board matters quarterly - ey matters quarterly | june 2015 4 our comments the aml/ cft legislations...

TRANSCRIPT

Issue 24, June 2015 | Singapore

01ISCA’s Ethics Pronouncementon anti-money laundering andcountering the financing ofterrorism

How it affects you

Board MattersQuarterly

05Two-phaseImplementation ofCompanies(Amendment) Act 2014

16Asia – Pacific FraudSurvey 2015

Fraud and corruption− driving awaytalent?

EditorialInternationally, there are increasing calls for professional accountants to adopt measures that are atleast up to the international standards recommended by the Financial Action Task Force (FATF), theglobal standard-setter for anti-money laundering and countering the financing of terrorism. As a memberof the FATF since 1992, Singapore is obliged to comply with the "International Standards on CombatingMoney Laundering and the Financing of Terrorism & Proliferation" issued by the FATF (FATFRecommendations). In response, the Institute of Singapore Chartered Accountants has issued the EP 200Anti-Money Laundering and Countering the Financing of Terrorism − Requirements and Guidelines forProfessional Accountants in Singapore which is benchmarked against the latest FATF Recommendations.Effective May 2015, all professional firms shall have in place systems and controls to address moneylaundering and terrorist financing concerns. We look at how this will affect the entities.

The Companies (Amendment) Bill was passed by Parliament in October 2014. On 15 April 2015,Accounting and Corporate Regulatory Authority announced that the legislative changes to the CompaniesAct will be effected in two phases. About 40% of the over 200 legislative amendments will take effect inthe first phase on 1 July 2015. The second phase encompassing the rest of the legislative amendments isexpected to come into effect in the first quarter of 2016. We highlight the selected key legislativeamendments to be implemented in each phase.

Our Asia−Pacific Fraud Survey 2015 found that almost eight in 10 respondents said they are unwilling towork for companies involved in bribery and corruption. About seven in 10 respondents, in Singapore andthe region, said that having a strong reputation for ethical behaviour is a commercial advantage. We lookat some of the key findings of the survey.

We hope you find Board Matters Quarterly useful, and share it with others. If you have feedback or ideasfor future issues, please contact us at [email protected].

Tan Seng ChoonPartner | Assurance | Professional Practice

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | June 2015 1

Section or Chapter title

All Rights Reserved – [Insert local EY firm Name] Board Matters Quarterly | June 2015 2

ISCA’s Ethics Pronouncement on Anti-Money Launderingand Countering the Financing of Terrorism

How it affects youWith money laundering andterrorist financing activitiesbecoming increasinglysophisticated, expectations onprofessional accountants todetect money laundering andterrorism financing are rising.Internationally, there areincreasing calls forprofessional accountants toadopt measures that are atleast up to the internationalstandards recommended bythe Financial Action Task Force(FATF), the global standard-setter for anti-moneylaundering and countering thefinancing of terrorism(AML/CFT).As a member of the FATF since1992, Singapore is obliged tocomply with the "InternationalStandards on CombatingMoney Laundering and theFinancing of Terrorism &Proliferation" issued by theFATF (FATFRecommendations).In response, the Institute ofSingapore CharteredAccountants (ISCA) has issuedthe EP 200 Anti-MoneyLaundering and Countering theFinancing of Terrorism −Requirements and Guidelines

for Professional Accountants inSingapore which isbenchmarked against the latestFATF Recommendations, andapplicable to professionalaccountants − including publicaccountants and professionalaccountants in business, andaccounting entities.Effective May 2015, allprofessional firms should havein place systems and controlsto address money launderingand terrorist financingconcerns.

Customer DueDiligence (CDD) – Whatyou need to knowAn important element in anyeffective anti-moneylaundering and the counteringthe financing of terrorismmeasure is CDD.The EP 200 requiresprofessional accountants toapply CDD when establishingand during the course of an on-going relationship with a client.The primary objective of CDD isto enable professionalaccountants to truly know theirclients well enough tounderstand and anticipate thatclient’s business behaviour so

that the professionalaccountants may effectivelydistinguish unusual andpossibly suspicious activityfrom usual and customarybehaviour.

