Account – Vehicles Cr20-8 £ 20-8 £1 Oct Disposals account 7,200 1 Jan Balance b/d 7,20031 Dec Balance c/d 3,000 31 Dec Profit & loss account 3,000

10,200 10,20020-9 £ 20-9 £

1 Jan Balance b/d 3,000(c)

Dr Disposals Account – Vehicles Cr20-8 £ 20-8 £1 Oct Vehicles account 12,000 1 Oct Vehicles account 5,50031 Dec Profit and loss account 700 (part-exchange allowance)

(profit on sale) 1 Oct Prov for dep'n account 7,20012,700 12,700

(d) Balance sheet (extract) of Rachael Hall as at 31 December 20-8

£ £ £Cost Dep’n to date Net

Fixed assetsVehicles 15,000 3,000 12,000

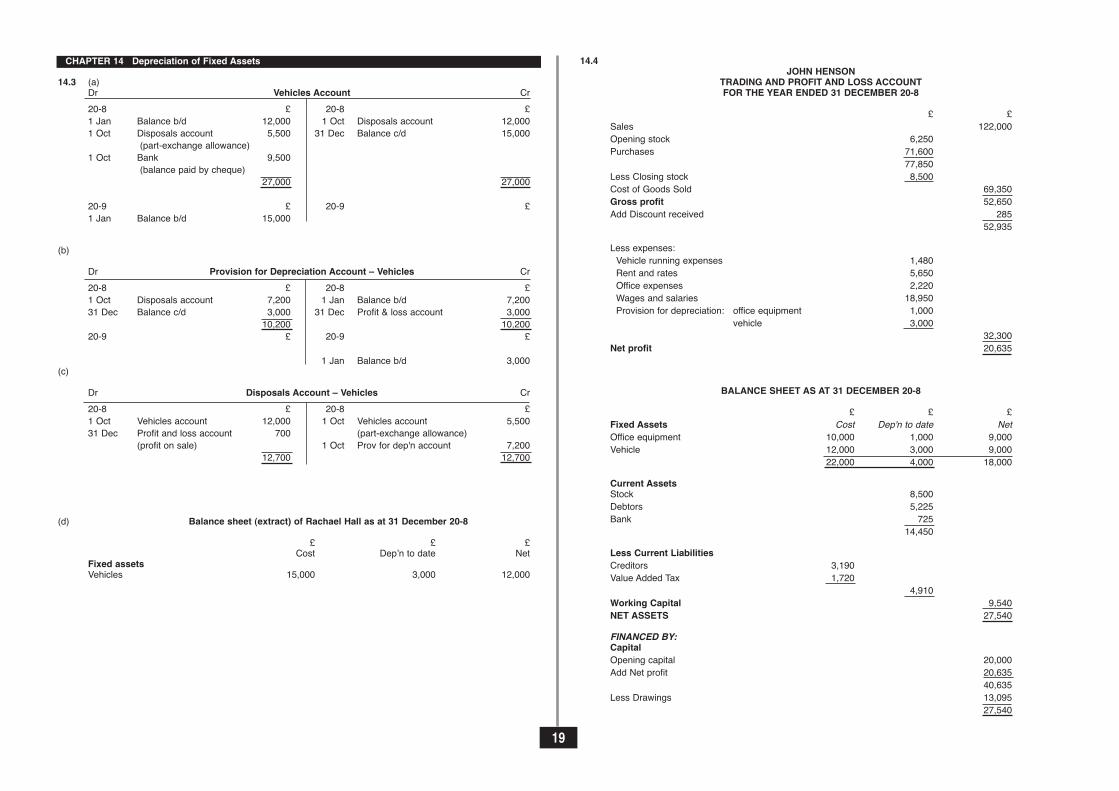

14.4JOHN HENSON

TRADING AND PROFIT AND LOSS ACCOUNTFOR THE YEAR ENDED 31 DECEMBER 20-8

£ £Sales 122,000Opening stock 6,250Purchases 71,600

77,850Less Closing stock 8,500Cost of Goods Sold 69,350Gross profit 52,650Add Discount received 285

52,935

Less expenses:Vehicle running expenses 1,480Rent and rates 5,650Office expenses 2,220Wages and salaries 18,950Provision for depreciation: office equipment 1,000

vehicle 3,00032,300

Net profit 20,635

BALANCE SHEET AS AT 31 DECEMBER 20-8

£ £ £Fixed Assets Cost Dep'n to date NetOffice equipment 10,000 1,000 9,000Vehicle 12,000 3,000 9,000

22,000 4,000 18,000

Current AssetsStock 8,500Debtors 5,225Bank 725

14,450

Less Current LiabilitiesCreditors 3,190Value Added Tax 1,720

4,910Working Capital 9,540NET ASSETS 27,540

FINANCED BY:CapitalOpening capital 20,000Add Net profit 20,635

40,635Less Drawings 13,095

27,540

19

CHAPTER 14 Depreciation of Fixed Assets

14.5SIMON ADO

TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 OCTOBER

£ £Sales (work done) 19,480Opening stock 180Purchases of materials 3,415

3,595Less Closing stock 190Cost of Goods Sold 3,405Gross profit 16,075Add Discount received 200

16,275

Less expenses:Advertising 90Telephone 710Motor expenses 580Provision for depreciation: van 2,000

tools and equipment 3003,680

Net profit 12,595

BALANCE SHEET OF SIMON ADO AS AT 31 OCTOBER

£ £ £Fixed Assets Cost Dep'n to date NetVan 8,000 2,000 6,000Tools and equipment 3,000 300 2,700

11,000 2,300 8,700

Current AssetsStock 190Prepayments 120Cash 320

630

Less Current LiabilitiesCreditors 85Bank overdraft 90

175Working Capital 455NET ASSETS 9,155

FINANCED BY:CapitalOpening capital 2,960Add Net profit 12,595

15,555Less Drawings 6,400

9,155

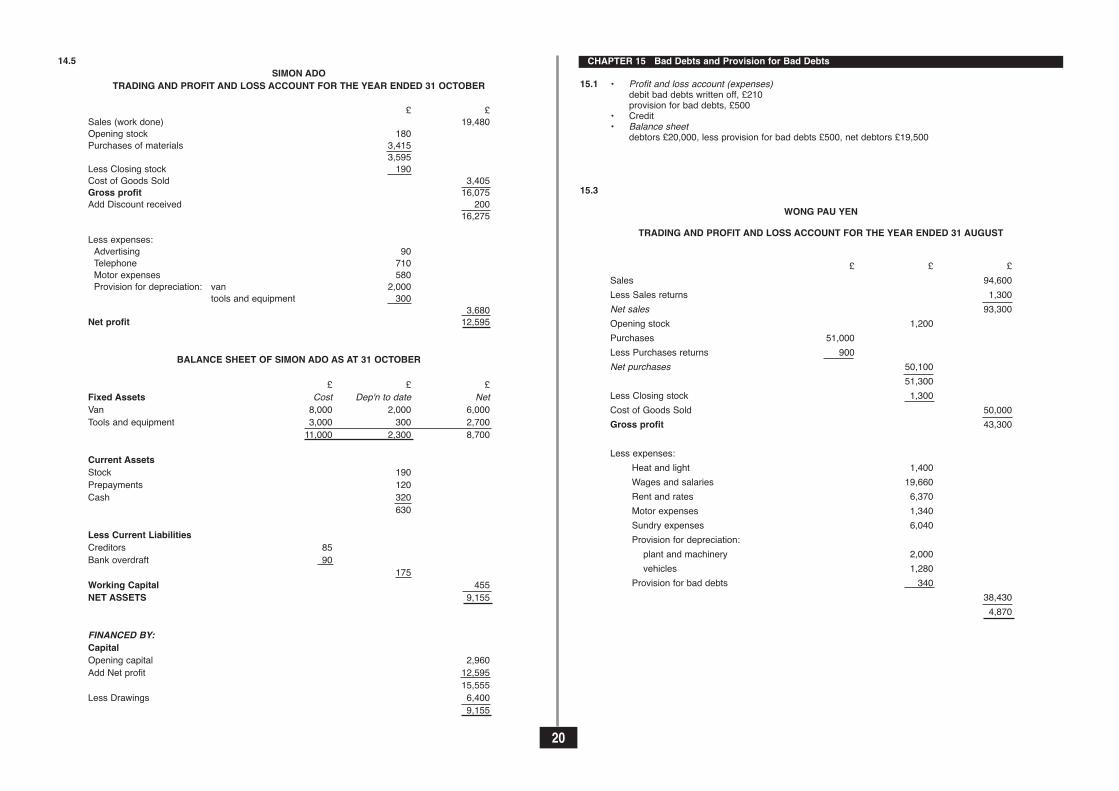

15.1 • Profit and loss account (expenses)debit bad debts written off, £210provision for bad debts, £500

