building the business case for sustainable agriculture · building the business case for...

TRANSCRIPT

© 2012 SAI Platform & IMD International. Not to be used or reproduced without permission.

Building the business case for sustainable agriculture

Dr. Aileen Ionescu-Somers, Director, Corporate Sustainability Management Platform, IMD

© SAI Platform & IMD 2012

Population: Increasing market demand for food, fiber and fuel

© SAI Platform & IMD 2012

Borneo – palm oil, timber

East/Southern Africa – biofuels,

tuna

Arctic – cod and pollack, carbon

Amazon – soy, cotton,

livestock, timber

Coral Triangle – tuna, live reef fish, aquaculture

Indus Delta – rice, cotton, sugarcane

seriously impacts ecosystems…..

…….leading to global threats………….

© SAI Platform & IMD 2012

human beings…….

Human rights abuses

© SAI Platform & IMD 2012

….and our climate

Global warming

© SAI Platform & IMD 2012

But it also threatens the supply base of companies

The business case equation:

NO SUPPLY = NO BUSINESS

ITS NOT ROCKET SCIENCE

© SAI Platform & IMD 2012

Lets recap on the economics

Negative externalities in the form of sustainability issues arise as a result of market failures Market failures are related to the non-internalization of costs.

For sustainability issues, the cost is to society and the planet. If costs are not internalized, companies become “free riders”

leading to the “tragedy of the commons” (Hardins)

© SAI Platform & IMD 2012

And….

Overexploitation of common property resources, or the Tragedy of the Commons.

© SAI Platform & IMD 2012

Our baseline for business cases

There are various ways of internalizing these costs: Regulation, taxes, other economic instruments…… In the absence of regulation, companies have to find other “business

cases” for internalization of their negative externalities. Companies will internalise social and environmental issues and

include them in business strategy when: 1) Regulations demand it

2) A competitive advantage, thus a business case, justifies it

© SAI Platform & IMD 2012 10

Compliance level of activity under

consideration

Level of environmental and social performance

Economic value generated

Company creates economic value by improving environmental and

social performance beyond compliance

The Smart Zone: Economic gain is high

Further improvements of environmental and social performance lead to decreases in economic performance

Further improvements are associated with an economic loss

Seeking the “Smart Zone” or the business case

© SAI Platform & IMD 2012

When business cases for sustainability are weak/weakly exploited, it can be due to:

Multiplicity and high level of fragmentation of sustainability issues

Increasingly complex and long value chains Issues ranging in complexity from micro to macro and affecting companies at various stages in the value chain

© SAI Platform & IMD 2012

How companies build business strategy

Start with analysing the business context. Understand: The macro business environment Forces that determine positioning within the

markets they serve Governmental Socio-cultural Economic Competitive

© SAI Platform & IMD 2012

Porter’s model: the five forces of industry competition

Degree of rivalry: Cutthroat competition, oligopoly, dispersion….

Threat of substitutes: Other products or services, placing the company in a weaker position

Supplier power: to ask for and receive higher prices in their sales negotiations

Buyer power: to obtain better deals through comparison shopping, threat of desertion, or other ways of weakening producer bargaining power

Barriers to entry: Preventing new firms from competing and weakening the position of existing firms

© SAI Platform & IMD 2012

Guess what? Sustainability is no different……..To build a business case companies must….

