brazilian sugarcane industry association uniÃo … · 1 joel velasco chief representative –...

TRANSCRIPT

1

Joel Velasco

Chief Representative – North America [email protected] www.unica.com.br

BRAZILIAN SUGARCANE INDUSTRY ASSOCIATION UNIÃO DA INDÚSTRIA DE CANA-DE-AÇÚCAR

2

OUTLINE

①! Introduction •! Brazil’s diversified sugarcane industry

②! Building Blocks of Energy Security •! Feedstock + Infrastructure + Price

③! Sugarcane & Climate Change •! Replacing fossils fuels with something better

④! Sugarcane & Sustainability •! Improving on sustainable practices

⑤! Global Biofuels Market •! Still a small, highly protected market

⑥! Sugarcane in the United States •! Meeting mandates sustainably

3 3

①!

4

ABOUT UNICA

•! UNICA is the leading sugarcane industry association, representing +100 producers and mills in Brazil

•! Responsible for 60% of all ethanol and sugar production in Brazil

•! Emerging as a leader in the generation of bioelectricity already meeting 3% (and soon 10%) of Brazil’s electricity demand

•! International presence, now in Washington & Brussels, to engage in constructive dialogue

5 Source: Ministry of Mines and Energy BEN (2008).

Other renewables 3.0%

Petroleum 36.7%

Natural Gas 9.6%

Coal 6.0% Uranium

1.6%

Hydroelectricity 14.7%

Other biomass 12.4%

SUGARCANE IS #1 RENEWABLE ENERGY SOURCE

6

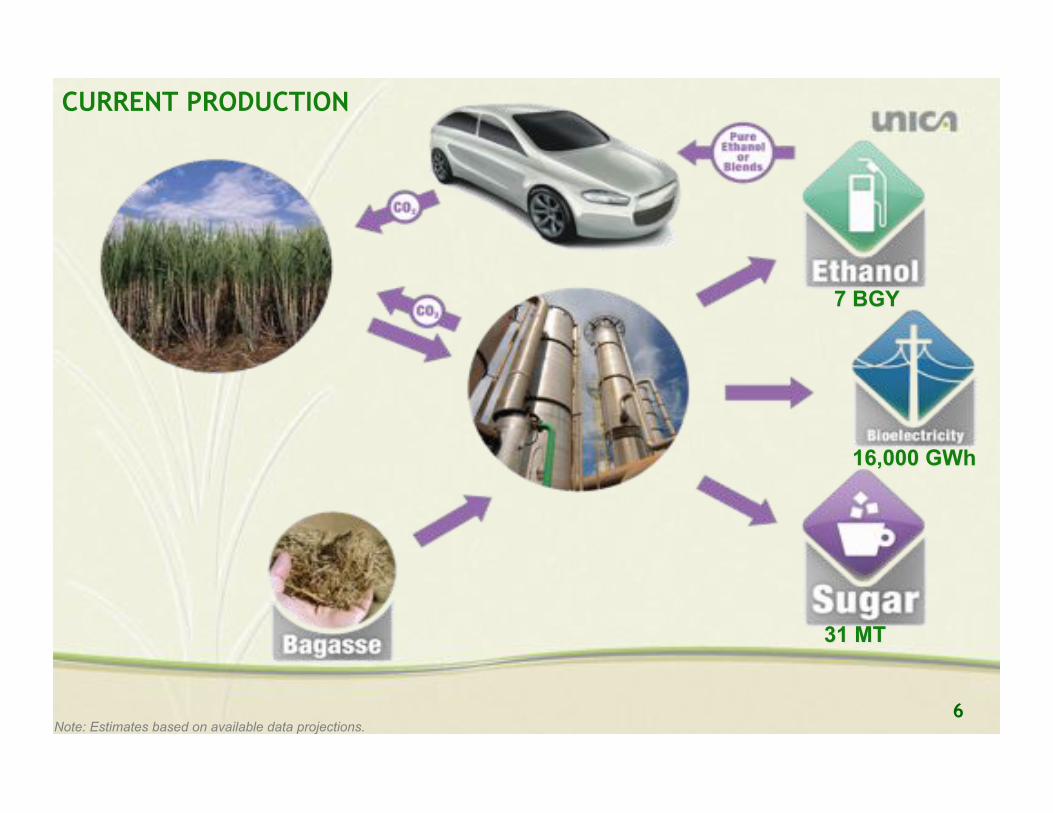

CURRENT PRODUCTION

Note: Estimates based on available data projections.

7

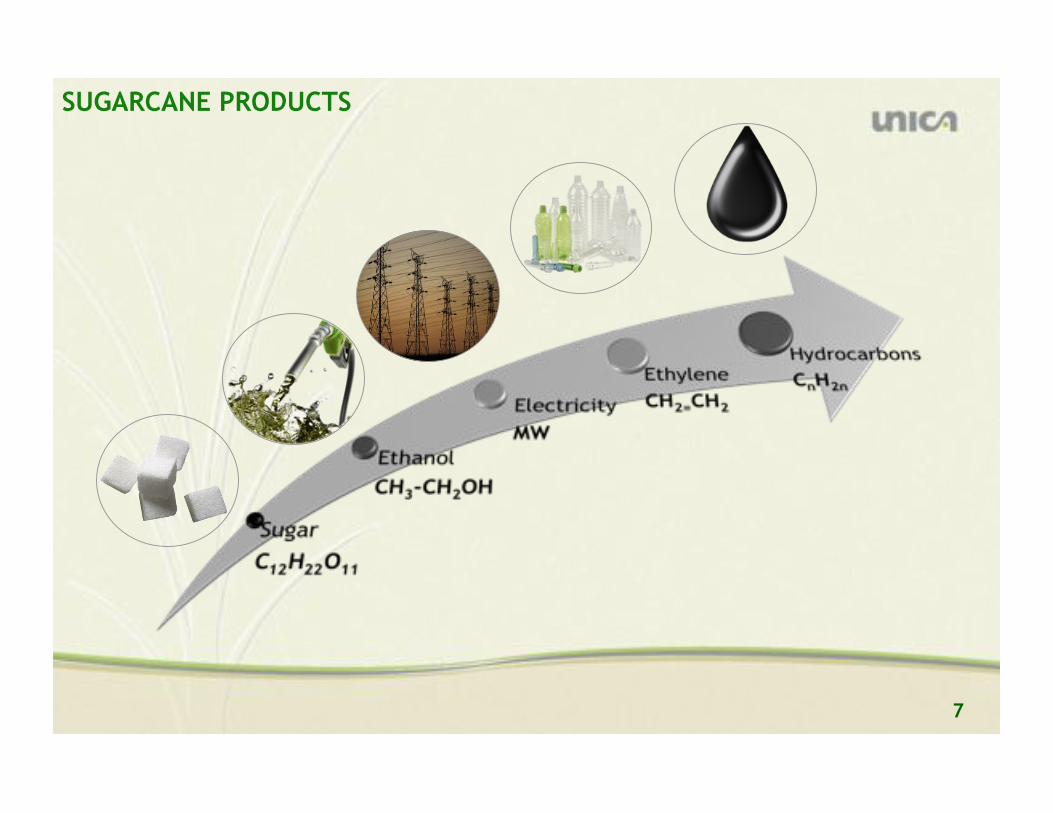

SUGARCANE PRODUCTS

8

BRAZILIAN PRODUCTION & ESTIMATES

Note: e = estimated data due to Northeast harvest; potential generation of surplus electricity has been calculated based on the utilization of 75% of the available bagasse and 50% of the available straw, and considering the sugarcane production during most recent harvest, Sources UNICA.

2008/09e 2015/16 2020/21

Sugarcane production (million tons) 569 829 1,038

Sugar (million tons) 31 41.3 45.0

Domestic Market and Stocks 10.2 11.4 12.1

Export 20.8 29.9 32.9

Ethanol (billion gallons) 7.2 12.4 17.2

Domestic Market and Stocks 6 9.2 13.1

Export 1.2 3.2 4.1

Bioelectricity (MW average) 1,800 8,158 13,158

Share of electricity demand (%) 3% 11% 14%

9 9

②!

