bti e-thursday-capital-markets-financial-services-industry-recent-tax-developments

TRANSCRIPT

Presented by:Presented by:

Presented by:

Bank Tax InstituteCapital Markets: Recent Tax Developments

Keith Anzel Managing Director and Chief Tax Officer Citigroup Global Markets, Inc.

Jack Burns Executive DirectorFinancial Services Tax Practice, Ernst & Young, LLP

Michael YaghmourPrincipalInternational Tax Services - Capital Markets, Ernst & Young, LLP

Slide 1 2

Presented by:

IntroductionTOPICS:► Section 871(m) New Regulations.► Broker Basis and Interest Reporting.► Section 305(c) Recent Developments.► Case Decisions on Debt/Equity, Economic Substance Doctrine (ESD)

► How broad (or narrow) is the 2nd Circuit decision regarding BNY and AIG?► BB+T Bank argues for U.S. Supreme Court Review► Several debt v. equity cases being heard

► Section 475 Identification Developments – CCA 201529006.► The Recent Basket Option and Basket Contract Guidance – IRS notices and the

SIFMA letter.► Global Tax Transparency, Common Reporting Standard (CRS) and other

developments. ► Total Loss-Absorbing Capacity and hybrid instruments (including the BEPS-hybrid

instrument initiative).► TAM 201517007, REMICs and Economic Substance.► BEPS addresses mandatory disclosure rules for reportable transactions.► Bad Debt Deduction Developments.

Slide 2 3

Presented by:

Section 871(m) Regulations ‐ Highlights

4

Finalizes with some important changes proposed regulations from December 2013.

Major changes: Delta threshold for withholding increased from 70% to

80%. Testing for delta only on a “one and done” basis. No withholding needed until payment or settlement. New rules that ease determination for withholding agents

in potentially connected transactions. New rules for complex derivatives.

Slide 3

Presented by:

Section 871(m) Regulations (cont.)

Effective date considerations: Instruments issued before January 1, 2016, are never subject to withholding (unless four factor statutory test applies).

Instruments issued during 2016 are not subject to withholding until January 1, 2018.

Instruments issued beginning January 1, 2017 are fully subject to the withholding rules.

Slide 4

Presented by:

Broker Basis and Interest Reporting In March 2015, new final, temporary and proposed regulations

were issued on information reporting by brokers for bond premium and acquisition premium and for transactions involving debt instruments and options under §§6045, 6045A and 6049.

Under the new rule for market discount bonds, the constant yield market discount election is presumed to be made in the most taxpayer‐favorable manner, reversing the previous presumption (ratable accrual) for market discount. But the old rule still applies to market discount bonds acquired in 2014.

The removal of the all‐OID election from basis reporting computations will reduce future complexity, but many brokers already designed and built systems to take into account the election.

The new regulations do not provide any relief or guidance regarding complex debt instruments.

Slide 5

Presented by:

Section 305(c) – The Problem

Section 305(c) and regulations say that an adjustment to the conversion ratio of a convertible bond to take into account taxable dividends on the underlying stock is a taxable dividend to the bondholder at the time of the adjustment (regardless of whether the conversion feature is in the money or likely to be exercised).

Amount of the dividend is not clear: A 2006 PLR held that it was the then value of the

additional shares of the underlying (i.e., assuming conversion).

Possibly the amount should be adjusted for the “delta” of the convertible (roughly speaking, the probability of conversion) with respect to convertible debt.

Other potential dividend income measurement issues

Slide 6

Presented by:

Section 305(c) ‐ Timeframe

Older converts generally were issued by non‐dividend paying issuers or did not adjust for regular dividends.

More common in the past 10 years or so for converts to have full adjustment features and to have been issued by dividend payers.

8

Slide 7

Presented by:

Section 305(c) – Solutions/Options

Change in accounting method? Theory is that failure to include dividend income is a

timing issue because eventually the stock will be sold. Not automatic: Requires IRS National Office approval. Offers back year audit protection. Takes effect as of first day of taxable year in which

election is made. Still under consideration by IRS and Treasury.

Slide 8

Presented by:

Application of the Economic Substance Doctrine: Recent Developments in FTC Generator Cases

Why these cases are relevant beyond FTC generators: Potential for expanded application, beyond the potential denial of FTC’s in these structured finance transactions.

