birla sunlife debt mutual funds for investing mutual fund advisor anandaraman @ 944 529-6519

TRANSCRIPT

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Know Your Fund

• It is an actively managed income scheme that is largely driven by two guiding factors:

• “Absolute return bias” where it endeavors to preserve the purchasing power of the capital.

• Generating “total returns” that comprises of capital gains and interest income

o For the purpose of exploring avenues of capital appreciation, it seeks to invest in government securities, corporate bonds etc.

o To capture higher interest income, it seeks to invest in structured credit instruments

• It may be considered by investors with investment horizon of 9 months and above.

Private & confidential. For internal circulation only

Outlook

The month gone by was by far the most action packed month in the recent past. As if base changes of the key macroeconomic variables weren’t enough to keep markets busy and buzzing, the economic survey, the railway budget, the scheduled as well as a surprise RBI policy meet brought interesting twists to almost every day of the shortest month in the calendar.

Growth

With the rebasing of GDP growth to 2012=100, previous years (FY13 and FY14) growth rates were revised upwards markedly. In light of this, the advance estimates for FY15 were being keenly watched by markets. Central Statistic Organisation has estimated growth in FY15 to rise to 7.4%, up 50bps from FY14’s rate of growth. While the increase is broadly in line with expectations, the levels have been restated as GDP growth now also measures value addition. Accordingly, we expect FY16 GDP to grow further to ~8.4%. A major driver of this is the reflationary impact of oil price decline. As far as the high frequency indicators are concerned, correcting for data capturing and sudden revision related issues, general economic activity seems to be picking up so far. (source: MOSPI, BSLAMC internal research)

Inflation

CPI inflation also saw a base change (2012=100). The key take away from this exercise was the move away from arithmetic mean to geometric mean, with the objective of reducing volatility caused by some items. This is expected to pull a statistical downward pressure on CPI. Resultantly, headline CPI inflation came in at 5.1% in January’15, rising from 4.3% in Dec’14 (new base). Core CPI also declined to 3.9%, most of this being a reflection of decline in the price of crude. WPI inflation turned negative again to -0.4% for the month of Jan. Apart from fuel disinflation, the core WPI inflation has also been on a softening trend, courtesy the commodity bear cycle underway. Continuous moderation in both retail and wholesale inflation, created conditions conducive for monetary easing. (source: MoSPI)

External Equation

Owing to falling oil prices, trade Deficit for Jan moderated by ~1bn$ to 8.3bn$. Keeping aside the price effect, the volume of oil imports seems to be growing. The same hold true for exports, where net of oil exports, the story doesn’t look as gloomy. We expect CAD in Q3 to rise to ~12-13bn$ and FY15 to range between ~25-27bn$. This is expected to improve further in FY16. (Source: Ministry of Commerce, BSLAMC internal Research)

Fiscal front

Even after exhausting more than the budgeted fiscal deficit by the month of Jan, the finance minister in the revised estimates for FY15 assured that 4.1% of GDP would be acheievd as the fiscal deifict number. For FY16, in a welcome deviation from the FRBM roadmap laid out by the Kelkar committee, the finance minister decided to defer it by a year and announced a fiscal deficit of 3.9% of GDP for FY16 (as against 3.6% suggested by the Kelkar committee). A large part of this etra stimulus in both a direct and an indirect (via the leverage route) is expected

Birla Sun Life Dynamic Bond Fund(An Open-ended Income Scheme)

Savings

Solutions

March 2015

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

Portfolio Action and Strategy

As on 27th Feb 2015, the modified duration of the scheme stands at 3.15 years and the YTM is 7.89%. The higher portfolio duration had been built chiefly through exposure to Sovereign Bonds which currently accounts for ~60% of the portfolio.

After benefiting from the 10 year benchmark rally in the last few months, we have gradually reduced the duration in the portfolio. Going forward, for an “absolute return oriented fund” like BSL Dynamic Bond Fund we believe that the risk-reward proposition is in favour of a more conservative accrual led strategy while keeping sufficient leeway for any opportunity on duration from time to time.

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

to go for capital spending. This in turn is expcted to have a multiplier effect on growth. As supply side improves, this is expected to exert some disinflation in the medium term. The FY16 Union Budget chose growth over consolidation in the backdrop of improved macroeconomic environment, expressed realistic growth targets and pragmatism basis the current stage of the economic cycle that we are in. RBI acknowledged these efforts and in another out of policy move, cut rates by 25bps on Mar 4th, taking repo to 7.5%. (Source: RBI, Ministry of Finance)

One more key reason behind this move in our view is the legislation on monetary policy framework which binds RBI to the mandate of maintaining price stability. While the operating procedure needs some more clarity, RBI as per this monetary policy framework would have to ensure CPI inflation of 4% by FY18 (starting Fy17). (Source: Ministry of Finance, RBI)

All this is likely to have the following impact on portfolio positioning-

Duration Funds shall be impacted positively by the budget and the rate cut. Formalization of monetary policy framework, focus on infrastructure creation, and credible budget math marginally outweigh negatives such as rise in service taxes, and fiscal stimulus from the Government.

Credit funds shall be benefitted because of focus of the government to bring back growth. A decent growth in the economy shall benefit the borrowers to improve their creditworthiness and command tighter spreads over the base curve.

No impact on Liquidity funds.

Private & confidential. For internal circulation only

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

** Represents thinly traded/ non traded securities and illiquid securities. Total Percentage of thinly/non traded securities is 8.57%.

Investment Objective

An Open-ended income scheme with the objective to generate optimal returns with high liquidity through active management of the portfolioby investing in high quality debt and money market instruments.

Rating Profile

Issuer % to NetAssets

IssuerAssets

% to Net

All data provided are as on February 27, 2015 unless otherwise provided

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Fund Details

Fund Manager : Mr. Maneesh Dangi

Managing Fund Since : September 12, 2007

Total Experience : 13 years

Date of inception : September 27, 2004

Nature of the scheme : An Open-ended Income Scheme

Default option : Quarterly Dividend Reinvestment

Monthly Dividend Sweep OptionFresh Purchase : ` 5 lacsAdditional Purchase : ` 1000/-

For Other OptionFresh Purchase : ` 5000/- Additional Purchase : ` 1000/-

Redemption Cheques : Within 10 working days issued

Systematic Investment : Available Plan (SIP)

Systematic Withdrawal : Available Plan (SWP)

Systematic Transfer : AvailablePlan (STP)

Regular Plan^Growth : 24.2736Quarterly Dividend : 11.3119Monthly Dividend : 10.9768Dividend : 10.5450

Direct Plan*Growth : 24.4810Quarterly Dividend : 11.4389Monthly Dividend : 10.9628

Benchmark : CRISIL Short Term Bond Fund(w.e.f 27th May 2013) Index

Entry Load : Nil

Exit Load** : For redemption / switch-out of units(w.e.f October 01, 2014) within 365 days from the date of

allotment: 1.00% of applicable NAV.

For redemption / switch-out of units after 365 days from the date of allotment: Nil.**Exit Load is NIL for units issued in Bonus & Dividend Reinvestment.

Modified Duration : 3.15 Years

Yield to Maturity : 7.89%

Standard Deviation : 2.98%

Key Features

Plans / Options & NAV (As on February 27, 2015)

Load Structure (Incl. for SIP)

Other Parameter

Dividend : 10.5545

Note:Standard Deviation is calculated on annualised basis using 1 year history of monthly returns, source: MFI Explorer.^This Plan under the scheme continues for fresh subscription and has been renamed w.e.f October 01, 2012 vide addendum no.33/2012 dated September 28, 2012 and is referred to as “Regular Plan” vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.*Separate Option for direct investments under SEBI Circular no. CIR/IMD/DF/21/2012 dated September 13, 2012 with effect from January 1, 2013 vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.