10

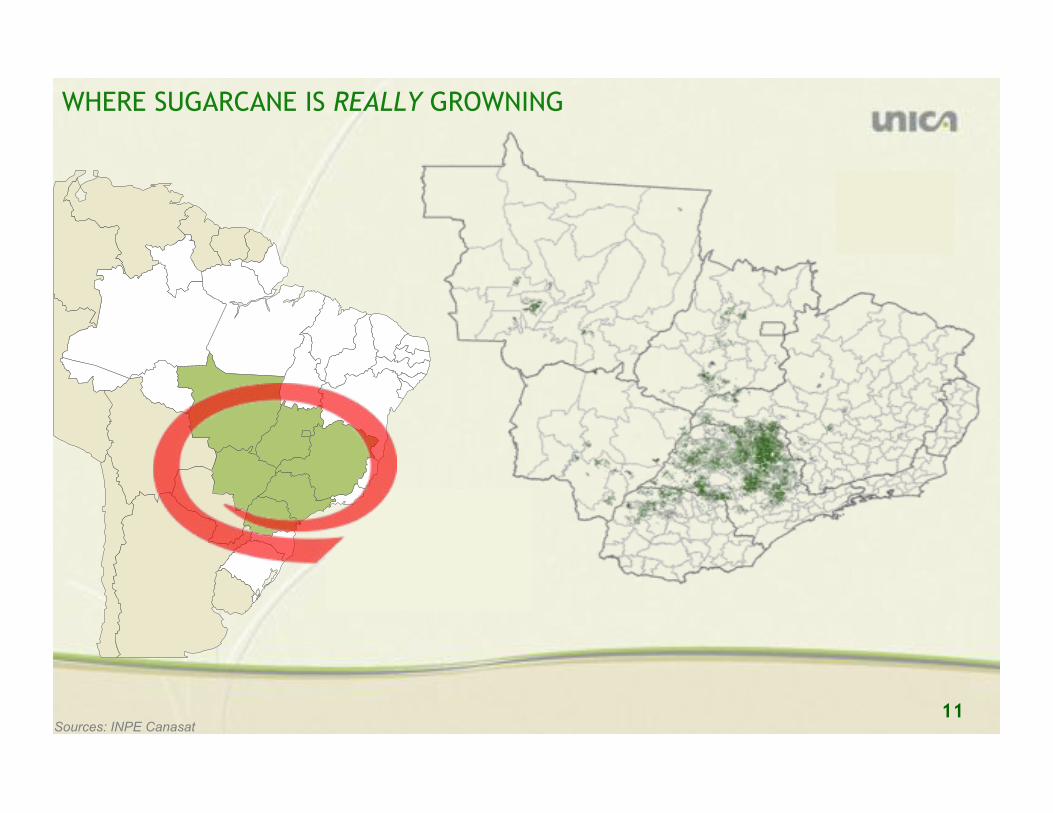

FEEDSTOCK: WHERE SUGARCANE IS GROWN

Sources: NIPE-Unicamp, IBGE and CTC

South-Central region

represents about 90% of sugarcane harvest

11 Sources: INPE Canasat

WHERE SUGARCANE IS REALLY GROWNING

12

INFRASTRUCTURE: FLEX FUEL CARS & DISTRIBUITON

13

0

1

2

3

4

5

6

7

8

0

200

400

600

800

1,000

1,200

1,400

Mill

ion

Ve

hic

les

Mill

ion

Lite

rs

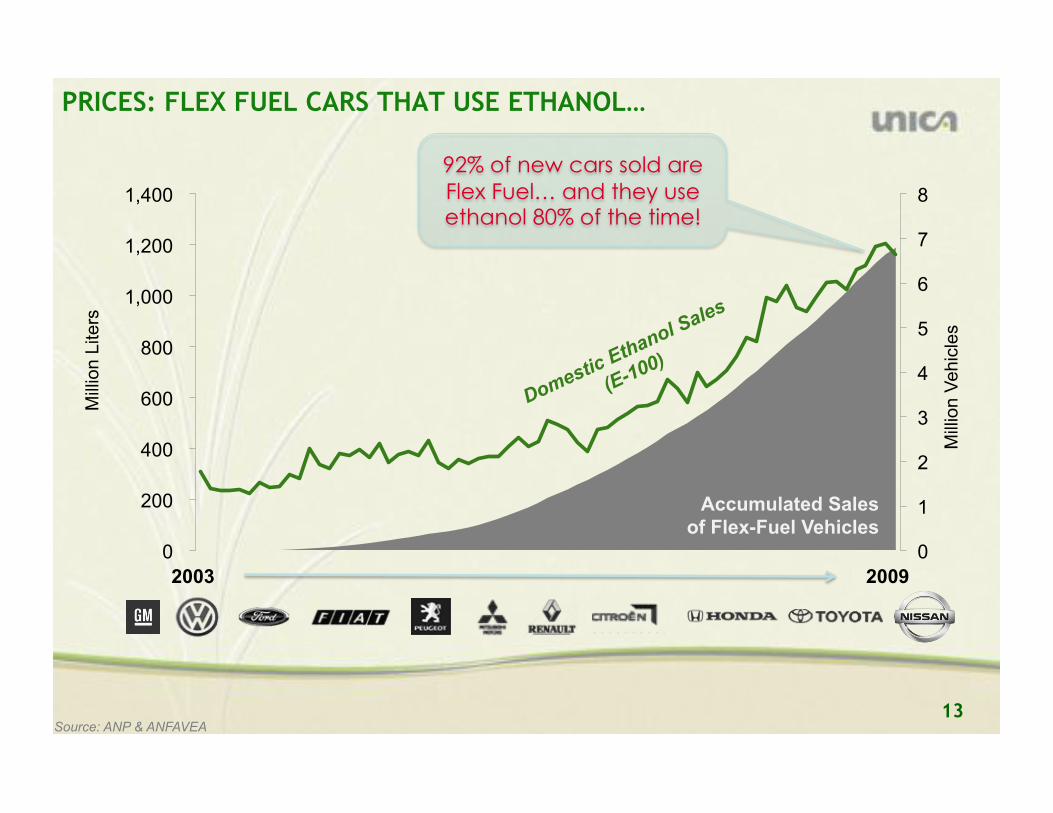

PRICES: FLEX FUEL CARS THAT USE ETHANOL…

Accumulated Sales of Flex-Fuel Vehicles

Source: ANP & ANFAVEA

92% of new cars sold are

Flex Fuel… and they use ethanol 80% of the time!

2009 2003

14

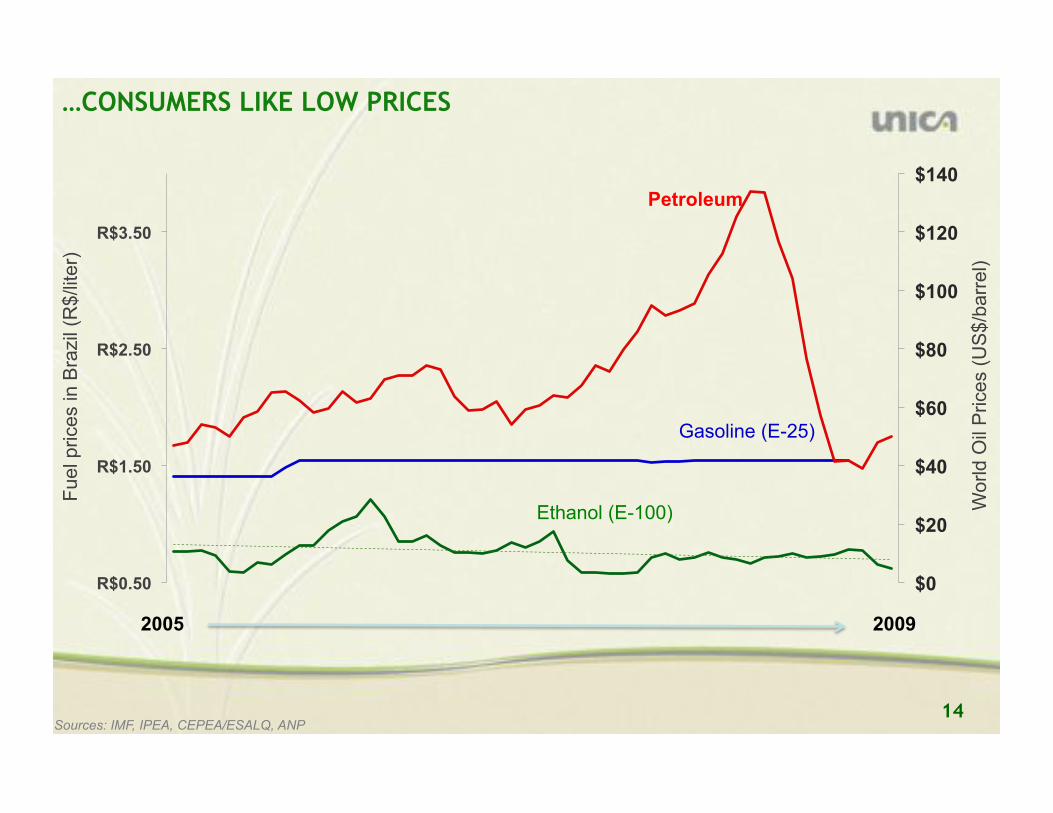

$0

$20

$40

$60

$80

$100

$120

$140

R$0.50

R$1.50

R$2.50

R$3.50

Petroleum

Gasoline (E-25)

