bsbfia304_certiii_business_master presentation 2

TRANSCRIPT

BSBFIA304MAINTAIN A FINANCIAL LEDGERPRESENTATION 2

PRESENTATION OBJECTIVES

At the end of this presentation you will be able to:

• Prepare a trial balance

• Identify and rectify errors in the trial balance

PREPARE A TRIAL BALANCE

A trial balance is prepared after accounts have been updated to

ensure the accounts are in balance

The trial balance will list all accounts that have a balance, record the

account balance as either a debit or credit and totals of the debits

and credits

Organisations will have detailed processes to be followed when

creating the trial balance and are likely to have mandatory templates

or software to be used for accuracy, efficiency and consistency.

The accounts are in balance if total debits = total credits

PREPARE A TRIAL BALANCEWhat is a trial balance?

• A report listing ending debit and credit balances for all accounts from the

general ledger at the end of a reporting period

What is the purpose of a trial balance?

• Debits must equal credits - a corresponding credit entry is recorded for

each debit entry that is recorded - double entry concept of accounting

• The trial balance is useful in ensuring account balances are accurately

extracted from the accounting ledgers

• Uncovers errors within the journal and posting process

• The trial balance is the first step in the preparation of financial

statements. It will be useful in the preparation of the organisation’s

financial statements

• Accounting software automatically prepares this information for us

PREPARE A TRIAL BALANCE

The trial balance is usually prepared monthly after all the journals

have been posted to the general ledger.

To prepare the following should be completed:

• Every ledger account balance in the general ledger must be listed

in the trial balance

• Amounts are entered in the debit column when the ledger account

has a debit balance

• Amounts are entered in the credit column when the ledger

account has a credit balance

• A date/time stamp of when it was balanced

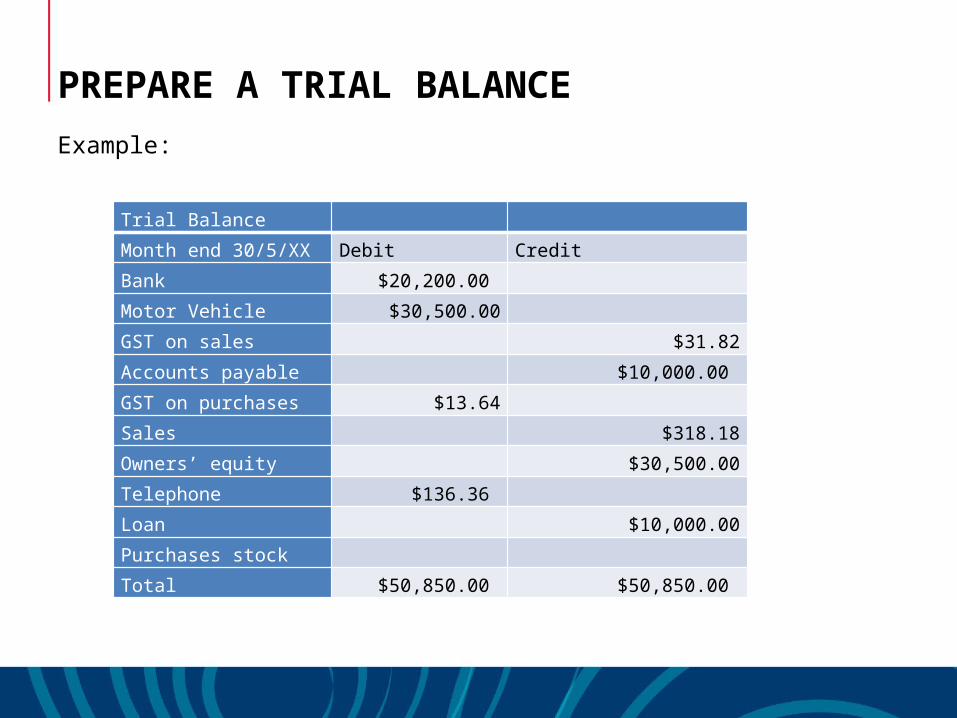

PREPARE A TRIAL BALANCE

Example:

Trial Balance

Month end 30/5/XX Debit Credit

Bank $20,200.00

Motor Vehicle $30,500.00

GST on sales $31.82

Accounts payable $10,000.00

GST on purchases $13.64

Sales $318.18

Owners’ equity $30,500.00

Telephone $136.36

Loan $10,000.00

Purchases stock

Total $50,850.00 $50,850.00

PREPARE A TRIAL BALANCE

Preparing a trial balance

• At the end of an accounting period, all ledger accounts are closed

• Ledger balances are posted into the trial balance

• Errors are identified as the trial balance is conducted

• Any adjustments needed at the period end that have not been

previously accounted for are incorporated into the trial balance

Developing a trial balance

• Prepare a worksheet with three columns. Complete these columns.