What are the CDDmeasuresThe CDD measures generallyinclude:► Identifying the client and its

beneficial owners► Verifying the identity of the

client and its beneficialowners using reliable,independent sourceinformation

► Understand the purpose andthe intended nature of thebusiness relationship

► Conducting ongoing duediligence on any continuingbusiness relationship andscrutiny of transactionsundertaken during thecourse of the relationship

Section or Chapter title

Board Matters Quarterly | June 2015 3

How CDD affects you?With the implementation of EP 200, professional accountants are required by law to make enquiries andobtain certain information regarding the identities of their clients and the clients’ beneficial owners.

Where a professional accountant is unable to carry out the CDD measures, for example, due to a client's refusalto provide information, business relations may not be commenced or may have to be terminated.

The information usually obtained when we conduct CDD is as follows:

Identification and verification of client’sidentity

Name, legal form and proof of existence:

► Certificate of incorporation,

► Certificate of good standing,

► Partnership agreement,

► Deed of trust, or

► Other appropriate documentation from areliable independent source.

The powers that regulate and bind the legalperson or arrangement:

► Memorandum and articles of association, and

► Names of the relevant persons having a seniormanagement position in the legal person orarrangement.

The address of the registered office and, ifdifferent, a principal place of business.

Identification and verification of beneficialowner’s identity

For legal persons (in the following order):

► The identity of the natural persons whoultimately have a controlling ownershipinterest in a legal person,

► The identity of the natural persons (if any)exercising control of the legal person orarrangement through other means, or

► The relevant natural person who holds theposition of senior managing official.

For legal arrangements:

Trusts − The identity of the settlor, the trustee(s),the protector (if any), the beneficiaries, and anyother natural person exercising ultimate effectivecontrol over the trust (including through a chainof control/ ownership).

Other types of legal arrangements: the identity ofpersons in equivalent of similar positions.

The address of the registered office and, ifdifferent, a principal place of business.

Board Matters Quarterly | June 2015 4

Our comments

The AML/ CFT legislations in Singapore provide a framework for discouraging money laundering andterrorist financing by establishing criminal sanctions for such activities and requiring the reporting of suspicioustransactions to the authorities.

These legislations have implications on the responsibilities of various parties, including the risk of criminalliability on non-compliance.

It is important that you understand the implications of AML/ CFT legislations, the important steps the variousparties have to take to comply with the law, and the enquiries to be made.

The information that you provide will be subject to the same standard of confidentiality as any other clients’information we hold.

Board Matters Quarterly | June 2015 5

Board Matters Quarterly | June 2015 6

Two-phase Implementationof Companies(Amendment) Act 2014

he Companies (Amendment) Bill waspassed by Parliament in October 2014.On 15 April 2015, the Accounting andCorporate Regulatory Authority (ACRA)announced that the legislative changesto the Companies Act (the Act) will beeffected in two phases.

About 40% of over 200 legislativeamendments will take effect in the firstphase beginning on and from 1 July2015. The second phase encompassingthe rest of the legislative amendments isexpected to come into effect in the firstquarter of 2016.

The details of selected key legislativeamendments to be implemented in eachphase are listed in the following pages.