Seek the economic relevance of sustainability

issues

© SAI Platform & IMD 2012

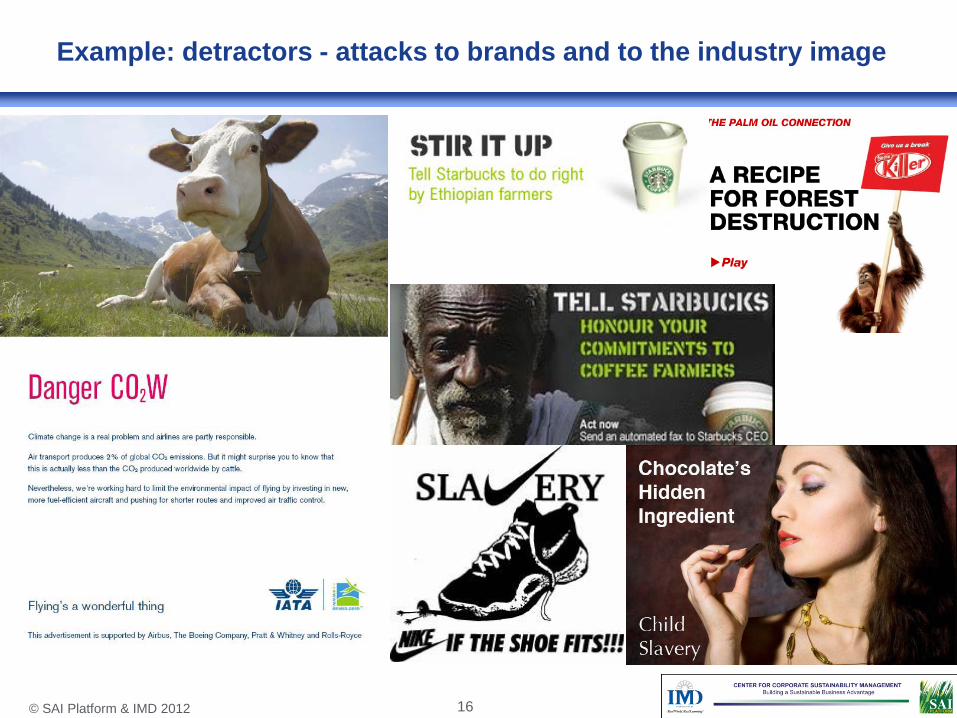

Stakeholder pressure

Which stakeholders are pushing the issues onto the corporate radar screen?

© SAI Platform & IMD 2012 16

Example: detractors - attacks to brands and to the industry image

© SAI Platform & IMD 2012

Stakeholder pressure

Employees

SuppliersShare-holders

Customers

„Contextual Environment“:Public Stakeholder

„Transactual Environment“:Marketal Stakeholder

„Contextual Environment“:Political Stakeholder

Cor

pora

tions

Regulators

Governments

PoliticalParties

Associations

ConsumerOrg.

FinancialInstit.

NGOsEmployees

SuppliersShare-holders

Customers

„Contextual Environment“:Public Stakeholder

„Transactual Environment“:Marketal Stakeholder

„Contextual Environment“:Political Stakeholder

Cor

pora

tions

Regulators

Governments

PoliticalParties

Associations

ConsumerOrg.

FinancialInstit.

NGOs

© SAI Platform & IMD 2012

Which transmission belts are stakeholders using?

NGOs/Consumer Organisations

Communities/ Cities

Governments /Regulators

Media

International

Agencies

Employees/

unions

Scientific Community

Shareholders/ Investors/ customers

Business and Industry

© SAI Platform & IMD 2012 19

Example: Retailers

“Retailers are actively asking direct questions about what we are doing on sustainable agriculture” (Environmental Strategy Manager, F&B company)

“WalMart and Tesco are currently pushing very hard for more sustainable

products.” (Manager, CSR reporting. Supplier of F&B industry)

© SAI Platform & IMD 2012 20

Input Industry

Trade

Processor

Food Industry

Restaurants

Consumer Farming Systems

Catering

Retailer

How do stakeholders act as transmission belts for SA issues

Stakeholders

SA ISSUES

SA ISSUES

© SAI Platform & IMD 2012

Map and prioritize the issues

Which issues are the most relevant and why?

How do you prioritize the issues?

