blx corporate presentation 3 q16 english

TRANSCRIPT

Color

Scheme

234 93 46

109 179 63

235 235 235

0 75 141

253 185 36

Accent

Color

Corporate Presentation As of September 30, 2016

31 179 179

192 0 0

Disclaimer

“This presentation contains forward-looking statements. These statements are made under the “safe harbor” provisions

established by the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements involve inherent risks

and uncertainties. The forward-looking statements in this presentation reflect the expectations of the Bank’s management

and are based on currently available data; however, actual experience with respect to these factors is subject to future

events and uncertainties, which could materially impact the Bank’s expectations. A number of factors could cause actual

performance and results to differ materially from those contained in any forward-looking statement, including but not limited

to the following: the anticipated growth of the Bank’s credit portfolio, including its trade finance portfolio; the continuation of

the Bank’s preferred creditor status; the impact of increasing interest rates and of improving macroeconomic environment in

the Region on the Bank’s financial condition; the execution of the Bank’s strategies and initiatives, including its revenue

diversification strategy; the adequacy of the Bank’s allowance for credit losses; the need for additional provisions for credit

losses; the volatility of the Bank’s Treasury trading revenues; the Bank’s ability to achieve future growth and increase its

number of clients, the Bank’s ability to reduce its liquidity levels and increase its leverage; the Bank’s ability to maintain its

investment-grade credit ratings; the availability and mix of future sources of funding for the Bank’s lending operations;

potential trading losses; existing and future governmental banking and tax regulations; the possibility of fraud; and the

adequacy of the Bank’s sources of liquidity to replace large deposit withdrawals.”

2

A Leading Franchise with a Solid Track Record

The Latin America Trade Finance Bank Key Financial Highlights

Remarkable Trajectory: + 36 years of Success

Bladex is the Latin American Trade Finance Bank, providing integrated

financial solutions across Latin America‟s foreign trade value chain

First Latin American bank to be listed on the NYSE and to be rated

Investment Grade (both in 1992)

Currently rated Baa2 / BBB / BBB+

Class “A” shareholders (Central Banks or designees from 23

Latin America (“LatAm”) countries) provide substantial support

and represent a direct link between the Bank and the governments

of Latin America

Multi-national DNA embedded in its regional presence, ownership

structure, management and organizational culture

Current Credit Ratings

FY’15 YoY

(%)

YTD’16 YoY

(%)

Profit for the period (mm): $104.0 +2% $73.7 -9%

Net Interest Income (mm): $145.5 +3% $117.5 +9%

Return on Average Equity: 11.0% 10.0%

Gross Loans (mm): $6,692 +0.1% $6,393 -5%

Total Assets (mm): $8,286 +3% $7,287 -9%

Total Deposits (mm): $2,795 +12% $3,126 0%

Market Capitalization (mm): $1,010 -13% $1,104 +22%

Non-performing loans to gross loan portfolio: 0.78% 1.31%

1988

1992

2003

2005

2009

2014

Following incorporation in 1978, Bladex initiated its operations in 1979 and issued its

first bond in the international capital markets

Bladex is granted a license to operate as an agency by the New York State

Banking Authorities

Bladex is the First Latin American bank registered with the SEC for its IPO,

establishing a full listing on the NYSE

Bladex conducts a Common Stock Rights Offering, with stand-by

commitments issued by a group of Class A shareholders and multilateral

organizations

Bladex launches its client diversification strategy into trade-oriented

corporations; expansion of its suite of products and services

Bladex initiates funding diversification strategy: increase in central bank

deposits, local & international debt sales, syndicated loan facilities

Bladex cooperates with the International Finance Corporation to

establish the first critical commodities finance facility in Latin America

1979 Moody’s Fitch S&P

Date of Rating Dec. 2007 Jul. 2012 May 2008

Date of Confirmation Nov. 2014 Jul. 2016 Jun. 2016

Date of Last Update Jul. 2016 Sep. 2016 Jun. 2016

Short-Term P-2 F2 A-2

Long-Term Baa2 BBB+ BBB

Perspective Stable Stable Negative*

3

(*) Revised from Stable as of October 28th, 2016

Strong and Unique Shareholder Structure

A unique shareholding structure

Class A shareholders provide substantial support to Bladex, representing a direct link between the Bank and the governments

of Latin America – most of which have granted preferred creditor status to the Bank – and also constituting the main source of

deposits, a very reliable funding source

Class A shareholders enjoy super-majority rights related to changes in the Bank‟s Articles of Incorporation