Board Matters Quarterly | June 2015 7

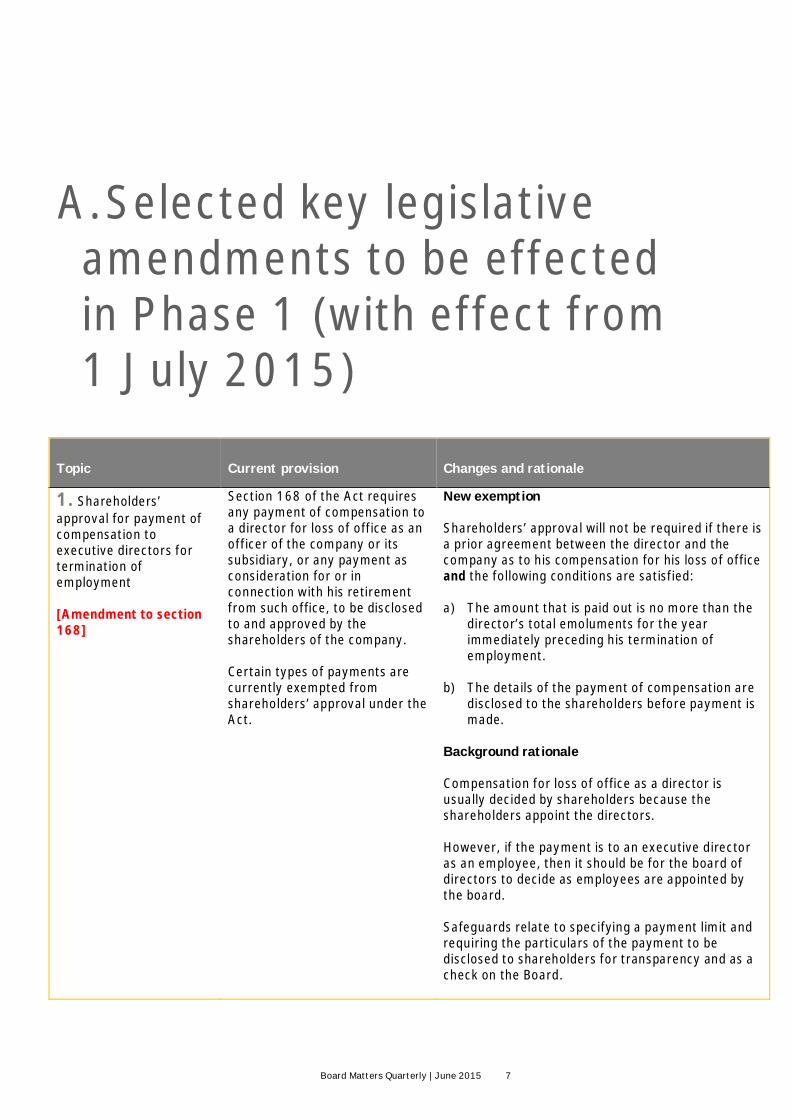

A.Selected key legislativeamendments to be effectedin Phase 1 (with effect from1 July 2015)

Topic Current provision Changes and rationale

1. Shareholders’approval for payment ofcompensation toexecutive directors fortermination ofemployment

[Amendment to section168]

Section 168 of the Act requiresany payment of compensation toa director for loss of office as anofficer of the company or itssubsidiary, or any payment asconsideration for or inconnection with his retirementfrom such office, to be disclosedto and approved by theshareholders of the company.

Certain types of payments arecurrently exempted fromshareholders’ approval under theAct.

New exemption

Shareholders’ approval will not be required if there isa prior agreement between the director and thecompany as to his compensation for his loss of officeand the following conditions are satisfied:

a) The amount that is paid out is no more than thedirector’s total emoluments for the yearimmediately preceding his termination ofemployment.

b) The details of the payment of compensation aredisclosed to the shareholders before payment ismade.

Background rationale

Compensation for loss of office as a director isusually decided by shareholders because theshareholders appoint the directors.

However, if the payment is to an executive directoras an employee, then it should be for the board ofdirectors to decide as employees are appointed bythe board.

Safeguards relate to specifying a payment limit andrequiring the particulars of the payment to bedisclosed to shareholders for transparency and as acheck on the Board.

Board Matters Quarterly | June 2015 8

Topic Current provision Changes and rationale

2. Allowing listedcompanies to makeselected off-marketacquisition of shares initself in accordance withan agreement authorizedby the company

[Amendment to section76D(1)]

Section 76D(1)(b) of the Actprohibits listed companies frommaking selective off-marketacquisitions.

This prohibition will be removed.

3. Financial assistance

[Amendment to section76]

Pursuant to Section 76 of theAct, a company may not givefinancial assistance to anyperson (whether directly orindirectly) for the acquisition orproposed acquisition of shares orunits of shares in the company orholding company.

The prohibition against the giving of financialassistance will no longer apply to private companiesand will only apply to public companies or companieswhose ultimate holding company is a publiccompany.

Background rationale

Private companies are usually closely held andshareholders have greater control over the decisionto give financial assistance.