• Credit• Balance sheet

debtors £20,000, less provision for bad debts £500, net debtors £19,500

15.3

WONG PAU YEN

TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 AUGUST

£ £ £Sales 94,600Less Sales returns 1,300Net sales 93,300Opening stock 1,200Purchases 51,000Less Purchases returns 900Net purchases 50,100

51,300Less Closing stock 1,300Cost of Goods Sold 50,000Gross profit 43,300

Less expenses:Heat and light 1,400Wages and salaries 19,660Rent and rates 6,370Motor expenses 1,340Sundry expenses 6,040Provision for depreciation:plant and machinery 2,000vehicles 1,280

Provision for bad debts 34038,4304,870

20

CHAPTER 15 Bad Debts and Provision for Bad Debts

BALANCE SHEET AS AT 31 AUGUST

£ £ £

Fixed Assets Cost Dep'n to date NetPlant and machinery 20,000 6,000 14,000Vehicles 10,000 4,880 5,120

30,000 10,880 19,120

Current AssetsStock 1,300Debtors 8,500Less Provision for bad debts 340

8,160Prepayment 360Cash 100

9,920

Less Current LiabilitiesCreditors 4,660Accruals 1,190Bank overdraft 1,690

7,540Working Capital 2,380NET ASSETS 21,500

FINANCED BY:CapitalOpening capital 24,230Add Net profit 4,870

29,100Less Drawings 7,600

21,500

15.5

D MARTINTRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER YEAR 6

£ £ £Sales 337,200Less Sales returns 4,950Net sales 332,250Opening stock 21,480Purchases 191,200Carriage inwards 1,200Less Purchases returns 3,600Net purchases 188,800

210,280Less Closing stock 24,900Cost of Goods Sold 185,380Gross profit 146,870

Add income:Discount received 2,090Reduction in provision for bad debts 400

149,360Less expenses:

Rent 14,000Electricity 4,160Salaries 53,300Carriage outwards 6,000Insurance 3,420Bad debts 2,400Bank interest 720Telephone 3,200Discount allowed 2,700Loan interest 2,600Loss on sale of vehicle 750Provision for depreciation:vehicles 5,000office furniture 1,000

99,250Net profit 50,110

21

BALANCE SHEET AS AT 31 DECEMBER YEAR 6

£ £ £Fixed Assets Cost Dep'n to date NetFreehold premises 160,000 – 160,000Motor vehicles 25,000 10,000 15,000Office furniture 10,000 3,500 6,500

195,000 13,500 181,500

Current AssetsStock 24,900Debtors 31,400Less Provision for bad debts 1,570

29,830Prepayments 4,780Cash 600

60,110

Less Current LiabilitiesCreditors 7,880Accruals 6,160Bank overdraft 7,000

21,040Working Capital 39,070

220,570Less Long-term LiabilitiesLoan from D Samson 26,000NET ASSETS 194,570

FINANCED BY:CapitalOpening capital 184,460Add Net profit 50,110

234,570Less Drawings 40,000

194,570

Loss on sale of vehicle: £cost price (1 January, year 3) 5,000depreciation at 20% pa (years 3, 4 and 5) 3,000book value at date of sale 2,000sale proceeds 1,250loss on sale (debited to profit and loss account) 750

22

16.1

EXTE

NDED

TRI

AL B

ALAN

CEAL

AN H

ARRI

S30

JUN

E 20

-2

CHAPTER 16 The Extended Trial Balance

20-1

17.1• Going concern concept

This presumes that the business to which the final accounts relate will continue to trade in the foreseeablefuture. The trading and profit and loss account and balance sheet are prepared on the basis that there isno intention to reduce significantly the size of the business or to liquidate the business. If the business wasnot a going concern, assets would have very different values, and the balance sheet would be affectedconsiderably.Example: fixed assets are valued at cost, less accumulated depreciation to date.

• Accruals conceptThis means that expenses and revenues are matched so that they concern the same goods and the sametime period.Examples: The accrual of an expense in profit and loss account which has been used in the accountingperiod but not yet paid for. The prepayment of an expense for the next accounting period. The recordingof opening and closing stocks in the trading account. The use of debtors' and creditors' accounts to recordamounts owing to the business, or owed by the business.

• Consistency conceptThis requires that, when a business adopts particular accounting methods, it should continue to use suchmethods consistently over a number of accounting periods. In this way, direct comparison between thefinal accounts of different years can be made.Examples: The continued use of a particular depreciation method, eg straight-line. The method of stockvaluation used. The treatment of capital and revenue expenditure.

• Prudence conceptThis concept requires that final accounts should always, where there is any doubt, report a conservativefigure for profit or the valuation of assets. To this end, profits are not to be anticipated and should only berecognised when it is reasonably certain that they will be realised; at the same time, all known liabilitiesshould be provided for.Examples: A provision for bad debts – the debtors have not yet gone bad, but it is expected, fromexperience, that a certain percentage will eventually need to be written off as bad debts. The valuation ofstock at the lower of cost and net realisable value in order to give the lower valuation for the final accounts.

17.4 (a) £ Opening stock at 1 January Year 7Balance from ledger (1 January Year 7) 17,300 (1.1) adjustment of incorrect stock value

12 items @ £15 each = £180 – £80 recorded 100 17,400

(1.2) items omitted from physical stock take, cost price 250 Revised stock valuation at 1 January Year 7 17,650

Closing stock at 31 March Year 7Balance from ledger (31 March Year 7) 16,200 (2.1) reduction to net realisable value (500)

15,700 (2.2) correction of undercast on stock sheet 3,000

18,700 (2.3) reduction to net realisable value: £190 – £150 (40)Revised stock valuation at 31 March Year 7 18,660

(b)TRADING ACCOUNT FOR QUARTER ENDED 31 MARCH YEAR 7

£ £Sales 107,800Opening stock 17,650Purchases 54,200

71,850Less Closing stock 18,660Cost of Goods Sold 53,190Gross profit 54,610

17.6 (a)STORES LEDGER RECORD

Date Receipts Issues Balance

Quantity Price Value Quantity Price Value Quantity Price Value

£ £ £ £ £ £

Year 3

1 Sep Balance 30 10.00 300

3 Sep 40 11.00 440 30 10.00 300

40 11.00 440

70 10.571 740

6 Sep 100 12.00 1,200 70 10.571 740

100 12.00 1,200

170 11.412 1,940

7 Sep 50 11.412 571 120 11.412 1,369

8 Sep 70 14.00 980 120 11.412 1,369

70 14.00 980

190 12.363 2,349

10 Sep 80 12.363 989 110 12.363 1,360

15 Sep 150 11.50 1,725 110 12.363 1,360

150 11.50 1,725

260 11.865 3,085

17 Sep 60 11.865 712 200 11.865 2,373

18 Sep 40 11.865 475 160 11.865 1,898

24 Sep 90 11.865 1,068 70 11.865 830

28 Sep 200 12.00 2,400 70 11.865 830

200 12.00 2,400

270 11.963 3,230

30 Sep 70 11.963 837 200 11.963 2,393

Note: rounding may cause some figures to differ; these should have no material effect

23

CHAPTER 17 The Regulatory Framework of Accounting

(b)VEE LIMITED

TRADING ACCOUNT FOR SEPTEMBER YEAR 3

£ £Sales: 130 units at £14 each 1,820

260 units at £16 each 4,1605,980

Opening stock 300Purchases 6,745

7,045Less Closing stock 2,393Cost of Goods Sold 4,652Gross profit 1,328

18.2 (a)

