branch less banking

TRANSCRIPT

Presented ByMurtaza Ali F09MB021Mohammad Umair Qasim F09MB034Usman Qamar F09MB045

Branchless Banking

Introduction

Branchless Banking (BB) represents a significantly cheaper alternative to conventional branch-based banking that allows financial institutions and other commercial players to offer financial services outside traditional bank premises by using delivery channels like retail agents, mobile phone etc.

BB can be used to substantially increase the financial services outreach to the un-banked communities.

History

United Kingdom is an early pioneer of Branchless banking service. Launched by Midland Bank (now part of HSBC) in 1989, First direct accounts are operated solely via the Internet, post, or telephone, and they do not themselves operate any retail branches (although HSBC branches can be used to make deposits) while at the same time offering a full range of banking services.

Permissible Models for Branchless Banking

One-to-one (1-1) ModelIn this model one bank offers mobile phone banking services in collaboration with a specific Telco. As a consequence, the services may only be offered to customers using mobile connection of that specific telco.The example of this model is Easy PaisaIt may be noted that one-to-one model does not necessarily require exclusivity. Therefore, one bank can have several one-to-one arrangements with many telcos or alternately, one telco can have several one-to-one arrangements with many banks.

One-to-one (1-1) Model

Advantages

It offers greater customization, good service standards, possibility of co branding and co marketing

Disadvantages

It lacks in outreach as it is limited to the customers of one telco only

One-to-many (1-∞) Model

In this model a bank offers mobile phone banking services to customers using mobile connection of any Telcos.This model offers the possibility to reach to any bankable customer who has a mobile phone connection.The example of this model is UBL Omni

Advantages

It offers greater customization, good service standards, possibility of co branding and co marketing.

One-to-many (1-∞) Model

Disadvantage

It lacks in outreach as it is limited to the customers of one telco only.

Many-to-many (∞-∞) ModelIn this model many banks and many telcos join hands to offer services to virtually all bankable customers.Under this system, a central transaction processing system (TPS) is necessitated, which must be controlled by an FI; or by a subsidiary owned and controlled by an FI or a group of FIs; or by a third party service provider under proper agency agreement with a bank.It is just like the existing ATM network in the country where customer of any bank can use ATM of any other bank.

Many-to-many (∞-∞) Model

The TPS should be capable of; i) settling all transactions on real time basis, ii) storing all proofs of transactions and iii) providing a day end statement of account

to all member banks.

Facilities offered by Branchless Banking

SystemOpening and maintaining a BB Account• A BB account can be opened and operated by a

customer with a bank through use of BB channels. Banks may associate such account to a particular branch or to a centralized branchless banking unit.

Account-to-account Fund transfer: • Customers may transfer funds to/from their BB

account from/to their other pre-registered accounts (current/saving bank accounts, loan limit accounts, credit card accounts etc.)

Person-to-person Fund Transfers: • Customer can transfer funds from their BB or

regular account to BB or regular accounts of same or some other bank of other customers.

Cash-in and Cash-out: • Customers may deposit and withdraw funds

from their BB account using a variety of options including bank-branch counters, ATM machines and authorized agent locations.

Facilities offered by Branchless Banking

System

Bill Payments: • A BB account can also be used to pay utility bills (e.g. Gas,

Electricity, Phone etc.)Merchant Payments: • Customers can use a BB account to make payments for

purchases of goods and services. Loan Disbursement/Repayment: • FIs, particularly MFBs may use BB accounts as a means to

disburse small loan amounts to their borrowers having BB accounts. The same accounts may be used by customers to repay their loan installments.

Remittances: • BB accounts may be used to send / receive remittances

subject to existing regulations.

Facilities offered by Branchless Banking

System

Risk-Based Customer Due Diligence

• To maximize the share of branchless banking and to reach those area where conventional banking is not available, a risk-based approach to customer due diligence is mentioned here.

• This approach is specific to the BB accounts and does not apply to the regular full service banking accounts.

