blue label telecomsblue label telecoms · blue label telecomsblue label telecoms ... • bangladesh...

TRANSCRIPT

Blue Label TelecomsBlue Label TelecomsFinal Results Presentation

for the year ended 31 May 2009y y

AGENDA

• Strategic Overview

• International Distribution

• Technologygy

• Value Added Services

• Financial OverviewFinancial Overview

• South African Distribution

Way Forward• Way Forward

Strategic Overview

Mark LevyMark LevyJoint CEO

3

Group Structure

South African Distribution International Distribution Technology Value Added Services

The Prepaid Company Gold Label Activi Technology Services Datacel

Crown Cellular Oxigen Services India - Transaction Junction - CellfindCrown Cellular 37.22% 60% Cellfind

Ventury Ukash – 16.9% Activi Deployment Services Content Connect Africa

Blue Label OneMatragon APS - 72% Blue Label Onet/a Mobile Services Company

(MSC)Kwikpay APS DRC - 90%

Virtual Voucher APS MOZAMBIQUE - 80%

APS NIGERIA - 51%

Blue Label Mexico - 70%

Sharedphone 50.1%

• 100% unless otherwise stated

4

Blue Label Australasia 50.5%

The Telecoms Landscape

• Emerging markets have continued to grow, g g g ,posting growth figures in the single digits instead of double-digit expansion

• In South Africa Prepaid ARPU is stableIn South Africa, Prepaid ARPU is stable• In the less evolved markets consumer

expenditure is also largely stable or dropping only slightlydropping only slightly

• Total mobile subscribers or SIMs in the local market are expected to reach 56 million by the end of 2009

• Mobile penetration expected to increase from 122% to over 150% by 2013y

• South African cellular market surpassed the 50-million connections milestone at the end of 2008 although only 68% of theseof 2008, although only 68% of these represented individual users

Source: (1) Creamer Media’s Engineering News Online; 31 July 2009; “SA cellular market exceeds 50 million connections mark (2) IDC EMCA Telecoms Services Dababase, Q1 2009 5

Global footprint

Bricks & mortarTechnology offerings

Af h i t

United Kingdom

• Afghanistan• Bangladesh• Benin• Botswana• Cyprus• Czech Republic• France• Germany• Ghana• Guinea BissauKingdom

I di

• Greece• Haiti• Indonesia• Ireland• Israel• Italy• Ivory Coast• Lesotho• Liberia• Middle East Region

Mexico

DRC

India

Nigeria

• Middle East Region• Netherlands• Pakistan• Poland• Russia• Rwanda• Sierra Leone• Spain• Sudan• Swaziland

S d

South AfricaMozambique Australia

• Sweden• Syria• Tanzania• Togo• Uganda• USA• Yemen• Zimbabwe

Two strategies for international expansion:- Bricks and Mortar

- Technology Offerings

6

BLT is focused on servicing the unbanked and badly banked market by providing access to cost effective transactional services

International Distribution

Mark LevyMark LevyJoint CEO

7

International Operations

overview• Enhance all technology offerings

• Continue to focus on growth of footprint• Continue to focus on growth of footprint

• Introduce to existing markets all Blue Label Telecoms’ products and services

• Providing additional tokens of value• Providing additional tokens of value, enhancing each country’s service offering and revenue streams

• Improved melded margin

8

I diIndia

Total connections 430,290,998

% Growth in total connections p.a. 48.48%

Prepaid as % of total connections 85.14%

Market penetration 30.34%

Prepaid ARPU (USD/month) 4.50

9

Consolidation of Oxigen India

• Proactive reduction in operating costs and cost management

• Revision of sales and revenue-generation strategies through:

- Rejuvenation, recovery and re-deployment of POS devices

- Higher rate of integration into retail

- Additional POS devices due to improved technical competence

- Direct Top-Up comprising 70% of prepaid recharge market

- Further expansion of product offering – in addition to airtime, rail, and toll

• Consolidation of technology solution and competencies including:

- Backend management and maintenance

- Hardware enhancements with increased capacity and capabilities

- Improved communications connectivity and reliability

10

Oxigen India

• Consolidation of the retail base• Consolidation of the retail base- Selling base increased during the period

Average sale per store increased- Average sale per store increased

- Selling Web vending sites and average sales per site doubled during the period

• Airtime sales growth- Sales Revenues grew consistently

• Oxicash

- Steady growth with a total in excess of 1.1 million wallets by the end of May 2009

11

Oxigen India – Breakthrough Initiatives

state bank of india• PINless top-up of airtime and Oxicash on mobile to consumer• Integration complete and live beta testing commenced

nokia ovi store• Oxicash is the exclusive mobile transactional partner for all Nokia products• Fulfill Nokia Extended Warranty

nokia – ovi store

• Oxigen for airtime sales through all Nokia branches

bank switch• mCheck – integrated and deployed for Oxigen and subsequent Oxicash

integration• Obopay – integration has commenced

• Improve connectivity, contain communications costs and reduce barrier to new cdma pos terminal roll-out

entry for new POS sites

12

M iMexico

Total connections 87,079,422

% Growth in total connections p.a. 13.47%p

Prepaid as % of total connections 88.62%

Market penetration 70.46%

Prepaid ARPU (USD/month) 8.31Prepaid ARPU (USD/month) 8.31

13

Blue Label Mexico

• Localisation, customisation and ,enhancements to the Blue Label AEON platform saw launch and commencement of trading in May 2009trading in May 2009

