black friday sale on 2017 tax planning tips - sullivanlaw.com friday sale on... · 5 {b2223037; 16}...

TRANSCRIPT

{B2223037; 16}

Black Friday Sale on 2017 Tax Planning Tips

(c) 2017

by Joseph B. Darby III, Esq.

Sullivan & Worcester LLP

One Post Office Square,

Boston, MA 02109

(617) 338-2985 (office)

(617) 719-1534 (cell)

SW Tax Briefings

One Post Office Square

Boston MA 02109

December 6, 2017

4:00 - 5:45 pm

{B2223037; 16}

Joseph B. Darby III, Esq.

Joseph B. Darby III, Esq. is a senior partner in the Boston office of Sullivan & Worcester, LLP, and

has been admitted to the practice of law in Massachusetts since 1979. He concentrates his legal

practice on tax and business law, and advises individuals and business entities on a wide variety of

tax-related matters, including income-tax planning for business and real estate transactions, estate

planning, wealth preservation, and represents taxpayers in tax controversies with the IRS and state

tax authorities. He is recognized as one of the Best Lawyers in America in the area of tax practice

by Best Lawyers®, the oldest and most respected peer-review publication in the American legal

profession

Mr. Darby is the author of the highly regarded Practical Guide to Mergers, Acquisitions and

Business Sales, the Second Edition of which was published in 2017 by The National Underwriter

Company, a Division of ALM Media, LLC, and he is a recognized authority in the structuring of

mergers, acquisitions, business sales, and related business transactions. He teaches a course entitled

Tax Aspects of Buying and Selling a Business at the Boston University School of Law Graduate

Tax Program (GTP).

Mr. Darby is also a recognized authority on the taxation of intellectual property, including tax issues

related to the development, licensing and exploitation of intellectual property rights, and the

migration of valuable intellectual property to offshore jurisdictions. He teaches two courses on

taxation of intellectual property at the GTP, the first entitled Taxation of Intellectual Property, and

the second entitled Structuring Intellectual Property Transactions.

Mr. Darby has been the recipient of numerous journalism and writing awards, including recognition

as “Tax Writer of the Year” in 2007 and 2011 by Practical International Tax Strategies, a Thomson

Reuters publication. He has authored 2 books and more than 1,000 articles for such diverse

publications as The Tax Lawyer, Worth Magazine, Venture Capital Magazine, Banker &

Tradesman, Mass High Tech, Hemispheres Magazine, Contract Professional, Trusts & Estates

Magazine, The Boston Globe, The Boston Herald, The Boston Business Journal and The Boston

Phoenix.

Mr. Darby was a sports writer in an earlier life, and wrote sports columns for numerous publications

including The Boston Herald, The Boston Phoenix, Hemispheres Magazine and Worcester

Magazine. The New England Press Association honored him with the First Place award in the

category of Sports Columns in 1990, beating out all other competitors that year.

Mr. Darby is the editor of an entertaining and informative tax blog entitled “Tax and Sports Update,” a

fun and readable tax blog that is billed, tongue in cheek, as “The ONLY tax newsletter with an

award-winning sports column.” The blog is at www.taxandsportsupdate.com.

Mr. Darby has served as pro bono legal counsel to a variety of Boston-area charitable organizations.

He is currently the President and a Board Member of the Watertown Police Foundation, an

organization formed to support the Watertown Police Department and the Watertown community at

large to cope with the challenges faced in the aftermath of the events of April 19, 2013. He is a

former President of the Boston Police Foundation (2008-2012), and served in a similar capacity for

that organization.

{B2223037; 16}

Mr. Darby received his B.S. degree in Mathematics and Political Science, from the University of

Illinois in 1974, with Departmental Honors in Mathematics, Magna Cum Laude, Phi Beta Kappa

and Bronze Plaque (top 1% of graduating class). He graduated with honors from Harvard Law

School in 1978.

Additional biographical information, including copies of numerous articles written by Mr. Darby, is

available at his firm website www.sandw.com.

{B2223037; 16}

Black Friday Sale on 2017 Tax Planning Tips

(c) 2017

By: Joseph B. Darby III, Esq.

Sullivan & Worcester, LLP One Post Office Square

Boston, MA 02109

(617) 338-2985 (work)

(617) 719-1534 (cell)

I. STATE OF THE UNION.

A. The State of the Union.

1. The United States in 2017 continues to be a politically divided country, with

ongoing acrimony and splenetic debates across a spectrum of issues, many of which directly or

indirectly implicate federal tax policy and the Internal Revenue Code.

2. The Republican Party holds the office of President and both houses of

Congress, and is trying mightily to enact tax reform. At this moment there are two competing bills

that have been passed, by the House of Representatives and by the Senate, respectively, and these

two bills will go through the Congressional reconciliation process and will eventually pass – or not.

It is hard to assume that ANYTHING is a sure thing in Congress these days, but at the moment the

expectation is that the Congress will in fact deliver a major piece of tax legislation before the end of

this year.

3. This Outline is supplemented by Exhibit A, which contains a special handout

that compares key provisions of the Senate and Congressional tax bills, and offers some thoughts on

where the legislative process may end up – and some thoughts on year-end 2017 tax strategies.

B. The Current State of the Internal Revenue Code…and the Public Fisc.

1. There is a very good chance that the Internal Revenue Code (the “Code”) will

continue to have the same legal characteristics as in recent years – namely, a massively complicated

statute that literally NO ONE fully understands, rife with political compromises and general

financial chicanery, offering expensive tax indulgences to favored constituencies, all while coming

no where close to actually paying for the current federal budget expenses.

2. Fact: The United States is $20.6 trillion in debt on the date of this seminar.

See the chart on the top of the next page.

4 {B2223037; 16}

3. The U.S. federal budget deficit for fiscal year (FY) 2018 (October 1, 2017

through September 30, 2018) is currently projected to be $440 billion. U.S. government spending

for FY 2018 is projected to be $4.094 trillion compared to projected revenue of $3.654 trillion.1 The

Treasury Department reported that the deficit for FY 2017 was $666 billion.

4. Revenue for FY 2017 was a record $3.3 trillion, but spending was also a

record at almost $4 trillion. The deficit was 14% higher than the prior year.

C. Four Reasons for the Budget Deficits.

1. These enormous federal budget deficits are the result of four factors.

2. First, the attacks that occurred on 9/11/2001 led to the War on Terror. U.S.

military spending rose from $437.4 billion in 2003 to a peak of $855.1 billion in 2011.

3. Second, mandatory spending, notably on Social Security and Medicare

benefits, has continually and inexorably increased (we have known about this for decades), and has

exceeded $2 trillion per year since FY 2011. These payments already comprise a large (and

growing) majority of the federal budget each year. Only an Act of Congress reducing these benefits

can change that inexorable calculus. It would, in other words, require an Act of Courage.2 How

likely is that to happen?

4. Third, the $787 billion economic stimulus package added to the 2009 deficit

by cutting taxes, extending unemployment benefits, and funding lots of miscellaneous federal

spending, much of it not particularly productive. This expansionary fiscal policy was intended to

1 Source: "2018 Budget. Table 2," Office of Management and Budget, March 16, 2017. “Mid-Session Review Fiscal

Year 2017. Table S-5,” OMB, July 15, 2016. 2 It would require a majority vote in both houses and a signature by the president. It is unlikely to happen until the

budget becomes an absolute crisis. A meaningful reduction in benefits would necessarily take a lot of money away from

current and future beneficiaries. The current political assumption – whether correct or not – is that enraged seniors

would vote lawmakers out of office. It has been called the “third rail” of U.S. politics.

5 {B2223037; 16}

push the economy out of recession. In fact, the Great Recession ended in the second quarter of

2009, but the huge deficits (in excess of $1 trillion per year) continued for many years thereafter.

5. Fourth, the Great Recession reduced federal revenue and taxes. Government

revenue fell from its pre-recession record of $2.57 trillion in FY 2007 to $2.1 trillion in FY 2009,

and did not fully recover until FY 2013 when it reached $2.78 trillion.

D. Why Does the Government Always Overspend?

1. The argument can be made that the more the government spends, the more it

stimulates the economy. That's because government spending is itself a component of gross

domestic product. An economically valid criticism is that government purchases “political” goods

and services, and that the expenditures are often wasteful, unproductive, politically expedient, and

crowd out private sector spending that would be much more efficient and productive. Debating the

benefits and drawbacks of governmental deficit spending can be the basis of a lively conversation,

not to mention a fist fight. They will not be addressed, or solved, in this Outline.