Date Details Folio Dr Cr20-8 £ £31 Dec Stock GL 22,600

Trading GL 22,600Stock valuation at 31 December 20-8transferred to trading account

(b)

Date Details Folio Dr Cr20-8 £ £31 Dec Profit and loss GL 890

Telephone expenses GL 890Transfer to profit and loss accountof expenditure for the year

(c)

Date Details Folio Dr Cr20-8 £ £31 Dec Profit and loss GL 23,930

Salaries GL 22,950Accruals GL 980

23,930 23,930Transfer to profit and loss accountof expenditure for the year

(d)

Date Details Folio Dr Cr20-8 £ £31 Dec Profit and loss GL 1,160

Prepayments GL 80Photocopying expenses GL 1,240

1,240 1,240Transfer to profit and loss accountof expenditure for the year

(e)

Date Details Folio Dr Cr20-8 £ £31 Dec Drawings GL 200

Motoring expenses GL 200Transfer of private motoring todrawings account

(f)

Date Details Folio Dr Cr20-8 £ £31 Dec Drawings GL 175

Purchases GL 175Goods taken for own useby the owner

(g)

Date Details Folio Dr Cr20-8 £ £31 Dec Profit and loss GL 500

Provision for depreciation - fixtures and fittings GL 500Depreciation charge for year onfixtures and fittings

24

CHAPTER 18 The Journal

(h)Date Details Folio Dr Cr20-8 £ £31 Dec Disposals GL 5,000

Machinery GL 5,000Provision for depreciation account– machinery GL 3,750Disposals GL 3,750Bank CB 2,400Disposals GL 2,000VAT GL 400Profit and loss GL 750Disposals GL 750

11,900 11,900Sale of machine no .................; profiton sale £750 transferred to profit and loss account

(i)Date Details Folio Dr Cr20-8 £ £31 Dec Bad debts written off GL 125

N Marshall SL 125

Account of N Marshall written off as a bad debt - see memo dated ...................

31 Dec Profit and loss GL 125Bad debts written off GL 125

Transfer to profit and loss accountof bad debts for the year

(j)

Date Details Folio Dr Cr20-8 £ £31 Dec Profit and loss GL 100

Provision for bad debts GL 100

Decrease in provision for bad debts

19.2 (a) error of omission

Date Details Folio Dr Cr£ £

J Rigby SL 150Sales GL 150

Sales invoice no ............. omitted fromthe accounts.

(b) mispost/error of commission

Date Details Folio Dr Cr£ £

H Price Limited PL 125H Prince PL 125

Correction of mispost – cheque no .....:to H Price Limited

(c) error of principle

Date Details Folio Dr Cr£ £

Delivery van GL 10,000Vehicle expenses GL 10,000

Correction of error – vehicle no ............invoice no ...............

(d) reversal of entries

Date Details Folio Dr Cr£ £

Postages GL 55Bank CB 55Postages GL 55Bank CB 55

110 110Correction of reversal of entrieson ...................

25

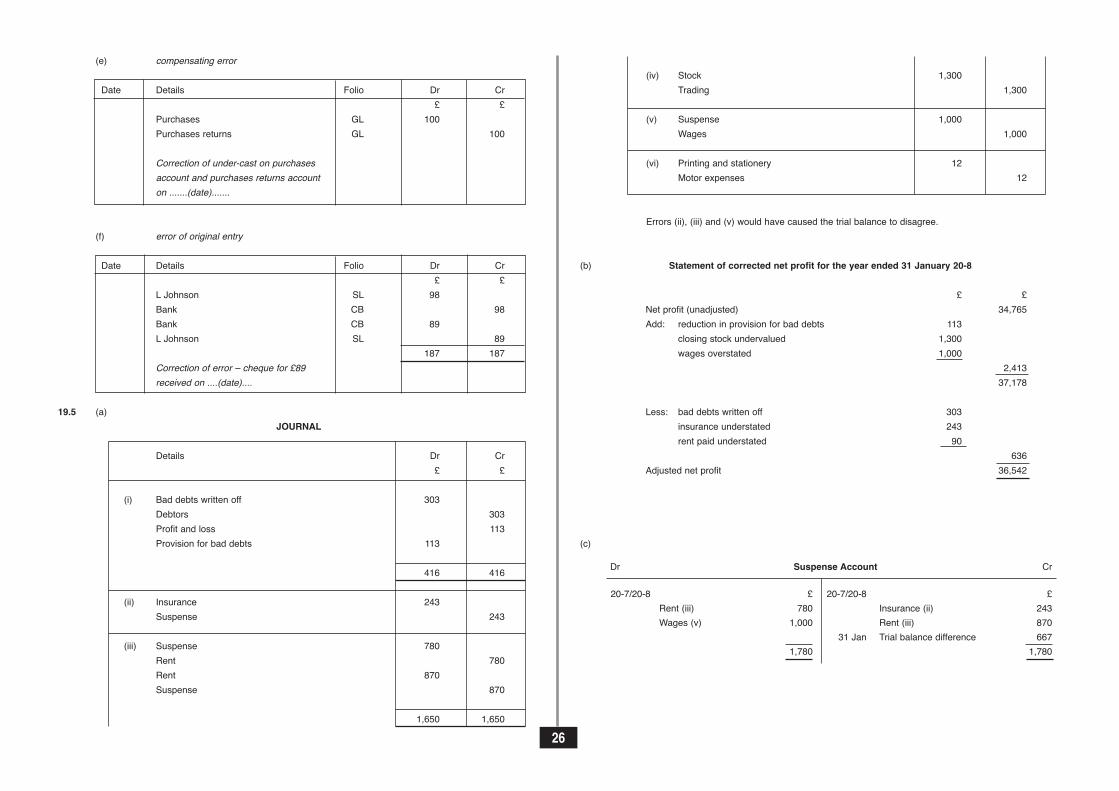

CHAPTER 19 Correction of Errors

(e) compensating error

Date Details Folio Dr Cr£ £

Purchases GL 100Purchases returns GL 100

Correction of under-cast on purchasesaccount and purchases returns accounton .......(date).......

(f) error of original entry

Date Details Folio Dr Cr£ £

L Johnson SL 98Bank CB 98Bank CB 89L Johnson SL 89

187 187Correction of error – cheque for £89received on ....(date)....

19.5 (a)JOURNAL

Details Dr Cr£ £

(i) Bad debts written off 303Debtors 303Profit and loss 113Provision for bad debts 113

416 416

(ii) Insurance 243Suspense 243

(iii) Suspense 780Rent 780Rent 870Suspense 870

1,650 1,650

(iv) Stock 1,300Trading 1,300

(v) Suspense 1,000Wages 1,000

(vi) Printing and stationery 12Motor expenses 12

Errors (ii), (iii) and (v) would have caused the trial balance to disagree.