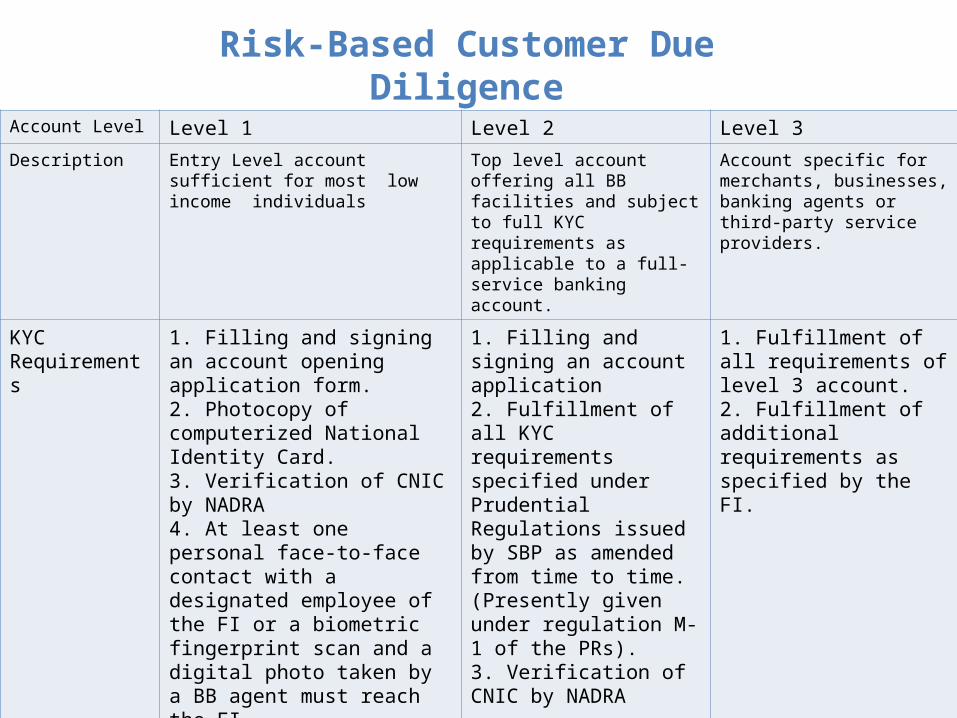

Account Level Level 1 Level 2 Level 3

Description Entry Level account sufficient for most low income individuals

Top level account offering all BB facilities and subject to full KYC requirements as applicable to a full-service banking account.

Account specific for merchants, businesses, banking agents or third-party service providers.

KYC Requirements

1. Filling and signing an account opening application form.2. Photocopy of computerized National Identity Card.3. Verification of CNIC by NADRA4. At least one personal face-to-face contact with a designated employee of the FI or a biometric fingerprint scan and a digital photo taken by a BB agent must reach the FI

1. Filling and signing an account application2. Fulfillment of all KYC requirements specified under Prudential Regulations issued by SBP as amended from time to time. (Presently given under regulation M-1 of the PRs).3. Verification of CNIC by NADRA

1. Fulfillment of all requirements of level 3 account.2. Fulfillment of additional requirements as specified by the FI.

MaximumBalanceLimits(debit/credit)

Rs. 60,000 FI must set limits commensurate with each customer’s profile.

FI must set limits commensurate with each customer’s profile.

Maximum Throughput Limits(debit/credit)

Rs. 10,000 per dayRs. 20,000 per monthRs. 120,000 per year

Risk-Based Customer Due Diligence

Super Agents: These may be organizations having well-

established owned or franchised retail outlets, or a distribution setup. These will be responsible for managing and controlling subagents. These may include fuel distribution companies, Pakistan Post, courier companies, chain stores etc.

Direct Agents: These may include large to medium sized stores

etc., which have a separate agency/service level agreement with the FI.

Agent Structure

Sub Agents: These are the branches/outlets or franchised locations managed by a super agent and not directly controlled by the FI on a day-to-day basis. However, in case of franchised locations, these must have a similar service level agreement with the super agent as the super agent will have with the FI.

Role of Agents

Agents may perform any or all of the following functions depending on the agency agreement and agent type as detailed in the following sections;• Opening of BB Accounts (Level 1 accounts only).• Cash in / Cash out for BB accounts.• Bills Payments (Both from registered BB customers as well as from walk-in customers (through cash) of any utility company).

• Loan disbursement / Repayment Collection (Without involving into loan marketing/approval functions).

Role of Agents

1) Banks wishing to provide branchless banking services or to bring in substantial changes in underlying technological infrastructure shall submit to the State Bank, an application describing the services to be offered, infrastructure modifications and how these services fit in the bank’s overall strategy.

