biotechnology - ibef · product development •india possesses the second-largest english-speaking...

TRANSCRIPT

BIOTECHNOLOGYNovember 2010

Manan

2

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

3

Advantage India

• India offers a significant cost advantage

over the US and is recognised globally

for its low-cost fermentation technology

and generic biologics.

• Manufacturing costs in India are

approximately 35 to 40 per cent of those

in the US, supported by low installation,

manpower and manufacturing costs.

• India is one of the preferred destinations in

custom research outsourcing (CRO) and

custom manufacturing outsourcing(CMO).

• The clinical trials market has witnessed 31

per cent growth during 2004-2008.

• CMO has recorded around 43 per cent

growth, at thrice the global market rate.

ADVANTAGE INDIA

Outsourcing

capabilities

Advantage

IndiaLow

manufacturing

cost

Vast skilled talent

pool

Innovative

product

development

• India possesses the second-largest English-speaking population in the world.

• In 2009, 15,000 scientists were engaged in the biotechnology sector.

• As of 2009, every year, 3 million graduates, 0.7 million postgraduates and 1,500 PhDs are added to India’s talent pool.

• It is equally supported by education infrastructure of more than 200 research institutes.

Source: Taking wings, Ernst & Young, 2009; ICE publication, ice website,

www.ice.gov.it/paesi/asia/india/upload/182/Sector%20Report%20Biotechnology%20-%202009.pdf , accessed 12 November 2010

Strong quality

and technical

capabilities

In 2009, India had more than

120 US Food and Drug

Administration (FDA)-

approved plants and around 84

UK Medicines and Healthcare

products Regulatory Agency

(MHRA)-approved plants, with

capabilities to manufacture

products of exceptional quality.

• The industry is constantly

engaged in upgrading

technology to enhance the

quality of products.

• India is expected to be one of

the top five innovative hubs

with contributions of around 50

per cent of drugs discovered

worldwide from India.

Biotechnology November 2010

4

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

5

Market overview

• In 2009–2010, the industry recorded revenues worth US$ 3 billion, registering y-o-y growth of 12.36 per cent (in US$ terms) over 2008–09.

• The industry is expected to witness robust growth and reach US$ 15 billion by 2015, driven by various government initiatives.

Sources: ABLE-Biospectrum industry survey, June 2010; Ernst &

Young analysis

MARKET OVERVIEW

US$

bill

ion

1.04

1.43

1.88

2.282.67

3.00

0

0.5

1

1.5

2

2.5

3

3.5

2004–2005 2005–2006 2006–2007 2007–2008 2008–2009 2009–2010

Indian biotechnology market size

Biotechnology November 2010

6

Bio-pharma Bio-services Bio-industrial Bio-informatics

Biotechnology

In 2009–2010, bio-services was the second-largest contributor to the industry, constituting 18.7 per cent of total revenues. This segment contributed 33 per cent of exports.

This segment

accounts for

majority of the

biotech industry’s

revenues. It

contributed 62 per

cent to total

revenues in 2009–

2010.

The bio-industrial

segment

contributed

approximately 4

per cent to total

revenues in

2009–2010.

The bio-

informatics

industry is at a

nascent stage,

contributing 1-2

per cent of total

revenues in

2009–2010.

Bio-agri

This segment

generated around

US$ 410 million

revenues in 2009–

2010, accounting

for 13.7 per cent

of total revenues.

Market segments

Sources: ABLE-Biospectrum industry survey, June 2010; Ernst & Young analysis

MARKET OVERVIEW

Biotechnology November 2010

7

Exports

• Revenues from biotech exports have been valued at US$1.57 billion in 2009–2010, constituting 52 per cent of the biotech industry’s revenues.

Sources: ABLE-Biospectrum industry survey, June 2010; Ernst & Young analysis

1 per cent1 per cent

2 per cent

0

0.2

0.4

0.6

0.8

1

1.2

Exports

Bio-pharma Bio-services Bio-agri

Bio-industrial Bioinformatics

US$

bill

ion

1.10

1.57

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Exports of biotechnology products Share of exports per segment

MARKET OVERVIEW

2007–08 2009–2010

63 per cent

33 per cent

Biotechnology November 2010

8

Domestic demand

Specialised

treatment

Preventive

healthcare

• The disease profile that inflicts the Indian population has experienced a gradual shift. The number of lifestyle-related diseases being reported is rising, which has led to the demand for various kinds of specialised treatment. Ailments such as cancer and diabetes have heightened the demand for biologic products.

