building a world class tech & digital ecosystem...

TRANSCRIPT

BUILDING A WORLD CLASS TECH & DIGITAL ECOSYSTEM

IN GREATER BIRMINGHAM

WHITE PAPER

www.siliconcanal.co.uk

1Executive Summary 5

2 Silicon Canal 6

2.1. Digital Technology Definition 7

3Introduction 9

3.1. Economic Benefit 10

3.2. Human Benefit 10

4 Findings & Recommendations 12

5 Building a Tech Ecosystem 14

6 Example Ecosystems 16

6.1. Austin, Texas, US 16

6.2. Michigan, US 17

7 The Birmingham Technopolis Wheel 18

7.1. Geography 19

7.2. Surrounding Ecosystems 19

8

Supporting Groups 20

8.1. Events & Meetups 20

8.2. Investors 21

8.2.1. Problems 22

8.2.2. Recommendations 22

8.3. Mentorship 23

8.3.1. Problems 23

8.3.2. Recommendations 23

8.4. Incubators 24

8.4.1. Problems 24

8.4.2. Recommendations 25

8.5. Chamber of Commerce 26

8.5.1. Problems 26

8.5.2. Recommendations 26

8.6. Co-Working Space 26

8.6.1. Problems 26

8.6.2. Recommendations 26

Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 3

Author: Silicon Canal

Contents

2 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper

9 Academic 28

9.1. Problems 28

9.2. Recommendations 29

10 Emerging Businesses 30

10.1. Startups 30

10.1.1. Problems 30

10.1.2. Recommendations 31

10.2. Scale-ups 31

10.2.1. Scale-ups Have a Dynamic

Effect on Local Ecosystems 32

10.2.2. Problems 32

10.2.3. Recommendations 32

10.3. SMEs 32

10.3.1. Problems 32

10.3.2. Recommendations 32

10.4. Midsize Businesses 33

10.4.1. Problems 33

10.4.2. Recommendations 33

11

Large Corporates 34

11.1. Problems 36

11.2. Recommendations 37

12 Local Government 38

12.1. Problems 38

12.2. Recommendations 39

13 Central Government 40

13.1. Problems 40

13.2. Recommendations 42

14 Appendix 43

14.1. Authors 43

14.1.1. Contributing Authors 43

4 Greater Birmingham Building a Digital Technology Innovation Cluster White Paper4 Greater Birmingham Building a Digital Technology Innovation Cluster White Paper

1

Executive Summary

4 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 5

Digital technology businesses are at the heart of the UK economy and are playing an important role in driving growth. The impact of this dynamic sector is profound, predicated on a fundamental belief in innovation and doing things differently. Digital technology businesses are transforming the employment landscape, driving productivity, and reimagining traditional industries.

Greater Birmingham’s identity is largely

characterised by its history; city of

a thousand trades, birth city of the

industrial revolution, home of the Lunar

Society and the heart of the automotive

industry. But what is its modern day

brand, what does Greater Birmingham

stand for in 2016?

With a diverse and young workforce,

strong transport connections, one of the

highest qualities of life in the country,

Greater Birmingham has all the raw

ingredients. Greater Birmingham has

a huge opportunity to grow into one

of Europe’s strongest tech & digital

ecosystems but in order for that to

happen, the ecosystem requires the

building blocks and, most important of all,

it needs leadership.

While many would focus on just the

current strengths and shout about these,

the journey really starts with having

a shared understanding of the gaps,

along with a clear strategy that supports

the sector to accelerate its output both

economically and creatively.

This document examines the Greater

Birmingham digital technology

ecosystem, identifies how it can improve

and suggests potential solutions to

grow the ecosystem into a successful

ecosystem that competes on an

international stage.

As technology advances so quickly it

now plays a pivotal role in stimulating

economic growth and a city’s GVA (Gross

Value Added), therefore it is essential

that we invest in and increase our

efforts towards rapid acceleration of the

tech and digital sectors across Greater

Birmingham.

For those working in technology,

a thriving technology ecosystem

means more talent to hire for growing

businesses, more technology companies

to work for, a better and wider variety of

learning and networking opportunities

to grow personally, and a feeling of

belonging to something big and exciting.

We believe that together we can make

this happen in Greater Birmingham.

2

Silicon CanalThis paper was produced

and co-ordinated by

Silicon Canal ambassadors.

Silicon Canal is a community interest

company with a mission to create a

world class digital technology ecosystem

across Greater Birmingham. Silicon

Canal is connecting, promoting and

supporting tech and digital businesses

from freelancers and startups through to

multinationals. Together, we can make

Greater Birmingham a beacon for tech

and digital companies.

Silicon Canal is entirely run by volunteers,

contributing their time and resources

because they care about the Greater

Birmingham technology ecosystem. We

are very thankful to our sponsors who

provide cash support for things like the

development of our directory (available

at www.siliconcanal.co.uk), the printing

of this paper and other activities.

Provides a software or firmware-based product or

service as its primary business

Primarily operates over a digital platform, such as applications or websites

Produces hardware products that directly enable

software-driven devices

OR

2.1. Digital Technology Definition

Greater Birmingham Building a Digital Technology Innovation Cluster White Paper 7

OR

Throughout this paper we refer to

technology and digital companies for

which we have adopted TechCityUK’s

definition of a “digital technology

company”. This is distinct from a more

generic “technology company”.

Many companies today use digital

channels for buying, selling and

exchanging information. This, however,

does not mean that the company is

intrinsically digital. A restaurant with

a website is not a digital technology

company, while a site that enables its

customers to order from restaurants

all over the city is. Equally, many

companies are evolving from a legacy

to a digital model.

A broad definition of: “any company

whose primary capability is producing

software or delivering software-enabled

hardware”, this is expanded to include

primary characteristics of a digital

technology company being:

6 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 7

1.46MPEOPLE

15%OF COMPANIES

5.4%GROWTH

3

IntroductionThere are over 1.46m people in digital employment all around the country. 15% of companies formed in the UK between 2013–14 were digital. A recent Tech Nation review shows people employed by digital companies in the UK is set to grow by 5.4% by 2020, which is higher than projected total job growth.1

In the last 35 years, two of the top ten

fastest growing UK occupations have

been in the technology sector. The

number of IT managers employed in the

UK has risen by a factor of 6.5, to over

327,000. This is coupled with the rise of

programmers and software developers

by a factor of 3, to more than 274,0002.

Employee growth for the IT industry

was 11.6% for London in 2013 and only

2.6% for the rest of the UK3. London

also currently accounts for 35% of the

UK’s tech turnover, with the South East

in second place with 22%; this means

more than half of the UK’s technology

turnover comes from the capital or the

South East. In fact, London has over 30%

of UK ICT businesses, which is its largest

share in any sector4.

If we look at the West Midlands in

comparison, it holds less than 3% of the

UK tech turnover. This contrast is even

more noticeable if we take into account

the populations of the regions; London

has almost 1.5 times the population

of the West Midlands, but has more

than 11 times the amount of technology

turnover. The following image shows

where Birmingham sits compared to

other cities in the UK.

This paper examines the Greater

Birmingham technology ecosystem,

identifies its current weaknesses and

suggests potential solutions to grow

the ecosystem into a successful world-

competing ecosystem. It should be noted

that building an ecosystem is a 20 year

journey and Greater Birmingham is at

the beginning of this journey. Greater

Birmingham is deliberately not defined

in geographical terms because Silicon

Canal has a policy of being open and

geographical boundaries prevent this.

Birmingham is seen as the centre of

gravity for the ecosystem.