2. Let us all instead consider the famous and chilling admonitions of Alexander

Fraser Tytler3:

“A democracy cannot exist as a permanent form of government. It can only exist

until the voters discover that they can vote themselves largesse from the public

treasury. From that moment on, the majority always votes for the candidates

promising the most benefits from the public treasury with the result that a democracy

always collapses over loose fiscal policy, always followed by a dictatorship. The

average age of the world's greatest civilizations has been 200 years. These nations

have progressed through this sequence: From bondage to spiritual faith; From

spiritual faith to great courage; From courage to liberty; From liberty to abundance;

From abundance to selfishness; From selfishness to apathy; From apathy to

dependence; From dependence back into bondage.”

II. A LOOK-BACK AT THE AMERICAN TAXPAYER RELIEF ACT OF 2012: TAXES

ARE NOW A LOT HIGHER!

NOTE: Throughout this Outline, various tax thresholds are triggered by

different income measurements, including taxable income (“TI”), adjusted gross

income (“AGI”), modified adjusted gross income (“MAGI”) and just plain “wages,”

depending on the tax changes involved. Pay attention to this odd mish-mash of trigger

levels as you review this Outline. Also, see Appendix A, which ambitiously attempts to

“chart” all the different inflection points and tax rates.

3 Alexander Fraser Tytler, Lord Woodhouselee FRSE (15 October 1747 – 5 January 1813) was a Scottish advocate,

judge, writer and historian who served as Professor of Universal History, and Greek and Roman Antiquities at the

University of Edinburgh.

6 {B2223037; 16}

A. Summary of the Major Provisions in ATRA-2012.

1. Income Tax Rate Increases. ATRA-2012 imposed steep tax increases on a

relatively narrow band of higher-earning taxpayers, increasing tax rates from the 2012 maximum

marginal tax rate of 35% to a new (nominal) maximum marginal tax rate in 2013 of 39.6%. The

maximum rates are applicable in 2017 for single taxpayers with TI over $418,400 ($426,700 for

2018) and for married taxpayers filing jointly with combined TI over $470,700 ($480,050 for 2018).

Moreover, with all the phase-outs now built into the tax law, the maximum federal income tax rate

is probably closer to 45% at its peak maximum marginal effective rate, and, with the addition of the

3.8% ObamaCare Medicare Tax, reaches an effective federal income tax rate of almost 50% at

some points in the federal tax brackets. In high-tax states such as California and New York, the

combined effective marginal income tax rate on income may now be at or above 60%.

2. Higher Tax Rates for Long Term Capital Gains (“LTCG”) and Qualified

Dividends of Certain Taxpayers. ATRA-2012 increases the maximum tax rate on long-term capital

gains and on “qualified dividends” from 15% in 2012 to 20% in 2013 and later years, and is

applicable in 2017 for unmarried taxpayers with TI of over $418,400, and for married taxpayers

filing jointly with combined TI over $470,700. These thresholds will continue to be indexed

annually for inflation. In addition, capital gains and qualified dividends are also potentially subject

to the Net Investment Income Tax (“NIIT”), as described more fully below.

3. AMT Relief. ATRA-2012 allegedly tried to deal with the run amok

alternative minimum tax (“AMT”) by providing for a permanent indexing for inflation of key AMT

elements, including the AMT exemption amount, the threshold for applying the 26% versus 28%

brackets to individual taxpayers, and the AMT phase-out levels. ATRA-2012 also modified the

AMT calculation so as to allow non-refundable personal credits to be taken against AMT tax

liability. The changes were projected to reduce the number of taxpayers paying the AMT in 2013

from about 28 million (absent the fix) down to “only” about 4 million. However, the AMT

continues to affect almost any person with significant income. The exemption amount, for example,

reaches the full phase out at relatively low thresholds. Meanwhile, all kinds of tax items are

add-backs to the AMT, including interest on private activity bonds, interest paid on mortgages on

second homes, state income taxes paid, tax preference items from flow through investments, etc.

One can pretty reasonably argue that for upper middle class taxpayers and wealthy taxpayers – i.e.,

our clients – the AMT is more often than not the “real” federal income tax.

4. Two Phase-Outs Reintroduced for Higher-Income Taxpayers.

a. ATRA-2012 reinstated the personal exemption phase-out (“PEP”),

and also reinstated the so-called “Pease Limitation” on Schedule A itemized deductions.

Both the PEP and the Pease Limitation apply to single taxpayers with AGI over $261,500 in

2017, and married taxpayers filing jointly with AGI over $313,800 in 2017. These

thresholds are indexed annually for inflation.

b. The PEP causes a taxpayer to lose 2% of the otherwise allowable

personal and dependency exemptions for each $2,500 that the taxpayer’s AGI exceeds the

applicable threshold (i.e., 2% for each $2,500 over $261,500 in 2017 of AGI for a single

taxpayer and over $313,800 in 2017 of AGI for joint filers).

7 {B2223037; 16}

c. At the same AGI levels, the Pease Limitation causes Schedule A

itemized deductions to be reduced at a rate of 3% of a taxpayer’s AGI over the specified

threshold amount, up to a maximum disallowance of 80% of the itemized deductions

claimed. For purposes of the 80% cap on disallowance, the itemized deductions taken into

account (i.e., multiplied by 80%) will not include the deductions for medical expenses,

investment interest expense, casualty or theft losses, or allowable wagering losses. A

taxpayer calculates that 3% phase-out and the 80% cap, and the reduction is the lesser of the

two amounts.

5. Medicare Taxes Increased.

a. Although not part of ATRA-2012, there were two additional new or

increased taxes enacted by the Patient Protection and Affordable Care Act of 2010, known

popularly as ObamaCare, that also went into effect on January 1, 2013, and these taxes are

referred to in this Outline collectively as the “Medicare Taxes.”

b. First, there is the Net Investment Income Tax that imposes a 3.8% tax

on the “net investment income” or “NII” of taxpayers with MAGI in excess of $200,000 for

single taxpayers and $250,000 for married taxpayers filing jointly. [NOTE: These

thresholds are NOT indexed.]

c. Second, there is a corresponding increase to the Medicare Hospital

Insurance Tax or “HI” tax of 0.9%, imposed on taxpayers with wages that exceed certain

threshold amounts ($200,000 of wages for single taxpayers, $250,000 of combined wages

for married taxpayers filing jointly), thereby increasing the HI component of FICA tax

withholding from 2.9% (1.45% paid by each of employee and employer) to 3.8% (2.35%

paid by the higher-compensated employee and 1.45% paid by the employer). Similar

increases apply for self-employed taxpayers under the Self-Employment Contributions Act

(“SECA”) system. NOTE: An employer is required to withhold from wages it pays to an

individual in excess of $200,000 in a calendar year, without regard to the individual’s filing

status or wages paid by another employer.

d. Significantly, the Medicare Taxes take effect at significantly lower

income thresholds than the increase in income tax rates, and in fact are imposed at

approximately the same levels as the AGI thresholds at which the PEP and Pease Limitation

take effect, which is AGI of over $250,000 for single taxpayers and AGI over $300,000 for

married couples filing jointly.

III. ESTATE AND GIFT TAX CHANGES INTRODUCED BY 2012 ACT

A. Overview of ATRA-2012 Estate and Gift Tax Changes.

1. ATRA-2012 produced a surprisingly pro-taxpayer compromise with respect

to gift and estate taxation. Under the 2012 Fiscal Cliff, the lifetime unified gift and estate tax credit

was supposed to drop back to the level of just $1 million, and the top gift and estate tax rates were

supposed to jump back to 55%. Under ATRA, the top estate tax rate increased to 40% (from 35%

in 2012), but the lifetime unified gift and estate tax credit and the lifetime generation-skipping

transfer (“GST”) exemption remain at the $5 million level, indexed for inflation from 2010 onward.

8 {B2223037; 16}

For 2017, the lifetime unified credit-equivalent amount was $5,490,000, increasing to $5,600,000 in

2018.

2. State death taxes continue to be deductible under Code Section 2058 in

calculating the federal taxable estate.

