broadband funding mechanisms - cátedra telefónica de...

TRANSCRIPT

Barcelona, July 2014

Broadband funding mechanisms Mauricio Agudelo, Technology, Media and Telecom Specialist

Imagen de ejemplo

Broadband financing mechanisms

Broadband funding case studies

Advantages and disadvantages of funding models

Practices contributing to mitigating project risk

Background

Conclusion

Imagen de ejemplo

BACKGROUND

Funding: one of the central issues facing broadband deployment

Its importance varies by broadband sector (fixed vs. mobile) and

sponsor (operator vs. local government)

Mechanisms can also vary by type of network (backbone vs. last mile

vs. submarine cable, depending on destination) and geography (urban

vs. rural)

Imagen de ejemplo

BROADBAND PROJECTS

ANALYZED

Geographic Mix

Local Backhaul/International

Urban/Suburban Rural

Financing

Strategies

Municipal

Stokab (Sweden)

Asturcom (Spain)

Kuuskaista (Finland)

Reso-LIAIN (France)

Oberhausen an der Donau

(Germany)

Government

Funding

Conectividad Rural de

Banda Ancha de R.

Dominicana

Autopista Mesoamericana de

la Informacion (C. America)

Argentina Conectada

French National Very High

Speed Plan (France)

BB Delivery UK (Great

Britain)

Public Private

Partnerships

Debitex (France)

KPN / Reggefiber

(Netherlands)

Todo Chile Conectado

(Chile)

Red Dorsal del Peru

Red Azteca de Colombia

Cable submarino a San

Andres (Colombia)

Operator-

funded

Empresa de

Telecomunicacione

s de Bogota

(Colombia)

Swisscom

(Switzerland)

Lattelecom (Latvia)

Andorra Telecom

Seabras 1 (Brazil-USA)

Internexa (Brazil)

Imagen de ejemplo

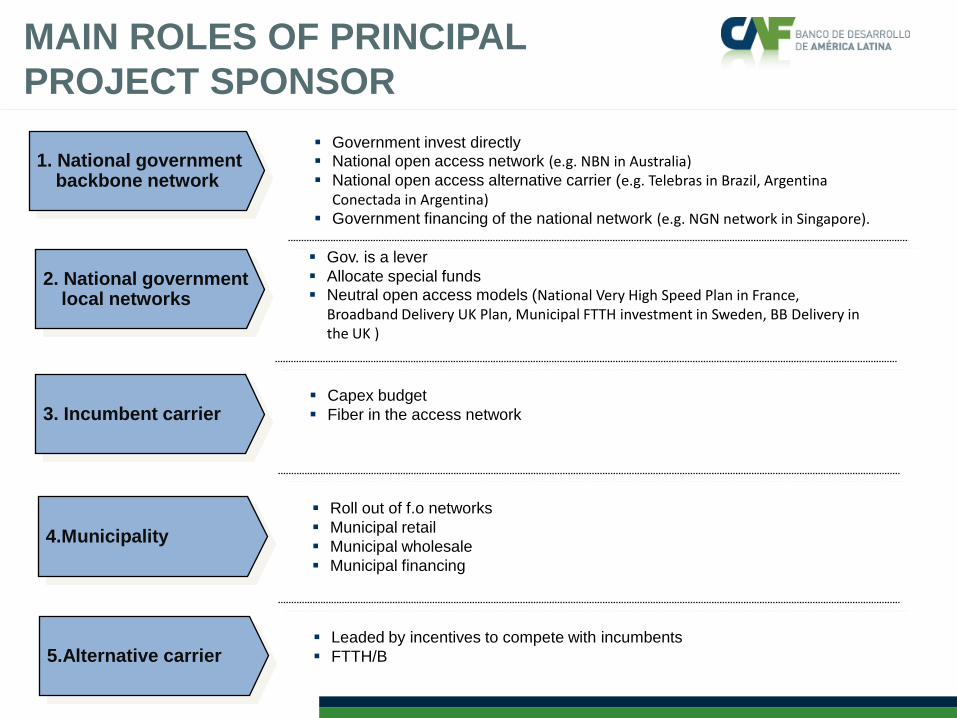

MAIN ROLES OF PRINCIPAL

PROJECT SPONSOR

1. National government backbone network

2. National government local networks

3. Incumbent carrier

Government invest directly National open access network (e.g. NBN in Australia) National open access alternative carrier (e.g. Telebras in Brazil, Argentina

Conectada in Argentina) Government financing of the national network (e.g. NGN network in Singapore).

Gov. is a lever

Allocate special funds Neutral open access models (National Very High Speed Plan in France,

Broadband Delivery UK Plan, Municipal FTTH investment in Sweden, BB Delivery in the UK )

Capex budget

Fiber in the access network

4.Municipality

Roll out of f.o networks

Municipal retail

Municipal wholesale

Municipal financing

5.Alternative carrier Leaded by incentives to compete with incumbents

FTTH/B

Imagen de ejemplo

Broadband financing mechanisms

Broadband funding case studies

Advantages and disadvantages of funding models

Practices contributing to mitigating project risk

Background

Conclusion

Imagen de ejemplo

Pension funds, insurance companies, etc

Tend to focus on stock exchange listed companies, rarely making exceptions

MAIN FINANCING STAKEHOLDERS

1. Institutional investors

2. Banking institutions:

3. Venture capitalists:

4. Angel investors

5. Governments

Driven by financial markets conditions

Extremely risk averse (typically to fund the replacement of existing networks,

rather than start-up broadband businesses)

Participation is done through funded risk-sharing facilities;

Constrained by a short-term investment horizon

Driven by a compelling investment thesis

Generally focused on growing vertically integrated closed broadband business

model

Two types of venture capitalists exist: seed/early stage funds and formal VC

funds

Fund a business at a start-up point with the purpose of capturing a high upside

by virtue of assuming a large equity position

Taken at the front-end of a process of a greenfield deployment (rarely asset

intensive)

Focused on providing seed financing and supporting investment readiness

analysis

Driven by policies pointing toward stimulating broadband roll-outs

Public finance sources tend to display national blanket coverage approaches

Typically focused on providing funding to open access business models

Imagen de ejemplo

TYPICAL FINANCING MODEL

STRUCTURE

PROJECT ENTITY

LENDER (S) • Commercial • Development Finance

Institutions

EQUITY INVESTORS • Financial sponsors

• Multilateral institutions (e.g.CAF)