Strategy means choice

© SAI Platform & IMD 2012 22

Issues in the food and beverage industry

Pesticides Pollution Labor issues Traceability

Traceability Obesity Nutrition/Health Allergies Responsible marketing Alcohol abuse Advertising to children Packaging Waste Recycling

Pollution - chemicals/pesticides Soil degradation Long term raw material supply Human rights Poverty Child labor Worker health and safety

Eco-efficiency/Energy Water security Food safety/traceability Emissions (air and water) Packaging waste /Recycling Health and safety of employees Diversity Long term raw material supply

Human rights Work conditions Corruption/Bribery Fair trade Animal welfare

Corruption/bribery Quality Food safety/traceability Packaging waste Recycling Transport (‘food miles’)

Sustainable agriculture Prices/Farmers income Animal welfare Water security Sustainable aquaculture Fair trade Slavery Traceability

InputIndustry

TradeProcessor

Food Industry

Restaurants

ConsumerFarmer

Catering

RetailerInput

IndustryTradeProcessor

Food Industry

Restaurants

ConsumerFarmer

Catering

RetailerFarming systems

© SAI Platform & IMD 2012

The value of value drivers: Contribution of managing sustainability issues to value creation?

Product excellence or profit focus is no longer “does it”

Figures are not enough

Share prices are increasingly dependent on intangible concepts such as Brand value or Intrinsic corporate competence and knowledge

© SAI Platform & IMD 2012

What’s needed?

individual assessment of problems

application of managerial knowledge of global as well as local context of business decisions

© SAI Platform & IMD 2012

The added value of sustainability

Sustainability is about finding a balance between economic, social and environmental factors

Social engagement

Environmental performance

Economic viability

Superior value

creation

© SAI Platform & IMD 2012 26

So managing sustainability issues makes a clear contribution to shareholder value

* Adapted from Rappaport (1986)

Value Drivers Stakeholder satisfaction

Operational readiness Strategy

& vision

Innovation in product & services Others…

Dividends and share prices

Shareholder Value

Cost management

Sales growth

duration Capital deployed

Value Contribution

Employee motivation,

Working relation with regulators

EHS management

systems, Resource efficiency

Openness to society and new markets,

Brand value and reputation

More incentives for innovation, especially de-materialization services

Sustainability contribution (examples)

© SAI Platform & IMD 2012

Competitiveness

VALUE DR I VERS

Bottom line

« We can improve our brand value. »

« We can cash in on opportunities (new

products/services). »

« We can be a first mover.»

« We can save money by reducing costs. »

« We can attract talent.»

« We can reduce risk. »

Stakeholder Pressure

Water Obesity Animal welfare

Natural resources

Farmers livelihoods

Climate change

Sustainability Issues

Changing dynamics Food & Beverage Industry Business Context

A business case is not found. It has to be built.

RIGHT T H I N G T O D O

© SAI Platform & IMD 2012

Back up slides

© SAI Platform & IMD 2012 29

“Sustainability means thinking ahead in terms of possibilities.”

Example of business case narrative: Heineken

Heineken has taken the initiative to promote sustainable farming with the objective to keep barley farming an attractive proposition to farmers. The initiative evolved to a partnership between growers, buyers and processing industry. The focus is on the complete rotation plan rather than on a single crop. Farmers are empowered to make smart choices regarding rotation scheme, soil scan, fertilisation plan and crop protection keeping in mind where they want to be in 10 years.

© SAI Platform & IMD 2012 30

Example of business case narrative: DeLaval

“Sustainable Dairy Farming is about reducing the environmental footprint of farms, while improving milk production, farm

profitability and the well-being of the people and animals involved. ”

© SAI Platform & IMD 2012 31

Example of business case narrative: Nestlé

“Creating Shared Value is a fundamental part of Nestlé's way of doing business that focuses on specific areas of the Company's core business activities – namely water, nutrition, and rural development – where value can best be created both for society and shareholders.”

Nestlé launched in August 2010 an initiative to create value across the coffee supply chain, from farmers to consumers to Nestlé own coffee brands.

© SAI Platform & IMD 2012 32

Example of business case narrative: Delhaize

“Sustainable sourcing must take account of how goods are produced and procured, as well as where. Our responsibility therefore ranges across issues of fair trade and fair conditions of work .”