BERKSHIRE

INNER LONDON

CAMBRIDGESHIRE CC

OUTER LONDON – WEST & NORTH WEST

OXFORDSHIRE

BRIGHTON AND HOVE

GLOUCESTERSHIRE, WILTSHIRE AND BRISTOL/BATH

OUTER LONDON – SO UTH

EDINBURGH, CITY OF

GLASGOW

GREATER MANCHE STER

BOURNEMOUTH & POOLE

LEEDS AREA

NORTHUMBERLA ND & TYNE WEAR

OUTER LONDON – EAST AND NORTH EAST

BIRMINGH AM

SOUTH YORKSH IRE

LIVERPOOL

NORFOLK

WORCESTERSHI RE

SOUTH WALES

DUNDEE & AN GUS

EAST YORKS HIRE & NORTHERN LINCOLNSHIRE

NORTHERN IRE LAND

0% 2% 4% 6% 8% 10% 12% 14%

Digital Employment as a % of Total Employment in the area

Lead sources:DuedilCareer BuilderNovember 2014, ONS

1 http://www.techcityuk.com/investors/#investor-top

2 http://www.techcityuk.com/investors/#investor-top

3 Office For National Statistics. Business Register and Employment Survey (BRES) 2013 provisional. 25 September 2014.

4 Department for Business, Innovation & Skills. Business population estimates for the UK and regions: 2013 statistical release. 23 October 2013.

8 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 9

3.2. Human BenefitFor members of the ecosystem, whether

they are a freelancer, startup founder

or working for a business of any size,

the benefits of a world class Greater

Birmingham tech ecosystem are similar:

3.1. Economic BenefitIn order for cities to compete economically, not just at a national level but on an international stage, they need to constantly evolve their business ecosystems and one of the keys to this is the encouragement and environment for innovation. This requires a city to change its skills and business base in line with world demand, which in today’s economy means constant change.

Birmingham has traditionally been the powerhouse of the automotive

industry and advanced engineering sector, and the region has long been

recognised as a city of entrepreneurial endeavour across a number of

sectors. For example, two of the world’s leading banks were established in

Birmingham (Midland Bank - now HSBC & TSB).

After a fallow period of under-investment and slow growth across business

and industry, Birmingham is experiencing a period of rapid and exceptional

growth. Investment in infrastructure has never been higher (it is one of

the highest in Europe) and confidence has returned across businesses in

traditional areas such as advanced engineering and automotive, as well

as the high value knowledge economies such as Business, Professional

and Financial Services (BPFS), Life Sciences, and Information, Technology,

Electronics & Communications (ITEC) (particularly marked with HSBC’s

relocation of its head office to the city).

The rapid acceleration of technology and its industries throughout the

world has demanded that digital adoption and innovation is embraced by

every sector and industry. Technology has become vital to every company’s

operations and success, and it’s usage and adoption is critical for growth.

Innovation is at the heart of all advances in tech and digital, and companies

that successfully innovate are well positioned as leaders within their fields.

If Birmingham is to compete on an international stage and continue its rapid

growth then it must continually create an environment that stimulates the

production of goods and services of a world-class nature. The information

revolution requires digital to be at the heart of a city’s ability to compete

and this must penetrate all areas, from Local Government, city infrastructure

through to businesses.

As the successful growth of Birmingham was built on its entrepreneurial

spirit and its innovation across industry, science, commerce and the arts,

the city is well placed and well regarded to lead with new advances in

technology and to adopt digital practices, products and services.

In a recent KPMG report, Birmingham was named as the 4th largest tech

area within the UK. Whilst this reflects the good work done within the city

in the sector, it shows that much is still to be done and that there is a large

opportunity for growth.

In addition, as technology advances so quickly and now plays a pivotal

role in stimulating economic growth and a city’s GVA*, it is essential that we

invest in and increase our efforts towards rapid acceleration of the tech and

digital sectors within the city.

GREATER JOB OPPORTUNITIES

HIGHER EARNINGS CEILING

GREATER RANGE OF JOBS

£

10 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 11

*GVA (Gross Value Added)

4

Findings & RecommendationsThis paper makes 29 recommendations for strengthening the Greater Birmingham tech ecosystem.Here are the key finding themes:

The ecosystem lacks depth

in any key segment. We have

some tech investors but not

enough. We have some University

spinouts but not enough. We

have some large tech companies

but not enough. We have some

startups but not enough. None

of the key stakeholders in any

given segment could be regarded

as outstanding enough to create

the rising tide required to benefit

others to rise with them.

The ecosystem is fragmented and siloed with some amazing

elements but with limited

collaboration and no joint

thinking or agenda.

The ecosystem lacks visibility at any level, be that locally,

nationally or internationally.

This ecosystem features some

great companies but they are

rarely profiled, and external

parties often assume these

companies are based elsewhere.

Here are the key recommendations:

Promote Raise the profile of the ecosystem locally and nationally.

Actions:

1. Identify key players across each segment of the ecosystem through a directory.

2. Create an ambassador programme and sign up 100 ambassadors.

3. Appoint a PR agency to promote the ecosystem.

4. Establish annual tech awards to promote the ecosystem.

5. Host industry leading tech conferences.

6. Promote and support the “Make it in Birmingham” campaign.

12 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 13

”It’s typical of Brum that the modern world was invented in Handsworth and nobody knows about it.”

Steven Knight, Peaky Blinders creator (http://www.theguardian.com/travel/2016/apr/29/steven-knight-peaky-blinders-birmingham)

Collaborate Foster collaboration in the ecosystem to create more joined up thinking.

Actions:

1. Working groups for different incubators and academic institutions to work together.

2. Increase tech networking events that attract a wider more diverse audience.

3. Enhance entrepreneur-to-entrepreneur learning opportunities.

4. More activity-based events where people get to use and practice business growth skills (i.e. hackathons).

Leadership Identify and elect a Mayor of Digital (MoD) for Greater Birmingham. Someone who can lead the agenda and act as a spokesperson for the ecosystem.

Actions:

1. Outline the role, identify a group of eligible candidates, run elections and find funding for the role.

2. Support MoD to put Greater Birmingham on the UK tech map in a similar way to what Tech North has achieved.

Support Foster key elements of support for the ecosystem: mentorship, investment, incubators, academic partnerships.

Actions:

1. Establish directory of mentors available for ecosystem players and promote this.

2. Support companies to be investment ready and promote them to investors.

3. Support the establishment of additional incubators in Greater Birmingham.

5

Building a Tech Ecosystem

Based on the research of Smilor et al., clusters require four prerequisites:

the achievement of scientific pre-eminence

the development and maintenance of new technologies for emerging industries

the attraction of major technology companies

the creation of home-grown technology companies

Fred Phillips (Austin, Texas Technopolis)

states that a region that succeeds is

likely to have “a robust local value chain

including strong R&D, manufacturing,

marketing and distribution and intensive

international connections; a critical

mass of companies in one or more

well defined ‘clusters’; and a relatively

compact geography.

Smilor, Gibson, and Kozmetsky

developed the conceptual framework of

the Technopolis Wheel, first published in

19885. The wheel is used for modelling

the interplay of high-technology

development and regional economic

growth in conjunction with seven key

segments: The research university; large

and startup technology firms; federal,

state, and local government; and support

groups (e.g. chamber of commerce,

venture and angel capital, IP lawyers

and other business professionals). The

Technopolis Wheel opposite has been

altered to reflect a UK six key segment

model. This model has been used to

analyse the strengths and weaknesses

of the Greater Birmingham ecosystem.

For the purposes of this white paper the

geography of Greater Birmingham is not

defined because this gives us the largest

remit to include as many contributing

elements as possible. Birmingham is

treated as the centre of the ecosystem

as it contains all the elements. However,

research shows geography plays an

important part in establishing a functional

ecosystem, so this may be revisited.