• Construction and project managers

• Infrastructure suppliers and contractors

PUBLIC FUNDS Grants

Low interest loans

PROJECT CASH FLOWS

FUNDING STRUCTURE

LOAN TERMS Limited or non recourse

Rate and tenor

Seniority

Collateral

Covenants

DEBT REPAYMENT

RETURN ON EQUITY INVESTED

LOAN TERMS Aligned with direct faciility

Imagen de ejemplo

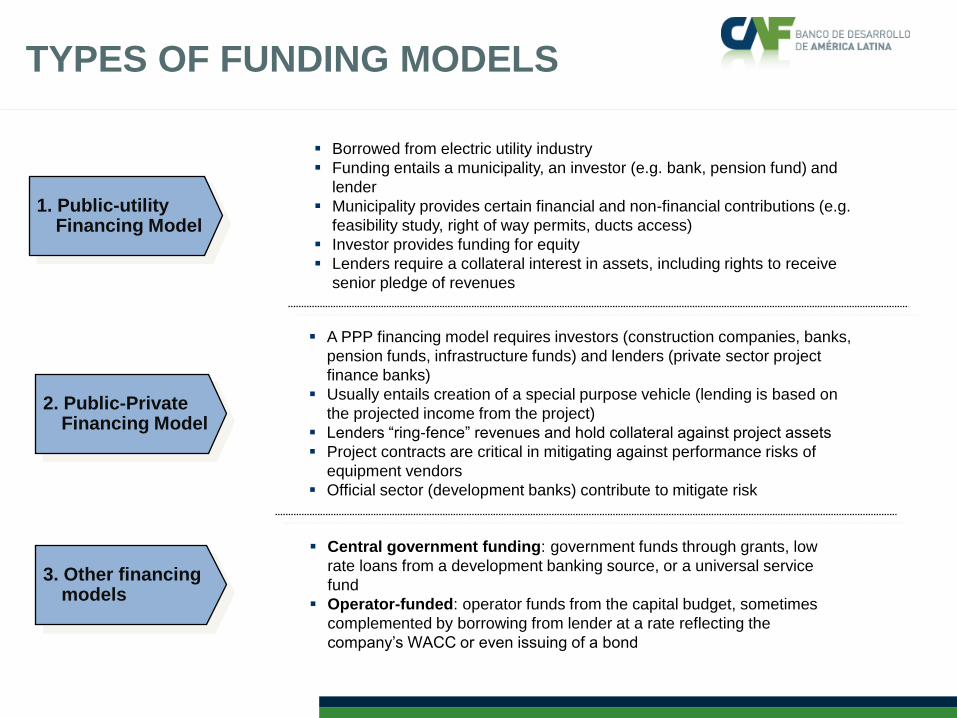

TYPES OF FUNDING MODELS

1. Public-utility Financing Model

2. Public-Private Financing Model

3. Other financing models

Borrowed from electric utility industry

Funding entails a municipality, an investor (e.g. bank, pension fund) and

lender

Municipality provides certain financial and non-financial contributions (e.g.

feasibility study, right of way permits, ducts access)

Investor provides funding for equity

Lenders require a collateral interest in assets, including rights to receive

senior pledge of revenues

A PPP financing model requires investors (construction companies, banks,

pension funds, infrastructure funds) and lenders (private sector project

finance banks)

Usually entails creation of a special purpose vehicle (lending is based on

the projected income from the project)

Lenders “ring-fence” revenues and hold collateral against project assets

Project contracts are critical in mitigating against performance risks of

equipment vendors

Official sector (development banks) contribute to mitigate risk

Central government funding: government funds through grants, low

rate loans from a development banking source, or a universal service

fund

Operator-funded: operator funds from the capital budget, sometimes

complemented by borrowing from lender at a rate reflecting the

company’s WACC or even issuing of a bond

Imagen de ejemplo

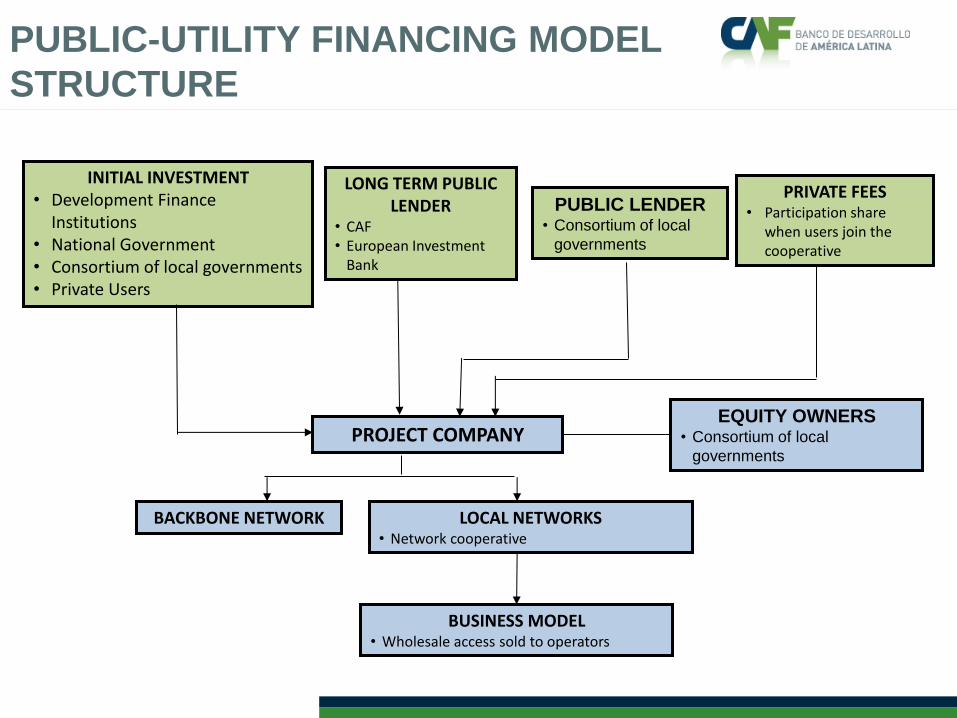

PUBLIC-UTILITY FINANCING MODEL

STRUCTURE

INITIAL INVESTMENT • Development Finance

Institutions • National Government • Consortium of local governments • Private Users

PUBLIC LENDER • Consortium of local

governments

PROJECT COMPANY

BUSINESS MODEL • Wholesale access sold to operators

BACKBONE NETWORK

LONG TERM PUBLIC LENDER

• CAF • European Investment

Bank

EQUITY OWNERS • Consortium of local

governments

LOCAL NETWORKS • Network cooperative

PRIVATE FEES • Participation share

when users join the cooperative

Imagen de ejemplo

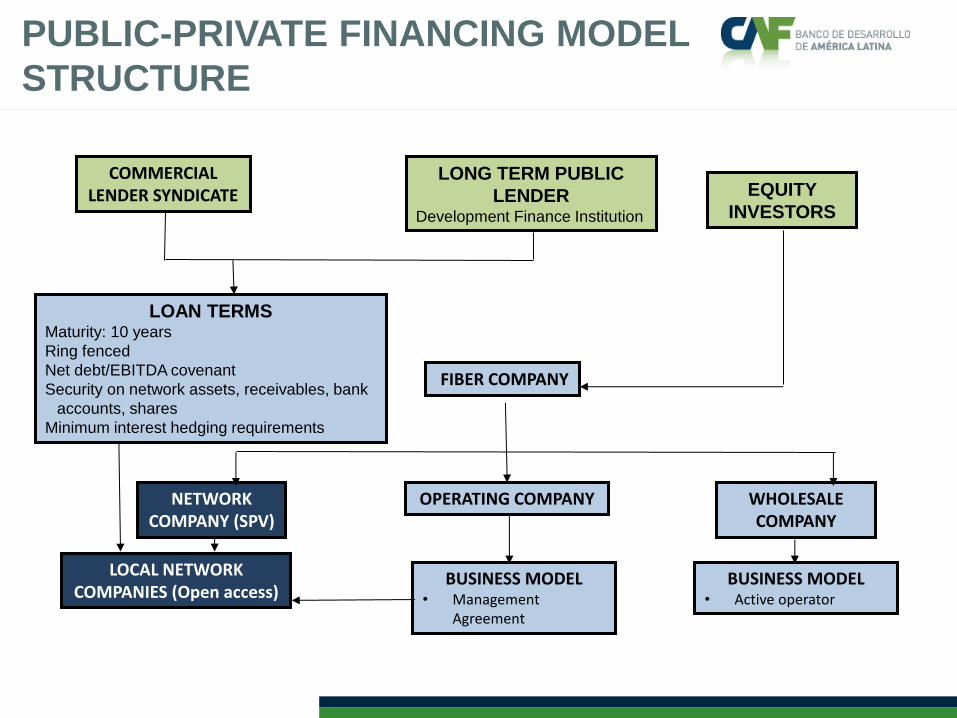

PUBLIC-PRIVATE FINANCING MODEL

STRUCTURE

COMMERCIAL LENDER SYNDICATE EQUITY

INVESTORS

LONG TERM PUBLIC

LENDER Development Finance Institution

FIBER COMPANY

LOAN TERMS Maturity: 10 years

Ring fenced

Net debt/EBITDA covenant

Security on network assets, receivables, bank

accounts, shares

Minimum interest hedging requirements

NETWORK COMPANY (SPV)