• Around 1.15 billion new cases of ailments are reported annually. The reported number of ailments is expected to rise by a compound annual growth rate (CAGR) of 30 per cent to reach 15 billion cases by 2015. A growing population, increasing affordability, easier access to healthcare facilities and a shift toward lifestyle diseases are driving this trend. Demographic changes have led to an increase in the demand for vaccines, both for geriatrics and pediatrics population.

Source: Ernst & Young research

MARKET OVERVIEW

Biotechnology November 2010

9

Growth drivers — increased healthcare expenditure and

funding for the biotechnology sector

• Healthcare expenditure, as a percentage of GDP, was recorded at 1.09 per cent for 2009–2010, with the growth being driven primarily by the rise in private expenditure.

• During 2007–2010, the percentage utilisationof allocated resources by the Department of Biotechnology (DBT) is 94.49 per cent as compared to science and technology sector average of 90.56 per cent.

Source: , "Mid term appraisal," Eleventh Five Year Plan,

National Biotechnology development strategy, dbtindia

website,

http://dbtindia.nic.in/biotechstrategy/National%20Biotechnolog

y%20Development%20Strategy.pdf , accessed 15 November

2010

Trend in funds availability for the biotechnology sector

Funds availability (US$ in million)

MARKET OVERVIEW

129.4

302.1

1354.2

0

200

400

600

800

1000

1200

1400

1600

Ninth Five year plan

Tenth five year plan

Eleventh five year plan

Biotechnology November 2010

10

Growth drivers — government support

Source: ―Biotechnology facilities,‖ dbtindia website, http://dbtindia.nic.in/uniquepage.asp?id_pk=41 , accessed 15 November 2010, Eleventh Five

Year Plan- mid term appraisal

MARKET OVERVIEW

New facilities

• The Department of Biotechnology (DBT) set up 35 facilities between 2002 and 2007 to produce and supply biologicals, reagents,

culture collections and laboratory animals to scientists, industries and students at nominal costs. To fill the viability gap in

developing new technologies, the Government of India (GoI) started a biotechnology industry partnership programme for

funding support.

Regulatory

• According to the National Biotechnology Development Strategy (NBDS), there is a positive inclination to set up a centralised

national biotechnology regulatory authority to provide a single-window clearance mechanism for all bio-safety clearances for

products.

International collaborations

• Various international collaborations with different countries are in the pipeline, directed at enabling the effective transition of

knowledge. A re-entry fellowship grant has been initiated with the UK-based Wellcome Trust. India has also partnered with

countries such as the UK, Russia, Italy, the US and France to enable knowledge transition.

Biotechnology November 2010

11

Growth drivers — rising incidence of chronic diseases

• Lifestyle diseases are set to assume a greater share of the healthcare market.

• Lifestyle diseases such as cardiac diseases, cancer and diabetes require biotechnology products for treatment, thereby increasing the revenues of biotech companies.

Source: Fortis Healthcare Limited 2008–09 annual report.

Perc

enta

ge s

har

e

22 14

1917

1615

1418

13 193 4

232

323

7 4

0

20

40

60

80

100

120

2001 2012

Acute infections Accidents Maternity / gynaec Heart disease Cancer

Genito-urinary Other circulatory Musculoskeletal Digestive Others

Changing disease profile

MARKET OVERVIEW

F

Biotechnology November 2010

12

Key trends — pharma companies are focusing on biotech

• Ranbaxy, Cadila Healthcare, Lupin, Wockhardtand Dr Reddy’s are among the major Indian pharmaceutical companies that have entered the bio-pharma segment.

Source: Ernst & Young research

MARKET OVERVIEW

Global companies setting up base

• Lonza is planning to set up a manufacturing base in India at an investment of US$ 150 million in Hyderabad. The investment outlay has been planned over two phases:

• Phase I (from 2011 to 2013) will include the development of R&D labs for more than 100 resources.

