bre bank securities 5 july 2007 periodic report equity...

TRANSCRIPT

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities BRE Bank Securities

Periodic Report

Monthly Report July 2007

Equity market Tekst Company News Banks. Tekst Gas & Oil. Tekst Telecommunications. Tekst Media. Tekst IT. Tekst Metals. Tekst Construction. Tekst Pharmaceuticals. Tekst Retail\Wholesale. Tekst Others. Tekst

BRE Bank Securities does not rule out offering brokerage services to an issuer of securities being the subject of a recommendation. Information concerning a conflict of interest arising in connection with issuing a recommendation (should such a conflict exist) is located on the final page of this report.

16 July 2007

WIG vs. indices in the region

BRE Bank Securities

Equity Market

Macroeconomics

Avg daily trading volume

Average P/E 2008

Average P/E 2007

WIG X X

X

PLN X m

BRE Bank Securities

Periodic Report

Monthly Report July 2007

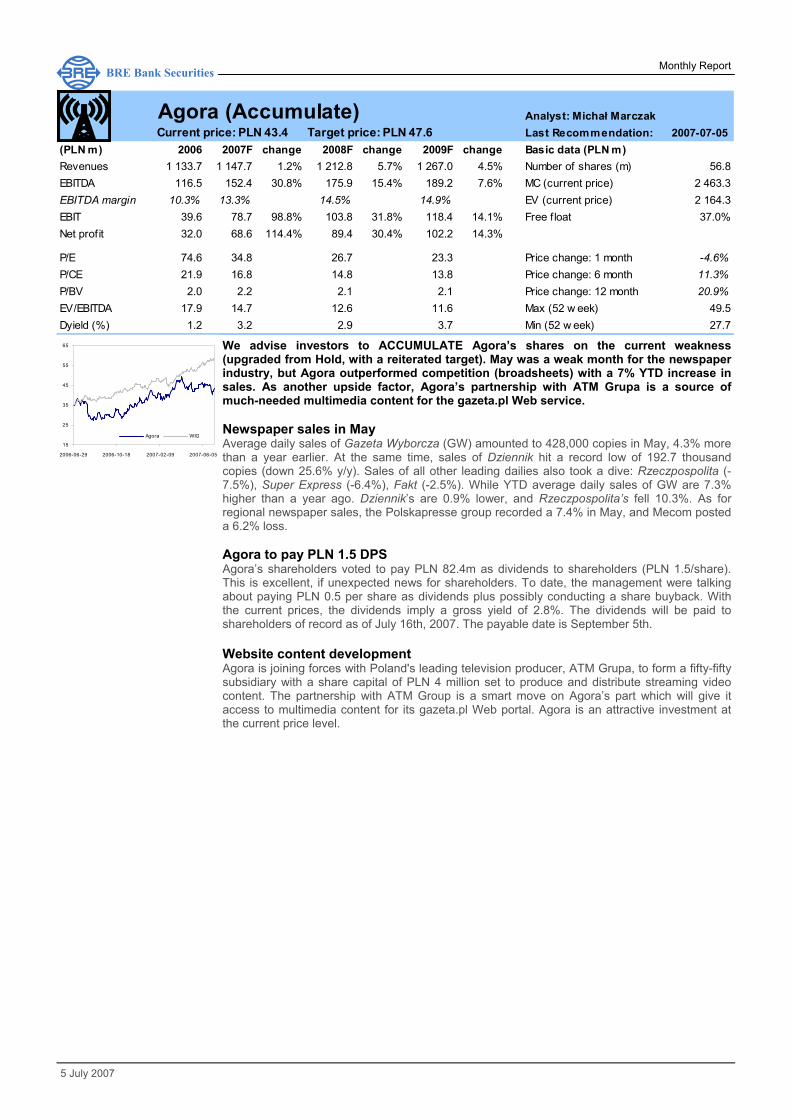

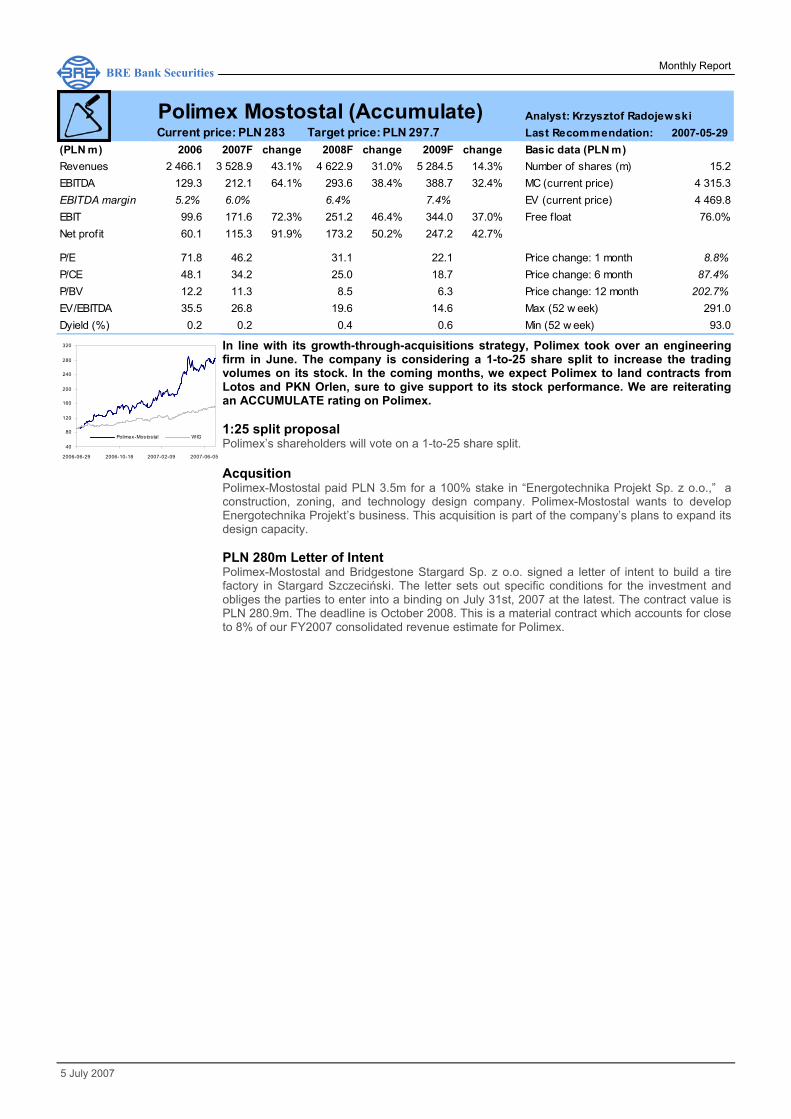

Equity market We expect equities to run out of breath in late August/early September, preceded by new record highs in indexes (driven by foreign markets). We still prefer WIG20 stocks over midcaps. In large caps, we advise to overweight commodity stocks (PKN, KGHM) as they gain on soaring commodity prices, and underweight banks. Banks. The WSE’s bank stock index WIG-Banki rose 1% since our last Monthly Report compared to a 3.6% gain in the WIG index and a 2.4% gain in the WIG20. We were right in advising investors to take profits on bank shares. June’s biggest losers were BZ WBK (6.5%), Bank Handlowy (5.4%), BPH (3.5%). July will be marked by FQ2 earnings previews. We anticipate that banks will show equally strong growth as in the first quarter, as indicated by the bank industry’s robust debt and asset growth. This rosy outlook is for the most part already priced in bank stocks. Gas&Oil. With the US’s supply cushion worn thin to the point of non-existence, as demand reaches its seasonal peak, another bout of gasoline price hikes is to be expected in July/August. Energy stocks will be further supported by an increase in crude oil prices spurred by hurricane fears in the Gulf of Mexico. Telecoms. After a suspected leak of TPSA’s new strategic objectives, we expect the management to just-reiterate their old targets, and announce the new strategy a few months later. We advise investors to reduce positions on the ongoing buy-back. Media. The media sector's weak performance is a result of slower ad revenue growth. We recommend to overweight Agora and underweight TVN at the current price level. IT. IT firms are still feeling the shortage of orders from the government. We maintain that a revival in government spending cannot be expected until after the summer holidays. Construction. Construction production slowed down to 16.3% y/y in May (YTD growth stood at 40% relative to a year earlier), somewhat dampening investor sentiment to building stocks. The sentiment will remain subdued until the second-quarter earnings season which promises to be good. We have an ACCUMULATE rating on Polimex. Retail. As the FMCG industry continues to consolidate, we expect a series of acquisition news, especially from Emperia which is preparing for an SPO after the summer holidays. Even so, neither Emperia nor Eurocash are our favorite investment picks at the current price levels. Ratings. We are upgrading our ratings on Agora (Accumulate), BZ WBK (Hold), Erbud (Accumulate), Bank Handlowy (Reduce), and downgrading TP SA (Reduce) and ZA Puławy (Hold) as of the date of this release. Our rating on Kredyt Bank is under revision. Provimi-Rolimpex is suspended.

BRE Bank Securities does not rule out offering brokerage services to an issuer of securities being the subject of a recommendation. Information concerning a conflict of interest arising in connection with issuing a recommendation (should such a conflict exist) is located on the final page of this report.