• Enhanced technology provides PINless h l ti b irecharge on a real-time basis

• Public Telephony launch in conjunction with p y jTelefonica, utilising our Sharedphone product and service, commenced in 2009 with a pilot of 2,000 units through towith a pilot of 2,000 units through to September

14

Blue Label Mexico

• Several Agreements for electronic airtime gdistribution technology signed with the distribution channels involving:

- POS implementation

- Multiple channel retail outlet integration

f- Petroleum forecourts

- Convenience outlets

Mi fi i- Micro-finance companies

• Provides BLM with in excess of 7,500 points of presenceof presence

• Since the roll-out of POS, the average sales transactional value per site has increased pper site per month

15

United Ki dKingdom

16

Ukash

• Consumer ability to Cash In, elect to y ,transact online or in a mobile environment, and to Cash Out at their convenience

• The business model of Ukash and its easeThe business model of Ukash and its ease of integration to third party devices and technology provides for rapid deployment and broad coverage based on the existingand broad coverage based on the existing retail presence of the third party

• Points of presence have grown – giving Uk h i i l t t i EUkash more issuing real estate in Europe and abroad as follows:

- Continued growth in EuropeR i d i t t i th USA- Remained consistent in the USA

- Launched in South Africa through BLT channels, Pick ‘n PayR tl l h d i A t li- Recently launched in Australia

17

Ukash

status• Points of Sale network continues to increase

through 7 new marketsP t S i id idi• Payment Service providers are now providing expansion of Merchant acceptance

• Physical outlets expanded in Portugal, ItalyPhysical outlets expanded in Portugal, Italy Germany, France, Belgium, Slovenia, Poland and Australia

• Growth continues per annum• MasterCard selected Ukash for Europe for re-

PowerPower• AUTP selected Ukash for cash payment for

airline industry• Spain – issuance of Ukash through ATM

18

Ukash – Successes over last 6 months

• Live in

- Portugal, Italy, Slovenia and Australia

• On-line issueOn line issue

- Buying Ukash online through bank account

• SkypeSkype

- Extended Ukash offering in Russia and Ukraine

• Key payment

• Service provider in South Africa

19

African Prepaid Services

20

Africa Prepaid Services

Nigeria

Democratic Republic of CCongo

Mozambique

21

Africa Prepaid Services (“APS”)

group• APS SA is responsible for implementation

of our African expansion initiative

• APS concluded an agreement with Multilinks-Telkom for Nigeria

• Set up in Nigeria necessitated employment of skilled and experienced staff subsequently transferred across to q yNigeria

22

Africa Prepaid Services

M biMozambique

Total connections 6 245 965Total connections 6,245,965

% Growth in total connections p.a. 24.70%

Prepaid as % of total connections 98.49%

Market penetration 25.71%

23

Prepaid ARPU (USD/month) 3.60

Africa Prepaid Services

mozambique• Expansion programme launched and

commencing through:

- Increase in cash generating assets

- Additional 5 new branches became fully ti l i loperational in more rural areas as per

Vodacom

• Started showing monthly improvement with• Started showing monthly improvement with the upward trend expected to continue in growth and profitability

• Awarded “Best Distributor of the Year” by Vodacom for the third consecutive year

24

Africa Prepaid Services

Democratic Republic of C

Total connections 10 990 451

Congo

Total connections 10,990,451

% Growth in total connections p.a. 37.22%

Prepaid as % of total connections 98.09%

Market penetration 14.78%

25

Prepaid ARPU (USD/month) 4.85

Africa Prepaid Services

democratic republic of congo• Operational changes over the past year:

- Extended Contractual arrangements with V d DRCVodacom DRC

• Focus on only:

V d i b lk i ti- Vodoxi – bulk printing

- Public telephony

SIM t t k ith i t d- SIM starter packs with no associated distribution costs and on-going airtime revenues

- Airtime sales – subject to discount provided and market conditions

26

Africa Prepaid Services

Ni iNigeria

Total connections 82 525 542Total connections 82,525,542

% Growth in total connections p.a. 55.93%

Prepaid as % of total connections 98.48%

Market penetration 45.11%

27

Prepaid ARPU (USD/month) 10.00

Africa Prepaid Services

nigeria• Signed a contract with Multilinks Telkom to

exclusively provide all mobile distribution and value-added services on behalf of thisand value added services on behalf of this CDMA operator in Nigeria

• APS Nigeria commenced trading in MayAPS Nigeria commenced trading in May 2009

• May sales met expectations and y psubsequent months have continued to yield similar results

28

Africa Prepaid Services

nigeria• May sales were on track with budget and

Multilink-Telkom’s prior periods:

M 2009 th i i ti l A il- May 2009 growth in airtime sales up on April 2009

- In excess of 50,000 new handset connectedIn excess of 50,000 new handset connected in May

• Increased subscriber base with more thl timonthly connections

• Increased value-added services offered by Multilinks Telkom to increase usageMultilinks-Telkom to increase usage patterns

