budget polices general government · budget polices general government this section includes budget...

TRANSCRIPT

BUDGET POLICES General Government

This section includes budget polices on the following: • Beautification Fund • Debt Financing • Investment Earnings • Long-Term

Compensation Strategy

• Property Tax • Capital Reserve Fund • Contingency Fund • Equipment

Replacement Fund • Risk Management • Sustainability

Budget Policies

_________________________________ D-2 City of Mercer Island 2007-2008 Budget

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-3

Beautification Fund Background The Beautification Fund was created in 1980 by Council ordinance. According to the ordinance, Business and Occupation Tax (B&O) revenues are deposited into the Beautification Fund. By Council policy, B&O tax collections were effectively split 65% to the Beautification Fund and 35% to the Contingency Fund in 2005 and 2006. The stated purposes of the Beautification Fund are: • Installation and maintenance of landscaping including plants and other landscaped materials on public

property or easements; • Acquisition, operation and maintenance of any building, facility, property or easement for park,

recreation, or open space purposes; • Undergrounding of power lines and lighting facilities for the operation and maintenance thereof on

public property or easements; • Promotion and support of a Central Business District (CBD) revitalization program; • The promotion, support, acquisition and installation of public art on public property or easements; • Acquisition or leasing of parking spaces for Mercer Island residents for the purpose of providing

additional parking; • Enforcement of parking restrictions, providing signage related to parking, providing permits and any

other expenses related to parking restrictions; and • All expenses including, but not limited to, professional fees, printing and publishing, incurred in

connection with the above-listed purposes. Effective January 1, 2006, the Council simplified the B&O tax structure increasing annual exemptions from $20,000 to $150,000, establishing a uniform tax rate of .10%, and changing the annual gross receipts threshold for filing quarterly B&O tax returns from $100,000 to $1,000,000. In addition to simplifying the tax structure for payers, this action all served to simplify the administrative process for the City staff. Historically, expenditures of the Beautification Fund included the operation and maintenance of the medians and planters in the downtown, the holiday lighting program, support for the chamber of commerce, maintenance of I-90 corridor landscaping and City support for The Northwest Center’s operation of the Mary Wayte Pool. Since creation of the Fund, a substantial sum has been spent on other beautification projects and the broad language of the Code has been construed to permit a variety of undertakings.

Budget Policies

_________________________________ D-4 City of Mercer Island 2007-2008 Budget

Budget Policies for 2007 - 2008 • Adjust the allocation of B&O tax revenue beginning in 2007 so that 100% goes to the Beautification

Fund to cover current beautification program costs. • Support the same expenditure items funded in 2005-2006 with exception of the $55,000 annual

transfer to the vegetation management CIP project (which will be funded from another source). • Monitor the effects of state-mandated B&O tax apportionment. The proposed biennial budget

assumes that apportionment, which takes effect in January 2008, will result in an estimated loss of $50,000 annually.

2007 – 2008 Budget Impact

2005 2006 2007 2008Actual Forecast Budget Budget

Revenues

Opening Fund Balance 619,624$ 653,688$ 455,428$ 153,528$ Business and Occupation Tax 331,123 205,000 330,000 330,000 Permit Parking Program 4,050 3,405 0 4,000

Subtotal Revenues 335,173$ 208,405$ 330,000$ 334,000$

Total Revenues 954,797$ 862,093$ 785,428$ 487,528$

ExpendituresChamber of Commerce 14,400$ 14,400$ 14,400$ 14,400$ Town Center Beautification 94,368 108,500 113,000 117,000 Financial Services 10,106 10,000 8,000 8,000 Permit Parking Program 0 1,500 1,500 1,500 Mary Wayte Pool Operations 100,000 100,000 100,000 100,000 Town Center Plaza 0 60,000 350,000 0 Interfund Transfers to I-90 21,320 57,265 45,000 62,000 Interfund Transfers to CIP for Veg Mgmt. 60,915 55,000 0 0

Subtotal Expenditures 301,109$ 406,665$ 631,900$ 302,900$

Ending Fund Balance 653,688$ 455,428$ 153,528$ 184,628$

Total Expenditures and Fund Balance 954,797$ 862,093$ 785,428$ 487,528$

Budget Policies

_________________________________ D-5 City of Mercer Island 2007-2008 Budget

Debt Financing Background The City of Mercer Island has prudently issued little debt over the years, maintaining a sizable debt capacity. The City has consistently followed a conservative fiscal management policy, which is reflected by the high Aa1 rating that Moody's has given the City for bond issues. Mercer Island is the only city in the State with an Aa1 rating – only Bellevue and Seattle have a higher rating. The total amount of debt obligations for cities is limited by state law. Mercer Island has significant legal capacity for funding foreseeable debt issues. As of 12/30/2005, the available debt capacity margin was $170,903,309 for general purposes (voted, non-voted and lease debt), $176,492,669 for utility purposes (voted debt), and $176,147,410 for open space and parks facilities (voted debt). When the city voters annexed to the King County Library district (KCLS) in 1994, KCLS agreed to pay $206,576 per year for 20 years as a lease purchase for the city constructed library building. That lease revenue is used to offset the amount due on the GO library bonds, thus reducing the total voted tax levy for the Mercer Island residents each year. That is reflected in the table below. In 1996, the City refinanced three bond issues to obtain interest savings for the taxpayers. The total present value savings for these issues amounted to over $548,000. In 2003, the City issued $2.29 million in Councilmanic bonds to acquire the property that the Community Center at Mercerview was sited on. This was in preparation for building a new community center at the site. In 2004, after a year of study and design, the Council authorized the construction of a new $12.4 million community center. Most of that project is being paid with City reserves, however, $2,040,000 in Councilmanic bonds were issued to complete the financing package. Both of these bond issues are being funded out of the Capital Improvement Fund through real estate excise taxes. Budget Policies for 2007 – 2008 • The City will confine long-term borrowing to fund approved capital improvement projects that

cannot be financed from current revenues. • The City will use debt financing only when the following conditions exist:

Object of the expenditure is a major new capital asset. Object of expenditure can be used by residents/taxpayers in the future. There are insufficient existing capital revenues available. All the revenue is needed at the same time (i.e. the project cannot be phased over time).