Disclaimer: This document is strictly confidential and meant for private circulation only and should not at any point of time be construed to be an invitation to the public for subscribing to the units of

Birla Sun Life Mutual Fund. Please note that this is not an advertisement. The document is solely for the information and understanding of intended recipients only. If you are not the intended recipient,

you are hereby notified that any use, distribution, reproduction or any action taken or omitted to be taken in reliance upon the same is prohibited and may be unlawful. Views expressed herein should

not be construed as investment advice to any party and are not necessarily those of Birla Sun Life Asset Management Company Ltd.(BSLAMC) or any of their officers, employees, personnel,

directors and BSLAMC and its officers, employees, personnel, directors do not accept responsibility for the editorial content. Wherever possible, all the figures and data given are dated, and the same

may or may not be relevant at a future date. Further the opinions expressed and facts referred to in this document are subject to change without notice and BSLAMC is under no obligation to update

the same. While utmost care has been exercised, BSLAMC or any of its officers, employees, personnel, directors make no representation or warranty, express or implied, as to the accuracy,

completeness or reliability of the content and hereby disclaim any liability with regard to the same. Recipients of this material should exercise due care and read the scheme information document

(including if necessary, obtaining the advice of tax/legal/accounting/financial/other professional(s) prior to taking of any decision, acting or omitting to act. Further, the recipient shall not

copy/circulate/reproduce/quote contents of this document, in part or in whole, or in any other manner whatsoever without prior and explicit approval of BSLAMC.

Mutual Fund: Birla Sun Life Mutual Fund

Asset Management Company/ Investment Manager: Birla Sun Life Asset Management Company Limited. CIN: U65991MH1994PLC080811

Registered Office: One India Bulls Centre, Tower - 1, 17th Floor Jupiter Mill Compound, 841, S. B. Marg, Elphinstone Road, Mumbai - 400013.

Private & confidential. For internal circulation only

Asset Allocation

Government Bond 55.48

Corporate Debt 6.87

Treasury Bills 3.85

Money Market Instruments 3.58

Floating Rate Note 0.68

State Government Bond 0.50

Margin Fixed Deposit 0.05

SWAP -0.06

Cash & Current Assets 29.06

Total Net Assets 100.00

Issuer % to Net RatingAssets

Issuer % to Net RatingAssets

Top Ten Portfolio Holdings

Government of India 59.32 Sovereign

Shriram Transport Finance Company Ltd IND AA+

Vodafone India Ltd 1.99 CRISIL A1+

Power Finance Corporation Ltd 1.77 CRISIL AAA

Reliance Jio Infocomm Limited 1.33 CRISIL AAA

Canara Bank 0.80 CRISIL A1+

2.45 CRISIL AA,

I L & F S Ltd 0.80 ICRA A1+

Tata Motors Finance Ltd 0.52 CRISIL AA

Housing Development Finance Corporation Ltd

State Government Securities 0.50 Sovereign

0.51 CRISIL AAA

Note: Risk is represented as:

(BLUE) investors understand that their principal will be at low risk

(YELLOW) investors understand that their principal will be at medium risk

(BROWN) investors understand that their principal will be at high risk

This product is suitable for investors who are seeking*:• income with capital growth over short term• investments in actively managed portfolio of high quality debt and money market

instruments including government securities.• low risk (BLUE)*Investors should consult their financial advisers if in doubt whether the product is suitable for them.

Product Labeling

-7.80%

0.00%

3.42%

7.71%

36.85%

59.82%

Unrated

Below AA

AA

AAA

Cash & Current Assets

Sovereign

Savings

Solutions

Birla Sun Life Income Plus(An Open-ended Income Scheme)

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Know Your Fund

• It is an actively managed income scheme that endeavors to generate income, through superior yields on its investments, at relatively

moderate levels of risk through diversified research based investment approach.

• Investments in a combination of bonds and government securities of varying maturities.

• The scheme has flexibility of changing the modified duration within a wide range depending upon fund managers’ view on market

conditions. Historically, the scheme has had a modified duration of as low as 3 months to as high as 10 years. Currently it endeavors to

maintain the modified duration of around 6-8 years.

• It may be considered by investors with investment horizon of 1 year and above.

Private & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

Outlook

The month gone by was by far the most action packed month in the recent past. As if base changes of the key macroeconomic variables weren’t enough to keep markets busy and buzzing, the economic survey, the railway budget, the scheduled as well as a surprise RBI policy meet brought interesting twists to almost every day of the shortest month in the calendar.

Growth

With the rebasing of GDP growth to 2012=100, previous years (FY13 and FY14) growth rates were revised upwards markedly. In light of this, the advance estimates for FY15 were being keenly watched by markets. Central Statistic Organisation has estimated growth in FY15 to rise to 7.4%, up 50bps from FY14’s rate of growth. While the increase is broadly in line with expectations, the levels have been restated as GDP growth now also measures value addition. Accordingly, we expect FY16 GDP to grow further to ~8.4%. A major driver of this is the reflationary impact of oil price decline. As far as the high frequency indicators are concerned, correcting for data capturing and sudden revision related issues, general economic activity seems to be picking up so far. (source: MOSPI, BSLAMC internal research)

Inflation

CPI inflation also saw a base change (2012=100). The key take away from this exercise was the move away from arithmetic mean to geometric mean, with the objective of reducing volatility caused by some items. This is expected to pull a statistical downward pressure on CPI. Resultantly, headline CPI inflation came in at 5.1% in January’15, rising from 4.3% in Dec’14 (new base). Core CPI also declined to 3.9%, most of this being a reflection of decline in the price of crude. WPI inflation turned negative again to -0.4% for the month of Jan. Apart from fuel disinflation, the core WPI inflation has also been on a softening trend, courtesy the commodity bear cycle underway. Continuous moderation in both retail and wholesale inflation, created conditions conducive for monetary easing. (source: MoSPI)

External Equation

Owing to falling oil prices, trade Deficit for Jan moderated by ~1bn$ to 8.3bn$. Keeping aside the price effect, the volume of oil imports seems to be growing. The same hold true for exports, where net of oil exports, the story doesn’t look as gloomy. We expect CAD in Q3 to rise to ~12-13bn$ and FY15 to range between ~25-27bn$. This is expected to improve further in FY16. (Source: Ministry of Commerce, BSLAMC internal Research)

Fiscal front

Even after exhausting more than the budgeted fiscal deficit by the month of Jan, the finance minister in the revised estimates for FY15 assured that 4.1% of GDP would be acheievd as the fiscal deifict number. For FY16, in a welcome deviation from the FRBM roadmap laid out by the Kelkar committee, the finance minister decided to defer it by a year and announced a fiscal deficit of 3.9% of GDP for FY16 (as against 3.6% suggested by the Kelkar committee). A large part of this etra stimulus in both a direct and an indirect (via the leverage route) is expected

March 2015

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Private & confidential. For internal circulation only

to go for capital spending. This in turn is expcted to have a multiplier effect on growth. As supply side improves, this is expected to exert some disinflation in the medium term. The FY16 Union Budget chose growth over consolidation in the backdrop of improved macroeconomic environment, expressed realistic growth targets and pragmatism basis the current stage of the economic cycle that we are in. RBI acknowledged these efforts and in another out of policy move, cut rates by 25bps on Mar 4th, taking repo to 7.5%. (Source: RBI, Ministry of Finance)

One more key reason behind this move in our view is the legislation on monetary policy framework which binds RBI to the mandate of maintaining price stability. While the operating procedure needs some more clarity, RBI as per this monetary policy framework would have to ensure CPI inflation of 4% by FY18 (starting Fy17). (Source: Ministry of Finance, RBI)

All this is likely to have the following impact on portfolio positioning-

Duration Funds shall be impacted positively by the budget and the rate cut. Formalization of monetary policy framework, focus on infrastructure creation, and credible budget math marginally outweigh negatives such as rise in service taxes, and fiscal stimulus from the Government.

Credit funds shall be benefitted because of focus of the government to bring back growth. A decent growth in the economy shall benefit the borrowers to improve their creditworthiness and command tighter spreads over the base curve.

No impact on Liquidity funds.