5 Creating The Technopolis, (Eds.) Smilor, Kozmetsky, and Gibson (1988c)

ACADEMIC

Computer Science

Business

Engineering

LARGE CORPORATES

FTSE 500 HQ’s

Major Sales or R&D

Major Employer

EMERGING COMPANIES

(STARTUPS)

University Spinouts

Large Company Spinouts

Other

LOCAL GOVERNMENT

Quality of Life

Competitive Rates

Infastructure

SUPPORT GROUPS

Community

Chamber of Commerce

Venture Capital

Angel Networks

Business

Incubators

CENTRAL GOVERNMENT

Sponsored Research

Programs

Education Support

14 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 15

TECHNOPOLIS WHEEL

6

Example EcosystemsWhen evaluating Greater Birmingham as a Technopolis6 it is useful to look at other cities to understand how they created a successful ecosystem. Two US case studies have been chosen because in-depth research data is available and only limited data is currently available for Europe.

6 “polis” is Greek for city-state

6.2. Michigan, USThis section is taken directly from “Rising to the Challenge: U.S. Innovation Policy for

the Global Economy” by National Research Council (US).

The steep decline in Michigan’s auto manufacturing industry, which led to the loss

of 800,000 jobs over the past decade, prompted state economic development

officials to launch an intensive drive to develop new industrial clusters. The goal was

to both diversify the state’s industrial base and to expand on its existing strengths in

automotive technologies and advanced manufacturing. Some 80% of U.S. automotive

R&D is done within a 50-mile radius of downtown Detroit.

After an extensive analysis, the Michigan Economic Development Corp. (MEDC) in

2005 targeted six industries: advanced energy storage, solar power, wind turbine

manufacturing, bio-energy, advanced materials, and defense. The campaign to

nurture a cluster in advanced batteries – a manufacturing industry that at the time

was based almost entirely in Asia—was launched. Of the $2.4 billion allocated by the

Department of Energy to advanced battery manufacturing projects under the American

Reinvestment and Recovery Act of 2009, $1.3 billion went to Michigan-based factories.

At a National Academies symposium on Michigan’s battery initiative, then Michigan

Governor Jennifer Granholm declared that the state “is well on its way to becoming the

advanced battery capital of the world.”

Michigan’s approach is characterized by a comprehensive strategy that included

investments in R&D, generous tax incentives, extensive training programs for engineers

and skilled production workers, and public-private partnerships that brought together

universities, industry, government agencies, and the U.S. Army.

6.1. Austin, Texas, USThis section is taken directly from “Sustaining The Technopolis: High-Technology

Development in Austin, Texas”, 1988-2012 By: David V. Gibson and John Sibley Butler.

Up to the mid-1980s Austin was largely known as the Capital of Texas and home of The

University of Texas’ flagship campus. UT Austin graduate students usually had to leave

the region for Dallas, Houston, or the East and West coasts to find employment and to

build careers.

In 1983 all this began to change with the winning of a national competition for the

nation’s first for-profit R&D consortium, the Microelectronics and Computer Technology

Corporation (MCC), followed by the recruitment of 3M research operations in 1984 and

winning the national competition for a second major R&D consortium, Sematech in

1988. At the same time firms such as IBM, Motorola, AMD, and Applied Materials were

expanding their Austin-based R&D operations.

While under the radar of most Austinites, local entrepreneurs were launching ventures

that would become global corporations based in Austin: In 1976, four professors left

UT Austin’s Applied Research Labs to form National Instruments; a UT undergraduate

student and his girlfriend dropped out in 1978 to found SaferWay later known as Whole

Foods; and in 1982 Michael Dell, an undergraduate pre-med major, launched PC

Limited in his UT Austin dorm room.

The power of the Austin Model resides in the effectiveness of the formal and informal

collaboration, coordination, cooperation and at times synergy among influencers

networking across public and private sectors during key targets of opportunity.

16 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 17

7

The Birmingham Technopolis WheelThe Greater Birmingham ecosystem is mapped to the six key segments of the technopolis wheel below:

This shows that we have weakness across all six segments with a combined score of 23/60.

Further indicators are available from TechCity UK’s 2015 TechNation report:

Birmingham had a

51% INCREASE in digital companies

started between 2010 & 2013

Perception of

Birmingham and the region is 90 POINTS BELOW the UK average

Of all businesses

started in Birmingham

in 2013 & 2014, 14% WERE DIGITAL

COMPANIES

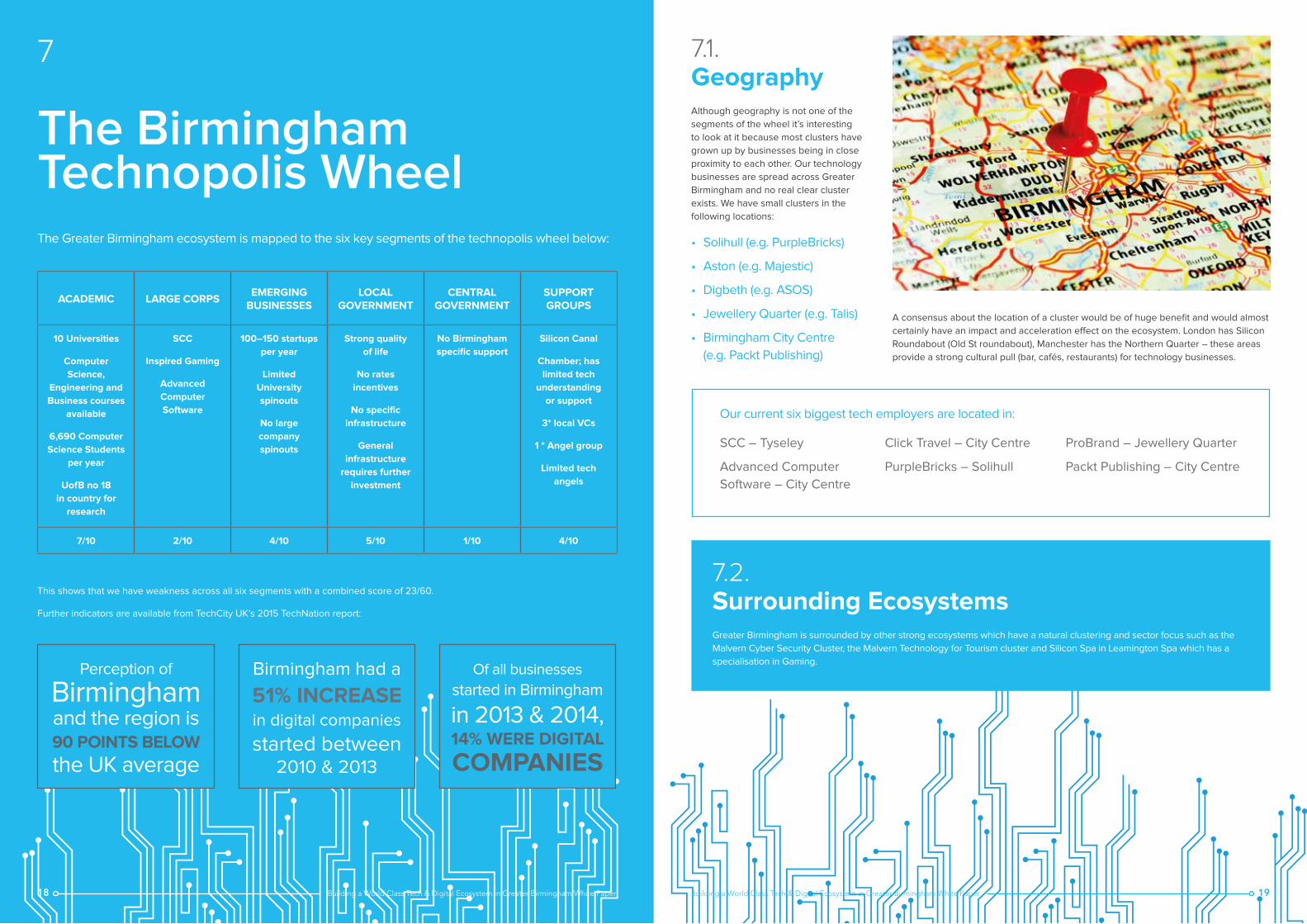

7.1. GeographyAlthough geography is not one of the

segments of the wheel it’s interesting

to look at it because most clusters have

grown up by businesses being in close

proximity to each other. Our technology

businesses are spread across Greater

Birmingham and no real clear cluster

exists. We have small clusters in the

following locations:

• Solihull (e.g. PurpleBricks)

• Aston (e.g. Majestic)

• Digbeth (e.g. ASOS)

• Jewellery Quarter (e.g. Talis)

• Birmingham City Centre

(e.g. Packt Publishing)

ACADEMIC LARGE CORPSEMERGING

BUSINESSESLOCAL

GOVERNMENTCENTRAL

GOVERNMENTSUPPORT GROUPS

10 Universities

Computer

Science,

Engineering and

Business courses

available

6,690 Computer

Science Students

per year

UofB no 18

in country for

research

SCC

Inspired Gaming

Advanced

Computer

Software

100–150 startups

per year

Limited

University

spinouts

No large

company

spinouts

Strong quality

of life

No rates

incentives

No specific

infrastructure

General

infrastructure

requires further

investment

No Birmingham

specific support

Silicon Canal

Chamber; has

limited tech

understanding

or support

3* local VCs

1 * Angel group

Limited tech

angels

7/10 2/10 4/10 5/10 1/10 4/10

18 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 19

7.2. Surrounding EcosystemsGreater Birmingham is surrounded by other strong ecosystems which have a natural clustering and sector focus such as the

Malvern Cyber Security Cluster, the Malvern Technology for Tourism cluster and Silicon Spa in Leamington Spa which has a

specialisation in Gaming.

A consensus about the location of a cluster would be of huge benefit and would almost

certainly have an impact and acceleration effect on the ecosystem. London has Silicon

Roundabout (Old St roundabout), Manchester has the Northern Quarter – these areas

provide a strong cultural pull (bar, cafés, restaurants) for technology businesses.

Our current six biggest tech employers are located in:

SCC – Tyseley

Advanced Computer

Software – City Centre

ProBrand – Jewellery Quarter

Packt Publishing – City Centre

Click Travel – City Centre

PurpleBricks – Solihull

8

Supporting GroupsThe table below shows that as an ecosystem we have some work to do to ensure that digital companies feel part of the ecosystem.

EDINBURGH, CITY OF

BRIGHTON & HOVE

LIVERPOOL

INNER LONDON

GLOUCESTERSHIRE, WILTSHIRE & BRIS TOL/BATH

NORTHUMERLAND & TYNE & WEAR

EAST YORKSHIRE AND NORTHERN LINCOLNSHIRE

GREATER MANCHESTER

BOURNEMOUTH AND POOLE

BIRMINGHAM

NORTHERN IRELAND

CAMBRIDGESHIRE CC

SOUTH YORKSHIRE

NORFOLK

SOUTH WALES

OXFORDSHIRE

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

CLUSTER ASSOCIATION

A ranking of cities, where digital companies felt part of a cluster (Cluster Association)

Source:Tech Nation, Feb 2015, ONS Categorisation

8.1. Events & MeetupsGreater Birmingham now boasts over

50 tech/digital events per month ranging

from technology specific to the more

sociable. There are also a number of

annual conferences that are driving

national and international speakers to

the ecosystem, the most notable of

those is Canvas run by 383 Project.

All of these events, meetups and

conferences are helping to link the

ecosystem and project it nationally.

7 Gov.uk - SEIS & EIS review

8 http://about.beauhurst.com/report-the-deal-2014-15

30

25

20

15

10

5

2011 2012 2013 2014Year

Crowd FundersAngel Networks

8.2. InvestorsVenture capital is a key source of

financing for new businesses. Venture

capital funds pool investors’ cash and

take equity stakes in startup firms

and small businesses with perceived,

long-term growth potential. In addition

to funding, venture firms typically

provide companies with managerial or

technical expertise and usually require

representation on the company’s board.

Venture capital is an important source

of funding startups that do not have

access to other capital, but which comes

first – do VCs flock to where startups are

already flourishing or do businesses set

up their offices in cities/areas that have

a healthy investment community?

Seed Crowd Funders versus Angel Networks

Angels play an important role, as they

often fund startups at the earliest stages

and bring a wealth of experience.

Nationally, there has been an increase

in the number of Angels, this has been

boosted by the introduction of SEIS

tax breaks in 2012. Since 2012 over

2700 have raised over £240m in SEIS

investment (May 2015)7. However there

has been a reduction in formal Angel

Networks over the same period8.

20 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 21

8.2.1. Problems

Limited number of VC’s:

Limited number of angel groups: 1 2 Very limited

tech angels: 3Growth in new businesses rose faster in

the West Midlands in the last two years

than in all other UK regions (FT 2014).

The Midlands is home to more than

317,000 enterprises, the third highest

nationally after London and the South

East (Barclays Entrepreneurs Index

2013). This said, while London is awash

with venture firms, there are only a

handful of venture firms in the region,

namely Finance Birmingham, Midven,

Catapult Ventures, and Mercia Fund.

At one point in time the ecosystem

had three active angel groups (CEBA,

Advantage Business Angels & Minerva).

Today only Minerva is still active, this

is mainly because commercially-viable,

alternative funding sources such as

crowdfunding have changed the market.

One of the contributing factors to the

success of many tech ecosystems is

angel investors who understand the tech

industry. Many of these angels made

their money through their own tech

startup or being an early employee of a

startup. Given Greater Birmingham has

not generated startups that have exited

there are not many tech angel investors,

those that are here have re-located or

made their money in other industries but

have an interest in tech.

8.2.2. Recommendations

Profile raising: Additional networking opportunities: 1 2 Create a tech specific angels

group in Birmingham: 3Invention and innovation have spurred

Silicon Valley’s growth with popular

press pouring out against-all-odds

success stories of entrepreneurs.

The visibility of Greater Birmingham’s

successful enterprises, and their venture

partners, needs to be developed

to signal the economic growth and

innovation in the area to a local, national

and international audience.

Venture firms should be encouraged to

collaborate with universities and local

tech clusters to educate entrepreneurs

and innovators about venture funding.

Events like VentureFest connect

investors with entrepreneurs, enabling

to generate greater economic impact

across Greater Birmingham.

This might be achieved with the

support of Minerva, as they already run

subgroups at multiple locations. The UK

Business Angel Association are keen to

support the establishment of a new angel

network in Greater Birmingham. If an

angel group is not a feasible option then

maybe a locally branded crowdfunding

site would be a suitable alternative.

8.3. MentorshipOne of the most powerful patterns in

successful startups is that the founders

have experienced mentors. Studies

have shown that companies, where a

founder is mentored by a top-performing

entrepreneur, are 3 times more likely

to be a top performing company9.

Almost every privately funded startup

acceleration programme is centred

around mentorship because it has a

huge positive impact on a startup’s

success chances.

8.3.1. Problems

Mentorship access: Mentorship quality:1 2Mentorship is generally restricted to

programmes that come attached with

conditions like rent, equity and fee

contracts. This puts some founders off

from participating.

There are not enough successful

founders in the region to provide

the large number of new starts with

advice. Therefore, advice is not readily

available on ideal levels, and the quality

sometimes suffers due to delivery by

under-qualified people (e.g. accountants,

lawyers, lecturers).

8.3.2. Recommendations

Online portal: Remote mentorship:1 2Provide an online portal for mentors that

any startup has access to, in some way.

Build a remote mentoring programme

where mentorship is delivered via video

conferencing. This will remove the

quality threshold of mentorship, and

is generally easier for mentors to

deliver advice.

9 http://techcrunch.com/2015/03/22/mentors-are-the-secret-weapons-of-successful-startups/

22 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 23

8.4. IncubatorsAn incubator can mean many things

to many people, but for the sake of

argument we define an incubator as

“a place that ideally has support staff

and equipment, made available at

low rent to new small businesses”.