(b) Statement of corrected net profit for the year ended 31 January 20-8

£ £Net profit (unadjusted) 34,765Add: reduction in provision for bad debts 113

closing stock undervalued 1,300wages overstated 1,000

2,41337,178

Less: bad debts written off 303insurance understated 243rent paid understated 90

636Adjusted net profit 36,542

(c)

Dr Suspense Account Cr

20-7/20-8 £ 20-7/20-8 £Rent (iii) 780 Insurance (ii) 243Wages (v) 1,000 Rent (iii) 870

31 Jan Trial balance difference 6671,780 1,780

26

20.4 (a) SALES LEDGER

Dr Arrow Valley Retailers Cr20-8 £ p 20-8 £ p1 Feb Balance b/d 826.40 20 Feb Bank 805.743 Feb Sales 338.59 20 Feb Discount allowed 20.66

28 Feb Balance c/d 338.591,164.99 1,164.99

1 Mar Balance b/d 338.59

Dr B Brick (Builders) Limited Cr20-8 £ p 20-8 £ p1 Feb Balance b/d 59.28 28 Feb Bad debts written off 59.28

Dr Mereford Manufacturing Company Cr20-8 £ p 20-8 £ p1 Feb Balance b/d 293.49 24 Feb Sales returns 56.293 Feb Sales 127.48 28 Feb Set-off: purchases ledger 364.68

420.97 420.97

Dr Redgrove Restorations Cr20-8 £ p 20-8 £ p1 Feb Balance b/d 724.86 7 Feb Sales returns 165.3817 Feb Sales 394.78 28 Feb Balance c/d 954.26

1,119.64 1,119.64

1 Mar Balance b/d 954.26

Dr Wyvern Warehouse Limited Cr20-8 £ p 20-8 £ p1 Feb Balance b/d 108.40 15 Feb Bank 105.6917 Feb Sales 427.91 15 Feb Discount allowed 2.71

28 Feb Balance c/d 427.91536.31 536.31

1 Mar Balance b/d 427.91

(b)Dr Sales Ledger Control Account Cr20-8 £ p 20-8 £ p1 Feb Balances b/d 2,012.43 28 Feb Sales returns 221.6728 Feb Credit sales 1,288.76 28 Feb Cheques received

from debtors 911.4328 Feb Cash discount allowed 23.3728 Feb Set-off: purchases ldgr. 364.6828 Feb Bad debts written off 59.2828 Feb Balances c/d 1,720.76

3,301.19 3,301.19

1 Mar Balances b/d 1,720.76

(c) Reconciliation of sales ledger control account with debtor balances

1 February 20-8 28 February 20-8£ p £ p

Arrow Valley Retailers 826.40 338.59B Brick (Builders) Limited 59.28 –Mereford Manufacturing Company 293.49 nilRedgrove Restorations 724.86 954.26Wyvern Warehouse Limited 108.40 427.91Sales ledger control account 2,012.43 1,720.76

20.5 (a)

Dr Sales Ledger Control Account Cr

20-7 £ 20-7 £1 Sep Balances b/d 12,000 1 Sep Balances b/d 800

Credit sales 23,150 Sales returns 738Cash refund 111 Cash discount allowed 1,000Dishonoured cheque 130 Bad debts written off 1,377

30 Sep Balances c/d 120 Cash received from debtors 700Cheques received from debtors 25,000

30 Sep Balances c/d 5,89635,511 35,511

1 Oct Balances b/d 5,896 1 Oct Balances b/d 120

(b)£

Sales ledger debit balances 6,007Sales ledger control account debit balance 5,896Difference 111

As the difference is the same amount as the cash refund to Mr Green, with the sales ledger debit balanceshigher, it seems likely that the cash refund has not been recorded on Mr Green's account in the sales ledger.

27

CHAPTER 20 Control Accounts

21.2 (a)

Dr Purchases Ledger Control Account Cr20-7 £ 20-7 £

Bank (missing figure) 41,734 1 Jan Balances b/d 1,34531 Dec Balances c/d 2,456 Purchases 42,845

44,190 44,190

Dr Rent Account Cr20-7 £ 20-7 £1 Jan Balance b/d 450 31 Dec Profit and loss account 1,500

Bank (missing figure) 1,450 31 Dec Balance c/d 4001,900 1,900

Dr Insurance Account Cr20-7 £ 20-7 £1 Jan Balance b/d 40 31 Dec Profit and loss account 750

Bank (missing figure) 735 31 Dec Balance c/d 25775 775

Dr Telephone Account Cr20-7 £ 20-7 £

Bank (missing figure) 1,100 1 Jan Balance b/d 35031 Dec Balance c/d 250 31 Dec Profit and loss account 1,000

1,350 1,350

Dr Motor Expenses Account Cr20-7 £ 20-7 £

Bank (missing figure) 1,279 1 Jan Balance b/d 5031 Dec Balance c/d 25 31 Dec Profit and loss account 1,254

1,304 1,304

Dr Wages Account Cr20-7 £ 20-7 £

Bank (missing figure) 25,419 1 Jan Balance b/d 34531 Dec Balance c/d 567 31 Dec Profit and loss account 25,641

25,986 25,986

Dr Professional Fees Account Cr20-7 £ 20-7 £

Bank (missing figure) 225 31 Dec Profit and loss account 27531 Dec Balance c/d 50

275 275

Dr Subscriptions Account Cr20-7 £ 20-7 £

Bank (missing figure) 70 1 Jan Balance b/d 3531 Dec Profit and loss account 35

70 70

Dr Cash Book (bank columns) Cr20-7 £ 20-7 £1 Jan Balance b/d 4,690 Purchases 41,734

Sales 85,998 Rent 1,450Insurance 735Telephone 1,100Motor expenses 1,279Wages 25,419Professional fees 225Subscriptions 70

31 Dec Balance c/d 18,67690,688 90,688

20-8 20-81 Jan Balance b/d 18,676

(b)

BILL THOMASTRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER 20-7

£ £Sales 85,998Less Purchases 42,845Gross profit 43,153Less expenses:

Telephone 1,000Rent paid 1,500Insurance 750Motor expenses 1,254Wages 25,641Professional fees 275Subscriptions 35

30,455Net profit 12,698

28

CHAPTER 21 Incomplete Records

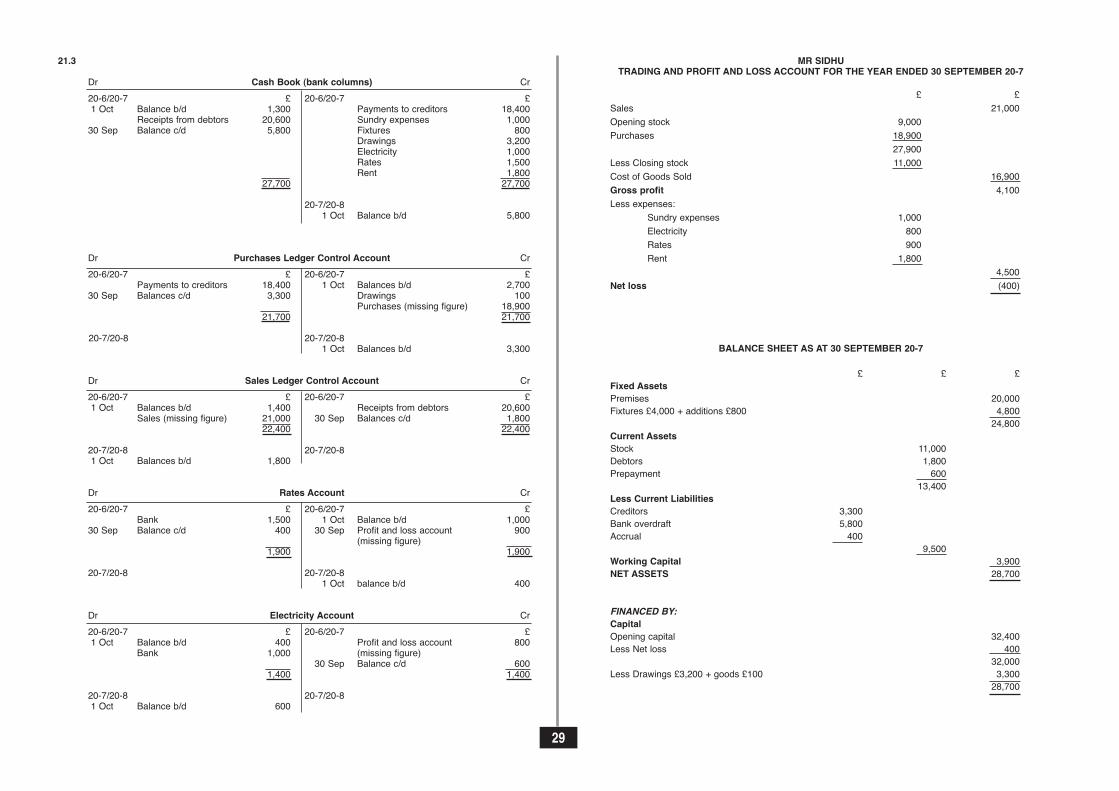

21.3

Dr Cash Book (bank columns) Cr20-6/20-7 £ 20-6/20-7 £1 Oct Balance b/d 1,300 Payments to creditors 18,400