Portfolio Action and Strategy

Based on our constructive view on interest rates, the scheme continues to be positioned at longer end of the yield curve with a mix of GOI securities (GOIs) and State development loans (SDLs) with relatively lower exposure to corporate bonds. The scheme continues to maintain overall exposure to Government Bonds at ~90% of the net assets and ~5% in corporate debt as on 27th Feb 2015. Within the provisions and limitations of the SID, the choice of investing in GOI-SDL- Corporate bond would continue to depend on the relative valuation, and, the preference for one security over the other may change owing to which, overall maturity may vary from time to time The scheme has YTM of 7.84% and Modified duration of 7.13 years as on 27th Feb 2015.

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

Investment Objective

An Open ended Income Scheme to generate consistent income through superior yields on its investments at moderate levels of risk through a diversified investment approach. This income may be complemented by price changes of instruments in the portfolio.

Portfolio & Asset Allocation

Issuer % to Net RatingAssets

Issuer % to Net RatingAssets

Government Bond 89.93

8.60% GOI (MD 02/06/2028) 33.12 Sovereign

9.20% GOI (MD 30/09/2030) 16.26 Sovereign

8.12% GOI (MD 10/12/2020) 4.95 Sovereign

8.83% GOI (MD 12/12/2041) 4.57 Sovereign

8.08% GOI (MD 02/08/2022) 4.35 Sovereign

8.26% GOI (MD 02/08/2027) 4.14 Sovereign

8.27% GOI (MD 09/06/2020) 3.62 Sovereign

8.24% GOI (MD 15/02/2027) 3.20 Sovereign

8.30% GOI (MD 31/12/2042) 3.19 Sovereign

7.80% GOI (MD 03/05/2020) 2.69 Sovereign

8.40% GOI (MD 28/07/2024) 2.64 Sovereign

8.32% GOI (MD 02/08/2032) 2.31 Sovereign

8.83% GOI (MD 25/11/2023) 1.91 Sovereign

8.28% GOI (M/D 21/09/2027) 1.45 Sovereign

9.23% GOI (MD 23/12/2043) 0.79 Sovereign

8.24% GOI (MD 10/11/2033) 0.73 Sovereign

Corporate Debt 5.44

HDB Financial Services Ltd ** 1.97 CRISIL AAA

IDFC Ltd. 1.30 ICRA AAA

India Infradebt Ltd ** 1.07 CRISIL AAA

Hindalco Industries Ltd ** 1.02 CRISIL AA

ICICI Bank Ltd ** 0.06 CRISIL AAA

Power Finance Corporation Ltd ** 0.01 CRISIL AAA

Floating Rate Note 0.52

Power Finance Corporation Ltd ** 0.52 CRISIL AAA

State Government Bond 0.13

8.64% Jharkhand SDL (MD 06/03/2023) 0.05 Sovereign

9.55% Tamilnadu SDL (MD 11/09/2023) 0.03 Sovereign

9.56% Maharashtra (MD 28/08/2023) 0.02 Sovereign

9.45% Rahasthan SDL (MD 26/03/2024) 0.02 Sovereign

8.51% Punjab SDL (MD 10/04/2023) 0.00 Sovereign

SWAP -0.03

7.09% Rec Mibor & Pay Fix

(MD12/01/20) ICICISEC

7.30% Rec Mibor & Pay Fix

(MD29/12/2019) HDFCBK

Cash & Current Assets 4.02

-0.01

-0.03

Total Net Assets 100.00

Rating Profile

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

All data provided are as on February 27, 2015 unless otherwise provided

Disclaimer: This document is strictly confidential and meant for private circulation only and should not at any point of time be construed to be an invitation to the public for subscribing to the units of

Birla Sun Life Mutual Fund. Please note that this is not an advertisement. The document is solely for the information and understanding of intended recipients only. If you are not the intended recipient,

you are hereby notified that any use, distribution, reproduction or any action taken or omitted to be taken in reliance upon the same is prohibited and may be unlawful. Views expressed herein should

not be construed as investment advice to any party and are not necessarily those of Birla Sun Life Asset Management Company Ltd.(BSLAMC) or any of their officers, employees, personnel,

directors and BSLAMC and its officers, employees, personnel, directors do not accept responsibility for the editorial content. Wherever possible, all the figures and data given are dated, and the same

may or may not be relevant at a future date. Further the opinions expressed and facts referred to in this document are subject to change without notice and BSLAMC is under no obligation to update

the same. While utmost care has been exercised, BSLAMC or any of its officers, employees, personnel, directors make no representation or warranty, express or implied, as to the accuracy,

completeness or reliability of the content and hereby disclaim any liability with regard to the same. Recipients of this material should exercise due care and read the scheme information document

(including if necessary, obtaining the advice of tax/legal/accounting/financial/other professional(s) prior to taking of any decision, acting or omitting to act. Further, the recipient shall not

copy/circulate/reproduce/quote contents of this document, in part or in whole, or in any other manner whatsoever without prior and explicit approval of BSLAMC.

Mutual Fund: Birla Sun Life Mutual Fund

Asset Management Company/ Investment Manager: Birla Sun Life Asset Management Company Limited. CIN: U65991MH1994PLC080811

Registered Office: One India Bulls Centre, Tower - 1, 17th Floor Jupiter Mill Compound, 841, S. B. Marg, Elphinstone Road, Mumbai - 400013.

Private & confidential. For internal circulation only

Fund Details

Fund Manager : Mr. Prasad Dhonde

Managing Fund Since : Jan 11, 2010

Total Experience : 16 years

Date of inception : October 21, 1995

Nature of the scheme : An Open-ended Income Scheme

Default option : Dividend Reinvestment

Fresh Purchase : ` 5000/-

Additional Purchase : ` 1000/-

Redemption Cheques : Within 10 working days issued

Systematic Investment : Available Plan (SIP)

Systematic Withdrawal : Available Plan (SWP)

Systematic Transfer : AvailablePlan (STP)

Regular Plan^Growth : 62.9182Quarterly Dividend : 13.5259

Direct Plan*Growth : 63.6803Quarterly Dividend : 13.7673

$$the dividend option under the scheme have been renamed w.e.f December 26, 2014. Please refer addendum no, 59/2014 dated December 17, 2014 for further details.

Benchmark : CRISIL Composite Bond Fund Index

Entry Load : Nil

Exit load** : Nil(w.e.f December 01, 2014) **Exit Load is NIL for units issued in

Bonus & Dividend Reinvestment.

Modified Duration : 7.13 YearsYield to Maturity : 7.84%Standard Deviation : 4.87%

Key Features

$$Plans / Options & NAV (As on February 27, 2015)

Load Structure# (Incl. for SIP)

Other Parameter

Dividend : 9.9986

Dividend : 9.9992

Note:Standard Deviation is calculated on annualised basis using 1 year history of monthly returns, source: MFI Explorer.^This Plan under the scheme continues for fresh subscription and has been renamed w.e.f October 01, 2012 vide addendum no.33/2012 dated September 28, 2012 and is referred to as “Regular Plan” vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.*Separate Option for direct investments under SEBI Circular no. CIR/IMD/DF/21/2012 dated September 13, 2012 with effect from January 1, 2013 vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.

Note: Risk is represented as:

(BLUE) investors understand that their principal will be at low risk

(YELLOW) investors understand that their principal will be at medium risk

(BROWN) investors understand that their principal will be at high risk

This product is suitable for investors who are seeking*:• income with capital growth over medium to long term• investments in a combination of debt and money market instruments including

government securities of varying maturities• medium risk (YELLOW)*Investors should consult their financial advisers if in doubt whether the product is suitable for them.

Product Labeling

** Represents thinly traded/ non traded securities and illiquid securities.

-2.03%

1.02%

4.94%

6.01%

90.06%

Unrated

AA

AAA

Cash & Current Assets

Sovereign

Birla Sun Life Medium Term Plan(An Open ended Income Scheme)

Savings

Solutions

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Know Your Fund

• Scheme is positioned where the majority of the portfolio is intended to be invested in high quality AA and above rated papers.