Ethanol (E-100)

Sources: IMF, IPEA, CEPEA/ESALQ, ANP

2005 2009

…CONSUMERS LIKE LOW PRICES

World O

il P

rices (

US

$/b

arr

el)

Fuel prices in B

razil

(R$/liter)

15

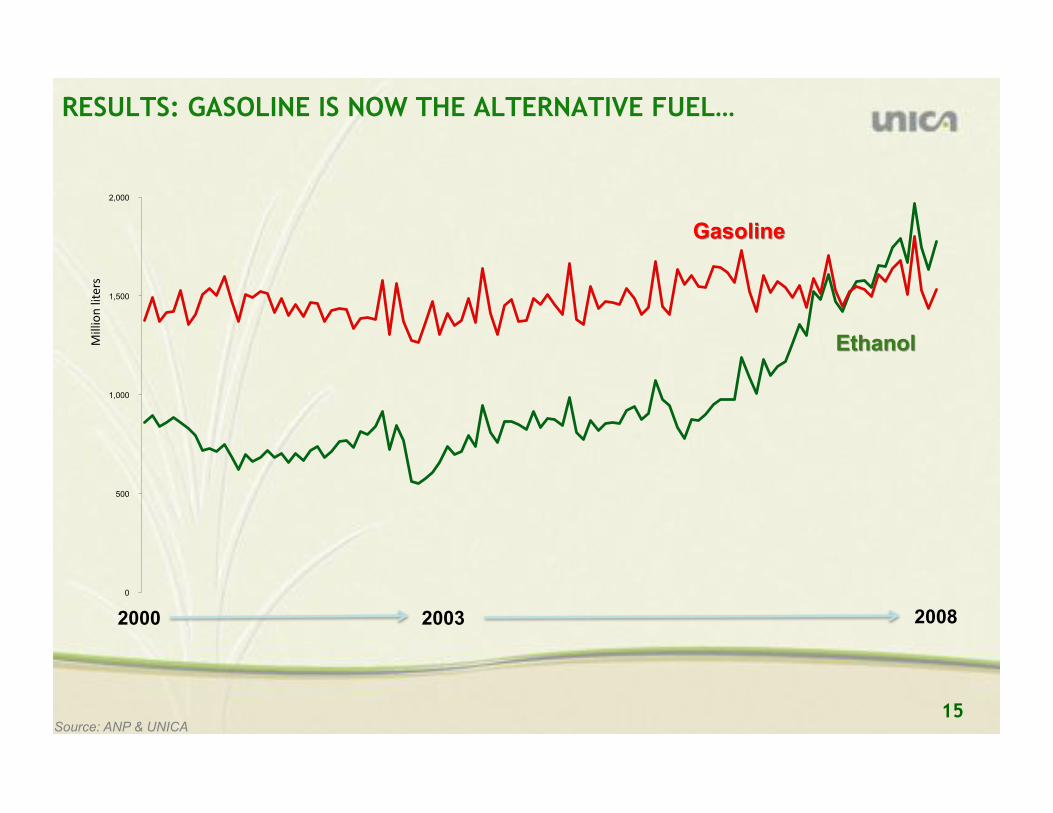

0

500

1,000

1,500

2,000

!"##"$%&#"'()*&

RESULTS: GASOLINE IS NOW THE ALTERNATIVE FUEL…

Source: ANP & UNICA

2000 2008 2003

16

Millions of Hectares (2007) %

total land

%

arable land

BRAZIL 851

TOTAL ARABLE LAND 354.8

1. Total Crop Land 76.7 9.0% 21.6%

Soybean 20.6 2.4% 5.8%

Corn 14.0 1.6% 3.9%

Sugarcane 7.8 0.9% 2.2%

Sugarcane for ethanol 3.4 0.4% 1.0%

Orange 0.9 0.1% 0.3%

2. Pastures 172.3 20% 49%

3. Available area Total arable land – (crop land + pastures)

105.8 12% 30%

…1% OF ARABLE LAND DISPLACES 50% GASOLINE

Sources: IBGE, UNICA

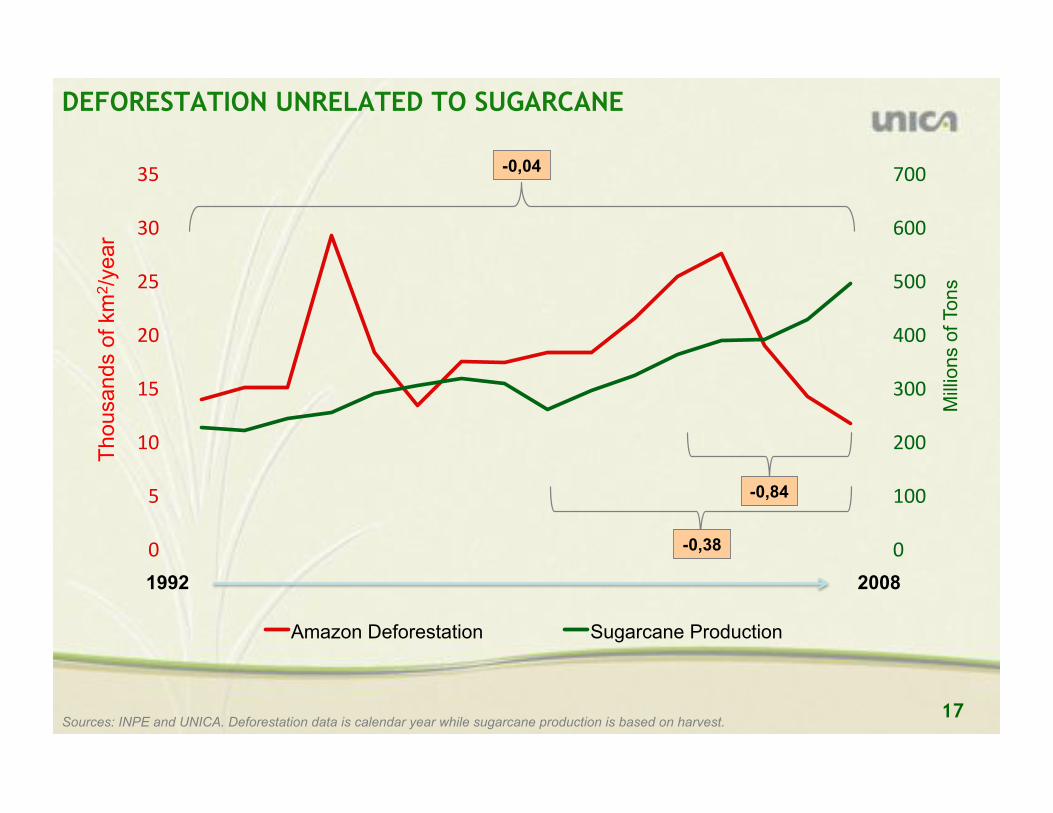

17 Sources: INPE and UNICA. Deforestation data is calendar year while sugarcane production is based on harvest.

+&

,++&

-++&

.++&

/++&

0++&

1++&

2++&

+&

0&

,+&

,0&

-+&

-0&

.+&

.0&

Mill

ions o

f Ton

s

Thousands o

f km

2/y

ear

Amazon Deforestation Sugarcane Production

-0,84

-0,38

-0,04

1992 2008

DEFORESTATION UNRELATED TO SUGARCANE

18 18

③!