• Phase II (from 2014 to 2015) will include the expansion of manufacturing capabilities and the provision for increasing R&D lab capacity for biologics with 200 additional resources.

Biotechnology November 2010

13

Key players

• The leading 20 companies (in terms of revenues) accounted for 52 per cent of industry revenues in 2009–2010.

• Biocon and Serum Institute of India are the two leading players in the industry.

• MNCs such as Novo Nordisk and Novozymesfeature among the leading 15 biotech companies.

• Of the top 10 companies, 5 generated revenues close to or greater than US$ 100 million in 2009–2010.

Leading 10 companies (2009–2010)

Company

Revenue

(US$ million)

2009–2010

Per cent change

since 2008–09

Biocon 245.83 29.34

Serum Institute of

India177.08 -23.70

Panacea Biotec 146.49 17.76

Nuziveedu Seeds 99.34 6.07

Reliance Life

sciences93.75 —

Quintiles 78.12 —

Rasi seeds 74.74 -4.48

NovoNordisk 71.25 3.64

Shantha Biotech 69.58 35.32

Mahyco 65.00 47.78

Sources: ABLE-Biospectrum industry survey, June 2010; Ernst &

Young analysis

MARKET OVERVIEW

Biotechnology November 2010

14

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

15

Industry infrastructure … (1/2)

Operational biotech parks

• The Eleventh Five Year Plan aims to establish biotechnology parks to involve small and medium enterprises in product development and translational research.

• Biotechnology infrastructure is witnessing a shift from traditional clusters to specialised industrial infrastructure such as biotech or science parks.

• States such as Andhra Pradesh, Maharashtra, Tamil Nadu and Kerala have been early movers in establishing world-class biotech parks and clusters.

• Investors such as TCG and Alexandria have significantly contributed in establishing biotechnology-related infrastructure in the country.

Jogindernagar

Shimla

Chandigarh

AlwarSohna

Jodhpur Jaipur

GandhinagarAnand

Jamnagar

Baroda

Aurangabad

Pune

Hyderabad

Bhubaneshwar

Konark

Midnapore

Pantnagar

BengaluruChennai

Puducherry

Visakhapatnam

Kochi

Karwar

Madurai

Source: Ernst & Young research, "Mid term appraisal," Eleventh

Five Year Plan

Ahmedabad

INDUSTRY INFRASTRUCTURE

Lucknow

Biotechnology November 2010

16

Details of key biotechnology parks

Parks City Area (in acres)

Shapoorji Pallonji Biotech Park Hyderabad 300

ICICI Knowledge Park Hyderabad 200

International Biotech Park Pune 103

Lucknow Biotech Park Lucknow 20

Golden Jubilee Biotech Park Chennai 8

Ticel Bio Park Chennai 5

• Around 27 operational parks are operational in India.

Industry infrastructure … (2/2)

INDUSTRY INFRASTRUCTURE

Source: Ernst & Young research

Biotechnology November 2010

17

Enabling research infrastructure

• In 2009–2010, postgraduate teaching programs in biotechnology were launched at 8 new universities in addition to existing 62 universities.

• Fellowships increased from 100 to 250 per year for PhD students in addition to 100 postdoctoral and 50 biotechnology overseas associate ships.

• The Eleventh Plan aims to provide grant-in-aid to industry for R&D in certain diseases such as malaria and kala-azar.

