bulletin no. 2012-28 highlights of this issue · highlights of this issue these synopses are...

TRANSCRIPT

Bulletin No. 2012-28July 9, 2012

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

Rev. Rul. 2012–19, page 16.Dividends and dividend equivalents on restricted stockand restricted stock units. This ruling addresses whetherdividends and dividend equivalents relating to restricted stockand restricted stock units that are performance-based com-pensation under section 162(m)(4)(C) of the Code must sepa-rately satisfy the requirements under section 162(m)(4)(C) tobe treated as performance-based compensation.

T.D. 9591, page 32.Final regulations under section 7874 of the Code provide rulesfor determining whether a foreign corporation is a surrogateforeign corporation. Specifically, the regulation explains whenthere is an indirect acquisition of a domestic corporation’s prop-erties for purposes of section 7874(a)(2)(B). In addition, theregulation includes a rule that in certain situations, a publiclytraded partnership may be treated as a surrogate foreign cor-poration. The regulation also provides rules for the treatmentof options of the surrogate foreign corporation for purposes ofsection 7874(a)(2)(B)(ii).

T.D. 9592, page 41.REG–107889–12, page 53.Temporary and proposed regulations under section 7874 ofthe Code provide guidance regarding whether a foreign corpo-ration has substantial business activities in the foreign countryin which, or under the law of which, the foreign corporation iscreated or organized.

Notice 2012–44, page 45.This notice provides guidance regarding certain qualified con-servation purposes eligible for financing with qualified energyconservation bonds under section 54D of the Code, particu-

larly (1) how to measure reductions of energy consumption inpublicly-owned buildings by at least 20 percent, and (2) whatconstitutes a “green community program.”

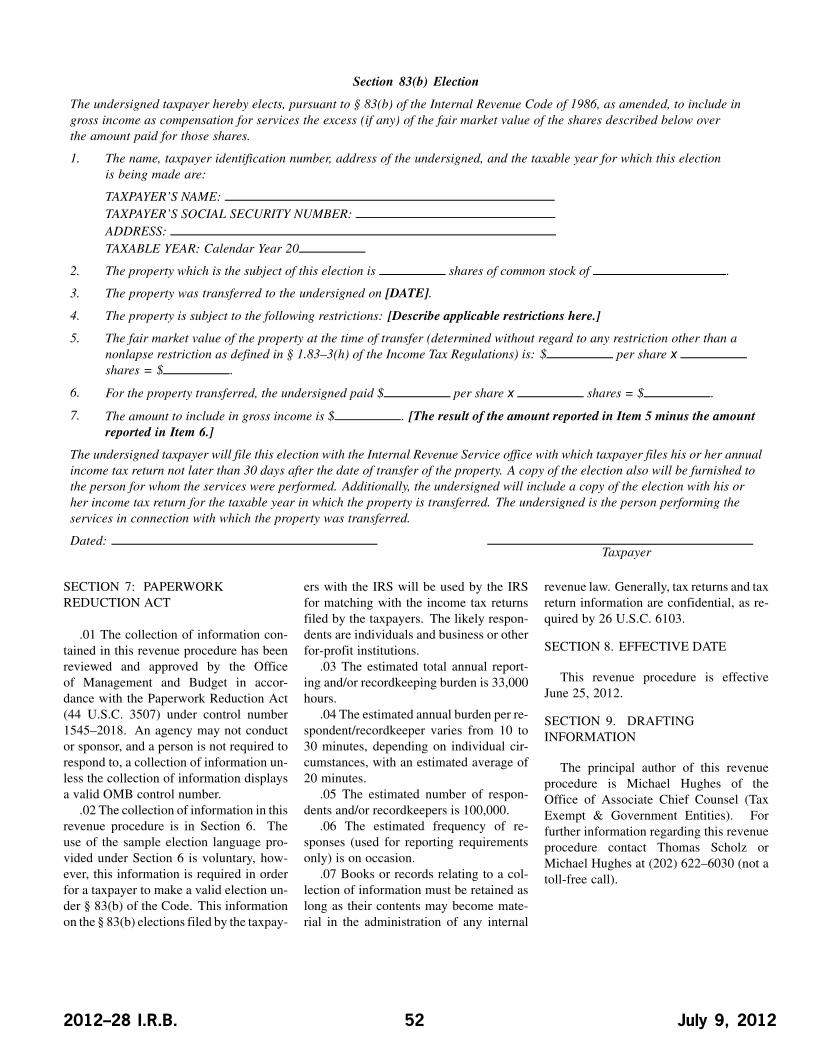

Rev. Proc. 2012–29, page 49.This procedure provides sample language that may be used(but is not required to be used) for making an election undersection 83(b) of the Code. Additionally, the procedure providesexamples of the income tax consequences of making such anelection.

EMPLOYEE PLANS

Rev. Rul. 2012–19, page 16.Dividends and dividend equivalents on restricted stockand restricted stock units. This ruling addresses whetherdividends and dividend equivalents relating to restricted stockand restricted stock units that are performance-based com-pensation under section 162(m)(4)(C) of the Code must sepa-rately satisfy the requirements under section 162(m)(4)(C) tobe treated as performance-based compensation.

Rev. Proc. 2012–29, page 49.This procedure provides sample language that may be used(but is not required to be used) for making an election undersection 83(b) of the Code. Additionally, the procedure providesexamples of the income tax consequences of making such anelection.

(Continued on the next page)

Finding Lists begin on page ii.

ESTATE TAX

T.D. 9593, page 17.REG–141832–11, page 54.Temporary and proposed regulations under section 2010 ofthe Code provide rules for determining the applicable creditamount and applicable exclusion amount allowed to the estateof a decedent against the gift or estate tax. In addition, theregulations provide rules for electing portability of a deceasedspousal unused exclusion amount to the surviving spouse andrules regarding the surviving spouse’s use of this amount. Theportability rules apply to married spouses where the death ofthe first spouse to die occurs on or after January 1, 2011.

GIFT TAX

T.D. 9593, page 17.REG–141832–11, page 54.Temporary and proposed regulations under section 2010 ofthe Code provide rules for determining the applicable creditamount and applicable exclusion amount allowed to the estateof a decedent against the gift or estate tax. In addition, theregulations provide rules for electing portability of a deceasedspousal unused exclusion amount to the surviving spouse andrules regarding the surviving spouse’s use of this amount. Theportability rules apply to married spouses where the death ofthe first spouse to die occurs on or after January 1, 2011.

July 9, 2012 2012–28 I.R.B.

The IRS MissionProvide America’s taxpayers top-quality service by helpingthem understand and meet their tax responsibilities and en-

force the law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly and may be obtained from theSuperintendent of Documents on a subscription basis. Bulletincontents are compiled semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, mod-ify, or amend any of those previously published in the Bulletin.All published rulings apply retroactively unless otherwise indi-cated. Procedures relating solely to matters of internal man-agement are not published; however, statements of internalpractices and procedures that affect the rights and duties oftaxpayers are published.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpayersor technical advice to Service field offices, identifying detailsand information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,

court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautionedagainst reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A,Tax Conventions and Other Related Items, and Subpart B, Leg-islation and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Secre-tary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative indexfor the matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

2012–28 I.R.B. July 9, 2012

July 9, 2012 2012–28 I.R.B.

Part I. Rulings and Decisions Under the Internal Revenue Codeof 1986Section 83.—PropertyTransferred in ConnectionWith Performance ofServices

The revenue procedures contains sample languagethat may be used (but is not required to be used) formaking an election under section 83(b) of the InternalRevenue Code. Additionally, the revenue procedureprovides examples of the income tax consequencesof making such an election. See Rev. Proc. 2012-29,page 49.

Section 162.—Dividendsand Dividend Equivalentson Restricted Stock andRestricted Stock Units26 CFR 1.162–27: Certain employee remunerationin excess of $1,000,000.

Dividends and dividend equivalentson restricted stock and restricted stockunits. This ruling addresses whether divi-dends and dividend equivalents relating torestricted stock and restricted stock unitsthat are performance-based compensationunder section 162(m)(4)(C) of the Codemust separately satisfy the requirementsunder section 162(m)(4)(C) to be treated asperformance-based compensation.

Rev. Rul. 2012–19

ISSUE

Whether dividends and dividend equiv-alents relating to restricted stock andrestricted stock units (RSUs) that areperformance-based compensation under§ 162(m)(4)(C) of the Internal RevenueCode must separately satisfy the require-ments under § 162(m)(4)(C) to be treatedas performance-based compensation.