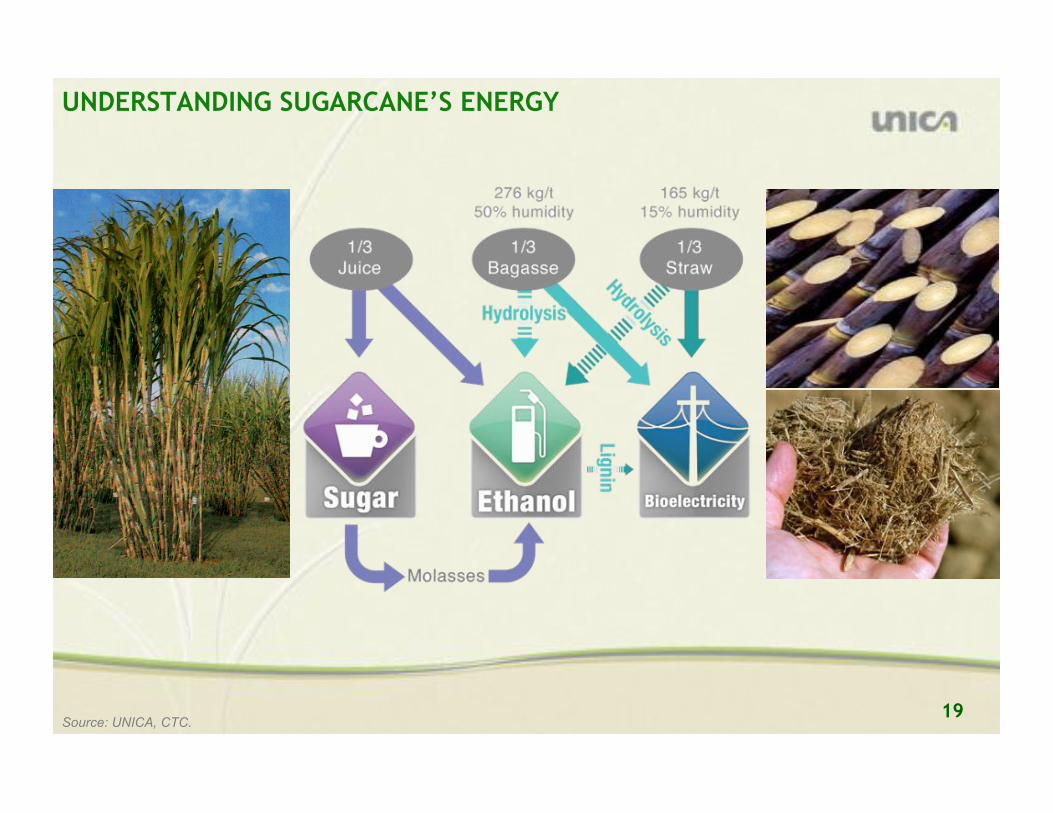

19 Source: UNICA, CTC.

UNDERSTANDING SUGARCANE’S ENERGY

20

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

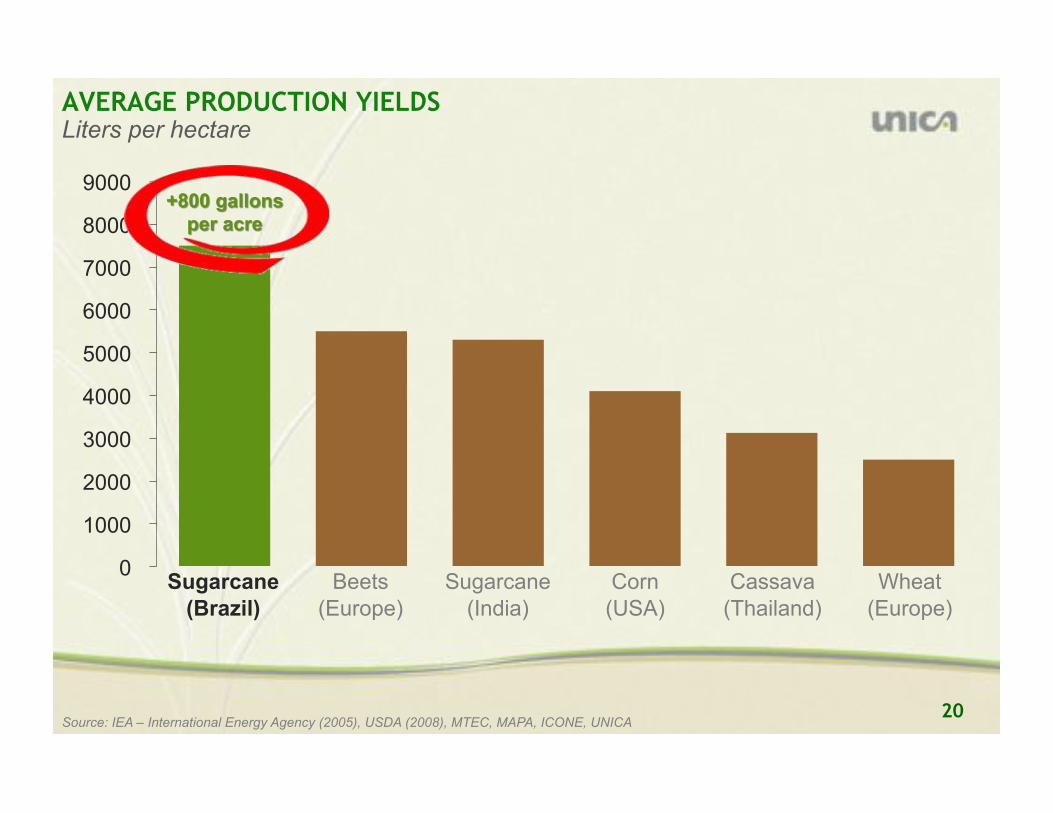

Liters per hectare AVERAGE PRODUCTION YIELDS

Source: IEA – International Energy Agency (2005), USDA (2008), MTEC, MAPA, ICONE, UNICA

Sugarcane (Brazil)

Beets (Europe)

Sugarcane (India)

Corn (USA)

Cassava (Thailand)

Wheat (Europe)

21

NET ENERGY BALANCE

0

1

2

3

4

5

6

7

8

9

10

Source: World Watch Institute, compilation of various sources.

Sugarcane (Brazil)

Beets (Europe)

Corn (USA)

Wheat (Europe)

Resulting energy for every unit of fossil fuel input

22

Note: Reductions represent well-to-wheel CO2-equivalent GHG emissions avoided from unit of ethanol compared to gasoline, calculated on a life-cycle basis.

-100%

-80%

-60%

-40%

-20%

0%

Ethanol from Grains (US/EU)

Ethanol from Sugar Beet (EU)

Ethanol from Sugar Cane (Brazil)

AVOIDED GREENHOUSE GAS EMISSIONS

Source: IEA – International Energy Agency (May, 2004), based on a review of recent articles.

Compared with “yesterday’s” gasoline baseline

23

2 METERS

3 METERS

2 METERS

3 METERS

1 METER

1 METER

4 METERS

22-36

tons C/ha

3-5

tons C/ha

5-7 years

Source: Polo de Biocombustivel (Weber Amaral) from various sources.

ABOVE & BELOW GROUND CARBON UPTAKE

24

Annual tons carbon per hectare

3-8 t C/ha 22-36 t C/ha

CANE VS. PASTURES: CARBON UPTAKE

Source: Polo de Biocombustivel (Weber Amaral) from various sources.