• Within the provisions and limitations of the SID, the scheme intends to run the portfolio on an accrual which would involves buying a

bond and holding it till maturity thereby earning from the accruing of interest. This would enable to minimize the interest rate risk to a

large extent.

• The scheme intends to have a stable and disciplined duration profile in the portfolio in order to minimize the return volatility.

• The scheme intends to invest in papers having maturity up to 2-2.5 years.

• It may be considered by investors with investment horizon of approx 2 year and above.

The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for

asset allocation, investment strategy and scheme specific risk factors.

Outlook

The month gone by had a flurry of data releases over and above the regular ones. For one, there was an out of policy surprise rate cut by RBI

sighting reasons of more than anticipated decline in inflation and inflationary expectations moderating to single digits for the first time in 21 quarters (Source: RBI). Then came the rebasing of GDP numbers which completely changed the manner in which Indian economy was being looked at. After these, the RBI policy was being keenly watched for, especially for the commentary.

The base year revision for national account statistics was long pending. With the shift of base year to 2011-12 from 2004-05 and some

changes in methodology, the GDP growth rate for FY13 and FY14 from 4.7% and 5% to 5.1% and 6.9% respectively (at market prices)

(Source: MOSPI). The change is owing to expansion of data set and falling deflator. This suggests that the slowdown in India’s growth was probably overstated. We are now awaiting the advance estimates for FY15 to get more colour on how to estimate growth in India going forward. As for all the high frequency indicators, some revival is in sight. The composite PMI index has gone up to 53.3 from 52.5 in Jan from

Dec (Source: HSBC Markit), MHCV sales are registering strong YoY growth rates and so is demand for petrol and diesel, tourist arrivals have been gaining strength and similar trend is visible in air traffic. Most importantly, with oil prices plummeting, personal disposable incomes would get a push and this should facilitate more consumption. While more clarity is awaited on base and methodology change, keeping that

aside, we are looking at growth reviving from ~5.5% in FY15 to ~6.5% in FY16.

On the inflation side, as December numbers came lower than expectations, RBI, as pre-committed announced a 25bps rate cut on Jan 15th

2015. As favourable base effects waned off in December, CPI rose marginally to 5%, more importantly the underlying momentum declined for the first time since February 14. Also, core CPI moderated further to 5.2% in December. WPI inflation also rose marginally to 0.1%,

despite a decline in MoM terms, the YoY picked up due to base turning unfavourable (Source: MOSPI). Going forward, both the headline prints

could remain marginally higher, but that has largely got to do with the base as the momentum is that of moderation only.

Developments on the external front were largely as anticipated. With December trade deficit correcting sharply to 9.4bn$ on account of declining gold and oil imports, we are on track to see CAD for FY15 moderating to ~20bn$ form 32.4bn$ in FY14. (Source: Bloomberg). The decline in oil prices are expected to play a major role in this saving and take CAD to even lower levels in FY16 (Assuming oil price remains

around current levels).

Private & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

February 2015

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Private & confidential. For internal circulation onlyPrivate & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

We ended up exhausting ~100% of our budgeted target of fiscal deficit by December. While this would have raised some eyebrows, but in a

record event of raising ~ Rs 22,000 crores from its disinvestment in Coal India Limited (source: PIB), the government seems to be on track to

achieve its target fiscal deficit of 4.1% of GDP for FY15 (source: Ministry of Finance). Needless to say, expenditure compression would be inevitable in this exercise. The union budget for FY16 will the next big thing to watch. The policy corridors seem to be divided between

stepping up of public investment to aid growth and adhering to fiscal consolidation road map that the current govt. had intended to tread on.

From here on, quarterly GDP data as per the new method, combined CPI data based on new consumption patterns, Union Budget and

especially the quality of fiscal deficit shall be crucial data points for market directions. Till then we believe, the market shall be range bound.

RBI Governor kept his word and acted no sooner he felt it was a right prescription for the economy, to lower the benchmark rate. Accordingly he surprised the markets with an intermittent cut in mid January 2015. Bond yields (yield on 10 year benchmark security) fell more than 10 bps post rate cut to ~7.70% thus taking cumulative rally to about 100 bps on the benchmark over the last one year. This cut led the market

to believe that the RBI will follow the action with another cut on 3rd February 2015, but as expected by us, it did not materialize, and for the right reasons.

From rates perspective, we believe that the Repo is likely to go to 7.25% in 2015, but what is crucial is the pace of rate cuts. We believe, the cuts are more likely in H12015 which shall be rates positive, but what can keep lid on the prospective rally are large open market operations

(OMO) sales that are likely in FY16 and a debate on terminal policy rate in this cycle.

From portfolio perspective, we have moderated duration across our key portfolios. We have also swapped some less liquid securities for

highly liquid securities in order to stay agile in the times to come.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Private & confidential. For internal circulation onlyPrivate & confidential. For internal circulation only

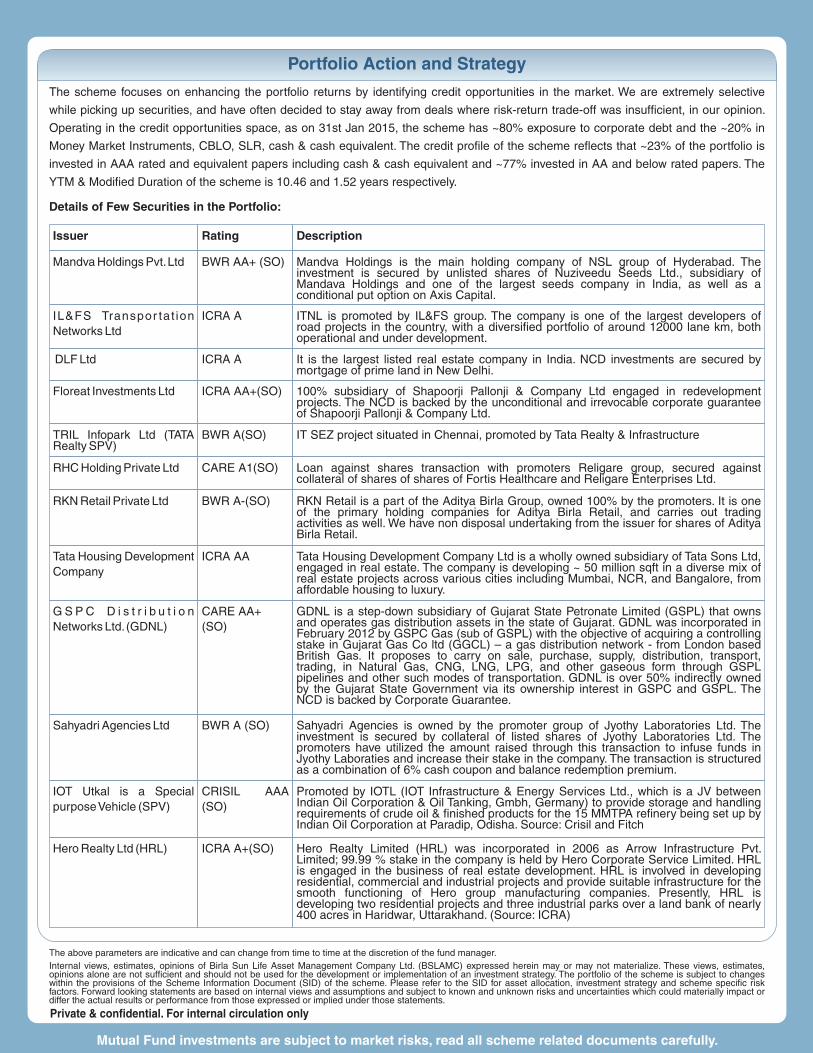

CARE AA+ (SO)

G S P C D i s t r i b u t i o n Networks Ltd. (GDNL)

GDNL is a step-down subsidiary of Gujarat State Petronate Limited (GSPL) that owns and operates gas distribution assets in the state of Gujarat. GDNL was incorporated in February 2012 by GSPC Gas (sub of GSPL) with the objective of acquiring a controlling stake in Gujarat Gas Co ltd (GGCL) – a gas distribution network - from London based British Gas. It proposes to carry on sale, purchase, supply, distribution, transport, trading, in Natural Gas, CNG, LNG, LPG, and other gaseous form through GSPL pipelines and other such modes of transportation. GDNL is over 50% indirectly owned by the Gujarat State Government via its ownership interest in GSPC and GSPL. The NCD is backed by Corporate Guarantee.