LOCAL NETWORK COMPANIES (Open access)

OPERATING COMPANY WHOLESALE COMPANY

BUSINESS MODEL • Active operator

BUSINESS MODEL • Management

Agreement

Imagen de ejemplo

Broadband financing mechanisms

Broadband funding case studies

Advantages and disadvantages of funding models

Practices contributing to mitigating project risk

Background

Conclusion

Imagen de ejemplo

THREE BROADBAND FINANCING

MODELS IN TWO CONTINENTS

Model Europe Cases Latin American cases

Public-owned

utilities

• Asturcom (Spain)

• Oberhausen an der Donau

(Germany)

• Kuuskaista (Finland)

• Debitex (France)

• Reso-LIAIN (France)

• Argentina Conectada

Operator-

sponsored

• KPN / Reggefiber (Netherland)

• Seabras 1 (US-Brazil)

• ETB (Colombia)

Public-private

funding

• Red Dorsal del Peru (Peru)

• Red Azteca (Colombia)

• Mesoamericana Information Highway

(Central America)

• Cable Submarino San Andres

(Colombia)

BACKBONE NETWORKS ROLL OUT IN LATAM

Inversiones estimadas en

USD 6.300 MM para

extender y modernizar redes

troncales

Existen dos grandes formas

para este despliegue:

licitación ó encargo a un

operador público

Imagen de ejemplo

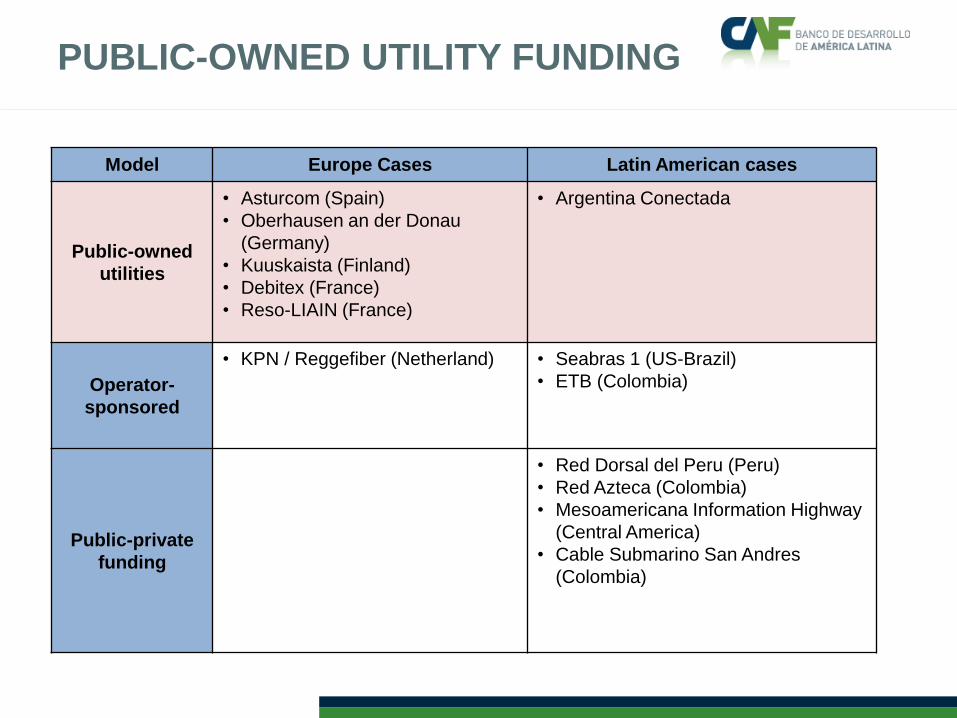

PUBLIC-OWNED UTILITY FUNDING

Model Europe Cases Latin American cases

Public-owned

utilities

• Asturcom (Spain)

• Oberhausen an der Donau

(Germany)

• Kuuskaista (Finland)

• Debitex (France)

• Reso-LIAIN (France)

• Argentina Conectada

Operator-

sponsored

• KPN / Reggefiber (Netherland)

• Seabras 1 (US-Brazil)

• ETB (Colombia)

Public-private

funding

• Red Dorsal del Peru (Peru)

• Red Azteca (Colombia)

• Mesoamericana Information Highway

(Central America)

• Cable Submarino San Andres

(Colombia)

Imagen de ejemplo

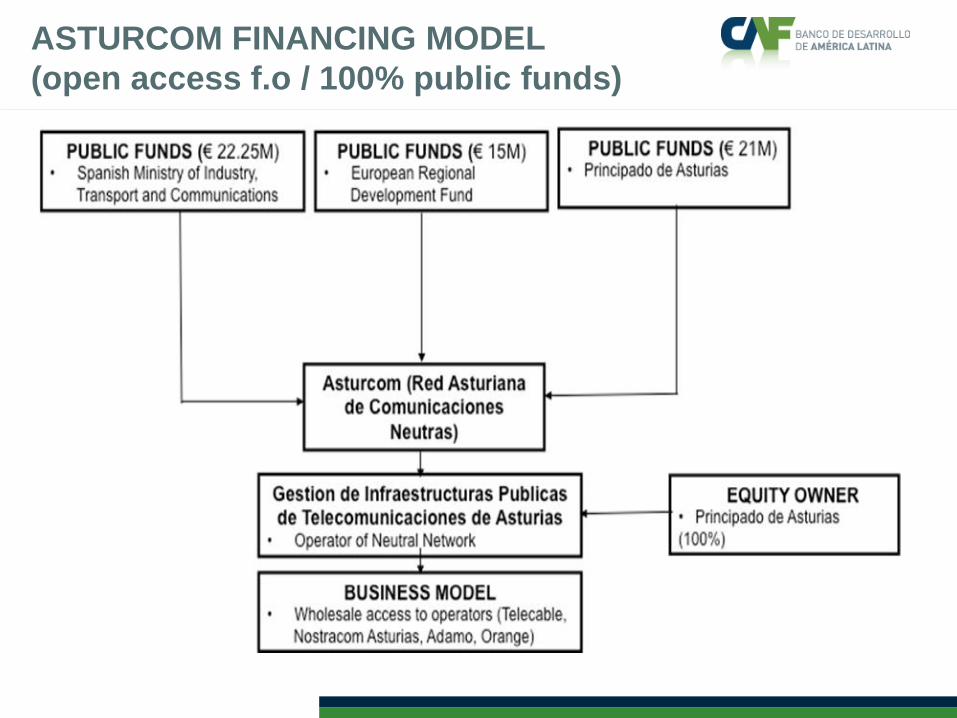

ASTURCOM FINANCING MODEL

(open access f.o / 100% public funds)

Imagen de ejemplo

OBERHAUSEN AN DER

DONAU FINANCING MODEL

Imagen de ejemplo

VERKKO-OSUUSKUNTA KUUSKAISTA

FINANCING MODEL (FTTH cooperative/7 towns)

Imagen de ejemplo

DEBITEX TELECOM FINANCING MODEL

(concession of public service)