Incubators vary in what they offer and

how long they support a new business,

typically they provide support from three

months through to one year. In most

cases incubators do not offer monetary

support, however, they will provide

startups with mentoring, desk space

and an internet connection.

Incubators are important for an

ecosystem as they support the earliest

stage entrepreneurs and position them

on the first rung on the ladder; they are

the ideal environment to educate the

next generation of entrepreneurs. They

also provide opportunities for young

people to hone valuable workplace

skills through internships and work

experience opportunities with startups.10

Incubated Entrepreneurs and startups

are likely to secure significant financial

investment – on average raising more

than £68,000. In addition to this, these

programmes are ideally placed to

quantify the number of startups still

operating. The figures for these startups

are encouraging, the survival rate for

startups reached almost 92%, compared

to a two-year survival rate of 75.6% for

all small businesses.11 Of the incubators

and startup programmes operating

within the UK in 2014, more than half

were launched within the last three

years – representing a 110% increase

since 2011. Despite efforts by the UK

Government to increase the number

of programmes operating outside of

London, almost two thirds (61%) are

based in the capital.

We have a number of incubators

across the ecosystem including;

Bizzinn, Entrepreneurs for the Future,

Entrepreneurial Spark, Serendip

incubator & Spark Business Incubator.

8.4.1. Problems

They are looking local:1

10 “the rise of the UK accelerator and incubator ecosystem.” 2014. 5 Nov. 2015 <http://cdn.news.o2.co.uk.s3.amazonaws.com/wp-content/uploads/2014/12/O2_WAYRA_Report_121214.pdf>

11 “the rise of the UK accelerator and incubator ecosystem.” 2014. 5 Nov. 2015 <http://cdn.news.o2.co.uk.s3.amazonaws.com/wp-content/uploads/2014/12/O2_WAYRA_Report_121214.pdf>

While a local incubator should support local talent, it is clear that the local talent pool is

not big enough. As a result they lower the bar of entry to increase numbers, which then

lowers the results and ends up in a race to the bottom. Because they look locally, they

have little or no national presence, and are therefore failing to promote the ecosystem

or attracting talent from other regions. If we look at some of the greatest incubators

around the world, we discover that they attract talent nationally and internationally

to their door, and act as brand ambassadors for their ecosystem. The corporate

incubators like Entrepreneurial Spark have a national presence but still recruit locally,

they do give some exposure of the ecosystem nationally, but it’s not clear by how

much. There are multiple reasons why they are only looking locally, some because they

are funded through European or Local Government grants and therefore restricted to

supporting local (funding strings). Or in the case of corporate incubators, they want

to grow business locally and have similar incubators across the country, which makes

them reluctant to overlap recruiting grounds.

They provide no next step:2Our incubators kick out startups at a rate of about 100-150 per year (Bizzinn = 10,

Entrepreneurs for the Future = 20, Entrepreneurial Spark = 80, Spark Business

Incubator = 10) but there is no logical next step for the startups. We don’t have an

accelerator, or an obvious funding route, that would keep them in the ecosystem.

Therefore, in all likelihood, they will either move away from the area or battle through

on their own, making the failure rate very high. We have very few standout startups in

the ecosystem that have made it beyond an A-Round of funding (Purple Bricks is the

exception but they never went through an incubator).

They think they are competing:3There appears to be the opinion, amongst the runners of the incubators, that they are

competing against each other, either for the limited European or Local Government

funding or for the startups themselves. This is not a zero sum game and it’s likely

more incubators will result in more startups being created. In London (strongest tech

ecosystem in Europe), there has been an explosion of incubators, although it’s not clear

what came first - the startup or the incubator.

8.4.2. Recommendations

Attract an international player:1If we are to play at an international level then we need to host an internationally

acclaimed incubator in the ecosystem. These take years to create and cost millions

in investment, so building our own is likely to take ten years, in what is now a very

competitive market. One option is to look to an established incubator and persuade

them to open a branch within our ecosystem. This is likely to work for a niche incubator

(connected car) as we are not able to show a deep startup talent pool to attract a

generalist incubator. Note: The Bakery (London based B2B incubator) is looking to

establish in Birmingham.

Incubator of incubatees:2A specialist incubator that focuses on providing support for graduates from other

incubators, providing continued support up to year two and focused on getting the

startups cash positive or securing additional investment, we believe that this would

almost certainly result in more successes. This could be an extension to an existing

incubator or a totally new provider backed by a combination of Local Government,

Corporates and Investors.

Incubator Working Group:3The creation of a working group that has the heads of each incubator on it, as well

as other stakeholders, would improve communication and collaboration between

incubators. This would hopefully lead to better resource usage (i.e. shared events,

mentors etc) and better placement of startups (to an appropriate incubator or passed

between where one is full).

24 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 25

8.5. Chamber of CommerceThe Greater Birmingham Chamber of

Commerce is a membership organisation

that provides support programmes and

a voice for local businesses.

8.5.1. Problems

Limited understanding or support for tech/digital businesses:1

It’s not clear that the Chamber has an understanding of the needs of digital businesses,

therefore, the support provided is likely to be generic. While this may not be an issue

for certain Digital businesses, it is clear startups require very specific support due to

their growth trajectory.

8.5.2. Recommendations

Education and support to the chamber:1A liaison and tech/digital advisor should be offered to the Chamber to help them better

support tech/digital businesses across Greater Birmingham.

8.6. Co-Working SpaceIn recent years, the number of

freelancers and independent workers

making up the global workforce has

risen exponentially.

Since 2008, the number of self-

employed people in the UK has risen

by almost 700,000 - from 3.8 to 4.5

million12. The Bank of England reported

earlier this year that ‘large numbers’

had chosen to go freelance, and one in

seven people are now believed to work

for themselves.

12 http://www.dailymail.co.uk/news/article-2992498/Jobs-boom-mothers-set-businesses-Number-self-employed-workers-risen-700-000-2008.html

8.6.1. Problems

No tech co-working space:1

Greater Birmingham has a lack of

co-working space in general and has

no dedicated tech working space that

would be akin to those in other cities,

such as TechHub, Central Working

or WeWork.

8.6.2. Recommendations

Attract external co-working spaces:1

Attract an internationally recognised

tech co-working space to establish itself

in Birmingham such as TechHub

or WeWork.

Co-working spaces, similar to

incubators, are designed to support

freelancers, entrepreneurs and startups.

But while incubators typically require

an application process, equity and a

commitment, co-working spaces allow

people to work on their own terms.

Co-working spaces offer more flexible

terms – one can usually rent space

indefinitely. Tenants of such office

spaces share rent costs, while still

reaping the benefits of solid professional

networks, a social workplace,

collaboration opportunities, and

extra office facilities (like cafés, wifi,

and gyms).

According to Co-Working London,

it now has 135 registered co-working

spaces. Manchester, a city half the size

of Birmingham, boasts over seven

co-working spaces.

Although not proven, it is likely that the

creation of co-working space results in

greater collaboration and startup creation.

26 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 27

9

AcademicGreater Birmingham has ten Universities

(University of Birmingham, Aston

University, Birmingham City University,

Newman University, University of

Law, BPP University, University

College Birmingham, University of

Wolverhampton, Warwick University and

Coventry University) and has around

5% of the UK’s developers and 6,690

students on computer science courses.

In the Complete University Guide the

University of Birmingham (10th) and

Aston University (34th) both rank in the

top 50 for Computer Science Courses.

The often cited reason as to why Silicon

Valley “got it right” was that university

leaders, such as Fred Terman, Provost

at Stanford, leveraged government

investment in R&D to expand their

departments, whilst at the same time

encouraging graduates, such as Hewlett

and Packard, to start new companies.

This created a virtuous circle as those

companies grew, not only recruiting

from nearby universities but also having

staff leave to start their own companies

or become venture capitalists, as they

cashed in their founder shares. Any

tech ecosystem therefore needs a tight

coupling between universities and local

established companies, startups

and entrepreneurs.