Analysts:

Marta Jeżewska (+48 22) 697 47 37 marta.jeż[email protected]

Michał Marczak (+48 22) 697 47 38 [email protected]

Krzysztof Radojewski (+48 22) 697 47 01 [email protected]

Kamil Kliszcz (+48 22) 697 47 06 [email protected] Piotr Janik (+48 22) 697 47 40 [email protected]

Macroeconomic Analyst Janusz Jankowiak

5 July 2007

WIG vs. indices in the region

BRE Bank Securities

Equity Market Macroeconomics

Avg daily trading volume

Average 2008 P/E

Average 2007P/E

WIG 66 952 20.6

17.9

PLN 2 010m

30000

35000

40000

45000

50000

55000

60000

65000

06-06-21 06-10-17 07-02-12 07-06-10

pkt

WIG BUX PX

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Table of Contents 1. Equity market ........................................................................................ 3 2. Current ratings by BRE Bank Securities S.A. ........................................ 5 3. Ratings statistics ................................................................................... 6 4. Macroeconomics ................................................................................... 7 5. Fund Flows ............................................................................................ 8 6. Financial Sector ..................................................................................... 10

6.1. BPH ............................................................................................ 12 6.2. BZ WBK ...................................................................................... 13 6.3. Handlowy .................................................................................... 14 6.4. ING BSK ..................................................................................... 15 6.5. Kredyt Bank ................................................................................ 16 6.6. Millennium .................................................................................. 17 6.7. Pekao SA ................................................................................... 18 6.8. PKO BP ...................................................................................... 19

7. Gas & Oil, Chemicals .............................................................................. 23 7.1. Lotos ........................................................................................... 24 7.2. PGNiG ........................................................................................ 25 7.3. PKN Orlen .................................................................................. 26 7.4. ZA Puławy .................................................................................. 28

8. Telecommunications .............................................................................. 29 8.1. Netia ........................................................................................... 30 8.2. TP SA ......................................................................................... 31 9. Media ..................................................................................................... 33 9.1. Agora .......................................................................................... 34 10. IT Sector ................................................................................................ 35 10.1. ABG Ster-Projekt ...................................................................... 37 10.2. Asseco Poland .......................................................................... 38 10.3. ComArch ................................................................................... 39 10.4. Macrologic ................................................................................ 40 10.5. Prokom Software ...................................................................... 41 10.6. Sygnity ...................................................................................... 42 10.7. Techmex ................................................................................... 43 11. Metals .................................................................................................... 44 11.1. Kęty ........................................................................................... 44 11.2. KGHM ........................................................................................ 45 11.3. Koelner ...................................................................................... 46 12. Construction .......................................................................................... 47 12.1. Budimex ..................................................................................... 50 12.2. Elektrobudowa ........................................................................... 51 12.3. Erbu ........................................................................................... 51 12.4. Hydrobudowa Śląsk ................................................................... 52 12.5. Polimex Mostostal ...................................................................... 53 12.6. Rafako ....................................................................................... 54 12.7. Ulma Construccion Polska ......................................................... 54 13. Pharmaceutical Manufacturers and Distributors .................................... 55 13.1. Farmacol .................................................................................... 55 13.2. PGF ........................................................................................... 55 13.3. Prosper ...................................................................................... 56 13.4. Torfarm ...................................................................................... 56 14. Retail\Wholesale .................................................................................... 57 14.1. Eldorado .................................................................................... 58 14.2. Eurocash ................................................................................... 59 15. Others .................................................................................................... 60 15.1. Kogeneracja .............................................................................. 60 15.2. Mondi ......................................................................................... 61

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Equity market June was marked by considerable stock volatility, both locally and globally, spurred mainly by increasing debt yields. Investors were rattled by concerns that, if US 10Y notes hit the 5.3% yield mark, or the German Bunds spiked to 4.7%, capital would switch from equity to debt. Fears of an increase in inflation and further rate hikes in the US and EU are exaggerated in our view (base inflation in both markets is in a downtrend, and stays in line with central bank targets). The probability of monetary loosening in the US decreased after a positive leading indicators report, but it is still higher than the probability of tightening. This guess is based on the assumption that, after rising to 3% in Q2, the US GDP will pull back down to 1.8% in the second half of the year on continued weakness in the construction industry, which should finally result in job cuts that will, in turn, reduce consumption. We will see similar trends in the EU where interest rate hikes (the two upcoming hikes are priced in) are in store to produce a cooling effect on the economy (2007 GDP growth projected at 2.7%, down to 2.0% in 2008). In some EU countries, the interest rate-sensitive construction industry already has an 18% share in the GDP. A slower GDP, and hence also company earnings, might spur a stronger correction in equity markets after the summer holidays, with the emergence of data confirming these predictions. However, such a downturn will not eliminate global excess liquidity, i.e. the availability of cheap money keeping the long uptrend in place. A market decline and the accompanying uncertainty will bring stock prices down to levels that investors should consider attractive. Simultaneously, bond yields will slide on expectations of interest rate cuts to 4.7% in the US (from 5.09%), and to 4.4% (from 4.57%) in the euro zone. The dollar’s expected further weakening should drive commodity prices and emerging markets. In the near term, foreign investors might turn their attention to the yen which is underpriced according to many analysts. A rapid appreciation could affect stock markets. In this environment, the Polish equity market is also in for a longer correction, additionally underpinned by IPOs. Note that the market is already very selective at this point. In line with our sector calls, small and mid-sized banks underwent a correction in June, while energy stocks and TPSA rallied. We expect these trends to continue through August, and see equities run out of breath in late August/early September, preceded by new record highs in indexes (driven by foreign markets). We still prefer WIG20 stocks over midcaps as cheaper and less prone to a downturn in case of a correction. Among large caps, our best bets are commodity stocks like PKN, KGHM which are gaining on soaring commodity prices, and our least favorite picks are banks (ING BSK, Handlowy, Millenium, BZ WBK), which will be the first to feel the impact of any monetary tightening. TPSA is no longer an attractive investment at the current price level. Real-estate developers are still under supply pressure. Polish stocks remain bullish amidst favorite market settings, despite looming macro trouble. But we should point out that the recent rallies are not as strong as observed in most emerging markets, also in our part of the world, which is most likely a sign of weakness. We see several reasons for this:

• large equity holdings by open pension funds (OFEs, ca. 39%) which have come close to the equity component cap (40%), and which will therefore generate lower demand for stocks going forward,

• increasing investments by investment fund companies (TFs) in foreign markets (though still relatively small),

• valuations relative to other emerging markets discourage foreign investors (commodity stocks are an exception),

• upcoming supply of shares from IPOs in the fall (ca. PLN 10bn). All these factors would be of no importance if the economy’s outlook were more rosy. But there is a real risk of a supply barrier obstructing growth. An inefficient labor market, paired with upward salary pressure and huge internal demand (which grows 3% over GDP), might cause the economy to overheat and spark a much harsher reaction from the Monetary Policy Council than the market is expecting. The budget provides for one more interest rate hike this year and two next year (the repo rate pegged at 5% in 2008). This scenario is priced in at this point, but the August/September inflation and productivity data could shift these expectations by another 50-100 bps. Such hikes would have a real impact on the economy (GDP slowdown in 2H2008 and 2009). We are most concerned about the bank sector where valuations already factor in the expected robust growth in lending at lower interest rates. From the standpoint of foreign investors, the zloty should appreciate further in the near term, supported by the interest rate situation. Against what is expected of the ECB, the hikes foreseen in the budget denote a strengthening of the zloty. But if foreign capital deems the Council’s reaction too late, and given that future economic growth is threatened by necessary remedial measures (monetary tightening), we will see a rapid outflow of capital. Concerns over a depreciation in the zloty imply a sellout on the Warsaw Stock Exchange.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Like we already said last month, we see this as “Scenario B”, but it will very likely play out toward the end of the summer. We will not know if these are valid concerns, or just another opportunity to buy share, until we see the Q4 data.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Current ratings by BRE Bank Securities

Security Rating Target Price Date Issued

ABG STER-PROJEKT Hold 7.87 2007-01-08 AGORA Accumulate 47.60 2007-07-05 ASSECO POLAND under revision 2007-05-11 BPH Accumulate 1079.00 2007-05-31 BUDIMEX Hold 121.70 2007-05-29 BZWBK Hold 284.10 2007-07-05 COMARCH Reduce 185.80 2007-02-05 ELEKTROBUDOWA Hold 221.50 2007-05-29 EMPERIA HOLDING Reduce 134.17 2007-05-21 ERBUD Accumulate 100.00 2007-07-05 EUROCASH Sell 7.38 2007-02-05 FARMACOL Accumulate 62.90 2007-06-25 HANDLOWY Reduce 109.00 2007-07-05 HYDROBUDOWA ŚLĄSK Hold 209.00 2007-05-29 ING BSK Reduce 953.50 2007-06-06 KĘTY Reduce 180.50 2007-06-06 KGHM Accumulate 119.00 2007-07-03 KOELNER Sell 53.72 2007-05-09 KOGENERACJA under revision 2007-06-06 KREDYT BANK under revision 2007-07-05 LOTOS Hold 45.80 2007-05-09 MACROLOGIC Buy 58.43 2007-02-13 MILLENNIUM Sell 10.54 2007-06-06 MONDI Reduce 80.00 2006-12-05 NETIA Sell 3.80 2006-09-06 PEKAO Hold 269.00 2007-06-06 PGF Reduce 98.40 2007-06-25 PGNiG Suspended 2007-02-05 PKN ORLEN Accumulate 61.00 2007-07-02 PKO BP Hold 54.44 2007-05-31 POLIMEX MOSTOSTAL Accumulate 297.70 2007-05-29 PROKOM SOFTWARE Hold 150.30 2007-02-05 PROSPER Hold 27.00 2007-06-25 PROVIMI-ROLIMPEX Suspended 2007-07-05 RAFAKO Reduce 11.40 2007-05-29 SYGNITY under revision 2007-06-06 TECHMEX under revision 2007-03-07 TELEKOMUNIKACJA POLSKA Reduce 20.20 2007-07-05 TORFARM Hold 95.3 2007-06-25 ULMA CONSTRUCCION POLSKA Hold 306.6 2007-05-29 ZA PUŁAWY Hold 127.98 2007-07-05

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Ratings issued in the past month

Ratings Statistics

All Clients of BRE Bank Securities

Statistics Sell Reduce Hold Accumulate Buy Sell Reduce Hold Accumulate Buy

count 4 9 13 6 1 1 2 6 2 0 % of total 12.1% 27.3% 39.4% 18.2% 3.0% 9.1% 18.2% 54.5% 18.2% 0.0%