Imagen de ejemplo

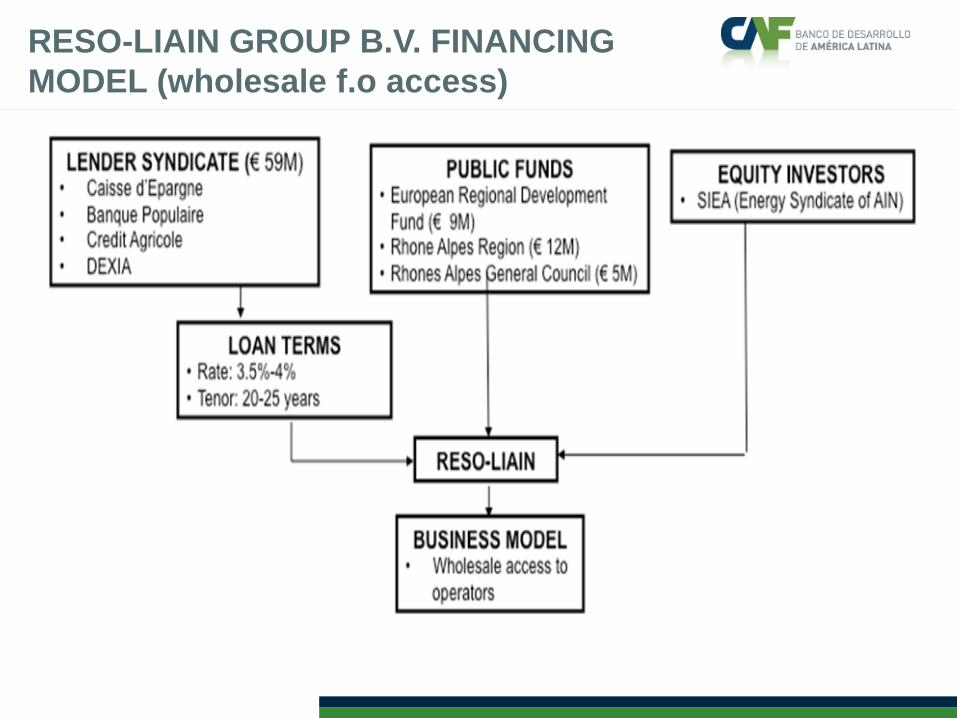

RESO-LIAIN GROUP B.V. FINANCING

MODEL (wholesale f.o access)

Imagen de ejemplo

ARGENTINA CONECTADA

Backbone network over most of the territory, wholly-owned by ARSAT, a

public company

National network entirely funded by the government

2012-13: $ 507 million

2014-15: $ 493 million

The networks within each province were funded through a “fideicomiso”

trustee with the Banco de Inversion y Comercio Exterior

Imagen de ejemplo

COMPARATIVE ANALYSIS OF

PUBLIC-OWNED BROADBAND PROJECTS

Funding

Type

Funding

Sources Asturcom

Oberhausen

an der Donau Kuuskaista

Debitex

Telecom

Reso-

LIAIN

Argentina

Conectada

Initial

Investment

Funding

Development

Funding

Institution

Yes No Yes No Yes Yes

Central

Government Yes No Yes No No Yes

Local

Government Yes No Yes Yes Yes Yes

Private Sector

(Carriers, other) No No Yes Yes No No

Long term

Lending

Development

Funding

Institution

No No Yes No No No

Local

Government No No Yes No No No

Commercial

Bank No Yes No Yes Yes No

Funding from coop. fees No No Yes No No No

Imagen de ejemplo

OPERATOR-SPONSORED MODELS

Model Europe Cases Latin American cases

Public-owned

utilities

• Asturcom (Spain)

• Oberhausen an der Donau

(Germany)

• Kuuskaista (Finland)

• Debitex (France)

• Reso-LIAIN (France)

• Argentina Conectada

Operator-

sponsored

• KPN / Reggefiber (Netherland)

• Seabras 1 (US-Brazil)

• ETB (Colombia)

Public-private

funding

• Red Dorsal del Peru (Peru)

• Red Azteca (Colombia)

• Mesoamericana Information Highway

(Central America)

• Cable Submarino San Andres

(Colombia)

Imagen de ejemplo

REGGEFIBER BUSINESS MODEL AS A

PASSIVE OPERATOR

Imagen de ejemplo

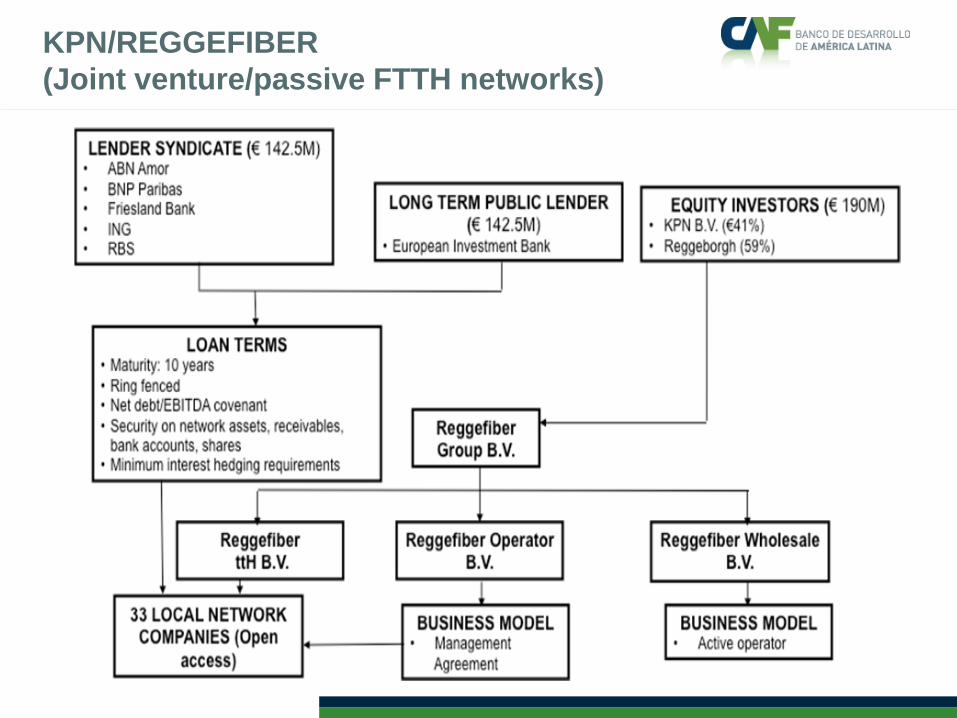

KPN/REGGEFIBER

(Joint venture/passive FTTH networks)

Imagen de ejemplo

MODELS SUCH AS KPN/REGGEFIBER ARE

ATTRACTIVE ON SEVERAL DIMENSIONS

Risk is reduced due to the joint ownership, ensuring stability, scale, and

lower costs

By lending on a non-recourse basis, equity investors benefit from a lower

investment risk

The draw test on the credit facility is driven by the number of acquired

customers, a market-driven threshold

Funds to be drawn are also subject to specific due diligence

Other incumbents have also entered into similar collaborative agreements

(e,g France Telecom to deploy FTTB/H networks in second tier cities and

rural areas of France, Deutsche Telekom has launched a pilot project with

EWE Tel - to roll out FTTH in regions of the federal state of Lower Saxony)