29

Technology

Mark LevyMark LevyJoint CEO

30

Activi

switching overview

POSTILION SwitchElectricity Cellular

NetworksVouchers(Ukash)

Banking(TJ)3rd Party Suppliers

AEON Switch3rd

PartyHost to Host

3rd Party Hosts

STD Accounting

Interface D t b

Accounting Package

AEONMerchant Terminal

Management

Database

Terminals Vending/ Touch WEB Bulk Integrated

Management System & EVD

Terminals gSelf Service Screen Browser Printing

g3rd Party

Retail devices31

Services

EFT Switching Platform

Core IT Infrastructure & Operational Platform

GroupMIS Pl tf

& Operational Support

EVD/VAS Platform

MIS Platform (and Accounting

/ Financial Management)

Card Management Platform (Gift

Cards/

Factory

Cards/ Loyalty)

Device Deployment & Support

32

The Mobile Services Company

• MSC launched mibli™ in June ’08 – rapid growth millions

• On-device portal to services, products & mobi-wallet• Supported by MSC and Activi AEON back-end systems• Launched MSC services for 3rd parties• Launched key new products and services:• Launched key new products and services:

- callink – low cost international calling- moova – music and content subscription service- mobi wallet – full-featured mobile wallet- msc media – groupwide advertising sales

• Key drivers:- Highly mobile-centric customers- Demographics centered on young adultsg p y g- Ownership of verticals & horizontals- Integration of transactionality- Economics of consumer spending patterns

Future:• Future:- International expansion of mibli™ user base- Growth in MSC services to 3rd parties- Expansion of subscription services- Extension of mobi wallet services to 3rd parties- Rapid enhancement of products & services on mibli™

33

Value Added Services

Mark LevyJoint CEO

34

Datacel

• Datacel continues to focus its strategy to gyparticipate in the whole of the insurance value chain

• Velociti’s inbound call centre serviced in excess of 500,000 customers

• The outbound direct selling has growth opportunity as companies develop more products and services for the emergingproducts and services for the emerging income groups

35

Cellfind

• Location-Based Services (LBS)( )- Vodacom

- MTN

• WASP Services- SMS, MMS, USSD

- Network billing etc.g

• Key drivers:- Network Operator performance & co-

marketingmarketing

- Uptake of new MTN and Traffic services

- New Value-added LBS products

- Extended WASP service offerings

- Extended White label offerings

- Changes in Network Billing Rulesg g

- Changes in WASPA Code of Conduct

36

Cellfind

future• Significant growth prospects for newly

launched MTN 2MyAid, MTN WhereRU and miTRAFFIC over the next 12 months

• White-Label offerings to be extended to:- Music/Content- Panic Buttons to Corporates- Panic Buttons to Corporates

• Corporate offerings with lower churn (Capitated Schemes)E i f B2C ff i l ti t• Expansion of B2C offerings relating to:

- Traffic- Weather- Content- LBS

• Look4info –corporate and consumer LBS-based information service to be launched 2009

37

Content Connect Africa

• Digital and Mobile Content Distribution

• Dominant player for South African & African independent music content

K t t t f• Key content aggregators for:

- MTN

- Vodacom- Vodacom

• Future:- Further integrated offerings with group subsidiaries.- Expanded on-deck distribution into multiple African

territories- Increased consumption of mobile content through p g

expanded group and 3rd party channels, e.g. mibli™ and the Mobile Services Company platform

38

Microsoft

• Past 18 months, working with Microsoft on the next generation of mobile services for the mass market.

• August 2009 – worldwide launch by Blue Label and Microsoft of mibli™ v7 based on the Microsoft OneApp mobile software

• Integrated eco-system consisting of Blue Label’s TRANSACTIONAL layer (Activi), Blue Label’s MOBILE SERVICES layer (MSC) and Microsoft’s OneApp on-phone software (owning the vertical), creating significant convergence

• Brings app-store functionality to the world’s phonesBrings app store functionality to the world s phones• Ease of creating and deploying new applications (owning the

horizontal)• Leverages massive Microsoft development community• Allows cross-network transactionality• Integrates entertainment & fun with utility, cost savings and

features never previously available in developing world markets• Creates massive entrepreneurial and social upliftment

opportunities• Provides cost savings and features previously unavailable to

usersusers• Plans to expand range and scope of services as well as into

new territories and existing user bases39

Financial Overview

David RivkindCFO

40

Financial highlights

Actual growth

Revenue R15.3bn 22%

EBITDA R568m

Operating profit R475m

73%

76%

NPAT R391m 116%

Core earnings R427m

Headline earnings per share 51.63 cents

58%

71%

Core earnings per share 55.93 cents 22%

Cash generated from operations R667m Xx%

41

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growthaudited unaudited GrowthR’000 R’000

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%Gross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470Finance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191Share of loss of associates and joint ventures (27 445) (19 661)Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

42

Financial Overview

segmental profile• South African distribution

• International distribution

• Value added services

• TechnologyTechnology

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

audited unaudited GrowthR’000 R’000

Segmental revenueGross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%

South African distribution 14 199 031 12 194 815 16.4%International distribution 724 163 500 268 44.8%Value added services 335 743 207 676 61.7%EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470