INDUSTRY INFRASTRUCTURE

Sources: Ernst & Young research, "Mid term appraisal," Eleventh

Five Year Plan

Key research institutes in India

• Central Drug Research Institute (CDRI), Lucknow

• National Institute of Pharmaceutical Education and Research

(NIPER), Mohali

• Indian Institute of Chemical Technology (IICT), Hyderabad

• Centre for Cellular & Molecular Biology (CCMB), Hyderabad

• Indian Institute of Chemical Biology (IICB), Kolkata

• Indian Toxicology Research Institute (ITRI), Lucknow

• Institute of Genomics and Integrative Biology (IGIB), New

Delhi

• Institute of Microbial Technology (IMTECH), Chandigarh

• National Chemical Laboratory (NCL), Pune

• National Centre for Biological Sciences (NCBS), Bengaluru

• Jawaharlal Nehru Centre for Advanced Scientific Research

(JNCASR), Bengaluru

• Indian Institute of Science (IISc), Bengaluru

• National Institute of Immunology (NII), New Delhi

Biotechnology November 2010

18

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

19

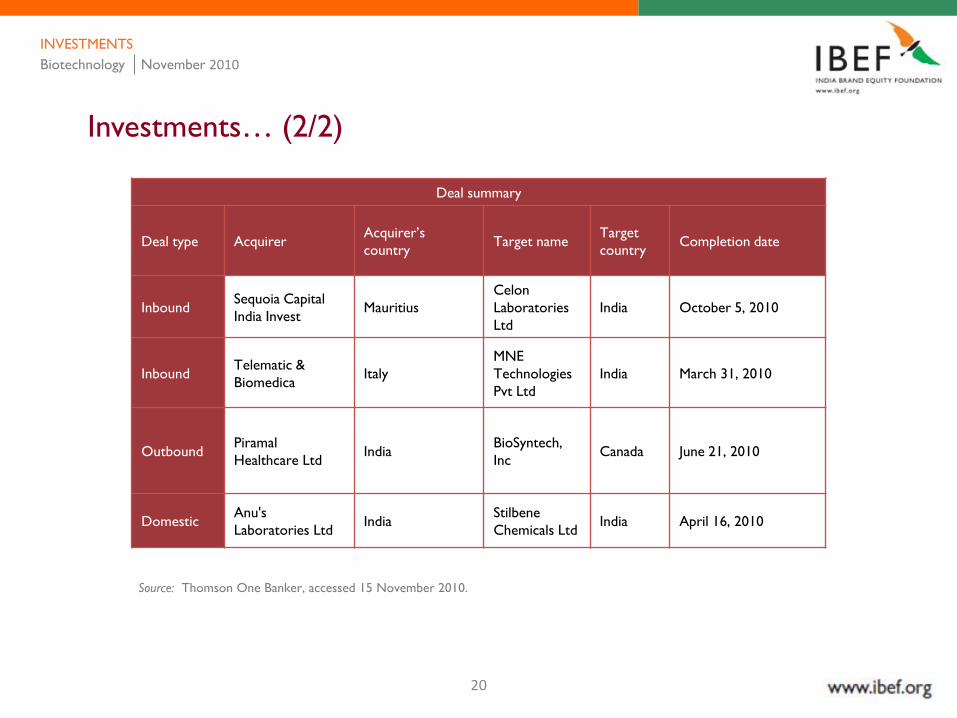

Investments… (1/2)

• Four deals were completed in 2010.

• In June 2010, Piramal Healthcare Ltd acquired Canadian biotechnology company Biosyntech, Inc for US$ 4.196 million.

Cumulative FDI inflow

Period: November 2000 to August 2010

SectorAmount of FDI inflow

(US$ million)

Drugs and pharmaceuticals 1,822.6

M&A scenario — details

Period: January 1, 2010 to October 31, 2010

Deal type No of dealsDeal value

(US$ million)

Inbound 2 24.25

Outbound 1 4.2

Domestic 1 — Source: ―Fact Sheet on Foreign Direct Investment (FDI),‖ Department

of Industrial Policy and Promotion website, www.dipp.nic.in, accessed

15 November 2010.Sources: Thomson One Banker, accessed 15 November 2010; Ernst &

Young analysis.

INVESTMENTS

Biotechnology November 2010

20

Deal summary

Deal type AcquirerAcquirer’s

countryTarget name

Target

countryCompletion date

InboundSequoia Capital

India InvestMauritius

Celon

Laboratories

Ltd

India October 5, 2010

InboundTelematic &

BiomedicaItaly

MNE

Technologies

Pvt Ltd

India March 31, 2010

OutboundPiramal

Healthcare LtdIndia

BioSyntech,

IncCanada June 21, 2010

DomesticAnu's

Laboratories LtdIndia

Stilbene

Chemicals LtdIndia April 16, 2010

Investments… (2/2)

INVESTMENTS

Source: Thomson One Banker, accessed 15 November 2010.