3. The applicable exclusion amount (credit-equivalent exclusion amount)

remains portable for estate and gift tax purposes, but note that portability does not apply for the

GST exemption.

4. While it is hard to consider any tax law “permanent” these days, the estate

and gift tax changes are no longer subject to the sunset provisions contained in the 2001 and 2010

Tax Acts, thereby making permanent the additional tax relief contained in the prior legislation, i.e.,

there is no longer a built-in ticking time bomb to return the credit-equivalent amount back to

$1 million and the estate tax rates back up to 55%. As a result, the large majority of American

citizens, including those in the middle class, upper-middle class, and “poor rich” class, are no longer

forced to engage in heavy-duty estate and gift tax planning – at least not for the moment.

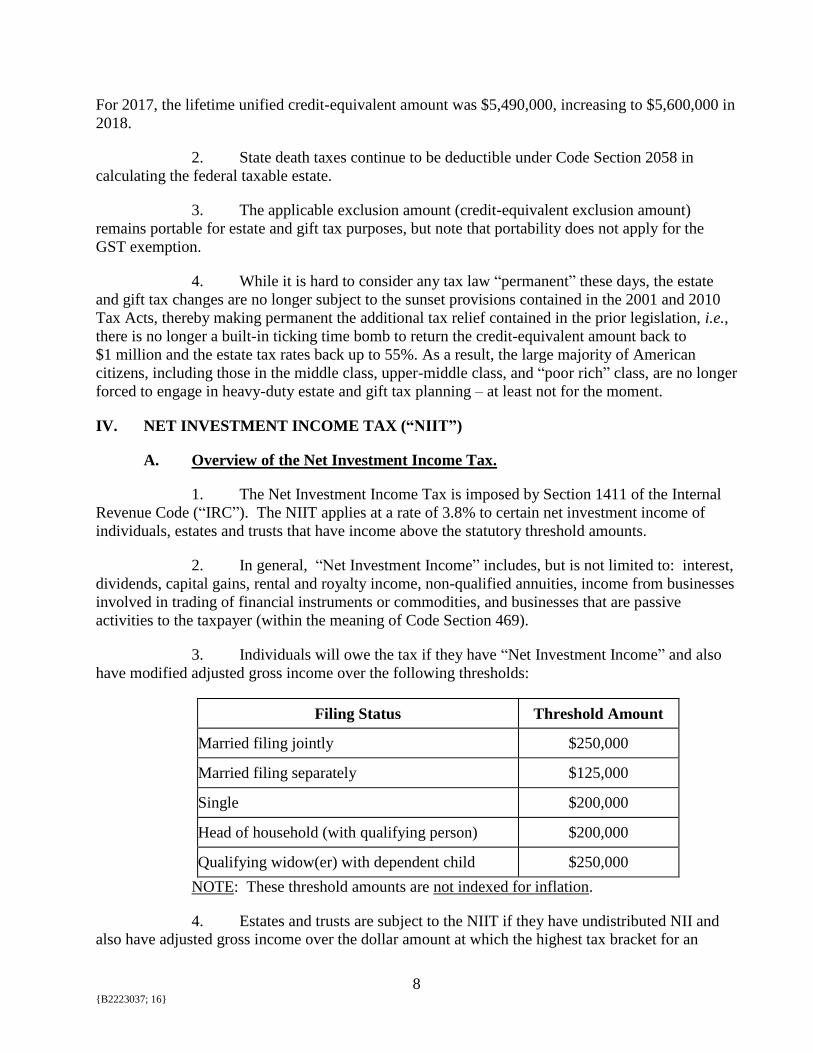

IV. NET INVESTMENT INCOME TAX (“NIIT”)

A. Overview of the Net Investment Income Tax.

1. The Net Investment Income Tax is imposed by Section 1411 of the Internal

Revenue Code (“IRC”). The NIIT applies at a rate of 3.8% to certain net investment income of

individuals, estates and trusts that have income above the statutory threshold amounts.

2. In general, “Net Investment Income” includes, but is not limited to: interest,

dividends, capital gains, rental and royalty income, non-qualified annuities, income from businesses

involved in trading of financial instruments or commodities, and businesses that are passive

activities to the taxpayer (within the meaning of Code Section 469).

3. Individuals will owe the tax if they have “Net Investment Income” and also

have modified adjusted gross income over the following thresholds:

Filing Status Threshold Amount

Married filing jointly $250,000

Married filing separately $125,000

Single $200,000

Head of household (with qualifying person) $200,000

Qualifying widow(er) with dependent child $250,000

NOTE: These threshold amounts are not indexed for inflation.

4. Estates and trusts are subject to the NIIT if they have undistributed NII and

also have adjusted gross income over the dollar amount at which the highest tax bracket for an

9 {B2223037; 16}

estate or trust begins for such taxable year. For tax year 2017, this threshold amount is $12,500.

There are special computational rules for certain trusts, including ESB Trusts. As a practical

matter, the NIIT becomes applicable to a trust at a very low income level ($12,500) compared to a

single individual ($200,000) or a married individual ($250,000 on a joint return).

B. Character of Trust Income as Active or Passive for NIIT Purposes.

1. Net Investment Income includes income from a taxpayer’s passive activities,

but does not include “active” income from businesses in which the taxpayer materially participates.

2. The IRS has never provided any useful guidance on what constitutes

“material participation” in an activity by either a trust or an estate, e.g., whether income from an

S corporation held by a trust or estate is active or passive (and, in turn, whether such income is

subject to the NIIT). For example, Regulations Section 1.469-5T(g), entitled “Material

participation of estates and trusts,” is and has been “[Reserved]” for a period of more than twenty

years.

3. The IRS currently takes the audit and litigation position that a trust (and

presumably an estate) can never materially participate in a real estate rental activity, i.e., that the

trust can never qualify as a “real estate professional” and thereby be eligible to treat the real estate

rental activity as an active business. With respect to a business operated through an S corporation,

or through an LLC, that is other than a real estate rental activity, the IRS has generally taken a

relatively narrow interpretation of the circumstances under which a trustee can satisfy the material

participation rules, and thus leans strongly toward characterizing such income as “passive” income

subject to the NIIT.

4. To date, only a brief reference in legislative history4 and two published cases,

Frank Aragona Trust v. Commissioner5 and Mattie Carter Trust v. United States,

6 provide any

guidance on material participation by a fiduciary for purposes of Section 469 (and, in turn, for

purposes of the NIIT). Fortunately, the two published cases, Aragona Trust and Carter Trust, were

huge victories for the trust/taxpayers, and in each case the court found that the activity was active

rather than passive. NOTE: Both cases were passive activity loss cases, not NIIT cases, but the

legal principles are identical, namely, whether the income (or loss) of the trust is active or passive

for purposes of Code Section 469.

5. On January 20, 2015, the Tax Section of the American Bar Association sent a

lengthy and thoughtful letter to the Commissioner of the Internal Revenue Service, expounding on

the question of how the NIIT should apply to estates and trusts. The letter discusses how

S corporation stock or other business interests should be treated in the hands of a trust or an estate

and generally argues that the income should be “active” rather than “passive” under a variety of

common factual circumstances. The letter is divided on whether, if a “true” trust distributes income

to a beneficiary, the “active” status should be measured by the participation of the trustee or the

beneficiary.

4 Senate Finance Committee, Tax Reform Act of 1986, S. Rep. No. 99-313, at 730 (1986) (“Senate Report”).

5 142 T.C. No. 9 (Mar. 27, 2014) (“Aragona Trust”).

6 256 F. Supp. 2d 536 (N.D. Tex. 2003) (“Carter Trust”).

10 {B2223037; 16}

C. NIIT Tax Planning Strategies.

1. Try to Stay under the Threshold Amount. The NIIT takes effect on MAGI

(essentially AGI) of $250,000 for married filing jointly, $200,000 for filing under single status. For

trusts, the 2017 threshold is $12,500 – VERY LOW. One of the strategies that may be useful in

staying under the applicable threshold is to use installment sales.

2. Invest through Tax-Deferred or Tax-Exempt Retirement Plans. Distributions

from IRAs, Roth IRAs, qualified pension plans (including 401(k) plans), or qualified annuity plans

are not subject to the NIIT, so investment build-up inside the plans avoids the NIIT. Likewise,

investments in tax-exempt bonds or similar tax-exempt investments are excluded from the NIIT.