Class A shareholders can only sell shares to other class A shareholders, thus maintaining the essence of the existing

shareholder structure and ensuring support from central banks

Shareholder Composition Board of Directors Composition

4

Out of 10 directors, 9 are

independent and one represents the

Bank‟s management (CEO)

Class A – Central Banks or

designees from 23 LatAm countries

Class B – LatAm & international

banks and financial institutions

Class E – Public Float (NYSE listed)

Defined Value Proposition with Strong Business

Fundamentals

Business Value Proposition Strong Underlying Business Fundamentals

Business Products & Services Multi-Pronged Business Segmentation

Global provider of natural

resources with positive

demographics

Sustained growth

and sound

economic

policies

Deep knowledge of

Latin America

Core competency in

trade finance

Support of

Investment &

Regional

Integration

Efficient

Measurement and

Management

In-depth knowledge of Latin America‟s local markets

Backed by 23 Latin American governments

Vast correspondent banking network throughout

LatAm & other regions of the world

Uniquely qualified staff with strong product expertise in

Trade Value Chain, Cross-border Finance, Supply-side

& Distribution, both intra-regional and inter-regional

Efficient organizational structure

LEAN, client focused efficient organizational structure

Single point of contact, providing client-specific

solutions, and focused on long-term relationships

Driver of progress,

economic growth and

development

Supporting

specialization in

both primary and

manufacturing

sectors

Enhancing LatAm‟s

role in global and

regional value chains

Growth of „Multi-latinas‟ as

drivers of business expansion

Supporting business

integration boosted by

free trade agreements

Bladex‟s products and services are categorized into three main areas: i) Financial

Intermediation Business, ii) Structuring and Syndications Business and iii) Treasury.

Financial Intermediation

Syndication and Structuring

Treasury

• Trade: Foreign trade products – short and medium term instruments that help drive

the cross-border activity of corporations.

• Working Capital: Support to trade finance clients throughout the entire production

cycle chain, across a wide range of primary, secondary and tertiary activity sectors.

Structured Credit and lending facilities for short and medium-term financing of supply

chain, materials & equipment, and inventories.

• Financial solutions designed to meet clients' needs.

• Provides access to structured funding for a wide base of financial institutions and

companies in Latin America.

• Debt capital market and deposit products for investment and cash flow optimization.

• Treasury services.

World-Class Standards in Corporate Governance

Enterprise-Wide Risk Management

5

Financial Institutions Among top 10 in their

respective markets

Significant corporate

banking activity / client

base

Corporations US Dollar generation

capacity

Growth oriented beyond

domestic market

Among top 10 in

respective industries

Track Record &

Corporate Governance

Focus on Strategic Sectors for the Region

Oil & Gas (upstream, integrated, and downstream),

Agribusiness, Food processing, Manufacturing, well

diversified in other sectors

Regional Focus Mexico

Central America and The

Caribbean

Brazil

South America

• Southern Cone (1)

• Andean Region (2)

(1) Includes Argentina, Chile,

Paraguay and Uruguay. (2) Includes Bolivia,

Colombia, Ecuador, Peru

and Venezuela

5

REGIONS

CLIENT BASE

INDUSTRY

SECTORS

Leverage Proven

Origination Capacity

LatAm GDP

Growth

LatAm Trade

Flow Growth

Bladex Client

Base Growth

Valued Products

& Services

15%+

ROAE Bladex

Origination

Active

Portfolio

Management

Improved Financial

Margins

NIM ~ 1.8% - 2.0%

Stable Fees from Use

of Capital

~ 15% – 20% of

Business Profit

Prudent Credit Risk

Management

Cost of Credit

~ 1.2% – 1.5%

Continued Focus on

Efficiency

Efficiency Ratio

< 30%

Sustainable Moderate

Growth

~ 3% to 8%

Core Financial Intermediation (On-book Portfolio)