FACTS

Corporation X and Corporation Yare publicly held corporations withinthe meaning of § 162(m)(2). Both cor-porations maintain plans under whichparticipating employees may be grantedrestricted common stock of the respec-tive corporation or RSUs based upon thecommon stock of the respective corpo-ration. The restricted stock and RSUs

granted under the plans of CorporationsX and Y vest upon the attainment of cer-tain preestablished, objective performancegoals and otherwise meet the require-ments of § 1.162–27(e). Accordingly, thecompensation received due to the vest-ing of the restricted stock and the vestingand payment of the RSUs is qualifiedperformance-based compensation that isexcluded from the applicable employeeremuneration to which the deduction limi-tation under § 162(m) applies.

Situation 1. Corporation X’s plan pro-vides that dividends and dividend equiv-alents otherwise payable to an employeeduring the period from grant through vest-ing with respect to performance-basedrestricted stock and RSU awards grantedto the employee are accumulated andbecome vested and payable only if therelated performance goals with respect tothe restricted stock and RSUs are satisfied.All other requirements of § 1.162–27(e)are met with respect to the grant of rightsto dividends and dividend equivalents.

Situation 2. Corporation Y’s planprovides for payment to an employee dur-ing the period from grant to vesting ofdividends and dividend equivalents withrespect to performance-based restrictedstock and RSU awards granted to the em-ployee at the same time dividends are paidon common stock of Corporation Y re-gardless of whether the performance goalsestablished with respect to the restrictedstock and RSUs are satisfied.

LAW

Section 162(a)(1) allows as a deductionall the ordinary and necessary expensespaid or incurred during the taxable year incarrying on any trade or business, includ-ing a reasonable allowance for salaries orother compensation for personal servicesactually rendered.

Section 162(m)(1) provides that in thecase of any publicly held corporation, nodeduction is allowed for applicable em-ployee remuneration with respect to anycovered employee to the extent that theamount of the remuneration for the taxableyear exceeds $1,000,000.

Section 162(m)(3) provides that theterm “covered employee” means any em-ployee of the taxpayer if (i) as of the closeof the taxable year, such employee is thechief executive officer of the taxpayer oris an individual acting in such a capac-ity, or (ii) the total compensation of suchemployee for the taxable year is requiredto be reported to shareholders under theSecurities Exchange Act of 1934 (Ex-change Act) by reason of such employeebeing among the four highest compensatedofficers for the taxable year (other thanthe chief executive officer). See Notice2007–49, 2007–1 C.B. 1429 (providingchanges to the application of this provi-sion based on changes in the ExchangeAct compensation disclosure rules).

Section 162(m)(4)(A) defines “applica-ble employee remuneration,” with respectto any covered employee for any taxableyear, generally as the aggregate amount al-lowable as a deduction for the taxable year(determined without regard to § 162(m))for remuneration for services performedby the employee (whether or not during thetaxable year).

Section 162(m)(4)(C) provides that ap-plicable employee remuneration does notinclude any remuneration payable solelyon account of the attainment of one ormore performance goals, but only if (i)the performance goals are determined bya compensation committee of the board ofdirectors of the taxpayer which is com-prised solely of two or more outside direc-tors, (ii) the material terms under which theremuneration is to be paid, including theperformance goals, are disclosed to share-holders and approved by a majority of thevote in a separate shareholder vote beforepayment of such remuneration, and (iii)before any payment of such remuneration,the compensation committee certifies thatthe performance goals and other materialterms were in fact satisfied. Rules with re-spect to these requirements are set forth in§§ 1.162–27(e)(2) through (e)(5).

Section 1.162–27(e)(2)(i) provides thatqualified performance-based compensa-tion must be paid solely on account ofthe attainment of one or more preestab-lished, objective performance goals. Sec-tion 1.162–27–(e)(2)(ii) provides that a

2012–28 I.R.B. 16 July 9, 2012

preestablished performance goal muststate, in terms of an objective formula orstandard, the method for computing theamount of compensation payable to theemployee if the goal is attained.

Section 1.162–27(e)(2)(iv) providesthat the determination of whether com-pensation satisfies the requirementsof § 1.162–27(e)(2) generally is madeon a grant-by-grant basis. Section1.162–27(e)(2)(iv) further provides that,except as provided in § 1.162–27(e)(2)(vi)(relating to stock options and stock ap-preciation rights), whether a grant ofrestricted stock or other stock-based com-pensation satisfies the performance goalrequirements is determined without regardto whether dividends, dividend equiva-lents, or other similar distributions withrespect to stock, on such stock-basedcompensation are payable prior to theattainment of the performance goal. Div-idends, dividend equivalents, or othersimilar distributions with respect to stockthat are treated as separate grants un-der § 1.162–27(e)(2)(iv) are not perfor-mance-based compensation unless theyseparately satisfy the performance goalrequirements. Such performance goalsmay or may not be the same as the per-formance goals for the related stock-basedcompensation.

ANALYSIS

Under § 1.162–27(e)(2)(iv), the divi-dends and dividend equivalents under Cor-poration X’s plan and under CorporationY’s plan are grants of compensation thatare separate and apart from the related re-stricted stock and RSU grants. Therefore,the grants of the dividends and dividendequivalents must separately satisfy the re-quirements of § 1.162–27(e) to be quali-fied performance-based compensation.

Situation 1. Under Corporation X’splan, participants’ rights to restrictedstock and RSUs are subject to perfor-mance goals that meet the requirementsof § 1.162–27(e) and are excluded fromapplicable remuneration for purposes ofapplying the § 162(m)(1) deduction limi-tation. Under the same plan, participants’rights to dividends and dividend equiv-alents vest and become payable only if

the same performance goals that applyto the related grants of restricted stockand RSUs are satisfied. Therefore, divi-dends and dividend equivalents under X’splan are also excluded from applicableremuneration for purposes of applying the§ 162(m)(1) deduction limitation.

Situation 2. The dividends and div-idend equivalents under Corporation Y’splan fail to satisfy the requirements un-der § 162(m)(4)(C) and § 1.162–27(e) be-cause the rights to these amounts do notvest and become payable solely on accountof the attainment of preestablished perfor-mance goals. Thus, these amounts arenot qualified performance-based compen-sation, regardless of whether the perfor-mance goals are met with respect to the re-lated restricted stock and RSUs.

HOLDINGS

Situation 1. With respect to Corpora-tion X, dividends and dividend equivalentspaid under X’s plan are qualified-perfor-mance based compensation and thereforeare excluded from applicable employee re-muneration for purposes of applying the$1,000,000 limitation on deductibility un-der § 162(m)(1).

Situation 2. With respect to Corpora-tion Y, dividends and dividend equivalentspaid under Y’s plan are not qualified-per-formance based compensation and there-fore are included in applicable employeeremuneration for purposes of applying the$1,000,000 limitation on deductibility un-der § 162(m)(1).

DRAFTING INFORMATION

This revenue ruling was prepared byDara Alderman of the Office of the Di-vision Counsel/Associate Chief Counsel(Tax Exempt & Government Entities). Forfurther information regarding this revenueruling, contact Ms. Alderman at (202)622–6030 (not a toll-free call).

Section 2010.—UnifiedCredit Against Estate Tax26 CFR 20.2001–2T: Valuation of adjusted tax-able gifts for purposes of determining the deceasedspousal unused exclusion amount of last deceasedspouse (temporary).

T.D. 9593

DEPARTMENT OF THETREASURYInternal Revenue Service26 CFR Parts 20, 25, and 602

Portability of a DeceasedSpousal Unused ExclusionAmount

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Temporary regulations.

SUMMARY: This document contains tem-porary regulations that provide guidanceon the estate and gift tax applicable ex-clusion amount, in general, as well as onthe applicable requirements for electingportability of a deceased spousal unusedexclusion (DSUE) amount to the surviv-ing spouse and on the applicable rules forthe surviving spouse’s use of this DSUEamount. The statutory provisions under-lying the portability rules were enacted aspart of the Tax Relief, Unemployment In-surance Reauthorization, and Job CreationAct of 2010. The portability rules affectmarried spouses where the death of thefirst spouse to die occurs on or after Jan-uary 1, 2011. The text of the temporaryregulations also serves as the text of pro-posed regulations (REG–141832–11) setforth in the notice of proposed rulemakingon this subject appearing elsewhere in thisissue of the Bulletin.

DATES: Effective Date: These regulationsare effective on June 15, 2012.

Applicability Dates: Sections ofthe temporary regulation relating toportability of a deceased spousal unusedexclusion amount apply to estates ofdecedents dying on or after January 1,2011. For specific dates of applicability,see §§20.2001–2T(b), 20.2010–1T(e),20.2010–2T(e), 20.2010–3T(f),25.2505–1T(e), and 25.2505–2T(g).

FOR FURTHER INFORMATIONCONTACT: Karlene Lesho (202)622–3090 (not a toll-free number).

July 9, 2012 17 2012–28 I.R.B.