3. Establish a Non-Grantor Charitable Lead Trust (“CLT”). There are other

reasons to consider a CLT besides the NIIT, but this is an added bonus. A taxpayer who is strongly

charitably inclined may want to contribute investment assets to a CLT. That way investment

income is taxed to the CLT rather than the taxpayer. By contrast, if the taxpayer keeps the

investment assets and makes a charitable contribution of the income, the charitable contribution can

offset the income tax (up to the 50% limit) but DOES NOT OFFSET THE NIIT. “Net income” is

net of charitable contributions deductions, but NIIT is not.

4. Sell Appreciated Assets Using a Charitable Remainder Trust. This strategy

defers recognition of a large amount of capital gain (which would ALL be subject to the NIIT if

recognized in a single year) and spreads it over a period of, say, 20 years. Assume Mr. and

Mrs. Entrepreneur want to sell their business for $5 million, and they have essentially zero tax basis

in the stock. The stock sale would generate $5 million of LTCG, taxed at 20%, plus the 3.8% NIIT.

Contribute the stock instead to a CRT, sell the stock, and then pay a 5% annuity for 20 years. The

Entrepreneurs receive $250,000 per year ($5 million X 5%), they get a current charitable

contribution deduction up from the transaction (a rough estimate is the contribution would be about

$500,000, and could be used in the current year plus the next five years to reduce taxable income),

and the NIIT is deferred, probably reduced substantially, and possibly eliminated entirely (if the

Entrepreneurs have no other income – not likely, but the NIIT is very likely to be reduced

substantially).

5. Consider Investing in Rental Real Estate – But You MUST Qualify as a Real

Estate Professional. Income from an active business under the passive activity loss rules (Code

Section 469) is not subject to the NIIT, and this includes rental income from real estate, but only if

the income is “active” which requires that the taxpayer meet the criteria of a real estate professional.

This means the taxpayer must spend more than 750 hours per year on real estate rental activities.

6. Capital Loss Harvesting. The NIIT is a tax on net investment income, and so

it makes sense to minimize gain in the current year by recognizing capital losses to offset current

capital gains.

7. Don’t Forget Investment Expenses. In addition to capital losses, remember

that certain expenses can be deducted in computing NII. These potential deductions include:

a. Deductions allocable to gross income from rents or royalties;

11 {B2223037; 16}

b. Deductions allocable to passive trades or businesses;

c. Penalties on early withdrawal from a CD or other savings account;

d. Net operating losses, subject to special rules;

e. Investment interest expenses (Code Section 163(d)(3) expenses);

f. Investment expenses defined in Code Section 163(d)(4)(C) (e.g., investment

advisory fees or other costs directly related to investment income); and

g. State income taxes related to the investment income.

V. INDIVIDUAL INCOME TAX PLANNING IDEAS IN 2017 AND BEYOND

A. Basic Strategies.

1. The “classic” income tax planning strategy is to defer income recognition and

accelerate deductions. However, even with “classic” tax planning, because of the stepping up of

brackets, phase-outs and other floors, ceilings and thresholds, the simple, intuitive strategy is no

longer necessarily the right way to go. It takes thoughtful planning over a timeline of a couple of

years to do it well.

2. But be aware that moving tax items may be counterproductive, especially if

the taxpayer is in the AMT, e.g., you may want to move income earlier in time and deductions later

in time!

3. Income-tax planning and gift and estate tax planning must be integrated in a

new and unprecedented way, particularly planning for the increase in tax basis.

4. Gifts of appreciated property can “transfer” income to younger family

members in lower tax brackets. But be aware of the Kiddie Tax issues.

5. Kiddie Tax planning is an interesting corner of the tax planning world. Give

children income producing assets early in life, and take advantage of the stepping up of the Kiddie

Tax. The first $2100 of income each year is taxed at preferential rates – the first $1050 is tax free

and the next $1050 is taxed at 10%. Moreover, Massachusetts tax does not kick in until $8000, so

even income taxed at the parents’ tax bracket saves Massachusetts tax. Consider, for example, a

gift of $100,000 of blue-chip growth stocks with a combined 2% annual dividend and anticipated

4% annual growth rate.

6. Also think about WHICH assets to use for gifting. It makes a difference.

7. Transferring high-basis assets (e.g., cash) to reduce the estate and keep it

below the lifetime credit equivalent amount ($5,490,000 in 2017) means that all income tax

liabilities are eliminated on death under Code Section 1014 step-up in tax basis. Realize that the

income tax rates and the estate tax rate are often pretty close to equal, and income tax is sometimes

even higher than estate tax. Therefore, retaining appreciated assets in the estate is often the winning

strategy.

12 {B2223037; 16}

8. Remember the Massachusetts estate tax kicks in above $1 million in estate

assets and goes as high as 16%. See the attached Exhibit B, discussing the strange calculation

formulas for Massachusetts Estate Taxes.

9. The Roth IRA, with permanent elimination of future income taxes on all

investment gains, is the way to go – if the federal government keeps its promises. Not everyone

trusts the U.S. government to keep its promises.

10. Think about making Roth IRA contributions for an amount equal to your

child’s earnings at the summer job. There is a cap of $5500 per year, but give the FULL amount of

the summer earnings each year.

11. Backdoor IRA. There are AGI limitations on the ability to make a

non-deductible annual contribution to a Roth IRA ($186,000 to $196,000 is phase out range in 2017

for married filers – $118,000 to $133,000 for single – and above those levels no contribution is

allowed) but there is no AGI limitation on a non-deductible contribution to a traditional IRA, even

if you already contributed the maximum to 401(k) or other qualified plans. You may be able to

make a non-deductible contribution to a traditional IRA and then later roll it over into a Roth IRA,

since there is no AGI limitation on the rollover transaction. Be aware that this works best if you

have no other existing IRA accounts; otherwise, income may be recognized on a prorated basis over

all the IRA accounts.

12. Interest rates are extremely low, so this continues to be a great time to do a

“freeze.”

13. GRATs are GREAT! Very low interest rates means enhanced transfers to

beneficiaries through a Grantor Retained Annuity Trust (“GRAT”).

14. Family loans for long periods at low applicable federal rates (“AFR rates”)

make a lot of sense as a very simple device to transfer wealth.

15. Installment sales to defective grantor trusts are a huge and leveraged play on

time value of money and freezing values at today’s value for estate and gift tax purposes.

16. Split-dollar loans can be used to finance large life insurance policies at the

abnormally low AFR rates.

17. But low interest rates take the juice out of Qualified Personal Residence

Trusts (“QPRTs”), unless the property can claim a huge discount and/or has great potential for

appreciation. This is an interesting topic to discuss further, because rental of the property by

parents after the QPRT period has expired becomes a de facto “gifting” strategy taxed at income tax

rates (to the kids). Furthermore, the discount is not only based on interest rates, but also on actual

life expectancy and even very elderly people can benefit from a QPRT if they survive the term. A

QPRT is often described as either “a win or a tie.” It may occupy or distract from other planning

opportunities, but it is never an outright loser. QPRT has potential asset protection benefits, the

wealth is tied up so kids can’t monetize the asset and spend or waste it, and the kids, if they die,

have fractional interest discounts.

13 {B2223037; 16}

18. Recognize that higher taxes means more wealth transfer if one uses a grantor

trust – parent pays the higher taxes for benefit of children and other heirs. Even if the parents are in

the maximum bracket, it’s no worse than a non-grantor trust.

19. Give Away Taxes. Charitable gifts transfer the taxes as well as making a

philanthropic act or statement. Sophisticated choices include private foundations, donor advised

funds, and charitable lead annuity trusts (“CLATs”).

20. But think about how BEST to make charitable transfers, and evaluate

carefully the 30% limitation versus the 50% limitation. Sometimes it actually makes sense to sell

stocks, pay the LTCG (and if necessary the NIIT) and then make gifts of cash at the 50% deduction

limitation rather than the 30% limitation.

21. On the investment side, increase portfolio emphasis on life insurance,

annuities and similar tax-deferred investments. Retirement plans are good, but Roths Rock!

B. Gifts of Appreciated Securities to Donees in Lower Tax Brackets, and

Income-Shifting in General – The “Kiddie Tax.”