Receipts from debtors 20,600 Sundry expenses 1,00030 Sep Balance c/d 5,800 Fixtures 800

Drawings 3,200Electricity 1,000Rates 1,500Rent 1,800

27,700 27,700

20-7/20-81 Oct Balance b/d 5,800

Dr Purchases Ledger Control Account Cr20-6/20-7 £ 20-6/20-7 £

Payments to creditors 18,400 1 Oct Balances b/d 2,70030 Sep Balances c/d 3,300 Drawings 100

Purchases (missing figure) 18,90021,700 21,700

20-7/20-8 20-7/20-81 Oct Balances b/d 3,300

Dr Sales Ledger Control Account Cr20-6/20-7 £ 20-6/20-7 £1 Oct Balances b/d 1,400 Receipts from debtors 20,600

Sales (missing figure) 21,000 30 Sep Balances c/d 1,80022,400 22,400

20-7/20-8 20-7/20-81 Oct Balances b/d 1,800

Dr Rates Account Cr20-6/20-7 £ 20-6/20-7 £

Bank 1,500 1 Oct Balance b/d 1,00030 Sep Balance c/d 400 30 Sep Profit and loss account 900

(missing figure)1,900 1,900

20-7/20-8 20-7/20-81 Oct balance b/d 400

Dr Electricity Account Cr20-6/20-7 £ 20-6/20-7 £1 Oct Balance b/d 400 Profit and loss account 800

Bank 1,000 (missing figure)30 Sep Balance c/d 600

1,400 1,400

20-7/20-8 20-7/20-81 Oct Balance b/d 600

MR SIDHUTRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 30 SEPTEMBER 20-7

£ £ Sales 21,000 Opening stock 9,000Purchases 18,900

27,900Less Closing stock 11,000Cost of Goods Sold 16,900 Gross profit 4,100 Less expenses:

Sundry expenses 1,000Electricity 800Rates 900Rent 1,800

4,500 Net loss (400)

BALANCE SHEET AS AT 30 SEPTEMBER 20-7

£ £ £Fixed AssetsPremises 20,000Fixtures £4,000 + additions £800 4,800

24,800Current AssetsStock 11,000Debtors 1,800Prepayment 600

13,400Less Current LiabilitiesCreditors 3,300Bank overdraft 5,800Accrual 400

9,500Working Capital 3,900NET ASSETS 28,700

FINANCED BY:CapitalOpening capital 32,400Less Net loss 400

32,000Less Drawings £3,200 + goods £100 3,300

28,700

29

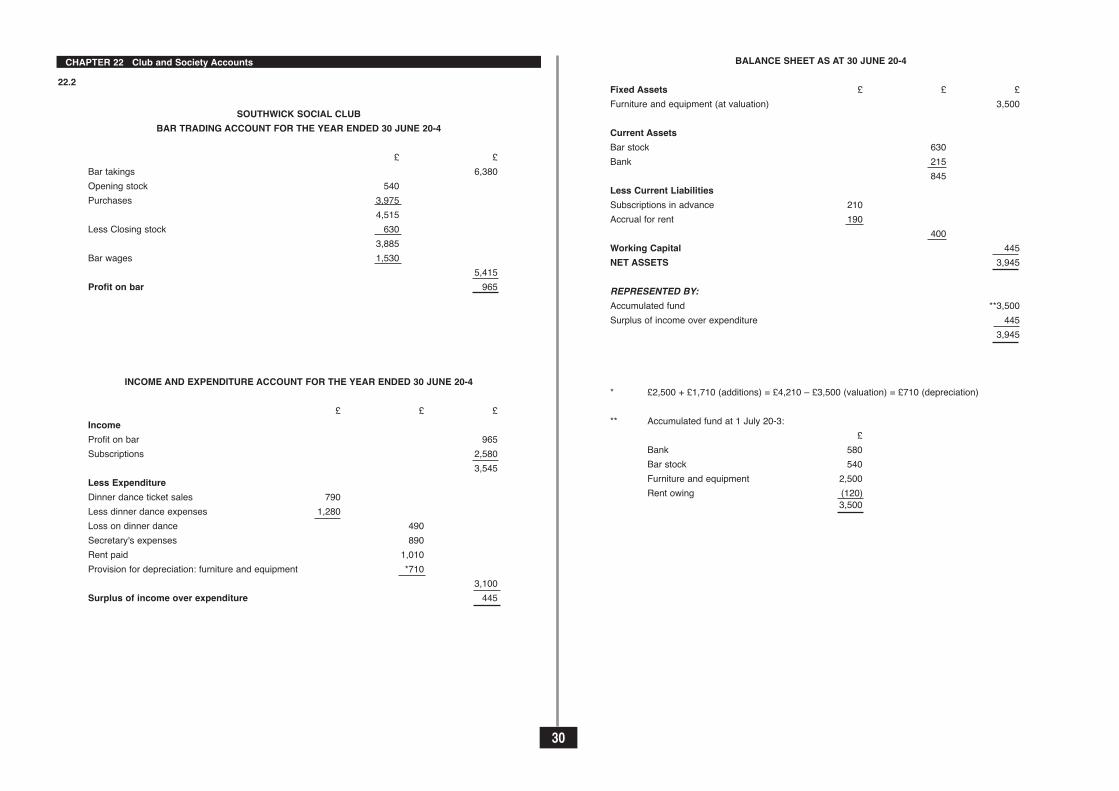

22.2

SOUTHWICK SOCIAL CLUBBAR TRADING ACCOUNT FOR THE YEAR ENDED 30 JUNE 20-4

£ £Bar takings 6,380Opening stock 540Purchases 3,975

4,515Less Closing stock 630

3,885Bar wages 1,530

5,415Profit on bar 965

INCOME AND EXPENDITURE ACCOUNT FOR THE YEAR ENDED 30 JUNE 20-4

£ £ £IncomeProfit on bar 965Subscriptions 2,580

3,545Less ExpenditureDinner dance ticket sales 790Less dinner dance expenses 1,280Loss on dinner dance 490Secretary's expenses 890Rent paid 1,010Provision for depreciation: furniture and equipment *710

3,100Surplus of income over expenditure 445

BALANCE SHEET AS AT 30 JUNE 20-4

Fixed Assets £ £ £Furniture and equipment (at valuation) 3,500

Current AssetsBar stock 630Bank 215

845Less Current LiabilitiesSubscriptions in advance 210Accrual for rent 190

400Working Capital 445NET ASSETS 3,945

REPRESENTED BY:Accumulated fund **3,500Surplus of income over expenditure 445

3,945

* £2,500 + £1,710 (additions) = £4,210 – £3,500 (valuation) = £710 (depreciation)

** Accumulated fund at 1 July 20-3:£

Bank 580 Bar stock 540 Furniture and equipment 2,500 Rent owing (120)

3,500

30

CHAPTER 22 Club and Society Accounts

22.4

BLANDFORD RAILWAY SOCIAL CLUBBAR TRADING ACCOUNT FOR THE YEAR ENDED 31 OCTOBER 20-6

£ £Bar sales 8,121Opening stock 342Purchases (note 1) 5,315

5,657Less Closing stock 312

5,345Bar wages 2,175

7,520Profit on bar 601

INCOME AND EXPENDITURE ACCOUNTFOR THE YEAR ENDED 31 OCTOBER 20-6

£ £IncomeProfit on bar 601Subscriptions (note 2) 10,357

10,958Less ExpenditureStationery 121Ground rent (note 3) 1,200Sundries 252Loss on sale of fittings 100Provision for depreciation: fixtures and fittings (note 4) 4,780

office equipment 2166,669

Surplus of income over expenditure 4,289

BALANCE SHEET AS AT 31 OCTOBER 20-6

£ £ £Fixed Assets Cost Dep'n to date NetClub house 62,000 – 62,000Fixtures and fittings 26,358 7,238 19,120Office equipment 1,200 336 864

89,558 7,584 81,984

Current AssetsBar stock 312Subscriptions in arrears 121Bank 4,100Cash 85

4,618

Less Current LiabilitiesCreditor 294Subscriptions prepaid 110Accrual for rent 400