Imagen de ejemplo

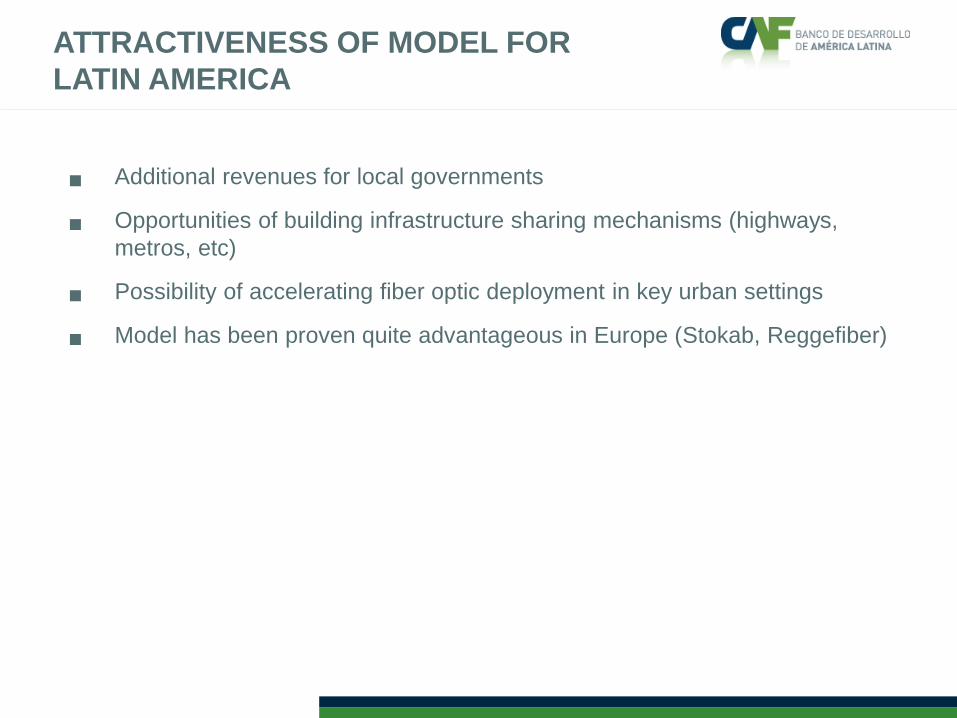

ATTRACTIVENESS OF MODEL FOR

LATIN AMERICA

Additional revenues for local governments

Opportunities of building infrastructure sharing mechanisms (highways,

metros, etc)

Possibility of accelerating fiber optic deployment in key urban settings

Model has been proven quite advantageous in Europe (Stokab, Reggefiber)

Imagen de ejemplo

SEABRAS 1

(Brazil – US submarine cable)

SEABORN

NETWORK, LLC

SEABRAS 1 PROJECT • Sao Paulo to New Jersey

• Total investment: US$ 425 mn

MULTILATERAL FACILITY • IFC US$ 25 mn

COFACE • French agency for export

promotion

• Provides a loan guarrantee

• Supports lending since Lucent-

Alcatel is equipment ptovider

Long-Term Loan Facility • Natixis US$ 290 million

guarranteed

FREE CASH FLOWS

Imagen de ejemplo

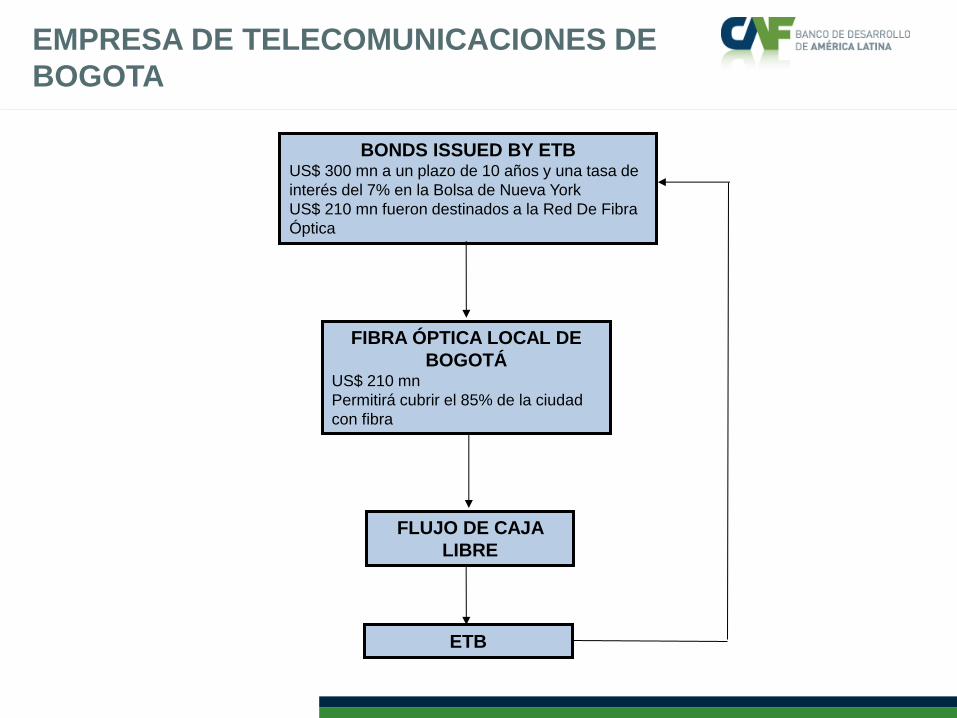

EMPRESA DE TELECOMUNICACIONES DE

BOGOTA

FIBRA ÓPTICA LOCAL DE

BOGOTÁ US$ 210 mn

Permitirá cubrir el 85% de la ciudad

con fibra

ETB

BONDS ISSUED BY ETB US$ 300 mn a un plazo de 10 años y una tasa de

interés del 7% en la Bolsa de Nueva York

US$ 210 mn fueron destinados a la Red De Fibra

Óptica

FLUJO DE CAJA

LIBRE

Imagen de ejemplo

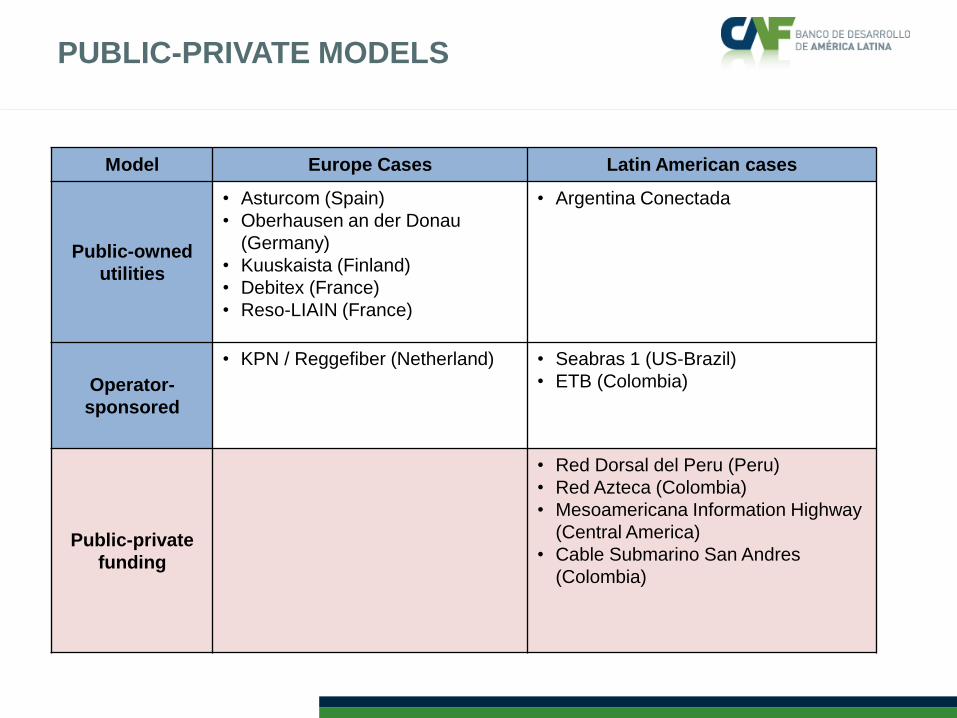

PUBLIC-PRIVATE MODELS

Model Europe Cases Latin American cases

Public-owned

utilities

• Asturcom (Spain)

• Oberhausen an der Donau

(Germany)

• Kuuskaista (Finland)

• Debitex (France)

• Reso-LIAIN (France)

• Argentina Conectada

Operator-

sponsored

• KPN / Reggefiber (Netherland)