1. Consider making transfers of appreciated securities in certain situations and

keeping your cash, which has full tax basis. For example, contributions to a charity may not

produce a full or substantial charitable deduction after taking account of the Pease Limitation and

the AMT impact on a taxpayer’s return, but to the extent that the taxpayer chooses to make

charitable contributions, low-basis stock will produce a charitable deduction equal to the fair market

value of the stock without having to pay the capital gains taxes.

2. Similarly, gifts of appreciated stock to an adult child (e.g., a child that is not

subject to the kiddie tax restrictions described below) will transfer the built-in gains to the child,

which is not optimal estate tax planning, but is very good income tax planning, especially if the

child is in the 15% tax bracket or lower, and therefore pays significantly lower capital gains tax on

the sale.

3. NOTE: Historically, wealthy taxpayers typically chose to transfer cash rather

than highly appreciated stock in order to maximize after-tax wealth transfer to the children.

However with the estate tax applicable only above $10,980,000 ($5,490,000 X 2) of assets for a

married couple in 2017 (subject to inflation indexing in future years), and with income tax rates

considerably more “progressive,” transfers of highly appreciated property that taxpayers plan to sell

anyhow may be more viable as an overall strategy, since children are likely to be in lower tax

brackets. Likewise, transfers of dividend-paying stocks will produce more after-tax wealth to

taxpayers in a lower tax bracket. On the other hand, if parents plan to hold assets until death, it is

better to hold highly appreciated property (because of the step-up in tax basis under Code Section

1014(a)). In general, income-shifting, especially through gifting of property, should be very much

in vogue in 2017 and beyond.

4. Kiddie Tax. The following two rules often affect the tax and reporting of the

investment income following gifts of securities to children:

14 {B2223037; 16}

a. If the child's interest, dividends and other unearned income total more

than $2100, part of that income may be subject to tax at the parent's tax rate instead of the

child's tax rate. See Form 8615 Instructions, Tax for Certain Children Who Have Unearned

Income.

b. If the child’s interest and dividend income (including capital gain

distributions) total less than $10,500, the child’s parent may be able to elect to include that

income on the parent's return rather than file a return for the child. See Form 8814, Parents’

Election To Report Child’s Interest and Dividends.

NOTE: For either of the foregoing rules to apply, the child must be required to file a return.

For filing requirement information, see Publication 929, Tax Rules for Children and Dependents,

and Do I Need to File a Tax Return? on IRS.gov.

5. Calculate the child's tax on Form 8615 and attach it to the child's tax return

when:

a. The child's unearned income was more than $2100,

b. The child meets one of the following age requirements:

i. The child was under age 18 at the end of the tax year

ii. The child was age 18 at the end of the tax year and the child’s

earned income did not exceed one-half of the child’s own

support for the year, or

iii. The child was a full-time student who was under age 24 at the

end of the tax year and the child’s earned income did not

exceed one half of the child’s own support for the year

(excluding scholarships),

c. At least one of the child's parents was alive at the end of the tax year,

d. The child is required to file a tax return for the tax year, and

e. The child does not file a joint return for the tax year.

6. A parent may be able to avoid having to file a tax return for the child by

including the child’s income on the parent’s tax return. To make this election, the parent should

attach Form 8814 to the parents from Form 1040 (PDF) when:

a. At the end of the tax year the child was under age 19 or under age 24,

if a full-time student,

b. The child’s interest and dividend income was less than $10,500 for

the tax year,

15 {B2223037; 16}

c. The child had income only from interest and dividends, which

includes Alaska Permanent Fund dividends and capital gain distributions,

d. No estimated tax payments were made for the tax year, and no prior

tax year’s tax overpayment was applied to the current tax year, under the child’s name and

Social Security number,

e. No federal income tax was withheld from the child’s income under

backup withholding,

f. The child is required to file a return unless the parent makes this

election,

g. The child does not file a joint return for the tax year,

h. The parent is the parent qualified to make the election or files a joint

return with the child’s other parent.

7. A child required to file Form 8615 may also be subject to the Net Investment

Income Tax (NIIT).

8. Examples of the Kiddie Tax.

a. Example 1. Ike has a 23 year old son, Junior, who earned $12,000 of

compensation income this year as a struggling law student. Ike gives Junior a family

heirloom, that is categorized as a collectible, valued at $100,000 with $0 basis. Junior sells

the family heirloom for his personal support. As a student under age 24, the kiddie tax

applies to Junior and he recognizes $2100 of gain at the kiddie tax rate and $97,900 of gain

at his parent’s rate. (NOTE: The parent’s tax rate is 28% on the collectibles gain, plus (very

likely) 3.8% for the NIIT, plus state capital gains tax.)

b. Example 2. Tina has a 19 year old son, Raymond, who has $150,000

of earned income as a popular lead guitarist of a local band after dropping out of school.

Tina gives Raymond a thoroughbred stallion that she has held for more than two years (the

long-term holding period for race horses), which stallion is valued at $100,000 with $0 tax

basis. Raymond, who receives a carryover tax basis and a tacking of the holding period,

then sells the stallion and uses the proceeds to buy a new convertible. As an non-student

over age 18 and because Raymond provides for more than 50% of his own support out of his

earned income, the kiddie tax does not apply to Raymond and he recognizes the $100,000 of

gain at his own rate.

c. Example 3. James has a 19 year old son, J. J., who has $30,000 of

earned income as a local artist. James gives J. J. a substantial stock portfolio as his

“inheritance” and the portfolio generates $100,000 annually in qualified dividends.

Raymond uses the dividends to support himself while he pursues his artistic career. As a

non-student over age 18, the kiddie tax does not apply to Raymond and he recognizes the

$100,000 of dividend income at his own federal income tax rate. NOTE: Since his earned

income is relatively low, he will be taxed on the qualified dividend income at the marginal

16 {B2223037; 16}

tax brackets for long-term capital gains, which in 2017 starts at 0% up to taxable income of

$91,900 and then at the 15% rate above $91,900. Since J. J. will have at the very least the

right to claim his personal exemption and standard deduction, most of his dividend income

should be tax free and only a modest portion taxed at the 15% tax rate. J. J. is also below

the $200,000 threshold for the NIIT. His parents, assuming they are in the maximum tax

bracket, would likely pay the maximum tax on the qualified dividend income of 20%, plus

3.8% for the NIIT.

C. S Corporation 10-Year Recognition Period Under Code Section 1374 Was

Shortened to Five Years Permanently in 2016.

1. When a C corporation converts to S corporation status, the corporation must

track its Net Unrealized Built-In Gains (“NUBIG”) and must pay a special corporate level tax at the

maximum corporate tax rate (currently 35%) if NUBIG is recognized by the corporation at any time

during the five-year recognition period following conversion to S status.

2. Congress shortened the recognition period on a permanent basis from ten

years to five years in 2015.

3. The 5-year rule is highly important for anyone with a former C corporation

that has converted to S corporation status and is currently counting down the years under Code

Section 1374.

D. The Rise of Roth IRAs. Roth retirement accounts are very intriguing, but often

misunderstood, as tax-advantaged investment vehicles. First of all, if income tax rates remain

exactly the same, and if no “outside” funds are used to pay income tax liabilities upon the

conversion of regular IRA to a Roth IRA, then the net after-tax benefits of a regular IRA versus a

Roth IRA are arguably identical.

2. Example: Assume a regular IRA account has exactly $1 million in assets,

and further assume that the investment strategy will produce exactly a 100% investment return over

the next 10 years. Assume that the Taxpayer will be subject to a 40% tax rate both in the current

year and in the tax year 10 years from now, and that the funds in the IRA will be used to pay the tax

liabilities that arise upon the conversion to a Roth IRA. Converting the regular IRA to a Roth IRA

results in $400,000 of tax liability in the current year, reducing the funds in the Roth IRA account to

$600,000. Over the next 10 years this amount doubles, to $1.2 million, which at that time can be

distributed tax-free (assuming the requirements of a qualified Roth distribution are met). By

contrast, if the taxpayer leaves the $1 million in the regular IRA account, and it doubles $2 million

over the next 10 years, and then the $2 million is distributed to the Taxpayer, subject to a 40% tax

rate, the Taxpayer will owe $800,000 of taxes at that time, and will be left with a net after-tax return

of $1.2 million. Thus, under this scenario, the regular IRA and the Roth IRA produce the same

after-tax return in the tenth year.