To clarify/ address concerns that the presentfinancial assistance prohibition may impedepotentially beneficial or innocuous transactions, thefollowing new exceptions will be introduced for apublic company or a subsidiary of a publiccompany:

a. Where the giving of assistance does notmaterially prejudice interests of company orshareholders or company’s ability to pay itscreditors (subject to the company satisfyingcertain prescribed conditions);

b. Distributions made in the course of thecompany’s winding up;

c. Allotment of bonus shares;

d. Redemption of redeemable shares of a companyin accordance with its constitution.

On safeguards to protect the interests ofshareholders and creditors, refer to Implementationof Companies (Amendment) Act 2014 – FrequentlyAsked Questions.

Board Matters Quarterly | June 2015 9

Topic Current provision Changes and rationale

4. Use of share capitalfor share issuanceexpenses, brokerage orcommissions, and issue ofshares by companies forno consideration

[New sections 67, 68]

NA A company may use its share capital to pay forexpenses (including brokerage or commission)incurred directly in the issue of new shares. Suchpayments made shall not be taken as reducing theamount of share capital of the company.

A company having a share capital may issue sharesfor which no consideration is payable to the issuingcompany.

5. Introduction of smallcompany audit exemption

[New section 205C andThirteenth Schedule]

An exempt private company withannual revenue of $5m or lessfor the financial year is exemptfrom auditing its financialstatements.

An exempt private company is acompany which has not morethan 20 members and in whichno corporation holds anybeneficial interest in its shares.

The audit exemption will now apply only to a “smallcompany”, applicable for financial years beginningon or after the change in the law i.e., 1 Jul 2015. Acompany qualifies as a small company if:

a. it is a private company in the financial year inquestion; and

b. it meets at least two of the following criteria fortwo consecutive financial years preceding thefinancial year in question:

i. total revenue for each financial year≤$10m;

ii. total assets at the end of each financialyear ≤ $10m;

iii. no. of employees at the end of eachfinancial year ≤ 50.

If a small company is part of a group of companies,the group must be a “small group” in order for thesmall company to qualify for the exemption. A smallgroup must meet at least two of the followingcriteria in each of the two consecutive financialyears preceding the financial year:

a) Consolidated revenue of the group for eachfinancial year ≤ $10 million

b) Value of the consolidated total assets of thegroup at the end of each financial year ≤$10 million

c) Aggregate number of employees of thegroup at the end of each financial year ≤ 50

Background rationale

It would reduce regulatory costs for smallercompanies that do not have wide market impact.

For further details on these amendments, refer toImplementation of Companies (Amendment) Act2014 – Frequently Asked Questions.

Board Matters Quarterly | June 2015 10

Topic Current provision Changes and rationale

6. Resignation ofauditors from non-publicinterest companies andpublic interest companies

[New sections 205AA to205AF]

An auditor may resign if he is notthe sole auditor of a company,or, where he is the sole auditor,at a general meeting where areplacement auditor isappointed.

An auditor of a non-public interest company (otherthan a subsidiary of a public interest company) mayresign before the end of the term of his appointmentby giving written notice to the company.

Auditors of public interest companies and theirsubsidiaries will be required to obtain ACRA’sconsent if they wish to resign before the end of theterm of their appointment. Examples of publicinterest companies are companies listed on theSingapore Exchange, financial institutions, and largecharities or institutions of public character.

Background rationale

This amendment intends to ensure that companiesare not unfairly left in the lurch without theirauditors but yet also allow auditors to resign insituations where the company refuses to hold ageneral meeting to appoint a replacement auditor.The requirement for ACRA’s consent will allow ACRAto stop the resignation if it is in the public interest todo so.

For further details on the requirement for auditors ofpublic interest companies and their subsidiaries toobtain ACRA’s consent for premature resignation,please refer to Implementation of Companies(Amendment) Act 2014 – Frequently AskedQuestions.

7. Requirement foralignment of financialyears of holdingcompanies and theirsubsidiaries

Pursuant to Section 200 of theAct, holding companies and theirsubsidiaries are required to havefinancial years that coincide.

This section has been repealed.