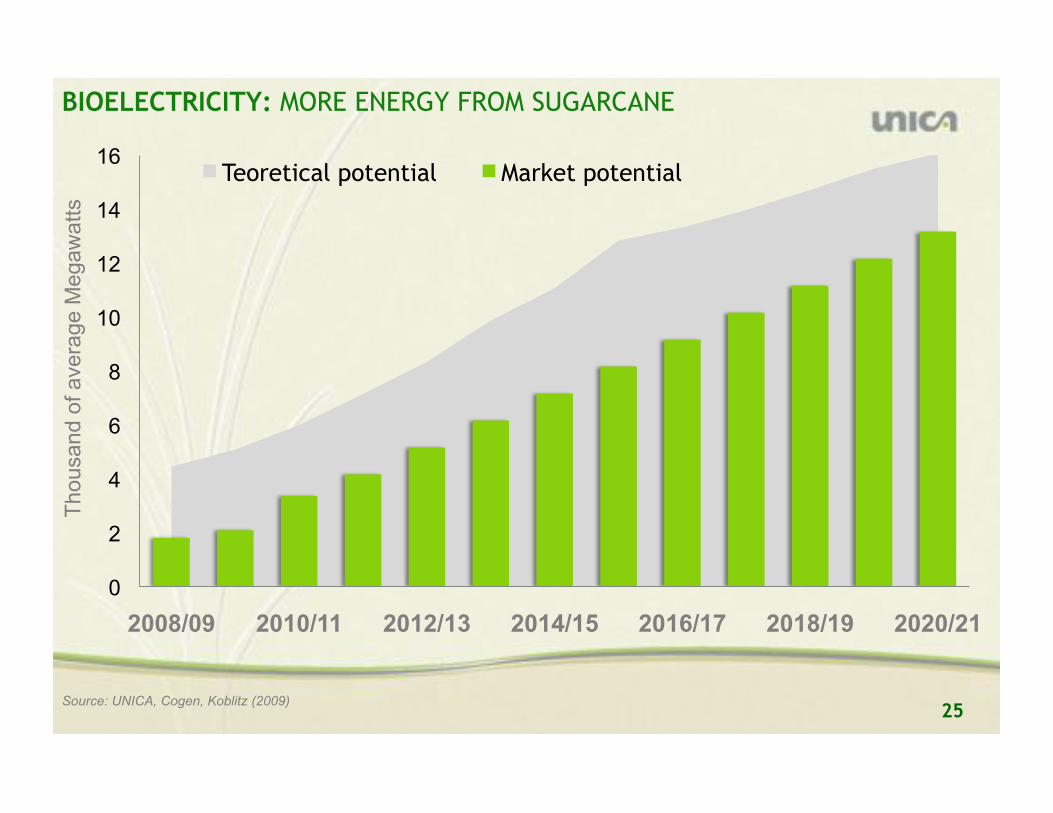

25 Source: UNICA, Cogen, Koblitz (2009)

BIOELECTRICITY: MORE ENERGY FROM SUGARCANE

0

2

4

6

8

10

12

14

16

2008/09 2010/11 2012/13 2014/15 2016/17 2018/19 2020/21

Thousand o

f avera

ge M

egaw

atts

Teoretical potential Market potential

26 26

④!

27 Source: UNICA staff

BIOFUEL SUSTAINABILITY FORUMS Multiple efforts at various levels

Sustainable Biofuels

International Forums

OECD

IEA

FAO

UNEP

G8+5

IDB

Multi-stakeholder Initiatives

Global Bioenergy Partnership (GBEP)

Roundtable on Sustainable Biofuels

(RSB)

Better Sugarcane Initiative (BSI)

Task 39 – Liquid Biofuels from

Biomass

Sugarcane Discussion Group with NGOs (SDG)

Government Policies

Brazil (PBCD & Immetro)

United States (EPA/RFS)

California LCFS

European Union (EC Directive)

UK (RTFO & Low CVP Fuels)

Germany (Meo-Consulting)

Sweden (SEI)

Verified Sustainable Ethanol

Netherlands (Cramer Commission)

28

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

'00

0 h

a

an

d '0

00

to

n

Food Production

Area

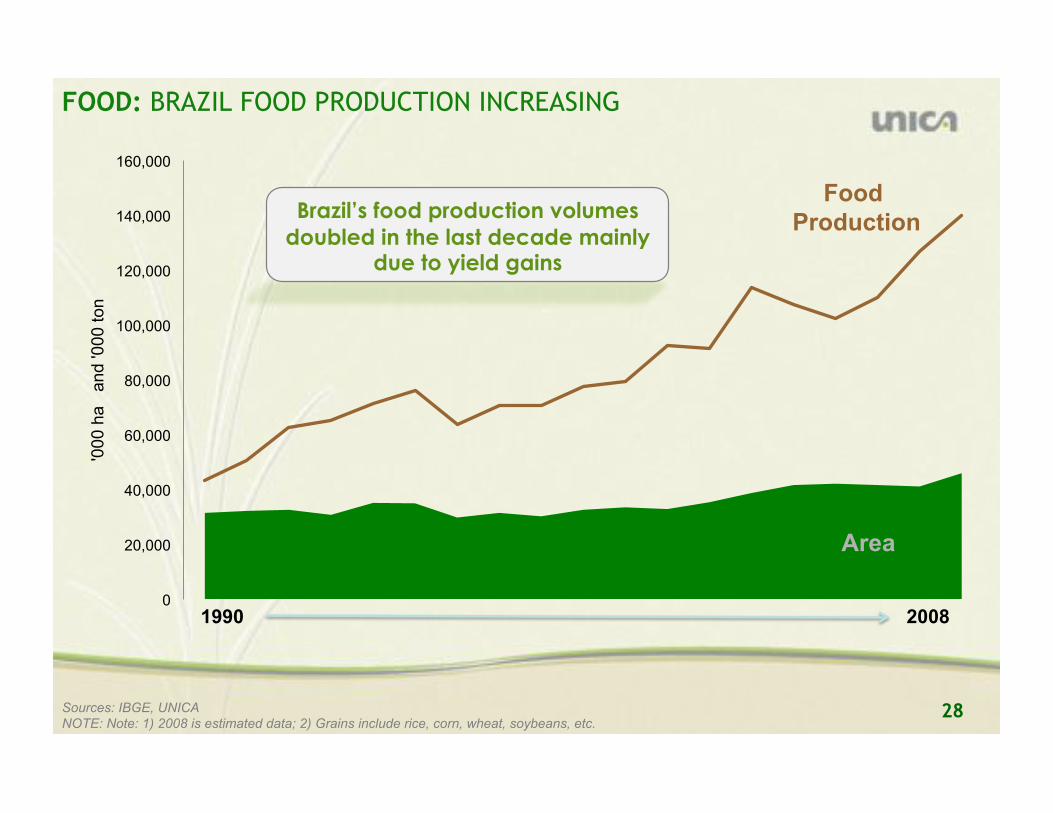

Sources: IBGE, UNICA NOTE: Note: 1) 2008 is estimated data; 2) Grains include rice, corn, wheat, soybeans, etc.

Brazil’s food production volumes

doubled in the last decade mainly due to yield gains

1990 2008

FOOD: BRAZIL FOOD PRODUCTION INCREASING

29

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Are

a (

'000 h

a)

Eth

anol (m

m liters

) S

ugar

('000 t

on

)

Ethanol

Sugar

Area

FOOD: SUGAR & ETHANOL PRODUCTION INCREASING

Sources: IBGE, UNICA

Brazil’s sugarcane ethanol volumes

have increased 130% and sugar more than 350%

1990 2008 2003

30 Source: HOFFMANN, R & OLIVEIRA, F. C. R. Evolução da remuneração das pessoas empregadas na cana-de-açúcar e em outras lavouras, no Brasil e em São Paulo. Piracicaba: ESALQ. 2008. Note: Amounts in Brazilian currency (August 2007, INPC Deflator)

JOBS: AVERAGE INCOME IN AGRICULTURE Sugarcane worker second highest income

0

100

200

300

400

500

600

700

800

Soybean Sugarcane Orange Coffee Corn

34()56(&!

$%'7#8&9%:$;(&

&<=&>3?6&-++2@&

BRAZIL SAO PAULO

31 Source: PNAD (1992, 2003, 2004 and 2005); MORAES, Márcia A.F. de. Número e qualidade dos empregos na agroindústria da cana-de-açúcar. In: A energia da cana-de-açúcar, 2007.