804Working Capital 3,814NET ASSETS 85,798

REPRESENTED BY:Accumulated fund (note 5) 78,509Donations (note 6) 3,000Surplus of income over expenditure 4,289

85,798

Notes:

1. Bar purchases for year:£5,210 (payments) – £189 (opening creditor) + £294 (closing creditor) = £5,315

2.Dr Subscriptions Control Account Cr

20-5/20-6 £ 20-5/20-6 £1 Nov Balance b/d 1 Nov Balance b/d

(subscriptions owing) 68 (subscriptions prepaid) 19431 Oct Income and expenditure Cash 80

account (missing figure) 10,357 Bank 10,14031 Oct Balance c/d 31 Oct Balance c/d

(subscriptions prepaid) 110 (subscriptions owing) 12110,535 10,535

31

£ £3. Ground rent for year:

• charge for year (£100 per month for 12 months) 1,200• prepayment at start of year 200• amount paid during year 600

800• accrual at end of year 400

4. Provision for depreciation on fixtures and fittings:• at cost at start of year 15,000• less fittings sold 1,642

13,358• new fixtures 13,000• at cost at end of year 26,358• accumulated depreciation at start of year 3,000• less depreciation on fittings sold 542

2,458• net book value before depreciation for year 23,900

• depreciation for year (£23,900 x 20%) 4,780

5. Assets and liabilities at 1 November 20-5: £ £Club house 62,000Fixtures and fittings 12,000Office equipment 1,080Bank 3,142Cash 60Subscriptions in arrears 68Bar stock 342Prepayment for rent 200

78,892Less: Subscriptions prepaid 194

Creditor 189383

Accumulated fund at start of year 78,509

6. As donations would seem to be of a material amount (£3,000), they have been capitalised, ie recorded onthe balance sheet as an addition to the accumulated fund. An alternative accounting treatment would be torecord them as income in the income and expenditure account. As to which is used, it is for the treasurer touse his or her judgement in the application of the materiality concept.

23.3 (a)PERCH AND TROUT

PARTNERSHIP APPROPRIATION ACCOUNT FOR THE YEAR ENDED 30 SEPTEMBER 20-7

£ £Net profit 30,500Add interest charged on partners' drawings:

Perch 640Trout 910

1,55032,050

Less appropriation of profits:Salary: Trout 6,000Interest allowed on partners' capitals:

Perch 2,000Trout 1,500

3,50022,550

Share of remaining profits:Perch (60%) 13,530Trout (40%) 9,020

22,550

(b)

Dr Partners' Current Accounts Cr

20-6/20-7 Perch Trout 20-6/20-7 Perch Trout£ £ £ £

1 Oct Balance b/d – 3,400 1 Oct Balance b/d 1,800 –30 Sep Drawings 12,785 18,275 30 Sep Salary – 6,00030 Sep Interest on drawings 640 910 30 Sep Interest on capital 2,000 1,50030 Sep Balance c/d 3,905 – 30 Sep Share of profits 13,530 9,020

30 Sep Balance c/d 6,06517,330 22,585 17,330 22,585

20-7/20-8 20-7/20-81 Oct Balance b/d – 6,065 1 Oct Balance b/d 3,905 –

32

CHAPTER 23 Partnership Accounts

23.4 (a)TUIGAMALA AND TATUPU

PARTNERSHIP PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 DECEMBER

£ £Gross profit 24,000Add commission receivable 500

24,500Less expenses:

Insurances 1,000Wages and salaries 2,400Provision for depreciation: equipment 2,000

fixtures 1,0806,480

Net profit 18,020

(b)

PARTNERSHIP APPROPRIATION ACCOUNT FOR THE YEAR ENDED 31 DECEMBER

£ £Net profit 18,020Add interest charged on partners' drawings:

Tuigamala 80Tatupu 45

12518,145

Less appropriation of profits:Salary: Tatupu 3,745Interest allowed on partners' capitals:

Tuigamala 3,200Tatupu 1,200

4,40010,000

Share of remaining profits:Tuigamala (75%) 7,500Tatupu (25%) 2,500

10,000

(c)

Dr Partners' Current Accounts Cr

Tuigamala Tatupu Tuigamala Tatupu£ £ £ £

1 Jan Balance b/d 200 – 1 Jan Balance b/d – –31 Dec Drawings 1,600 900 31 Dec Salary – 3,74531 Dec Interest on drawings 80 45 31 Dec Interest on capital 3,200 1,20031 Dec Balances c/d 8,820 6,500 31 Dec Share of profits 7,500 2,500

10,700 7,445 10,700 7,445

1 Jan Balances b/d 8,820 6,500

(d)

PARTNERS' BALANCE SHEET AS AT 31 DECEMBER

£ £ £Fixed Assets Cost Dep'n to date NetPremises 40,000 – 40,000Equipment 20,000 4,000 16,000Fixtures 9,000 2,880 6,120

69,000 6,880 62,120

Current AssetsDebtors 16,000Less Provision for bad debts 320

15,680Income accrual 300Prepayment 150Cash 450

16,580Less Current LiabilitiesCreditors 7,500Accrual 50Bank overdraft 830

8,380Working Capital 8,200NET ASSETS 70,320

FINANCED BY:Capital AccountsTuigamala 40,000Tatupu 15,000

55,000Current AccountsTuigamala 8,820Tatupu 6,500

15,32070,320

33

24.2 (a)

Dr Revaluation Account Cr

Year 8 £ Year 8 £31 Dec Bad debt written off 1,200 31 Dec Goodwill 5,000

Stock 300 Buildings 7,800Capital accounts:Northwood (60%) 6,780Varley (40%) 4,520

12,800 12,800

(b)

Dr Bank Account Cr

Year 8 £ Year 8 £31 Dec Balance b/d 8,080 31 Dec Northwood (see workings below) 43,140

Year 9 Year 91 Jan Rodger: capital account 40,000 1 Jan Balance c/d 4,940

48,080 48,080

1 Jan Balance b/d 4,940

Note: £Northwood's capital account 82,000Northwood's current account 4,360Share of revaluation account 6,780

93,140Less Loan to new partnership 50,000Amount paid from partnership bank account 43,140

(c)

Dr Goodwill Account Cr

Year 8 £ Year 8 £31 Dec Balance b/d 18,00031 Dec Revaluation 5,000

Year 9 Year 91 Jan Rodger: capital account 8,000 1 Jan Varley: capital account (80%) 24,800

Rodger: capital account (20%) 6,20031,000 31,000

(d)

VARLEY AND RODGER, IN PARTNERSHIPBALANCE SHEET AS AT 1 JANUARY YEAR 9

£ £Fixed AssetsBuildings 80,000Fixtures and fittings 21,800Car 12,000

113,800Current AssetsStock 12,420Debtors 14,100Bank 4,940

31,460Less Current LiabilitiesCreditors 7,400Working Capital 24,060

137,860Less Long-term LiabilitiesLoan account: Northwood 50,000

87,860

FINANCED BY:Capital AccountsVarley £52,000 + £4,520 – £24,800 31,720Rodger £12,000 + £40,000 + £8,000 – £6,200 53,800