2) SBP shall pre-screen the overall financial condition of the FI as well as the compliance with the SBP rules and regulations based on the latest available onsite and offsite reports

3) Based on the review, a principle approval of the application will be granted.

4) After getting this principle approval the FI shall, in turn notify the SBP on the actual date of launching/ enhancement of its BB services.

Branchless Banking Procedures

5) Within thirty (30) days from such launching/enhancement, banks shall submit to the SBP, the following documentary requirements

Business objectives Description of Banks electronic system List of Software and hardware components Contingency and Disaster recovery plan Copy of Contracts with service provider

6) If after the evaluation of the submitted documents, SBP still finds some unresolved issues and grey areas, the bank may be required to make a presentation and/or to submit any documents relating to of its branchless banking to SBP.

7) Upon completion of evaluation, the Authorization will be granted.

Branchless Banking Procedures

Market Leaders in Branchless Banking:1. Easy Paisa (Telenor in collaboration with

Tameer Microfinance bank)2. Omni Shop (UBL)

Major Branchless Banking Service Providers in

Pakistan

Easy Paisa

The largest branchless banking service in Pakistan which offers the most convenient

access to Financial Services for all Pakistanis.

Easypaisa offers two kind of services :

1.Over-the-counter (OTC) products: where the customer can go up to any of the 5500 plus certified merchants for financial transactions

2. Mobile products: where the customer can use their mobile handset for financial transactions.

Easy Paisa

Products and services

• Money Transfer: Using Money Transfer from easy paisa, you can send and receive money to and from anyone from any easy paisa shop in the most efficient, secure and convenient way.

• Features:Any person with a valid Nadra CNIC can send money or receive money

This service is not limited to Telenor subscribers; other mobile network subscribers can also use this service

Sending/Receiving can be done from more than 4,000 easypaisa shops all over Pakistan

Service charges for money transferTransaction

Amount Fee Tax on Fee* Total Charges

Rs. 1-1000 Rs. 50 Rs. 8 Rs. 58

Rs. 1001-2500 Rs. 100 Rs. 16 Rs. 116

Rs. 2501-4000 Rs. 150 Rs. 24 Rs. 174

Rs. 4001-6000 Rs. 200 Rs. 32 Rs. 232

Rs. 6001-8000 Rs. 250 Rs. 40 Rs. 290

Rs. 8001-10000 Rs. 300 Rs. 48 Rs. 348

All fees are subject to 16% FED as per Government Regulations

Bill Payment• Easypaisa bill payment service brings you a hassle

free yet secure solution to pay your Electricity, Gas and Telephone (PTCL) bills:

Utility Companies On Board • PTCL (Pakistan Telecommunication Company

Limited) • SSGC (Sui Southern Gas Company)• SNGPL (Sui Northern Gas Pipelines Ltd)• KESC (Karachi Electric Supply Company)• HESCO (Hyderabad Electric Supply Company)• MEPCO (Multan Electric Power Company)

Charges on payment of bills:• Rs. 10 to be charged from the customer

for any Utility Bill Paid of any denomination

• No FED is applicable here

Bill Payment

Mobile Account

• Telenor subscribers will now be able to pay bills, transfer money and use many more services from their own mobile phones

• Mobile Accounts are actual bank accounts and work just like a normal bank account

• Can be opened through: – Telenor Sales and Service Centers, – Telenor Franchise– Tameer Bank branch

Features Any Telenor current or new subscriber can open a

Mobile Account. No prior Bank Account is needed; Anyone with a Telenor SIM can avail and use this

service Send money to any person with a valid NADRA CNIC

or to any other easypaisa Mobile Account. Utility bills can also be paid instantly from an

easypaisa Mobile Account Cash Deposit into a Mobile Account or Cash

Withdrawal from any Mobile Account can be done at more than 5,000 easypaisa merchants in more than 450 cities in Pakistan

Mobile Account

How to open a Mobile Account

Easy Paisa Mobile Account is offered to only Telenor customers. Steps to open an account are:

1) Go to any Telenor Service Center, Franchise or Tameer Bank

2) You should have a Telenor SIM (registered in your name)

3) You should carry original CNIC 4) Fill in a form plus photograph (will be taken

by Telenor Staff in real time) 5) Sign the form plus thumb impression 6) Get the receipt and you are done