42.3%

66.0%

80.4%

60.8%

85.8%

93.8%

0%

20%

40%

60%

80%

100%

NORTHEAST CENTER-SOUTH SAO PAULO (UNICA)

1992 2005

JOBS: IMPROVING FORMAL EMPLOYMENT Industry workers receive full benefits

32 Source: UNICA’s GRI Report (2008)

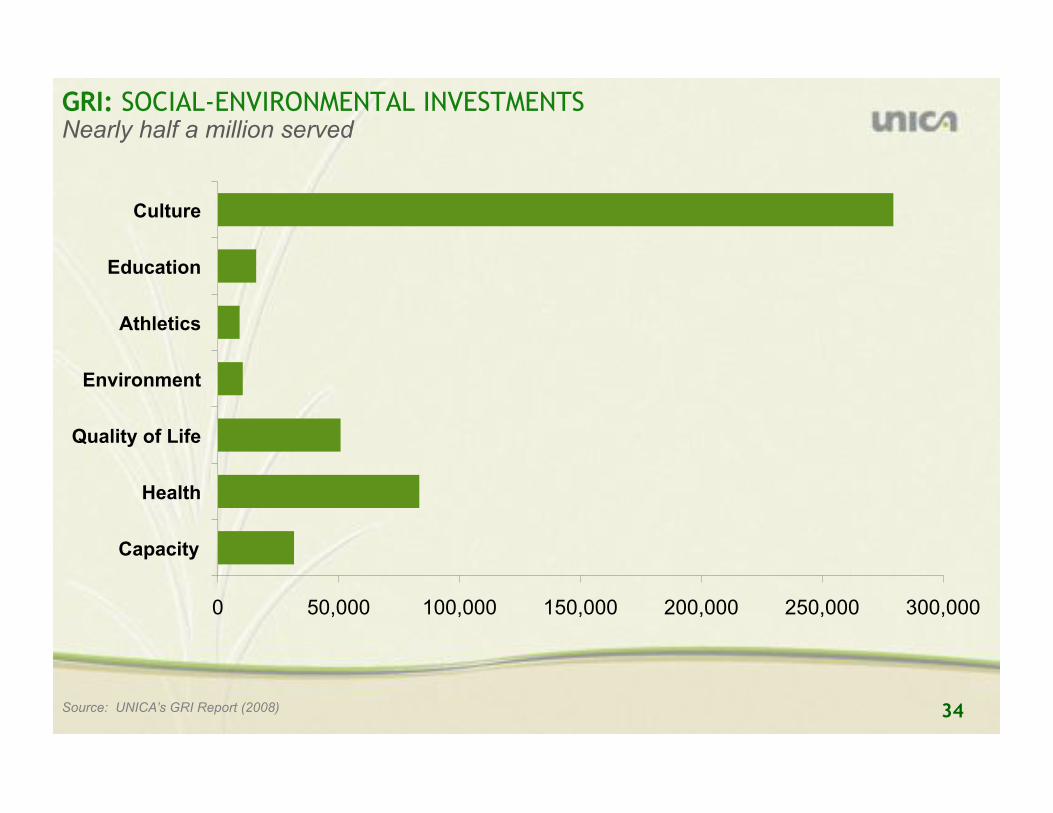

GRI: SOCIAL-ENVIRONMENTAL INVESTMENTS First trade association to undertake this effort

33 Source: UNICA’s GRI Report (2008)

US$75 million (R$160 million) invested

0 10 20 30 40 50 60 70 80 90

Capacity

Health

Quality of Life

Environment

Athletics

Education

Culture

Amounts in Millions of Brazilian Real (R$)

GRI: SOCIAL-ENVIRONMENTAL INVESTMENTS

34 Source: UNICA’s GRI Report (2008)

Nearly half a million served

0 50,000 100,000 150,000 200,000 250,000 300,000

Capacity

Health

Quality of Life

Environment

Athletics

Education

Culture

GRI: SOCIAL-ENVIRONMENTAL INVESTMENTS

35 35

⑤!

36

Petroleum

4,252 MT

(184.9 BGJ)

Ethanol 36 MT

(0.96 BGJ)

Sunflower 31 MT

Biodiesel 3.2 MT

(0.12 BGJ)

Castor Seed 1.4 MT

Soy 214 MT

Notes: Million tons, 2005. Data for palm, gasoline, diesel, LPG and Kerosene is from 2003. BGJ = Billions of Giga Joules Sources: FAO, Oil World, F.O. Licht, LCM, EIA. Elaboration: Icone and UNICA.

Rapeseed 47 MT

Gaso-line

1237 MT (53.8 BGJ)

Diesel 1077 MT (46.1 BGJ)

Total (Energy Equiv.) = 115.7 BGJ 1.1 BGJ

Palm 8 MT

LPG 391 MT

(11.9 BGJ)

Kerosene 92 MT (3.9 BGJ)

Sugar Cane 1,292 MT

Corn 702 MT

Wheat 628 MT

WORLD FUELS PRODUCTION

Renewable energy represent less than 1%

FOSSIL RENEWABLE

SOURCE FUEL FUEL SOURCE

37 Source: UNICA

ETHANOL: VALUES & GROWTH DRIVERS

!!Renewable source of energy

!!Octane booster

!! Fuel extender

!! Fuel substitute

!! Low pollution fuel (reduce GHG emissions)

!! Social development inducer in rural areas

!! In line with Kyoto & Sustainable Development

!! Environmental concerns (climate change)

!! Energy security ! high oil prices

!! Support to farm incomes

Valu

es

Drivers

38 Source: FOLicht, Secex, USITC, European Comission, LMC. As prepared by UNICA

ETHANOL TRADE VS. PRODUCTION

Only about 10% of total production

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006 2007

Billio

ns o

f L

iters

10%

39 Source: Brazilian Ministry of Trade & Development (SECEX)

BRAZILIAN ETHANOL EXPORTS BY DESTINATION

2006 2007 2008

Others 600 742 810

European Union 582 1,008 1,473

Caribbean (CBI) 486 931 1,316

United States 1,749 850 1,519

-

1,000

2,000

3,000

4,000

5,000

Mil

lio

n L

ite

rs

3.4 bi liters $ 1.6 bi

3.5 bi liters $ 1.5 bi

5.1 bi liters $ 2.4 bi

40

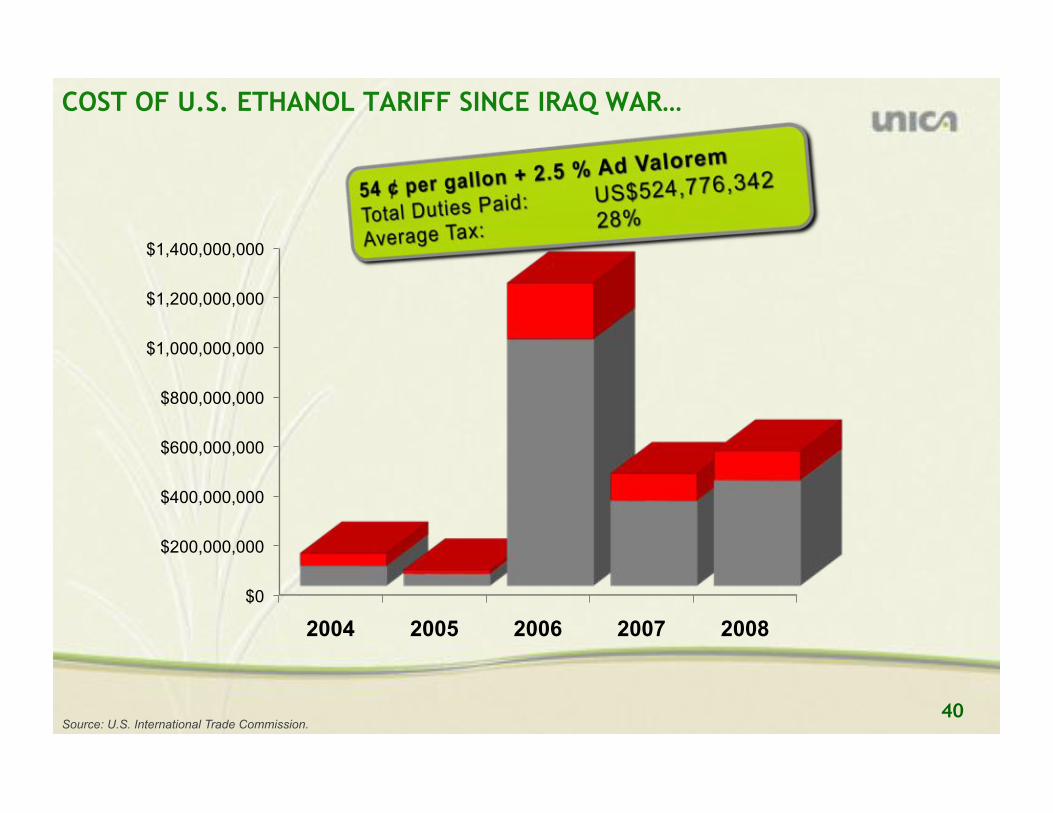

$0

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

2004 2005 2006 2007 2008

Source: U.S. International Trade Commission.