Solid Capitalization

A minimum of 13.5%

Tier 1 Basel III Ratio

Target Consistent

Core Performance

Financial

Institutions Syndications &

Structuring

Partners Trade

Services

Distribution:

Asset Distribution & Services

Fee Based

Services:

Investors Other

Tap Additional Income Sources

15%+

ROAE

12%+

ROAE

3%+

ROAE

6

Financial Business Model targets

sustainable, superior returns

• Our Financial Business Model is based on our proven origination capacity of well-diversified Latin American risk. With an adequate risk-

return profile, together with solid operational efficiency and capitalization, the Bank aims to deliver a consistent return through its ROAE

and to its shareholders from its core financial intermediation activities, commensurate with its cost of capital. The Bank‟s efforts to enhance

its asset distribution and trade finance services, aim to increase its return target well above the Bank‟s cost of capital.

Strategy Hones Strengths & Positions to Seize

Growth Opportunities

Develop Emerging Businesses

• Develop robust syndication

platform

• Expand diversified market

distribution capabilities

Risk sharing programs

Secondary market transactions

Securitization Platform

• Expand vendor finance and

leasing capabilities

Local Presence (i.e. SOFOM in

Mexico)

Build New Businesses

• Explore adjacent markets &

establish pipeline of new business

activities in trade and regional

integration, such as:

Credit Insurance

Structured Trade Finance

Trade-related Services

Factoring

Trade related - infrastructure

projects

Strengthen Core Business

• Active credit portfolio

management

Achieve greater risk dispersion

Improve quality of earnings

Achieve sustainable &

consistent return on equity

• Expand Contingency Business

Develop Guarantee and L/C

Issuance Platform

• Improve Operating Efficiency

through LEAN Processes,

Structure & Organization

+

+

7

Core ROAE = 12% ROAE = 15%

Adhering to World-Class Standards

(*) Except for the Bank‟s Chief Executive Officer (CEO), all

other members of the Board of Directors are independent.

Board of Directors*

CEO

Commercial

Division

Internal Audit

Risk Policy and

Assessment Committee Finance & Business

Committee

Nomination

and Compensation

Committee

Audit and

Compliance Committee

Very high corporate governance

standards

Multiple regulators: FED, SEC,

NYSDFS, Superintendency of Banks

of Panama, and other entities

throughout the Region

Commercial

Division

8

Enterprise risk management &

externally certified internal audit

function

Internal alignment of corporate

culture, measurement system

and process management to

optimize total shareholder return

.

FIRST LINE

OF DEFENSE

Operating

Management

-------------------------

Front end &

enabling functions

THIRD LINE OF DEFENSE

Assurance

-------------------------

Audit function

Finance

Division

SECOND LINE OF DEFENSE

Monitoring

-------------------------

Risk function

Corporate Services Risk Management

Division

Commercial Strategy Focused on Diversification

9

Sustained Portfolio Growth Commercial Portfolio Composition

Commercial Portfolio By Country Commercial Portfolio By Industry

As of September 30, 2016 As of September 30, 2016

9

Reduced exposure to Brazil by

22 percentage points since 2005

to September 30, 2016

As of September 30, 2016

10

… and Focus on Asset Quality

Impaired Loans Evolution

Proven track record of strong asset quality, with significant risk mitigants:

• Low-risk asset class, with short-dated exposures, and superior loss performance

• US dollar based lending, no meaningful net FX exposures

• Floating-rate lending and funding model minimizes interest rate risk exposure

• Conservative loss reserve methodology (IFRS 9)

• Pro-active loss prevention, and diligent recovery processes

10

11

Low risk Business

Commercial Portfolio by Type of Transaction

• As of September 30, 2016, 75% of commercial portfolio

had a remaining maturity term of 1 year, with average

maturity of 117 days.