SUPPLEMENTARY INFORMATION:

Paperwork Reduction Act

The collection of information containedin these regulations has been reviewed and,pending receipt and evaluation of publiccomments, approved by the Office of Man-agement and Budget under control num-ber 1545–0015. Responses to this collec-tion of information are voluntary to obtainthe benefit of being able to elect portabil-ity or to take advantage of the special re-porting requirements applicable to certainassets, and, for certain estates, to opt out ofa deemed portability election.

An agency may not conduct or sponsor,and a person is not required to respond to, acollection of information unless the collec-tion of information displays a valid controlnumber. For further information concern-ing this collection of information, and theaddress for the submission of comments onthe collection of information and the accu-racy of the estimated burden, and sugges-tions for reducing this burden, please re-fer to the preamble of the cross-referencingnotice of proposed rulemaking publishedin this issue of the Bulletin.

Books and records relating to a collec-tion of information must be retained aslong as their contents may become mate-rial in the administration of any internalrevenue law. Generally, tax returns and taxreturn information are confidential, as re-quired by 26 U.S.C. 6103.

Background

On December 17, 2010, in section303 of the Tax Relief, UnemploymentInsurance Reauthorization, and Job Cre-ation Act of 2010, Public Law 111–312(124 Stat. 3296, 3302) (TRUIRJCA),Congress amended section 2010(c) of theInternal Revenue Code (Code) to allowportability of the applicable exclusionamount between spouses, and it madeconforming amendments to sections2505(a), 2631(c), and 6018(a)(1) of theCode. Section 303 of TRUIRJCA directsthe Secretary to issue such regulations asmay be necessary or appropriate to carryout section 303(a) of TRUIRJCA.

This document contains amendmentsto the Estate Tax Regulations (26 CFRpart 20) under sections 2001 and 2010of the Code and to the Gift Tax Regula-tions (26 CFR part 25) under section 2505

of the Code. The temporary regulationsaddress not only the amendments madeto section 2010(c) by TRUIRJCA andthe conforming amendment to section2505(a), but also the entirety of sections2010 and 2505 of the Code for which thereare no existing regulations. Finally, theamendment to the Estate Tax Regulationsunder section 2001 of the Code clarifiesthe application of the rule in section2010(c)(5)(B) to section 2001 of the Code.

Section 303(a) of TRUIRJCA

Section 303(a) of TRUIRJCA amendssection 2010(c) of the Code by strik-ing paragraph (2) of section 2010(c) andadding new paragraphs (2) through (6) ofsection 2010(c). Section 2010(c)(2) nowdefines the applicable exclusion amount,used to determine the applicable creditamount, as the sum of the basic exclu-sion amount and, in the case of a surviv-ing spouse, the DSUE amount. Section2010(c)(3) provides that the basic exclu-sion amount is $5,000,000, to be adjustedfor inflation in each year after calendaryear 2011. Section 2010(c)(4) defines theDSUE amount to mean the lesser of (A)the basic exclusion amount or (B) the ba-sic exclusion amount of the last deceasedspouse of the surviving spouse, less theamount with respect to which the tentativetax is determined under section 2001(b)(1)on the estate of such deceased spouse.

Section 2010(c)(5) describes specialrules relating to the portability of a DSUEamount. Section 2010(c)(5)(A) providescertain requirements that must be metto allow a surviving spouse to take intoaccount a DSUE amount of a deceasedspouse. In particular, the executor of theestate of the deceased spouse must filean estate tax return, compute the DSUEamount on such return, elect portabilityof the DSUE amount on such return, andensure that such return is filed within thetime prescribed by law (including ex-tensions) for filing such return. Section2010(c)(5)(B) allows the Secretary to ex-amine a return of the deceased spouse todetermine the DSUE amount, even afterthe expiration of the time provided undersection 6501 for assessing a tax underchapter 11 or 12.

Section 2010(c)(6) directs the Secretaryto prescribe regulations as may be nec-

essary or appropriate to carry out section2010(c).

Notice 2011–82

On October 17, 2011, the Departmentof the Treasury (Treasury) and the IRSissued Notice 2011–82, 2011–42 I.R.B.516, which can be found on www.IRS.gov.Notice 2011–82 alerts taxpayers to therequirements for the estate of a deceasedspouse to elect portability of a DSUEamount. In addition, Notice 2011–82announces that the estate of a deceasedspouse will be deemed to elect portabilityof the DSUE amount by timely filing acomplete and properly-prepared estate taxreturn, and that such return will be deemedto include a computation of the DSUEamount until such time as the IRS revisesthe estate tax return to expressly containthe DSUE amount computation. Notice2011–82 also provides guidance to theestates of deceased spouses who choosenot to make the portability election. No-tice 2011–82 announces that Treasuryand the IRS intend to issue regulationsto implement section 303 of TRUIRJCA.Accordingly, Treasury and the IRS invitedcomments on a number of specific issues.Treasury and the IRS received commentson these issues, as well as additional issuesidentified by commenters. The commentsare discussed in more detail in the “Ex-planation of Provisions” section of thispreamble.

Notice 2012–21

On March 3, 2012, Treasury and theIRS issued Notice 2012–21, 2012–10I.R.B. 450, which can be found onwww.IRS.gov. Notice 2012–21 grants toqualifying estates a six-month extension oftime for filing an estate tax return to electportability of an unused exclusion amountprovided that the qualifying estate filesForm 4768, “Application for Extension ofTime to File a Return and/or Pay U.S. Es-tate (and Generation-Skipping Transfer)Taxes,” within 15 months of the decedent’sdeath. A qualifying estate is the estate ofa person who died, survived by a spouse,during the first half of calendar year 2011,and whose gross estate has a fair marketvalue that does not exceed $5 million.With the extension granted by this notice,the estate tax return must be filed within15 months of the decedent’s death.

2012–28 I.R.B. 18 July 9, 2012

Explanation of Provisions

1. Rules in Section 2010(a), (b), and (d)of the Code

The temporary regulations in§20.2010–1T(a) state the general rule ofsection 2010(a) that an applicable creditamount will be allowed to the estate ofevery decedent against the estate tax im-posed by section 2001. The temporaryregulations in §20.2010–1T(b) incorpo-rate the rule in section 2010(b) relatingto an adjustment to the applicable creditamount for certain gifts made before 1977.Finally, as provided in section 2010(d), thetemporary regulations in §20.2010–1T(c)limit the amount of the allowable credit sothat it does not exceed the amount of theestate tax imposed by section 2001.

2. Explanation of Applicable Terms

The temporary regulations in§20.2010–1T(d) define terms relevant tocomputing the credit amount allowableunder section 2010. The relevant termsinclude applicable credit amount, appli-cable exclusion amount, basic exclusionamount, DSUE amount, and last deceasedspouse.

3. Making the Portability Election

a. Election Required on Estate Tax Return

The temporary regulations in§20.2010–2T(a) require an executor elect-ing portability to make that election ona timely-filed estate tax return. The lastreturn filed by the due date of the return,including extensions actually granted,will supersede any previously-filed re-turn. Thus, an executor may supersedea previously-filed portability electionon a subsequent timely-filed estate taxreturn if the executor satisfies the require-ment in §20.2010–2T(a)(3)(i). But see§20.2010–2T(a)(6) when contrary elec-tions are made by more than one personpermitted to make the election. The tem-porary regulations in §20.2010–2T(a)(4)provide that a portability election is irrev-ocable once the due date (as extended) ofthe return has passed.

b. Timely Filing Required

For a valid portability election, sec-tion 2010(c)(5) requires the executor to

make the election on an estate tax returnfiled within the “time prescribed by law”(including extensions) for filing that re-turn. Section 6075(a) requires the filingof an estate tax return made under section6018(a) within 9 months of the date of thedecedent’s death. Section 6018(a) requiresan estate tax return to be filed when thegross estate of a citizen or resident exceedsthe excess (if any) of the basic exclusionamount in effect under section 2010(c) inthe calendar year of the decedent’s deathover the sum of the decedent’s adjustedtaxable gifts as defined in section 2001(b)and the amount allowed to the decedent asa specific exemption under section 2521as in effect prior to its repeal by the TaxReform Act of 1976.

A commenter on Notice 2011–82 notedthat neither section 2010(c)(5)(A) nor anyother section of the Code provides a “timeprescribed by law” for filing an estate taxreturn on behalf of a decedent’s estatewhen the basic exclusion amount exceedsthe value of the decedent’s gross estate.Accordingly, the commenter requestedthat the regulations clarify the meaning of“time prescribed by law” as it applies insection 2010(c)(5)(A).

For executors who are required to filean estate tax return under section 6018(a),section 6075(a) requires the executor tofile the estate tax return within nine monthsafter the decedent’s date of death. Whenan executor is not required to file an estatetax return under section 6018(a), the Codedoes not specify a due date for a returnfiled for the purpose of making the porta-bility election. The temporary regulationsin §20.2010–2T(a)(1) require every estateelecting portability of a decedent’s DSUEamount to file an estate tax return within 9months of the decedent’s date of death, un-less an extension of time for filing has beengranted. (See Notice 2012–21 providingfor an extension of time to file an estate taxreturn for the estates of certain decedentswho died in the first half of calendar year2011.) This timing requirement for filing areturn applies to all estates electing porta-bility regardless of the size of the gross es-tate. The temporary regulations provide in§20.2010–2T(a)(1) that an estate choosingto elect portability will be considered forpurposes of Subtitle B and Subtitle F of theCode to be required to file a return undersection 6018(a).