Ratings changed as of July 5th

Security Rating Previous Target Price Date Issued

AGORA Hold Accumulate 47.60 2007-06-06

BZWBK Reduce Hold 284.10 2007-06-06

FARMACOL Accumulate under revision 62.90 2007-06-25

HANDLOWY Sell Accumulate 109.00 2007-06-06

ING BSK Reduce Hold 953.50 2007-06-06

KĘTY Reduce Hold 180.50 2007-06-06

KGHM Accumulate Hold 119.00 2007-07-03

KOGENERACJA under revision Buy 2007-06-06

KREDYT BANK Hold Accumulate 23.51 2007-06-06

MILLENNIUM Sell Hold 10.54 2007-06-06

PEKAO Hold Accumulate 269.00 2007-06-06

PGF Reduce under revision 98.40 2007-06-25

PKN ORLEN Accumulate Buy 61.00 2007-07-02

PROSPER Hold under revision 27.00 2007-06-25

TORFARM Hold under revision 95.30 2007-06-25

Security Rating Previous Target Price Date Issued

TP SA Reduce Hold 20.20 2007-07-05

ZA PUŁAWY Hold Buy 127.98 2007-07-05

HANDLOWY Reduce Sell 109.00 2007-07-05

KREDYT BANK Under revision Hold - 2007-07-05

BZ WBK Hold Reduce 284.10 2007-07-05

ERBUD Accumulate Hold 100.00 2007-07-05

AGORA Accumulate Hold 47.60 2007-07-05

PROVIMI-ROLIMPEX Zawieszona Hold - 2007-07-05

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Slower economic growth, paired with increasing salaries and inflation, indicates that the Polish economy is bumping against significant supply obstacles. Meanwhile, next year’s budget plans suggest that the Polish government wants to continue its policy of supporting demand with a fiscal impulse, leading to a deepening macroeconomic imbalance. We expect a harsh reaction from the Central Bank, manifested in policy tightening. The sub-optimal policy mix will slow economic growth dramatically in 2009. Any measure to stimulate demand, especially amidst a robust autonomous demand (unless designed to rapidly throw the fundamentals off balance), must be countered with appropriate supply measures. It seems reasonable that, if the govern-ment wants to influence aggregate demand through fiscal policy, then, to prevent prices from increasing, it also has to create an environment that will foster supply. Unfortunately, recent pro-supply measures do not look promising. 2005-2008 core macroeonomic indicators, delivery and forecasts

Source: GUS, Ministry of Finance The key macroeconomic indicators look good. But the Polish Business Roundtable (PRB) of-fered more cautious forecasts as regards economic growth (5.3%), inflation (average annual CPI 2.7%), and the C/A deficit (C/A -4.8%.GDP). Contrary to bleak predictions, the zloty held strong in June. It was confirmed that any weak-ness on our currency attracts euro-selling exporters to the market, protecting the zloty against a sharp downturn. Interest rate hike expectations are also not without importance. The market is just starting to appreciate the scale of this and next year’s hikes (5% and 6% respectively, repo rate at period-ends). Given the expected weakening of the dollar against the euro, it is reasonable to anticipate that the zloty will appreciate against the dollar in the third quarter (2.75). At the same time, it will stay below 3.90 against the euro. If expectations of a rate hike to 5% by the Monetary Policy Council by the end of the year are maintained, and the ECB stops tightening at 4.00% until fall, the zloty/euro exchange rate might temporarily fall as low as 3.70. The debt market responded with a sharp rise in yields to the steepening in the base market curve and increasing inflation expectations in Poland. Volatility increased markedly over the past few weeks. The reason besides global factors was the distribution of votes within the Monetary Policy Council (a steady 6:4 in favor of tightening) determining possible interest rate hike decisions. The monetary policy is obviously data dependent, although most investors are inclined to think that the Council is already behind the curve and will have to apply more dras-tic measures to bring inflation back on track. Hence, even if one Council member changes sides, market expectations will change. Any suggestion of a change of heart within the Council in favor of tightening might raise the curve even steeper. And if the market becomes convinced that the cycle will significantly exceed the current expectations (50bps this year), the correction will be deep. This would definitely have happened in case of a hike in June, as the 5.80% mark on 10Y bonds would have been far exceeded.

Indicator 2005 2006 2007P 2008F GDP % 103.6 106.1 106.5 105.7 Exports % 108.0 114.5 111.0 109.0 imports % 104.7 115.8 115.5 111.2 Local demand % 102.4 106.6 108.5 106.8 Consumption % 102.7 104.9 105.3 104.7 -private % 102.0 105.2 106.4 105.8 -public % 105.0 103.7 101.5 101.0 accumulation % 101.4 114.1 119.4 113.4 -gross fixed-asset expenditure % 106.5 116.5 118.0 114.0 CPI (avg./year) % 102.1 101.0 102.0 102.3 PPI (avg./year) % 100.7 102.3 102.3 102.3 Avg. gross salary PLN 2 360.6 2 477.2 2 656.0 2 815.0 Avg. employment thousands 8 786.4 8 982.0 9 242.0 9 453.0 Unemployment rate (end-of-year) % 17.6 14.9 11.3 9.9 PLN/USD (avg.) PLN 3.23 3.1 2.84 2.77 PLN/EUR (avg.) PLN 4.03 3.9 3.81 3.74 USD/EUR (avg.) USD 1.24 1.26 1.34 1.35 C/A to GDP % -1.7 -2.3 -3.9 -4.7

Macroeconomics

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

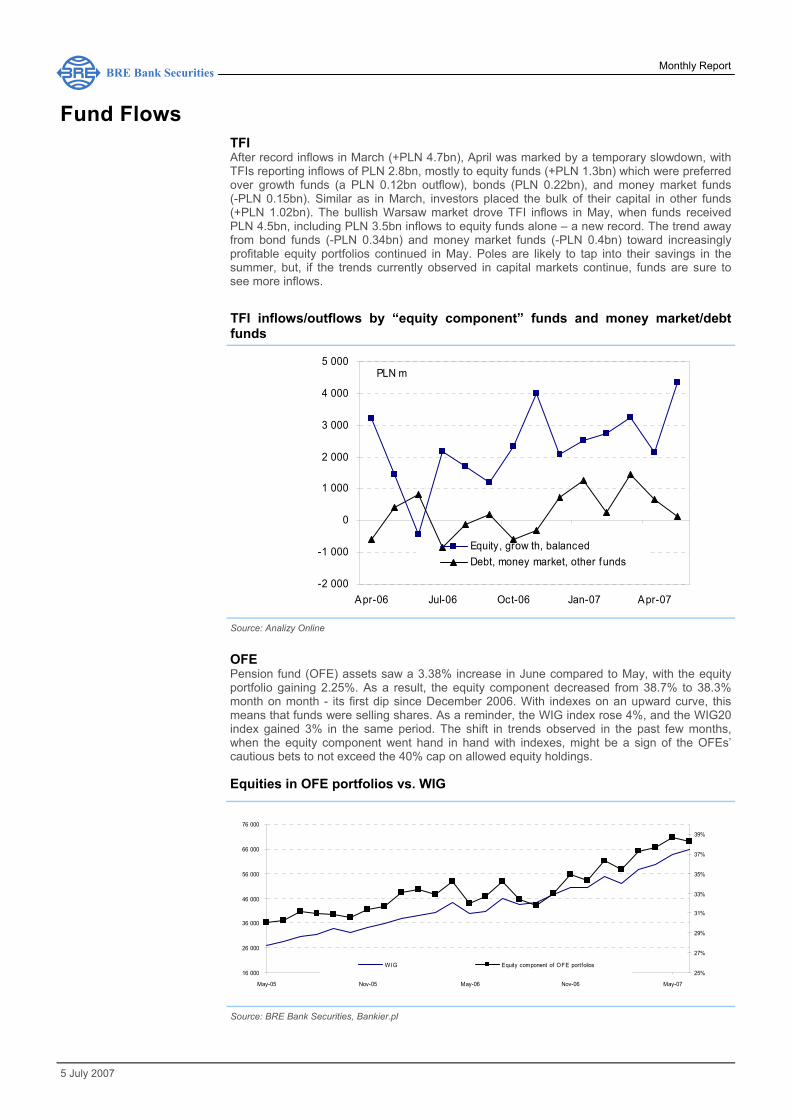

TFI After record inflows in March (+PLN 4.7bn), April was marked by a temporary slowdown, with TFIs reporting inflows of PLN 2.8bn, mostly to equity funds (+PLN 1.3bn) which were preferred over growth funds (a PLN 0.12bn outflow), bonds (PLN 0.22bn), and money market funds (-PLN 0.15bn). Similar as in March, investors placed the bulk of their capital in other funds (+PLN 1.02bn). The bullish Warsaw market drove TFI inflows in May, when funds received PLN 4.5bn, including PLN 3.5bn inflows to equity funds alone – a new record. The trend away from bond funds (-PLN 0.34bn) and money market funds (-PLN 0.4bn) toward increasingly profitable equity portfolios continued in May. Poles are likely to tap into their savings in the summer, but, if the trends currently observed in capital markets continue, funds are sure to see more inflows.

Fund Flows

TFI inflows/outflows by “equity component” funds and money market/debt funds

Source: Analizy Online

OFE Pension fund (OFE) assets saw a 3.38% increase in June compared to May, with the equity portfolio gaining 2.25%. As a result, the equity component decreased from 38.7% to 38.3% month on month - its first dip since December 2006. With indexes on an upward curve, this means that funds were selling shares. As a reminder, the WIG index rose 4%, and the WIG20 index gained 3% in the same period. The shift in trends observed in the past few months, when the equity component went hand in hand with indexes, might be a sign of the OFEs’ cautious bets to not exceed the 40% cap on allowed equity holdings.