Board Matters Quarterly | June 2015 11

Topic Current provision Changes and rationale

8. Abolition oftransitional arrangementsfor share warrants

[Amendment to section66]

The bearer of a share warrantissued before 29 December1967 is entitled, on hissurrender of the warrant forcancellation to have his nameentered into the company’sregister of members.

Bearers of share warrants will be given a two-yearperiod, from the time the amendment is effected, tosurrender the warrants for cancellation and havetheir names entered in the register of members.Companies will cancel any outstanding sharewarrants that are not surrendered.

Background rationale

This transitional arrangement has been in place formore than 40 years. It was put in place for bearersof share warrants issued before 29 December 1967to convert the warrants to registered shares. Thisamendment is intended to addresses the growinginternational expectations to strengthentransparency of companies.

9. Limits on preferentialpayments to employeesof insolvent companies

[Amendment to section328]

Employees of an insolventcompany are currently entitledto be paid their wages andsalaries, followed by anyretrenchment benefits and ex-gratia payments, ahead of otherunsecured creditors. The limit inthe Act on such prioritypayments is “five months’ salaryof the employee or $7,500,whichever is lower”.

The limit will be changed to “five months’ salary orfive times the salary cap for non-workmen referredto in Part IV of the Employment Act, whichever islower”.

Background rationale

The $7,500 limit is based on the monthly salary capof $1,500 for non-workmen under the EmploymentAct in 1993 more than two decades ago. Thisapproach has the benefit of ensuring that the limitwill be automatically updated each time the salarycap for non-workmen is adjusted in the EmploymentAct.

The list of amendments to the Act to be effected from 1 July 2015 can be found here.

Board Matters Quarterly | June 2015 12

B.Selected key legislativeamendments to be effected inPhase 2 (with effect from Q12016)

Topic Current provision Changes and rationale

1. Requirement forshareholders’approval to re-appoint directorsaged 70 and above

[Repeal of section153]

Approval from shareholdersmust be sought for theappointment of person who is70 years old and above asdirector of a public company orsubsidiary of a public company.

This requirement will be repealed.

Background rationale

A person’s ability to act as a director of a company isnot principally determined by his age and other factorsshould be taken into account.

Today, persons of or above 70 years of age can becapable of doing the job of a director, and are oftenre−appointed in practice.

2. Loans to directors

[Amendment tosection 162

Section 162 currently prohibitsa company from making a loanto or giving a security orguarantee to a director.

The restrictions on companies providing loans orguarantees or security for any loans to their directorshave been extended to include quasi-loans and credittransactions.

3. Directors’disclosurerequirements to beextended to ChiefExecutive Officers

[Amendment tosection 156]

Directors are required todisclose:

(a) Conflict of interests intransactions

(b) Shareholdings in companyand related corporations

Such disclosure requirements will be extended to CEOsof companies.

Background rationale

CEOs play an increasingly important role in companydecisions making. This change is consistent with theapproach already adopted for listed companies underthe Securities and Futures Act which similar disclosuresby both directors and CEOs are already required.

Board Matters Quarterly | June 2015 13

Topic Current provision Changes and rationale

4. Power ofRegistrar to debardirectors andsecretaries

[New section155B]

NA a. The Registrar will be empowered to debar anydirector or secretary of a company if thecompany is in default of certain filingrequirements under the Act.

b. A debarred person cannot take on any newappointments as a director or companysecretary. However, he may continue with hisexisting appointments.

The Registrar may, upon application of the personagainst whom the debarment order was made, liftthe debarment when the default has been rectifiedor on other prescribed grounds, subject to anyconditions the Registrar may prescribe.

Background rationale

This is intended to prevent irresponsible directorsand company secretaries from holding similarpositions in other companies, and promote greatercompliance with filing requirements.

5. Appointment ofproxies

[Amendment tosection 181]

Unless the articles of a companyprovide otherwise, a member of acompany can only appoint up to 2proxies to attend a general meetingand such proxies can only vote on apoll.

Specified intermediaries, such as banks and capitalmarkets services licence holders that providecustodial services, may appoint more than twoproxies who may attend, speak and vote on a showof hands at meetings but each proxy must onlyexercise the rights attached to a different share orshares held by him.