BWR A (SO)Sahyadri Agencies Ltd Sahyadri Agencies is owned by the promoter group of Jyothy Laboratories Ltd. The investment is secured by collateral of listed shares of Jyothy Laboratories Ltd. The promoters have utilized the amount raised through this transaction to infuse funds in Jyothy Laboraties and increase their stake in the company. The transaction is structured as a combination of 6% cash coupon and balance redemption premium.

ICRA AATata Housing Development Company

Tata Housing Development Company Ltd is a wholly owned subsidiary of Tata Sons Ltd, engaged in real estate. The company is developing ~ 50 million sqft in a diverse mix of real estate projects across various cities including Mumbai, NCR, and Bangalore, from affordable housing to luxury.

Portfolio Action and Strategy

The scheme focuses on enhancing the portfolio returns by identifying credit opportunities in the market. We are extremely selective

while picking up securities, and have often decided to stay away from deals where risk-return trade-off was insufficient, in our opinion.

Operating in the credit opportunities space, as on 31st Jan 2015, the scheme has ~80% exposure to corporate debt and the ~20% in

Money Market Instruments, CBLO, SLR, cash & cash equivalent. The credit profile of the scheme reflects that ~23% of the portfolio is

invested in AAA rated and equivalent papers including cash & cash equivalent and ~77% invested in AA and below rated papers. The

YTM & Modified Duration of the scheme is 10.46 and 1.52 years respectively.

Details of Few Securities in the Portfolio:

Issuer Rating

BWR AA+ (SO)

Description

Mandva Holdings Pvt. Ltd Mandva Holdings is the main holding company of NSL group of Hyderabad. The investment is secured by unlisted shares of Nuziveedu Seeds Ltd., subsidiary of Mandava Holdings and one of the largest seeds company in India, as well as a conditional put option on Axis Capital.

ICRA AIL&FS Transpor tat ion Networks Ltd

ITNL is promoted by IL&FS group. The company is one of the largest developers of road projects in the country, with a diversified portfolio of around 12000 lane km, both operational and under development.

ICRA ADLF Ltd It is the largest listed real estate company in India. NCD investments are secured by mortgage of prime land in New Delhi.

ICRA AA+(SO)Floreat Investments Ltd 100% subsidiary of Shapoorji Pallonji & Company Ltd engaged in redevelopment projects. The NCD is backed by the unconditional and irrevocable corporate guarantee of Shapoorji Pallonji & Company Ltd.

BWR A(SO)TRIL Infopark Ltd (TATA Realty SPV)

IT SEZ project situated in Chennai, promoted by Tata Realty & Infrastructure

CARE A1(SO)RHC Holding Private Ltd Loan against shares transaction with promoters Religare group, secured against collateral of shares of shares of Fortis Healthcare and Religare Enterprises Ltd.

BWR A-(SO)RKN Retail Private Ltd RKN Retail is a part of the Aditya Birla Group, owned 100% by the promoters. It is one of the primary holding companies for Aditya Birla Retail, and carries out trading activities as well. We have non disposal undertaking from the issuer for shares of Aditya Birla Retail.

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

CRISIL AAA (SO)

IOT Utkal is a Special purpose Vehicle (SPV)

Promoted by IOTL (IOT Infrastructure & Energy Services Ltd., which is a JV between Indian Oil Corporation & Oil Tanking, Gmbh, Germany) to provide storage and handling requirements of crude oil & finished products for the 15 MMTPA refinery being set up by Indian Oil Corporation at Paradip, Odisha. Source: Crisil and Fitch

ICRA A+(SO)Hero Realty Ltd (HRL) Hero Realty Limited (HRL) was incorporated in 2006 as Arrow Infrastructure Pvt. Limited; 99.99 % stake in the company is held by Hero Corporate Service Limited. HRL is engaged in the business of real estate development. HRL is involved in developing residential, commercial and industrial projects and provide suitable infrastructure for the smooth functioning of Hero group manufacturing companies. Presently, HRL is developing two residential projects and three industrial parks over a land bank of nearly 400 acres in Haridwar, Uttarakhand. (Source: ICRA)

Investment Objective

The primary investment objective of the Scheme is to generate regular income through investments in debt & money market instruments in order to make regular dividend payments to unit holders & secondary objective is growth of capital.

All data provided are as on January 30, 2015 unless otherwise provided

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Fund Details

Fund Manager : Mr. Maneesh Dangi

Managing Fund Since : September 01, 2014

Total Experience : 14 years

Date of inception : March 25, 2009

Nature of the scheme : An Open-ended Income Scheme

Regular Plan^Growth : 16.7832Quarterly Dividend : 10.4953Half Yearly Dividend : 11.1814Dividend : 12.4410

Direct Plan*Growth : 16.9978Quarterly Dividend : 10.5912Half Yearly Dividend : 11.5051Dividend : 12.5965

Institutional Plan$Growth : 16.2938Quarterly Dividend : -Half Yearly Dividend : -

Benchmark : CRISIL AA Short Term Bond Fund(w.e.f 27th May 2013) Index

Entry Load : Nil

Exit Load** : For redemption/switch-out of unitswithin 365 days from the date ofallotment: 2.00% of applicableNAV.

For redemption/switch-out of unitsafter 365 days but before 730 days from the date of allotment: 1.00% ofapplicable NAV.

For redemption/switch-out of unitsafter 730 days from the date ofallotment: Nil

**Exit Load is NIL for units issued in Bonus & Dividend Reinvestment.

Modified Duration : 1.52 Years

Yield to Maturity : 10.46%

Standard Deviation : 2.08%

Plans / Options & NAV (As on January 30, 2015)

Load Structure

Other Parameter

Note:Standard Deviation is calculated on annualised basis using 1 year history of monthly returns, source: MFI Explorer.

Disclaimer: This document is strictly confidential and meant for private circulation only and should not at any point of time be construed to be an invitation to the public for subscribing to the units of

Birla Sun Life Mutual Fund. Please note that this is not an advertisement. The document is solely for the information and understanding of intended recipients only. If you are not the intended recipient,

you are hereby notified that any use, distribution, reproduction or any action taken or omitted to be taken in reliance upon the same is prohibited and may be unlawful. Views expressed herein should

not be construed as investment advice to any party and are not necessarily those of Birla Sun Life Asset Management Company Ltd.(BSLAMC) or any of their officers, employees, personnel,

directors and BSLAMC and its officers, employees, personnel, directors do not accept responsibility for the editorial content. Wherever possible, all the figures and data given are dated, and the same

may or may not be relevant at a future date. Further the opinions expressed and facts referred to in this document are subject to change without notice and BSLAMC is under no obligation to update

the same. While utmost care has been exercised, BSLAMC or any of its officers, employees, personnel, directors make no representation or warranty, express or implied, as to the accuracy,

completeness or reliability of the content and hereby disclaim any liability with regard to the same. Recipients of this material should exercise due care and read the scheme information document

(including if necessary, obtaining the advice of tax/legal/accounting/financial/other professional(s) prior to taking of any decision, acting or omitting to act. Further, the recipient shall not

copy/circulate/reproduce/quote contents of this document, in part or in whole, or in any other manner whatsoever without prior and explicit approval of BSLAMC.

Mutual Fund: Birla Sun Life Mutual Fund

Asset Management Company/ Investment Manager: Birla Sun Life Asset Management Company Limited. CIN: U65991MH1994PLC080811

Registered Office: One India Bulls Centre, Tower - 1, 17th Floor Jupiter Mill Compound, 841, S. B. Marg, Elphinstone Road, Mumbai - 400013.

