bio-based building blocks and polymers in the world

TRANSCRIPT

Bio-based Building Blocks and Polymers in the World

Capacities, Production and Applications: Status Quo and Trends towards 2020

Authors: Florence Aeschelmann (nova-Institute), Michael Carus (nova-institute) and ten renowned international experts

This is the short version of the full maket study (474 pages, 3,000 €). Both are available at www.bio-based.eu/markets.

Saccharose

Fatty acidsGlycerol

Epichlorohydrin

Epoxy resins

Starch

1,3 Propanediol

Isobutanol

Succinate

Acrylic acid

Superabsorbent Polymers

Other Furan-based polymers

PEF

p-Xylene

Ethylene

Propylene

Vinyl Chloride

Methyl Metacrylate

Isosorbide

SBR

THF

Teraphtalic acidPBT

PBS

PET

PE

PU

PU

PA

Polyols

PU

PP

PU

PC

PVC

PTTPLA

HMF

PHA

FDCA

PHA

PA

PMMAPBAT

EPDM

HMDA

Caprolactam

AdipicAcid

3-HP

PET-like

Lactic acid

Sorbitol

Ethanol

Lignocellulose

Natural Rubber

Plant oilsFructose

Natural RubberStarch-based PolymersLignin-based PolymersCellulose-based Polymers

Glucose

Lysine

PU

MEG

1,4 Butanediol

Diacids (Sebacic acid)

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

2 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 3

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Bio-based polymers – Production capacity will triple from 5.1 million tonnes in 2013 to 17 million tonnes in 2020. Bio-based drop-in PET and the new polymers PLA and PHA show the fastest rates of market growth. The lion’s share of capital investment is expected to take place in Asia. The 5.1 million tonnes bio-based production capacity represent a 2% share of overall structural polymer production at 256 million tonnes in 2013. The bio-based polymer turnover was about €10 billion worldwide in 2013.

Two years after the first market study was released, Germany’s nova-Institute is publishing a complete update of the most comprehensive market study of bio-based polymers ever made. This update will expand the market study’s range, including bio-based building blocks as precursor of bio-based polymers.

The nova-Institute carried out this study in collaboration with renowned international experts from the field of bio-based building blocks and polymers. The study investigates every kind of bio-based polymer and, for the first time, several major building blocks produced around the world.

BIO-BASED STRUCTURAL POLYMERS CURRENT BIO-BASED CARBON CONTENT*

PRODUCING COMPANIES IN 2013 AND UNTIL 2020

LOCATIONS IN 2013 AND UNTIL 2020

PRODUCTION CAPACITIES IN 2013 (TONNES)

Cellulose acetate CA 50% 17 20 850,000

Epoxies – 30% – – 1,210,000

Ethylene propylene diene monomer rubber

EPDM 50% to 70% 1 1 45,000

Polyamides PA 40% to 100% 9 11 85,000

Poly(butylene adipate-co-terephthalate)

PBAT Up to 50%** 4 5 75,000

Polybutylene succinate PBS Up to 100%** 10 11 100,000

Polyethylene PE 100% 1 1 200,000

Polyethylene terephtalate PET 20% 5 5 600,000

Polyhydroxyalkanoates PHA 100% 14 16 32,000

Polylactic acid PLA 100% 28 34 195,000

Polytrimethylene terephthalate PTT 27% 1 2 110,000

Polyurethanes PUR 10% to 100% 7 7 1,200,000

Starch Blends*** – 25% to 100% 15 16 430,000

Total 112 129 5,132,000

* Bio-based carbon content: fraction of carbon derived from biomass in a product (EN 16575 Bio-based products – Vocabulary)

** Currently still mostly fossil-based with existing drop-in solutions and a steady upward trend

*** Starch in plastic compound

Table 1: Bio-based polymers, short names, current bio-based carbon content, producing companies with locations and production capacities in 2013

Imprint

Bio-based Building Blocks and Polymers in the World – Capacities, Production and Applications: Status Quo and Trends toward 2020

PublisherMichael Carus (V.i.S.d.P.)

nova-Institut GmbHChemiepark KnapsackIndustriestraße 30050354 Hürth, Germany

Authors of the short versionFlorence Aeschelmann (nova-Institute)[email protected],Michael Carus (nova-Institute)

LayoutNorma Sott

Edition2015-05

Order the full report

The full report can be ordered for 3,000 € plus VAT at www.bio-based.eu/markets

All nova-Institute graphs can be downloaded at http://bio-based.eu/graphics/#top.

All European Bioplastics graphs can be downloaded at http://en.european-bioplastics.org/press/press-pictures/labelling-logos-charts

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

4 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 5

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Share of bio-based polymers in the total polymer marketRather than simply listing the usual structural polymers, Figure 1 gives an overview of all kinds of polymers, including rubber products, man-made fibres and functional polymers. This figure includes bio-based shares at different levels.The bio-based share for structural polymers, which are the focus of the study, is 2%. For polymers overall, however, the bio-based share is even higher (8.3%) because of the higher bio-based shares in rubber (natural rubber) and man-made fibres (mainly cellulosic fibres). In 2011, these shares were 1.5% and 8.2% respectively. The bio-based share is clearly growing at a faster rate than that of the global polymer market.

This study focuses exclusively on bio-based building block and polymer producers, and the market data therefore does not cover the bio-based plastics branch. We must clearly differentiate between these two terms. A polymer is a chemical compound consisting of repeating structural units (monomers) synthesized through a polymerization or fermentation process, whereas a plastic material constitutes a blend of one or more polymers and additives.

Table 1 gives an overview on the covered bio-based polymers and the producing companies with their locations and production capacities in 2013.