Technology 22 512 27 850 (19.2%)Total 15 281 449 12 930 609 18.2%

% Contribution% ContributionFinance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191Share of loss of associates and joint ventures (27 445) (19 661)

% Contribution% Contribution

South African distribution 92.9% 94.3%International distribution 4.8% 3.9%Value added services 2 2% 1 6%Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%

Value added services 2.2% 1.6%Technology 0.1% 0.2%Total 100% 100%

Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

44

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

audited unaudited GrowthR’000 R’000

Gross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%

Segmental gross profit

EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470

South African distribution 813 590 545 771International distribution 75 488 63 441Value added services 160 903 92 108Technology 15 628 17 782

Finance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191 11%Share of loss of associates and joint ventures (27 445) (19 661)

Total 1 065 609 719 102

Gross profit %Gross profit %

Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%

South African distribution 5.73% 4.48%International distribution 10.41% 12.68%Value added services 47.92% 44.35%Technology 69.43% 63.85%Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

Total 6.97% 5.56%

45

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

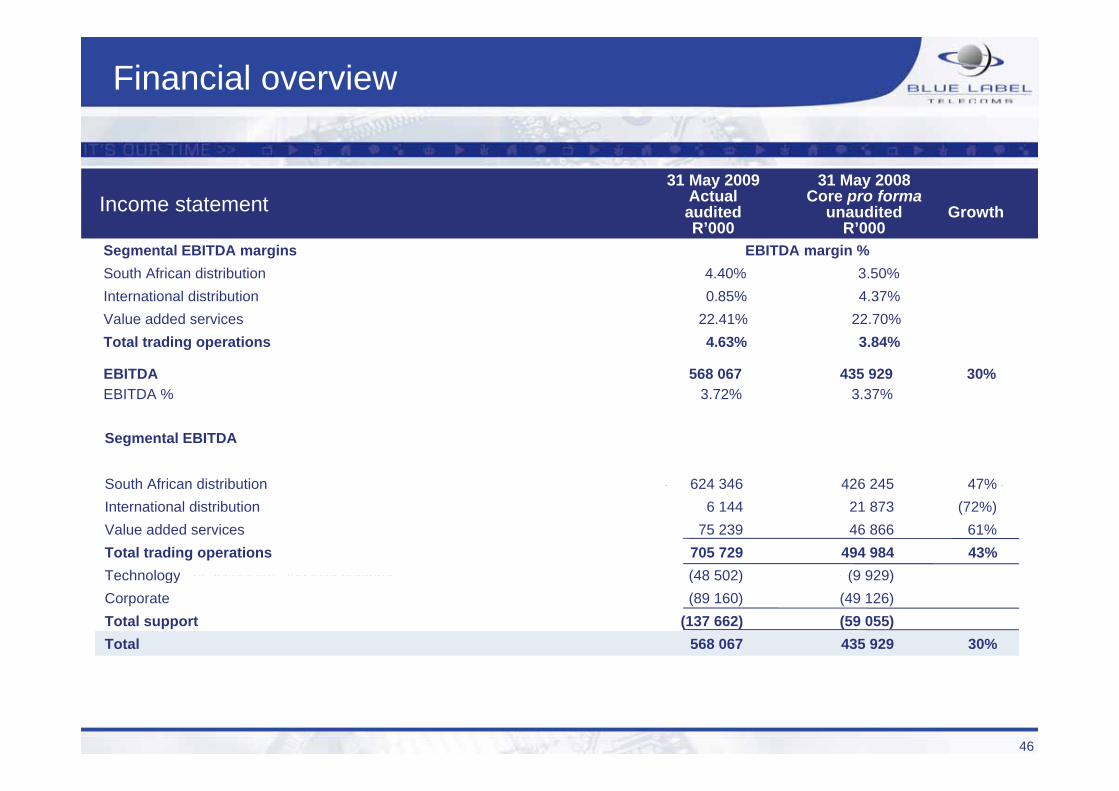

Segmental EBITDA margins EBITDA margin %South African distribution 4.40% 3.50%International distribution 0.85% 4.37%

audited unaudited GrowthR’000 R’000

Gross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%

Value added services 22.41% 22.70%Total trading operations 4.63% 3.84%

EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470

Segmental EBITDA

South African distribution 624 346 426 245 47%Finance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191Share of loss of associates and joint ventures (27 445) (19 661)

South African distribution 624 346 426 245 47%International distribution 6 144 21 873 (72%)Value added services 75 239 46 866 61%Total trading operations 705 729 494 984 43%Technology (48 502) (9 929)Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%

Technology (48 502) (9 929)Corporate (89 160) (49 126)Total support (137 662) (59 055)Total 568 067 435 929 30%

Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

46

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

audited unaudited GrowthR’000 R’000

Gross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470Finance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191Share of loss of associates and joint ventures (27 445) (19 661)• The group earned finance income of R205m

I t d i t t i bl d bt b l R47 (R16 i i i d)Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%

• Imputed interest receivable on debtors balances – R47m (R16m in prior period)• Interest on liquid working capital – R158m• Decline in finance income of R65m net of this IFRS adjustment due to:

• Cash resources utilised to gain early settlement discounts

Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

• Interest forfeiture due to acquisitions • Gradual decline in interest rates.