• When the City finances capital projects by issuing bonds, it will pay back the bonds within a period not to exceed the expected useful life of the project.

• Whenever possible, the City will use special assessment, revenue or other self-supporting bonds instead of general obligation bonds.

• The City will not use long-term debt for current operations.

Budget Policies

_________________________________ D-6 City of Mercer Island 2007-2008 Budget

2007 - 2008 Budget Impact 2005 2006 2007 2008

Expenditures Actual Forecast Budget BudgetVoted Debt

1996 Refunding Bonds 359,203$ 360,190$ 360,310$ 199,060$ City Hall bonds 456,600 463,413 463,617 457,403 Total Voted Debt 815,803$ 823,603$ 823,927$ 656,463$ King County Library Payment (206,576)$ (206,576)$ (206,576)$ (206,576)$ Transfers from General Fund-Tax Reduction (170,000) (69,000)

Total Amount to be levied in taxes 439,227$ 548,027$ 617,351$ 449,887$ Non-voted Debt

Mercerview Property Acquisition 224,829$ 221,529$ 218,023$ 214,186$ CCMV Construction 148,185 151,310 149,310 152,310

Total Non-voted Debt 373,014$ 372,839$ 367,333$ 366,496$

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-7

Investment Earnings Background The City pools its cash and invests it in certificates of deposit (CD's) and other investments authorized by the Revised Code of Washington. To forecast interest earnings, the Finance Department computes the average cash balances for all funds for the year using an expected market interest rate of the most recent average earnings rate. By pooling and investing its cash, the City is able to obtain the best possible rate of return on its investment. City funds are always fully invested in a combination of timed deposits, money market accounts and an interest bearing checking account. For maximum interest earnings the City has all of our state revenues wired directly into a City account with the State Investment Pool. The State Investment Pool has the advantage of paying excellent rates while being liquid. Most of the City's funds are currently invested in the State Pool. Historically, the General Fund has collected all interest earnings and has held the investment certificates in its name. At the end of each month each fund with a positive cash balance that earns interest was allocated a portion of the current month's earnings based on the ratio of the fund's cash balance to the City's total cash balance. Beginning in 2007, interest earnings will be distributed as follows:

a. Water Utility Fund, Sewer Utility Fund, Storm Water Utility Fund, Firemen’s Pension, Youth Services Endowment Fund, and Contingency Fund based on cash balance;

b. LEOFF I long-term care reserve based on cash balance (this reserve will be moved from the Contingency Fund to the General Fund on 12/31/06);

c. $300,000 annually to the General Fund (which is approximately 1.5% of General Fund budget). This policy will be re-visited biennially to maintain the 1.5% allocation;

d. Street Fund, Capital Improvement Fund, and Technology & Equipment Fund for those CIP projects that have investment interest as a budgeted revenue source;

e. Any remaining balance would be allocated to the Capital Reserve Fund for unspecified CIP projects.

The City treasurer's primary objective in investing cash is to preserve the principle of the investment while striving to maximize investment returns. Budget Policy for 2007 - 2008 • Continue the cash investment policy and practice outlined above in 2007-2008. Conservatively

forecast interest revenues.

Budget Policies

_________________________________ D-8 City of Mercer Island 2007-2008 Budget

2007 - 2008 Budget Impact

Revenues ($1,000’s) 2005

Actual 2006

Forecast 2007

Budget 2008

Budget General Fund $274 $575 $300 $300 General Fund – LEOFF 1 Reserve 0 0 35 35 Other Funds 727 409 494 504 Total Revenues $ 1,001 $ 984 $ 829 $ 839

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-9

LEOFF I Retiree Costs Background Law Enforcement Officers and Fire Fighters (LEOFF) Retirement System membership is made up of all full-time law enforcement officers and fire fighters in the State of Washington. This retirement system was initiated in 1970, consolidating the several police pensions systems of First Class cities and the municipal firemen’s pension systems. As of October 1, 1977, LEOFF was divided into a two-tier system. All of those employed prior to October 1, 1977, became members of Plan I and those first employed on or after October 1, 1977, became members of Plan II. LEOFF Plan I provides the medical benefit of 100% reimbursement of all medically necessary expenses to each LEOFF Plan I member (members are persons who terminate service with five years or more of service but do not withdraw their contributions). LEOFF Plan I membership consists of active and retired members who are relatively young in age. This young age means the greatest impact of medical costs remains in the future. LEOFF Plan I Medical Benefit One of the major distinctions between LEOFF Plan I and Plan II is the LEOFF Plan I medical benefit. This benefit is set forth as follows:

“Whenever any active member, or any member retired… on account of… sickness… not caused or brought on by dissipation or abuse, of which the disability board shall be judge, is confined in any hospital or in home, and whether or not so confined, requires medical services, the employer shall pay… the necessary medical services not payable from some other source….” [RCW 41.26.150(1)]

In other words, the employer is required to pay all of the reasonable costs for medical services incurred by active and retired members not paid by insurance obtained by either the employer or someone else. These costs range from simple visits to a physician to major surgical procedures and placement in a nursing home. The statutory definition clearly defines the minimum medical services covered. While the minimum medical services are defined, it is possible that the scope of these enumerated medical services may be increased by a separate entity known as a Disability Board. Another important aspect of this medical benefit is the burden of payment. None of the cost is borne by retirement funds. Moreover, the state is not liable for any cost of this benefit. These costs are the complete responsibility of the individual LEOFF Plan I employer. The Disability Board The pivotal point in the extent of LEOFF Plan I medical costs is the local disability board. This board is responsible for the determination of duty and non-duty disability and the approval of medical care costs for LEOFF Plan I members within the jurisdiction. The Disability Board is made up of two council members, one LEOFF Plan I active or retired police officer, one LEOFF Plan I active or retired fire fighter, and one citizen at large. The Disability Board has the authority to decide the extent of what will be actually covered beyond the minimum LEOFF Plan I medical services, as well as whether or not the expense is a reasonable medical necessity. A LEOFF Plan I member may appeal disability board decisions directly to the state.