COST OF U.S. ETHANOL TARIFF SINCE IRAQ WAR…

41

80.9

59.1

43.3

12.4

2.4 0.9 0

10

20

30

40

50

60

70

80

90

USA Japan EU Brazil China India

Auto

s p

er

100 p

eople

Fonte: ANFAVEA, ONU, JAMA, ACEA. Developed by UNICA. Data from 2005 except for India (2004).

USE OF AUTOMOBILES

What fuel will emerging economies use?

42

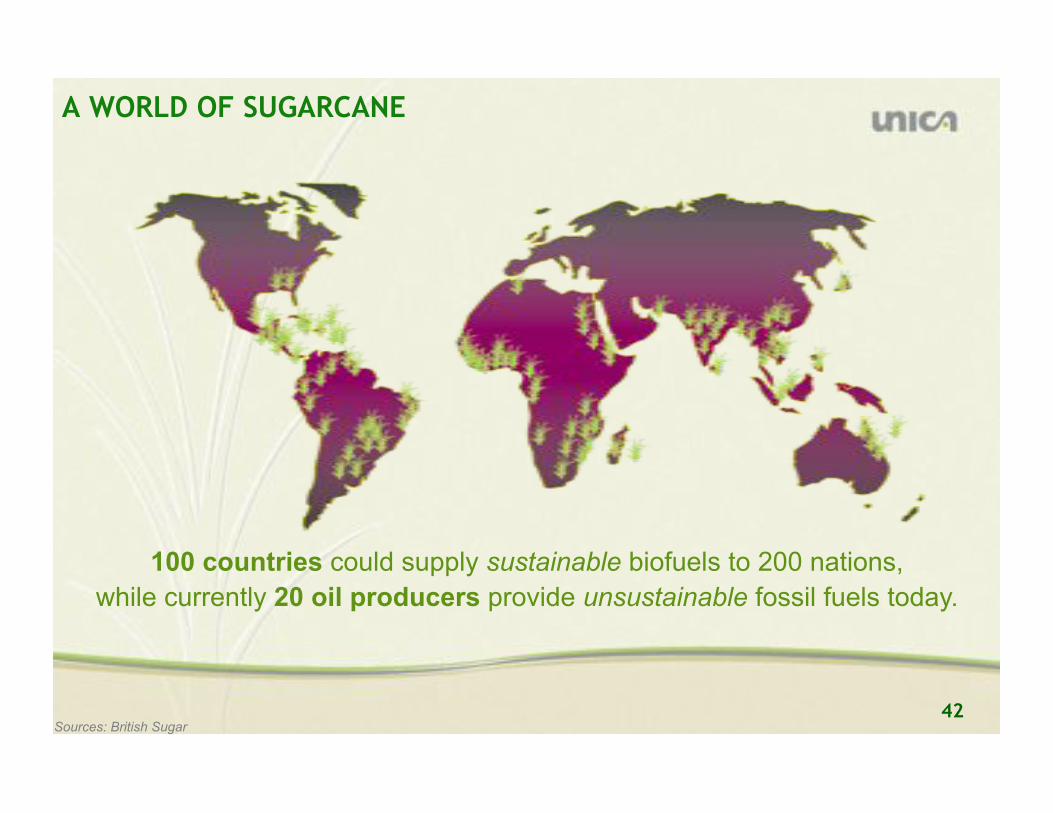

100 countries could supply sustainable biofuels to 200 nations,

while currently 20 oil producers provide unsustainable fossil fuels today.

A WORLD OF SUGARCANE

Sources: British Sugar

43 43

⑥!

44

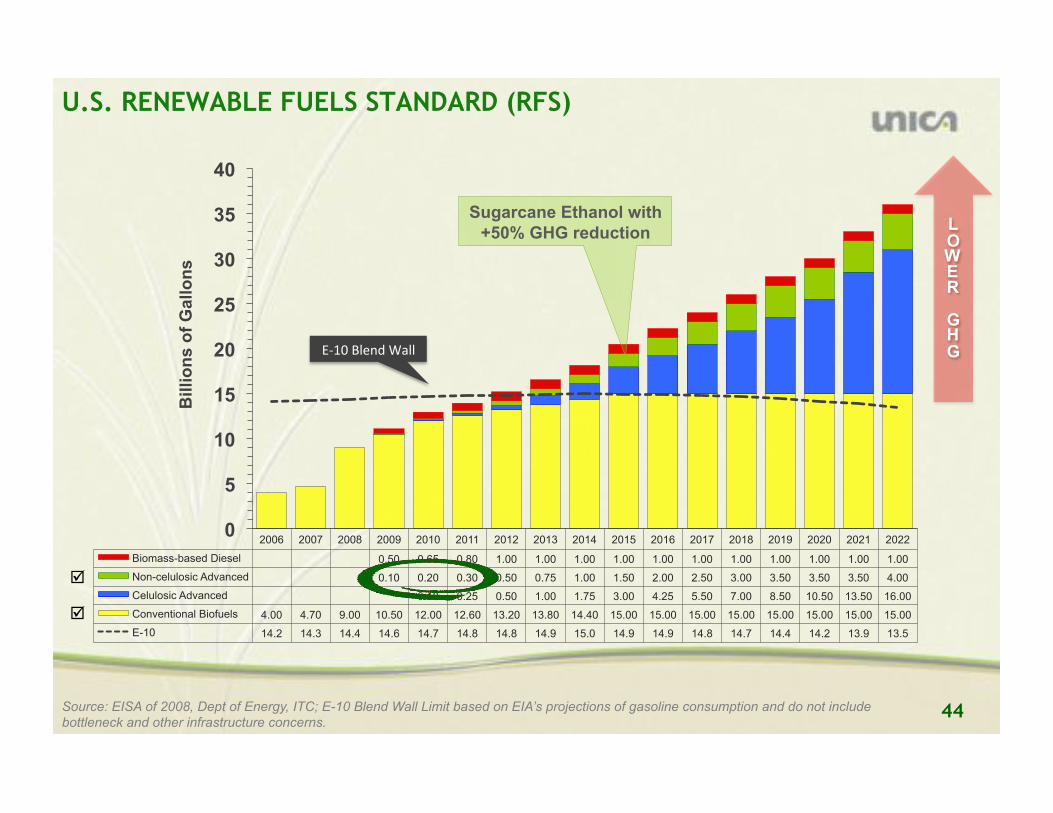

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Biomass-based Diesel 0.50 0.65 0.80 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00 1.00

Non-celulosic Advanced 0.10 0.20 0.30 0.50 0.75 1.00 1.50 2.00 2.50 3.00 3.50 3.50 3.50 4.00

Celulosic Advanced 0.10 0.25 0.50 1.00 1.75 3.00 4.25 5.50 7.00 8.50 10.50 13.50 16.00

Conventional Biofuels 4.00 4.70 9.00 10.50 12.00 12.60 13.20 13.80 14.40 15.00 15.00 15.00 15.00 15.00 15.00 15.00 15.00

E-10 14.2 14.3 14.4 14.6 14.7 14.8 14.8 14.9 15.0 14.9 14.9 14.8 14.7 14.4 14.2 13.9 13.5

0

5

10

15

20

25

30

35

40 B

illi

on

s o

f G

all

on

s

AB,+&C#(%D&E5##&

"

"

L

OWER

GH

G

U.S. RENEWABLE FUELS STANDARD (RFS)

Source: EISA of 2008, Dept of Energy, ITC; E-10 Blend Wall Limit based on EIA’s projections of gasoline consumption and do not include bottleneck and other infrastructure concerns.

Sugarcane Ethanol with +50% GHG reduction

45

EPA’S LAND USE MODEL

Source: Environmental Protection Agency (EPA), May 2009.