47

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

audited unaudited GrowthR’000 R’000

Gross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470Finance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191Share of loss of associates and joint ventures (27 445) (19 661)• R108m relates to imputed interest payable on creditors’ balances in terms of IFRS (R101m in prior period)Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

48

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

audited unaudited GrowthR’000 R’000

Gross profit % 6.97% 5.56%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37%

• Oxigen Services India• Revenue increased by 31% from R1.02bn to R1.34bn.EBITDA % 3.72% 3.37%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470

Revenue increased by 31% from R1.02bn to R1.34bn.• Improvement in company’s performance in the last quarter

• Ukash• Purchased for strategic reasons – technology offering in line with group’s objective to increase value added servicesFinance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191Share of loss of associates and joint ventures (27 445) (19 661)

• Purchased for strategic reasons technology offering in line with group s objective to increase value added services

Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%

Oxigen Services India Pvt Ltd (25 940) (19 661) (32%)Smart Voucher Limited (Ukash) (2 286) - -Other 781 - -Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

Total (27 445) (19 661) (40%)

49

Financial overview

Income statement31 May 2009 31 May 2008

Actual Core pro formaaudited unaudited Growth

Revenue 15 281 449 12 930 609 18%Cost of inventories sold (14 215 840) (12 211 507)Gross profit 1 065 609 719 102 48%

audited unaudited GrowthR’000 R’000

Core net profit

Gross profit % 6.97% 5.56% 25%Other income 22 368 68 142Overheads (519 910) (351 315)EBITDA 568 067 435 929 30%EBITDA % 3 72% 3 37% 10%

South African distribution 537 815 407 320 130 495International distribution 17 279 10 601 6 678International distribution associates (28 226) (19 661) (8 565)EBITDA % 3.72% 3.37% 10%Depreciation, amortisation and impairment charges (93 220) (73 675)Operating profit 474 847 362 254 31%Net finance income 92 347 132 866Finance income 205 046 239 470

Value added services 49 497 33 450 16 047Total operations 576 365 431 710 144 655

Technology (55 250) (11 339) (43 911)

Finance expense (112 699) (106 604)Net profit before taxation 567 194 495 120Taxation (174 784) (138 929)Net profit after taxation 392 410 356 191 11%Share of loss of associates and joint ventures (27 445) (19 661)

Corporate (93 915) (49 429) (44 486)Total support (149 165) (60 768) (88 397)

Total 427 200 370 942 56 258C i h 55 93 48 40 7 53Share of loss of associates and joint ventures (27 445) (19 661)Minorities interest 25 582 (507)Net profit after taxation and minority interest 390 547 336 023 16%Amortisation on intangibles raised through business combinations net of tax 36 653 34 919Core net profit after taxation 427 200 370 942 15%

Core earnings per share 55.93c 48.40c 7.53c

Earnings per share for profit attributable to equity holders (cents)- Basic 51.13 43.85 17%- Headline 51.63 43.55 19%