• Medium term commercial portfolio had a remaining

maturity term of 2.3 years.

• Commercial portfolio - remaining maturity of 294 days.

11

Commercial Portfolio by Term

• Bladex‟s portfolio is composed primarily of trade

assets, low-risk class, with short-dated exposures, and

superior loss performance.

Diversified Regional and Global Funding

Sources….

(*) Original Currency: all non-

USD denominated liabilities

are hedged into US Dollars

with the exception of most

MXN issuances which fund

assets in the same currency.

Funding Highlights

• Proven capacity to secure funding and maintain high

liquidity levels, even during crises

• Deposits from central banks shareholders or designees

provide a resilient funding base. They represent 70% of the

Bank‟s total deposits as of September 30, 2016.

• Focus on increased diversification of global and regional

funding sources on numerous relevant dimensions: client

base, geography and currency

• Broad access to debt capital markets through public and

private debt issuance programs in USD and other

currencies, and international syndications

• Increased focus in medium and long-term funding to match

a growing asset base with similar characteristics and

consolidate the funding base stability maintaining

competitive funding costs

Deposits by Type of Client Diversified Funding Sources

As of September 30, 2016 As of September 30, 2016

Funding Sources and Cost of Funds

Funding by Currency (*)

12

(US$ million)

As of September 30, 2016

…with Conservative Liquidity Management

Liquidity Management Highlights Liquidity Placements

Liquidity Coverage Ratio Liquidity Ratio

(US$ million)

As of September 30, 2016

Advanced liquidity management operating under Basel III

framework, monitoring liquidity through Liquidity Coverage Ratio

(“LCR”) and Net Stable Funding Ratio (“NSFR”)

1.19x NSFR

1.04x LCR (Basel III)

Liquid balances mainly held in cash-equivalent deposits in A-1 /

P-1 rated financial institutions or A-rated negotiable money market

instruments.

High-quality, short-term trade finance book, which serves as an

alternate source of liquidity, with approximately $1 billion in loans

maturing on a monthly basis

13

14

Expanding Earnings Capacity & Profitability...

Profit for the period Net Interest Income & Margin

Fees and Other Income Efficiency Ratio

Financial Information corresponding to the year 2014-2016 were prepared in accordance with International Financial Reporting Standards (IFRS) as issued by IASB.

The financial information corresponding to the years 2011-2013 follow the previous accounting standard, US-GAAP. Bladex completed its transition process to IFRS

from US-GAAP in 2015.

(US$ million, except percentages)

(US$ million) (US$ million, except percentages)

(US$ million)