85,520Current AccountVarley 2,340

87,860

34

CHAPTER 24 Changes in Partnerships

35

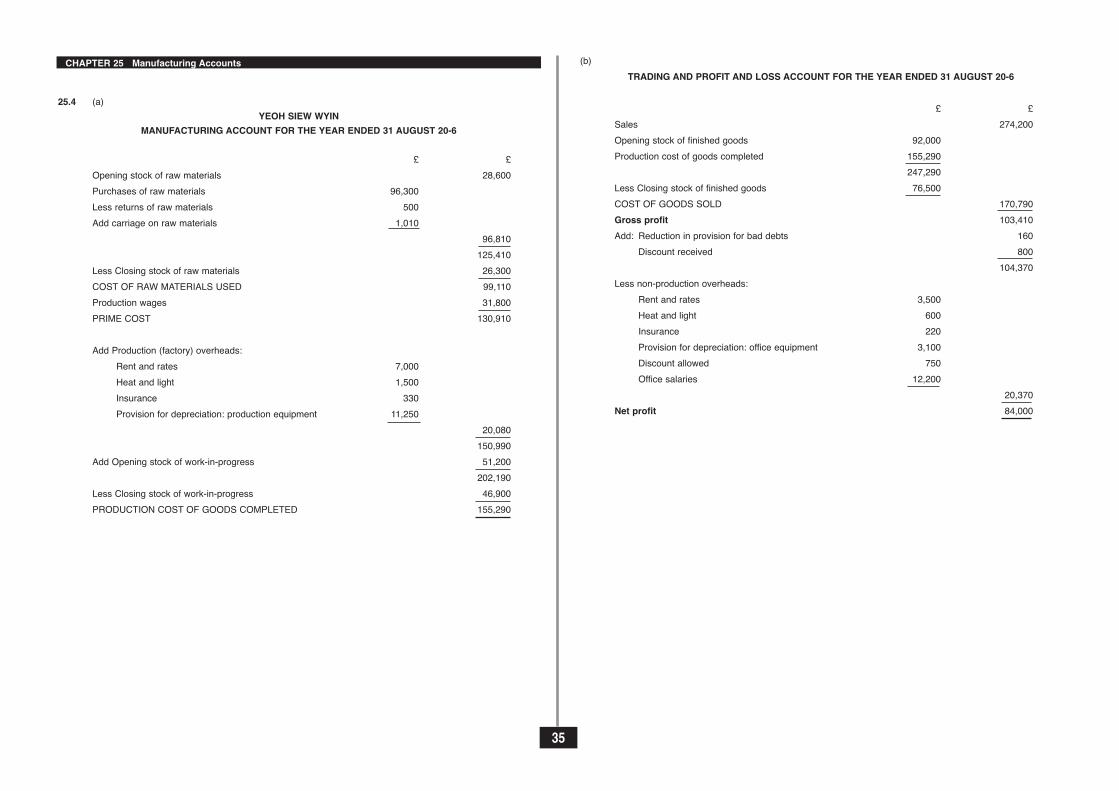

25.4 (a)YEOH SIEW WYIN

MANUFACTURING ACCOUNT FOR THE YEAR ENDED 31 AUGUST 20-6

£ £Opening stock of raw materials 28,600Purchases of raw materials 96,300Less returns of raw materials 500Add carriage on raw materials 1,010

96,810125,410

Less Closing stock of raw materials 26,300COST OF RAW MATERIALS USED 99,110Production wages 31,800PRIME COST 130,910

Add Production (factory) overheads:Rent and rates 7,000Heat and light 1,500Insurance 330Provision for depreciation: production equipment 11,250

20,080150,990

Add Opening stock of work-in-progress 51,200202,190

Less Closing stock of work-in-progress 46,900PRODUCTION COST OF GOODS COMPLETED 155,290

CHAPTER 25 Manufacturing Accounts (b)TRADING AND PROFIT AND LOSS ACCOUNT FOR THE YEAR ENDED 31 AUGUST 20-6

£ £Sales 274,200Opening stock of finished goods 92,000Production cost of goods completed 155,290

247,290Less Closing stock of finished goods 76,500COST OF GOODS SOLD 170,790Gross profit 103,410Add: Reduction in provision for bad debts 160

Discount received 800104,370

Less non-production overheads:Rent and rates 3,500Heat and light 600Insurance 220Provision for depreciation: office equipment 3,100Discount allowed 750Office salaries 12,200

20,370Net profit 84,000

36

25.5 (a) TAMSIN AUSTENMANUFACTURING, TRADING AND PROFIT AND LOSS ACCOUNT

FOR THE YEAR ENDED 31 DECEMBER 20-3

£ £ £Opening stock of raw materials 6,244Add Purchases of raw materials 110,335

116,579Less Closing stock of raw materials 7,183COST OF RAW MATERIALS USED 109,396Factory direct wages 47,317PRIME COST 156,713Add Production overheads:

Factory indirect wages 19,852Provision for depreciation: factory premises 4,400Provision for depreciation: plant and machinery 12,900

37,152PRODUCTION COST OF GOODS COMPLETED 193,865Sales 347,168

Opening stock of finished goods 10,084Production cost of goods completed 193,865

203,949Less Closing stock of finished goods 12,046COST OF GOODS SOLD 191,903Gross profit 155,265

Less Non-production overheads:Selling and distribution expenses 53,166Provision for depreciation: delivery vans 3,875

57,041Administration expenses 39,995Finance costs 3,511

100,547Net profit 54,718

(b)BALANCE SHEET AS AT 31 DECEMBER 20-3

Fixed Assets Cost Dep'n to date Net£ £ £

Factory premises 220,000 22,000 198,000Plant and machinery 115,500 77,400 38,100Delivery vans 33,000 19,375 13,625

368,500 118,775 249,725

Current AssetsStocks: raw materials 7,183

finished goods 12,04619,229

Debtors 36,410Prepayment 596

56,235

Less Current LiabilitiesCreditors 15,827Accrual 1,274Bank 34,864

51,965Working Capital 4,270NET ASSETS 253,995

FINANCED BY:CapitalOpening capital 199,277Add Net Profit 54,718

253,995

37

26.1 (a) MASON MOTORS LIMITEDSTATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20-1

£Retained earningsBalance at 1 January 20-1 100,000Profit for the year 75,000

175,000Less Dividends paid 10,000Less Transfer to general reserve 20,000Balance at 31 December 20-1 145,000

(b) The £20,000 transferred to general reserve has been earned as profits and belongs to the shareholders.It is represented by assets in the statement of financial position and is not a bank balance available torebuild the garage forecourt.

26.5 PLAYFAIR LTDINCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 20-3

£ £Revenue 2,340,000Opening inventories 250,000Purchases 1,650,000Less Closing inventories 280,000Cost of Goods Sold 1,620,000Gross profit 720,000Less Overheads:Administrative expenses 210,000Distribution costs 320,000

530,000Profit from operations 190,000Less Finance costs 40,000Profit before tax 150,000Less Tax 30,000Profit for the year 120,000

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 20-3

£Retained earningsBalance at 1 January 20-3 540,000Profit for the year 120,000

660,000Less Dividends paid 50,000Balance at 31 December 20-3 610,000

CHAPTER 26 Limited Company Financial Statements STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 20-3