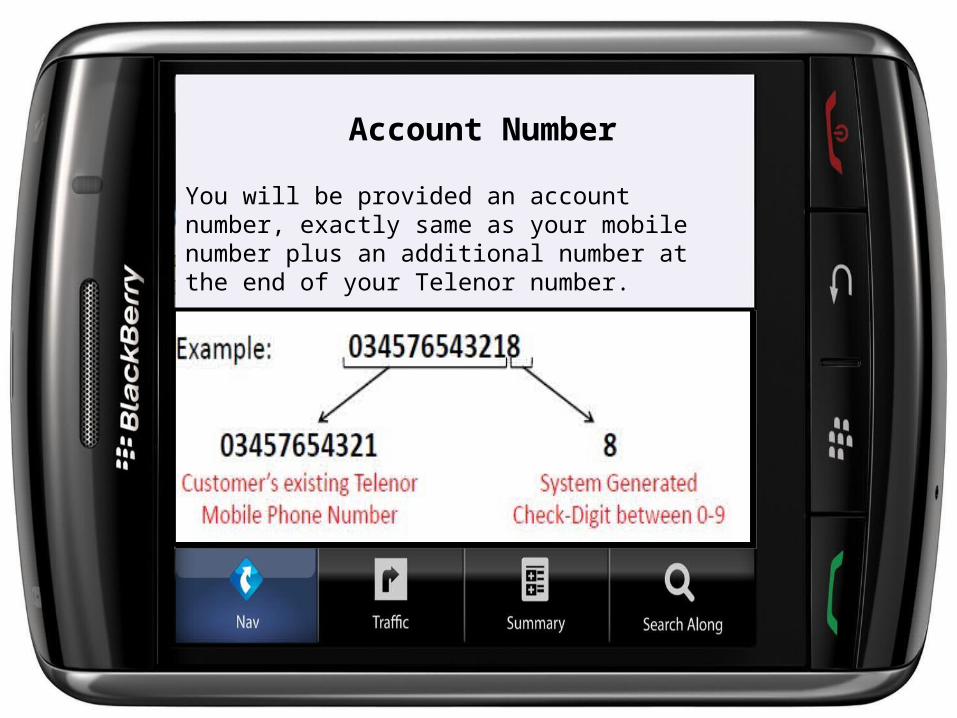

You will be provided an account number, exactly same as your mobile number plus an additional number at the end of your Telenor number.

Account Number

Transaction limits for Bank Account

The following transactional limits apply to all easypaisa Mobile Account, as regulated by the State Bank of Pakistan. Rs. 10,000 per day, Rs. 20,000 per month and Rs. 120,000 per year. These limits apply on both credits and debits in a Mobile

Account

A customer can only keep a maximum of Rs. 60,000 in his easypaisa Mobile Account at any time

Money Transfer (from an easypaisa Mobile Account to another easypaisa

Mobile Account) SlabStart

SlabEnd

Charges FED*Total

Charges

1 1000 20 3.20 23.20

1001 2500 40 6.40 46.40

2501 4000 60 9.60 69.60

4001 6000 80 12.80 92.80

6001 8000 100 16.00 116.00

8001 10000 120 19.20 139.20

16% FED is applicable on banking services charges“

Money Transfer (from a CNIC to an easypaisa Mobile Account) `

Slab Start

Slab End

Charges FED*Total

Charges

1 1000 30 4.80 34.80

1001 2500 60 9.60 69.60

2501 4000 90 14.40 104.40

4001 6000 120 19.20 139.20

6001 8000 150 24.00 174.00

8001 10000 180 28.80 208.80

16% FED is applicable on banking services charges“

Money Transfer (from an easypaisa Mobile account to a CNIC)

Slab Start

Slab End

Charges FED*Total

Charges

1 1000 40 6.40 46.40

1001 2500 80 12.80 92.80

2501 4000 120 19.20 139.20

4001 6000 160 25.60 185.60

6001 8000 200 32.00 232.00

8001 10000 240 38.40 278.40

16% FED is applicable on banking services charges“

To ensure that all transactions made through easypaisa are secure, important security needs have been addressed:

The selection of merchants through which transactions are taking place has been governed by all stringent measures described by the SBP.

The security of all customer information is through documentation that is based on State Bank of Pakistan’s guidelines. Account opening involves verification of CNIC through NADRA.

