bolivia pension fund management from public to private h. von gersdorff

TRANSCRIPT

BOLIVIAPENSION FUND MANAGEMENT

From Public to Private H. von Gersdorff

THE OLD DEFINED-BENEFIT PENSION THE OLD DEFINED-BENEFIT PENSION SYSTEMSYSTEM

Of a basic pension system, administered by a public agency (FOPEBA)

38 Complementary Funds, including the eight social security funds of public universities.

IN 1996, THE IN 1996, THE SYSTEM SYSTEM CONSISTEDCONSISTED

FOPEBA coverage:

Approximately 300,000 active affiliates, of which about 65% were public sector employees.

Retirees added up to roughly 120,000.

Affiliates as a share of the total (urban) economically active population in 1996 were roughly 12% (22%).

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1

COSSMIL

JUDICIAL BRANCH

UNIVERSITIES'INSURANCES (8)

PRIVATE BANKING

STATE BANKING

FOPEBA

26 COMPLEMENTARYFUNDS

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1

COSSMIL

JUDICIAL BRANCH

UNIVERSITIES'INSURANCES (8)

PRIVATE BANKING

STATE BANKING

FOPEBA

26 COMPLEMENTARYFUNDS

MEMBERS BY MANAGING MEMBERS BY MANAGING INSTITUTIONINSTITUTION

MEMBERS BY MANAGING MEMBERS BY MANAGING INSTITUTIONINSTITUTION

NUMBER OF INDIVIDUALS UP TO DEC. 1995

ENTITIES

14.0002.552

12.5057.668

306.570306.698

MINIMUM AVERAGE MAXIMUMCONTRIBUTION RATES (*) 8,9 % 14,5 % 22 %

Employee 2,5 % 7,0 % 13,0 %

Employer 4,5 % 6,0 % 11,0 %

State 1,5 % 1,5 % 1,5 %

$US MILLIONS % GDP (*) COSSMIL IS NOT INCLUDED

Annual Pension Amount 250 3,6 %

Annual Contributions 205 3,0 %

Reserves 114 1,6 %

Deficit (NPV 96) 3.175

THE NEW DEFINED-CONTRIBUTION THE NEW DEFINED-CONTRIBUTION PENSION SYSTEMPENSION SYSTEM

CONTRIBUTIONSCONTRIBUTIONS

12.5%, WHICH INCLUDES:12.5%, WHICH INCLUDES:

Closed the old pension system

and

Established a new pension system based on individual capitalization accounts.

LAW 1732 ENACTED ON NOVEMBER 1996 :LAW 1732 ENACTED ON NOVEMBER 1996 :

AFFILIATIONAFFILIATION

All current contributors to the old pension system were automatically transferred to the individual capitalization system on May 1, 1997

to be deposited in each individual’s account. insurance premium. for the AFPs’.

10% 2% 0.5%

Corporations Established in Bolivia.1.000.000 SDRs. Infrastructure.

FUNDS ADMINISTRATION FUNDS ADMINISTRATION

GIVEN BY THE SUPERINTENDENCY

LICENSE

AFP CONSTITUTION

AFPAFP

PUBLIC INTERNATIONAL PUBLIC INTERNATIONAL BIDDINGBIDDING

CompetitiveCompetitiveTransparency Transparency Eficiency Eficiency

AFP

Separate Equity Prudent Investment Criteria Efficient Administration Quality Services

WHO MANAGES THE SYSTEM?WHO MANAGES THE SYSTEM?

MANAGEMENT

Individual Capitalization accounts and Collective Capitalization Fund managed by two private pension fund administrators (AFPs).

COMPETITION IN THE MAYOR CITIES PLANNED COMPETITION IN THE MAYOR CITIES PLANNED FOR JANUARY 1º, 2000.FOR JANUARY 1º, 2000.

La PazLa Paz

CochabambaCochabamba

Santa CruzSanta Cruz

El AltoEl Alto

Initially these AFPs share the market in the four major cities of the country.

and

Have regional monopolies in their area of exclusivity .

THE MARKET WILL OPEN TO NEW ENTRANTS.

IN MAY 2002IN MAY 2002

Instead of privatizing Bolivia held bidding for 50% of shares and management control of enterprises. Bidders bid amount to be invested in enterprise.