This rule will benefit the IRS as wellas taxpayers choosing the benefit of porta-bility because the records required tocompute and verify the DSUE amount aremore likely to be available at the time ofthe death of the first deceased spouse thanat the time of a subsequent transfer bythe surviving spouse by gift or at death,which could occur many years later. Thisrule also is consistent with the “TechnicalExplanation of the Revenue ProvisionsContained in the ’Tax Relief, Unemploy-ment Insurance Reauthorization, and JobCreation Act of 2010’ Scheduled for Con-sideration by the United States Senate,”J. Comm. On Taxation, 111th Cong.,JCX–55–10 (Dec. 10, 2010) (TechnicalExplanation), which suggests that estatesdeciding to elect portability that are nototherwise required to file an estate taxreturn under section 6018(a) are intendedto be subject to the same timely-filing re-quirements applicable to estates requiredto file an estate tax return under section6018(a). The Technical Explanation statesthat the DSUE amount is available to asurviving spouse “only if an election ismade on a timely filed estate tax return(including extensions) of the predeceasedspouse . . . regardless of whether thepredeceased spouse otherwise is requiredto file an estate tax return.” JCX–55–10,page 52; see also “General Explanationof Tax Legislation Enacted in the 111th

Congress,” J. Comm. On Taxation, 111th

Cong., JCS–2–11, pages 554–555 (March2011) (General Explanation) (incorporat-ing the same language from the TechnicalExplanation).

c. Portability Election upon Filing of“Complete and Properly-Prepared”Estate Tax Return

Notice 2011–82 provides that the estateof a decedent dying after December 31,2010, will be deemed to make the porta-bility election upon the timely filing of a“complete and properly-prepared” estatetax return. The temporary regulations in§20.2010–2T(a)(2) provide that the estateof a decedent (survived by a spouse) makesthe portability election by timely filing acomplete and properly-prepared estate taxreturn for the decedent’s estate.

Several commenters responding to No-tice 2011–82 requested that Treasury andthe IRS define what is meant by a “com-

July 9, 2012 19 2012–28 I.R.B.

plete and properly-prepared” estate tax re-turn. Commenters further requested thatTreasury and the IRS consider the cost andburden associated with filing an estate taxreturn and establishing and substantiatingthe values reported on such return for thoseestates that are not required to file a returnunder section 6018(a) but are filing sucha return solely to elect portability of thedecedent’s DSUE amount.

The temporary regulations in§20.2010–2T(a)(7)(i) provide that an es-tate tax return prepared in accordance withall applicable requirements is considereda “complete and properly-prepared” estatetax return. The temporary regulations in§20.2010–2T(a)(7)(ii), however, providethat executors of estates that are not oth-erwise required to file an estate tax returnunder section 6018(a) do not have to reportthe value of certain property that qualifiesfor the marital or charitable deduction. Ifan executor chooses to make use of thisspecial rule in filing an estate tax return,the executor must estimate the total valueof the gross estate (including the valuesof the property that do not have to bereported on the estate tax return underthis provision), based on a determinationmade in good faith and with due diligenceregarding the value of all of the assetsincludible in the gross estate. The instruc-tions issued with respect to the estate taxreturn (“Instructions for Form 706”) willprovide ranges of dollar values, and theexecutor must identify on the estate taxreturn the particular range within whichfalls the executor’s best estimate of the to-tal gross estate. An amount correspondingto this range will be included on line 1,part 2, of the estate tax return, along withan indication of whether the line 1 totalincludes an estimate under this specialrule. By signing the return, the executoris certifying, under penalties of perjury,that the estimate falls within the identifiedrange of values to the best of the execu-tor’s knowledge and belief. The inquiryrequired to determine the executor’s bestestimate is the same an executor of anyestate must make under current law todetermine whether the estate has a filingobligation pursuant to section 6018(a);that is, to determine whether the fair mar-ket value of the gross estate exceeds theexcess of the basic exclusion amount overthe sum of the decedent’s adjusted taxablegifts and the amount allowed to the dece-

dent as a specific exemption under section2521.

d. Opting Out of Portability Election

If the executor of the estate of a dece-dent with a surviving spouse does not wishto make the portability election, the tempo-rary regulations in §20.2010–2T(a)(3) re-quire the executor to make an affirmativestatement on the estate tax return signi-fying the decision to have the portabilityelection not apply. If no estate tax returnis required for that decedent’s estate un-der section 6018(a), not filing a timely re-turn will be considered to be an affirma-tive statement signifying the decision notto make a portability election.

e. Executor Responsible For MakingPortability Election

A commenter responding to Notice2011–82 suggested that the temporary reg-ulations allow a surviving spouse to filean estate tax return on behalf of a dece-dent independently of a duly-appointedexecutor if the surviving spouse notifiesthe executor of the intention to file andthe executor does not, in fact, file a return.Section 2010(c)(5), however, permits onlythe executor of the decedent’s estate to filethe estate tax return and make the porta-bility election. Section 2203 defines theterm “executor” for purposes of the estatetax to mean “the executor or administratorof the decedent, or, if there is no executoror administrator appointed, qualified, andacting within the United States, then anyperson in actual or constructive possessionof any property of the decedent.”

The temporary regulations in§20.2010–2T(a)(6)(i) provide that an ex-ecutor or administrator that is appointed,qualified, and acting within the UnitedStates for the decedent’s estate (an ap-pointed executor), may file an estate tax re-turn to elect portability or to opt to have theportability election not apply. The tempo-rary regulations in §20.2010–2T(a)(6)(ii)provide that, if there is no appointed ex-ecutor, any person in actual or constructivepossession of any property of the dece-dent may file the estate tax return to electportability or to opt to have the portabilityelection not apply. The temporary regu-lations in §20.2010–2T(a)(6)(ii) refer tosuch a person as a “non-appointed execu-tor” and provide that a portability election

made by a non-appointed executor cannotbe superseded by a contrary election madeby another non-appointed executor of thatsame decedent’s estate.

4. Computing the DSUE Amount

a. Computation Required On Estate TaxReturn to Elect Portability

The temporary regulations in§20.2010–2T(b)(1) require that an execu-tor include a computation of the DSUEamount on the estate tax return of thedecedent to allow portability of that dece-dent’s DSUE amount. A complete andproperly-prepared return contains theinformation required to compute a dece-dent’s DSUE amount. Accordingly, in atransitional rule consistent with Notice2011–82, the temporary regulations in§20.2010–2T(b)(2) provide that the IRSwill deem the required computation of thedecedent’s DSUE amount to have beenmade on an estate tax return that is con-sidered complete and properly-prepared.The temporary regulations further clarifythat, once the IRS revises the prescribedform for the estate tax return expresslyto include the computation of the DSUEamount, executors that previously filedan estate tax return pursuant to the tran-sitional rule will not be required to file asupplemental estate tax return using therevised form.

b. Method of Computing the DSUEAmount

Section 2010(c)(4) defines the DSUEamount as the lesser of (A) the basic ex-clusion amount, or (B) the excess of (i)the basic exclusion amount of the lastdeceased spouse of the surviving spouse,over (ii) the amount with respect to whichthe tentative tax is determined under sec-tion 2001(b)(1) on the estate of suchdeceased spouse.

The temporary regulations in§20.2010–2T(c)(1)(i) confirm that theterm “basic exclusion amount” referred toin section 2010(c)(4)(A) means the basicexclusion amount in effect in the year ofthe death of the decedent whose DSUEamount is being computed. Generally,only the basic exclusion amount of thedecedent, as in effect in the year of thedecedent’s death, will be known at thetime the DSUE amount must be computed

2012–28 I.R.B. 20 July 9, 2012

and reported on the decedent’s estate taxreturn. Because section 2010(c)(5)(A)requires the executor of an estate elect-ing portability to compute and report theDSUE amount on a timely-filed estate taxreturn, and because the basic exclusionamount is integral to this computation, theterm “basic exclusion amount” in section2010(c)(4)(A) necessarily refers to suchdecedent’s basic exclusion amount.