Budget Policies

_________________________________ D-10 City of Mercer Island 2007-2008 Budget

Insurance The provisions of LEOFF Plan I make clear that the employer is expected to utilize insurance to reduce the financial liability of the risks connected with the medical benefit. The City of Mercer Island insures the LEOFF Plan I members through the Association of Washington Cities (AWC) Employees Benefits Trust. The trust has entered into contracts with Regence Blue Shield to provide indemnity health care coverage and with Group Health Cooperative to provide managed health care coverage. However, these medical insurance Plans do not cover expenses related to long term care services. The Association of Washington Cities, through its Employee Benefit Trust offers long term care insurance Plans underwritten by UNUM Life Insurance Company of America. This Plan is structured to primarily meet the LEOFF Plan I liability for nursing home and in-home expense. Both in 1996 and in 2002, the City of Mercer Island received quotes directly from UNUM Life Insurance Company of America to cover the LEOFF Plan I members. In 1996, the annual cost to cover Mercer Island LEOFF Plan I members was in excess of $64,000 per year and covered approximately 60 percent of the total long term care expenses. Additionally, several LEOFF Plan I members were not insurable based on their health history. In 2002, the annual cost to cover the LEOFF Plan 1 members was in excess of $125,000. Government entitlement programs don’t offer complete protection either. Medicare was designed to help older people pay for the same kind of acute care as traditional health insurance, and it provides only limited post-hospital care. In fact, Medicare pays for less than 5 percent of long-term care costs. Medicaid, designed for low-income individuals, currently covers about half of the bills for nursing home residents. But the program has strict eligibility requirements that force middle-income participants to spend down their personal assets. The vast majority of Mercer Island’s LEOFF Plan I members would be ineligible for Medicaid benefits. Mercer Island Disability Board Long Term Care and Nursing Facility Care Rule The Disability Board approved long term care and nursing facility care procedures in October of 2002. These rules require the City to pay for long term care expenses based upon the average cost of three (3) nursing facilities or services in the member’s geographic locality for 24 hour-a-day care in a semi-private room as private pay. The Disability Board Secretary will determine the three (3) nursing facilities or services that will be used to average the cost. To date, the City has experienced two (2) long term care reimbursement claims. In February 2003, the City paid at total of $58,146 to satisfy its first claim for long term care expenses. The second claim amounted to $99,011 paid out in 2004 and 2005. There are thirty-nine (39) remaining City of Mercer Island LEOFF I members. The potential for future claims for long term care expenses from a number of Mercer Island LEOFF Plan I members is probable. Therefore, a source of funding must be considered and established. Funding Source To date, the City has accumulated $700,000 of a $1.1 million target to fund the LEOFF I long term care obligation. The LEOFF 1 members’ medical insurance premiums and direct medical costs have been absorbed through expenditure savings in the General Fund budget resulting from position vacancies and budgeting employee benefits based on full family coverage. Over the last four years in particular, however, the City’s ability to absorb these costs in this fashion has been eroded away completely due to

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-11

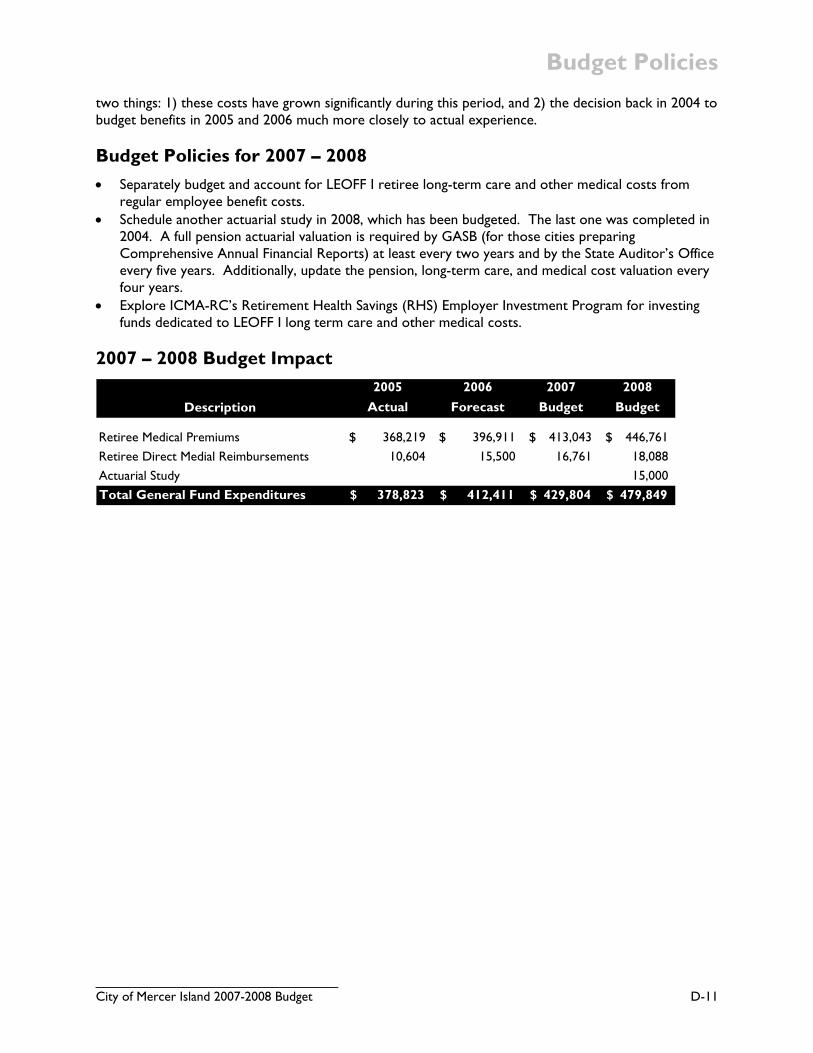

two things: 1) these costs have grown significantly during this period, and 2) the decision back in 2004 to budget benefits in 2005 and 2006 much more closely to actual experience. Budget Policies for 2007 – 2008 • Separately budget and account for LEOFF I retiree long-term care and other medical costs from

regular employee benefit costs. • Schedule another actuarial study in 2008, which has been budgeted. The last one was completed in

2004. A full pension actuarial valuation is required by GASB (for those cities preparing Comprehensive Annual Financial Reports) at least every two years and by the State Auditor’s Office every five years. Additionally, update the pension, long-term care, and medical cost valuation every four years.

• Explore ICMA-RC’s Retirement Health Savings (RHS) Employer Investment Program for investing funds dedicated to LEOFF I long term care and other medical costs.