50% of shares of Government transferred to Bolivians older than 21 in 1995. Shares to be managed by AFP in Collective Capitalization Fund and used to pay old age benefit at age 65.

CAPITALIZATIONCAPITALIZATION

Strategic Partner Capital Injections by Enterprise(Millions US$)

Strategic Partner'sInvestment

Corani 58.80ENTEL 610.00Ferroviaria Andina 13.25Ferroviaria Oriental 25.85Guaracachi 47.13Lloyd Aéreo Boliviano 47.48Petrolera Andina 264.78Petrolera Chaco 306.67Transredes 263.50Valle Hermoso 33.92

Total 1,671.37Source: Pension Intendency

Enterprises Privatization

Transaction in markets authorized by the regulatory framework and the Pensions Superintendency.

Only in securities authorized by the Pension Law or Supreme Decree issued by the Executive.

Diversification requirements through limits by categories of assets according to their risk rating.

Limits by issuer and groups of issuers.

Limits for foreign investments established by the board of directors of the Central Bank, between 10 % and 50 % of the ICF.

INVESTMENTINVESTMENT

TRANSITION

Reduces the net present value of the Government Reduces the net present value of the Government liabilities .liabilities .

Gives a clear signal about the commitment to the Gives a clear signal about the commitment to the reform.reform.

Simplifies the process of reform.Simplifies the process of reform.

Is equitable among all sectors of the working Is equitable among all sectors of the working population.population.

Makes clear that the members are the owners of the Makes clear that the members are the owners of the resources in the system.resources in the system.

THE OLD PENSION SYSTEM CLOSES COMPLETELY AT THE START THE OLD PENSION SYSTEM CLOSES COMPLETELY AT THE START OF THE NEW PENSION SYSTEM. OF THE NEW PENSION SYSTEM.

BENEFITSBENEFITS

THE NEW SYSTEM INCORPORATES ALL WORKERS, WITHOUT THE NEW SYSTEM INCORPORATES ALL WORKERS, WITHOUT EXCEPTIONS FOR THE PRESIDENT, MILITARY, POLICE, OIL EXCEPTIONS FOR THE PRESIDENT, MILITARY, POLICE, OIL WORKERS, POLITICIANS, JUDICIARY ETC.WORKERS, POLITICIANS, JUDICIARY ETC.

% of GDP

US$ mn. (1996)

FINANCING REQUIREMENTSFINANCING REQUIREMENTSFINANCING REQUIREMENTSFINANCING REQUIREMENTS

ACTUAL FINANCING REQUIREMENTSACTUAL FINANCING REQUIREMENTS

YEARYEAR 19901990 19961996 19971997 19981998 19991999 20002000

% OF GDP % OF GDP 0.70.7 2.12.1 3.23.2 3.63.6 3.73.7 4.34.3

PLANNED FINANCING PLANNED FINANCING REQUIREMENTSREQUIREMENTS

YEARYEAR 19971997 19981998 19991999 20002000 20072007 20272027 20372037

2.5

170

4.1

289

3.9

285

3.3

252

1.33

134

0.86

141

0.18

72

THE OBJECTIVES FOR THE BIDDING PROCESS WERE TO ATTRACT A LARGE NUMBER OF REPUTABLE AND EXPERIENCED PENSION FUND MANAGERS, TO CREATE A COMPETITIVE PROCESS AND TO SELECT THE BEST POSSIBLE AFPs.

Asset AdministrationAsset Administration

At least US$10 billion in assets under management,At least US$10 billion in assets under management,

at least 20 years of portfolio management, and at least 20 years of portfolio management, and

at least 10 years of experience as an international at least 10 years of experience as an international portfolio investor.portfolio investor.

THE MAIN CRITERIA TO QUALIFY WERE:THE MAIN CRITERIA TO QUALIFY WERE:

SELECTION OF THE AFPsSELECTION OF THE AFPs

Records administration and Records administration and maintenancemaintenance

At least 100,000 accounts, and At least 100,000 accounts, and

5 million transactions a year.5 million transactions a year.