Biotechnology November 2010

21

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

22

• The National Biotechnology Development Strategy (NBDS), approved in 2007, was aimed at strengthening the industry’s human resources and infrastructure while promoting growth and trade. To further support the NBDS, the GoI allocated US$ 375 million for biotech R&D in 2009, which constitutes around 30 per cent of the total budget allocation for this sector.

• The authority to approve biotech products rests with various agencies such as the Review Committee on Genetic Manipulation (RCGM), the Genetic Engineering Approval Committee (GEAC) and the Drugs Controller General of India (DCGI). The NBDS has proposed the establishment of an independent and autonomous statutory body, the National Biotechnology Regulatory Authority (NBRA), to provide a consistent mechanism for regulatory approvals.

• In July 2008, India’s DBT drafted a new legislation, the National Biotechnology Regulatory Act, to establish and empower the NBRA.

• In the Eleventh Plan, the approval process for legal framework ―The Protection and Utilisation of Public Funded Intellectual Property Bill, 2008‖ was initiated. The bill aims to promote innovation and patenting between innovators and institutions on a profit-sharing basis.

Policy and regulatory framework… (1/2)

Source: ―Policy and rules,‖ Department of Biotechnology website, www.dbtindia.nic.in, accessed 15 November 2010; "Mid term appraisal," Eleventh

Five Year Plan

POLICY AND REGULATORY FRAMEWORK

Biotechnology November 2010

23

Government of India

Ministry of Science & Technology Ministry of Environment & Forests

Recombinant DNA

Advisory Committee

(RDAC)

Regulatory Committee

on Genetic Manipulation

(RCGM)

Genetic Engineering Approval

Committee (GEAC)

Institutional Biosafety

Committee (IBSC)

Department of BiotechnologyDepartment of Environment, Forests

& Wildlife

Policy and regulatory framework… (2/2)

Source: ―Policy and rules,‖ Department of Biotechnology website, www.dbtindia.nic.in, accessed 15 November 2010.

POLICY AND REGULATORY FRAMEWORK

Biotechnology November 2010

24

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

25

• In India, the oncology market in 2008 was valued at around US$ 225 million and is expected to reach US$ 850 million by 2012, growing at a CAGR of nearly 30 per cent.

• Companies such as Dabur, Biocon, Dr Reddy’s, Intas, Roche, Cipla and Sun Pharmaceuticals have a significant market presence in the Indian oncology market.

• In addition, current size for cancer diagnostics and treatment equipment is close to US$ 270 million in 2009, which form the largest segment in medical devices segment and is an opportunity for segment related diversification.

• Novo Nordisk, Eli Lilly, Biocon and Shantha Biotech are the leading players in this segment, while Ranbaxy, Sun Pharma and Glenmark are among the new players.

• Companies are targeting the development of drugs with non-invasive insulin delivery technology.

Opportunities — product segments … (1/3)

Sources: "Mid term appraisal," Eleventh Five Year Plan, ―Cancer drug market to touch $48b in 2008,‖ The Times of India website,

www.timesofindia.indiatimes.com, accessed 18 January 2010, ICE publication,

www.ice.gov.it/paesi/asia/india/upload/182/Sector%20Report%20Biotechnology%20-%202009.pdf , accessed 15 November 2010

OPPORTUNITIES

• According to the Eleventh Plan, India is well-poised to become the world’s vaccine manufacturing hub with vaccines for various therapy areas at various stages of clinical trial.

• Development of vaccines for a wide array of diseases are in various stages of approval. Phase –iii clinical trials for rotaviral vaccine have been initiated and vaccines for diseases such as rabies, typhoid, leprosy, anthrax, cholera, malaria and Japanese encephalitis are in various stages of trials. India is well positioned to launch about four vaccines a year beginning 2012.

• Vaccine for H1N1 has been developed under government’s programme for development of indigenous products.

Vaccines

Oncology

Insulin

Biotechnology November 2010

26

Opportunities — product segments … (2/3)

• Stem cell research is an emerging opportunity area. India is the second country after the US to allow human clinical trials for drugs using stem cell research. Stem cell research centres at AIIMS and CMC Vellore have been launched.