Private & confidential. For internal circulation only

Issuer % to Net RatingAssets

Issuer % to Net RatingAssets

Corporate Debt 80.56RHC Holding Pvt Ltd ** 11.05 CARE A(SO)RKN RETAIL PVT. LTD ** 9.83 BWR A-(SO)IL & FS Education and Technology 9.69 IND AA-(SO)Services Ltd **DLF Ltd ** 9.32 ICRA ARelationships Properties Pvt Ltd ** 6.22 CARE AA-(SO)Sterlite Technologies Ltd ** 4.17 CRISIL A+S.D. Corporation Pvt. Ltd ** 3.49 ICRA AA+(SO)Coffee Day Natural Resources 3.27 BWR A-(SO)Private Limited **TRIL Infopark Ltd (TATA Realty SPV) ** 2.99 BWR A(SO)IL&FS Transportation Networks Ltd ** 2.85 ICRA AReliance Jio Infocomm Limited 2.72 CRISIL AAAReliance Ports and Terminals Ltd ** 2.66 CRISIL AAAHero Realty Ltd ** 2.07 ICRA A+(SO)Securities Trading Corp Ind Ltd ** 2.02 ICRA AAReliance Jio Infocomm Limited ** 1.95 CRISIL AAATata Housing Development Co Ltd ** 1.91 ICRA AASahyadri Agencies Ltd ** 1.53 BWR A(SO)Hero Fincorp Limited ** 0.86 CRISIL AA+Floreat Investments Ltd ** 0.82 ICRA AA+(SO)Cholamandalam Investment and 0.69 ICRA AAFinance Company Ltd **Sesa Sterlite Ltd ** 0.27 CRISIL AA+RHC Holding Pvt Ltd ** 0.16 IND A

Portfolio & Asset Allocation

Kotak Mahindra Prime Ltd ** 0.02 CRISIL AAA

Money Market Instruments 13.74Housing Development Finance 7.54 ICRA A1+Corporation LtdOriental Bank of Commerce 4.86 CRISIL A1+ICICI Securities Ltd 1.35 CRISIL A1+

Mutual Fund Units 3.80Birla Sun Life Floating Rate - 3.80 ShtTer- Gr-Dir Plan

SWAP -0.077.13% Rec Mibor & Pay Fix 0.00 (MD16/01/17) HSBCBK7.13% Rec Mibor & Pay Fix 0.00 (MD16/01/17) ICICISEC7.50% Rec Mibor & Pay Fix -0.03(MD23/12/2016) HSBCBK7.49% Rec Mibor & Pay Fix -0.04 (MD23/12/2016) HDFCBK

Cash & Current Assets 1.96

Total Net Assets 100.00

Rating Profile

^This Plan under the scheme continues for fresh subscription and has been renamed w.e.f October 01, 2012 vide addendum no.33/2012 dated September 28, 2012 and is referred to as “Regular Plan” vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.

*Separate Option for direct investments under SEBI Circular no. CIR/IMD/DF/21/2012 dated September 13, 2012 with effect from January 1, 2013 vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.

$This Plan under the scheme is discontinued for fresh subscription w.e.f October 01, 2012 vide addendum no.33/2012 dated September 28, 2012. For further details, please refer our website www.birlasunlife.com.

Note: Risk is represented as:

(BLUE) investors understand that their principal will be at low risk

(YELLOW) investors understand that their principal will be at medium risk

(BROWN) investors understand that their principal will be at high risk

This product is suitable for investors who are seeking*:• income with capital growth over medium to long term• investments in debt and money market instruments• medium risk (YELLOW)*Investors should consult their financial advisers if in doubt whether the product is suitable for them.

Product Labeling

** Represents thinly traded/ non traded securities and illiquid securities.

1.96%

3.73%

10.08%

21.08%

63.15%

Cash & Current Assets

Unrated

AA

AAA

Below AA

Savings

Solutions Birla Sun Life Short Term Fund(An Open-ended Income Scheme)

(Erstwhile Birla Sun Life Income Fund. Name changed w.e.f February 01, 2012)

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Know Your Fund

• An actively managed open ended short term income scheme that endeavors to generate superior levels of yields at relatively lower level of risk with low volatility

• The scheme, as per provisions of SID, has the flexibility to invest in diversified portfolio of securities issued by corporate or state/central government and money market instruments with short to medium term maturity.

• However, to contain volatility in the portfolio, it seeks to follow a discipline of restricting its exposure in government securities.

• Intends to maintain good quality portfolio by investing in highly rated debt securities (AAA/AA+) with more emphasis on AAA corporate bonds.

• It may be considered by investors with investment horizon of 6 months and above.

Private & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

Outlook

The month gone by was by far the most action packed month in the recent past. As if base changes of the key macroeconomic variables weren’t enough to keep markets busy and buzzing, the economic survey, the railway budget, the scheduled as well as a surprise RBI policy meet brought interesting twists to almost every day of the shortest month in the calendar.

Growth

With the rebasing of GDP growth to 2012=100, previous years (FY13 and FY14) growth rates were revised upwards markedly. In light of this, the advance estimates for FY15 were being keenly watched by markets. Central Statistic Organisation has estimated growth in FY15 to rise to 7.4%, up 50bps from FY14’s rate of growth. While the increase is broadly in line with expectations, the levels have been restated as GDP growth now also measures value addition. Accordingly, we expect FY16 GDP to grow further to ~8.4%. A major driver of this is the reflationary impact of oil price decline. As far as the high frequency indicators are concerned, correcting for data capturing and sudden revision related issues, general economic activity seems to be picking up so far. (source: MOSPI, BSLAMC internal research)

Inflation

CPI inflation also saw a base change (2012=100). The key take away from this exercise was the move away from arithmetic mean to geometric mean, with the objective of reducing volatility caused by some items. This is expected to pull a statistical downward pressure on CPI. Resultantly, headline CPI inflation came in at 5.1% in January’15, rising from 4.3% in Dec’14 (new base). Core CPI also declined to 3.9%, most of this being a reflection of decline in the price of crude. WPI inflation turned negative again to -0.4% for the month of Jan. Apart from fuel disinflation, the core WPI inflation has also been on a softening trend, courtesy the commodity bear cycle underway. Continuous moderation in both retail and wholesale inflation, created conditions conducive for monetary easing. (source: MoSPI)

External Equation

Owing to falling oil prices, trade Deficit for Jan moderated by ~1bn$ to 8.3bn$. Keeping aside the price effect, the volume of oil imports seems to be growing. The same hold true for exports, where net of oil exports, the story doesn’t look as gloomy. We expect CAD in Q3 to rise to ~12-13bn$ and FY15 to range between ~25-27bn$. This is expected to improve further in FY16. (Source: Ministry of Commerce, BSLAMC internal Research)

March 2015

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Private & confidential. For internal circulation only

Fiscal front

Even after exhausting more than the budgeted fiscal deficit by the month of Jan, the finance minister in the revised estimates for FY15 assured that 4.1% of GDP would be acheievd as the fiscal deifict number. For FY16, in a welcome deviation from the FRBM roadmap laid out by the Kelkar committee, the finance minister decided to defer it by a year and announced a fiscal deficit of 3.9% of GDP for FY16 (as against 3.6% suggested by the Kelkar committee). A large part of this etra stimulus in both a direct and an indirect (via the leverage route) is expected to go for capital spending. This in turn is expcted to have a multiplier effect on growth. As supply side improves, this is expected to exert some disinflation in the medium term. The FY16 Union Budget chose growth over consolidation in the backdrop of improved macroeconomic environment, expressed realistic growth targets and pragmatism basis the current stage of the economic cycle that we are in. RBI acknowledged these efforts and in another out of policy move, cut rates by 25bps on Mar 4th, taking repo to 7.5%. (Source: RBI, Ministry of Finance)

One more key reason behind this move in our view is the legislation on monetary policy framework which binds RBI to the mandate of maintaining price stability. While the operating procedure needs some more clarity, RBI as per this monetary policy framework would have to ensure CPI inflation of 4% by FY18 (starting Fy17). (Source: Ministry of Finance, RBI)

All this is likely to have the following impact on portfolio positioning-

Duration Funds shall be impacted positively by the budget and the rate cut. Formalization of monetary policy framework, focus on infrastructure creation, and credible budget math marginally outweigh negatives such as rise in service taxes, and fiscal stimulus from the Government.