© SAI Platform & IMD 2012 33

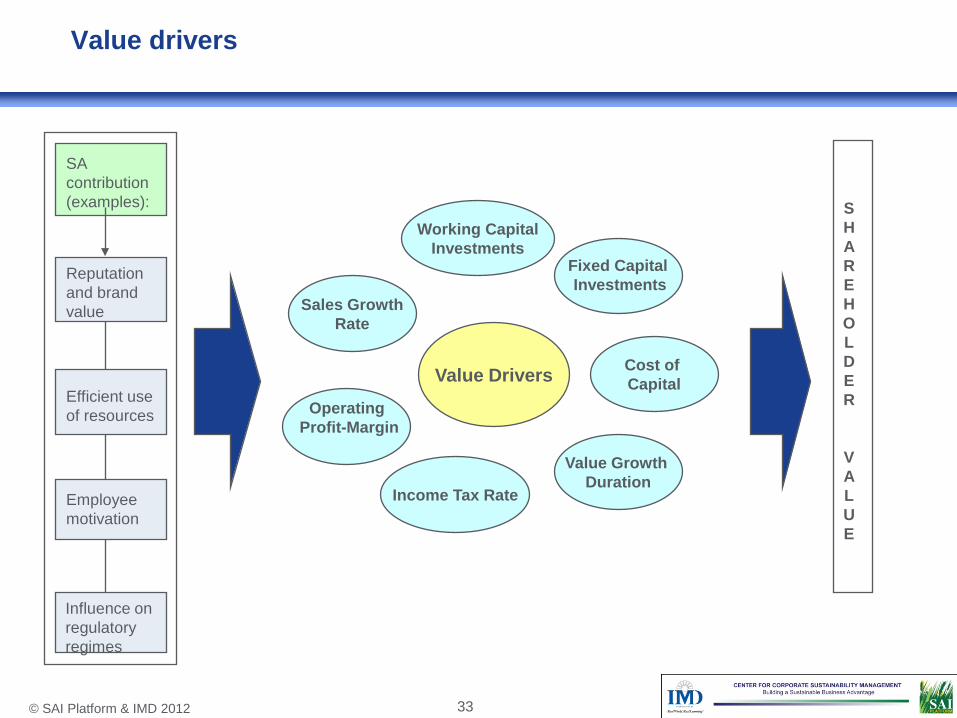

SA contribution (examples):

Reputation and brand value

Efficient use of resources

Employee motivation

Influence on regulatory regimes

S H A R E H O L D E R

V A L U E

Value Drivers Cost of Capital

Value Growth Duration

Operating Profit-Margin

Sales Growth Rate

Income Tax Rate

Working Capital Investments

Fixed Capital Investments

Value drivers

© SAI Platform & IMD 2012 34

SA issues affecting strategic risks and opportunities

Radical innovation for new products and markets

Economic performance

Social performance

Environmental performance

Incremental improvements in

SA issues affecting operational risks and opportunities

Economic value

• Brand value and reputation • License to operate • Attract and retain talent

Net cost decreases through incremental innovation

Net revenue increases through radical innovation

Systemization of sustainability issues, value drivers and relevant corporate activities

• Local air pollution • Biodiversity

• Health • Safety

• Human rights • Monetary flows

Obesity / Malnutrition Sustainable Agriculture

© SAI Platform & IMD 2012 35

Example: Ben & Jerry’s

27.5 31.6 31.9 34.9 37.9 42.8 47.66 52.94

43.2 38 36.7 35.5 33.633.6

32.31 26.4

22.8 20.616.6 14.4 14.4

10.910.8

1.2 2.34.1 7.3 7.4 6.2

5.52 4.571.4 1.8 2.11.2 1.15.4 7.5 10.7 6.4 4.9 4.4 2.51 2.6

10.2

0

10

20

30

40

50

60

70

80

90

100

2002 2003 2004 2005 2006 2007 2008 2009

Ben & Jerry's Haagen Dazs Own Label Green & Blacks The Skinny Cow Others

Ben & Jerry’s is a pioneer in supporting environmental and social causes with the direct engagement of consumers,

suppliers and local communities and results in the market are

consistently good.