2007 – 2008 Budget Impact

Description2005

Actual2006

Forecast2007

Budget2008

Budget

Retiree Medical Premiums 368,219$ 396,911$ 413,043$ 446,761$ Retiree Direct Medial Reimbursements 10,604 15,500 16,761 18,088 Actuarial Study 15,000 Total General Fund Expenditures 378,823$ 412,411$ 429,804$ 479,849$

Budget Policies

_________________________________ D-12 City of Mercer Island 2007-2008 Budget

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-13

Long Term Compensation Strategy Background This management and budget policy recognizes the significance of the fact that approximately two-thirds of the City's operating expenditures are devoted to salary and benefits for employees. The City’s employees are the means by which basic municipal services and Council policy directives are implemented. The primary objectives of this compensation strategy are to build both flexibility and predictability into our human resources systems. Forces such as the regional economy and labor market are outside of local control. Nevertheless, it is in the City’s best interest to anticipate, when possible, factors that drive compensation decisions. This management and budget policy outlines the philosophy and assumptions underlying the City’s compensation strategy. To implement it, specific actions will be taken during the next two years. These are listed below in the section titled Budget Policy for 2007-2008. Compensation Strategy

• Earnings will be viewed and compared on a "total cost of compensation" basis. Total compensation includes base pay, performance/variable pay, and benefits.

• Approved full and part-time positions represent valuable labor potential. Therefore, we fill vacancies in each such position carefully.

• We expect to remain competitive at approximately the mid-point of the market. We look at comparable positions in both the public and private employment sectors for our labor market.

• Employees must share in the cost of their health care benefits. • Compensation decisions (including labor negotiations) will be made using the best data available.

The City’s philosophy strives to create a balance between fair and equitable pay for employees, enabling management to recognize and reward excellent performance while exercising fiscal prudence by keeping the City's salary budget within its fiscal ability to pay. As a general rule, the City’s policy is to make sure that every job is classified and every employee’s salary is at least at the range minimum of that classification. It is also the policy of the City to ensure that salaries do not exceed the range maximum. An employee’s salary may be fixed at 5% less than the range minimum to allow for those who may require extensive on-the-job training to be hired at entry level. In extraordinary circumstances, such as to attract or retain valued employees, the City Manager has latitude to set salary outside the range. Competitive Compensation for the Non-Union Workforce Compensation awards and/or increases may occur for one or more of the following reasons:

1. Incentive to continue improved work quality, either for technical performance, customer service, or team performance.

2. The temporary addition of substantial responsibilities (such as temporary assignment or extra duty).

3. Special achievement.

Budget Policies

_________________________________ D-14 City of Mercer Island 2007-2008 Budget

Salary increases may occur as a condition of satisfactory completion of probation. The starting salary will be set at an amount that does not exceed the amount budgeted for the position in the annual budget. Salary adjustments resulting from performance and annual compensation guidelines must be approved by the Human Resources Manager, Finance Director and City Manager before becoming effective. Performance Awards/Merit Pay Funds are set aside for performance awards as part of the appropriation made by the City Council for all non-represented employees. The Human Resources Manager, Finance Director and City Manager will approve performance awards to reward behaviors and performance consistent with the mission of the department and the City vision. Performance awards will follow the guidelines set forth below:

1. The budgeted funding for awards does not exceed 2% of the amount of salaries for all non-represented employees.

2. Performance awards are available beginning January 1st of each New Year for which the City Council has appropriated funds for that purpose.

Budget Policies for 2007 - 2008 • Negotiate market-based collective bargaining agreements. Police and Records unions will negotiate

new or successor agreements during the 2007 – 2008 Biennium. • Review each position vacancy for the potential of attrition or work redesign. • Analyze personnel forecasting, benchmarking and reporting (e.g. indirect pay costs, employee

demographics, tenure, turnover rate, salary spreads, total compensation reports for all employees, health benefit cost trends).

• Maintain the City’s commitment to high standards of employee performance evaluation by continuing to track and report employee performance measures.

• On a regular basis, benchmark Mercer Island’s compensation against that paid by comparable cities. Develop proposal for any necessary market adjustment.

• Continue pay for performance system under which successive years of outstanding and exceptional performance are recognized. Consistently outstanding performance may be recognized by the City Manager at up to the 75th percentile of pay for comparable positions. Unless it cannot be matched, position comparisons are made to cities east of Lake Washington in King County that have similar size and services as Mercer Island. Continue funding at up to 2% of total salaries for non-represented employees.

2007 - 2008 Budget Impact Collective bargaining and compensation awards ratified by the City Council will determine the budget impact.