Bank of NY Mellon Corp. v. Comm’r, 140 T.C. 15 (Feb. 11, 2013), as modified byT.C. Memo. 2013-225 (Sep. 23, 2013): Summary of Lower Court Decision;

Facts► BNY transferred income-producing US assets to Trust Arrangement, referred to as

“STARS.”► Trust became subject to UK taxes on its income, which were claimed as foreign tax

credits (“FTCs”) for US federal income tax purposes.► BNY obtained $1.5 billion of below market cost financing from a UK bank. The

financing was approximately 300 bps below market because the UK bank also obtained UK tax benefits from the UK Trust Arrangement and provided rebate payments to BNY equal to a portion of the UK Bank’s UK tax benefits.

Tax Court Holdings► The Trust lacked economic substance► The result of the Tax Court’s determination that the transaction lacked economic

substance was as follows:► FTCs disallowed ► Deduction for foreign taxes not allowed► Interest expense deductions allowed► Income from rebate payments exempted from tax► No penalties (not assessed)

.

Initiation:

US Bank

Non-US Bank(UK)

Non-US SPE

(UK Trust)

US Assets

Equity (for UK tax purposes)

$“Repo Loan”

(for US tax purposes)

Ongoing:

US Bank

Non-US Bank(UK)

Non-US SPE

(UK Trust)

$ Rebate

UK Tax on

Income

Income from

Assets

$

Slide 9 10

Presented by:

Application of the Economic Substance Doctrine: Recent Developments in FTC Generator Cases (cont.)

Bank of NY Mellon Corp. v. Comm’r.Second Circuit Court of Appeals, September 9, 2015: 116 AFTR 2d 2015-6014 (CA-2, 2015)

The 2nd Circuit Court of Appeals confirmed the “economic substance doctrine” (ESD) judgment of the U.S. Tax Court to deny BNY Mellon Corp.’s foreign tax credits.

However, the court concluded that the underlying $1.5b loan had its own separate, legitimate substance that qualifies it for interest deduction.

In the same opinion, the court addressed an interlocutory appeal by AIG and ruled adverse to AIG, in a manner consistent with the BNY decision.

Initiation:

US Bank

Non-US Bank(UK)

Non-US SPE

(UK Trust)

US Assets

Equity (for UK tax purposes)

$“Repo Loan”

(for US tax purposes)

Ongoing:

US Bank

Non-US Bank(UK)

Non-US SPE

(UK Trust)

$ Rebate

UK Tax on

Income

Income from

Assets

$

Slide 10 11

Presented by:

Application of the Economic Substance Doctrine: Recent Developments in FTC Generator Cases

- Are the BNY and AIG decisions by the Second Circuit Court of Appeals potentially important to other types of transactions?

- Foreign Tax Expense (in the “Expected Profit” test):

a) Compaq and IES (5th and 8th

Circuits).b) The impact of the Second

Circuit decision – limited or broad?

c) Someday, there will be regulations (maybe!)

Initiation:

US Bank

Non-US Bank(UK)

Non-US SPE

(UK Trust)

US Assets

Equity (for UK tax purposes)

$“Repo Loan”

(for US tax purposes)

Ongoing:

US Bank

Non-US Bank(UK)

Non-US SPE

(UK Trust)

$ Rebate

UK Tax on

Income

Income from

Assets

$

Slide 11 12

Other cases: Santander (Sovereign Bank), Wells Fargo, BB+T Bank(request for U.S. Supreme Court Review)

Presented by:

Miscellaneous Cases

• Hewlett Packard: Also an FTC Generator case. The Tax Court held for Government on debt/equity grounds, rather than ESD grounds. TC memo 2012‐35. Briefs to Ninth Circuit Court of Appeals filed by Taxpayer and IRS in 2015.

• TYCO: Post‐Inversion Debt of U.S. Group Companies being challenged by IRS on debt v. equity grounds. Tax Court Trial to Commence in 2016.

• Slone v. Commr.: (116 AFTR 2d 2015‐2112)‐ Company with appreciated assets was sold to liquidator. IRS asserts transferee liability. Tax court held for Taxpayer. Ninth Circuit Reverses and Remands after applying ESD.

• U.S. v. Deutsche Bank AG (SDNY) – Company with Appreciated Assets sold to liquidator. IRS asserts transferee liability.