Background rationale

The amendment was intended to:

► Facilitates indirect investors attending andvoting at shareholders’ meetings as proxies.

► Enhances corporate governance andencourages more active shareholderparticipation.

► Longer cut-off time allow the companies morelead time to process proxy submissions andhandle administrative matters.

Board Matters Quarterly | June 2015 14

Topic Current provision Changes and rationale

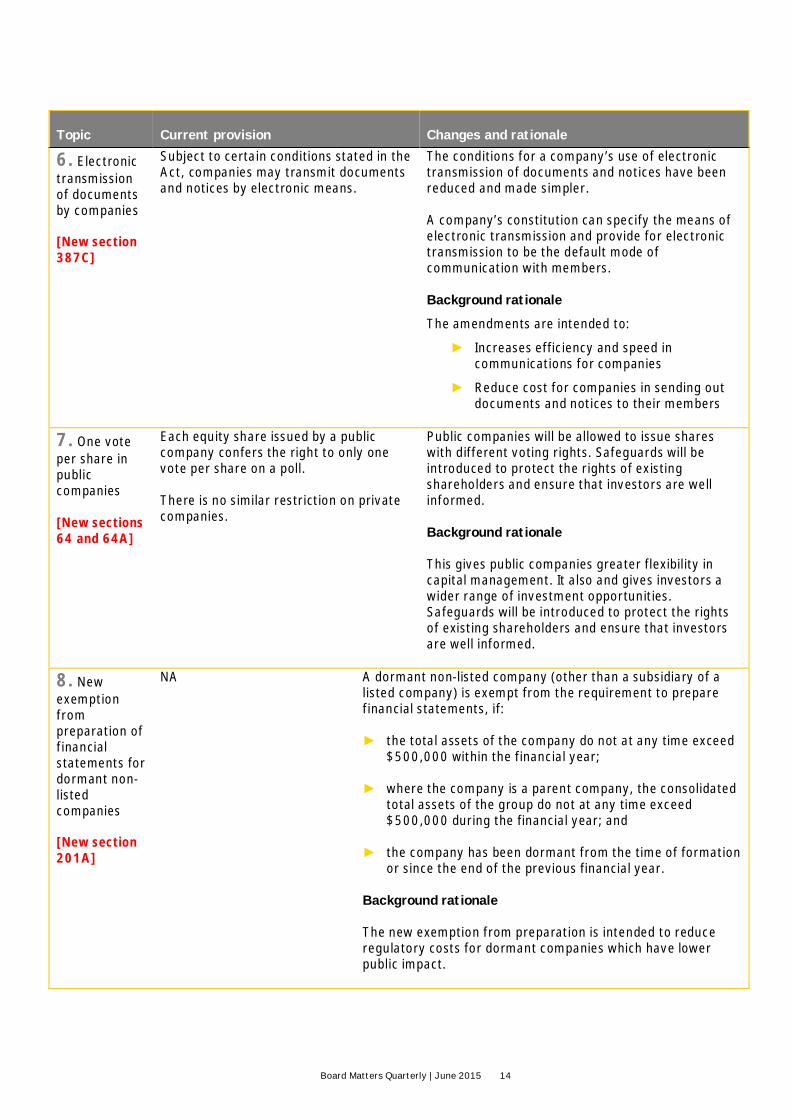

6. Electronictransmissionof documentsby companies

[New section387C]

Subject to certain conditions stated in theAct, companies may transmit documentsand notices by electronic means.

The conditions for a company’s use of electronictransmission of documents and notices have beenreduced and made simpler.

A company’s constitution can specify the means ofelectronic transmission and provide for electronictransmission to be the default mode ofcommunication with members.

Background rationale

The amendments are intended to:

► Increases efficiency and speed incommunications for companies

► Reduce cost for companies in sending outdocuments and notices to their members

7. One voteper share inpubliccompanies

[New sections64 and 64A]

Each equity share issued by a publiccompany confers the right to only onevote per share on a poll.

There is no similar restriction on privatecompanies.