3. However, if one makes certain (seemingly practical) assumptions, one can

argue that a Roth conversion at this time may make a lot of sense.

a. First, given the current, rather steep stepping up of income tax

brackets, even if there is no further increase in tax rates, it would probably cost less to pay

17 {B2223037; 16}

tax on $1 million in 2017 (or especially if the conversion is spread out over this year and the

next few years) rather than try to distribute twice as much taxable income, namely $2

million or more, ten or more years from now. The point is that spreading recognition of $1

million of taxable income now is probably going to have a lower tax cost than distributing

the $1 million plus investment growth (e.g., $2 million) later in time. NOTE: It is possible

that the stepping up of tax brackets will somewhat offset or reduce this “back end bulge”

problem, but hopefully one’s investment portfolio performs better than the inflation rate.

b. Second, if marginal tax rates increase substantially further in future

years, then paying taxes at today’s rates may appear reasonable or even cheap in retrospect.

c. Third, and most compelling, the Taxpayer can convert the entire

$1 million held in the regular IRA account to a Roth IRA, and then pay the $400,000 tax bill

with non-IRA funds. This has the effect of allowing the taxpayer to contribute an extra

$400,000 to the Roth IRA. If this $1 million then doubles to $2 million over the next

10 years, the entire amount can be distributed thereafter without any further tax cost. This

ability to leverage the amount of funds contributed to the Roth IRA is clearly more

advantageous than continuing to hold the investment in a regular IRA for many taxpayers.

d. Converting to a Roth IRA is not so beneficial if the taxpayer believes

that the federal income tax rates applicable to him or her are likely to decline in future years.

Realistically, taxpayers and their advisors have to project the future direction of U.S. income

taxation, which is impossible, the future direction of the taxpayer’s income, which may be

somewhat possible, and then make educated guesses from there.

E. Booming Business in 1031 Like-Kind Exchange Transactions Threatened by

Pending Tax Legislation in December 2017.

1. In light of the significantly increased income tax rates starting in 2013 – and

especially the increase on long-term capital gains taxes – there has been a booming business in

using like-kind exchanges (“LKEs”) to defer recognition of taxable gain.

2. Real estate is an industry that is heavily dependent on LKEs, but there has

been an increased interest in the use of like-kind exchanges for classes of assets beyond or in

addition to real estate. For example, like-kind exchanges have been regularly used to exchange

assets such as motor vehicles, airplanes, radio and television spectrum licenses, farm animals, major

league baseball contracts, gold investments, and even various categories of intellectual property. If

you are interested, you may obtain a copy of the Author’s Outline entitled “Like Kind and Loving

It: 1031 Exchanges of Art, Airplanes, Automobiles and Wine Collections.”

3. Determining when and under what circumstances investment or business

property is “like-kind” is beyond the scope of this Outline, but see Chapter 19 of Joseph B.

Darby III, Practical Guide to Mergers, Acquisitions and Business Sales, Second Edition, published

by National Underwriter Company, a division of ALM Media, LLC, for a more complete discussion

of the business opportunities to utilize Code Section 1031.

18 {B2223037; 16}

4. The pending House and Senate Bills in December 2017 would both restrict

like-kind exchanges to real property and essentially eliminate art, airplanes, automobiles and wine

collections (and everything else).

F. Using the Principal Residence as Your Principal Tax Shelter.

1. A principal residence is eligible for an exclusion of gain on sale of up to

$250,000 for single individuals and $500,000 for married couples.

2. Generally speaking, the requirements for claiming an exclusion of gain from the

sale of a principal residence are relatively straightforward. In order to be eligible for the exclusion, the

taxpayer must have owned and used the home as a principal residence for at least two years during the

five years prior to disposition.

3. Whether or not a home is a principal residence is a question of fact for which

no bright line test exists. While physical presence by the taxpayer is generally the controlling factor,

all facts and circumstances are considered in the analysis.

4. To the extent that a taxpayer is able to exclude the gain for regular income

tax purposes, it will also excluded from the NIIT (unlike gain from the sale of a second home) and

so tax-smart investing in 2017 and beyond literally begins at home

5. The pending tax bills would both rather dramatically restrict this popular

exclusion provision. The bills both require ownership and use as a principal residence for five of

eight prior years, among other limitations.

G. Why Real Estate Works So Well as a Tax Shelter.

1. Real estate embodies many smart tax-planning strategies.

2. You can offset losses from one real estate rental activity (a “passive activity

loss,” or “PAL”) against income or gain from another investment (a “passive income generator” or

“PIG”). Moreover, you can control whether you are creating PALs or PIGs by how much debt you

put on the property.

3. Example 1. X buys a building for $1 million that produces $100,000 of net

rental income (a PIG). X then buys a second building with enough interest-only debt so that it

produces a net rental loss of -$100,000 (a PAL). X can offset the income from the PIG with the

PAL, to produce zero taxable income. Meanwhile, the properties will throw off significant cash

flow because of the depreciation. Note that it is often possible in to obtain interest-only debt on the

property, and also qualified non-recourse debt, and X can therefore configure his debt arrangements

to minimize risk, minimize income taxes, and maximize current cash flow.

4. Example 2. After a few years, both real estate rental properties do well, the

annual rents increase, and property 1, the PIG, becomes a bigger PIG while property 2, the PAL,

becomes a skinnier PAL and eventually turns into a small PIG (perhaps called a PIGlet?). The

dreaded specter of taxable income looms. Fortunately, X decides to refinance properties 1 and 2

and use the loan proceeds to buy property 3. Under the interest tracing rules the interest on the

19 {B2223037; 16}

refinancing loans is deductible with respect to the purchase of property 3, which will turn property 3

into a PAL, and the losses from property 3 can be used to offset the taxable income generated by

properties 1 and 2. All three properties continue to generate cash flow thanks to depreciation.

5. You can eventually exit from real estate investments using either of two

strategies:

a. Code Section 1031 allows you to rollover the sale proceeds into a new

“real estate” property if you want to shift market, location, or other strategic redeployment

of capital.

b. Even the “worst case” is pretty good: You recognize all the

accumulated depreciation over many years later as “unrecaptured Section 1250 gain,” pay a

special federal-level capital gains tax rate of 25% on such gain in the year of sale (after you

have claimed depreciation deductions worth as much as 39.6% in tax benefits many years

earlier), and you pay LTCG tax rates on the appreciation in value above the original

purchase price thanks to Code Section 1231.

c. If you qualify as a real estate professional and meet the material

participation requirements, then there no NIIT on you “investment” gains.

H. Life Insurance Products.

1. The Author of this Outline has never been a particularly strong fan of life

insurance products as investment assets per se. Instead, the most clear-cut situations in which life

insurance made sense included the following:

a. Purchasing what might be called “death insurance”, pursuant to which

a young working couple with young children could insure against premature death of the

breadwinners by having term insurance at fairly low premiums and with a high death

benefit, to hedge against the risk that either or both of the parents might die prematurely

before entering their high income earning years. For example, a 35-year old husband with a

wife and two young children might buy several million dollars of term life insurance, at a

relatively low annual premium, to insure that his family will have the money to raise the

children and send them through college, in the case he were killed in an auto accident the

next week.

b. The other common use was for what might be called “estate tax

insurance,” pursuant to which a married couple would purchase a second-to-die policy,

expecting to pay a lengthy but relatively low fixed premium, and which insurance would pay

a very substantial cash death benefit (e.g., millions of dollars) which could then be used to

pay the estate tax of the second-to-die spouse. This strategy was especially beneficial for a

married couple with substantial illiquid assets, such as real estate, a family business, or any

other similar assets where the value of the assets in the estate of the latter-to-die spouse

(absent an effective and aggressive estate tax planning) would result in a substantial estate

tax liability and the estate would lack the liquidity to pay the estate tax.

20 {B2223037; 16}

2. Because of the significant increase in income tax rates and the opportunity

for a life insurance product to accumulate tax-free build up within the policy and then make tax-free

loans (but subject to interest) to the policyholder, there is now a greater potential to create an

investment vehicle that produces strong economic returns coupled with low or even zero income tax

consequences and very minimal adverse estate tax consequences, all wrapped up into one

sophisticated package.