• Starr International Company, Inc. (U.S. District Court): Non‐U.S. investor holding U.S. dividend‐paying stock and is subject, for many years, to 30% U.S. withholding tax. Investor moves from Bermuda‐to‐Ireland‐to‐Switzerland and claims 15% withholding tax treaty rate under the U.S.‐Switzerland treaty. IRS denies discretionary grant of treaty benefits. Taxpayer asserts it was not treaty shopping.

Slide 12 13

Presented by:

Section 475Identification Developments & CCA 201529006

Taxpayer originated and sold mortgage loans. Under the sale contracts, purchaser had the right to require Taxpayer to repurchase the loans upon a breach of warranties and representations (W&R Obligations).

Taxpayer treated the W&R Obligations as securities and marked them to market under section 475.

Taxpayer argued that its W&R Obligations were a separate security in the nature of a “put option” on the underlying loans.

14Slide 13

Presented by:

Section 475Identification Developments & CCA 201529006 (cont.)

The IRS determined that the Taxpayer’s W&R Obligations were not securities within the meaning of section 475 because “the W&R Obligation were material and integral to the sales contracts, not independent financial instruments, investments, positions or bets on the value of those mortgages.”

“Securities” include a note, bond, debenture or other evidence of indebtedness or certain class of financial instruments, which is not the case of W&R Obligations.

The “value” of Taxpayer’s W&R Obligations was not determined by market forces but for breach of contract by Taxpayer.

Neither party of the mortgage sale transaction regarded the Taxpayer’s W&R Obligation as an actual and independent financial instrument—for example, the contract does not address it as a separate security and parties did not assigned a price for it.

Courts have consistently judged that rights to liquidated or other damages in bilateral sales contracts do not cause those contracts to be treated as “options.”

15Slide 14

Presented by:

The Recent Basket OptionIRS Notices and the SIFMA letter

The Treasury and the IRS issued Notices 2015‐47 and 2015‐48 (2015) on “Basket Option Contracts” (option contract) and “Basket Contracts” (other derivatives). Basket Option Contracts (options referencing a basket of

actively traded property) are characterized as “listed transactions.”

Other Basket Contracts (derivatives referencing baskets of various types of property, including hedge fund interests and actively traded property) are characterized as “transactions of interest.”

The purposes of these Notices are to prevent taxpayers from deferring income recognition and converting short‐term capital gains to long‐term capital gains through the use of derivatives (options and other derivatives).

16Slide 15

Presented by:

The Recent Basket OptionIRS Notices and the SIFMA letter (cont.)

• SIFMA suggests that the Notices should be “narrowed”:

To prevent over‐disclosure. To avoid administrative and tax filing burdens. To prevent potential market dislocation, due to

“reportable transactions” being often seen as “tax shelters.”

To clarify the scope of “participating” entities.

17Slide 16

Presented by:

The Recent Basket OptionIRS notices and the SIFMA letter (cont.)

• Specific recommendations: To introduce a definition of “transaction of interest”

(TI). To provide specific requirements for TI and Listed

Transactions (LT). To exclude certain financial assets/transactions. To change the 11/5/2015 due date to one year from

the date of the final updated Notices.

18Slide 17

Presented by:

Global Tax Transparency - Introduction

The global tax and regulatory environment is rapidly evolving as numerous countries worldwide have focused on tax transparency as a means of ensuring tax compliance of their residents.

Many countries have recently introduced or are planning to introduce rules that will require financial institutions to collect and provide to tax authorities, in the country of residence of the beneficial owner, comprehensive information on accounts held by their clients.

Many banks want to inform their customers about upcoming developments and encourage them to contact their tax advisers or accountants to get a better understanding of how these changes will impact their personal circumstances.

19Slide 18

Presented by:

Global Tax Transparency – Introduction (cont.)