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-15

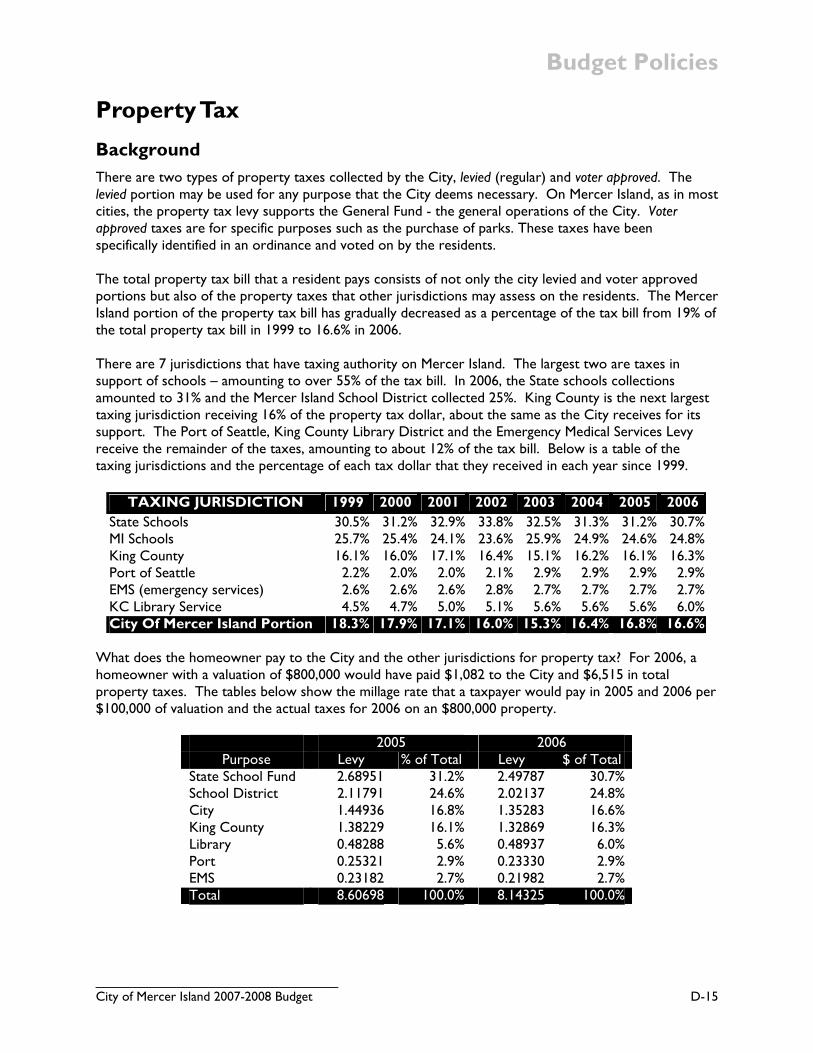

Property Tax Background There are two types of property taxes collected by the City, levied (regular) and voter approved. The levied portion may be used for any purpose that the City deems necessary. On Mercer Island, as in most cities, the property tax levy supports the General Fund - the general operations of the City. Voter approved taxes are for specific purposes such as the purchase of parks. These taxes have been specifically identified in an ordinance and voted on by the residents. The total property tax bill that a resident pays consists of not only the city levied and voter approved portions but also of the property taxes that other jurisdictions may assess on the residents. The Mercer Island portion of the property tax bill has gradually decreased as a percentage of the tax bill from 19% of the total property tax bill in 1999 to 16.6% in 2006. There are 7 jurisdictions that have taxing authority on Mercer Island. The largest two are taxes in support of schools – amounting to over 55% of the tax bill. In 2006, the State schools collections amounted to 31% and the Mercer Island School District collected 25%. King County is the next largest taxing jurisdiction receiving 16% of the property tax dollar, about the same as the City receives for its support. The Port of Seattle, King County Library District and the Emergency Medical Services Levy receive the remainder of the taxes, amounting to about 12% of the tax bill. Below is a table of the taxing jurisdictions and the percentage of each tax dollar that they received in each year since 1999.

TAXING JURISDICTION 1999 2000 2001 2002 2003 2004 2005 2006 State Schools 30.5% 31.2% 32.9% 33.8% 32.5% 31.3% 31.2% 30.7% MI Schools 25.7% 25.4% 24.1% 23.6% 25.9% 24.9% 24.6% 24.8% King County 16.1% 16.0% 17.1% 16.4% 15.1% 16.2% 16.1% 16.3% Port of Seattle 2.2% 2.0% 2.0% 2.1% 2.9% 2.9% 2.9% 2.9% EMS (emergency services) 2.6% 2.6% 2.6% 2.8% 2.7% 2.7% 2.7% 2.7% KC Library Service 4.5% 4.7% 5.0% 5.1% 5.6% 5.6% 5.6% 6.0% City Of Mercer Island Portion 18.3% 17.9% 17.1% 16.0% 15.3% 16.4% 16.8% 16.6%

What does the homeowner pay to the City and the other jurisdictions for property tax? For 2006, a homeowner with a valuation of $800,000 would have paid $1,082 to the City and $6,515 in total property taxes. The tables below show the millage rate that a taxpayer would pay in 2005 and 2006 per $100,000 of valuation and the actual taxes for 2006 on an $800,000 property.

2005 2006 Purpose Levy % of Total Levy $ of Total

State School Fund 2.68951 31.2% 2.49787 30.7% School District 2.11791 24.6% 2.02137 24.8% City 1.44936 16.8% 1.35283 16.6% King County 1.38229 16.1% 1.32869 16.3% Library 0.48288 5.6% 0.48937 6.0% Port 0.25321 2.9% 0.23330 2.9% EMS 0.23182 2.7% 0.21982 2.7% Total 8.60698 100.0% 8.14325 100.0%

Budget Policies

_________________________________ D-16 City of Mercer Island 2007-2008 Budget

For an $800,000 home, the 2006 property tax levy breaks down as follows:

Purpose % of Total

in 2006 Prop Tax

Levy State School Fund 30.7% $1,998 School District 24.8% $1,617 City 16.6% $1,082 King County 16.3% $1,063 Library 6.0% $391 Port 2.9% $187 EMS 2.7% $176 Total 100.0% $6,515

Regular Levy and Referendums Each November, as required by Washington State law, the City Council sets the property tax levy for the coming year. Up until November of 1997, this levy was restricted to a maximum of 106% of the previous year's levy plus the full levy authority for new construction. However, in 1997, the Washington State Legislature passed Referendum 47 on to the voters of the state who in turn approved it by a 60% majority. This referendum set a limit on property tax increases to be the lesser of 106% or the rate of inflation, whichever was less. In 2001, Initiative 747 passed in the State which further changed the property tax law. Initiative 747 limits the property tax levy to a maximum of 101% of the previous years levy, or the rate of inflation, whichever is less. (Since the rate of inflation is normally above 1% the effective limit for property tax will normally be 1%). The initiative also allows higher property tax increases if approved by the voters, a provision that was already in the statutes. The initiative sponsors intended for voters to have a say in the size of tax increases. Inflation, for the purposes of the referendum, is defined as the increase in the Implicit Price Deflator (IPD) for the previous 12 months as published in September of each year by the Bureau of Economic Analysis. This is not the same thing as the Consumer Price Index (CPI), which most cities, including Mercer Island, have used for many years as the measure of inflation to increase employee wages. The wage contracts specify the CPI to be used as the wage adjuster. The IPD has been both higher and lower than the CPI – the two indexes track different items. During 2006, I-747 was declared unconstitutional by a King County Superior Court judge. Attorney General Rob McKenna will appeal the ruling to the Washington State Supreme Court. He also will be seeking a “stay” until the Supreme Court has ruled. If the “stay” is granted or if there is a Supreme Court ruling by Nov 30, 2006 - reversing the lower court’s decision - then the maximum allowable increase will be 1%. If the “stay” isn’t granted or if there is no decision by Nov 30, 2006, then jurisdictions with a population of 10,000 or more will be allowed to increase their levy by the lesser of 6% or the IPD. Levy Policy For many years, the Council policy was to raise the levy by the full amount allowed by law. However, beginning in the 1995-96 Budget, the City Council chose to provide property tax relief to Mercer Island residents by “ramping down” the annual increase allowed by law. The Council policy was to attempt to lower the increase by .5% per year, targeting the rate of inflation. The rate of inflation for the City was considered to be the CPI that the City uses in its union wage contracts, since the cost of salaries, at 70% of the budget, largely drives the rate of increase of the budget. This CPI is the one used by all our