Public companies will be allowed to issue shareswith different voting rights. Safeguards will beintroduced to protect the rights of existingshareholders and ensure that investors are wellinformed.

Background rationale

This gives public companies greater flexibility incapital management. It also and gives investors awider range of investment opportunities.Safeguards will be introduced to protect the rightsof existing shareholders and ensure that investorsare well informed.

8. Newexemptionfrompreparation offinancialstatements fordormant non-listedcompanies

[New section201A]

NA A dormant non-listed company (other than a subsidiary of alisted company) is exempt from the requirement to preparefinancial statements, if:

► the total assets of the company do not at any time exceed$500,000 within the financial year;

► where the company is a parent company, the consolidatedtotal assets of the group do not at any time exceed$500,000 during the financial year; and

► the company has been dormant from the time of formationor since the end of the previous financial year.

Background rationale

The new exemption from preparation is intended to reduceregulatory costs for dormant companies which have lowerpublic impact.

Board Matters Quarterly | June 2015 15

Topic Current provision Changes and rationale

9. Certain amendments relating to foreign companies will also be introduced. These include:

► The introduction of three additional grounds where the Registrar may strike off a foreign company► A new requirement for a foreign company to file with the Registrar similar components of its financial

statements similar as to those expected of a Singapore-incorporated company

Please refer to Board Matters Quarterly Issue 22 December 2014 for more details on the changes relating toforeign companies.

If in doubt, directors of the company should seek professional advice to better understand the changes broughtabout by the amendments, and its impact on the company and how directors should discharge its duties.

Board Matters Quarterly | June 2015 16

Board Matters Quarterly | June 2015 17

Asia – Pacific Fraud Survey 2015

Fraud and corruption –driving away talent?Across Asia Pacific, compliance has never been more challenging − or moreimportant − with 8 out of 10 respondents saying they would be unwilling to workfor companies involved in bribery and corruption, according to the Asia- Pacific

by EY. In this environment, ensuring that companies haveFraud Survey 2015high ethical standards and use technology proactively to prevent and detectfraud, bribery and corruption will be key to both retain quality talent and makecompliance programs more sustainable.

Board Matters Quarterly | June 2015 18

Board Matters Quarterly | June 2015 18

Compliance becomes increasinglydemanding

Respondents report business success is beingchallenged by increasing regulation and slower thanexpected economic growth. Half say stronger localanti-corruption enforcement is a major challenge.

These expanding regulatory demands are requiringcompanies operating in APAC to look at increasingnumbers of financial transactions and relationships ingreater depth. And they need to do so with limitedcompliance resources.

This sentiment is particularly notable in Indonesia,Thailand and China, reflecting strong anti-corruptionstances from the governments in these countries.

At the same time the talent pool for qualifiedcompliance professionals is limited. Discussions withheads of compliance in various industries indicatethat teams across APAC are finding it hard to recruitand retain compliance professionals.

Ethics are vital in the war for talent

Running an ethical business is now central toattracting and retaining top talent. Mostrespondents say they would be unwilling to work forcompanies involved in bribery and corruption.

Board Matters Quarterly | June 2015 19

Internal controls, policies andprocedures are not always workingCodes of conduct are not being followed andwhistleblower programs are either missing orunderused.

Of particular concern is the finding that thepercentage of respondents prepared to use theircompany’s whistleblower hotline has droppeddramatically since the survey in 2013 (from 81% to53%).

Risk is building up all along the valuechainMany respondents do not grasp the extent of thefraud, bribery and corruption risk posed by thirdparties. Nor do they fully understand theirresponsibilities when it comes to economic and tradesanctions.

The survey found that more than half (56%) of therespondents think third parties (joint venturepartners, distributors, agents and vendors) are a riskto their business in relation to ABAC compliance. But72% of respondents are confident that theirorganization is effectively managing the fraud,bribery and corruption risks associated with thesethird parties.

This confidence is misplaced given the legal andreputational exposure it creates, as evidenced by thecontinuing focus by regulators on the part thirdparties often play in bribery and corruption scandals.Companies entering into a business relationship witha third party should conduct as much due diligence asan acquisition and should also extend their ethicalframework to monitoring third-party behaviour.