Credit funds shall be benefitted because of focus of the government to bring back growth. A decent growth in the economy shall benefit the borrowers to improve their creditworthiness and command tighter spreads over the base curve.

No impact on Liquidity funds.

Portfolio Action and Strategy

The portfolio is invested in securities spanning across the maturity profile ranging from <1/1-3/3-5 years. A major part of the portfolio (~60%) is invested in high quality corporate bonds along with ~30% exposure to Government securities, state government securities & Treasury Bills and ~12% in money market instruments & CBLO, cash & cash equivalent. The modified duration of the scheme stands at 1.68 years. In order to maintain a high credit quality, more than ~85% of the portfolio is invested in AAA rated and equivalent papers. The YTM as on 27th Feb 2015 is 8.41%.

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

Investment Objective

An open-ended income scheme with the objective to generate income and capital appreciation by investing 100% of the corpus in a diversified portfolio of debt and money market securities.

All data provided are as on February 27, 2015 unless otherwise provided

Portfolio & Asset Allocation

Issuer % to Net RatingAssets

Issuer % to Net RatingAssets

Corporate Debt 58.35Power Finance Corporation Ltd ** 9.18 CRISIL AAAHousing Development Finance Corporation Ltd **LIC Housing Finance Ltd ** 5.82 CRISIL AAARural Electrification Corporation Ltd ** 4.39 CRISIL AAANABHA POWER LTD ** 3.85 ICRA AAA(SO)IDFC Ltd. ** 3.34 ICRA AAAL&T Finance Ltd ** 3.15 ICRA AA+Rural Electrification Corporation Ltd 1.72 CRISIL AAASundaram Finance Ltd ** 1.51 ICRA AA+IL&FS Financial Services Ltd ** 1.45 IND AAAKotak Mahindra Prime Ltd ** 1.43 CRISIL AAAAditya Birla Nuvo Ltd ** 1.43 ICRA AA+Tata Capital Financial Services Ltd ** 1.22 ICRA AA+PNB Housing Finance Ltd ** 1.19 CRISIL AA+Tata Capital Financial Services Ltd ** 1.18 CRISIL AA+Bajaj Finance Ltd ** 1.02 ICRA AA+Talwandi Sabo Power Ltd ** 0.95 CRISIL AA+ (SO)Sesa Sterlite Ltd ** 0.79 CRISIL AA+Reliance Jio Infocomm Limited ** 0.79 CRISIL AAALIC Housing Finance Ltd ** 0.56 CARE AAATata Sons Ltd ** 0.56 CRISIL AAAICICI Home Finance Company Ltd ** 0.56 ICRA AAAExport Import Bank of India ** 0.41 CRISIL AAAPower Grid Corporation of India Ltd ** 0.40 CRISIL AAACholamandalam Investment and Finance Company Ltd **National Bank For Agriculture and Rural DevelopmentTata Capital Housing Finance Ltd ** 0.39 CRISIL AA+Power Finance Corporation Ltd 0.32 CRISIL AAATata Motors Finance Ltd ** 0.27 CRISIL AAIDFC Ltd. 0.24 ICRA AAAAirport Authority of India Ltd ** 0.16 CRISIL AAAKotak Mahindra Prime Ltd ** 0.08 ICRA AAAHDB Financial Services Ltd ** 0.03 CRISIL AAANational Bank For Agriculture and Rural Development **Government Bond 12.987.80% GOI (MD 03/05/2020). 4.88 Sovereign

9.16 CRISIL AAA

0.40 ICRA AA

0.39 CRISIL AAA

0.00 CRISIL AAA

7.28% GOI (MD 03/06/2019) 3.48 Sovereign8.12% GOI (MD 10/12/2020) 3.43 Sovereign6.49% GOI (MD 08/06/2015) 0.78 Sovereign7.46% GOI 2017 (M/D. 28/8/2017) 0.39 SovereignTreasury Bills 9.69364 Days Tbill (MD 19/03/2015) 2.75 Sovereign91 Days Tbill (MD 22/05/2015) 1.93 Sovereign91Days Tbill (MD 05/03/2015) 1.57 Sovereign182Days Tbill (MD 18/06/2015) 1.54 Sovereign91Days Tbill (MD 12/03/2015) 1.15 Sovereign364 Days Tbill (MD 05/03/2015) 0.71 Sovereign364 Days Tbill (MD 03/09/2015) 0.05 SovereignState Government Bond 7.098.58% Karnataka SDL (MD 25/10/2016) 5.85 Sovereign8.75% Gujarat SDL(MD 03/10/2016) 0.57 Sovereign9.60% Gujarat SDL(MD 12/03/2018) 0.41 Sovereign8.67% Karnataka SDL (MD 18/07/2017) 0.18 Sovereign8.43% Madhya Pradesh SDL (MD 19/12/2017) 0.08 SovereignMoney Market Instruments 6.54Bank of India 3.17 CRISIL A1+Rural Electrification Corporation Ltd 1.57 CARE A1+Housing Development Finance Corporation LtdBank of Baroda 0.39 ICRA A1+Indian Bank 0.39 IND A1+Canara Bank 0.16 CRISIL A1+Oriental Bank of Commerce 0.07 CRISIL A1+Axis Bank Ltd 0.06 CRISIL A1+SWAP -0.017.33% Rec Mibor & Pay Fix (MD08/01/17) HSBCBK7.46% Rec Mibor & Pay Fix (MD29/12/2016) HDFCBK 7.48% Rec Mibor & Pay Fix (MD29/12/2016) HSBCBKCash & Current Assets 5.36

0.73 ICRA A1+

0.00

0.00

0.00

Total Net Assets 100.00

Rating Profile

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Disclaimer: This document is strictly confidential and meant for private circulation only and should not at any point of time be construed to be an invitation to the public for subscribing to the units of

Birla Sun Life Mutual Fund. Please note that this is not an advertisement. The document is solely for the information and understanding of intended recipients only. If you are not the intended recipient,

you are hereby notified that any use, distribution, reproduction or any action taken or omitted to be taken in reliance upon the same is prohibited and may be unlawful. Views expressed herein should

not be construed as investment advice to any party and are not necessarily those of Birla Sun Life Asset Management Company Ltd.(BSLAMC) or any of their officers, employees, personnel,

directors and BSLAMC and its officers, employees, personnel, directors do not accept responsibility for the editorial content. Wherever possible, all the figures and data given are dated, and the same

may or may not be relevant at a future date. Further the opinions expressed and facts referred to in this document are subject to change without notice and BSLAMC is under no obligation to update

the same. While utmost care has been exercised, BSLAMC or any of its officers, employees, personnel, directors make no representation or warranty, express or implied, as to the accuracy,

completeness or reliability of the content and hereby disclaim any liability with regard to the same. Recipients of this material should exercise due care and read the scheme information document

(including if necessary, obtaining the advice of tax/legal/accounting/financial/other professional(s) prior to taking of any decision, acting or omitting to act. Further, the recipient shall not

copy/circulate/reproduce/quote contents of this document, in part or in whole, or in any other manner whatsoever without prior and explicit approval of BSLAMC.

Mutual Fund: Birla Sun Life Mutual Fund

Asset Management Company/ Investment Manager: Birla Sun Life Asset Management Company Limited. CIN: U65991MH1994PLC080811

Registered Office: One India Bulls Centre, Tower - 1, 17th Floor Jupiter Mill Compound, 841, S. B. Marg, Elphinstone Road, Mumbai - 400013.