© SAI Platform & IMD 2012

Back up slides

© SAI Platform & IMD 2012

BARRIERS: to progress in sustainable sourcing

Reported pain points Engagement, change,

reward Knowledge

Resource leverage

Lack of middle management buy-in

Short-term mindsets Difficulties in integrating into

business models Organizational silos Difficulties in making the

business case across departments and BUs

Non-integration of CSM targets within rewards and evaluation systems

Lack of systematic performance measurement and benchmarking

Difficulties in building effective networks to support innovation

Barriers to transforming markets/educating customers

Lack of quantification tools of specific business cases and emerging risks

Lack of adequate KPIs

Poor cost effectiveness of

activities related to sustainable sourcing

Difficulties in pushing energy/resource savings to the next level

High cost of innovation Low impact on brand

leverage

Responses from 22 global organizations participating in CSM workshop in April 2009

© SAI Platform & IMD 2012

Example: Competitive disadvantage

Lower environmental and social standards in sourcing within emerging markets creates a ‘non level playing field’ Amongst other factors, this impacts competitiveness of

for ex. Europe-based manufacturing and services Where legislation either does not exist or is not complied

with, global companies are sometimes required to adopt a quasi-governmental role to legitimize themselves

© SAI Platform & IMD 2012

Managers shying away from complexity Fragmentation of demand for internalization of issues

Business relevance has not been thought through or

highlighted in the company strategy Value drivers for sustainability action unidentified and

unconsolidated in the minds of managers

Weak/weakly exploited business cases are due to:

© SAI Platform & IMD 2012

The food and beverage industry value chain: Issues

Pesticides Pollution Labor issues Traceability

Traceability Obesity Nutrition/Health Allergies Responsible marketing Alcohol abuse Advertising to children Packaging Waste Recycling

Emissions – Air, water, soil Soil degradation Long term raw material supply Human rights Poverty Child labor Worker health and safety

Eco-efficiency/Energy Water security Food safety/traceability Emissions (air and water) Packaging waste /Recycling Health and safety of employees Diversity

Human rights Work conditions Corruption/Bribery Fair trade Animal welfare

Corruption/bribery Quality Food safety/traceability Packaging waste Recycling Transport (‘food miles’) Health - obesity

Sustainable agriculture Sustainable aquaculture Animal welfare Water security Fair trade Slavery Traceability Biofuels

InputIndustry

TradeProcessor

Food Industry

Restaurants

ConsumerFarmer

Catering

RetailerInput

IndustryTradeProcessor

Food Industry

Restaurants

ConsumerFarmer

Catering

Retailer

© SAI Platform & IMD 2012

Value Drivers Food security/Health

Sustainability issues affecting strategic risks and opportunities

Climate Change

Radical innovation for new products and markets

H&S performance

Social performance

Environmental performance

Incremental improvements in

• Local air pollution • Biodiversity

• Human rights • Monetary flows

Sustainability issues affecting operational risks and opportunities

• Health • Safety

Economic value

• Brand value and reputation • License to operate • Attract and retain talent

Net cost decreases through incremental innovation

Net revenue increases through radical innovation

© SAI Platform & IMD 2012

Current focus of stakeholder pressure

Attention on known branded global US or European companies Small and medium-sized companies produce between

two thirds and three quarters of nation’s GNP and are often linked to similar social and environmental issues Large, often state-owned companies in emerging

markets are more ruthless in behavior but rarely in the spotlight

© SAI Platform & IMD 2012

Drivers and response

Processes determining actions Companies come under direct pressure from NGOs/media to take

responsibility for risks in the supply chain Companies decide that they need to include suppliers in their due diligence

to reduce risk An observed event with other companies/industries drives the agenda (i.e.

NIKE)

Drivers Reputation/brand/license to operate

- Risk management - Retaining or increasing brand value

Criteria determining actions Level of perceived corporate exposure to supplier behaviour Compliance requirements

© SAI Platform & IMD 2012

The Responsible Corporate Customer: Influencing suppliers

Clearly defined mission Ensure responsible environmental and social behaviour of suppliers

Set and enforce standards in the way suppliers do business

Ensure compliance with EHS regulation

Ensure production according to a number of set sustainability principles

Highly focused on “first tier” suppliers

© SAI Platform & IMD 2012

So what type of tools do companies use to source sustainably?