Experience in establishing new Experience in establishing new systemssystemsAt least 100,000 clients that did not have previous At least 100,000 clients that did not have previous experience with a retirement planexperience with a retirement plan

THE MAIN CRITERIA TO QUALIFY WERE:THE MAIN CRITERIA TO QUALIFY WERE:

SELECTION OF THE AFPsSELECTION OF THE AFPs

Argentaria (Spain) – Invesco (USA) – AFP Argentaria (Spain) – Invesco (USA) – AFP Magister (Chile)Magister (Chile)

•Banco Bilbao Vizcaya (Spain)Banco Bilbao Vizcaya (Spain)

•Citibank (USA)Citibank (USA)

•Dresdner Bank AG – Allianz AG Holding Dresdner Bank AG – Allianz AG Holding (Germany)(Germany)

•Franklin Templeton (USA) – AFP Provida (Chile)Franklin Templeton (USA) – AFP Provida (Chile)

•Goldman Sachs Assets Mgt. – Financial Goldman Sachs Assets Mgt. – Financial Administrative Services (USA)Administrative Services (USA)

•JP Morgan Asset Management (USA) – Aetna JP Morgan Asset Management (USA) – Aetna (USA) – AFP Santa María (Chile)(USA) – AFP Santa María (Chile)

•Morgan Stanley Asset Management (USA)- Morgan Stanley Asset Management (USA)- Cruz Blanca (Chile)Cruz Blanca (Chile)

•Swiss Bank Corp Brinson (Switzerland) – AON Swiss Bank Corp Brinson (Switzerland) – AON Consulting (USA)Consulting (USA)

COMPANIES THAT QUALIFIED WERE:COMPANIES THAT QUALIFIED WERE:

SELECTION OF THE AFPsSELECTION OF THE AFPs

SELECTION OF THE AFPsSELECTION OF THE AFPs

THE LOWEST BIDDER WAS ONE OF THE THE LOWEST BIDDER WAS ONE OF THE SELECTED AFP AND THE NEXT LOWEST SELECTED AFP AND THE NEXT LOWEST BIDDER THAT MATCHED THE LOWEST BID BIDDER THAT MATCHED THE LOWEST BID WAS THE SECOND SELECTED AFP.WAS THE SECOND SELECTED AFP.

Asset management fee

fee for benefits payment.

and

0.5% of the affiliates salary.

ECONOMIC BIDDING WAS ASSESSED ON ONE ECONOMIC BIDDING WAS ASSESSED ON ONE VARIABLE “AVERAGE MONTHLY VARIABLE “AVERAGE MONTHLY

MANAGEMENT FEE PER ACCOUNT”.MANAGEMENT FEE PER ACCOUNT”.AFPAFP

THIS FEE WAS A WEIGHTED AVERAGE OF:

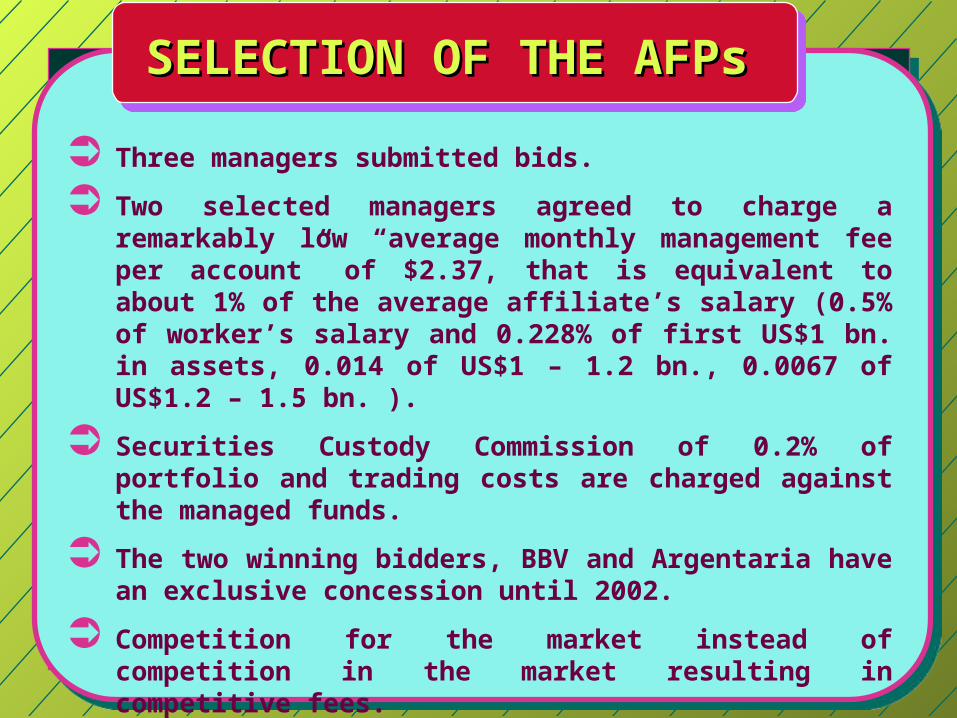

Three managers submitted bids.