In responding to Notice 2011–82, sev-eral commenters also argued that thereference to “basic exclusion amount”in section 2010(c)(4)(B)(i) should be in-terpreted to mean “applicable exclusionamount,” citing to the computation ofthe DSUE amount in Example 3 on page53 of the Technical Explanation and tofootnote 1582A that was added to theGeneral Explanation by the “ERRATA— ‘General Explanation of Tax Legis-lation Enacted in the 111th Congress’”(ERRATA). JCX–20–11, at page 1. Ex-ample 3 computes the DSUE amount ofa deceased spouse who was preceded indeath by one spouse and was survived byanother spouse. The deceased spouse’sDSUE amount is computed using the ap-plicable exclusion amount rather than thebasic exclusion amount of the deceasedspouse (as reduced by the amount of thedeceased spouse’s taxable estate). Exam-ple 3 is reproduced verbatim in the GeneralExplanation. See JCS–2–11 at page 555.The ERRATA acknowledges that section2010(c)(4)(B)(i) uses the term basic exclu-sion amount, but notes that “[a] technicalcorrection may be necessary to replace thereference to the basic exclusion amount ofthe last deceased spouse of the survivingspouse with a reference to the applicableexclusion amount of such last deceasedspouse, so that the statute reflects intent.”JCX–20–11, at page 1, n. 1582A.

Treasury and the IRS have carefullyconsidered this issue. Construing thelanguage of section 2010(c)(4)(B)(i) asreferring to the same number describedin section 2010(c)(4)(A) would lead toan illogical result because it would ef-fectively render the use of “basic exclu-sion amount” in section 2010(c)(4)(A)meaningless. Specifically, the basic ex-clusion amount (the amount referencedin section 2010(c)(4)(A)) cannot be lessthan that same number reduced by an-other number (the amount referenced insection 2010(c)(4)(B)). Under such an in-

terpretation, the basic exclusion amountreferenced in section 2010(c)(4)(A) couldnot limit or impact the DSUE amount, andthus it would serve no purpose as writ-ten. Based on the principle that a statuteshould not be construed in a manner thatrenders a provision of that statute super-fluous and consistent with the indicia oflegislative intent reflected in the TechnicalExplanation and the General Explana-tion, and in the exercise of the expressauthority granted by Congress in sections2010(c)(6) and 7805, Treasury and theIRS have determined that the referencein section 2010(c)(4)(B)(i) to the basicexclusion amount is properly interpretedto mean the applicable exclusion amount.Thus, the temporary regulations adopt thisinterpretation.

c. Effect of Gift Taxes Paid and Payableon Computing the DSUE Amount

Several commenters on Notice2011–82 suggested that, for purposesof computing the DSUE amount undersection 2010(c)(4), the amount referredto in section 2010(c)(4)(B)(ii), which isthe amount on which the decedent’s ten-tative tax is determined under section2001(b)(1), be construed to take into ac-count gift tax paid by such decedent. Thecommenters noted that, to avoid usingexclusion for amounts on which gift taxwas paid, this construction should applyin computing the DSUE amount of sucha decedent if (1) gift tax was paid by adecedent on transfers that caused the totalof his or her taxable transfers to exceed theapplicable exclusion amount at the timeof the transfer, and (2) the total adjustedtaxable gifts of the decedent is less thanthe applicable exclusion amount on thedate of his or her death. The temporaryregulations in §20.2010–2T(c)(2) providethat amounts on which gift taxes were paidby a decedent are excluded from adjustedtaxable gifts for the purpose of computingthat decedent’s DSUE amount.

d. Potential Impact of Credits in Sections2013 — 2015 on the DSUE Amount

Commenters on Notice 2011–82 askedfor clarification as to whether the DSUEamount is determined before or after theapplication of other available credits, suchas the credit for tax on prior transfers (sec-tion 2013), the credit for foreign death

taxes (section 2014), and the credit fordeath taxes on remainders (section 2015).The issue of the impact of the credits insections 2013 to 2015 on computing theDSUE amount merits further considera-tion. The temporary regulations reserve§20.2010–2T(c)(3) to provide future guid-ance on this issue. Treasury and the IRSrequest comments regarding appropriaterules to coordinate these credits with porta-bility of the exclusion. For the manner ofsubmitting these comments, see the noticeof proposed rulemaking on this subject ap-pearing elsewhere in this issue of the Bul-letin.

5. Use of the DSUE Amount by theSurviving Spouse

a. Date DSUE Amount May Be Taken intoConsideration by Surviving Spouse

Commenters on Notice 2011–82 askedfor clarification on when the DSUEamount of a decedent is available tothe surviving spouse or to the survivingspouse’s estate for use in determiningthe surviving spouse’s applicable exclu-sion amount. The temporary regulationsin §§20.2010–3T(a) and 25.2505–2T(a)provide that, if the decedent is the lastdeceased spouse of the surviving spouseon the date of a transfer by the surviv-ing spouse that is subject to gift or estatetax, the surviving spouse, or the estateof the surviving spouse, of that dece-dent may take into account that dece-dent’s DSUE amount in determiningthe applicable exclusion amount of thesurviving spouse when computing thesurviving spouse’s gift or estate tax lia-bility on that transfer. This rule appliesonly if the decedent’s executor electedportability. In addition, the temporaryregulations in §§20.2010–3T(c)(1) and25.2505–2T(d)(1) provide that a porta-bility election made by the executor ofa decedent’s estate is effective as of thedate of the decedent’s death. Thus, theDSUE amount of a decedent survived by aspouse may be included in determining theapplicable exclusion amount of the sur-viving spouse under section 2010(c)(2),subject to any applicable limitations, withrespect to all transfers occurring after thedeath of the decedent, if the executor ofthe decedent’s estate makes a portabilityelection and the election is not superseded

July 9, 2012 21 2012–28 I.R.B.

by the executor of the decedent’s estatebefore the due date of the return, includingextensions.

b. Last Deceased Spouse Limitation onDSUE Amount Available to SurvivingSpouse

Some commenters responding to No-tice 2011–82 suggested that the reg-ulations clarify the scope of the lastdeceased spouse limitation in section2010(c)(4)(B)(i). The temporary regula-tions in §20.2010–1T(d)(5) explain thatthe term “last deceased spouse” referredto in section 2010(c)(4)(B)(i) means themost recently deceased individual whowas married to the surviving spouse atthat individual’s death, except that an in-dividual dying before calendar year 2011cannot be considered the last deceasedspouse of such surviving spouse. The tem-porary regulations in §§20.2010–3T(a)(3)and 25.2505–2T(a)(3) clarify that remar-riage alone does not affect who will beconsidered the last deceased spouse anddoes not prevent the surviving spousefrom including in the surviving spouse’sapplicable exclusion amount the DSUEamount of the deceased spouse who mostrecently preceded the surviving spousein death. The temporary regulations fur-ther clarify that the identity of the lastdeceased spouse of the surviving spousefor purposes of portability is not affectedby whether the estate of the last deceasedspouse elects portability of the deceasedspouse’s DSUE amount or whether the lastdeceased spouse has any DSUE amountavailable. This is consistent with the statu-tory language, which refers to the “lastdeceased spouse of such surviving spouse”without further qualification, as well aswith the Technical Explanation, whichstates that “[t]he last deceased spouselimitation applies whether or not the lastdeceased spouse has any unused exclusionor the last deceased spouse’s estate makesa timely election.” JCX–55–10, at page52, n. 57; see also General Explanation,JCS–2–11, at page 554, n. 1582.

For purposes of determining the ap-plicable credit amount under section2505(a)(1), a commenter asked Treasuryand the IRS to clarify when one determinesthe identity of the last deceased spouse.Although section 2505(a)(1) refers to theapplicable credit amount in effect under

section 2010(c) as would apply if the donordied as of the end of the calendar year,this does not mean that the identity of thelast deceased spouse is subject to changefor purposes of computing the survivingspouse’s applicable exclusion amount ifthe surviving spouse is preceded in deathby a subsequent spouse after the gift trans-fer but before the end of the calendaryear. Therefore, the temporary regulationsprovide in §25.2505–2T(a) that for pur-poses of determining a surviving spouse’sapplicable exclusion amount when thesurviving spouse makes a taxable gift, thesurviving spouse’s last deceased spouse isidentified as of the date of the taxable gift.See §20.2010–3T(a) for a comparable rulefor estate tax purposes.

c. DSUE Amount Available in Case ofMultiple Spouses and Previously-AppliedDSUE Amount

Some commenters responding to No-tice 2011–82 requested that the regulationsclarify the outcome when a survivingspouse is preceded in death by more thanone spouse. In particular, commentersasked how the DSUE amount to be in-cluded in the applicable exclusion amountof a surviving spouse is affected when adecedent who is currently considered thelast deceased spouse of such survivingspouse either has no DSUE amount orhas a smaller amount of DSUE in com-parison to a decedent who previously wasconsidered the last deceased spouse ofsuch surviving spouse. The temporaryregulations clarify that, in either situation,the surviving spouse may not apply anyremaining DSUE amount from a priordeceased spouse.