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-17

neighboring cities. The Council reached the “inflation” goal during the 2001 budget. Since 2001, the Council has normally followed the State law and increased taxes by 1%. However, in 2002, 2005 and 2006 the Council decreased property taxes by paying for some voted debt out of reserves. The present Council policy concerning the property tax levy stresses flexibility in the property tax policy. The Council is committed to fiscal responsibility as well as keeping this community affordable for its citizens. Thus, each year, the Council reviews the regular property tax levy in light of:

• current economic conditions • the fiscal health of the City (particularly the City's six largest revenue sources and the outlook

for salary and health benefits) • the six year financial forecast

Property Tax Factors The General Fund has always relied heavily on the property tax, with property tax at about 45% of the total budget. Because Mercer Island is primarily a residential community with modest business growth to support the City revenue base, the property tax is the most stable, predictable, and largest of all City revenues. Mercer Island is unlike other eastside cities that are supported heavily by taxes from business activity and sales taxes. For cities such as Redmond, Kirkland, and Bellevue, property tax is less than 20% of the total revenue base. The limit in property tax collections for those cities due to the changes in the state law has been more easily covered by their other revenue sources. Effect of increases on taxpayers and city One of the questions that must be considered in any discussion of the property tax is the effect on both the taxpayer and the City with a 1% tax increase. Based on 2006 property assessments, a 1% property tax increase in 2007 amounts to about $86,000 in total new revenue or $10.82 for an $800,000 home. Strategic Property Tax policies To guide staff in setting the budget and future property tax levies new polices and guidelines need to be set in the following areas:

• The annual amount of “regular” property tax that will be set each year to support the general fund.

• The use of “banked capacity” by the City. • Factors and circumstances which would lead the City to consider going to the voters for a tax

increase to support operations. Regular property tax annual amount Under normal circumstances, the City would plan to take the full 1% property tax increase to preserve the financial well-being of the City and to protect the property tax base for the future. Of course, decisions each year will stand on their own and the Council will always consider the general health of the City’s finances. Banked capacity The banked capacity provision allowed under RCW 84.55.092, Protection of Future Levy Capacity, allows local taxing districts to calculate levies based on the maximum lawful levy since 1985. If a taxing district voluntarily levies less than its maximum levy amount in a prior year, it will have some banked capacity that it could use in the future. The King County Assessors Office keeps track of the banked capacity of each jurisdiction. Banked capacity is a tool that may be considered for use by the Council.

Budget Policies

_________________________________ D-18 City of Mercer Island 2007-2008 Budget

Voted tax increases for operations The Council will determine an appropriate level of service for the Island as part of the budget process. The choice remains to balance the budget by raising taxes or by cutting services. In addition, if the cost of the services cannot be supported by the forecasted revenues with a 1% tax increase, the Council may consider authorizing a ballot measure for a voter approved operation levy. If the cost of services can be financed without an increase in property taxes, the Council will consider forestalling the annual 1% increase allowed under state law. Budget Policies for 2007 - 2008 • Each year, the regular property tax levy rate will be reviewed by the City Council to determine the

appropriate level of funding given current economic conditions, the fiscal health of the City, and the six-year financial forecast. Given an estimated increase of $150,000 in new construction based property taxes (1.75%) in both 2007 and 2008, council-approved property taxes for 2007 and 2008 are proposed as follows: • For 2007, the property tax should be increased by 1%. • For 2008, the property tax should be reviewed in light of prevailing financial conditions. For

budgeting purposes, the proposed biennial budget assumes a 1% increase for 2008. • The property tax excess levy rate for general obligation bonds will be set at the amount required to

pay debt service charges on the bonds as they become due. 2007 - 2008 Budget Impact