15

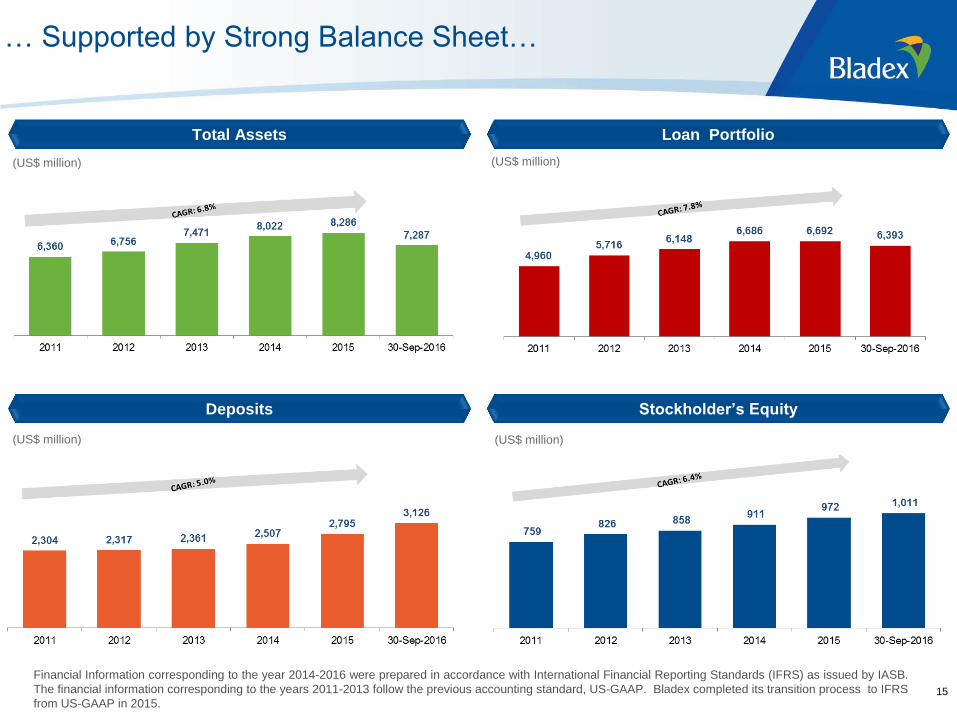

… Supported by Strong Balance Sheet…

Total Assets Loan Portfolio

Deposits Stockholder’s Equity

(US$ million) (US$ million)

(US$ million) (US$ million)

Financial Information corresponding to the year 2014-2016 were prepared in accordance with International Financial Reporting Standards (IFRS) as issued by IASB.

The financial information corresponding to the years 2011-2013 follow the previous accounting standard, US-GAAP. Bladex completed its transition process to IFRS

from US-GAAP in 2015.

Return on Average Equity “ROAE” Return on Average Assets “ROAA”

…and Solid Performance

Tier 1 Capital Ratio

16

Risk Weighted Assets – Basel III

(US$ million)

2011 n.a.

2012 n.a.

2013 n.a.

2014 $5,914

2015 $6,104

30-Sep-16 $6,373

n.a. means not available

Financial Information corresponding to the year 2014-2016 were prepared in accordance with International Financial Reporting Standards (IFRS) as issued by IASB.

The financial information corresponding to the years 2011-2013 follow the previous accounting standard, US-GAAP. Bladex completed its transition process to IFRS

from US-GAAP in 2015.

17

Key Financial Metrics

17

Financial Information corresponding to the year 2014-2016 were prepared in accordance with International Financial Reporting Standards (IFRS) as issued by IASB.

The financial information corresponding to the years 2011-2013 follow the previous accounting standard, US-GAAP. Bladex completed its transition process to

IFRS from US-GAAP in 2015.

(In US$ million, except percentages) 2011 2012 2013 2014 2015 9M16

Total Income $138.8 $137.4 $133.7 $167.6 $173.9 $124.8

Business Profit $66.3 $83.5 $89.4 $99.7 $99.0 $78.1

Non-Core Items 16.9 9.5 (4.6) 2.7 5.0 (4.4)

Net Profit $83.2 $93.0 $84.8 $102.4 $104.0 $73.7

EPS (US$) $2.25 $2.46 $2.21 $2.65 $2.67 $1.89

Return on Average Equity (ROAE) 11.4% 11.6% 10.0% 11.5% 11.0% 10.0%

Business Return on Average Equity ("Business ROAE") 9.1% 10.4% 10.6% 11.2% 10.4% 10.6%

Return on Average Assets (ROAA) 1.5% 1.5% 1.2% 1.4% 1.3% 1.3%

Busines Return on Assets ("Business ROAA") 1.2% 1.4% 1.3% 1.3% 1.3% 1.4%

Net Interest Margin ("NIM") 1.81% 1.70% 1.75% 1.88% 1.84% 2.08%

Net Interest Spread ("NIS") 1.62% 1.44% 1.55% 1.72% 1.68% 1.86%

Loan Portfolio 4,960 5,716 6,148 6,686 6,692 6,393

Commercial Portfolio 5,354 5,953 6,630 7,187 7,155 6,688

Allowance for expected credit losses on loans at amortized cost and off-

balance sheet credit risk to Commercial Portfolio (%) 1.82% 1.31% 1.18% 1.22% 1.33% 1.67%