• A new treatment for heart attack is under development at the research centre of India’s biggest stem cell banking company, LifeCell, in collaboration with US-based device manufacturer for stem cell harvesting, Harvest Technologies. In addition, stem cell finds application in the treatment of Parkinson’s disease, Alzheimer's disease and diabetes.

Sources: Ernst & Young research, "Mid term appraisal," Eleventh Five Year Plan, ABLE-Biospectrum industry survey, June 2010; ―Biotechnology

industry in India: Opportunities for growth,‖ http://www.eximbankindia.com/op/op137.pdf , accessed 17 November 2010

OPPORTUNITIES

Stem cell research

Nanotechnology

• The GoI supports nanotechnology through its Vision Group initiative. The GoI plans to build three national institutes for nano-science by investing US$ 250 million in infrastructure programmes.

• Nanotechnology has the potential to revolutionise the Indian agriculture scenario and transform the entire food industry. Several Indian firms and research institutes are also working on developing drug delivery products using nanotechnology.

Biotechnology November 2010

27

Opportunities — biosimilars … (3/3)

• The increasing use of biologics in disease areas such as cancer and auto-immune and orphan diseases, in addition to healthcare cost containment, has driven the growth of biosimilars.

• Companies in this space include Reliance Biopharma, Shantha Biotech, Panacea Biotec, Wockhardt, Dr Reddy’s, Biocon, Intas Biopharmaceuticals and Avesthagen.

Future opportunity in biosimilars (US$ billion)

Sources: ―Teva investor presentation,‖ Teva Pharm website, www.tevapharm.com, accessed 28 January 2010; Ernst & Young research.

OPPORTUNITIES

14.0

39.0

23.0

76.0

115.0

Patents expired before 2010 Patents expiring 2010-2015 Patents expiring 2016-2020 Biosimilar opportunity-2008 brand value

Biosimilar opportunity-2015 brand value

Biotechnology November 2010

28

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

BIOTECHNOLOGY November 2010

29

Industry associations

Association of Biotechnology Led Enterprises (ABLE)

# 123/C, 16th Main Road, 5th Cross, 4th Block

Near Sony World Showroom/Headstart School

Koramangala, Bengaluru – 560034

Phone: 91 80 41636853 25633853

E-mail: [email protected]

Website: www.ableindia.org

INDUSTRY ASSOCIATIONS

All India Biotech Association (AIBA)

"VIPPS Center" 2. Local Shopping Centre Block EFGH, Masjid Moth,

Greater Kailash-II, New Delhi-110048

Tel: 91 11 29211487 (Direct), 29220546/547

Fax: 91 11 29223089, 29229166

Email: [email protected]

Website: www.aibaonline.com

Biotechnology November 2010

30

Note

Wherever applicable, numbers in the report have been rounded off to the nearest whole number.

Conversion rate used: US$ 1= INR 48

NOTE

Biotechnology November 2010

31

India Brand Equity Foundation (IBEF) engaged Ernst &

Young Pvt Ltd to prepare this presentation and the same

has been prepared by Ernst & Young in consultation with

IBEF.

All rights reserved. All copyright in this presentation and

related works is solely and exclusively owned by IBEF. The

same may not be reproduced, wholly or in part in any

material form (including photocopying or storing it in any

medium by electronic means and whether or not

transiently or incidentally to some other use of this

presentation), modified or in any manner communicated

to any third party except with the written approval of

IBEF.

This presentation is for information purposes only. While

due care has been taken during the compilation of this

presentation to ensure that the information is accurate to

the best of Ernst & Young and IBEF’s knowledge and belief,

the content is not to be construed in any manner

whatsoever as a substitute for professional advice.

Ernst & Young and IBEF neither recommend nor endorse

any specific products or services that may have been

mentioned in this presentation and nor do they assume

any liability or responsibility for the outcome of decisions

taken as a result of any reliance placed on this

presentation.

Neither Ernst & Young nor IBEF shall be liable for any

direct or indirect damages that may arise due to any act

or omission on the part of the user due to any reliance

placed or guidance taken from any portion of this

presentation.

DISCLAIMER

BIOTECHNOLOGY November 2010