Two selected managers agreed to charge a remarkably low “average monthly management fee per account” of $2.37, that is equivalent to about 1% of the average affiliate’s salary (0.5% of worker’s salary and 0.228% of first US$1 bn. in assets, 0.014 of US$1 – 1.2 bn., 0.0067 of US$1.2 – 1.5 bn. ).

Securities Custody Commission of 0.2% of portfolio and trading costs are charged against the managed funds.

The two winning bidders, BBV and Argentaria have an exclusive concession until 2002.

Competition for the market instead of competition in the market resulting in competitive fees.

Capitalization and pension assets that the AFP manages are kept by a global custodian.

SELECTION OF THE AFPsSELECTION OF THE AFPs

RESULTS

AFPs have 655,321 members (June 2001), of which 90% AFPs have 655,321 members (June 2001), of which 90% contribute, surpassing the targets set in the contract contribute, surpassing the targets set in the contract with the AFPs. with the AFPs. Of the 614,600 fully validated accounts Of the 614,600 fully validated accounts 229,605 are in the public sector and 355,605 in the 229,605 are in the public sector and 355,605 in the private sector. private sector.

Process to transfer disability and survivorship Process to transfer disability and survivorship insurance from AFPs to insurance companies has been insurance from AFPs to insurance companies has been launched and will be carried out through an launched and will be carried out through an international bidding process.international bidding process.

The Superintendency is operating and regulations are The Superintendency is operating and regulations are being issued and implemented.being issued and implemented.

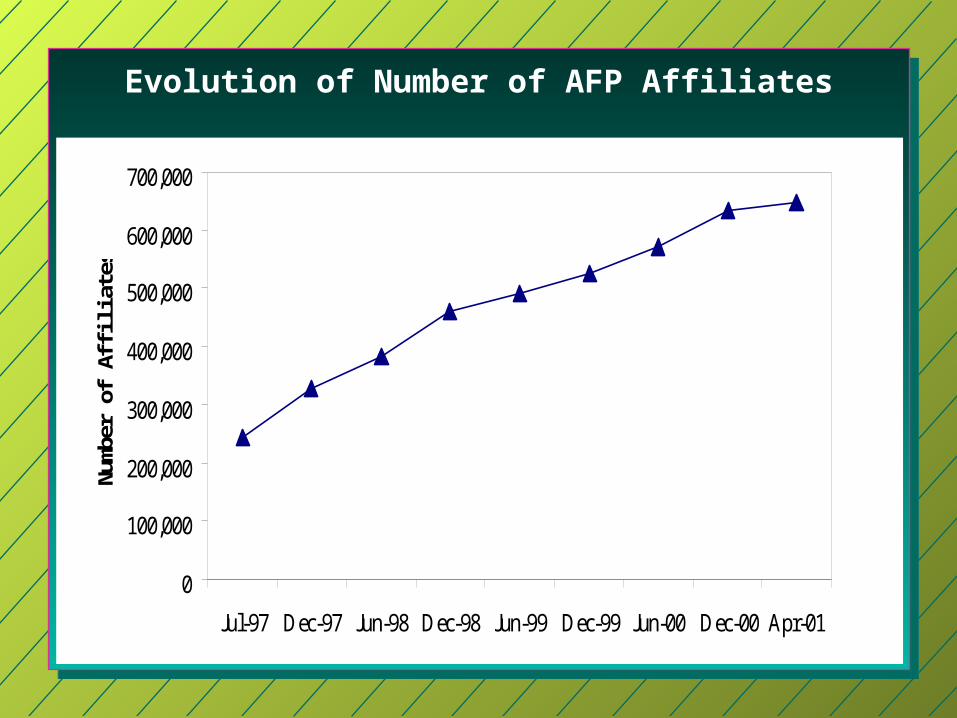

Evolution of Number of AFP Affiliates

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Jul-97 Dec-97 Jun-98 Dec-98 Jun-99 Dec-99 Jun-00 Dec-00 Apr-01