Non-Performing Loans to gross Loan Portfolio (%) 0.65% 0.00% 0.05% 0.06% 0.78% 1.31%

Allowance for expected credit losses on loans at amortized cost and off-

balance sheet credit risk to Non-Performing Loans (x times) 3.0 0.0 25.0 21.7 1.8 1.3

Efficiency Ratio 36% 42% 41% 32% 30% 27%

Business Efficiency Ratio 39% 43% 37% 32% 31% 26%

Market Capitalization 596 822 1,081 1,167 1,010 1,104

Total assets 6,360 6,756 7,471 8,022 8,286 7,287

Tier 1 Capital Ratio Basel III (Basel I for years 2011-2013) 18.6% 17.9% 15.9% 15.5% 16.1% 15.9%

Leverage 8.4 8.2 8.7 8.8 8.5 7.2

Performance

Efficiency

Scale &

Capitalization

Portfolio Quality

Results

Bladex Value Proposition to Shareholders

• Bladex offers investors access

to an entire continent with

compelling long-term growth

prospects

• Business model provides

diversified exposure to

emerging markets, but with

well mitigated Credit Quality,

Market, & Operational risks

• Committed to total

shareholder return (“TSR”) …

Attractive dividend yield

(annual dividend yield over

5.0%) as a function of core

business growth (target 40% -

50% payout ratio)

• Attractive valuation multiples

18

Dividends per Share

BLX Stock Price and Volume Evolution

Diversified Commercial Portfolio with Robust Asset Quality

Defined Strategy to Achieve Sustainable Growth

Diversified Funding & Conservative Liquidity

Management

Experienced Management and Conservative Risk Management

Practices

Compelling Returns sustained by Strong and Reliable Performance Metrics

Leading Franchise in LatAm

with Solid Track Record

Trade Finance Bank in Latin America with more than 35 years of Remarkable Success

Investment Grade Profile with Strong and Unique Shareholding Structure

Deep knowledge of Latin America with Core in Trade Finance

Strategically positioned to capture growth opportunities

Sustainable Portfolio Strategy focused on Diversification

Strong Asset Quality Management and a Low Risk Core Business Focus

Increased diversification of Regional and Global Funding Sources

Advanced Liquidity Management operating under Basel III Framework

Profit for 2015 of $104.0 million (+2% YoY), and $73.7 million for 9M16.

Return on Average Equity of 10.0% for 9M16.

Solid 15.9% Tier 1 Capitalization Ratio (Basel III) as of September 30, 2016.

Seasoned Senior Management with ample experience in C-Suite roles

World-Class Standards in Corporate Governance, focused on Enterprise-Wide Risk Management

Investment Highlights

19

PANAMA HEAD OFFICE Torre V, Business Park

Ave. La Rotonda, Costa del Este

Apartado 0819-08730

Panamá, República de Panamá

Tel: (507) 210-8500

ARGENTINA Av. Corrientes 222 –P.18º

(1043AAP) Capital Federal

Buenos Aires, Argentina

Tel: (54-11) 4331-2535

Contact: Federico Pérez Sartori

Email: [email protected]

BRAZIL Rua Leopoldo Couto de Magalhäes

Junior 110, 1º andar

04542-000, Sao Paulo, Brazil

Tel: (55-11) 2198-9606

Contact: Roberto Kanegae

Email: [email protected]

MEXICO MEXICO CITY Rubén Darío 281, piso 15, Oficina #1501

Colonia Bosque de Chapultepec

CP. 11580, México D.F.