Cost Dep’n Net£ £ £

Non-current Assets

Land 500,000 – 500,000

Plant and equipment 800,000 390,000 410,000

1,300,000 390,000 910,000

Current Assets

Inventories 280,000

Trade and other receivables 350,000

Cash and cash equivalents 140,000

770,000

Less Current LiabilitiesTrade and other payables 210,000

Tax liability 30,000

240,000

Net Current Assets 530,000

1,440,000

Less Non-current LiabilitiesLong-term loan 200,000

NET ASSETS 1,240,000

EQUITY

Issued share capital (£1 ordinary shares) 580,000

Share premium 50,000

Retained earnings 610,000

TOTAL EQUITY 1,240,000

continued

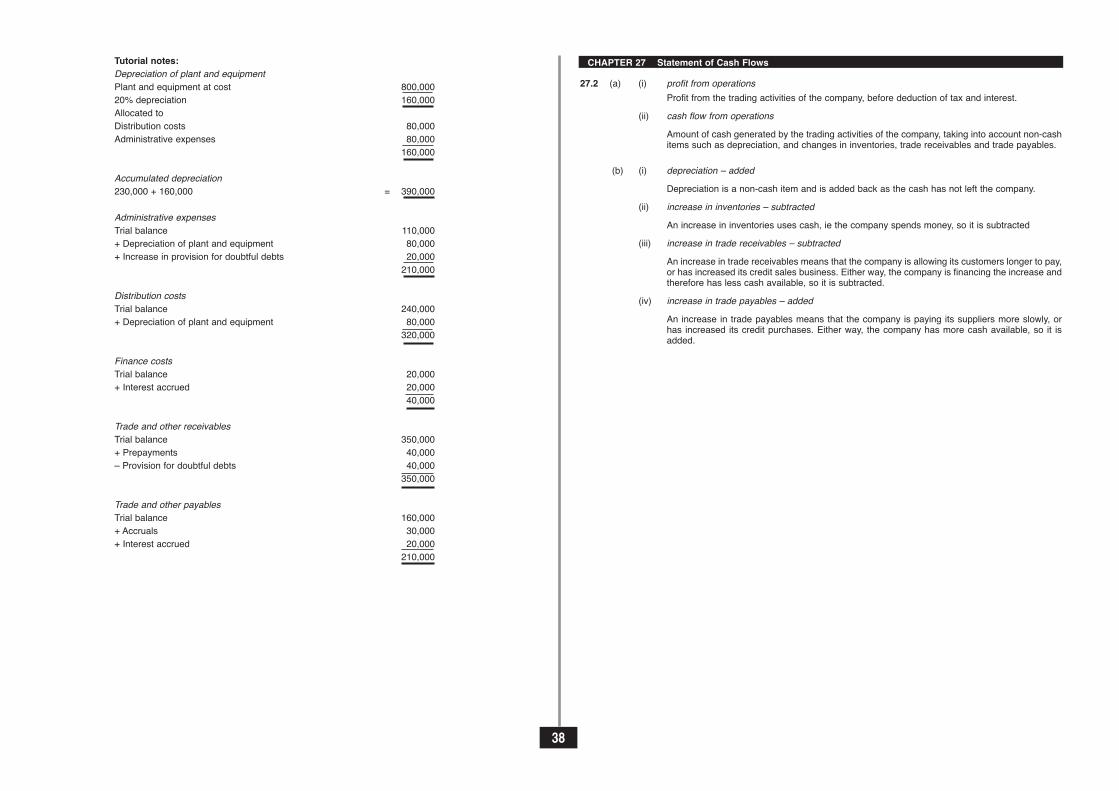

27.2 (a) (i) profit from operationsProfit from the trading activities of the company, before deduction of tax and interest.

(ii) cash flow from operationsAmount of cash generated by the trading activities of the company, taking into account non-cashitems such as depreciation, and changes in inventories, trade receivables and trade payables.

(b) (i) depreciation – addedDepreciation is a non-cash item and is added back as the cash has not left the company.

(ii) increase in inventories – subtractedAn increase in inventories uses cash, ie the company spends money, so it is subtracted

(iii) increase in trade receivables – subtractedAn increase in trade receivables means that the company is allowing its customers longer to pay,or has increased its credit sales business. Either way, the company is financing the increase andtherefore has less cash available, so it is subtracted.

(iv) increase in trade payables – addedAn increase in trade payables means that the company is paying its suppliers more slowly, orhas increased its credit purchases. Either way, the company has more cash available, so it isadded.

38

CHAPTER 27 Statement of Cash FlowsTutorial notes:Depreciation of plant and equipmentPlant and equipment at cost 800,00020% depreciation 160,000Allocated toDistribution costs 80,000Administrative expenses 80,000

160,000

Accumulated depreciation230,000 + 160,000 = 390,000

Administrative expensesTrial balance 110,000+ Depreciation of plant and equipment 80,000+ Increase in provision for doubtful debts 20,000

210,000

Distribution costsTrial balance 240,000+ Depreciation of plant and equipment 80,000

320,000

Finance costsTrial balance 20,000+ Interest accrued 20,000

40,000

Trade and other receivablesTrial balance 350,000+ Prepayments 40,000– Provision for doubtful debts 40,000

350,000

Trade and other payablesTrial balance 160,000+ Accruals 30,000+ Interest accrued 20,000

210,000

27.5

WILLIAMS LIMITED

STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 30 SEPTEMBER 20-6

£ £

Net cash (used in)/ from operating activities (see below) 21,500

Cash flows from investing activities

Purchase of non-current assets (10,000)

Net cash (used in)/ from investing activities (10,000)

Cash flows from financing activities

Repayment of long-term borrowings (bank loan) (7,000)

Dividends paid (8,200)

Net cash (used in)/ from financing activities (15,200)

Net increase/(decrease) in cash and cash equivalents (3,700)

Cash and cash equivalents at beginning of year (1,000)

Cash and cash equivalents at end of year (4,700)

Reconciliation of profit from operations to net cash flow from operating activities £

Profit from operations (before tax and interest) 12,700

Adjustments for:

Depreciation for year 11,600

Increase in inventories (3,800)

Increase in trade receivables (4,200)

Increase in trade payables 7,400

Cash (used in)/from operations 23,700

Interest paid (2,200)

Income taxes paid –

Net cash (used in)/ from operating activities 21,500

39

27.4

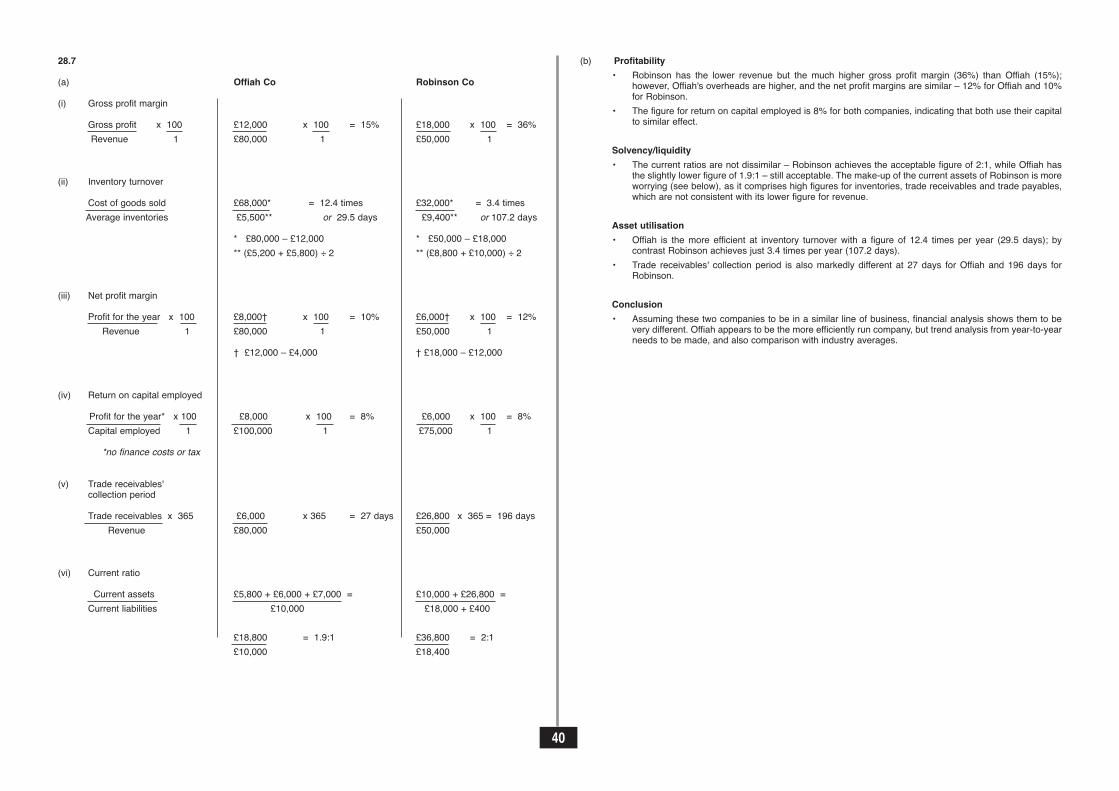

28.4 Business A Business B(a) gross profit percentage 13.4% 44.0%(b) net profit percentage 1.4% 4.2%(c) inventory turnover 33 days or 95 days or

10.9 times per year 3.8 times per year(d) current ratio 1.3:1 2.4:1(e) liquid capital ratio 0.05:1 1.3:1(f) trade receviables’ collection period 1 day* 60 days(g) return on capital employed 11% 8.1%* revenue figure used for this calculation; this is unrealistic because most supermarket sales will be for cashrather than on creditBusiness A is a grocery supermarket chain; business B the heavy engineering companyReasons:Business A low net profit percentage; high inventory turnover; short trade receivables’ collection period,