In addition, the temporary regula-tions address how to compute the DSUEamount included in the applicable exclu-sion amount of a surviving spouse whomade gifts between the deaths of twodecedents, each of whom were at separatetimes the last deceased spouse of suchsurviving spouse. First, the temporaryregulations in §25.2505–2T(b) create anordering rule by providing that, when asurviving spouse makes a taxable gift, theDSUE amount of the decedent who is thelast deceased spouse of such survivingspouse will be considered to apply againstthe amount of the surviving spouse’s tax-able gifts for that calendar year before the

surviving spouse’s own basic exclusionamount will apply.

Second, the temporary regulations,in §§25.2505–2T(c) and 20.2010–3T(b),compute the DSUE amount available tosuch a surviving spouse or to his or her es-tate, respectively, as including both: (i) theDSUE amount of the surviving spouse’slast deceased spouse, and (ii) any DSUEamount actually applied to taxable giftspursuant to the rule in §25.2505–2T(b) tothe extent the DSUE amount so appliedwas from a decedent who no longer is thelast deceased spouse for purposes of sec-tion 2010(c)(4)(B)(i). Under the rules in§25.2505–2T, a surviving spouse may usethe DSUE amount of a predeceased spouseas long as, for each transfer, such DSUEamount is from the surviving spouse’slast deceased spouse at the time of thattransfer. Thus, a spouse who has survivedmultiple spouses may use each last de-ceased spouse’s DSUE amount before thedeath of that spouse’s next spouse, andthereby may apply the DSUE amount ofmultiple deceased spouses in succession.However, this does not permit the surviv-ing spouse to use the sum of the DSUEamounts of those deceased spouses at onetime, and a surviving spouse may not usethe remaining DSUE amount of a priordeceased spouse following the death of asubsequent spouse.

6. Authority to Examine Returns ofDeceased Spouses

Section 2010(c)(5)(B) confirms theIRS’s authority to examine returns of eachdeceased spouse of the surviving spouseto determine the allowable DSUE amounteven if the period of limitations on as-sessment under section 6501 has expiredfor the tax under chapters 11 or 12 withrespect to such returns.

Section 7602(a) provides that the IRSmay examine any books, papers, records,or other data which may be relevant or ma-terial to an inquiry for the purpose of ascer-taining the accuracy of any return or deter-mining the liability of any person for anyinternal revenue tax or liability. The re-turns of each deceased spouse whose ex-ecutor elected portability are relevant ormaterial to the determination of the allow-able DSUE amount to be applied by thesurviving spouse to a taxable transfer.

2012–28 I.R.B. 22 July 9, 2012

Accordingly, the temporary regu-lations confirm in §§20.2001–2T(a),20.2010–2T(d), 20.2010–3T(d), and25.2505–2T(e) that, in determining theallowable DSUE amount, the IRS mayexamine any one or more returns of eachdeceased spouse of the surviving spousewhose executor elected portability. Uponexamination, the IRS may adjust or elim-inate the DSUE amount reported on areturn; however, the IRS may make an as-sessment of additional tax with respect tothe deceased spouse’s return only withinthe period of limitations under section6501. The ability of the IRS to examine re-turns of a deceased spouse applies to eachtransfer by the surviving spouse to whicha DSUE amount is or has been applied.The returns and return information of adeceased spouse may be disclosed to thesurviving spouse or the surviving spouse’sestate as appropriate under section 6103.

A commenter to Notice 2011–82 sug-gested that the regulations clarify whetherthe IRS’s authority to examine returnseven after the period of limitations onassessment has expired, as confirmed insection 2010(c)(5)(B), would suspend thesubstantive review and examination ofthe estate tax return of a decedent witha surviving spouse. Except to the extentprovided in section 2010(c)(5)(B) withregard to the computation of the DSUEamount, the limitation in section 6501continues to apply to the estate tax returnso examination of the estate tax return willnot be suspended solely because of thepossibility of future reviews to determinethe decedent’s DSUE amount.

7. Applicability of Portability Rules toNonresidents Who Are Not Citizens

Several commenters requested that theregulations clarify the applicability ofthe rules in section 2010(c) to estates ofnonresidents who are not citizens. In re-sponse to these comments, the temporaryregulations provide in §20.2010–2T(a)(5)that an executor of the estate of a non-resident decedent who was not a citizenof the United States at the time of deathmay not make a portability election onbehalf of that decedent. The tempo-rary regulations in §§20.2010–3T(e) and25.2505–2T(f) provide that a nonresidentsurviving spouse who was not a citizenof the United States at the time of such

surviving spouse’s death may not takeinto account the DSUE amount of anydeceased spouse of such surviving spouse,except to the extent allowed under a treatyobligation of the United States.

8. Applicability of Portability in Case ofQualified Domestic Trusts

A commenter suggested that the regula-tions clarify how the portability rules applywhen a qualified domestic trust (QDOT)(defined in section 2056A(a)) is createdfor the benefit of a surviving spouse who isa not a citizen of the United States. Whenproperty of a decedent passes to a QDOT,the decedent’s estate is allowed a maritaldeduction under section 2056(d)(2) forthe value of such property. Ultimately,however, estate tax is imposed on suchproperty under section 2056A as distribu-tions constituting taxable events are madefrom the QDOT. The estate tax imposedby section 2056A is the decedent’s estatetax liability, and that tax generally equalsthe amount of additional estate tax thatwould have been imposed under section2001 if the amount involved in the taxableevent had been included in the decedent’staxable estate and had not been deductibleunder section 2056. See §20.2056A–5(a).The estate tax that would have been im-posed under section 2001 is computedby determining the net tax under section2001 after the allowance of any credits,including the applicable credit amountdetermined under section 2010(c). Conse-quently, when a QDOT has been createdfor the benefit of a decedent’s survivingspouse, the executor of the decedent’sestate will compute a DSUE amount, ona preliminary basis, that may decrease asdistributions constituting taxable eventsunder section 2056A are made.

Commenters made several suggestionsfor applying portability to this situation.One proposal is to allow a decedent’sDSUE amount to be computed and avail-able to the surviving spouse as of the dateof death of the decedent, without regardto the estate tax to be imposed by section2056A. A second suggestion is to allow anexecutor of such an estate to elect porta-bility with respect to only a portion of theDSUE amount so that an executor couldreserve a portion of the decedent’s DSUEamount for the estate tax to be imposedby section 2056A. A third proposal is to

allow the decedent’s applicable exclu-sion amount and the initially-determinedDSUE amount to be applied on a chrono-logical, or first come, first served, basis;that is, by applying the decedent’s appli-cable exclusion amount on the occurrenceof a taxable event subject to the estatetax imposed by section 2056A and at thetime of a transfer by the surviving spousesubject to the gift tax imposed by section2501, in each case, to the extent applica-ble exclusion amount or DSUE amount,respectively, is available at such times.

Each of the proposals raises issues offairness, complexity, and administrability.The applicable exclusion amount first andforemost belongs to the decedent. Porta-bility of a DSUE amount allows a surviv-ing spouse to use a decedent’s exclusionamount only to the extent it is not used bythat decedent. Accordingly, the temporaryregulations allow the decedent’s estate fullavailability of the decedent’s applicableexclusion amount until such time as thefinal estate tax liability of the decedentis computed. The temporary regulationsin §20.2010–2T(c)(4) provide that theexecutor of a decedent’s estate claiminga marital deduction for property passingto a QDOT shall compute the decedent’sDSUE amount on a preliminary basis onthe decedent’s estate tax return for the pur-pose of electing portability, although suchamount subsequently will be reduced bythe estate tax imposed by section 2056A.The temporary regulations further pro-vide that the DSUE amount of such adecedent shall be redetermined upon thefinal distribution or other taxable eventon which estate tax under section 2056Ais imposed, which is generally upon thedeath of the surviving spouse or the earliertermination of all QDOTs created for thatsurviving spouse. The temporary regula-tions provide in §20.2010–3T(c)(2) thatthe earliest date such a decedent’s DSUEamount may be included in determiningthe applicable exclusion amount availableto the surviving spouse or the survivingspouse’s estate is the date of the event thattriggers the final estate tax liability of thedecedent under section 2056A. Generally,this means that such a decedent’s DSUEamount will be available for transfers oc-curring by reason of the surviving spouse’sdeath, but generally will not be avail-able to the surviving spouse during life.However, the decedent’s DSUE amount

July 9, 2012 23 2012–28 I.R.B.

will be available to apply to the survivingspouse’s taxable gifts made in the yearof the surviving spouse’s death, or, if theevent terminating the QDOT occurs priorto the surviving spouse’s death, then inthe year of that terminating event and/orany subsequent year during the survivingspouse’s life. Treasury and the IRS requestfurther comments on this issue. For themanner of submitting these comments, seethe notice of proposed rulemaking on thissubject appearing elsewhere in this issueof the Bulletin.