Security of all transactions will be ensured using Unstructured Supplementary Service Data (USSD) protocol. USSD is a lot safer as compared to SMS

Security Concerns

Customers across Pakistan can open a UBL Omni bank account at any UBL Omni Dukaan of their choice by using

their CNIC number and mobile phone number

UBL Omni

• Direct challenge to Telenor Easy paisa • All mobile networks have a support for UBL omni• Customers across Pakistan can open a UBL Omni

bank account at any UBL Omni Dukaan of their choice, whether close to their home or place of work, by using their CNIC number and mobile phone number

• UBL Omni account holder will subsequently be able to deposit and withdraw cash, make utility bill payments, send or receive money, purchase mobile card vouchers, make postpaid mobile bill payment.

• People without a UBL Omni bank account will also be entertained at a UBL Omni Dukaan where they can make utility bill payments, send or receive money, purchase mobile card vouchers and make postpaid mobile bill payments.

UBL Omni

For Walk In Customers1. Account Opening2. money Transfer3. Mobile Voucher Purchase4. Utility Bill Payments

For Account holders1. Omni Dukaan2. Internet Banking

Omni Services

Omni Dukan

• People without a UBL Omni bank account will also be entertained at a UBL Omni Dukaan

• Located in more than 100 cities• Customer can open a UBL Omni bank account at any

UBL Omni Dukaan • Omni account holders can make

– utility bill payments, – send or receive money, – purchase mobile card vouchers and – make postpaid mobile bill payments.

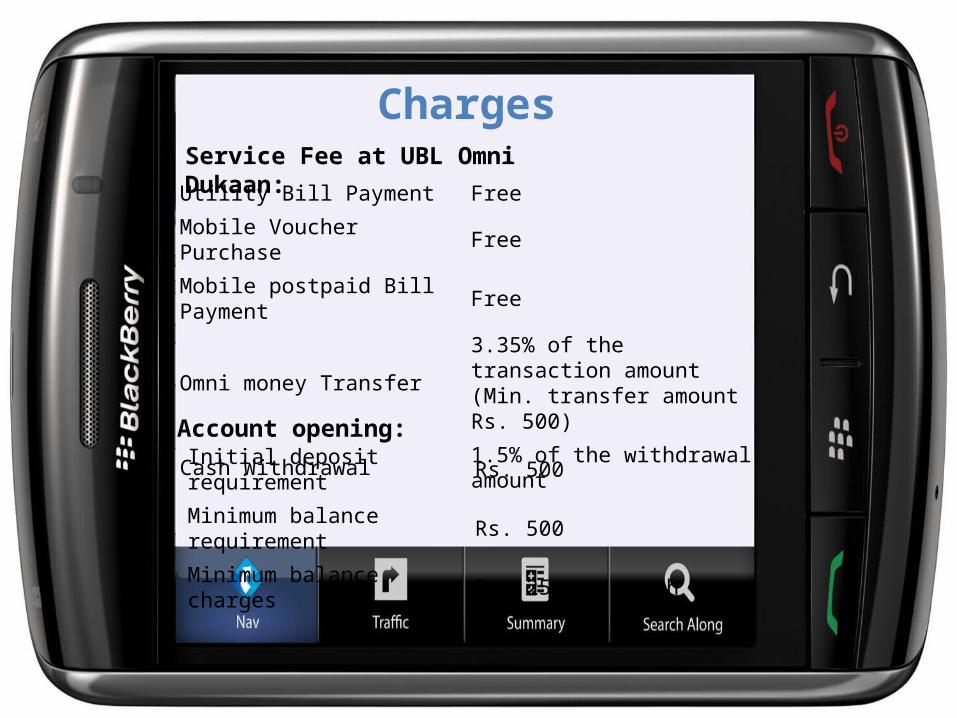

Utility Bill Payment Free

Mobile Voucher Purchase Free

Mobile postpaid Bill Payment Free

Omni money Transfer3.35% of the transaction amount (Min. transfer amount Rs. 500)

Cash Withdrawal 1.5% of the withdrawal amount

Charges

Account opening:Initial deposit requirement Rs. 500

Minimum balance requirement Rs. 500

Minimum balance charges Rs. 25 per month

Service Fee at UBL Omni Dukaan:

Risk Associated to Branchless Banking

Agents Related Risks

– Agents may operate in hard-to reach or dangerous areas & they lack physical security systems and specially trained personnel

– Use of retail agents raises special concerns regarding consumer protection and compliance

– Client's profiles and financial data stored unencrypted on information systems of agents and TPS premises is vulnerable to leakage.