Equities in OFE portfolios vs. WIG

Source: BRE Bank Securities, Bankier.pl

-2 000

-1 000

0

1 000

2 000

3 000

4 000

5 000

Apr-06 Jul-06 Oct-06 Jan-07 Apr-07

PLN m

Equity, grow th, balanced Debt, money market, other funds

16 000

26 000

36 000

46 000

56 000

66 000

76 000

May-05 Nov-05 May-06 Nov-06 May-07

25%

27%

29%

31%

33%

35%

37%

39%

WIG Equity component of OFE portfolios

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Emerging market funds Between May 30th and June 27th, EM funds received $3.1bn in inflows (+0.27%). The biggest gainers were Latin America (+$2.5bn; +8.07%) and global funds (+$2.3bn; +0.31%). EMEA funds recorded total outflows of $0.2bn (-0.49%), but this should not raise concerns about local index volatility in the future. Asian market funds were the biggest losers with a whopping $1.4bn combined outflow (-0.98%), but the situation seems to have steadied in the past few weeks. Overall, despite negative flows in May and June, the last two weeks of June witnessed a rebound (+$0.6bn; +0.004%), possibly showing that sentiment has eased for the time being.

Weekly inflows/outflows for selected emerging market funds

Source: EmergingPortfolio.com

GEM

-3 000-2 500-2 000-1 500-1 000

-5000

5001 0001 500

4-01

4-03

4-05

4-07

4-09

4-11

4-01

4-03

4-05

mln USD EMEA

-2 000

-1 500

-1 000

-500

0

500

1 000

4-01

4-03

4-05 4-07

4-09

4-11

4-014-0

34-0

5

mln USD$ millions $ millions

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Financial Sector Pengab down for second month in a row The banking industry’s sentiment indicator fell 2.4pts to 38pts in June. For the first time in months, the indicator was lower than in the corresponding period a year earlier (in June 2006, it stood 1.2pts over the current level). If it goes any further down, we will be able to speak about a trend reversal. The Pengab is a product of surveys conducted on 200 bank outlets. Last month, branch managers predicted that Poles will shift away from deposits and toward financial instru-ments. In loans, demand for zloty financing and home loans is expected to decline, while de-mand for corporate loans will probably pick up. We are reiterating our outlook on the sector. We believe that banks are fully capable of fulfilling our long-term forecasts. As for the Pengab slip-page, no one can expect the industry to stay super-optimistic for too long. We think that, as last year's comparable base increases, branch managers worry about their capacity to continue to show strong growth. Loan demand is threatened by expectations of interest rate hikes. We as-sume that volumes will continue to rise, though at a slower pace.

Banks netted PLN 3.6bn for FQ1’07, chalking up 22.3% Y/Y increase The GUS reported that net income generated by banks in FQ1 chalked up a 22.3% y/y increase to PLN 3.6bn. Household loans surged 38.7%, and corporate loans rose 17.5%. The survey included 64 commercial banks and 583 co-op banks. These numbers are in line with preliminary statistics released earlier by the GINB, showing an aggregate net income generated by the bank sector at PLN 3.64bn after a 22% increase. The market has already discounted the strong earnings expected for FY2007. We predict that the banks in our coverage universe will report an 18% y/y increase in their FY2007 bottom line income. UOKiK’s intercharge battle Almost six month after the competition watchdog UOKiK ruled on the intercharge fee issue and accused leading Polish banks of fixing prices, nothing has been done as a way of punishment. The fines imposed on 20 banks (PLN 164m in total) were enforceable immediately, but the banks appealed and nothing more has been heard in the matter since then. Now, the UOKiK decided to go to court. The case files are around 25 thousand pages, so, this is shaping up to be a long process. As long as the UOKiK stops at cash fines, bank earnings will not suffer. Most of the listed banks fined (except for Bank Handlowy) recognized appropriate allowances back in Q4’06. We think that banks will scale intercharge fees back in the future as card payment vol-umes increase. What could hurt bank income would be if the court ordered a rapid and deep cut in the fees. Another risk is that retailers will claim back the fees unlawfully charged in the past. As things stand, however, we think that the probability of the worst-case scenario is very low. Kwaśniak to advise NBP President, Janc appointed GINB head Wojciech Kwaśniak, who recently resigned from his position as head of the General Inspector-ate for Banking Supervision (GINB), accepted a job as advisor to Sławomir Skrzypek in matters concerning Poland's financial security network. He was replaced by Alfred Janc, Professor with the Poznań University of Economics. The change poses a risk of delays in the Pekao/BPH merger schedule and sale of the “Mini-BPH” spun off from BPH. Bank supervision has not given clearance to the merger yet, and the new Head of GINB will probably need some time to ac-quaint himself with the documentation.

Pengab; left-hand chart: 01.06 – 06.07; right-hand chart: 01.1993 – 06.07

0

10

20

30

40

50

60

Jan-93 Sep-94 May -96 Jan-98 Sep-99 May -01 J an-03 Sep-04 May -06

28.8

28.1 28

.7

33.6 34

.5 35.8

34.5

3436

.2 36.8

42

39

35.8

3335

.1

40.9

37.4 39

.2 40.9

39.9

43.4

43.6

40.3

39.5

38 38.3 40

.744

.1

40.5

38.1

20

25

30

35

40

45

50

Jan-

05

Mar-

05

May-

05

Jul-

05

Sep-

05

Nov-

05

Jan-

06

Mar-

06

May-

06

Jul-

06

Sep-

06

Nov-

06

Jan-

07

Mar-

07

May-

07

Source: BRE Bank Securities, Polish Bank Association

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Mortgage loans still on upward curve PLN 11bn-worth of mortgage loans have been sold year to date. The average loan amount is on an upward trend, reaching PLN 180,000 in Q1 vs. PLN 150,000–160,000 a year earlier. At the beginning of the year, the Polish Bank’s Association (ZBP) forecasted that this year’s sales will amount to PLN 54bn, and has recently reiterated this forecast. We agree with the PLN 54bn target, and predict that mortgage loans sales will continue to increase relative to Q1. To meet the ZBP’s estimates, banks have to sell over PLN 15bn in home loans on average per quarter. BIK issued 40% more credit reports in May than a year earlier The credit information bureau (BIK) issued 1.29m credit reports to banks in May, 40% more than a year earlier. In the period from January to the end of May, the BIK issued 5.59m credit scores, 38% than in the corresponding period of 2006 (915,000 in January, 861,000 in Febru-ary, 1.37 million in March, and 1.14 million in April). Consumer demand for loans continues to be strong. SKOKs gearing up to conquer Russia and Romania The credit and savings union “SKOK" hopes to increase the number of members from 1.6 mil-lion now to 2 million next year. In the future, they hope to lure approximately 30% of Poles, among others by installing some 600 ATMs across the country and opening a clearing center. In terms of credit card issuances, the target for this year is ~0.8 million. All these undertakings will be financed through an upcoming IPO. SKOK also has ambitions to expand internationally, and move into Russia and Romania. SKOK is potentially a dangerous rival to banks that are targeting clients in small towns and rural areas. While its operating scale is relatively small for now, a goal to have 30% of Poles in its client base means that it is determined to expand its reach. Interest rate hikes will not boost profit margins According to Parkiet, a competitive market environment will not allow banks to widen their mar-gins in case of an interest rate hike. Bankers say that such hikes could end the borrowing boom. We agree that monetary policy tightening will not lead to margin expansion. On the lending side, interest rates will only rise on floating-rate facilities (mainly home and corporate loans). On the deposits side, the main beneficiaries of the hike will be banks with large current-account bases. All in all, monetary tightening is good for the bank sector to the extent that it does not affect the lending business. Expander seeks new investor GE wants to find a new investor for Expander, but without giving up its controlling stake in the financial intermediary. The investor’s role would be to develop the financial intermediary’s offer-ing. GE wants to complete the process by the end of the year, and hopes to start receiving of-fers in early July. GE’s advisor in the process is Rothschild Polska. We suspect that GE is accu-mulating cash to pay for BPH. Also, a new investor with decision-making powers will enable GE to focus on the incorporation of BPH into its organization after the takeover. Recent rumors that GE was planning to back out of the Mini-BPH acquisition have not been confirmed. However, the plans to entrust Expander to another investor probably prove that they were false. Dominet gains ground After the takeover by Belgium’s Fortis group, Dominet Bank’s organization will be streamlined to reinforce the business departments and the network expansion department. The bank’s new CEO Jacek Obłękowski revealed that the 2008-2012 growth strategy will be ready to present to the supervisory board in the middle of the year. This means that the changes will start after the summer. The strategy will be designed so as to ensure fast and visible growth while maintaining profitability and security of business. The bank has plans to increase the number of its own branches as well as franchise outlets. Dominet Bank’s entire sales network currently comprises 180 outlets, but this number will be multiplied several times in a few years’ time. The CEO also disclosed that the bank was working on new products, including a home financing facility set to be launched in late 2007 / early 2008. Dominet’s growth poses a competitive threat to listed banks. Considering that all banks have plans to increase market share, the battle is going to be fierce.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska19 Last Recommendation: 2007-05-31(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 2 175.5 2 238.9 2.9% 2 346.1 4.8% Number of shares (m) 28.7Interest margin 3.5% 3.5% 3.6% MC (current price) 28 228.1Revenue f/banking oper. 3 533.6 3 646.0 3.2% 3 873.0 6.2% Free float 25.3%Operating profit 1 853.8 2 171.2 17.1% 2 195.8 1.1%Gross profit 1 633.6 1 895.1 16.0% 1 898.6 0.2%Net prof it 1 267.8 1 493.7 17.8% 1 491.6 -0.1%

ROE 19.2% 21.1% 20.0% Price change: 1 month -1.4%P/E 22.3 18.9 18.9 Price change: 6 month 6.5%P/BV 4.1 3.9 3.7 Price change: 12 month 40.6%D/PS 30.0 36.2 42.7 42.6 Max (52 w eek) 1 088.0Dyield (%) 3.1 3.7 4.3 4.3 Min (52 w eek) 680.0