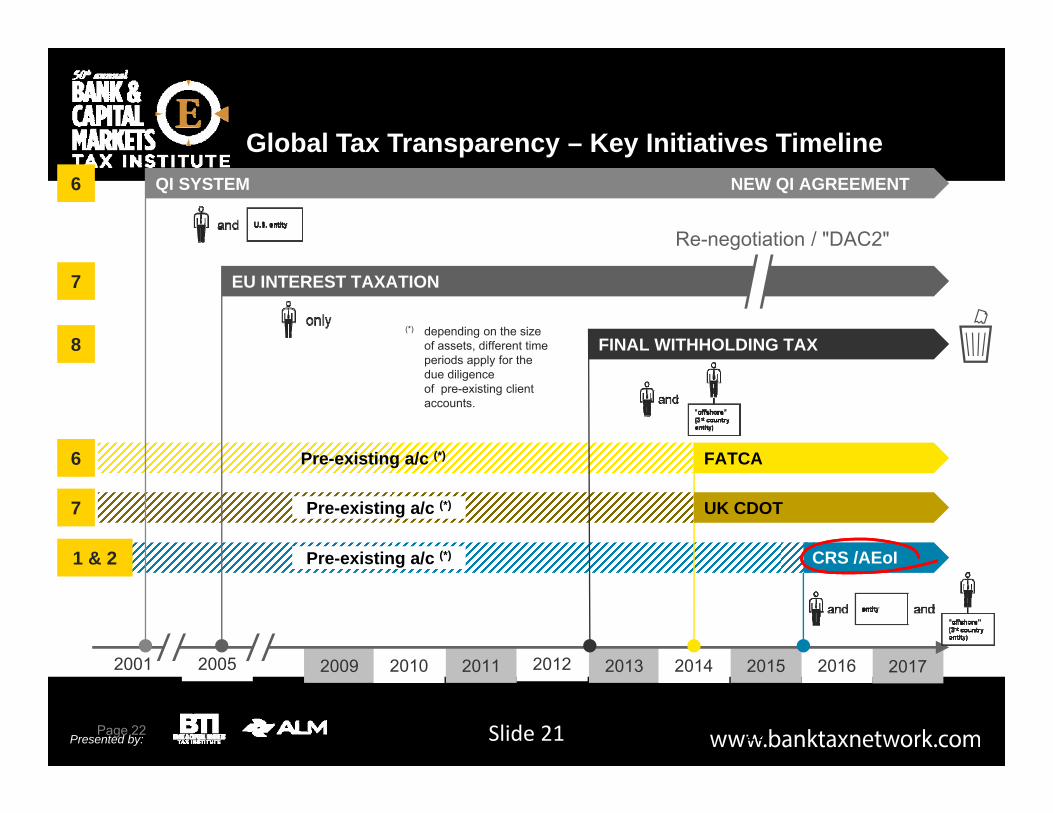

For financial institutions globally, the automatic exchange of information (AEOI) pertaining to their non‐US clients will commence under the OECD Common Reporting Standard (“CRS”), with early adopter countries requiring that 2016 account information be filed in 2017. This is in addition to the current reporting and withholding regimes, like US QI, US FATCA, EU Savings Directive, UK CDOT reporting, and others.

Concurrently, many countries offer voluntary disclosure programs to facilitate compliance by their residents in anticipation of the upcoming regimes.

20Slide 19

Presented by:

Global Tax Transparency – Key Initiatives

21Slide 20

Presented by: 22

Global Tax Transparency – Key Initiatives Timeline

Page 22

(*) depending on the size of assets, different time periods apply for the due diligenceof pre-existing client accounts.

20172016

Pre-existing a/c (*)

2011 2013 20152012 201420092001 2005 2010

QI SYSTEM NEW QI AGREEMENT

EU INTEREST TAXATION

FATCA

Re-negotiation / "DAC2"

CRS /AEoI

FINAL WITHHOLDING TAX

UK CDOTPre-existing a/c (*)

Pre-existing a/c (*)1 & 2

7

6

6

7

8

Slide 21

Presented by:

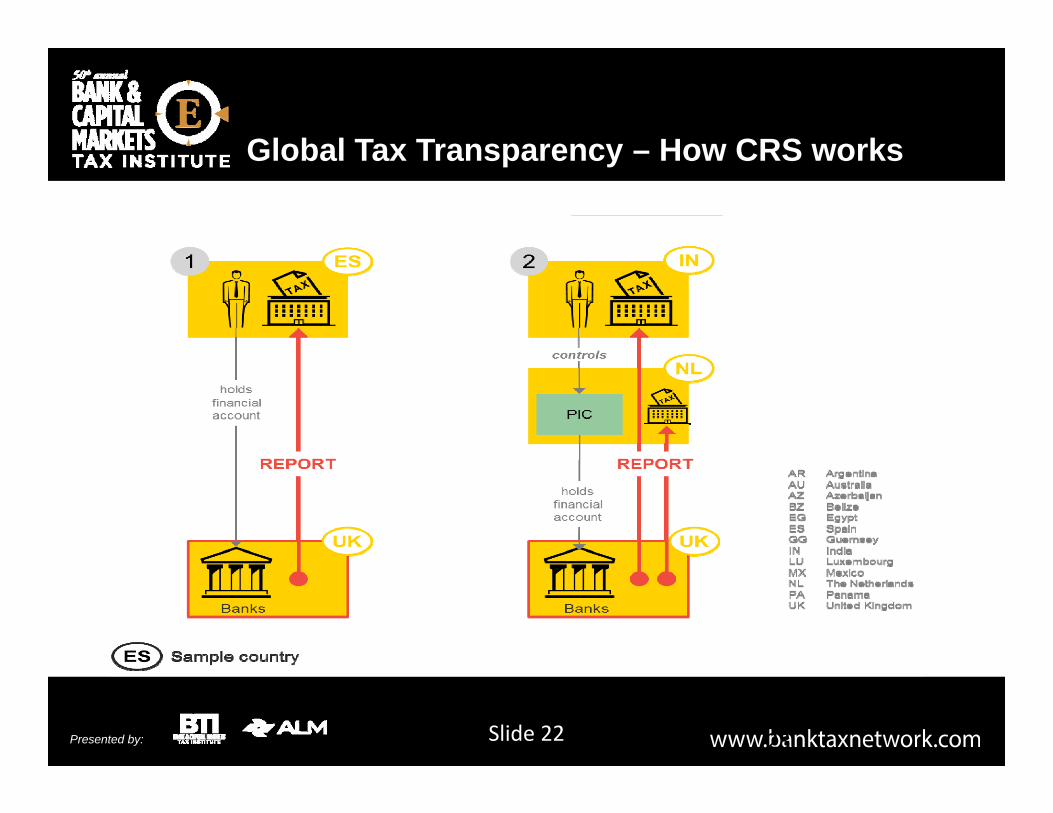

Global Tax Transparency – How CRS works

23Slide 22

Presented by:

TLAC and hybrid instruments (including the BEPS-hybrid instrument initiative)

24

US

Parent

Potential TLAC

instrument to 3rd parties

TLAC Instrument Debt – UK TaxEquity – US Tax

UK

Subsidiary

Slide 23

Consider: BEPS Hybrid Proposals

Presented by:

TAM (PLR) 201517007 REMICs and Economic Substance

Facts Insurance Sub owned a portfolio of residential mortgage‐backed

securities (RMBS) consisting of regular interests in real estate mortgage investment conduits (REMICs).

Sub formed Trust, which elected REMIC status. Sub contributed RMBS to Trust in exchange for Notes constituting the REMIC regular interests and a Certificate constituting the REMIC residual interest (which Certificate was entitled to true residual cashflows).

Sub sold the Notes to the public. Sub guaranteed the Notes as to principal and interest and also provided prepayment protection.

Sub claimed a capital loss in Year 3 upon the sale of the Notes based on the spread between their "issue price" and their allocated tax basis.

Sub amortized the built‐in loss on the Certificate as an ordinary loss over the REMIC's expected life per IRC §860F(b)(1)(D)(ii).

25Slide 24

Presented by:

TAM (PLR) 201517007REMICs and Economic Substance (cont.)

(cont.)RulingThe TAM concluded that where the requirements for REMIC status are met, then only REMIC rules apply. As such: A REMIC sponsor has a choice of either retaining its interests in the REMIC or

transferring them. If and when a sponsor sells any such REMIC interest to a third party, the sponsor

may then recognize gain or loss equal to the difference between its adjusted tax basis in the interest sold and the amount received.

If a REMIC sponsor retains one or more REMIC interests and, if the issue price of a retained interest is more or less than the sponsor's basis in that interest, then the sponsor has unrecognized gain or loss, which is taken into account over the life of the instrument.

26Slide 25

Presented by:

Bad Debt Expense and FAA 2015-53501F

FAA 20153501F‐ Taxpayer not entitled to partial bad debt deduction

because it did not satisfy the “charge‐off” requirement.

‐ Impairments claimed on a loan‐by‐loan basis, as contra‐assets in general ledger

‐ Taxpayer probably not a bank eligible for LB+I Bad Debt Directive benefits.

‐ The guidance states that the charge‐off requirements, per International Proprietaries, are not satisfied

‐ Measurement also questioned

27Slide 26

Presented by:

BEPS and Mandatory Disclosure

BEPS Addresses Mandatory Disclosure Rules for Reportable Transactions

(aimed at aggressive tax planning).A. The search for Greater Global Transparency includes tax

sensitive transactions.B. Industry Working Group provided comments to OECD

Committee in April, 2015, regarding Mandatory Transaction Disclosure Recommendations.