Tel: (52-55) 5280-0822

Contact: Alejandro Barrientos

Email: [email protected]

MONTERREY Torre Avalanz, piso 20 oficina 2035

Batallón de San Patricio #109

Col. Valle Oriente, San Pedro, Garza

García

Nuevo León, C.P. 66260, México

Tel: (52-81) 4780-2377

Contact: Alejandro Barrientos

Email: [email protected]

PERU Dean Valdivia 243

Piso 7, Oficina 701

San Isidro, Lima

Tel: (511) 207-8800

Contact: Victor Mantilla

Email: [email protected]

COLOMBIA Calle 113 # 7-45

Edificio Teleport Business Park

Torre B, Oficina 1008

Bogotá, Colombia

Tel: (57-1) 214-3677

Contact: Camilo Alvarado

Email: [email protected]

UNITED STATES NEW YORK AGENCY

10 Bank Street, Suite 1220

White Plains, NY 10606

Tel: (001) 914-328-6640

Contacto: Pierre Dulin

Email: [email protected]

Regional Presence in Latin America

20

21

22

Balance Sheet

Financial Information corresponding to the year 2014-2016 were prepared in accordance with International Financial Reporting Standards (IFRS) as

issued by IASB. Bladex completed its transition process to IFRS from US-GAAP in 2015.

22

(In US$ million)31-Dec-2014 31-Dec-2015 30-Sep-2016

Assets

Cash and cash equivalents $781 $1,300 $755

Financial instruments:

At fair value through profit or loss 58 53 0

At fair value through OCI 339 142 56

Securities at amortized cost, net 55 108 89

Loans at amortized cost 6,686 6,692 6,393

Allowance for expected credit losses (78) (90) (106)

Unearned interest & deferred fees (9) (9) (9)

Loans at amortized cost, net 6,600 6,592 6,278

At fair value - derivative financial instruments used for hedging - receivable 12 7 27

Other assets 178 83 82

Total assets $8,022 $8,286 $7,287

Liabilities and stockholders' equity

Total deposits $2,507 $2,795 $3,126

At fair value - derivative financial instruments used for hedging - payable 40 30 35

Securities sold under repurchase agreements 301 114 101

Short-term borrowings and debt 2,693 2,430 1,132

Long-term borrowings and debt, net 1,400 1,882 1,831

Allowance for expected credit losses on off-balance sheet credit risk 10 5 5

Other liabilities 162 57 45

Total stockholders' equity 911 972 1,011

Total liabilities and stockholders' equity $8,022 $8,286 $7,287

23

Profit and Loss

23 Financial Information corresponding to the year 2014-2016 were prepared in accordance with International Financial Reporting Standards

(IFRS) as issued by IASB. Bladex completed its transition process to IFRS from US-GAAP in 2015.

(In US$ thousand) 2014 2015 9M16

Interest income $212,898 $220,312 $184,448

Interest expense 71,562 74,833 66,924

Net Interest Income 141,336 145,479 117,524

Other income

Fees and commissions, net 17,502 19,200 10,178

Derivate financial instruments and foreign currency exchange 208 (23) (135)

Gain (loss) per financial instrument at fair value through profit or loss 2,361 5,731 (4,091)

Gain (loss) per financial instrument at fair value through OCI 1,871 363 (246)

Gain on sale of loans at amortized cost 2,546 1,505 490

Other income, net 1,786 1,603 1,057

Net other income 26,274 28,379 7,253

Total Income 167,610 173,858 124,777

Expenses

Impairment loss from expected credit losses on loans at amortized cost 6,782 17,248 17,186

Impairment loss from expected credit losses on investment securities 1,030 5,290 276

Impairment loss (gain) from expected credit losses on off-balance sheet financial instruments 3,819 (4,448) (59)

Operating expenses

Salaries and other employee expenses 31,566 30,435 19,008

Depreciation of equipment and leasehold improvements 1,545 1,371 1,039

Amortization of intangible assets 942 596 425

Professional services 5,177 4,621 2,614

Maintenance and repairs 1,544 1,635 1,353

Other expenses 12,839 13,126 9,234

Total operating expenses 53,612 51,784 33,673

Total Expenses 65,243 69,874 51,076

Profit for the Period $102,366 $103,984 $73,701