• Seabras 1 (US-Brazil)

• ETB (Colombia)

Public-private

funding

• Red Dorsal del Peru (Peru)

• Red Azteca (Colombia)

• Mesoamericana Information Highway

(Central America)

• Cable Submarino San Andres

(Colombia)

Imagen de ejemplo

RED DORSAL DEL PERU

FITEL • Handles bid for construction of

Network

• Provides funding from Universal

Service Funds

• Regulates transport tariff at a monthly

maximum of US$ 27 for 1 Mbps link

RED DORSAL

DEL PERÚ

Project Cost:

US$ 323 million

TV AZTECA TOTAL PLAY • Contributes the remaining funds

required for network deployment

• Obtains a license for 20 years with an

option to extend

• Transport tariff is regulated

FREE CASHFLOWS

Imagen de ejemplo

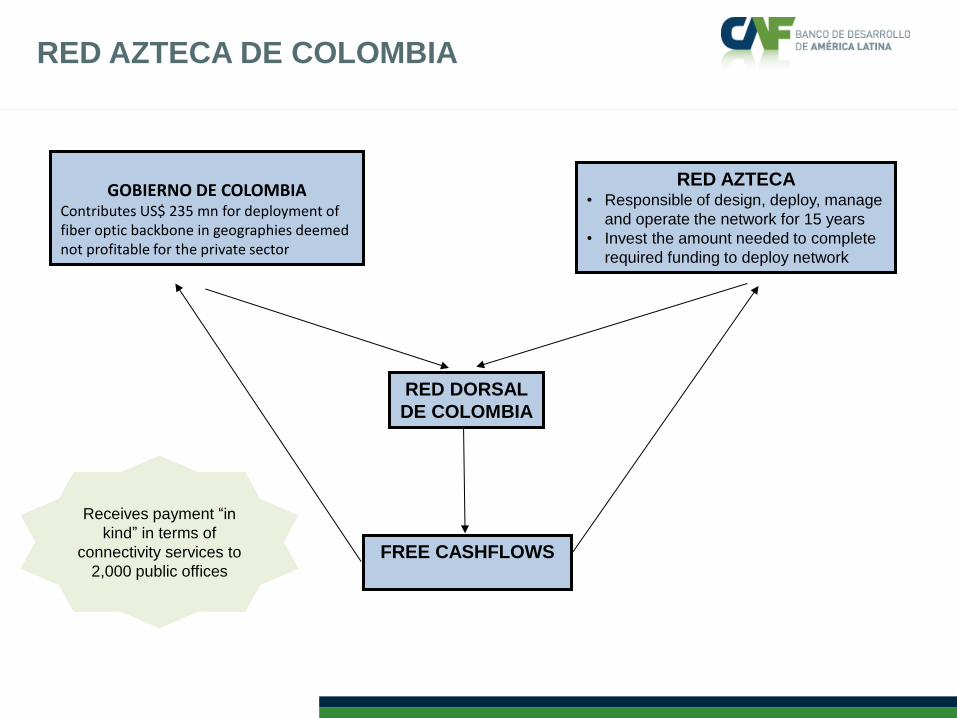

RED AZTECA DE COLOMBIA

GOBIERNO DE COLOMBIA

Contributes US$ 235 mn for deployment of fiber optic backbone in geographies deemed not profitable for the private sector

RED DORSAL

DE COLOMBIA

RED AZTECA • Responsible of design, deploy, manage

and operate the network for 15 years

• Invest the amount needed to complete

required funding to deploy network

FREE CASHFLOWS

Receives payment “in

kind” in terms of

connectivity services to

2,000 public offices

Imagen de ejemplo

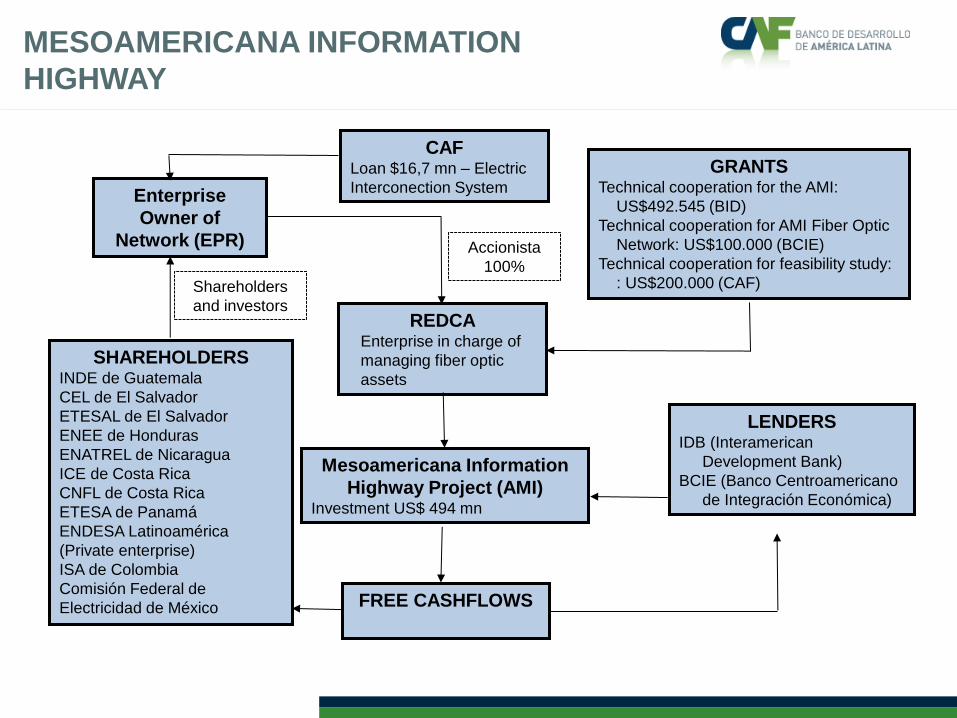

MESOAMERICANA INFORMATION

HIGHWAY

Enterprise

Owner of

Network (EPR)

GRANTS Technical cooperation for the AMI:

US$492.545 (BID)

Technical cooperation for AMI Fiber Optic

Network: US$100.000 (BCIE)

Technical cooperation for feasibility study:

: US$200.000 (CAF)

REDCA Enterprise in charge of

managing fiber optic

assets

SHAREHOLDERS INDE de Guatemala

CEL de El Salvador

ETESAL de El Salvador

ENEE de Honduras

ENATREL de Nicaragua

ICE de Costa Rica

CNFL de Costa Rica

ETESA de Panamá

ENDESA Latinoamérica

(Private enterprise)

ISA de Colombia

Comisión Federal de

Electricidad de México

Shareholders

and investors

Accionista

100%

CAF Loan $16,7 mn – Electric

Interconection System

Mesoamericana Information

Highway Project (AMI) Investment US$ 494 mn

LENDERS IDB (Interamerican

Development Bank)

BCIE (Banco Centroamericano

de Integración Económica)

FREE CASHFLOWS

Imagen de ejemplo

CABLE SUBMARINO SAN ANDRES

Submarine cable between Panama, Colombia and Latin American countries

Sponsor is a private company

Of the $63 million of total project cost, the IFC provided $10 million, and the

remainder was shared between the Colombian government and the private

project sponsor

Project included loans provided to the private sponsor from Colombian

banks

Imagen de ejemplo

Broadband financing mechanisms

Broadband funding case studies

Advantages and disadvantages of funding models

Practices contributing to mitigating project risk

Background

Conclusion

Imagen de ejemplo

PUBLIC-OWNED UTILITIES

Model Description Advantages Disadvantages Examples

discussed

1. Direct

Subsidy

Public funds pay

for broadband

project for an

open access

business model

Government retains

ownership of

infrastructure

Government can ensure

own needs are covered

Ongoing financing required

Continued reliance on state aid

Public sector assumes market risk

Competitive encroachment could

erode project viability

Asturcom

(Spain)