3. The illustration provided separately by the Author shows how this might

work. NOTE: This is not an endorsement of any company or any product, and merely illustrates a

possible strategy that treats the life insurance product primarily as a tax-deferred investment

vehicle.

a. A 55-year old professional earning a good income decides to invest

$50,000 per year for 12 years into a whole life insurance product, beginning at age 56 and

with the final payment contributed at age 68, when the individual anticipates retirement.

b. Over 12 years, the cumulative premium is $600,000. Some portion or

all of this $600,000 represents the “tax basis” of the owner in the insurance policy.7

c. Starting at age 69, the policy owner begins making annual

distributions to himself, starting with $21,382, and building up at a rate of 5% per year over

the ensuing years. The initial distribution will be a tax-free return of tax basis in the life

insurance policy, if the policy is in fact properly classified as an insurance policy. This is a

critical element because if it fails to meet financial guidelines at the onset as set forth in the

definition of life insurance, the arrangement may be treated as a modified endowment

contract, and treated therefore as an annuity, meaning that some or all of the initial

distributions will be treated as a taxable income. Partial taxability is not the end of the

world, but it does change the after-tax net benefit of the investment structure. The goal is to

make sure the product qualifies as a life insurance product and enjoys the advantages of tax-

free distribution of tax basis first, and the ability to make loans that are characterized as

loans, and not distributions.

d. At some point, the tax basis in the investment is depleted and brought

down to zero, and thereafter the cash advances are treated as loans rather than as

distributions.

e. There are two ways the insurance industry can account for loans, and

in the illustration shown, the loan is treated as a separate and distinct financial transaction,

not as a reduction in the cash surrender value of the policy. This means that the cash

surrender value, unreduced by the loan amounts outstanding, continues to earn a dividend

return. The dividend return is significant because it offsets in part the interest that will be

charged on the loans. Moreover, since the dividends and the loan interest rate are likely to

be somewhat correlated both if inflation kicks in or, in all events, as investment returns and

an interest rate returns vary up and down over time, and this correlation will help make sure

7There is a fairly significant debate as to what the proper calculation is for the tax basis in a life insurance product. The

IRS is currently arguing that the tax basis needs to be reduced by the value of the annual death benefit enjoyed by the

insured individual, but the issue is the subject of on-going dispute.

21 {B2223037; 16}

that there is probably a relatively modest spread over time between interest costs and

dividend distributions. For example, the spread between the dividend return and the interest

rate cost might be 2% or 3%, rather than the full amount of the interest rate charged on the

loan. This is pretty important, because it hedges the risk that rising interest rates could

completely devastate the economic value of the investment. It is not a complete investment

hedge, but it does provide some element of protection.8

f. The tax advantages of this structure should be familiar to accountants

and other tax planners because it is almost identical to the manner in which a private

company, e.g., an S corporation, returns value to its shareholders. Obviously, shareholders

in an S corporation can make distributions to themselves that are first a return of outside tax

basis, and, if the tax basis is brought down to zero, it is pretty common to make loans from

the company to the shareholders that would provide tax-free access to corporate cash. The

difference is that, unlike an S corporation or an LLC, the life insurance policy is able to do

an internal tax-free build up initially (tax-free to the owner of the policy) and then can lend

the money out, thereby providing both a tax-free internal building up of wealth and then

tax-free access to that internal wealth build up. An S corporation offers the second

opportunity, but not the first.

g. This is not an endorsement of any company or product, but simply

raises the issue of looking more closely at the investment benefits of life insurance policies

because of their unique tax attributes. Note that in the projected calculations the policy is

assumed to be owned by the insured and is includible in his estate. The death benefit is

initially set at $1 million, and the value does not significantly increase above that amount

over the many years of the projected ownership of the policy. Rather, beginning around age

90, the cash surrender value starts to decrease rapidly and goes down to a comparatively

modest amount of $210,000 at age 100. The point is that this offers a way to have an

investment asset that has a lot of value, but does not result in a substantial estate tax liability

at the end of the ownership period, because the death benefit is actuarially diminished by the

accumulation of the outstanding loans over time. In effect, the death benefit is being used to

pay off the accrued loan balance and accrued interest of the policy, so that in effect it

becomes a self-created and self-funded viatical arrangement.

h. The Author of this Outline has always noted with candor that life

insurance companies and other insurance companies tend to be quite profitable, and that

profit is earned through the use of your money. If you could invest the money as they do,

and cut out the middleman, you would get a better economic return on your investment than

life insurance offers. However, your investments in the stock market are depleted each year

by the taxes imposed on interest, dividends and capital gains, and these tax costs rose

dramatically for higher earning individuals under ATRA-2012. It is not a level investment

playing field, and so insurance deserves to be considered in the investment mix going

forward. A taxpayer should evaluate an insurance purchase with good advisors and open

eyes, but clearly the higher the tax rates on interest, dividends and capital gains, the more

8It is important to understand what internal accounting mechanism is used by a particular insurance provider. Make

sure that they show the tax consequences of making the loans and how it affects their anticipated internal build up once

the outside tax basis has been depleted and the policy is providing loans to the owners.

22 {B2223037; 16}

advantageous one is likely to find life insurance as an investment asset, in addition to the

other two prominent uses noted above.

I. Liquidating an Existing Charitable Remainder Trust.

1. The idea is that an existing charitable remainder trust (“CRT”) structure can

be liquidated “early” on a win-win basis. The taxpayer with the lead annuity has an asset that can

be characterized as a capital asset, and therefore sold at capital gains rates, even though it would

otherwise produce a long schedule of ordinary income paid over a significant period of time.

2. The charity that is the remainder beneficiary has a strong interest in such a

termination because, by liquidating the lead interest, it can accelerate its access to the economic

benefits of the remainder interest. The concept is to sell the lead interest to the charity for a

promissory note, so the charity immediately thereafter owns the entire beneficial interest in the

underlying property.

3. The trust then sells the underlying property, enjoying a non-taxable

recognition of gain, and uses the sale proceeds to pay off the promissory note, which in turn

produces long-term capital gain to the taxpayer selling the lead annuity interest.

NOTE: It would not be appropriate to set this up as a step transaction, but it is a viable

strategy for an existing “old and cold” CRT.

J. Set up a New CRT in Order to Produce an Up-Front Income Tax Deduction.

1. This is really an income tax strategy where the goal is to manufacture and

create tax deductions at a point in time when, for example, the taxpayer recognizes a very large

amount of income, e.g., from the exercise of non-qualified stock options or other similar ordinary

income transactions.

2. The reason that a CRT makes more sense than a charitable lead annuity trust

or other similar device is that the charitable lead trust deduction is subject to a 30% limitation on

deductibility, whereas the CRT will produce a deduction eligible for the 50% limitation on

deductibility and is therefore more usable and efficient. Moreover, after a few years, it may lead

into the other strategy noted above.

K. Combining of Income Tax and Estate Tax Planning.

1. Income tax planning and estate tax planning have clearly merged into a

larger, more integrated planning environment in recent years.

2. The single biggest factor is the step-up in tax basis under Code

Section 1014(a), which, in this era of very high unified estate and gift tax credits, makes it possible

to retain highly appreciated assets in an estate, avoid federal income taxation (but possibly not state

taxation) and also avoid paying federal income tax on the appreciation of investment assets.

3. Integrated tax planning for the wealthy will involve strategies for making

money, keeping money and then passing it on to heirs, charities and other favored persons. All

23 {B2223037; 16}

three steps need to be implemented effectively, and they are interactive in most cases, calling on

both early wealth-planning strategies and early income tax planning strategies.

L. Taxpayers Will Need to Reconsider Their Investment Strategies.

1. Taxpayers have modified investment decisions based on the fact that federal

income taxes on capital gains and qualified dividends for high-income taxpayers increased by 8.8%

compared to 2012.

2. These tax rates are still well below the maximum rates imposed on interest

income, royalty income, and other forms of ordinary income, but taxpayers may consider more

carefully the possibility of investing in growth stocks that pay low dividends and in effect reinvest

profits within the company, allowing for a deferral of tax.

3. Other intriguing possibilities include investing in tax-exempt obligations of

state and local government (though with a strong caveat to consider risks, since state and local

government finances are increasingly shaky) and also the use of tax-free build up through life

insurance products and Roth IRA accounts, as discussed elsewhere in this Outline.