50

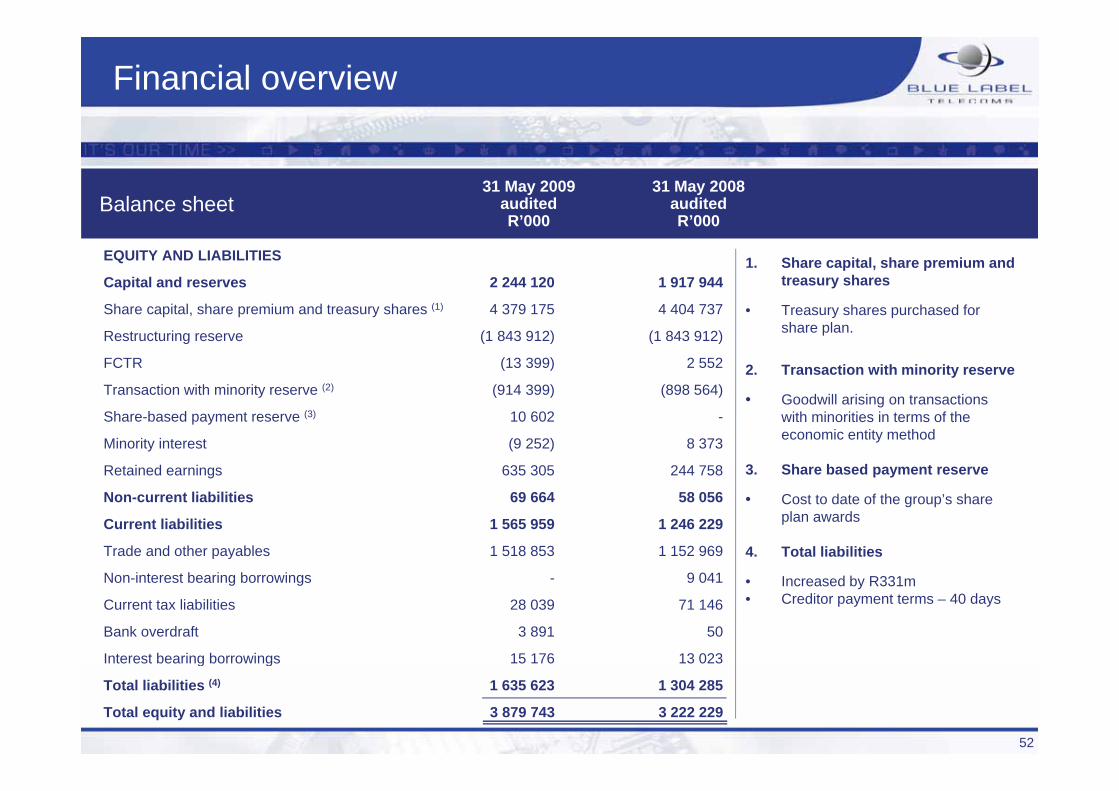

Financial overview

Balance sheet31 May 2009 31 May 2008

audited auditedR’000 R’000

ASSETS

Non-current assets (2) 736 634 712 759

R’000 R’000

1. Total assets

• Increased by R658m (20.4%) to Property, plant and equipment 105 011 69 484

Intangible assets and goodwill 460 325 489 786

Investments in associates and joint ventures 109 837 81 356

R3.9bn.

2. Non-current assets

• Increased by R24m

• PPE - Capex mainly on POS Financial assets at amortised cost 54 096 72 133

Deferred taxation assets 7 365 -

Current assets (3) 3 143 109 2 509 470

p ydevices

• Amortisation of intangibles assets

• Net increase in investment in associates - Ukash and Oxigen

Financial assets at fair value 10 5 672

Financial assets at amortised cost 67 449 53 163

Inventories 384 361 484 501

L i bl 29 920 7 103

India.

• Net decrease in unactivated starter packs (Financial assets at amortised cost)

3 C t tLoans receivable 29 920 7 103

Trade and other receivables 898 571 630 687

Current tax assets 2 101 -

C h d h i l t 1 760 697 1 328 344

3. Current assets

• Increased by R633m

• Increase in cash resources

• Stock turn averaged 3 timesCash and cash equivalents 1 760 697 1 328 344

Total assets (1) 3 879 743 3 222 229• Debtors collection – 21 days

51

Financial overview

Balance sheet31 May 2009 31 May 2008

audited auditedR’000 R’000

EQUITY AND LIABILITIES

Capital and reserves 2 244 120 1 917 944

Sh it l h i d t h (1) 4 379 175 4 404 737

1. Share capital, share premium and treasury shares

T h h d f

R’000 R’000

Share capital, share premium and treasury shares (1) 4 379 175 4 404 737

Restructuring reserve (1 843 912) (1 843 912)

FCTR (13 399) 2 552

Transaction with minority reserve (2) (914 399) (898 564)

• Treasury shares purchased for share plan.

2. Transaction with minority reserve

G d ill i i t tiy ( ) ( )

Share-based payment reserve (3) 10 602 -

Minority interest (9 252) 8 373

Retained earnings 635 305 244 758

• Goodwill arising on transactions with minorities in terms of the economic entity method

3. Share based payment reserve

Non-current liabilities 69 664 58 056

Current liabilities 1 565 959 1 246 229

Trade and other payables 1 518 853 1 152 969

Non interest bearing borro ings 9 041

• Cost to date of the group’s share plan awards

4. Total liabilities

Non-interest bearing borrowings - 9 041

Current tax liabilities 28 039 71 146

Bank overdraft 3 891 50

Interest bearing borrowings 15 176 13 023

• Increased by R331m• Creditor payment terms – 40 days

g g

Total liabilities (4) 1 635 623 1 304 285

Total equity and liabilities 3 879 743 3 222 229

52

Financial overview

Cash flow31 May 2009

auditedR’000

1. Cash flows from operating activities

R’000

Cash flows from operating activities (1) 666 994

C h fl f i ti ti iti (2) (206 731)

• Profit growth + working capital management = R667m of operating cash generated

Cash flows from investing activities (2) (206 731)

Cash flows from financing activities (10 624)

Increase in cash and cash equivalents 449 639

2. Cash flows from investing activities

• Acquisition of group companiesCash and cash equivalents at the beginning of the period 1 328 294

Translation difference (21 127)

• Acquisition of group companies –R102m

• Capex – R74m

• Additions to intangible assets –R29Cash and cash equivalents at end of period 1 756 806 R29m

53

Financial overview

Dividends

No dividend has been declared in line with group’s present stated policyThe group intends to declare dividends in the financial year commencing 1 June 2010