Nu

mbe

r of

Aff

ilia

tes

Number of Affiliates in each AFP, Jul. 1997-Apr. 2001

(as % of total affiliates)

0%

10%

20%

30%

40%

50%

60%Ju

l-97

Oct

-97

Jan-

98

Apr

-98

Jul-9

8

Oct

-98

Jan-

99

Apr

-99

Jul-9

9

Oct

-99

Jan-

00

Apr

-00

Jul-0

0

Oct

-00

Jan-

01

Apr

-01

Aff

ilia

ted P

erce

nta

ge

PFA Futuro de Bolivia

PFA Previsión BBV

RESULTS

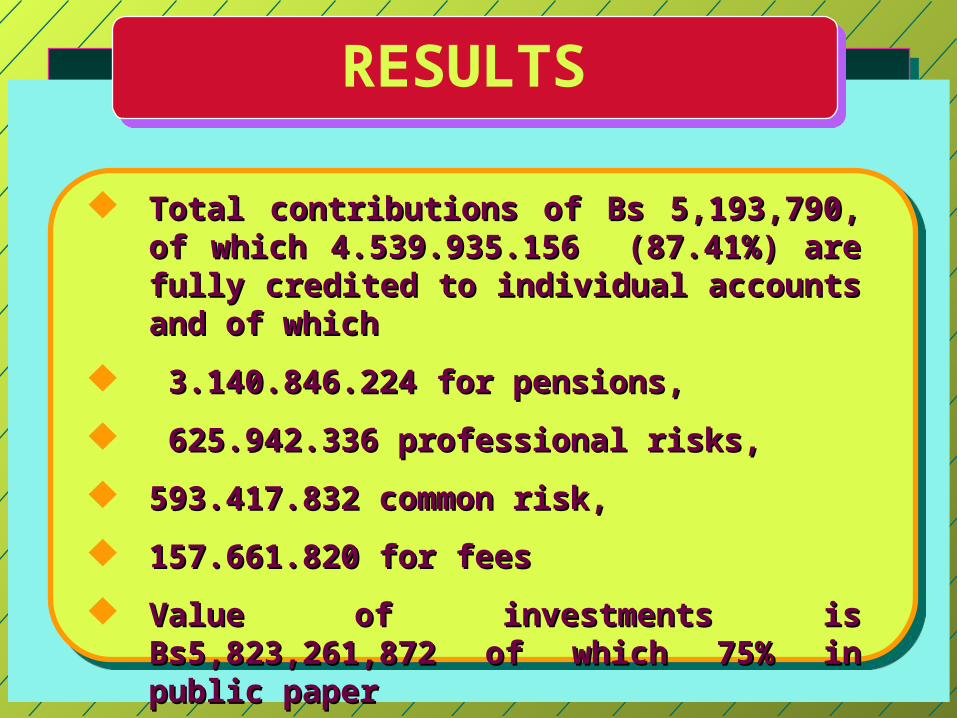

Total contributions of Bs 5,193,790, of which Total contributions of Bs 5,193,790, of which 4.539.935.1564.539.935.156 (87.41%) are fully credited to (87.41%) are fully credited to individual accounts and of whichindividual accounts and of which

3.140.846.224 for pensions,3.140.846.224 for pensions,

625.942.336 professional risks, 625.942.336 professional risks,

593.417.832 common risk, 593.417.832 common risk,

157.661.820 for fees157.661.820 for fees

Value of investments is Bs5,823,261,872 of Value of investments is Bs5,823,261,872 of which 75% in public paperwhich 75% in public paper

Fund Value by AFP, June 1997-April 2001 (in Millions $US)

0

100

200

300

400

500

600

700

800

900

1,000

Mil

lion

US

$

PFA Previsión BBV

PFA Futuro de Bolivia

Total PFA

PORTFOLIO

Instrum. Book Value

US$ mn

Yieldin %

Matur.in days

MarketValue

Days to maturity

Shareportfolio

Treasury Bonds

(3)

573 8.0 5,504 602 2,962 63.32

Treasury Bonds

(2)