Argentina

Conectada(Arge

ntina)

2. Local

Investment

Government

invests as would a

private player in a

private venture

deploying the

infrastructure

No state aid

Local government bears

the failure risk alone

More lenient credit terms

(rates, maturity) based

on municipal profile

Need to rely on public funds to

invest

Risk of impacting local taxes

Potential competitive retaliation

Highly dependent on income of

population

3. Private

credit

financing

Same as above,

but funds

borrowed from

private sources

Service revenues

are earmarked to

service debt

No impact on taxes

Does not need to reach

critical mass in order to

qualify for Development

Finance support

Potentially, but not necessarily,

worse credit terms than from public

sources

Forces a period of full service ran

by local government

Risk of bankruptcy unless

favorable covenants are negotiated

Oberhausen an

der Donau

(Germany)

Debitex

(France)

4. Public

/Private credit

financing

Similar as above,

but funds

borrowed from

public and private

sources

Private lenders tend to

follow the more lenient

credit terms of public

sources, sometimes

enabled by partial risk

guarantees

No impact on local taxes

Borrowing from private sources

could be affected by restricted

access to capital

Reso-LIAN

(France)

Verkko-

osuuskunta

Kuuskaista

(Finland) only

public financing

Imagen de ejemplo

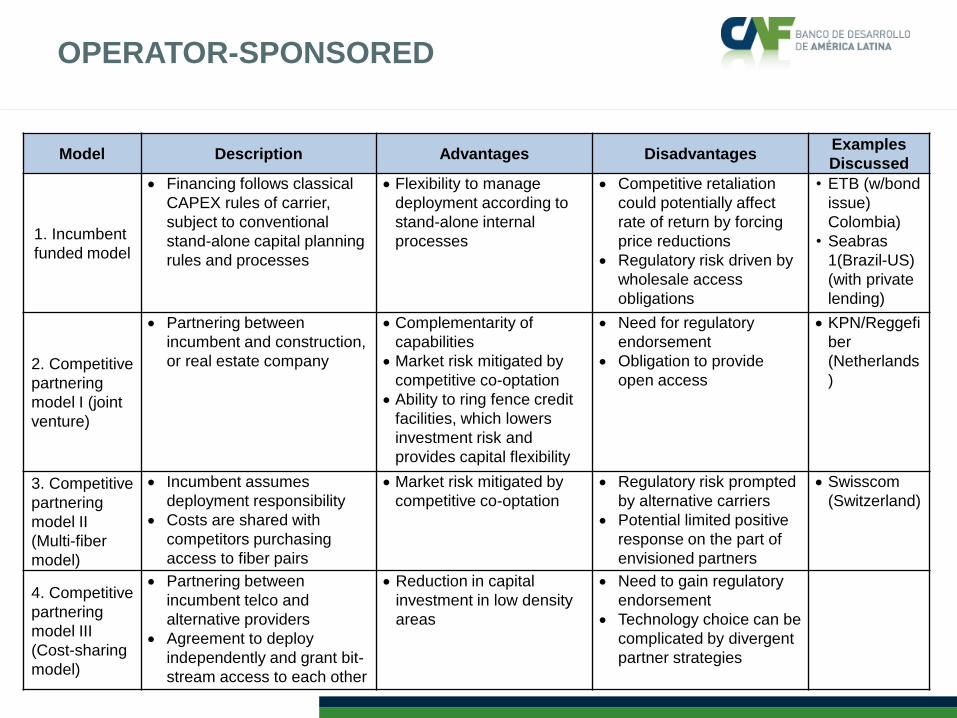

OPERATOR-SPONSORED

Model Description Advantages Disadvantages Examples

Discussed

1. Incumbent

funded model

Financing follows classical

CAPEX rules of carrier,

subject to conventional

stand-alone capital planning

rules and processes

Flexibility to manage

deployment according to

stand-alone internal

processes

Competitive retaliation

could potentially affect

rate of return by forcing

price reductions

Regulatory risk driven by

wholesale access

obligations

• ETB (w/bond

issue)

Colombia)

• Seabras

1(Brazil-US)

(with private

lending)

2. Competitive

partnering

model I (joint

venture)

Partnering between

incumbent and construction,

or real estate company

Complementarity of

capabilities

Market risk mitigated by

competitive co-optation

Ability to ring fence credit

facilities, which lowers

investment risk and

provides capital flexibility

Need for regulatory

endorsement

Obligation to provide

open access

KPN/Reggefi

ber

(Netherlands

)

3. Competitive

partnering

model II

(Multi-fiber

model)

Incumbent assumes

deployment responsibility

Costs are shared with

competitors purchasing

access to fiber pairs

Market risk mitigated by

competitive co-optation

Regulatory risk prompted

by alternative carriers

Potential limited positive

response on the part of

envisioned partners

Swisscom

(Switzerland)

4. Competitive

partnering

model III

(Cost-sharing

model)

Partnering between

incumbent telco and

alternative providers

Agreement to deploy

independently and grant bit-

stream access to each other

Reduction in capital

investment in low density

areas

Need to gain regulatory

endorsement

Technology choice can be

complicated by divergent

partner strategies

Imagen de ejemplo

PUBLIC-PRIVATE PARTNERSHIPS

Model Description Advantages Disadvantages Examples Discussed

1. Debt-facilitation

model

Public entity

facilitates access to

tax-exempt

financing

No commitment to

use public funds

No public funds are

placed at risk

Potential misalignment

of objectives between

parties

Limited leverage of

public party capabilities

(Right of Way, facilities)

Mesoamericana

Information Highway

(C. America)

2. Debt-guarantee

model

Government

guarantees debt,

secured by private

party

Access to better

financial terms of

debt

Public funds are placed

at risk

Cable San Andres

(Colombia)

3. Public service

delegation

Private player

deploys broadband

network with or

without partial

public subsidy

Player has a

concession to resell

the passive or

active layers to

service providers

Risk is assumed by

outside player

Subsidy is needed to

attract the concession

holder

Lack of commitment

of project sponsor

might result in service

failure

Red Dorsal Peruana

Red Azteca de

Colombia

Imagen de ejemplo

AS SHOWN, NO “ONE-SIZE FITS ALL” MODEL

Optimal models are driven by the characteristics of the

market in which they are applied

o Public-owned models are appropriate for rural settings

o As expected, operator-sponsored are most suited to urban

environments

o Public-private models are the best choice in backbone and

open access networks

Financing model suitability is also a function of the reliance

on equity, debt or public funds

Imagen de ejemplo

THERE IS AN IMPLICIT ADVANTAGE TO RELY

ON PUBLIC LENDERS

They have a pricing advantage over commercial lenders

derived from credit rating and profit model

They tend to offer longer maturity products of 10 years and

more

Public lenders can also contribute with much need

technology and industry expertise, either through internal

resources or grants

Their participation provides a project credibility stamp that

can help attracting commercial lenders

Imagen de ejemplo

Broadband financing mechanisms

Broadband funding case studies

Advantages and disadvantages of funding models

Practices contributing to mitigating project risk

Background

Conclusion

Imagen de ejemplo 1. Careful

development of business plan

2. Careful assessment of project risks

3. Demand aggregation to achieve critical mass

Careful assessment of future revenues (avoid over-optimism in subscriber

uptake or ARPU)

Do not underestimate timing of competitive retaliation

Stress-test the business plan

Even if primary funding comes from public sources, pay attention to

business plan and project context

Search for agreements to share deployment costs

Secure a third party in search and negotiation of appropriate funding

Completion risk (construction)

Technology risk (substitution, premature obsolescence, replacement costs)