54

South African Distribution

Brett LevyJoint CEO

55

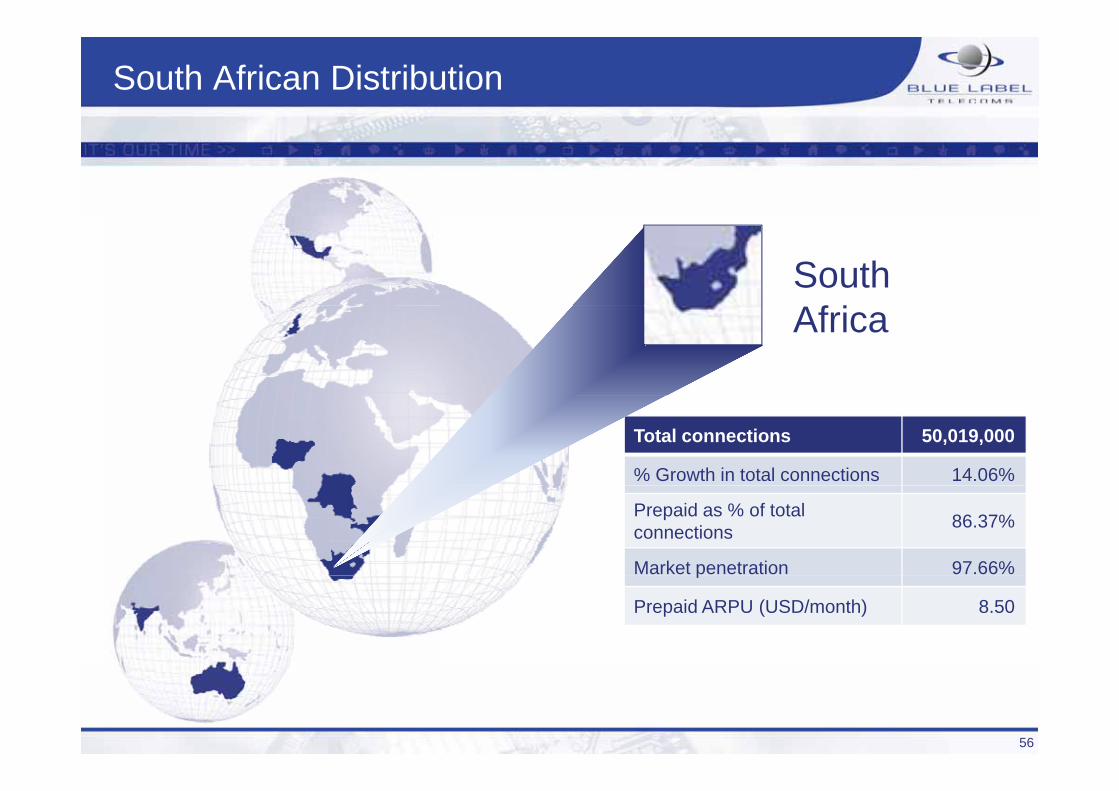

South African Distribution

South Af iAfrica

Total connections 50,019,000

% Growth in total connections 14.06%

Prepaid as % of total connections 86.37%

Market penetration 97.66%p

Prepaid ARPU (USD/month) 8.50

56

RICA

• Onus on all South Africa’s telecommunications operators and retailers to gather and register personal details of all South African existing and new mobileSouth African, existing and new, mobile phone subscribers

• BLT has formulated to RICA registration t t th t i bl t i t idstrategy that is able to register prepaid

mobile phone subscribers in support of our retail customers, nationally

• In conjunction with the South African Mobile operators, we have a number of RICA data collection solutions that will seamlesslycollection solutions that will seamlessly integrate into the current store setups, with minimal impact on hardware, software and IT tIT systems

57

Algoa Bus Ticketing

• A new cashless bus ticket system was introduced in Nelson Mandela Bay at the beginning of August 2009beginning of August 2009

• Allows consumers to travel a set route as many times as they like in a day, week ormany times as they like in a day, week or month using the same pass

• Bus vouchers are available at 600 outlets

58

Remittances

• Currently 2 million (60%) migrant workers, sending R6.1 billion across continent

• 5.7 million South Africans live away from 5.7 million South Africans live away from immediate family

• Total domestic market is R12 billion annuallyannually

• 60% of remittances reach their beneficiaries in informal ways due to high transactional feesfees

• Remittances are recognised as one of the world’s largest poverty reduction effortsW ld id 150 illi i t t• Worldwide 150 million migrants sent US$300 billion in 2006

• Remittance pathways increase education d d d hild l bspend and reduce child labour

59

Remittances

• Influencing factors to consider:- Ease

Familiarity- Familiarity- Cost- Speed- Risk tolerance- Access

• Existing remittance channels:Existing remittance channels:- Taxi driver- Friend or relative- Post office

• In many African countries, remittance flows are large enough to rival aid flowsg g

60

Gidani

• In 2006, the National Lottery Board awarded Gidani a tender to manage the running of South Africa’sa tender to manage the running of South Africa s National Lottery

• In December 2006, Gidani appointed Activi to assist it with the rollout and maintenance of new Lotto

hi S th Af imachines across South Africa• In July 2009, Gidani announced that lottery players

will be able to play Lotto through a cell phone, bank ATM and online bankingg

• The first time in Africa – made possible by Activi’s technology platform

• The new method of playing Lotto was launched th h FNBthrough FNB

• Other banks have indicated that they will come on board later in the year

• Access to nearly one million FNB mobile bankingAccess to nearly one million FNB mobile banking customers, as well as registered users and 3 400 FNB ATM’s

• Shoprite pilot brings Lotto to till points, also off Activi’s technology platform (mid August)Activi s technology platform (mid-August)