– Physical or logical access to agents and TPS information system without proper controls may result into illegitimate access by disgruntled employees and malicious persons.

Wireless/ e-Banking Technology Risks

– Technology risk but in particular strategic, operational, legal and reputation risks, thereby influencing the overall risk profile of banking.

– wireless communication are still evolving, creating considerable uncertainty regarding the scalability of existing wireless products

– Physical or logical access to Telco facilities by unauthorized person especially in case where Short Message Service (SMS)

– Interruption in services of Telco due to technical or non-technical issue and non availability of any parallel system may cause disruption in service availability.

– Customer without proper awareness might store PIN on his/her mobile device which may be revealed easily on stealing

Physical Security of Telco, FI, Agent and TPS Facilities should be properly managedAvailability of Services and back up plan in case of disaster.Client transit data confidentiality and integrityClient stored data confidentiality and integrityClient profiling and maintenance of clients spending behaviorAccountability and Non-Repudiation in case of criminal incidentsError messaging and exception handling to avoid exposure of clients informationAuthentication of clientTo educate End User about information security.

Measures for Risk Mitigation

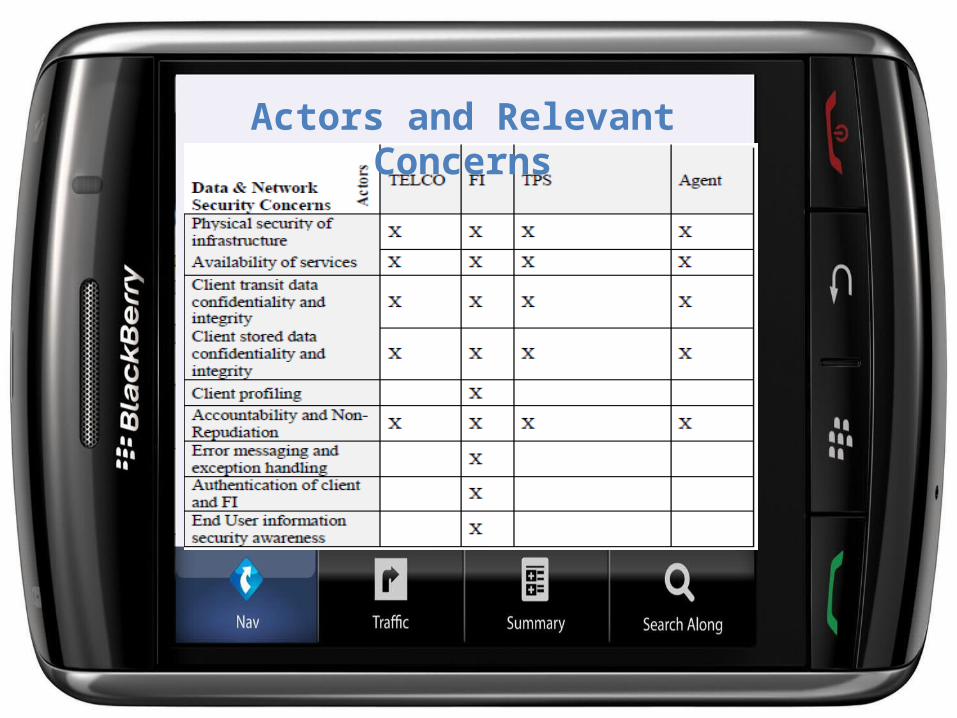

Actors and Relevant Concerns

Contribution Towards Economy• Remittance flow is widely believed to be a strong

contributor to economy.

• Remittances also offer significant potential to support low income and vulnerable groups in the country.

• Currently, Pakistan’s figure for domestic remittances through the formal channel stands at $6.95 billion.

• It is also estimated that approximately $2 to 4 Billion is transacted through informal channels

Contribution Towards Economy

• There are multiple entry barriers which push people towards informal channels: this includes • absence of any infrastructure close to home

• cumbersome documentation process

• By breaking these barriers, Branchless Banking aims to bring the bulk of informal activity into formal sector which will contribute to the economy of the country in a substantial way.

Thank YouDon’t Bother to Ask Questions

ANSWERS ARE NOT THERE!!:P