Special Analyses

It has been determined that this Trea-sury decision is not considered a signifi-cant regulatory action as defined in Execu-tive Order 12866, as supplemented by Ex-ecutive Order 13563. Therefore, a regula-tory assessment is not required. In addi-tion, section 553(b) of the AdministrativeProcedure Act (5 U.S.C. chapter 5) doesnot apply to these regulations because theyare excepted from the notice and commentrequirements of section 553(b) and (c) ofthe Administrative Procedure Act underthe interpretive rule and good cause ex-ceptions provided by section 553(b)(3)(A)and (B) of that Act. These regulationsare necessary to provide immediate guid-ance to estates of a decedent with a surviv-ing spouse and to spouses surviving sucha decedent on the application of the porta-bility rules of section 2010(c), which ap-plies to estates of decedents dying and giftsmade after December 31, 2010. These reg-ulations provide necessary guidance to ad-dress fundamental issues concerning theportability election, the computation of theDSUE amount, the identity of the last de-ceased spouse, and the application of theDSUE amount by the surviving spouse. Inaddition, the issues addressed by the regu-lations have been publicly noticed and sub-ject to comment through the publication ofNotice 2011–82. For these reasons, goodcause exists for dispensing with notice andpublic comment pursuant to section 553(b)and (c) of the Administrative ProcedureAct. For the applicability of the Regula-tory Flexibility Act (5 U.S.C. chapter 6),please refer to the Special Analyses sectionof the preamble to the cross-referenced no-tice of proposed rulemaking published inthis issue of the Bulletin. Pursuant to sec-tion 7805(f) of the Code, these regulations

have been submitted to the Chief Counselfor Advocacy of the Small Business Ad-ministration for comment on their impacton small business.

Drafting Information

The principal author of these temporaryregulations is Karlene Lesho, Office of theAssociate Chief Counsel (Passthroughsand Special Industries). Other personnelfrom the IRS and the Treasury Departmentparticipated in their development.

* * * * *

Amendments to the Regulations

Accordingly, 26 CFR parts 20, 25, and602 are amended as follows:

PART 20—ESTATE TAX; ESTATE OFDECEDENTS DYING AFTER AUGUST16, 1954

Paragraph 1. The authority citation forpart 20 is amended by adding entries innumerical order to read as follows:

Authority: 26 U.S.C. 7805. * * *Section 20.2010–0T also issued under

26 U.S.C. 2010(c)(6).Section 20.2010–1T also issued under

26 U.S.C. 2010(c)(6).Section 20.2010–2T also issued under

26 U.S.C. 2010(c)(6).Section 20.2010–3T also issued under

26 U.S.C. 2010(c)(6). * * *Par. 2. Section 20.2001–2T is added to

read as follows:

§20.2001–2T Valuation of adjustedtaxable gifts for purposes of determiningthe deceased spousal unused exclusionamount of last deceased spouse(temporary).

(a) General rule. Notwithstanding§20.2001–1(b), see §§20.2010–2T(d) and20.2010–3T(d) for additional rules regard-ing the authority of the Internal RevenueService to examine any gift or other taxreturn(s), even if the time within which atax may be assessed under section 6501has expired, for the purpose of determin-ing the deceased spousal unused exclusion(DSUE) amount available under section2010(c) of the Internal Revenue Code(Code).

(b) Effective/applicability date. Para-graph (a) of this section applies to the

estates of decedents dying in calendar year2011 or a subsequent year in which the ap-plicable exclusion amount is determinedunder section 2010(c) of the Code byadding the basic exclusion amount and, inthe case of a surviving spouse, the DSUEamount.

(c) Expiration date. The applicabilityof this section expires on or before June 15,2015.

Par. 3. Section 20.2010–0T is added toread as follows:

§20.2010–0T Table of contents(temporary).

This section lists the table of contentsfor §§20.2010–1T through 20.2010–3T.

§20.2010–1T Unified credit against estatetax; in general (temporary).

(a) General rule.(b) Special rule in case of certain gifts

made before 1977.(c) Credit limitation.(d) Explanation of terms.(1) Applicable credit amount.(2) Applicable exclusion amount.(3) Basic exclusion amount.(4) Deceased spousal unused exclusion

(DSUE) amount.(5) Last deceased spouse.(e) Effective/applicability date.(f) Expiration date.

§20.2010–2T Portability provisionsapplicable to estate of a decedent survivedby a spouse (temporary).

(a) Election required for portability.(1) Timely filing required.(2) Portability election upon filing of

estate tax return.(3) Portability election not made; re-

quirements for election not to apply.(4) Election irrevocable.(5) Estates eligible to make the election.(6) Persons permitted to make the elec-

tion.(7) Requirements of return.(b) Computation required for portabil-

ity election.(1) General rule.(2) Transitional rule.(c) Computation of the DSUE amount.(1) General rule.(2) Special rule to consider gift taxes

paid by decedent.

2012–28 I.R.B. 24 July 9, 2012

(3) [Reserved](4) Special rule in case of property pass-

ing to qualified domestic trust.(5) Examples.(d) Authority to examine returns of

decedent.(e) Effective/applicability date.(f) Expiration date.

§20.2010–3T Portability provisionsapplicable to the surviving spouse’s estate(temporary).

(a) Surviving spouse’s estate limited toDSUE amount of last deceased spouse.

(1) In general.(2) No DSUE amount available from

last deceased spouse.(3) Identity of last deceased spouse

unchanged by subsequent marriage or di-vorce.

(b) Special rule in case of multiple de-ceased spouses and a previously-appliedDSUE amount.

(1) In general.(2) Example.(c) Date DSUE amount taken into con-

sideration by surviving spouse’s estate.(1) General rule.(2) Special rule when property passes

to surviving spouse in a qualified domestictrust.

(d) Authority to examine returns of de-ceased spouses.

(e) Availability of DSUE amount for es-tates of nonresidents who are not citizens.

(f) Effective/applicability date.(g) Expiration date.Par. 4. Section 20.2010–1T is added to

read as follows:

§20.2010–1T Unified credit against estatetax; in general (temporary).

(a) General rule. Section 2010(a) al-lows the estate of every decedent a creditagainst the estate tax imposed by section2001. The allowable credit is the applica-ble credit amount. See paragraph (d)(1) ofthis section for an explanation of the termapplicable credit amount.

(b) Special rule in case of certain giftsmade before 1977. The applicable creditamount allowable under paragraph (a) ofthis section must be reduced by an amountequal to 20 percent of the aggregateamount allowed as a specific exemptionunder section 2521 (as in effect before its

repeal by the Tax Reform Act of 1976) forgifts made by the decedent after Septem-ber 8, 1976, and before January 1, 1977.

(c) Credit limitation. The applicablecredit amount allowed under paragraph (a)of this section cannot exceed the amountof the estate tax imposed by section 2001.

(d) Explanation of terms. The expla-nation of terms in this section applies tothis section and to §§20.2010–2T and20.2010–3T.

(1) Applicable credit amount. The termapplicable credit amount refers to the al-lowable credit against estate tax imposedby section 2001 and gift tax imposedby section 2501. The applicable creditamount equals the amount of the tentativetax that would be determined under sec-tion 2001(c) if the amount on which suchtentative tax is to be computed were equalto the applicable exclusion amount. Theapplicable credit amount is determined byapplying the unified rate schedule in sec-tion 2001(c) to the applicable exclusionamount.

(2) Applicable exclusion amount. Theapplicable exclusion amount equals thesum of the basic exclusion amount and,in the case of a surviving spouse, the de-ceased spousal unused exclusion (DSUE)amount.

(3) Basic exclusion amount. The basicexclusion amount is the sum of—

(i) For any decedent dying in calendaryear 2011, $5,000,000; and

(ii) For any decedent dying after calen-dar year 2011, $5,000,000 multiplied bythe cost-of-living adjustment determinedunder section 1(f)(3) for that calendar yearby substituting “calendar year 2010” for“calendar year 1992” in section 1(f)(3)(B)and by rounding to the nearest multiple of$10,000.

(4) Deceased spousal unused exclusion(DSUE) amount. The term DSUE amountrefers, generally, to the unused portion ofa decedent’s applicable exclusion amountto the extent this amount does not ex-ceed the basic exclusion amount in effectin the year of the decedent’s death. Forrules on computing the DSUE amount, see§§20.2010–2T(c) and 20.2010–3T(b).

(5) Last deceased spouse. The term lastdeceased spouse means the most recentlydeceased individual who, at that indi-vidual’s death after December 31, 2010,was married to the surviving spouse. See§§20.2010–3T(a) and 25.2505–2T(a) of

this chapter for additional rules pertainingto the identity of the last deceased spousefor purposes of determining the applicableexclusion amount of the surviving spouse.