Revenues ($1,000’s) 2005

Actual 2006

Forecast 2007

Budget 2008

Budget

Regular Levy $ 7,776 $ 8,104 $ 8,739 $ 8,977

Luther Burbank M & O Levy 0 435 455 472

GO Bond Levy 147 63 0 0

Levy Lid Raise for City Hall 455 460 460 460

Total Tax Revenues $8,378 $9,062 $9,654 $9,909

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-19

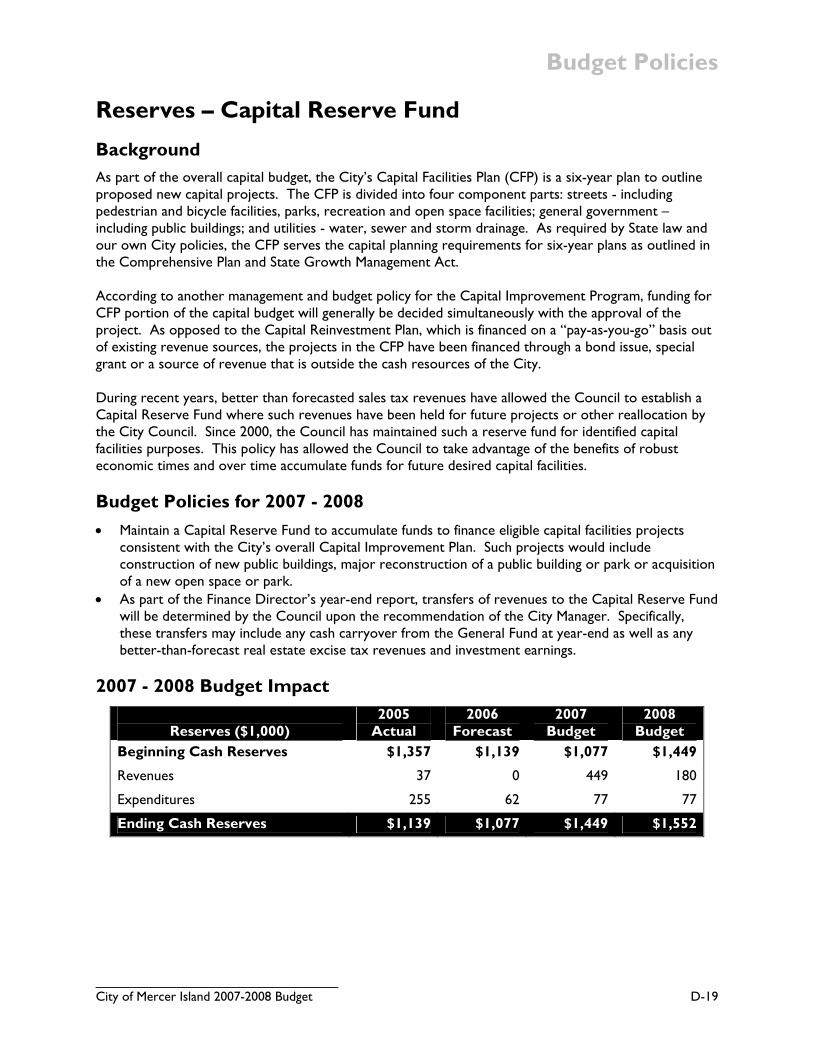

Reserves – Capital Reserve Fund Background As part of the overall capital budget, the City’s Capital Facilities Plan (CFP) is a six-year plan to outline proposed new capital projects. The CFP is divided into four component parts: streets - including pedestrian and bicycle facilities, parks, recreation and open space facilities; general government – including public buildings; and utilities - water, sewer and storm drainage. As required by State law and our own City policies, the CFP serves the capital planning requirements for six-year plans as outlined in the Comprehensive Plan and State Growth Management Act. According to another management and budget policy for the Capital Improvement Program, funding for CFP portion of the capital budget will generally be decided simultaneously with the approval of the project. As opposed to the Capital Reinvestment Plan, which is financed on a “pay-as-you-go” basis out of existing revenue sources, the projects in the CFP have been financed through a bond issue, special grant or a source of revenue that is outside the cash resources of the City. During recent years, better than forecasted sales tax revenues have allowed the Council to establish a Capital Reserve Fund where such revenues have been held for future projects or other reallocation by the City Council. Since 2000, the Council has maintained such a reserve fund for identified capital facilities purposes. This policy has allowed the Council to take advantage of the benefits of robust economic times and over time accumulate funds for future desired capital facilities. Budget Policies for 2007 - 2008 • Maintain a Capital Reserve Fund to accumulate funds to finance eligible capital facilities projects

consistent with the City’s overall Capital Improvement Plan. Such projects would include construction of new public buildings, major reconstruction of a public building or park or acquisition of a new open space or park.

• As part of the Finance Director’s year-end report, transfers of revenues to the Capital Reserve Fund will be determined by the Council upon the recommendation of the City Manager. Specifically, these transfers may include any cash carryover from the General Fund at year-end as well as any better-than-forecast real estate excise tax revenues and investment earnings.

2007 - 2008 Budget Impact

Reserves ($1,000)

2005 Actual

2006 Forecast

2007 Budget

2008 Budget

Beginning Cash Reserves $1,357 $1,139 $1,077 $1,449

Revenues 37 0 449 180

Expenditures 255 62 77 77

Ending Cash Reserves $1,139 $1,077 $1,449 $1,552

Budget Policies

_________________________________ D-20 City of Mercer Island 2007-2008 Budget

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-21

Reserves – Contingency Fund Background The City has established a contingency reserve to provide for unanticipated expenditures of a non-recurring nature, to meet unanticipated significant revenue shortfalls, and/or to meet unexpected increases in service delivery costs. In the past, the Contingency Fund received revenues from two sources:

1. 35% of all B&O tax revenue. 2. An appropriation of funds by the City Council as necessary to increase the Contingency Fund

balance to the specified target level. Targeted Goal As a long term goal, the Contingency Fund is to be funded at a target level of 10% of General Fund expenditures. In addition, state law limits the amount of cash that can be kept in the Contingency Fund to 37½ cents per thousand dollars of assessed valuation. For 2006, the legal limit for the fund is $2,148,900. Based upon a 2005 Milliman and Robertson, Inc. actuarial study, the City faces a total liability of $1.1 million for LEOFF I long-term care expenses. In 2004, the Council agreed to transfer $253,178 to the Contingency Fund as a reserve for unfunded LEOFF 1 medical benefits. In 2005, the Council allocated an additional $296,822 from the Contingency Fund balance bringing the total reserve for LEOFF I long term care to $550,000. In 2006 and additional $150,000 will be transferred from the General Fund, increasing the LEOFF I reserve to $700,000. Beginning in 2007, the City will transfer the LEOFF I long term care reserve to the General Fund in order to prevent any conflict with state-mandated contingency fund limits. Budget Policies for 2007 – 2008 • Transfer LEOFF I long-term care reserve ($700,000) to the General Fund to avoid any potential

conflict with the state-mandated 37½ cent per $1,000 of assessed valuation legal limit for Contingency Fund cash.

• Beginning 1/1/07, cease allocating B&O tax revenue to the Contingency Fund. Instead, all B&O tax revenue will go to the Beautification Fund to cover beautification-related costs.

• Allocate interest revenue to the Contingency Fund in lieu of B&O tax based on the cash balance in the fund per the Investment Earnings Management and Budget Policy. At current investment rates, this source should generate approximately $100,000 annually.

• Maintain the Contingency Fund target level of 10% of General Fund expenditures. In order to meet the target in 2007-2008 biennium, a relatively small transfer in the range of $15,000-$20,000 from the 2006 and 2007 year-end General Fund surplus will be necessary.