M. Monitor and Plan for Recognition of Capital Gains.

1. The increase in the capital gains tax rate above certain AGI thresholds

($418,400 for single and $470,700 for married, in 2017), and the imposition of the NIIT on NII at

significantly lower AGI thresholds (frozen at $200,000/$250,000 for single/married) suggests that

taxpayers should carefully evaluate the years in which they will recognize capital gains, recognize

offsetting capital losses, and manage recognition of passive income and passive losses, all in order

to make sure these transactions are timed and coordinated in order to maximize the offsetting

positions and minimize the net taxable income or gain.

2. This is easier to say than to do. That said, moving losses forward and

deferring gain recognition is always a standard strategy in capital gains management. The NIIT is a

bigger and more complicated issue because the thresholds are low and essentially sinking (by virtue

of not being indexed), but this also suggests repositioning family gain recognition to lower brackets

(e.g., gifts of highly appreciated property to children and grandchildren who are at lower tax

brackets).

VI. FOR BUSINESSES, INCOME TAX PLANNING IDEAS IN 2017 AND BEYOND

A. Converting to S Corporation Status to Avoid Medicare Taxes.

1. Taxpayers for years used S Corporation status to avoid the 2.9% HI tax on

net earnings from self employment, by paying a low level of “reasonable” compensation subject to

the HI tax, and then distributing the rest of the profits through the K-1.

2. This strategy has continued to work for active shareholders in an

S Corporation, who are able to treat K-1 distributions as active income not subject to the HI tax (the

same strategy works for the new 3.8% HI tax) and also works to avoid the new NIIT tax on passive

income, which do not tax active income distributed by an S corporation trade or business.

24 {B2223037; 16}

3. By contrast, owners of a single member LLC will likely be subject to the full

3.8% tax on all income derived from the LLC. NOTE: Income allocated to shareholders in an

S Corporation are subject to NIIT.9

4. The proposed tax bills both have complicated new provisions on

pass-through entities that are designed to lower tax rates (based on invested capital) but also modify

the ability to play games with the amount of income subject to either FICA or NIIT taxation. The

bills also seem to eliminate distinctions between S corporations and LLCs. There is a distinct

possibility that these rules could lead to a return in some cases to C corporation status as the

preferred operating vehicle for at least some businesses.

5. Note that even in recent years some smaller businesses have operated as

C corporations in order to take advantage of the lower tax rates on the first $50,000 or $75,000 of

income. Similar opportunities may arise, especially if the C corporation rate is reduced to 20%

while individual (and pass-through) rates remain at 35% or above.

B. Taxation of C Corporations.

1. The corporate tax rate would drop from 35% (and higher at some levels due

to phase-outs) to a maximum of 20%, and (in the House Bill but not the Senate Bill) 25% for

personal service corporations.

2. This rate reduction is both termendously beneficial to U.S.-based

corporations and also should end the embarassing “expatriation” problem that has afflicted the U.S.

business community over the past ten years. See the Author’s article, “Building the New Berlin

Wall,” which excoriates the current U.S. policy of trying to prevent U.S. corporations from

“inverting” in order to escape the highest corporate tax rates of any major country.

VII. STRATEGIES FOR ESTATE AND GIFT TAX PLANNING FOR 2017 AND

BEYOND

A. Income Tax Strategies.

1. Estate planning in 2017, like all prior years, consists of three basic principles:

(1) use all your deductions, exemptions and exclusions available under the Internal Revenue Code,

(2) use the deductions, exemptions and exclusions as early in time as possible, so that the

subsequent income and subsequent growth from those transferred assets inures to the benefit of the

next generation rather than the present generation, and (3) take appropriate steps to reduce the

valuation placed on transferred assets, such as through the use of GRATs, installment sales of

partnership interests to defective grantor trusts, and a variety of other strategies.

2. The estate tax provisions for the moment are comparatively favorable

compared to historic standards, because the $5,490,000 exemption per person, which is doubled to

almost $11 million for married couples, and thanks to the enactment on a permanent basis of

“portability,” means that married couples that have less than $11 million of assets (and this will

9 See Treas. Reg. §§ 1.1411-1(f)(1), 1.1411-6(a).

25 {B2223037; 16}

continue to be indexed for inflation going forward) will generally not be subject to estate and gift

tax liabilities.

3. That said, any taxpayers with substantially more assets than the $11 million

threshold may also be in for an early Christmas present, if the lifetime exemption amount is

approximately doubled to $10 million per person ($20 million for a married couple).

4. The number of people in the estate tax regime each year is already very

small. The Joint Committee on Taxation estimates that 99.8% of decedents each year will pay zero

estate tax, and only 0.2% – 2 out of every 1000 decedents – will play ANY federal estate tax.

B. Portability Is Complicated and Valuable.

1. Tax advisors and accountants will need to focus on utilization of portability.

Basically, if a married spouse dies without using the full $5 million unified estate and gift tax credit

($5.49 million in 2017, as adjusted for inflation), the surviving spouse can use it. However, there

are various rules that affect when the surviving spouse can use it, especially if the surviving spouse

subsequently remarries. Using this to maximum effect will be an important issue.

2. Note that the lifetime exclusion amount is “frozen” (i.e., ceases to be indexed

for inflation) on the death of the first spouse, and meanwhile the GST exemption is not portable at

all. Therefore, using these tax attributes early and effectively will continue to be an important part

of estate-planning for wealthy individuals. However, note that the onerous impact of the NIIT rules

on trusts in particular will complicate the structuring of “dynasty” trusts going forward. See the

further discussion on Trust Income Taxation, below.

3. Complicating this exercise is the increased benefit derived from a step-up in

tax basis under Code Section 1014, which may in some cases militate in favor of using portability to

delay the “step up” event until the death of the second-to-die spouse, assuming assets generally

appreciate in value over longer periods of time.

C. Pay Attention to MA Estate Tax.

1. Here in Massachusetts, while the federal threshold of $10 million pushes an

awful lot of people out of the estate planning arena for federal purposes, Massachusetts continues to

have a decoupled Massachusetts estate tax that takes effect upon $1 million of assets.

2. The “simple” solution to Massachusetts estate tax planning is simple and

glib: Move! In particular, many MA residents later in life choose to change residency to a state

such as Florida without an estate tax. However, the Massachusetts Department of Revenue is very

aggressive about auditing residency issues, especially where a taxpayer retains a residence in

Massachusetts, and where that residence is the former principal residence. Massachusetts usually

audits residency issues in connection with income tax returns, but will probably pay increasing

attention to residency in connection with estate tax audits as well.

3. With all these factors, for a large portion of the client base of a typical law or

accounting firm, estate planning will probably be more focused on Massachusetts estate tax

planning rather than federal tax planning.

26 {B2223037; 16}

D. Trust Income Taxation is Complicated and Brutal.

1. The secret hidden bomb in the ATRA-2012 was the imposition of the NIIT

on trusts. The NIIT tax kicks in for individuals at $200,000 of MAGI for single filers and $250,000

for married filing jointly, but, for trusts, it kicks in at the threshold at which the maximum tax rate

takes effect, e.g., $12,500 for 2017. The major stunner here is that while trusts can typically

distribute out their distributable net income (“DNI”) to beneficiaries and thereby pass the income

from the trust out to the beneficiaries, so that the NIIT applies, if at all, at the beneficiary level,

trusts typically do not pass out capital gains. This means that if a trust sells substantial capital

assets, ranging from real estate to stock to bonds to whatever, and the trust instrument does not

provide for the distribution of capital gains as part of the trust income (that is certainly the situation

for a large majority of trusts), then the effect is that capital gains at the trust level will be subject not

only to a 20% capital gains tax rate, but also a 3.8% health care tax.

2. Although it is pretty unusual in most circumstances, a trust can elect to treat

capital gains as part of the trust income, and thus as part of distributable net income, and potentially

LTCG recognized at the trust level could then be distributed and taxed at the capital gains rates of

the beneficiaries, just like the distribution of trust income from interest, dividends, royalties and

similar investments. However, the trust instrument needs to provide for this, or at least provide for

the trustee to make a reasonable determination of the allocations between principal and income

under The Massachusetts Principal and Income Act (MGL Section 203D). These distribution

decisions are probably locked in place for the vast majority of existing trusts, and so the capital

gains for these trusts will be subject to the 20% capital gains tax plus the 3.8% NIIT. A new trust

will have the opportunity to determine how best to treat capital gains under these circumstances.