75 8.34 1,211 76 848 7.98

Bonds 60 10.7 2,898 60 1478 6.39

CD w/o coupons

96 8.69 595 106 268 11.11

CD with coupons

54 9.84 904 57 408 5.99

Liquid 43 43 4.48

Total 908 951 100

Profits per Affiliate (in $US)

Year Year Year Year1997 1998 1999 2000

PFA Futuro de Bolivia -6.40 0.74 0.29 4.43

PFA Previsión BBV -3.18 2.99 -1.00 1.47

Total PFA -4.80 1.96 -0.38 2.88

Source: PFA Futuro de Bolivia and PFA Previsión BBV

Detail

THE CONTRACT

The contract is what the companies are really The contract is what the companies are really bidding about. It is important to envision bidding about. It is important to envision contingencies. In competition within the contingencies. In competition within the market there is more flexibility to address market there is more flexibility to address contingencies. In a bidding the country Is contingencies. In a bidding the country Is bound by the terms of the contract.bound by the terms of the contract.

What happens when the contract comes to an What happens when the contract comes to an end? How do you select the new managers? end? How do you select the new managers?

Dispute resolution mechanisms.Dispute resolution mechanisms.

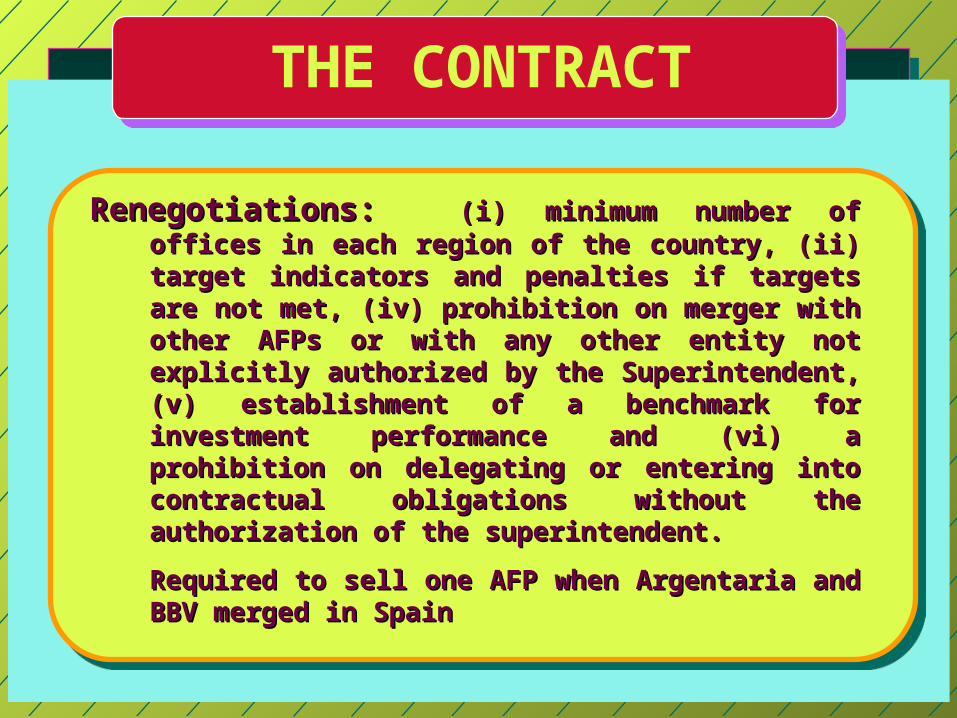

THE CONTRACT

Renegotiations: Renegotiations: (i) minimum number of offices in (i) minimum number of offices in each region of the country, (ii) target each region of the country, (ii) target indicators and penalties if targets are not met, indicators and penalties if targets are not met, (iv) prohibition on merger with other AFPs or (iv) prohibition on merger with other AFPs or with any other entity not explicitly authorized with any other entity not explicitly authorized by the Superintendent, (v) establishment of a by the Superintendent, (v) establishment of a benchmark for investment performance and benchmark for investment performance and (vi) a prohibition on delegating or entering (vi) a prohibition on delegating or entering into contractual obligations without the into contractual obligations without the authorization of the superintendent.authorization of the superintendent.

Required to sell one AFP when Argentaria and Required to sell one AFP when Argentaria and BBV merged in SpainBBV merged in Spain