Current price: PLN 983 Target price: PLN 1079BPH (Accumulate)

600

800

1000

1200

2006-06-29 2006-10-18 2007-02-09 2007-06-05

BPH WIG

Not much has changed over the past month in the way of obtaining clearance necessary to divide BPH, incorporate one part to Pekao, and sell the other part, the Mini-BPH. Bank supervision authorities are taking their time, and UniCredit and GE Money are still in talks. That said, we are not changing our outlook on BPH. Our valuation is a sum of two parts: the per-share price of Pekao multiplied by the exchange ratio (3.3 shares of Pekao for 1 share of BPH), and the selling price of the Mini-BPH. Our current per-share target on BPH (PLN 1079/share) is 82% the assets to be transferred to Pekao (the target on Pekao is PLN 269/share), and 18% the value of Mini-BPH’s assets (based on the assumption that GE Money will buy the Mini-BPH for just under PLN 5.5bn, i.e. ca. EUR 1.46bn). The selling price remains the big question: the market prices the Mini-BPH at EUR 1bn-EUR 1.5bn (PLN 3.75bn-PLN 5.64bn). If we assume that it sells for EUR 1bn (PLN 3.76bn, PLN 130 per one share of BPH), the per-share price of BPH would amount to PLN 1019/share. These are very conservative assumptions. We are reiterating an ACCUMULATE rating on BPH as an option to buy into Pekao at a lower price than its current market value. Support rating for BPH Fitch affirmed BPH’s support rating ('1') on Rating Watch Negative. The support rating was retained in light of the upcoming divestment by UniCredit. In April 2007, GE Money was granted an exclusive right to negotiate the acquisition of the Mini-BPH. But the spin-off has not yet been approved by bank supervision. Fitch believes that GE Money can provide sufficient support for BPH to receive a rating of ‘1’. But the negative outlook signals that, after the sale, the rating can be either downgraded or retained, but cannot be raised. Until UniCredit and GE Money reach an agreement, BPH’s support rating will remain on Rating Watch Negative. GE Money rumored to be backing out According to WSJ Polska, GE Money might back out of the negotiations to acquire the Mini-BPH due to a deadlock in the talks. Reportedly, the lack of spin-off clearance from banking supervision is not the only bone of contention. GE Money refuses to accept certain sale terms sought by UniCredit, including a two-year ban on the employees of the part of BPH to be taken over by Pekao from accepting employment with the part to be taken over by GE, and a two-year freeze preventing the new BPH from reaching out to clients of Pekao. Those are all unconfirmed rumors. Differing positions are inherent in all negotiations. The WSJ does not mention anything about the selling price, which, we would have thought to be the toughest issue. The market would respond negatively to GE Money’s withdrawal from the talks. Subsequent reactions would depend on UniCredito which could either continue its talks with another bidder, or hold a new tender. The longer this takes, the worse for the current BPH’s market value.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska44 Last Recommendation: 2007-07-05(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 1 034.2 1 228.6 18.8% 1 450.5 18.1% 1 663.8 14.7% Number of shares (m) 73.0Interest margin 3.3% 3.4% 3.5% 3.6% MC (current price) 21 348.2Revenue f/banking oper. 2 365.2 2 922.0 23.5% 3 390.7 16.0% 3 827.7 12.9% Free float 29.5%Operating profit 1 084.1 1 534.4 41.5% 1 852.1 20.7% 2 123.6 14.7%Gross profit 689.5 1 065.5 54.5% 1 515.4 42.2% 1 756.0 15.9%Net prof it 758.2 1 080.6 42.5% 1 233.2 14.1% 1 395.2 13.1%

ROE 20.7% 25.2% 25.0% 25.2% Price change: 1 month -5.6%P/E 28.2 19.8 17.3 15.3 Price change: 6 month 30.0%P/BV 5.4 4.6 4.1 3.7 Price change: 12 month 62.6%D/PS 6.0 6.0 8.9 10.1 Max (52 w eek) 315.3Dyield (%) 2.1 2.1 3.0 3.5 Min (52 w eek) 174.0

BZ WBK (Hold)Current price: PLN 292.6 Target price: PLN 284.1

170

210

250

290

330

2006-06-29 2006-10-18 2007-02-09 2007-06-05

BZ WBK WIG

BZ WBK's stock fell 6.5% since our last rating, prompting us to upgrade from Reduce to HOLD. We expect strong second-quarter earnings figures from the bank. Broad exposure to corporate clients and equity market trading will be the driving force behind bank earnings, in addition to Retail. Income will receive an additional boost from dividends from CU (PLN 60.33m) which are 13.8% higher this year than last. The bank trades on a ‘07 P/E ratio of 19.8, i.e. below the sector average of 23, but we believe that its stock already prices in the good FY2007 earnings outlook. Our FY2007 net income estimate for BZ WBK is PLN 1081m (an expected 42.5% increase on FY2006). PLN 400m on branch expansion BZ WBK has earmarked PLN 400m for sales network expansion in the next four years, including setting up of 250 branches (in addition to the 380 already in operation), development of the agency network, and increasing the number of ATMs. The expansion will focus on areas where the bank has a weaker presence, mainly in the east of Poland. It will bring about a ca. 25% increase in the employee headcount (some 2.4 thousand people). The goal of this exercise is to increase market share in loans and deposits to 10% from 6%. CEO Mateusz Morawiecki also hopes to double BZ WBK’s share in the mortgage loan market (now ca. 3%). The CEO estimates that the bank’s second-quarter net income will be 10% higher than a year earlier, when it stood at PLN 250m. We did not consider expansion on such a scale in our earnings projections for BZ WBK, and assumed that the bank would open 100 new branches in the next three years. Setting up 250 outlets entails higher costs and larger staff upsizing than we predicted. But such larger costs will potentially be offset by improved income generated through better exposure to markets not covered to date. The expansion will influence earnings for the next two years.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska12 Last Recommendation: 2007-07-05(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 1 026.4 1 173.2 14.3% 1 336.9 14.0% 1 497.0 12.0% Number of shares (m) 130.7Interest margin 3.0% 3.1% 3.2% 3.4% MC (current price) 16 071.1Revenue f/banking oper. 2 096.3 2 298.4 9.6% 2 583.6 12.4% 2 848.5 10.3% Free float 25.0%Operating profit 801.8 857.8 7.0% 1 075.4 25.4% 1 269.4 18.0%Gross profit 796.3 832.1 4.5% 820.1 -1.4% 1 007.5 22.8%Net prof it 657.1 664.3 1.1% 816.0 22.8% 964.5 18.2%

ROE 12.3% 12.1% 14.4% 16.4% Price change: 1 month -5.7%P/E 24.5 24.2 19.7 16.7 Price change: 6 month 39.8%P/BV 3.0 2.9 2.8 2.7 Price change: 12 month 80.4%D/PS 3.6 4.1 4.6 5.6 Max (52 w eek) 137.5Dyield (%) 2.9 3.3 3.7 4.6 Min (52 w eek) 65.7

Current price: PLN 123 Target price: PLN 109Handlowy (Reduce)

50

65

80

95

110

125

140

2006-06-29 2006-10-18 2007-02-09 2007-06-05

Bank Handlowy WIG

Bank Handlowy reported excellent earnings for the first quarter. We assume that the growth trend in the bank’s operating income before provisions will continue in the second quarter, driven by both the Retail, and the Corporate lines. Costs should also remain under control, although increasing bond yields might slightly hurt the FQ2 figures. The other eight banks in our coverage universe increased the share of financial income and capital gains in the total banking income to 9.5% in FQ1’07. In case of Bank Handlowy, this ratio is close to 21%. Bank Handlowy’s stock fell 5.4% since our last Monthly Report, prompting us to upgrade from Sell to REDUCE, with a reiterated advice to take profits on the stock.

ING BSK reported very good FQ1 earnings performance, showing a 32% y/y increase in operating income before provisions. Our forecast for FY2007 predicts an over-37% improvement. We believe that the rosy earnings outlook is already priced in the bank’s stock. Earnings growth will be generated mainly from the rebounding Corporate business, as well as good exposure to investment funds. In turn, Retail will lag behind competition. We are reiterating a REDUCE rating on ING BSK.

Analyst: Marta Jeżewska017 Last Recommendation: 2007-06-06

(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 936.3 1 081.8 15.5% 1 242.5 14.9% 1 393.0 12.1% Number of shares (m) 13.0Interest margin 2.1% 2.1% 2.1% 2.1% MC (current price) 13 985.8Revenue f/banking oper. 1 755.4 2 079.6 18.5% 2 366.3 13.8% 2 625.9 11.0% Free float 18.5%Operating profit 539.6 741.5 37.4% 917.7 23.8% 1 071.4 16.8%Gross profit 705.6 753.3 6.8% 774.5 2.8% 886.4 14.5%Net prof it 591.4 619.4 4.7% 708.9 14.4% 827.3 16.7%

ROE 16.2% 15.9% 16.8% 17.8% Price change: 1 month 3.8%P/E 23.7 22.6 19.7 16.9 Price change: 6 month 38.5%P/BV 3.7 3.5 3.2 2.9 Price change: 12 month 72.3%D/PS 27.5 27.9 23.8 27.2 Max (52 w eek) 1 075.0Dyield (%) 2.6 2.6 2.2 2.5 Min (52 w eek) 609.0