If an ecosystem is to build a future supply

of technologists and entrepreneurs then

it must also support, develop and inspire

from an early age, programs such as

STEMNET, Code Club, the Big Bang Fair,

Science Week are an important part of

the ecosystem.

9.1. Problems

Relevance of University curriculum:1As stated in the Coder Supply & Demand13 report “employers often feel that what

university graduates learn on courses has little or no practical relevance for commercial

activities.” Universities are under different pressures to industry, and are often focused

on producing computer scientists capable of becoming good lecturers, professors,

researchers, thinkers and coders, rather than business founders and leaders. Findings

from the IBM Institute for Business Value14 show that “in terms of economic value, only

51% of industry and academic leaders believe Higher Education is providing value for

money, and just 49% view it as contributing to economic growth and competitiveness.

The report Coder Supply & Demand by Chris Meah of the School articulates the

problem with the current coder supply in Greater Birmingham13.

Rising cost of education:2Demand for higher education is growing – and so are the costs. With the average

student debt in England now at £43,50015, many students, as well as parents are

asking “is it worth it?”, especially if there are no suitable jobs to be had at the end of a

university course. Computer Science has the highest graduate unemployment rate 14%;

strange when you consider everyone is crying out for technical and programming skills,

100,000 per year in fact.16

As education costs rise it is likely that more and more foreign students from wealthy

backgrounds will increasingly be those who can afford the high fees (Aston had 20%

foreign students in 2013). Whilst this is good for universities, it is not so good for local

employers, because these students will most likely be going back home on completion

of their education (due to Visa limitations).

Lack of spin outs (using University IP):3University of Birmingham’s Alta Innovations shows 21 spin outs, Aston University shows

16 spinouts, Birmingham City University shows just one spinout16. This compares to

Oxford University with 110 spinouts, Imperial College London which has 95 spinouts

and Cambridge University which has 93 spinouts. The University of Warwick, with 40

spinouts, is the ecosystem’s strongest.

13 http://siliconcanal.co.uk/wp-content/uploads/2016/01/Report-Birmingham-Coder-Supply-Demand.pdf 14 http://www-935.ibm.com/services/us/gbs/thoughtleadership/15 http://www.telegraph.co.uk/education/universityeducation/student-finance/9740974/English-students-in-twice-as-much-debt-as-rest-of-UK.html16 http://www.theguardian.com/higher-education-network/blog/2013/sep/16/computer-science-graduates-unemployment-bme17 http://www.spinoutsuk.co.uk/listings/university-listings/Default.aspx

9.2. Recommendations

Create better collaborations:1To fully exploit technology’s potential (as opposed to being steamrolled by it),

Higher Education leaders must collaborate more closely with industry leaders

and entrepreneurs. In this emerging ecosystem, one-on-one relationships will be

supplemented and replaced by a network of organisations contributing to better

and more relevant outcomes. The announcement of the new Universities Centre

at Innovation Birmingham Campus may be a step towards creating this collaboration.

Also the School of Code initiative is a great example of collaboration between

different groups.

Appoint an education ambassador:2Whilst creating better collaborations may be a medium term goal, an immediate benefit

could be achieved by having one or more education ambassadors as part of the Silicon

Canal community, whose role is to reach out to universities to guide them on the needs

of the tech community – maybe deliver guest lectures and become involved in the

curriculum of relevant courses (Computer Science, Business Studies, Marketing etc).

Encourage talent to stay or come back:3A strong drive to educate students about the reasons to stay should be undertaken,

publicising the benefits to students of staying (e.g. low housing costs, a growing

cultural scene, good transport links, high quality of life etc). The diversity that keeping

foreign students brings, is where innovation thrives. From 1995 to 2005, 52.4 percent

of engineering and technology startups in Silicon Valley had one or more people born

outside the United States as founders. Note that considering immigration reform was

also a recommendation from two recent TechUK reports. The Greater Birmingham

diaspora should also be targeted to return to the ecosystem, we are already seeing

many 30 somethings returning from London to start families.

CHRIS MEAH & BHISH PATELCo-founders of School of Code

28 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 29

10

Emerging Businesses10.1. StartupsA startup is an entrepreneurial venture or a new business in the form of a company designed to search for a repeatable and scalable business model. The key term here is scalable, there are many new businesses that are not startups because they are lifestyle businesses and not scalable businesses.

Startups are the new blood of any

tech ecosystem; they are the babies,

that become toddlers, that become

teenagers, that become the next

big corporate. The below shows the

evolution of a startup – this journey

takes anywhere between 3–10 years.

Startups, and particularly Scale-ups

(businesses growing 20% in revenue or

staff year on year), provide the highest

amount of employment growth of any

business type 18. Therefore, attracting or

creating startups with the potential of

becoming a scale-up are critical for the

sustainability and growth of an ecosystem.

10.1.1. Problems

Not producing enough startups:1Because the failure rates of startups are

so high, an ecosystem needs to produce

hundreds of quality startups on an annual

basis18. The ratios look like the diagram to the

right (this is based on US figures so may be

even worse for the UK), which means that if we

are creating just 200 startups per year across

the ecosystem, it is going to take us five years

to seed a startup that may end up becoming a

large corporate. The ecosystem needs to be

creating 500+ startups per year to create

a sustainable ecosystem.

Supportive environment: 2While the ecosystem has incubators supporting startups, these are silos with little support

available outside of those environments. When an individual thinks about starting a

startup they don’t think of this ecosystem as a place to do it – they look to London or

further afield, which means we are losing an important part of the supply at the earliest

stage. We have few mechanisms for discovering individuals who are looking to create

their own startup.

No ‘hero’ startups:3If you look at many ecosystems, one of the key ingredients for catalysing the

ecosystem is a successful startup that acts as a lightning rod for new startups to build

around. An example of this effect would be Skype and the ecosystem that grew up

around Skype in Estonia. The Greater Birmingham ecosystem doesn’t have that yet.

18 https://www.cbinsights.com/blog/venture-capital-funnel/

10.1.2. Recommendations

Champion Startups:1A ecosystem wide campaign to promote startups. A set of tech awards could be the

start of that but wider support from local media (Radio, TV, Digital News) is required to

promote starting a business as a viable alternative to employment.

Green Light programme:2The London Co-Fund has adopted a green light programme for vetting startups and

rating startups based on their investment readiness (Red, Amber, Green). A similar

scheme could be created in Greater Birmingham, and once we have established a

list of ‘Green Lighted’ startups it should be circulated to all European investors on a

monthly/quarterly basis. This would have the effect of raising the profile of the

ecosystem and individual startups.

STARTUP

ESTABLISHED

GROWTH

LARGE

1,000

100

10

1

A ‘scale-up’ is an enterprise with

average annualised growth in

employees or turnover greater than 20%

per annum over a three year period,

and with more than 10 employees at the

beginning of the observation period.

This is the same definition used by the

Organisation for Economic Co-operation

and Development (OECD), Nesta and

Endeavor, as well as many national and

international statistics agencies.

Scale-ups bring job creation and GVA

increases, which are disproportional to

their size. Just adding a few scale-ups

per year to Greater Birmingham would

have an exponential effect.

The OECD has conducted a detailed

study across 18 countries analysing the

link between the dynamic of business

growth (as measured by employment)

and economic growth. This found

that companies which have been in

existence more than five years, in

aggregate, reduced employment every

year between 2001 and 2011; whereas,

companies which were less than five

years old were, in aggregate, net job

creators in each of these years.19

The Scale-up report provides the

following factors, in order of importance,

as the key reasons why companies are

unable to scale in the UK.20

Companies have issues:

• Finding employees

to hire who have the

skills they need

• Building their

leadership capability

• Accessing customers in other

markets / home market

• Accessing the right

combination of finance

• Navigating infrastructure

The report tells us that in 2014

Birmingham and Solihull LEP had 229

Scale-ups across all sectors (i.e. not just

tech/digital). This compares to 420 in

Sheffield City Region and 233 in

Greater Manchester.