C. Final Reports: Issued by OECD: October, 2015

28Slide 27

Presented by:

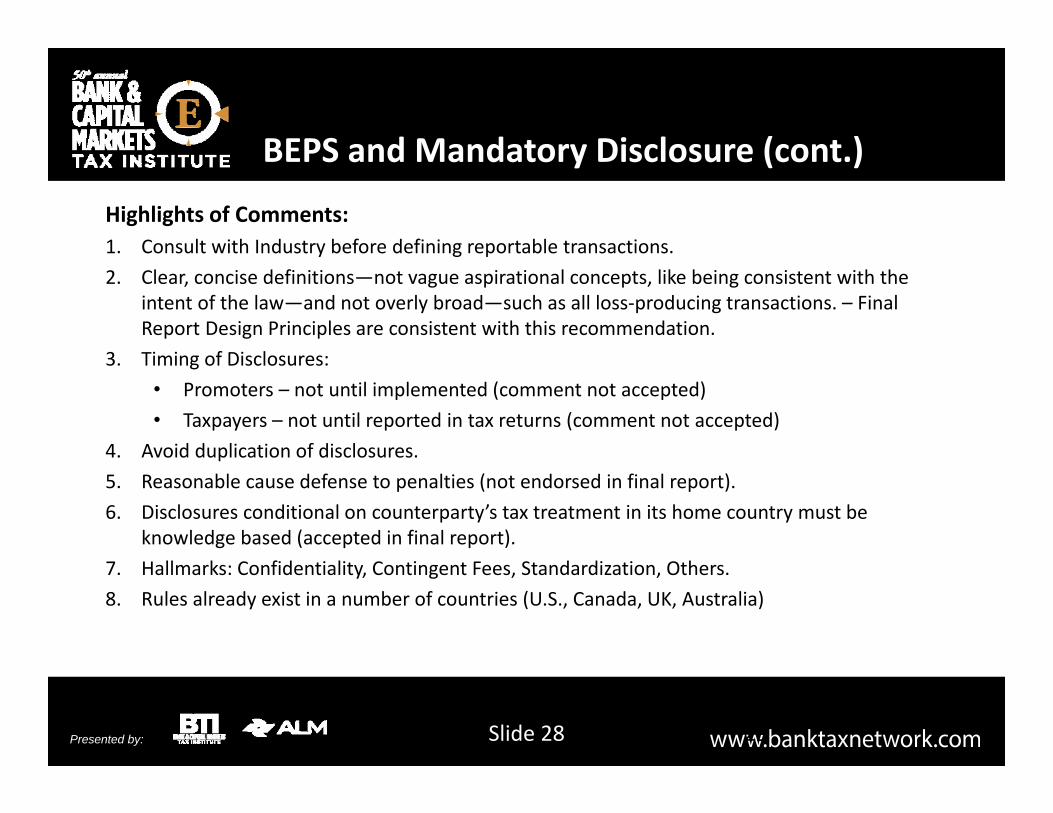

Highlights of Comments:1. Consult with Industry before defining reportable transactions.2. Clear, concise definitions—not vague aspirational concepts, like being consistent with the

intent of the law—and not overly broad—such as all loss‐producing transactions. – Final Report Design Principles are consistent with this recommendation.

3. Timing of Disclosures:• Promoters – not until implemented (comment not accepted)• Taxpayers – not until reported in tax returns (comment not accepted)

4. Avoid duplication of disclosures.5. Reasonable cause defense to penalties (not endorsed in final report).6. Disclosures conditional on counterparty’s tax treatment in its home country must be

knowledge based (accepted in final report).7. Hallmarks: Confidentiality, Contingent Fees, Standardization, Others.8. Rules already exist in a number of countries (U.S., Canada, UK, Australia)

29Slide 28

BEPS and Mandatory Disclosure (cont.)

Presented by:

Caveat and Limitations

Due to the preliminary nature of this document, it does not constitute tax advice or an opinion and hence cannot be relied upon for any purpose, including penalty protection. In order for EY to render tax advice or issue an opinion, additional steps may be required including, but not limited to, research, obtaining written representations from management, and/or verifying the facts upon which the opinion would be based.

Slide 29 30