ING BSK (Reduce)Current price: PLN 1075 Target price: PLN 953.5

500

600

700

800

900

1000

1100

2006-06-29 2006-10-18 2007-02-09 2007-06-05

ING BSK WIG

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska011 Last Recommendation: 2007-07-05(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 780.0 878.6 12.6% 1 002.5 14.1% 1 123.0 12.0% Number of shares (m) 271.7Interest margin 3.6% 3.8% 4.0% 4.2% MC (current price) 7 606.4Revenue f/banking oper. 1 202.8 1 336.3 11.1% 1 509.0 12.9% 1 687.5 11.8% Free float 14.5%Operating profit 439.8 422.4 -4.0% 528.9 25.2% 645.3 22.0%Gross profit 321.4 460.6 43.3% 375.8 -18.4% 456.0 21.3%Net prof it 468.1 304.4 -35.0% 369.4 21.3% 452.6 22.5%

ROE 24.8% 13.9% 15.2% 16.7% Price change: 1 month 10.2%P/E 16.2 25.0 20.6 16.8 Price change: 6 month 31.1%P/BV 3.6 3.3 3.0 2.7 Price change: 12 month 67.2%D/PS 0.2 0.4 0.4 0.6 Max (52 w eek) 28.0Dyield (%) 0.8 1.3 1.4 2.2 Min (52 w eek) 15.0

Kredyt Bank (Under Review)Current price: PLN 28 Target price: -

Sales figures suggest that Kredyt Bank had a successful second quarter, rendering our FY2007 net income estimate overly conservative. Intense efforts to increase sales, paired with a tightening partnership with other KBC companies (Warta, KBC TFI), make for a promising bottom line outlook. ING BSK continues to expand its product offering, especially on the Retail front, and does so while keeping cost growth at a pace close to the inflation rate. Pre-tax income could receive an additional boost from NPL provision reversals as the bank steps up its debt recovery efforts. Our long-term forecasts assume that ING BSK's cost of risk will be on a par with other banks’, or even lower in the next few quarters. As the second-quarter earnings season approaches, we expect a revision in the bank’s full-year earnings guidance. Our investment rating on Kredyt Bank is under revision. FQ2 mortgage loan sales top PLN 1 billion ING BSK sold mortgage loans worth PLN 1 billion in the second quarter. In FQ1’07, the bank extended 3.9 thousand home loans with a total value of PLN 532m, marking a whopping 82.7% increase on FQ1’06. A sales preview in April pegged the full-year sales at over PLN 2.5bn. A KBC manager said that the objective of maintaining a 7%-8% market share in new sales might not be achieved this year. Hence, the market could not have expected such a huge surge in sales. In our valuation model, we assumed FY2007 mortgage loan sales at 2.5bn for Kredyt Bank, which, assuming a market total of PLN 57bn, would make for a 4.4% share in new sales. We might have to revise this view after the second-quarter earnings release. Sales of PLN 1 billion represent an 87% increase on FQ2 2006. Historically, FQ1’06 sales were PLN 291m, up to PLN 535m in FQ2’06, compared to PLN 532m in FQ1’07 and PLN 1 billion in FQ2’07. All this paints a very bright second-quarter earnings picture. Tapping into household savings Belgium’s KBC is committed to increasing market share to ca. 10%, and those plans include its insurance subsidiary Warta whose market share is currently a little over 3%. One way to fulfill this goal is for Warta, Kredyt Bank and the investment fund company KBC TFI to launch a joint offer. Two such campaigns are in the making. KBC TFI is also working to up its market share. According to VP Piotr Habiera, the AUM of the KBC TFI investment funds will reach PLN 5bn in June. Mr. Habiera also said that, like in the first quarter, the Kredyt Bank group grew faster than the market in the second quarter in household savings. In our view, this indicates an acceleration in product sales growth, which will be reflected in the bank’s volumes. This is excellent news, especially when coupled together with the fact that the bank also outpaces the market in lending growth. Supervisory Board member delegated to Management Board Mr. Andrzej Witkowski, Chairman of Kredyt Bank’s Supervisory Board, was temporarily delegated to the Management Board. We think that this might be the beginning of the management reshuffling that we have been waiting for since Mr. Konrad Kozik and Mr. Bohdan Mierzwiński left the bank.

13

15

17

19

21

23

25

27

29

2006-06-29 2006-10-18 2007-02-09 2007-06-05

Kredyt Bank WIG

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska16 Last Recommendation: 2007-06-06(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 650.5 762.3 17.2% 921.8 20.9% 1 107.8 20.2% Number of shares (m) 849.2Interest margin 2.8% 2.8% 2.8% 2.9% MC (current price) 11 803.6Revenue f/banking oper. 1 253.0 1 535.1 22.5% 1 866.1 21.6% 2 205.3 18.2% Free float 34.5%Operating profit 409.4 565.2 38.1% 767.1 35.7% 1 005.4 31.1%Gross profit 709.7 370.7 -47.8% 473.1 27.6% 639.6 35.2%Net prof it 300.8 383.2 27.4% 518.0 35.2% 684.7 32.2%

ROE 13.1% 16.4% 19.8% 22.8% Price change: 1 month 3.0%P/E 39.2 30.8 22.8 17.2 Price change: 6 month 69.5%P/BV 5.3 4.8 4.2 3.7 Price change: 12 month 152.7%D/PS 0.5 0.2 0.2 0.3 Max (52 w eek) 13.9Dyield (%) 3.9 1.2 1.6 2.1 Min (52 w eek) 5.3

Millennium (Sell)Current price: PLN 13.9 Target price: PLN 10.5

3

6

9

12

15

2006-06-29 2006-10-18 2007-02-09 2007-06-05

Millennium WIG

Millennium is going to kick off the bank industry’s second-quarter earnings season on July 23rd. We expect strong performance underpinned by booming fundamentals. Business income should be good, while operating income will be impacted by expansion costs (although the bank has to date surprised on the upside on the cost front) and provision charge-offs. Less intense debt recovery efforts, paired with a strong lending business (requiring recognition of IBNR reserves), could hoist the charge-offs higher. Millennium trades on a ’07 P/E of 29.8, displaying a 31% premium to the sector average. Even assuming the highest possible net income CAGR for the next three years (FY09/06 CAGR=31.5%), the ’09 P/E estimate of 16.7 is still higher than the peer average (4%). We advise investors to take profits on Millennium shares, and reiterate a SELL rating on the stock. New strategy Millennium’s old strategy pegged the FY2008 ROE and C/I ratio at 15% and 65% max respectively. The bank’s estimates were made taking into account the network expansion and rebranding plans revealed early last year (160 new branches including 40 to be redesigned). Amidst a booming market environment, by fully leveraging the industry’s most attractive product offering and keeping a tight rein on expansion costs, Millennium succeeded in achieving its financial targets one year ahead of the plan. On June 1st, the bank revealed a new strategy developed as part and parcel of the strategy adopted across the BCP group. ROE and C/I ratio targets were revised to 20% and 55% max respectively, to be achieved in FY2009. Millennium also raised its sales targets. Retail will work to acquire approximately 400,000 new clients (from 800,000 now to 1.2 million, a 50% increase). As regards the key product, mortgage loans, Millennium aims to achieve a 12% share in the total portfolio of these loans, and keep its Top-3 position (in all sales, not only new sales as previously). To succeed, the bank will have to keep growing faster than the market for the next three years (its current share in the mortgage loan portfolio is 10.5%). In credit cards, the target market share is 8%, and cash loan sales are set at PLN 2 billion in FY2009and PLN 1 billion in FY2007, with an assumed intermediate goal of PLN 1.5bn in FY2008 (this is our assumption). Growth in the Retail segment is also partly generated by investment funds, where Millennium hopes to achieve a 6% market share and move into the top five in terms of AUM - goals that also require above-average growth in the next three years (market share currently stands at 4%). In the Corporate segment, Millennium basically left its old targets intact: to acquire 1500 new SME clients annually, increase income by 20% a year, and gain a 7% piece of the market pie. Income growth is to be driven by new accounts and lease financing, as well as a broader product offering, including factoring services and cash management products.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska016 Last Recommendation: 2007-06-06(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 2 377.0 2 552.4 7.4% 2 824.9 10.7% 3 094.0 9.5% Number of shares (m) 167.0Interest margin 3.7% 3.6% 3.7% 3.8% MC (current price) 44 591.1Revenue f/banking oper. 4 656.4 5 047.6 8.4% 5 563.2 10.2% 6 117.2 10.0% Free float 43.1%Operating profit 2 335.2 2 656.8 13.8% 3 087.6 16.2% 3 545.7 14.8%Gross profit 1 873.6 2 203.8 17.6% 2 572.8 16.7% 2 991.9 16.3%Net prof it 1 787.5 2 081.7 16.5% 2 421.2 16.3% 2 775.0 14.6%

ROE 20.7% 22.7% 24.7% 26.4% Price change: 1 month -1.3%P/E 24.9 21.4 18.4 16.1 Price change: 6 month 16.1%P/BV 5.0 4.7 4.4 4.1 Price change: 12 month 41.6%D/PS 7.4 9.0 10.5 12.2 Max (52 w eek) 271.7Dyield (%) 2.8 3.4 3.9 4.6 Min (52 w eek) 182.5

Current price: PLN 267 Target price: PLN 269Pekao (Hold)