• The first time in Africa

61

Blue Label Telecoms : SA DistributionPeriod : 1 June 2008 31 May 2009

Total Prepaid Product Revenue & Voucher Counts

Period : 1 June 2008 - 31 May 2009

122,500,000

140,000,000

R 1,400,000,000

R 1,600,000,000

87,500,000

105,000,000

R 1,000,000,000

R 1,200,000,000

ntVAT

52 500 000

70,000,000

R 600 000 000

R 800,000,000

Vouc

her C

oun

Rev

enue

Exc

l. V

35,000,000

52,500,000

R 400,000,000

R 600,000,000R

0

17,500,000

R 0

R 200,000,000

200806 200807 200808 200809 200810 200811 200812 200901 200902 200903 200904 200905

Sales Excl. VAT Voucher Count

(Crown Cellular, Kwikpay, Matragon, The Prepaid Company, Ventury, Virtual Voucher)

Blue Label Telecoms : SA DistributionPeriod : 1 June 2008 31 May 2009

Device Split May 2009 Devices GIS Regional Spread May 2009

Period : 1 June 2008 - 31 May 2009

Terminals68.93% Free State

7.14%

2009

Eastern Cape12.97%

Gauteng35.09%

Kwazulu Natal12.39%

Bulk Printing UnitsGateway Units Integrated

Kiosk Units2.87%

Touch Screen Units

Vending Machine6.58%

Limpopo3.62%

Mpumalanga4 47%

North West

Northern Cape1.75%

Western Cape18 11%0.48%

y1.42%

gPoint Sale Devices11.46%

Units8.26%

4.47%4.47%18.11%

(Kwikpay, Matragon, Ventury, Virtual Voucher)

Blue Label Telecoms : SA Electronic DistributionPeriod : 1 June 2008 31 May 2009

Revenue by Market Segment

Period : 1 June 2008 - 31 May 2009

R 32,000,000

R 36,000,000

R 230,000,000

R 260,000,000

R 24,000,000

R 28,000,000

R 170,000,000

R 200,000,000

e -M

6

2, M

3, M

4

R 16,000,000

R 20,000,000

R 110,000,000

R 140,000,000

Rev

enue

Rev

enue

-M

2

R 12,000,000

R 16,000,000

R 80,000,000

R 110,000,000

R 8,000,000R 50,000,000

M2 - Petrolum Industry M3 - Independent Multi Lane Retailer M4 - Independent Single Lane Retailer M6 - 2nd Tier Wholesalers

(Kwikpay, Matragon, Ventury, Virtual Voucher)

Blue Label Telecoms : SA DistributionPeriod : 1 June 2008 31 May 2009

250.00%

Period : 1 June 2008 - 31 May 2009

201.73%206.96%

200.00%

150.00%

100.00%

24.21% 21.82% 22.28% 22.31%26.62%

0 40%6.26% 7.75%

50.00%

37 20% 36 97%

0.40%0.00%

Telkom Electricity Cell C MTN Vodacom Overall Growth

-37.20%-36.97%-50.00%

Voucher Count Growth % PT Sales Excl. VAT Growth % PT

(Crown Cellular, Kwikpay, Matragon, The Prepaid Company, Ventury, Virtual Voucher)

Blue Label Telecoms : SA Electronic DistributionPeriod : 1 June 2008 31 May 2009

Growth % per Region: June 2008 vs May 2009

Period : 1 June 2008 - 31 May 2009

167.61%

160.00%

180.00%

124.01%

120.00%

140.00%

61.19%

85.09% 82.30%91.39%

78.95%80.00%

100.00%

52.69% 51.85% 50.71%

27.38%

51.69%

28.93% 27.94%36.05% 34.96%

22.82% 19.48%

39.50%40.00%

60.00%

15.45%19.48%

0.00%

20.00%

Eastern Cape

Free State Gauteng Kwa Zulu Natal

Limpopo Mpumalanga North West Northern Cape

Western Cape

Overall GrowthCape Natal Cape Cape Growth

Voucher Count Growth % Sales Excl. VAT Growth %

(Kwikpay, Matragon, Ventury, Virtual Voucher)

Blue Label Telecoms : SA Distribution

Monthly Sales by Region

R 160 000 000

R 180,000,000

R 200,000,000

R 80 000 000

R 90,000,000

R 100,000,000

al, L

impo

po,

ern

Cap

e

R 120,000,000

R 140,000,000

R 160,000,000

R 60,000,000

R 70,000,000

R 80,000,000

aute

ng

Kw

a-Zu

lu N

ata

Cap

e an

d W

este

R 80,000,000

R 100,000,000

R 40,000,000

R 50,000,000

onth

ly S

ales

Ga

pe,F

ree

Stat

e,

est,

Nor

ther

n C

R 40,000,000

R 60,000,000

R 20,000,000

R 30,000,000

Mo

es E

aste

rn C

apan

ga, N

orth

We

R 0

R 20,000,000

R 0

R 10,000,000

200806 200807 200808 200809 200810 200811 200812 200901 200902 200903 200904 200905Mon

thly

Sal

Mpu

mal

a

Eastern Cape Free State Kwa Zulu Natal Limpopo Mpumalanga

North West Northern Cape Western Cape Gauteng

Blue Label TelecomsBlue Label TelecomsFinal Results Presentation

Thank youyQ&A