(e) Effective/applicability date. Para-graphs (d)(2), (d)(3), (d)(4), and (d)(5) ofthis section apply to the estates of dece-dents dying in calendar year 2011 or a sub-sequent year in which the applicable exclu-sion amount is determined under section2010(c) of the Internal Revenue Code byadding the basic exclusion amount and, inthe case of a surviving spouse, the DSUEamount. Paragraphs (a), (b), (c), and (d)(1)of this section apply to the estates of dece-dents dying on or after June 15, 2012.

(f) Expiration date. The applicability ofthis section expires on or before June 15,2015.

Par. 5. Section 20.2010–2T is added toread as follows:

§20.2010–2T Portability provisionsapplicable to estate of a decedent survivedby a spouse (temporary).

(a) Election required for portability.To allow a decedent’s surviving spouse totake into account that decedent’s deceasedspousal unused exclusion (DSUE) amount,the executor of the decedent’s estate mustelect portability of the DSUE amount ona timely-filed Form 706, “United StatesEstate (and Generation-Skipping Trans-fer) Tax Return” (estate tax return). Thiselection is referred to in this section and in§20.2010–3T as the portability election.

(1) Timely filing required. An estatethat elects portability will be considered,for purposes of Subtitle B and Subtitle Fof the Internal Revenue Code (Code), tobe required to file a return under section6018(a). Accordingly, the due date of anestate tax return required to elect portabil-ity is 9 months after the decedent’s dateof death or the last day of the period cov-ered by an extension (if an extension oftime for filing has been obtained). See§§20.6075–1 and 20.6081–1 for additionalrules relating to the time for filing estatetax returns.

(2) Portability election upon filing ofestate tax return. Upon the timely filingof a complete and properly-prepared estatetax return, an executor of an estate of adecedent (survived by a spouse) will haveelected portability of the decedent’s DSUEamount unless the executor chooses not to

July 9, 2012 25 2012–28 I.R.B.

elect portability and satisfies the require-ment in paragraph (a)(3)(i) of this section.See paragraph (a)(7) of this section for thereturn requirements related to the portabil-ity election.

(3) Portability election not made; re-quirements for election not to apply. Theexecutor of the estate of a decedent (sur-vived by a spouse) will not make or be con-sidered to make the portability election ifeither of the following applies:

(i) The executor states affirmatively ona timely-filed estate tax return, or in an at-tachment to that estate tax return, that theestate is not electing portability under sec-tion 2010(c)(5). The manner in which theexecutor may make this affirmative state-ment on the estate tax return will be asset forth in the instructions issued with re-spect to such form (“Instructions for Form706”).

(ii) The executor does not timely file anestate tax return in accordance with para-graph (a)(1) of this section.

(4) Election irrevocable. An execu-tor of the estate of a decedent (survivedby a spouse) who timely files an estatetax return may make and may supersede aportability election previously made, pro-vided that the estate tax return reportingthe decision not to make a portability elec-tion is filed on or before the due date ofthe return, including extensions actuallygranted. However, see paragraph (a)(6)of this section when contrary elections aremade by more than one person permittedto make the election. The portability elec-tion, once made, becomes irrevocable oncethe due date of the estate tax return, in-cluding extensions actually granted, haspassed.

(5) Estates eligible to make the election.An executor may elect portability on be-half of the estate of a decedent (survived bya spouse) if the decedent dies in calendaryear 2011 or during a subsequent period inwhich portability of a DSUE amount is ineffect. However, an executor of the estateof a nonresident decedent who was not acitizen of the United States at the time ofdeath may not elect portability on behalf ofthat decedent, and the timely filing of sucha decedent’s estate tax return will not con-stitute the making of a portability election.

(6) Persons permitted to make the elec-tion—(i) Appointed executor. An execu-tor or administrator of the estate of a dece-dent (survived by a spouse) that is ap-

pointed, qualified, and acting within theUnited States, within the meaning of sec-tion 2203 (an appointed executor), mayfile the estate tax return on behalf of theestate of the decedent and, in so doing,elect portability of the decedent’s DSUEamount. An appointed executor also mayelect not to have portability apply pursuantto paragraph (a)(3) of this section.

(ii) Non-appointed executor. If thereis no appointed executor, any person inactual or constructive possession of anyproperty of the decedent (a non-appointedexecutor) may file the estate tax return onbehalf of the estate of the decedent and, inso doing, elect portability of the decedent’sDSUE amount, or, by complying withparagraph (a)(3) of this section, may electnot to have portability apply. A portabilityelection made by a non-appointed execu-tor cannot be superseded by a contraryelection made by another non-appointedexecutor of that same decedent’s estate(unless such other non-appointed execu-tor is the successor of the non-appointedexecutor who made the election). See§20.6018–2 for additional rules relatingto persons permitted to file the estate taxreturn.

(7) Requirements of return—(i) Gen-eral rule. An estate tax return will beconsidered complete and properly-pre-pared for purposes of this section if itis prepared in accordance with the in-structions issued for the estate tax return(Instructions for Form 706) and if the re-quirements of §§20.6018–2, 20.6018–3,and 20.6018–4 are satisfied. However,see paragraph (a)(7)(ii) of this section forreduced requirements applicable to certainproperty of certain estates.

(ii) Reporting of value not requiredfor certain property—(A) In general. Aspecial rule applies with respect to certainproperty of estates in which the executoris not required to file an estate tax re-turn under section 6018(a), as determinedwithout regard to paragraph (a)(1) of thissection. With respect to such an estate, forbequests, devises, or transfers of propertyincluded in the gross estate, the value ofwhich is deductible under section 2056or 2056A (marital deduction property) orunder section 2055(a) (charitable deduc-tion property), an executor is not requiredto report a value for such property onthe estate tax return (except to the extentprovided in this paragraph (a)(7)(ii)(A))

and will be required to report only the de-scription, ownership, and/or beneficiary ofsuch property, along with all other infor-mation necessary to establish the right ofthe estate to the deduction in accordancewith §§20.2056(a)–1(b)(i) through (iii)and 20.2055–1(c), as applicable. How-ever, this rule does not apply to maritaldeduction property or charitable deductionproperty if—

(1) The value of such property relatesto, affects, or is needed to determine, thevalue passing from the decedent to anotherrecipient;

(2) The value of such property is neededto determine the estate’s eligibility for theprovisions of sections 2032, 2032A, 6166,or another provision of the Code;

(3) Less than the entire value of an inter-est in property includible in the decedent’sgross estate is marital deduction propertyor charitable deduction property; or

(4) A partial disclaimer or partial qual-ified terminable interest property (QTIP)election is made with respect to a bequest,devise, or transfer of property includible inthe gross estate, part of which is maritaldeduction property or charitable deductionproperty.

(B) Statement required on the return.Paragraph (a)(7)(ii)(A) of this section ap-plies only if the executor exercises duediligence to estimate the fair market valueof the gross estate, including the propertydescribed in paragraph (a)(7)(ii)(A) of thissection. The Instructions for Form 706will provide ranges of dollar values, andthe executor must identify on the estate taxreturn an amount corresponding to the par-ticular range within which falls the execu-tor’s best estimate of the total gross es-tate. Until such time as the prescribed formfor the estate tax return expressly includesthis estimate in the manner described in thepreceding sentence, the executor must in-clude the executor’s best estimate, roundedto the nearest $250,000, on or attached tothe estate tax return, signed under penaltiesof perjury.

(C) Examples. The following exam-ples illustrate the application of paragraph(a)(7)(ii) of this section. In each example,assume that Husband (H) dies in 2011, sur-vived by his wife (W), that both H and Ware US citizens, that H’s gross estate doesnot exceed the excess of the applicable ex-clusion amount for the year of his deathover the total amount of H’s adjusted tax-

2012–28 I.R.B. 26 July 9, 2012

able gifts and any specific exemption un-der section 2521, and that H’s executor (E)timely files Form 706 solely to make theportability election.

Example 1. (i) Facts. The assets includible inH’s gross estate consist of a parcel of real propertyand bank accounts held jointly with W with rightsof survivorship, a life insurance policy payable to W,and a survivor annuity payable to W for her life. Hmade no taxable gifts during his lifetime.

(ii) Application. E files an estate tax return onwhich these assets are identified on the proper sched-ule, but E provides no information on the return withregard to the date of death value of these assets in ac-cordance with paragraph (a)(7)(ii)(A) of this section.To establish the estate’s entitlement to the marital de-duction in accordance with §20.2056(a)–1(b) (exceptwith regard to establishing the value of the property)and the instructions for the estate tax return, E in-cludes with the estate tax return evidence to verifythe title of each jointly held asset, to confirm that Wis the sole beneficiary of both the life insurance policyand the survivor annuity, and to verify that the annuityis exclusively for W’s life. Finally, E certifies on theestate return E’s best estimate, determined by exercis-ing due diligence, of the fair market value of the grossestate in accordance with paragraph (a)(7)(ii)(B) ofthis section. The estate tax return is considered com-plete and properly prepared and E has elected porta-bility.