We are still waiting for an official OK to the BPH spin-off and the BPH/Pekao merger. Bank supervision is taking its time, raising concerns over possible delays in both the merger itself, and the synergies it is expected to bring to Pekao. But, in our opinion, the impact of such delays will not be terribly harmful. Our target per-share price on Pekao’s stock (PLN 269) was calculated based on its valuation “as is,” i.e. without taking into account the merger or the placement of stock consideration to BPH’s shareholders (our usual approach) to which we added the expected cost and revenue synergies. Without those synergies, the target would be closer to PLN 256 per share. Going back to the delays, they are obviously not good for the process, but they do not affect the synergies achievable on the merger. In the near term, Pekao’s stock will rally on strong FQ2 earnings performance driven by cash inflows to investment funds, good exposure to Retail, and accelerating corporate lending. We are reiterating a HOLD rating on Pekao. Pekao files prospectus Pekao filed the prospectus with the Polish Financial Authority (KNF) as scheduled, but this punctuality will do nothing to speed up the merger process as the bank continues to wait for official clearance to conduct the BPH spin-off and incorporate the remaining portion. After a recent change in the position of the President of the General Inspectorate for Bank Supervision (GINB), Pekao will probably be asked to submit more documents, and the new GINB Head Alfred Janc will have to take time to acquaint himself with the thousands of pages of merger documentation. Added to this are UniCredit’s negotiations with GE Money regarding the acquisition of the Mini-BPH. Because GE Money will have to hold a tender offer for the Mini-BPH’s outstanding shares, a solution is needed to ensure that it does not pay more for such shares than it is going to pay for the 71.3% stake acquired from UniCredit. Pekao and BPH are ready to combine their operations. In our view, Pekao’s current market value does not factor in the merger yet. GINB analyses not ready yet The analyses are needed to review the BPH spin-off clearance request filed in January. A delay is a given at this point, but it will not affect our positive outlook on Pekao, which reports consistently strong financial performance. The post-merger savings potential is also intact, except that they might be achieved later than originally hoped. Unfortunately, the delays will have some implications for BPH. BPH’s shareholders stand to benefit from two sources of cash flows: Pekao shares and the selling price of the Mini-BPH, and it looks like they will have to wait longer to get these assets. What is more, BPH could face erosion of business as it continues to wait for the spin-off. GA called after supervisory board resignations Pekao called a general meeting of shareholders for July 25th to appoint new supervisory board members and amend the bylaws. The meeting is necessitated by two resignations: Andrea Moneta and Jerzy Starak. Andrea Moneta was formerly in charge of UniCredit’s Polish operations, but his stepping down is not due to any problems in the local market. His replacement is Mr. Federico Ghizzoni, already appointed as member of BPH’s supervisory board. We do not know the reasons behind Mr. Starak’s resignation. Overall, these developments should not affect Pekao’s stock performance. Merger in the Ukraine UniCredit Ukraina and HVB Ukraina signed an agreement to merge by the end of the year. This should come as no surprise to investors given the activity leading up to this deal. Good news for Pekao as owner of the new company.

160

200

240

280

320

2006-06-29 2006-10-18 2007-02-09 2007-06-05

Pekao WIG

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Marta Jeżewska016 Last Recommendation: 2007-05-31

(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Net interest income 3 808.7 4 444.8 16.7% 5 143.3 15.7% 5 986.8 16.4% Number of shares (m) 1 000.0Interest margin 3.9% 4.2% 4.4% 4.7% MC (current price) 55 900.0Revenue f/banking oper. 6 038.9 7 015.9 16.2% 7 990.5 13.9% 9 098.0 13.9% Free float 43.1%Operating profit 2 705.8 3 571.3 32.0% 4 273.7 19.7% 5 159.9 20.7%Gross profit 2 167.0 2 701.5 24.7% 3 316.1 22.8% 3 868.6 16.7%Net prof it 2 149.1 2 610.1 21.5% 3 042.5 16.6% 3 674.9 20.8%

ROE 22.9% 24.0% 24.4% 26.0% Price change: 1 month 1.5%P/E 26.0 21.4 18.4 15.2 Price change: 6 month 21.5%P/BV 5.5 4.8 4.2 3.7 Price change: 12 month 50.7%D/PS 0.8 1.0 1.3 1.5 Max (52 w eek) 56.0Dyield (%) 1.4 1.8 2.3 2.7 Min (52 w eek) 35.8

PKO BP (Hold)Current price: PLN 55.9 Target price: PLN 54.4

30

35

40

45

50

55

60

65

2006-06-29 2006-10-18 2007-02-09 2007-06-05

PKO BP WIG

We welcomed the two management board appointments and the nomination of Rafał Juszczak to the position of PKO BP’s CEO. A complete management board is a guarantee of fulfillment of the bank’s new six-year strategy. We expect strong FQ2 sales figures from PKO BP even despite the management reshuffling, driven mainly by mortgage loans and SME financing facilities. We would like to see more robust growth in retail lending and corporate loans, and, while this is entirely possible in case of the former, an acceleration in the latter will not happen until the bank comes up with a better financing offer for businesses. The PKO BP investment funds, which are gradually picking up momentum, will no doubt have a handsome share in the FQ2 earnings. Strong sales will drive interest- and fee income, but operating income could be affected by higher bond yields bringing the value of the debt portfolio to the negative territory. We are reiterating a HOLD rating on PKO BP. Rafał Juszczak named CEO Rafał Juszczak, acting CEO since March and Management Board member since July 1st, 2006, was appointed as PKO BP’s new CEO. The supervisory board also appointed four VPs: Ms. Aldona Michalak (put in charge of quality assurance as of July1st), Mr. Mariusz Klimczak (in charge of corporate banking as of July 15th), Mr. Adam Skowroński (in charge of finance and accounting as of July 23rd), and Ms. Berenika Duda–Uryn (HR management as of September 10th). Marek Głuchowski said that there is still an IT management vacancy left in the board. The CEO appointment is in line with expectations. We welcome the fact that Mr. Juszczak was involved in developing PKO BP’s new strategy, and was the one to present it to shareholders We are also glad the four management board vacancies are finally filled. Three of the new VPs (except for Ms. Berenika Duda–Uryn) have a history with PKO BP. Their nominations are consistent with their expertise. Now that the management board is complete, the 2007–2012 strategic targets have a better chance of being fulfilled.Eight out of the nine positions prescribed in the bank’s bylaws are filled, and there is still one spot waiting for someone to head IT. FQ2 better than a year ago CEO Rafał Juszczak said that the bank’s second-quarter earnings results will be better than a year ago, and will have followed the same trends as observed in the first quarter. We agree. Net income in FQ2 2006 was PLN 471m, and, in FQ1 2007, it was already PLN 672m. The FQ1’07 net income chalked up a 40% increase on FQ1’06, among others thanks to (aside from a fast-paced business) low costs and debt recovery efforts. Second-quarter growth will be impacted by cost of risk, higher expenses (upped recently), and higher bond yields. While we are sure that PKO BP’s FQ2’07 earnings results will be better than a year ago, we have doubts whether they will display much quarter-on-quarter improvement. Strategy implementation PKO BP appointed 16 dedicated teams to manage 28 new initiatives, including three teams dedicated to the corporate segment, where the bank admits to being behind competition. PKO BO is recruiting experts to implement new products like factoring, cash management, e-banking, and a special hotline for business clients. The bank is also preparing to roll out the ZSI system throughout its entire branch network. Only four are working on the ZSI so far. The rollout will start in August, and end in 2008. The ZSI will facilitate the establishment of special accounting centers that will help generate savings and downsizing. The bank plans to reduce staff by 1500 people a year, including through voluntary leave schemes. We welcome the fact that PKO BP is finally setting about to bringing the strategy into effect. We believe that it is fully capable of achieving most, if not all of the objectives it set for itself. The layoff plans were disclosed a long time ago.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Key strategic goals The three main targets of the new strategy as pinpointed by the new CEO are human resources management, roll-out of the central computer system (ZSI), and an acceleration in sales. The first goal will involve staff reductions (depending on the ZSI rollout) as well as development of a new incentive system. The bank reiterated its plan to reduce the headcount by 1500 people a year through 2008, but adds that it will probably launch a voluntary leave program next year. After 2008, the scale of the layoffs will increase. As for sales, more emphasis will be placed on the Corporate business. CEO committed to develop the Corporate business PKO BP intends to assume lead of the market among others by targeting government-owned companies. The corporate business is very important for the new CEO. While the bank has an established presence in Retail, there is still much to be done to attract business clients. PKO BP’s Corporate business line is the source of a significant growth potential. While Retail no longer has much capacity to increase market share, there is a large piece of the corporate pie to be had. Thanks to the majority shareholder and large geographic coverage, PKO BP has excellent exposure both to large businesses, and SMEs. The SME portfolio has displayed healthy growth for some time, but the offer directed to the more demanding prospects has to be significantly revamped. Loan agreement PKO BP signed a ten-year PLN 250m loan agreement with “Operator Logistyczny Paliw Płynnych.” This is proof of the bank’s capacity to take advantage of the momentum in the corporate segment, with special focus on government-owned companies. ZSI rollout The ZSI rollout is not expected to affect costs considerably in the next few quarters as the expenses it entails will be offset by the savings generated on centralized processes. Robert Działak says that if the ZSI is implemented at all PKO BP branches by the end of 2008, it will be a big success. The main cost impact will hit the bank in 2009-2010, but it will go hand in hand with centralization savings. Again, the bank did not provide us with any cost estimates. We predict that amortization charges will soar in the years ahead. The double-digit income growth target in the new strategy was set taking into account the ZSI costs. Our net income forecasts are in line with the bank’s guidance. Moving into insurance An insurance business can help PKO BP maintain its leading market position. The bank does not intend to wait until it is allowed to join forces with PZU to form a banking and insurance organization, and plans to start its own insurance company. However, Rafał Juszczak is all in favor of the idea to form a national finance group that would include PKO BP, Bank Pocztowy, BGK, and PZU. We have big reservations as to PKO BP’s insurance plans. To create value adequate to the bank’s, a large organization is needed that, however, will be hard to develop in a fiercely competitive market with such established players as PZU, especially considering that the government would then become the owner of two competing firms. Capital injection plans Marek Głuchowski, Chairman of PKO BP’s supervisory board, said that the bank was considering making capital injections of around PLN 15bn in a five-year horizon, and pondering moving into the insurance business. Additional capital is not needed yet this year. This is one of the 28 initiatives set out in the new strategy. One solution would be a new stock offering. Mr. Głuchowski also reiterated that the bank wants to expand outside of Poland. In our view, such huge capital proliferation plans (PKO BP’s equity at FQ1’07 stood at PLN 10.8bn) can be treated as a harbinger of an equally considerable acquisition. The bank is keeping a tight lid on such plans for now. Capital needs There is no need for a capital injection yet this year, but such a need could arise next year to support the bank’s robust lending business (according to the CEO, monthly mortgage sales currently stand at PLN 1.5bn, and annual sales are expected to exceed PLN 15bn) and comply with the CAR requirements set by Basel II. PKO BP will take out a CHF mortgage loan. Next year’s capital needs could be satisfied through a stock offering. Naturally, the government has to keep an over-50% stake in the bank after such an offering. PKO BP seeks controlling stake in Bank Pocztowy PKO BP is negotiating the terms of Bank Pocztowy takeover with the Polish Post Office. PKO BP’s current stake is 25% plus one share. The Polish Post owns the rest. The negotiations are for a 25% stake minimum to give PKO BP control. By selling its shareholdings, the Polish Post would raise the capital needed to carry out a restructuring. Marek Głuchowski that this might be