Pricing risk in the supply of equipment

Economic and financial risk (stress testing the business plan)

Currency fluctuation risk

Political and regulatory risk

Environmental risk (for example, trench digging)

Force majeure risk

Aggregate demand from public agencies and businesses resident in

area of deployment to gain “anchor tenants”

Sign demand aggregation contracts in anticipation or parallel to

deployment

In the case of submarine cables, aggregation could be conducted with

content providers or CDNs

Consider demand aggregation through grassroots facilitation among

consumer groups in “last mile” projects

RECOMMENDATIONS (cont…)

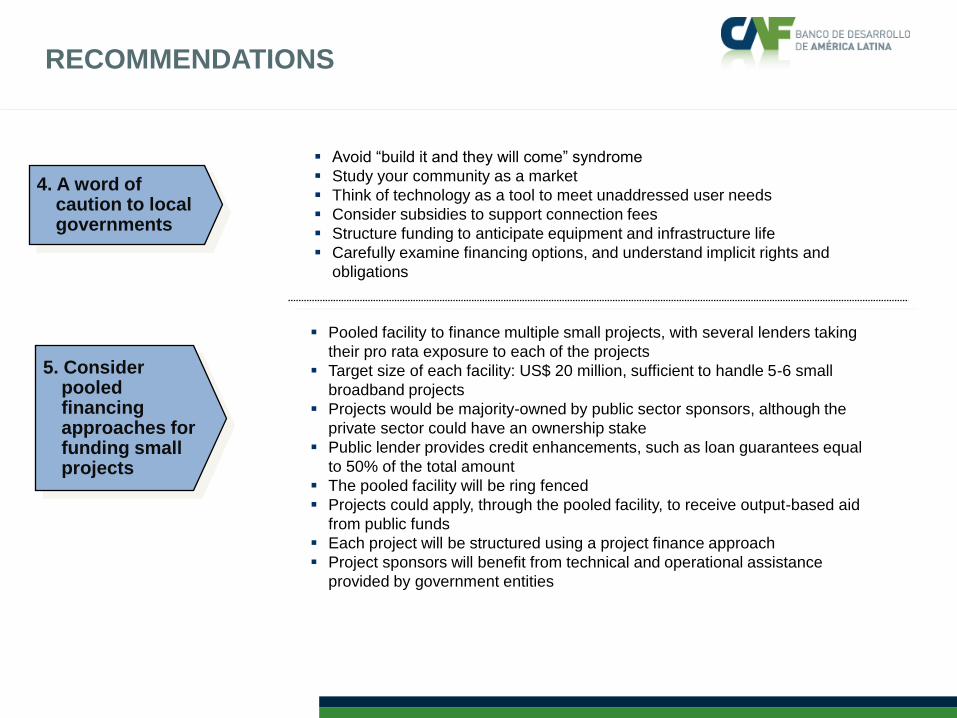

Imagen de ejemplo 4. A word of caution to local governments

5. Consider pooled financing approaches for funding small projects

Avoid “build it and they will come” syndrome

Study your community as a market

Think of technology as a tool to meet unaddressed user needs

Consider subsidies to support connection fees

Structure funding to anticipate equipment and infrastructure life

Carefully examine financing options, and understand implicit rights and

obligations

Pooled facility to finance multiple small projects, with several lenders taking

their pro rata exposure to each of the projects

Target size of each facility: US$ 20 million, sufficient to handle 5-6 small

broadband projects

Projects would be majority-owned by public sector sponsors, although the

private sector could have an ownership stake

Public lender provides credit enhancements, such as loan guarantees equal

to 50% of the total amount

The pooled facility will be ring fenced

Projects could apply, through the pooled facility, to receive output-based aid

from public funds

Each project will be structured using a project finance approach

Project sponsors will benefit from technical and operational assistance

provided by government entities

RECOMMENDATIONS

Imagen de ejemplo

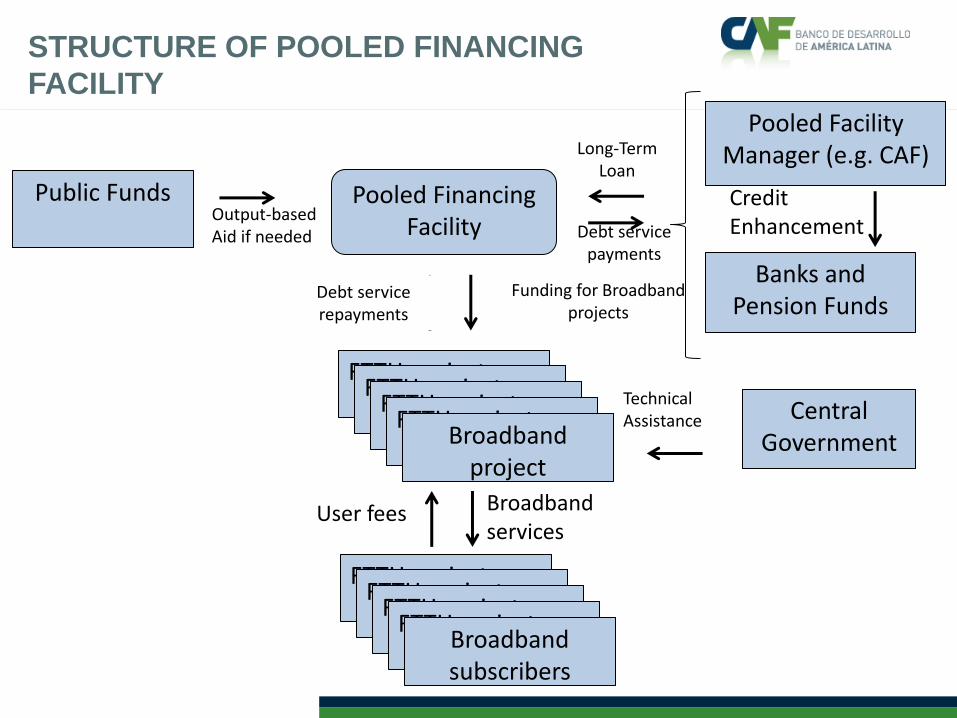

STRUCTURE OF POOLED FINANCING

FACILITY

Pooled Financing Facility

FTTH project FTTH project

FTTH project FTTH project

Broadband project

FTTH project FTTH project

FTTH project FTTH project

Broadband subscribers

Funding for Broadband projects

Debt service repayments

Broadband services

User fees

Pooled Facility Manager (e.g. CAF)

Banks and Pension Funds

Credit Enhancement

Long-Term Loan

Debt service payments

Public Funds Output-based Aid if needed

Central Government

Technical Assistance

Imagen de ejemplo

BENEFITS OF POOLED FINANCING

Small broadband projects can be financed without

reliance on the financial abilities of local governments or

the central government

Small projects could attract funding at more lenient terms

than if they were to go directly to the private debt markets

Financial accountability and transparency will be assured

by the lenders to the pooled facility because they would

be use conventional project finance funding structures to

mitigate risk

Private lenders gain experience in financing broadband

ventures, which help them gain an understanding of risk

mitigation strategies, and make them more inclined to

offer credit to other projects

Imagen de ejemplo

Broadband financing mechanisms

Broadband funding case studies

Advantages and disadvantages of funding models

Practices contributing to mitigating project risk

Background

Conclusion

Imagen de ejemplo

CONCLUSION

Success or failure of a broadband project is a function of

the investment case (revenues, CAPEX and OPEX) and the

financing model

Not “one size fits all” funding models

Optimal model depends on projects sponsor and business

plan

There is an implicit advantage to rely on public lenders such

as the CAF, IDB and EIB

Consider practices that contribute to mitigate the project

financial risk

www.caf.com

http://publicaciones.caf.com/

Detrás de todo lo que hacemos estás tú.

www.caf.com