Assessment criteria Very industry specific Environmental criteria clear (EU a highly regulated environment) Social criteria much less defined

Actions, processes and tools Questionnaires Part of supplier qualifying process and audit approach (checklists), Supplier guidelines Monitoring/enforcement (beyond 'tick-box’ exercise) – “going and

seeing” Sign-offs on business principles Pilot projects Partnerships with suppliers/coaching companies (particularly in Asia)

– Preferred supplier relationships

© SAI Platform & IMD 2012

What do we mean by a partnership?

A sustainability partnership as a form of collaboration that includes one corporation and any other combination of actors (government, civil society and corporate sector) aims to create social and/or environmental benefits

Partnership “Hub”

Partner 2 Partner 3

Partner 1

Drivers Formation and utilization Effects

• Complexity • Stakeholder

pressure • Key individuals • Organizational

cultures

• On Companies • On other

partners • On Individuals • Social and

environmental • Industry and

business systems

Replication

• Scope • Barriers • Success

factors

• Composition • Mission • Barriers and success factors • Key processes and activities • Key events • Key strengths and weaknesses

© SAI Platform & IMD 2012

Examples of Roundtables/Dialogues/partnerships/ Certification Schemes

Aquaculture Dialogues

© SAI Platform & IMD 2012

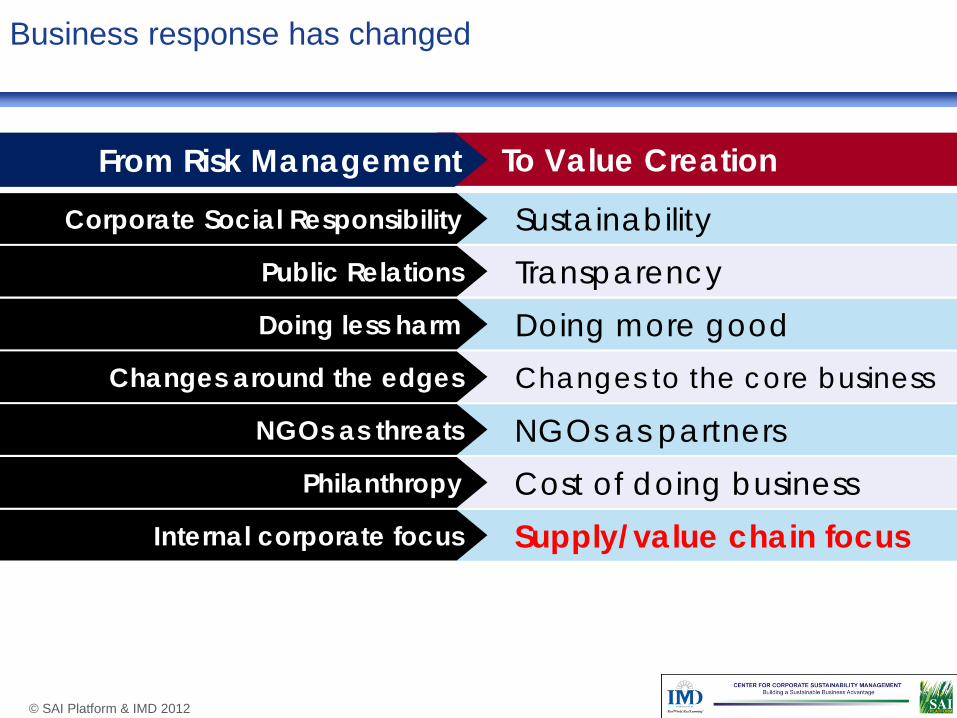

To Value Creation

Sustainability Transparency Doing more good Changes to the core business

NGOs as partners Cost of doing business Supply/value chain focus

From Risk Management Corporate Social Responsibility

Public Relations

Doing less harm

Changes around the edges

NGOs as threats

Philanthropy

Internal corporate focus

Business response has changed

© SAI Platform & IMD 2012

A value proposition of sustainability for global companies

Sustainable agriculture is about securing long-term supply of strategic resources allowing companies to stay in business and keep producing what their customers and consumers need

Sustainability is NOT ONLY a differentiator, but

a potential entry point to markets and a key to securing existing markets

© SAI Platform & IMD 2012

Unilever’s business case for sustainable sourcing - agricultural

“Changing weather patterns, water scarcity and unsustainable farming practices are putting pressure on agricultural supplies.