46

EPA: “INDIRECT LAND USE” EFFECT

Source: See Figure 2.1-4. “Regional Crop Expansion by Renewable Fuel, 2022 (acres per thousand ethanol equivalent gallons of biofuel production) in page 284 of Discussion Draft of Environmental Protection Agency (EPA) Regulatory Impact Analysis, May 2009.

Ac

res

pe

r T

ho

us

an

d G

all

on

s E

tha

no

l P

rod

uc

ed

47

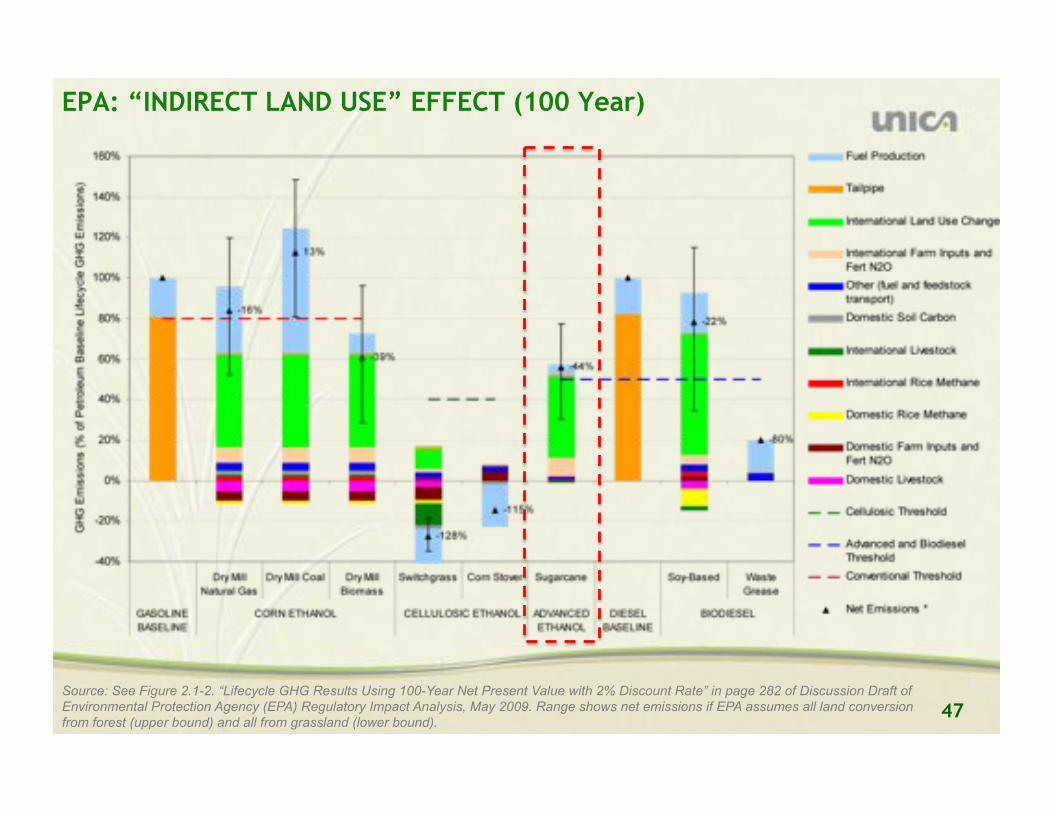

EPA: “INDIRECT LAND USE” EFFECT (100 Year)

Source: See Figure 2.1-2. “Lifecycle GHG Results Using 100-Year Net Present Value with 2% Discount Rate” in page 282 of Discussion Draft of Environmental Protection Agency (EPA) Regulatory Impact Analysis, May 2009. Range shows net emissions if EPA assumes all land conversion from forest (upper bound) and all from grassland (lower bound).

48

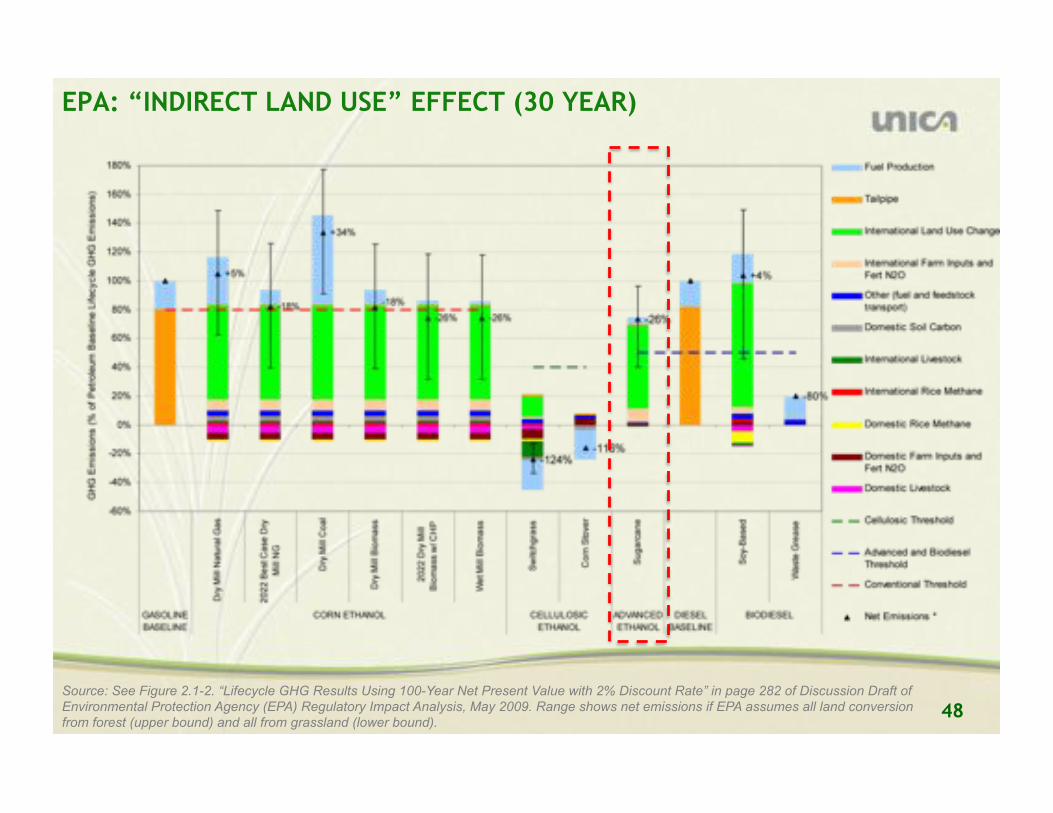

EPA: “INDIRECT LAND USE” EFFECT (30 YEAR)

Source: See Figure 2.1-2. “Lifecycle GHG Results Using 100-Year Net Present Value with 2% Discount Rate” in page 282 of Discussion Draft of Environmental Protection Agency (EPA) Regulatory Impact Analysis, May 2009. Range shows net emissions if EPA assumes all land conversion from forest (upper bound) and all from grassland (lower bound).

49

96 86

69

27

0

20

40

60

80

100

120

Gasoline LCFS in 2020 Corn Ethanol Sugarcane Ethanol

Gra

ms o

f C

O2 p

er

meg

ajo

ule

CALIFORNIA’S LOW CARBON FUELS STANDARD (LCFS)

Source: California Air Resources Board’s Low Carbon Fuel Standard, March 2009.

50

96 86

69

27

0

20

40

60

80

100

120

Gasoline LCFS in 2020 Corn Ethanol Sugarcane Ethanol

Gra

ms o

f C

O2 p

er

meg

ajo

ule

LCFS WITH “INDIRECT LAND USE” PENALTY

Source: California Air Resources Board’s Low Carbon Fuel Standard, March 2009.

ILU

C u

sin

g

GTA

P

51

87

88

89

90

91

92

93

94

95

96

97

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

LCFS & SUGARCANE SIMULATION

Source: California Air Resources Board’s Low Carbon Fuel Standard, March 2009.

Gra

ms o

f C

O2 p

or

me

ga

jou

le

RE

PO

RT

ING

ON

LY

52

SUGARCANE “INDIRECT LAND USE” EFFECT

Source: UNICA, California Air Resources Board’s Low Carbon Fuel Standard, March 2009.

53 53