If you compare the Midlands on the basis

of population to growing companies then

this shows how far behind the Midlands

is. The following statement is taken from

“THE DEAL Making Sense of UK Equity

Investment 2014/15”.

“There’s a completely different picture

down in the Midlands – both East

35

23

2662

31

23

1217

20

26 93

30

30 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 31

19 http://www.oecd-ilibrary.org/science-and-technology/the-dynamics-of-employment-growth_5jz417hj6hg6-en

20 http://www.scaleupreport.org/scaleup-report.pdf

10.2. Scale-upsand West – where we’ve seen just 12

and 17 growing companies per million

respectively. To put it another way,

for every growing company we’ve

discovered in the East Midlands, we’ve

found more than seven in London and

almost five in the North East. This should

be extremely concerning for these

regions – it’s all well and good hoping

for a manufacturing recovery (although

there’s little sign of that yet) but the

region can’t rely on this alone. We’d

advise those involved in encouraging

growth in these areas to hop on a train

– north or south, it doesn’t matter – and

see what they can learn.”

10.2.1. Scale-ups Have a Dynamic Effect on Local Ecosystems

Scale-up companies can be major

contributors to local economies,

especially with regards to acting as role

models and inspiring others. Scale-

up companies can have a particularly

dynamic effect on local ecosystems

when they are clustered together,

buying goods and services from each

other, attracting and developing talented

people and building networks with the

local ecosystem. The top 50 fastest

growing companies around Cambridge,

for example, added more than 5,900

jobs between 2012 and 2013.

10.2.2. Problems

There are no identified scale-ups:1No organisation is identifying and tracking tech/digital scale-ups across Greater

Birmingham. Most organisations are not even aware of the term scale-up.

10.2.3. Recommendations

Identify scale-ups:1Identify, publish and track a list of Greater Birmingham tech/digital Scale-ups.

10.3. SMEsSmall to medium enterprises (<50

employees) make up the vast majority

of the digital businesses across Greater

Birmingham with 94% of creative firms

in the city being classed as micro-

businesses, employing fewer than ten

people21. Very few of these businesses

ever get beyond the £1m turnover (less

than 1%)22 and many are stagnant.

10.3.1. Problems

No voice:1Given the number of SMEs in the ecosystem they have no collective voice.

10.3.2. Recommendations

Identify & Promote:1Identify all the tech/digital SMEs in the ecosystem and then promote as many

as possible through Silicon Canal, national organisations such as TechCity and

media outlets.

Stagnant:2Many SMEs are not growing above the £1m turnover.

10.4. Midsize BusinessesMid-size tech businesses of between

50–250 employees are the future large

corporations and have very specific

needs. These businesses are more

likely to survive over the long term and

continue to grow compared to their

startup counterparts. While the region

has a range of these businesses

(Pro-Brand, Packt Publishing, Purple

Bricks, Click Travel, Mobile Fun, Names.

co.uk) they are often unknown by the

wider community and their engagement

with the ecosystem appears limited.

A mid-sized business may also be

a scale-up, if it is growing fast enough

to qualify.

10.4.1. Problems

Lack of tech talent:1This quote from Simon McLean, Executive Chairman at Click Travel describes the

problem. “For us it’s really quite simple: access to technical talent. So much so that we

now have development teams in Romania and Bulgaria.

We have a current live opportunity which highlights precisely the problem – we’ve

been hunting for a Software Test Engineer for over 6 months now, a position which we

wanted to fill locally in Birmingham. But we’ve interviewed no end of candidates and

not found anyone who is up to scratch, hence we’ve now hired in Romania.

From a financial perspective I think the West Midlands is very strong. We’re fortunate

enough not to need external financing, but if we did there are no end of opportunities

in the region, together with local specialists who can source finance from further afield.

10.4.2. Recommendations

Celebrate our mid-sized businesses:1Develop case studies for each business and signpost jobs. Create a future 20 list of our

next large corporates and publish this on an annual basis.

Lack of visibility:2Most of these mid-sized tech businesses are unknown to the ecosystem, making it

harder for them to recruit.

21 http://www.birmingham.gov.uk/cs/Satellite?blobcol=urldata&blobheader=application%2Fpdf&blobheadername1=Content-Disposition&blobkey=id&blobtable=MungoBlobs&blobwhere=122350444582-2&ssbinary=true&blobheadervalue1=attachment%3B+filename%3D90259Sector_Profile_Digital_%26_Creative.pdf

22 http://www.oxfordhandbooks.com/view/10.1093/oxfordhb/9780199546992.001.0001/oxfordhb-9780199546992-e-10

32 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 33

11

Large CorporatesForward thinking companies recognise that speed and agility will be key determining factors of success in the digital, consumer-driven economy. As change accelerates, organisations will need to rethink how their business environment operates, how they partner and how they interact with customers. A recent IBM Institute for Business Value report23 highlighted that these changes are “necessitating the emergence of new economic ecosystems, as organisations recognise they cannot navigate this future alone. They must embrace the concept of mutuality, a level of formal or informal collaboration among organisations around shared ideals, standards, or goals”.

23 http://www-935.ibm.com/services/us/gbs/thoughtleadership/ecosystempartnering/

24 http://www.techuk.org/insights/reports/item/2099-techuk-manifesto

25 http://digitalbirmingham.co.uk/publication/1802/

In a business context, an ecosystem

is a complex web of interdependent

enterprises and relationships aimed

at creating and allocating business

value. There is something mutual

and multiplicative about business

ecosystems — the whole is greater than

the sum of the individual parts. If this

was not the case, there would be no

incentive to be part of the system.24

For a large company to locate into a

particular city or region, it no longer

needs just economic incentives, good

infrastructure and a pool of talent it

can draw upon for future employees.

It now also needs access to a broader

ecosystem consisting of SME’s,

entrepreneurs, universities, local

government and other organisations

who formally or informally operate

together to produce something of

greater value for the mutual benefit

of the ecosystem as a whole.

The importance of tech clusters to

the UK economy was recognised in a

recent techUK24 report where one of

the recommendations was that central

government (i.e. BIS and the Cabinet

Office) should work with clusters to

support and nurture local firms whilst at

the same time recognising the vital roles

universities play. Large corporates can

play their part in this by engaging with

and supporting these clusters.

Large corporates are more likely to

engage if they know there are economic

benefits to be had by providing

technology to smaller local firms. For

example, the recent Greater Birmingham

Digital Audit25 highlighted that whilst

digital technology is having a significant

impact on the growth of businesses in

Greater Birmingham (54% of businesses

say their turnover increased during

2014 and one in four attribute this

growth to increased use of digital

technology), too few businesses are

taking advantage of digital technology.

Only 43% of businesses state they

fully understand the benefits digital

technology can bring – and just over a

third of businesses identified investment

in digital technologies as a high priority

for the future.

The other key element large

corporations bring to an ecosystem

are spin outs. A great example of this

is that of PayPal in the US. The original

founders and employees of PayPal are

known as the PayPal Mafia and have

gone on to found some of the biggest

tech companies. The picture opposite

shows some of their achievements

(picture courtesy of Rudi Leismann).

34 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 35

11.1. Problems

Competition rather than collaboration:1In the mid 1960’s New Jersey tried to emulate the “magic” of Silicon Valley by hiring

Fred Terman, who was retiring from Stanford, to try and recreate the culture of

cooperation and information exchange that had defined that region. Terman drafted

a plan to build a new institution like Stanford but the plan never got off the ground

because industry would not cooperate. RCA would not sign up for a partnership with

Bell Labs, Esso didn’t want to share its best researchers with a university, and Merck

and other drug firms wanted to keep their research dollars in house.

Having a great ecosystem is no good if no one knows about it:2

The issue Birmingham (along with other cities outside the Greater London area) has

is that no matter how great their ecosystems are, they will always be overwhelmed

by the sheer volume of success stories being generated by a London-focused media.