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

achieved through a small stock placement to Bank Pocztowy’s employees. Bank Pocztowy has PLN 2bn assets and PLN 165m equity, while PKO BP's equity is PLN 9bn, and assets are over PLN 100bn. The talks are definitely not about assets but, rather, post offices. The two banks already cooperate in selling products and services and PKO BP has access to PO outlets. By taking over control, PKO BP would in a way make it easier for itself to carry out its strategic plans, which investors should welcome as good news. Aside from owning Bank Pocztowy, PKO BP is also thinking about working together with cooperative banks (it is unclear on what terms). In our view, acquisition of Bank Pocztowy, although a smart move, would not have much impact on PKO BP’s consolidated accounts. Also, the bank’s new strategy factors in the partnership with the Polish post, with financial targets partially conditioned on this cooperation. The potential takeover will not influence our financial projections for PKO BP. Bank Pocztowy sets up new PO stands Bank Pocztowy has set up 345 financial service points at post offices to date. This number will be 1.2 thousand by the end of the year, and 3.3 thousand by 2009. Most of the stands use payment terminals operated by PKO BP’s subsidiary e-Service. Bank Pocztowy’s growth agenda is to develop the sales network through PO outlets without opening new independent branches in addition to the 60 already in place. The bank also launched electronic banking services on June 1st, and plans to develop the functionality of the “Pocztowy 24” e-banking system. The remote banking service was developed jointly with Inteligo Financial Services S.A., also member of the PKO BP group. Bank Pocztowy currently manages over 170 thousand accounts, but hopes to attract more clients through the partnership with the Polish Post Office. PKO BP subsidiaries are joining forces to grow Bank Pocztowy, which, for now, plays an immaterial role from PKO BP’s earnings standpoint. PKO BP set to conquer new markets In addition to opening branch offices in the UK and expanding through Kredobank in the Ukraine, PKO BP also wants to establish a presence in other markets including Russia, Romania, and Belarus by acquiring banks there. The goal is to achieve a significant position in each of these countries, says CEO Rafał Juszczak. PKO BP plans to make a $35m capital injection in its Ukrainian subsidiary, and increase market share from 2% to 10%. We are skeptical about the acquisition plans for the Russian and Belarusian markets. Bulgaria is a possibility, but we have heard many times before about PKO BP’s international expansion plans (the bank even made bids for a Romanian and a Serbian bank) which, however, never actually materialized. We believe that, by allocating resources to international markets, the bank will lose focus on the growth prospects that present themselves locally. The international agenda is PKO BP’s response to the Pekao/BH merger and loss of leading positions in many markets to the enlarged Pekao. Loan sales going strong PKO BP sold PLN 2.89bn-worth of mortgage loans and PLN 1bn in consumer loans in April and May, and hopes to generate over PLN 5 billion from consumer loans by the end of the year. PLN 1.445bn in monthly home loan sales is an excellent result and one that is in line with the bank’s agenda to increase sales in FY2007 relative to FY2006 to at least PLN 1.2bn a month. In turn, FQ1 consumer loan sales disappointed investors: retail loans excluding home loans and HNWs rose a mere 9% y/y and fell 4% q/q despite efforts to accelerate growth. The growth rate including HNW clients amounted to 20% - also a less-than-stellar result, surprising for a bank with a broad exposure to retail clients like PKO BP’s. We hope that sales pick up going forward. Retail loans up over 10% PKO BP hopes to grow its retail loan portfolio by over 10% in FY2007. YTD, the bank has sold PLN 2.2bn in cash loans, and PLN 6.5bn in mortgage loans. The target for cash loans is PLN 5bn-plus. PKO BP is going to launch a special offer for seniors in the second half of the year. The number of credit cards in circulation is expected to exceed the 1 million mark. After FQ1’07, that number stood at 943,000, and increased to 960,000 by the end of May. For FY2007, we expect retail loans to increase 25%. The bank’s targets are in line with our forecasts. PKO Inwestycje partners with Polish Rails A year ago, the Polish Rails (PKP) and PKO Inwestycje (subsidiary of PKO BP) signed a Letter of Intent regarding building projects. Now, the partners are preparing a project in Warsaw. PKP will contribute 24 ha of land, and the bank will provide the cash and know–how. The work will start toward the end of next year, after the site is cleared and all necessary permits are obtained. Initially, construction work will take place on 6 hectares, but we have no clue what exactly the two firms will be building there (the architectural plans are yet to be developed). CEO Rafał hopes that PKO BP and PKP will tighten their business relationship. The national rail operator owns a lot of land all over Poland, and is looking for investors. PKO Inwestycje’s real-estate development business leaves a mark on PKO BP’s consolidated income and costs. The projects referred to above will last for the next few years, spanning beyond our forecast horizon. We think that PKO Inwestycje will be contributing to the group’s income over the next few years.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Inteligo moves to Ukraine, launches MVNO business Ukraine’s Kredobank will soon launch a mobile telephony and electronic banking services. Inteligo will unveil its offering late this year. The MVNO services will be targeted mainly to PKO BP and Kredobank clients, and the plan is to acquire more than 50 thousand users. The bank is about to finalize talks with Polkomtel. Inteligo’s electronic banking services have 2.1 million users, of which 0.6 millions are its own clients, and the rest are PKO BP clients. By the end of the year, the number of accounts is expected to increase to 2 million. The bank has been reported to be negotiating with an operator for some time. Mobile telephony is an added-value service rather than a legitimate attempt at garnering market share. MVNO is not going to have much impact on Polish operations, but it might be different in the Ukraine. We welcome the plans to develop Kredobank. The plans to launch electronic banking in the Ukraine date back to PKO BP's former VP in charge of Retail, Jacek Obłękowski.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Gas & Oil, Chemicals Azeri oil enough to feed Odessa-Płock pipeline? The Azerbaijani oil company Socar made an assertion that its crude oil reserves amount to 1.35 billion tons, meaning that it can increase output and open new export channels. This means that the Odessa-Brody-Płock pipeline project could be pulled off even without involvement by Kazakhstan (Socar extracts ca. 8.8 million tons of oil a year), although the latter will not leave Azerbaijan’s declaration without a response. This raises questions about investments in Azeri deposit exploration and purchase guarantees that will be expected of Polish refineries after the pipeline is up and running. It is no secret that Caucasian oil producers want to gain interests in the refining sector, and will probably propose to purchase stakes in Polish refineries. Russia to launch Rebco futures trading During the Saint Petersburg economic forum, an agreement was signed to establish a commodity exchange in the city that will trade in Rebco oil futures (scheduled for mid-2008) with an aim of tightening the Urals-Brent differential. In our opinion, this exchange will not manage to change the spread between the high-sulfur Russian crude and Brent. All previous attempts at narrowing it were a fiasco as the only way to do this is to enhance Urals’s export quality (by not mixing it with lower-grade crude types). But one reason that makes the Saint Petersburg exchange a viable idea is to increase Primorsk’s transshipment capacity, translating into a more significant role of spot contracts on Russian oil deliveries that will probably be indexed to the futures. OMV’s hostile move on MOL After increasing it shareholding interests from 10% to 18.6%, Austria’s energy giant OMV is determined to take over its Hungarian counterpart, MOL. But MOL’s management have no interest in a closer relationship with OMV, and do not intend to help the Austrians, and neither does the Hungarian government which officially announced that it is going to do everything in its power to stop the acquisition. But we cannot rule out that OMV will hold a tender offer for MOL’s shares and get its hands on a majority stake against MOL’s will, especially if we consider the press reports that financing is already in place to make such a move. US gasoline inventories on a downturn The US Department of Energy reported that the country’s gasoline inventories fell by 0.75 million barrels in the week ended June 22nd, contrary to the market’s expectations of a 1mmbbl increase. Although refiners increased their capacity utilization rates by 1.8 ppts, output remained flat (on the same level as in the period when the CUR was decreasing) as refineries, troubled by plant failures, struggled to keep it from falling by using third-party semi-finished products. Now that the plants are operational again, refiners reduced purchases of these products to not overload the limited capacity. Flat production, persistently high demand, and a decline in imports from 1.3mmbbl to 1.1mmbbl were the determining factors of the US gasoline market's performance last week. We still expect gasoline prices to accelerate in July and August, and drive refinery margins.

BRE Bank Securities

5 July 2007

Monthly Report BRE Bank Securities

Analyst: Kamil KliszczLast Recommendation: 2007-05-09

(PLN m) 2006 2007F change 2008F change 2009F change Basic data (PLN m)Revenues 12 812.7 11 932.5 -6.9% 11 814.3 -1.0% 14 547.6 23.1% Number of shares (m) 113.7EBITDA 1 101.7 1 027.5 -6.7% 985.1 -4.1% 1 344.6 36.5% MC (current price) 6 145.5EBITDA margin 8.6% 8.6% 8.3% 9.2% EV (current price) 6 172.6EBIT 804.3 650.9 -19.1% 474.4 -27.1% 707.9 49.2% Free float 41.2%Net profit 666.1 491.6 -26.2% 326.0 -33.7% 483.5 48.3%