• Total debit and credit columns and compare the totals

• If it doesn’t balance begin to cross check your totals

Account titles Debits Credits

PREPARE A TRIAL BALANCE

Limitations of a trial balance

If the total of all debit balances matches the total of all credit

balances you could say it is balanced.

However, even if these match, there could be errors present:

• It is possible that an incorrect debit entry could be restored

with an incorrect credit entry equal to this amount

• Any transactions not recorded at all would not be identified by

a trial balance because both the debit and credit sides would

be left out

IDENTIFY AND RECTIFY ERRORS IN THE TRIAL BALANCE

The following are some other errors that may occur when preparing

the trial balance:

• Recorded an incorrect amount for a debit or credit

• Failing to post a journal entry in the ledger

• Forgetting an account in the trial balance

• Neglected to record a transaction altogether

• Incorrect allocation of debit and credit

It is not unusual that a trial balance will not balance on first attempt

IDENTIFY AND RECTIFY ERRORS IN TRIAL BALANCE

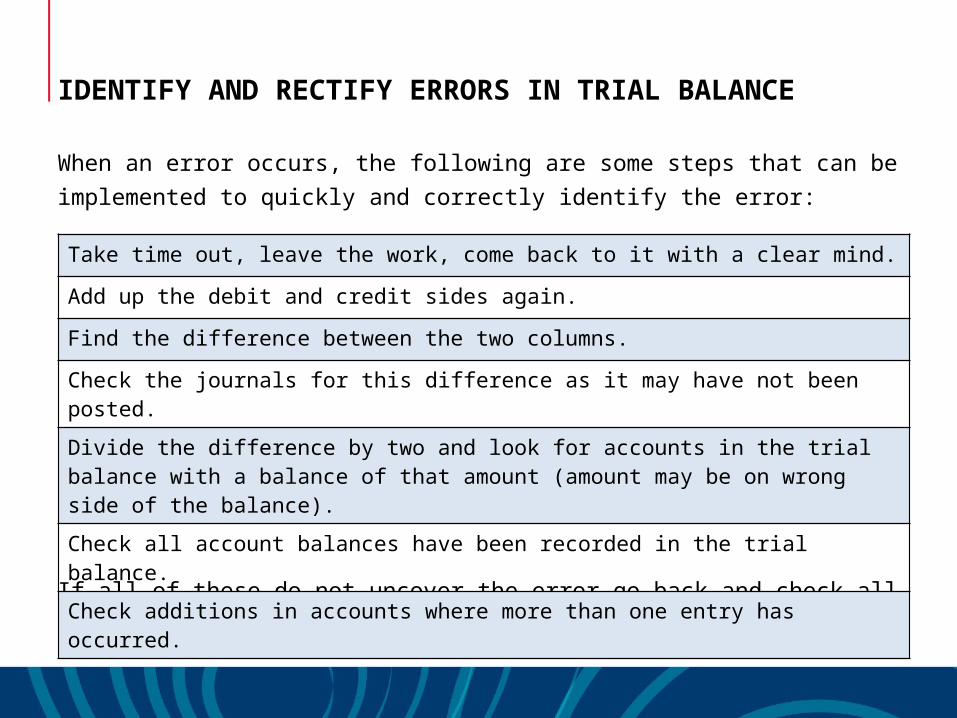

When an error occurs, the following are some steps that can be

implemented to quickly and correctly identify the error:

If all of these do not uncover the error go back and check all the

postings from the journals to the ledger.

Take time out, leave the work, come back to it with a clear mind.

Add up the debit and credit sides again.

Find the difference between the two columns.

Check the journals for this difference as it may have not been posted.

Divide the difference by two and look for accounts in the trial balance with a balance of that amount (amount may be on wrong side of the balance).

Check all account balances have been recorded in the trial balance.

Check additions in accounts where more than one entry has occurred.

IDENTIFY AND RECTIFY ERRORS IN TRIAL BALANCE

The amount and detail of information that has been entered into each

step leading up to the trial balance can result in possible errors.

Errors can be frustrating but the benefit of preparing a trial balance

on regular basis, eg: monthly, is clear

• Finding an error in a month’s worth of information and

transactions will take far less time than if the balance was

performed on a quarterly or annual basis.

Remember: always double check each transaction entry at each

step for accuracy and always ask for verification and clarification!

PRESENTATION OBJECTIVES

Now that you have completed this presentation, you will be able to:

• Prepare a trial balance

• Identify and rectify errors in the trial balance