Cyber threats underestimatedThe potential impact of cybercrime requires thatcybersecurity be viewed as a business risk, ratherthan merely an IT issue. Fundamentally, because acyber-attack may affect business operations, financialstatements and legal exposure, its reputation is onthe line.

While many businesses have increased their focus oncybersecurity, their efforts have been primarily onprotecting their information by preventing breaches.Unfortunately, the current threat environment is suchthat it is only a matter of time before all businesseswill suffer a major cyber breach.

Given our survey’s findings, APAC companies need toput in place:

Strong ethical leadershipCompliance starts at the top. Leadership mustengage proactively in compliance activities, anddemonstrate and communicate about ethicalbehaviour.

Strong, effective ethics policies andguidelinesSimply having Anti-Bribery/ Anti-Corruption (ABAC)policies and codes of conduct is not enough – thesepolicies must also lead to behavioural change.Turning policies into reality comes down to relevance.Employees need to understand what is required ofthem – and believe it is important.

Starting points include translating codes of conductinto local languages and using local examples duringABAC training. Global organizations should be opento feedback from local offices on the challenges ofdealing with changes to policies and procedures.

Board Matters Quarterly | June 2015 20

Third-party due diligenceGiven the vast majority of reported US ForeignCorrupt Practices Act (FCPA) cases involves thirdparty intermediaries, APAC organizations need toimprove their due diligence and monitoring of all thirdparties.

Companies also need to be aware of fraud, briberyand corruption risks in relation to transactions. Thoseinvolved in M&A need to make sure the rightquestions are asked and diligence is targeted on theright areas.

Big data and forensic data analyticsAPAC organizations should leverage FDA to improvetheir ability to identify transactions that may indicatethe presence of fraud, bribery and corruption, andmake their in-house compliance resources moreefficient and effective.

FDA integrates statistical analysis, anomalydetection, data visualization and text mining toidentify unusual transactions.

Whistleblower hotlinesEvery company needs a whistleblower hotline as partof a broader fraud, bribery and corruption riskmanagement framework. However, implementing ahotline is not enough. Employees must also beconfident that their reports will be dealt with in atransparent and confidential manner — and those theywill be protected from retaliation.

What’s expected and what it takes

Overall, the 2015 survey results deliver a strongmessage of support for those performingcompliance-related roles. There are severalexamples of leading practice – such as theusefulness of anti-bribery training. Regulators,consumers and other external stakeholders expectmore than just the basics. What is expected is aneffective and sustainable integrity and complianceprogram underpinned by a culture of ethicalbusiness behaviour.

Creating this requires significant investment. Theresponses from financial services organizationsshow how that investment can move the dial in theright direction, but respondents in these businessesalso know how much effort has been required toachieve this.

For boards and shareholders, the message is clear:good compliance is not a barrier to growth. Nor is itoptional. In the current environment, it is a criticalcomponent to sustain success for the organization,its employees and shareholders.

About the survey

Between 5 and 23 February 2015, our researchers— the global market research agency Ipsos —conducted 1,508 online or in-person interviews withemployees of large companies in 14 APACterritories.

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction andadvisory services. The insights and quality services wedeliver help build trust and confidence in the capitalmarkets and in economies the world over. We developoutstanding leaders who team to deliver on ourpromises to all of our stakeholders. In so doing, we playa critical role in building a better working world for ourpeople, for our clients and for our communities.

EY refers to the global organization, and may refer to oneor more, of the member firms of Ernst & Young GlobalLimited, each of which is a separate legal entity.Ernst & Young Global Limited, a UK company limitedby guarantee, does not provide services to clients.For more information about our organization,please visit ey.com.

© 2015 Ernst & Young LLP.

All Rights Reserved.

APAC no. 12000501

ED None

Ernst & Young LLP (UEN T08LL0859H) is a limited liability partnershipregistered in Singapore under the Limited Liability Partnerships Act (Chapter 163A).

This material has been prepared for general informational purposes onlyand is not intended to be relied upon as accounting, tax, or otherprofessional advice. Please refer to your advisors for specific advice.

www.ey.com