Private & confidential. For internal circulation only

Fund Details

Fund Manager : Mr. Prasad Dhonde

Managing Fund Since : July 01, 2011

Total Experience : 16 years

Date of inception : March 3, 1997

Nature of the scheme : An Open-ended Income Scheme

Default option : Dividend Reinvestment

Fresh Purchase : ` 5000/-

Additional Purchase : ` 1000/-

Redemption Cheques : Within 10 working days issued

Systematic Investment : Available Plan (SIP)

Systematic Withdrawal : Available Plan (SWP)

Systematic Transfer : AvailablePlan (STP)

Regular Plan^Growth : 51.8887Monthly Dividend : 11.8083Dividend : 10.3412

Direct Plan*Growth : 52.0068Monthly Dividend : 11.8139Dividend :

Benchmark : CRISIL Short Term Bond Fund(w.e.f 27th May 2013) Index

Entry Load : Nil

Exit load** : For Redemption / Switchout of units (w.e.f November 26, 2014) within 30 days from the date of

allotment: 0.25% of applicable NAV.

For Redemption / Switchout of units after 30 days from the date of allotment: Nil**Exit Load is NIL for units issued in Bonus & Dividend Reinvestment.

Modified Duration : 1.68 Years

Yield to Maturity : 8.41%

Standard Deviation : 1.59%

Key Features

Plans / Options & NAV (As on February 27, 2015)

Load Structure (Incl. for SIP)

Other Parameter

10.3084

Note:Standard Deviation is calculated on annualised basis using 1 year history of monthly returns, source: MFI Explorer.^This Plan under the scheme continues for fresh subscription and has been renamed w.e.f October 01, 2012 vide addendum no.33/2012 dated September 28, 2012 and is referred to as “Regular Plan” vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.*Separate Option for direct investments under SEBI Circular no. CIR/IMD/DF/21/2012 dated September 13, 2012 with effect from January 1, 2013 vide Notice-cum-Addendum no.44/2012 dated December 27, 2012. For further details, please refer our website www.birlasunlife.com.

Note: Risk is represented as:

(BLUE) investors understand that their principal will be at low risk

(YELLOW) investors understand that their principal will be at medium risk

(BROWN) investors understand that their principal will be at high risk

This product is suitable for investors who are seeking*:

• income with capital growth over short term

• investments in debt and money market instruments.

• low risk (BLUE)

*Investors should consult their financial advisers if in doubt whether the product is suitable for them.

Product Labeling

** Represents thinly traded/ non traded securities and illiquid securities.

-1.58%

6.94%

13.50%

29.76%

51.39%

Unrated

Cash & Current Assets

AA

Sovereign

AAA

Birla Sun Life Short Term Opportunities Fund(An Open ended Income Scheme)

Savings

Solutions

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Know Your Fund

• Scheme is positioned where the majority of the portfolio is intended to be invested in high quality AA and above rated papers.

• Within the provisions and limitations of the SID, the scheme intends to run the portfolio on an accrual which would involves buying a

bond and holding it till maturity thereby earning from the accruing of interest. This would enable to minimize the interest rate risk to a

large extent.

• The scheme intends to have a stable and disciplined duration profile in the portfolio in order to minimize the return volatility.

• It may be considered by investors with investment horizon of approx 1 year and above.

The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for

asset allocation, investment strategy and scheme specific risk factors.

Outlook

The month gone by had a flurry of data releases over and above the regular ones. For one, there was an out of policy surprise rate cut by RBI

sighting reasons of more than anticipated decline in inflation and inflationary expectations moderating to single digits for the first time in 21 quarters (Source: RBI). Then came the rebasing of GDP numbers which completely changed the manner in which Indian economy was being looked at. After these, the RBI policy was being keenly watched for, especially for the commentary.

The base year revision for national account statistics was long pending. With the shift of base year to 2011-12 from 2004-05 and some

changes in methodology, the GDP growth rate for FY13 and FY14 from 4.7% and 5% to 5.1% and 6.9% respectively (at market prices)

(Source: MOSPI). The change is owing to expansion of data set and falling deflator. This suggests that the slowdown in India’s growth was probably overstated. We are now awaiting the advance estimates for FY15 to get more colour on how to estimate growth in India going forward. As for all the high frequency indicators, some revival is in sight. The composite PMI index has gone up to 53.3 from 52.5 in Jan from

Dec (Source: HSBC Markit), MHCV sales are registering strong YoY growth rates and so is demand for petrol and diesel, tourist arrivals have been gaining strength and similar trend is visible in air traffic. Most importantly, with oil prices plummeting, personal disposable incomes would get a push and this should facilitate more consumption. While more clarity is awaited on base and methodology change, keeping that

aside, we are looking at growth reviving from ~5.5% in FY15 to ~6.5% in FY16.

On the inflation side, as December numbers came lower than expectations, RBI, as pre-committed announced a 25bps rate cut on Jan 15th

2015. As favourable base effects waned off in December, CPI rose marginally to 5%, more importantly the underlying momentum declined for the first time since February 14. Also, core CPI moderated further to 5.2% in December. WPI inflation also rose marginally to 0.1%,

despite a decline in MoM terms, the YoY picked up due to base turning unfavourable (Source: MOSPI). Going forward, both the headline prints

could remain marginally higher, but that has largely got to do with the base as the momentum is that of moderation only.

Developments on the external front were largely as anticipated. With December trade deficit correcting sharply to 9.4bn$ on account of declining gold and oil imports, we are on track to see CAD for FY15 moderating to ~20bn$ form 32.4bn$ in FY14. (Source: Bloomberg). The decline in oil prices are expected to play a major role in this saving and take CAD to even lower levels in FY16 (Assuming oil price remains

around current levels).

Private & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

February 2015

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Private & confidential. For internal circulation onlyPrivate & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

We ended up exhausting ~100% of our budgeted target of fiscal deficit by December. While this would have raised some eyebrows, but in a

record event of raising ~ Rs 22,000 crores from its disinvestment in Coal India Limited (source: PIB), the government seems to be on track to

achieve its target fiscal deficit of 4.1% of GDP for FY15 (source: Ministry of Finance). Needless to say, expenditure compression would be inevitable in this exercise. The union budget for FY16 will the next big thing to watch. The policy corridors seem to be divided between

stepping up of public investment to aid growth and adhering to fiscal consolidation road map that the current govt. had intended to tread on.

From here on, quarterly GDP data as per the new method, combined CPI data based on new consumption patterns, Union Budget and

especially the quality of fiscal deficit shall be crucial data points for market directions. Till then we believe, the market shall be range bound.

RBI Governor kept his word and acted no sooner he felt it was a right prescription for the economy, to lower the benchmark rate. Accordingly he surprised the markets with an intermittent cut in mid January 2015. Bond yields (yield on 10 year benchmark security) fell more than 10 bps post rate cut to ~7.70% thus taking cumulative rally to about 100 bps on the benchmark over the last one year. This cut led the market

to believe that the RBI will follow the action with another cut on 3rd February 2015, but as expected by us, it did not materialize, and for the right reasons.

From rates perspective, we believe that the Repo is likely to go to 7.25% in 2015, but what is crucial is the pace of rate cuts. We believe, the cuts are more likely in H12015 which shall be rates positive, but what can keep lid on the prospective rally are large open market operations

(OMO) sales that are likely in FY16 and a debate on terminal policy rate in this cycle.

From portfolio perspective, we have moderated duration across our key portfolios. We have also swapped some less liquid securities for

highly liquid securities in order to stay agile in the times to come.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Private & confidential. For internal circulation onlyPrivate & confidential. For internal circulation only

The above parameters are indicative and can change from time to time at the discretion of the fund manager.Internal views, estimates, opinions of Birla Sun Life Asset Management Company Ltd. (BSLAMC) expressed herein may or may not materialize. These views, estimates, opinions alone are not sufficient and should not be used for the development or implementation of an investment strategy. The portfolio of the scheme is subject to changes within the provisions of the Scheme Information Document (SID) of the scheme. Please refer to the SID for asset allocation, investment strategy and scheme specific risk factors. Forward looking statements are based on internal views and assumptions and subject to known and unknown risks and uncertainties which could materially impact or differ the actual results or performance from those expressed or implied under those statements.

CARE AA+ (SO)

G S P C D i s t r i b u t i o n Networks Ltd. (GDNL)