Budget Policies

_________________________________ D-22 City of Mercer Island 2007-2008 Budget

2007 - 2008 Budget Impact Reserves ($1,000)

2005 Actual

2006 Forecast

2007 Budget

2008 Budget

Beginning Cash Reserves $2,368 $2,454 $2,014 $2,114

Revenues from B&O 173 110 0 0

Interest Earnings 0 0 100 106

Interfund from General Fund 0 150 0 0

Expenditures (87) (700) 0 0

Ending Cash Reserves $2,454 $2,014 $2,114 $2,220

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-23

Reserves – Equipment Replacement Background The individual units of the City's fleet of vehicles and equipment are assigned to the various departments, but are accounted for in the City's Equipment Rental Fund. Each department is assessed an amount to cover vehicle and equipment operations, maintenance and replacement costs. A Reserve Fund exists for the accumulation of funds for equipment replacement, including both vehicles and emergency radios. The current fleet of vehicles and equipment stands at 136 units and has an estimated asset value of approximately $4.9 million (based on purchase cost). For the 2007-2008 biennial budget City staff overhauled fleet replacement rate model, incorporating salvage or trade-in values in the vehicle replacement rate calculation and, where appropriate, updated each vehicle’s inflationary and useful life assumptions. In overhauling the fleet replacement model, a cumulative surplus of $270,150 was identified, which breaks down as follow:

General Government vehicles: $178,708 Utility vehicles: $91,442.

The Reserve Fund for equipment replacement currently is maintained to allow for future inflation costs at a rate of 1%. For specialized equipment, the rate may vary. Vehicle replacements in 2005 amounted to $407,000 and in 2006 the forecast is for replacements of $190,000. Replacements for 2007 and 2008 are budgeted at $1.2 million and $770,000 respectively. Budget Policies for 2007 - 2008 • Continue the departmental charges based on actual vehicle operations and maintenance expenses

and overhead, plus a charge for vehicle replacement. • Develop reserve and operating policies for the Equipment Rental Fund. • Review prior to each new biennium the replacement schedule on a cost and use basis. • Replace vehicles when the forecast cost of maintenance is greater for the old vehicle than the costs

of its replacement. • Major vehicles not included in the Equipment Rental Fund (e.g. fire trucks) will be replaced through

means other than the Reserve Fund. • Additions to the City's vehicle and equipment fleet will be paid for with funds other than the

Equipment Rental Reserve Fund.

Budget Policies

_________________________________ D-24 City of Mercer Island 2007-2008 Budget

2007 - 2008 Budget Impact 2005

Actual 2006

Forecast 2007

Budget 2008

Budget Beginning Cash Reserves (1,000’s) $2,423 $2,776 $2,716 $1,940

Revenues – vehicles replacement 791 790 852 861

All other revenues 438 36 29 29

Total Revenues $1,229 $826 $881 $890

Expenditures (1,000’s) Operations and Maintenance (469) (696) (436) (441) Vehicle Replacements (407) (190) (1,221) (770)

Ending Cash Reserves $2,776 $2,716 $1,940 $1,620

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-25

Risk Management Background Mercer Island is one of the charter members of the municipal self-insured liability pool - Washington Cities Insurance Authority (WCIA). Through WCIA and an interlocal agreement with approximately 80 other cities, the City of Mercer Island insures general liability, automobile liability, errors and omissions, police enforcement, employee administration, and advertising liability. Each member city is insured for $1 million per occurrence with no deductible and no limit in number of claims. Each city also is covered by an additional $4 million per year for large claims. Participation in WCIA's program has resulted in the City continuing to be covered on a per occurrence basis with tail coverage back through 1981. The pool presently is self-insured and uses an annual actuarial study to determine member "premiums" and reserve policies. WCIA's long-term goals are to provide prudent planning and effective management to allow member cities liability protection comparable to or better than that available in the private market. Loss control procedures are reviewed with the cities to assist members to more effectively prevent, control or subrogate liability risks. Other Insurance The City purchases property insurance through a pooled arrangement with the other member cities of WCIA. The City continues to retain the first $5,000 of property loss through its Self-Insurance Fund which maintains about $100,000 to cover nondeductible losses. Industrial insurance is provided by the state with premiums paid based on the number of hours worked. The City's workforce is divided into four classes with different rates for each class. Volunteers are also covered by industrial insurance. Budget Policies for 2007 - 2008 • Continue to participate in the Washington Cities Insurance Authority during the 2007–2008

biennium. • Continue to review opportunities for efficiencies and reductions in risk-based insurance costs. 2007 - 2008 Budget Impact

Expenditures ($1,000s)

2005 Actual

2006 Forecast

2007 Budget

2008 Budget

Liability Insurance-WCIA $340.5 $360 $ 360 $ 370

Carrier Property 70 80 80 82.5

Specialty Insurance 3 5 7.5 7.5

Total Expenditures $413.5 $445 $ 447.5 $ 460

Budget Policies

_________________________________ D-26 City of Mercer Island 2007-2008 Budget

Budget Policies

_________________________________ City of Mercer Island 2007-2008 Budget D-27

Sustainability Background Leading scientists have reached a consensus that our planet’s climate is changing. The rate at which global warming is occurring is still being debated, but there’s overwhelming evidence that human activity is at least partly responsible, and that we can at least slow the rate of change by changing our behavior. Years before climate change was being publicly debated, both the residents of Mercer Island and their City government were embracing wise use of resources. In the early 1990s, the Island was the first community in King County to begin diverting 60% or more of its residential waste stream through recycling. In addition, the Island’s households have demonstrated repeatedly their ability to dramatically curtail water consumption during drought times. The City continues to undertake efforts to curtail its consumption of scarce resources including electric energy, water, fossil fuels and land fill space. During the 2007-2008 biennium, the City will set new targets for conservation and efficiencies in order to set a demonstrable example to local residents and businesses to follow. Budget Policies for 2007-2008 • Conduct appropriate research in early 2007 that would lead to Council approval of new

performance standards for efficiencies and consumption in the following areas: • Fuel consumption • Vehicle emissions • Facilities energy use • Water conservation • Recycling and reuse • Expand bicycling and pedestrian infrastructure

• Undertake a public education effort to report on the success of the City’s efforts and encourage conservation by residents and businesses.

2007 – 2008 Budget Impact Budget impact will be assessed during the mid-biennial budget review in November 2007.

Budget Policies

_________________________________ D-28 City of Mercer Island 2007-2008 Budget

BUDGET POLICES Utility Funds

Budget Policies

_________________________________ D-30 City of Mercer Island 2007-2008 Budget