Companies, especially international ones, will only see this and naturally be drawn to

that area.

Lack of Large Corporations: 3The Greater Birmingham ecosystem can count the large tech companies on one hand.

Attracting them appears to be difficult because there are no special tax breaks, it

doesn’t possess a particularly strong talent pool, or have any key customers or partners

based here, either.

11.2. Recommendations

Create value through collaboration rather than competition:1

In traditional markets, value creation is incremental as organisations typically cover

costs plus some return on assets. In ecosystems, organisations create value through

their engagement within the system as a whole. Once companies realise there is

more to be gained through collaboration rather than competition, they are more likely

to participate in the ecosystem. We need to develop good news stories and positive

references for how success has been achieved through collaboration and publicise

these to potential corporates, showing them that Greater Birmingham has a thriving

ecosystem that they can benefit from by joining. For example, Greater Birmingham

has a great history in manufacturing, and even though this has been greatly diminished

over the past two decades, there is no reason why traditional manufacturing should

not take advantage of new technologies, such as the Internet of Things (IoT) being

developed by smaller startups. Such collaborations could be used as a success story

to sell to other corporates encouraging them to move (or expand) into the area.

Promote the ecosystem through one off and regular events:2

There are already a number of tech events and meetups in and around Birmingham

which happen on an ad-hoc basis. These tend to be focused on particular areas

of interest and take place in regular locations, but by and large don’t attract large

corporates unless they are heard about by employees who happen to live in the area.

We should hold one big event to kick things off, where as many large corporates as

possible are invited to launch the whitepaper and manifesto, where the benefits of

them participating in the wider area ecosystem are highlighted. We should try and

engage national as well as local media in this event.

Target specific Large Corporations:3Work with Marketing Birmingham to devise a specific soft landing package that is

competitive. Draw up a shortlist of target large corporates and actively try to attract

them to Greater Birmingham.

36 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 37

12

Local GovernmentThe last detailed profile of Birmingham’s digital and creative sector from Birmingham Council was published in 201227. It reported that this sector contributed £890 million to the city’s economy and boasted 5800 businesses within the region, employing 34,000 people. If the predicted growth of this sector was correct, creative and digital businesses in Birmingham should now be contributing over £1 billion into the city’s economy. These figures looked at the very wide remit of Creative businesses and did not focus on just tech and digital.

A lot of what is needed to create the

UK’s leading digital ecosystem is already

in place; high-quality graduates, a young

population, incubators and partnerships

with local universities. However, there is

no joined-up thinking or programmes led

by local government to support potential

scale-up businesses within this sector.

12.1. Problems

A bystander of the local digital ecosystem:1As we have already identified, most of the ingredients to create the UK’s leading

tech city are already here. However, tech companies have taken it upon themselves

to create a credible, nationally recognised tech ecosystem/cluster. The TechUK

Manifesto recommends that a body similar to the Government Digital Service should be

established to act at the regional level28, and that is something that Silicon Canal would

fully endorse. This would provide the tech industry with a platform to share ideas with

decision makers and influence local business policy.

The bias toward traditional industries:2It’s natural that Birmingham and the Black Country predominantly provide support for

manufacturing businesses within the region. There is a proud manufacturing tradition

in the area and millions of jobs depend on this industry thriving. But by ignoring other

emerging sectors (such as the digital and creative sector), local government runs the

risk of making the same mistakes that the UK Government has made over the past

two decades.

Limited understanding of Digital & Tech:3Birmingham City Council has no experienced digital/tech person in a senior position

who champions the sector. The Local Enterprise Partnership (LEP) also has little

representation for digital.

27 http://www.birmingham.gov.uk/cs/Satellite?blobcol=urldata&blobheader=application%2Fpdf&blobheadername1=Content-Disposition&blobkey=id&blobtable=MungoBlobs&blobwhere=122350444582-2&ssbinary=true&blobheadervalue1=attachment%3B+filename%3D90259Sector_Profile_Digital_%26_Creative.pdf

28 Securing our digital future: The TechUK manifesto for growth and jobs 2015-2020

12.2. Recommendations

Get involved, promote, support and celebrate:1A great example of how local government can champion the creative and digital sector in Birmingham is by publishing data from the

fastest growing companies in the region. This approach was trialled by the business community (in partnership with ‘The Silicon Valley

comes to the UK’ initiative) in Cambridge.29 Publishing up-to-date data on the performance of the fastest growing companies in the

region will be a valuable resource for investors, journalists and potential business partners. It will demonstrate economic strength

to outsiders, whilst providing a dynamic effect on the local ecosystem by encouraging the cluster of companies to use each other’s

service or product.

Remodel grants and financial assistance that is available:2One of the biggest finance initiatives from central government over the last parliament was the introduction of the Regional Growth

Fund. This initiative wasn’t geared towards the digital and creative sector, therefore, tech SMEs failed to benefit from any direct

financial assistance from central government. Regardless of this, we believe that the Regional Growth Fund has not produced effective

results through the investment that was made.

30The National Audit Office has reported that the cost of each job created through the Regional Growth Fund cost £37,400. If we were

to compare this with the Endeavour programme that focuses on emerging economies, which cost just £405 per job created (many

of which were tech jobs), we can conclude that the model of finance, or the focus of the funding, is wrong. Local government should

investigate this further and deliver a new working model for financial support to a wider range of local businesses.

29 http://www.nesta.org.uk/news/new-big-data-resource-puts-cambridge-cluster-map

30 https://www.nao.org.uk/report/progress-report-on-the-regional-growth-fund/

31 http://www.labourdigital.org/

Keep the talent that we develop:3We would encourage local government to adopt a policy suggestion from the former shadow business secretary, Chuka Umunna,

and begin lobbying parliament to reform visa regulations to create a one-year “Programmers’ Passport” for digitally skilled migrants

from outside of the EU31. This would allow local businesses to recruit foreign students that completed their studies in the region, which

would provide tech businesses in Greater Birmingham with wider pool of developers, thus reducing the skills gap in the short-term.

Deputy Mayor of Digital:4Support the establishment of a Mayor for Birmingham and the appointment of a Deputy Mayor of Digital.

Deliver a Manifesto:5Create a digital manifesto to drive forward the Greater Birmingham agenda.

38 Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper Building a World Class Tech & Digital Ecosystem in Greater Birmingham White Paper 39

13

Central GovernmentThe UK’s technology trade association,

formerly known as Intellect, was

relaunched in 2013 as TechUK. Its

mission is to engage with the whole

tech sector, ranging from startups to

international IT suppliers and consumer

tech firms. During the relaunch the

TechUK chief executive, Julian David,

revealed that new research figures

showed that there are twice as many

tech companies in the UK than the

government realised.

It could be argued that for over a

generation, through successive

governments, the emergence of the

UK’s tech industry was growing at

a rapid pace and completely under

the radar of appointed policy makers

that were ignorant to a sector that

was playing a vital, innovative role by

supporting a number of key industries

throughout the global recession.

Would a UK government of the past

two decades display a similar kind

of ignorance to the true size of the

manufacturing industry? Or the financial

sector? Thankfully, steps were taken

to compensate for this oversight, as

the coalition government established

the Ministerial Digital Taskforce (which

still remains) to deliver a strategy that

supports and encourages further growth

in the tech industry.

13.1. Problems

A delayed response to a rapidly growing sector:1

The explosion of user-friendly

technology, since the turn of the

millennium, has left the UK government

playing catch up – in 2013, 90% of the

world’s data was created in the two

years that preceded it33 and the tech

industry had to organically accelerate

its growth to meet demand. Despite

the unprecedented demand for new

technology solutions, recent figures

suggest that there is still someway to go

before it slows down. A quarter of SMEs

still do not possess basic digital skills and

there is a proven positive link between

digital skill levels and turnover growth.34