Food security is increasingly under threat as standards of living improve around the world and demand for food increases.

Sustainable agricultural sourcing is therefore a strategic priority for our business and brands.

Building on many years of work in this area and as part of our Sustainable Living Plan, we have set ourselves a new target to source 100% of our agricultural raw materials sustainably by 2020”.

© SAI Platform & IMD 2012

So where are we now?

© SAI Platform & IMD 2012

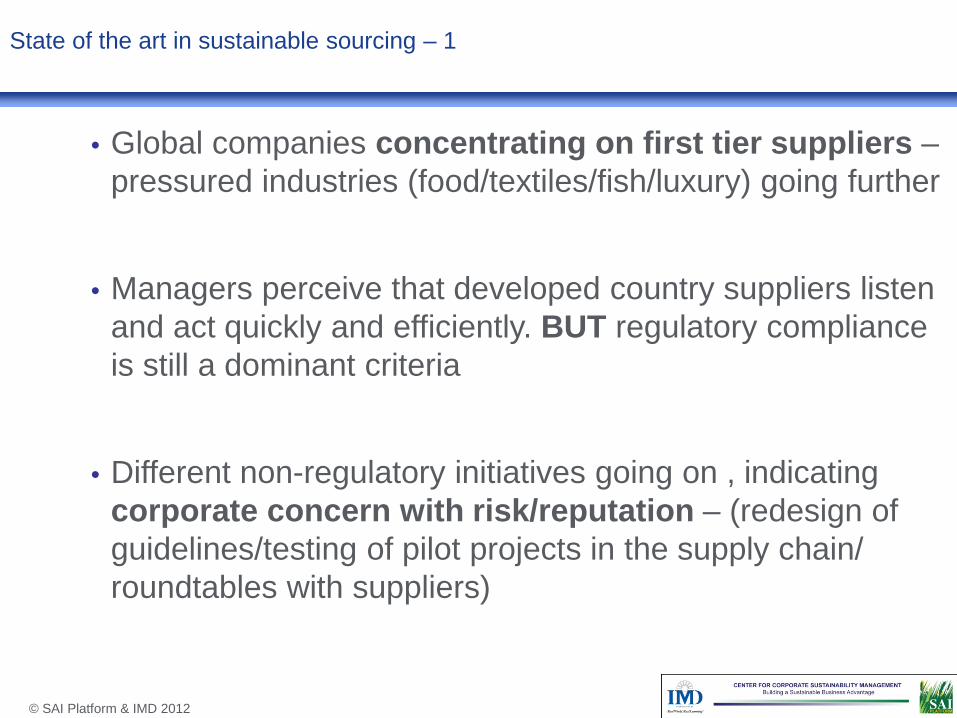

State of the art in sustainable sourcing – 1

• Global companies concentrating on first tier suppliers –pressured industries (food/textiles/fish/luxury) going further

• Managers perceive that developed country suppliers listen and act quickly and efficiently. BUT regulatory compliance is still a dominant criteria

• Different non-regulatory initiatives going on , indicating corporate concern with risk/reputation – (redesign of guidelines/testing of pilot projects in the supply chain/ roundtables with suppliers)

© SAI Platform & IMD 2012

State of the art in sustainable sourcing – 2

• Asian supply chain challenges – cultural differences (EHS/human rights issues), non enforcement of regulation by government, monitoring and evaluation difficulties

• Long-term relationships based on trust/partnerships viewed as most effective strategy

• Overall, a step-by-step continuous improvement rather than a ‘leap-frog’ approach

© SAI Platform & IMD 2012

State of the art in sustainable sourcing – 3

Supplying companies are generally meeting expectations in Europe/US – if they do not, they lose business (‘open and shut’ business case).

Difficulties remain in Asia but…….. Corporate customers are very aware of where the power sits and

outside of compliance issues, can define own standards. although this has led to sometimes excessive diversity in

expectations and demands from suppliers Corporate suppliers are reactive rather than proactive unless

there is a product responsibility risk

© SAI Platform & IMD 2012

State of the art in sustainable sourcing – 4

What supplying companies should do differently Formalize management systems so as to manage customer

requirements Look back in the supply chain at own suppliers (‘domino effect’)

Be more proactive in asking for help – take on more of a

partnership/collaborative stance

© SAI Platform & IMD 2012

State of the art in sustainable sourcing – 5

• Success factors • Threat of impending legislation • Fewer suppliers facilitates monitoring and overview: For some industries,

numerous suppliers make it difficult to ‘keep tabs’

• Close, long-term, ‘trust’-laden relationships

• Stumbling blocks

• Non-enforcement of environmental and social legislation in Asia creates a non-level playing field, a competitive issue on a global level

• Lack of consumer willingness to pay: When consumers demand, business case is strengthened

• Prohibitive costs of going up further in the supply chain beyond first tier suppliers

© SAI Platform & IMD 2012

State of the art in sustainable sourcing – 6

Companies can expect…….

• Increasing stakeholder pressure transmitted up the value chain

• Over the next ten years, exponentially higher expectations leading to more stringent requirements

• Increased push for legislative solutions and enforced standards from NGOs (including consumer organisations) and unions

© SAI Platform & IMD 2012

State of the art in sustainable sourcing – 7

More homogeneous approaches, i.e. sharing of

questionnaires/checklists Implement of industry standards where feasible

Rationalization of lists of suppliers/reducing numbers to

increase level of overview

And more streamlining of requirements……….

© SAI Platform & IMD 2012

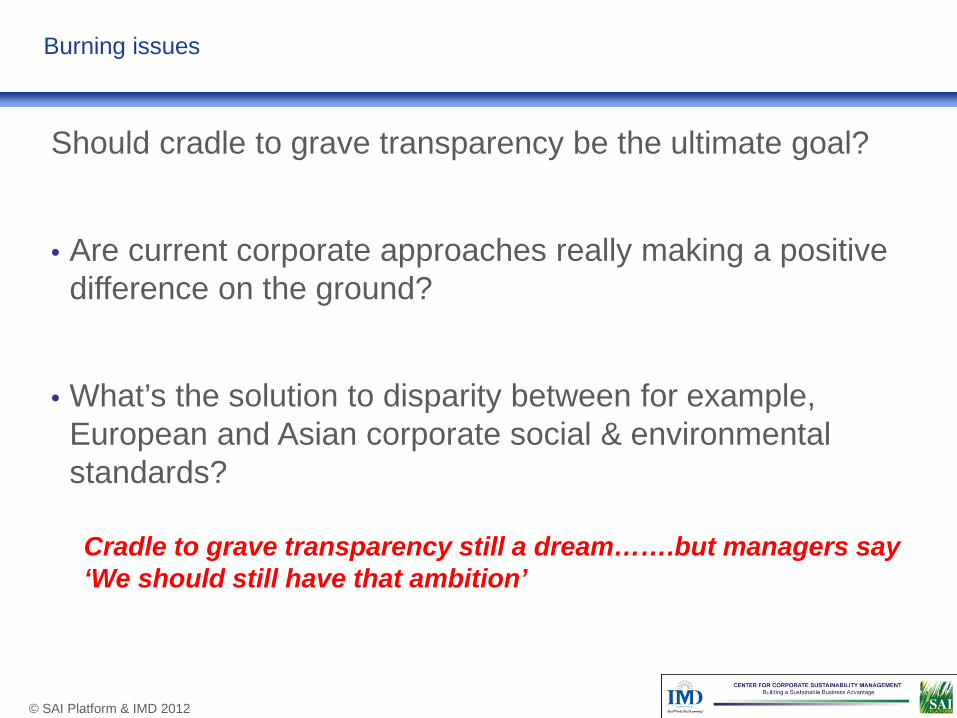

Burning issues

Should cradle to grave transparency be the ultimate goal?

• Are current corporate approaches really making a positive difference on the ground?

• What’s the solution to disparity between for example, European and Asian corporate social & environmental standards?

Cradle to grave transparency still a dream…….but managers say ‘We should still have that ambition’