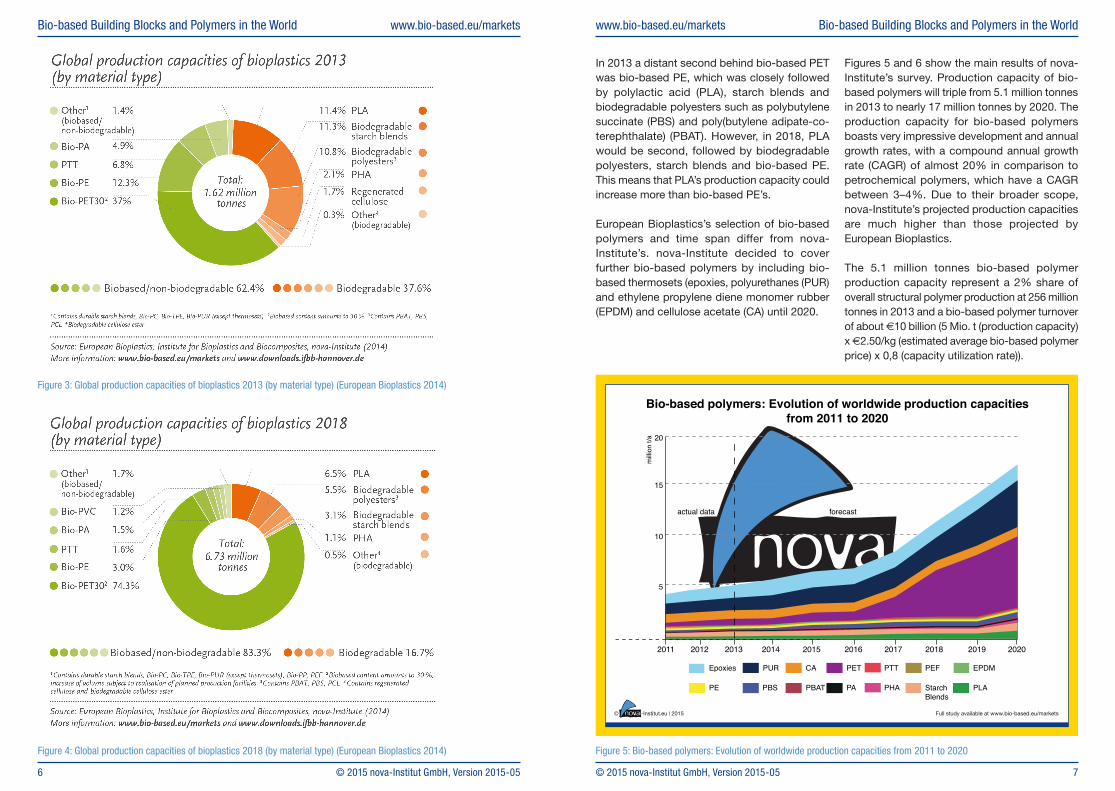

Bio-based polymersIn 2014, for the first time, the association “European Bioplastics” used nova-Institute’s market study as its main data source for their recently published market data. For European Bioplastics’s selection of bio-based polymers, which differs from nova-Institute’s selection, bio-based polymers production capacities are projected to grow by more than 400% by 2018.1 The graph in Figure 2 shows European Bioplastics’s growth projection of bio-based polymers production; by 2018, these could grow by over 400%, or from 1.6 million tonnes in 2013 to 6.7 million tonnes in 2018 in absolute terms. The market is clearly dominated by bio-based and non-biodegradable polymers.

Drop-in bio-based polymers such as polyethylene terephthalate (PET) and polyethylene (PE) lead this category. Drop-in bio-based polymers are chemically identical to their petrochemical counterparts but at least partially derived from biomass. European Bioplastics uses plastic as a synonym for polymer.

The global capacities in 2013 and 2018 have been split by material type in Figures 3 and 4 respectively. Bio-based PET is the overall market leader and is expected to grow at a quick rate, from 37% in 2013 to 74% in 2018. As a consequence, the bio-based non-biodegradable polymers market is expected to grow strongly as well since bio-based PET is part of this category.

Figure 1: Polymers worldwide, bio-based shares (2013)

ⓒ –Institute.eu|2015

Polymers worldwide, bio-based shares (2013)

Rubber productsTotal 26.5 million t (2012)

bio-based:11.3 million t (2012)

(43% of total)

Functional and structural polymers***

Total 314 million t (2013)*bio-based: 15.2 million t

(4.8% of total)

Man-made fibresTotal 55 million t (2013)

bio-based: 6 million t (2013)(11% of total)

ca. 95% not covered by polymer statistics

Paper starch8 million t (2013)

Bio-based functional polymers for paints, coatings,

adhesives and others2 million t

Linoleum100,000 t

Bio-based structural polymers

5.1 million t(2013)**

PE & PETStarch Blends

PLAPHA/PHB

PACA...

(*): Data from PlasticsEurope 2014. Original data show 299 million tonnes for 2013 in total. With the same sharesas 2011 (PlasticsEurope 2012) this would mean: 251 million tonnes structural polymers and 48 million tonnesfunctional polymers plus bio-based polymers (nova 2015); (**): nova-Institute 2015; (***): Polymers coveringthermoplastic and thermosets; Different additional sources, like International Rubber Study Group(www.macplas.it, 13-07-10), The Fiber Year 2014 (14-05)

Structural polymers***256 million t total (2013)*

bio-based:5.2 million t (2013)

(2% of total)

Polymers***Total ca. 393 million t

bio-based:32.5 million t(8.3% of total)

Functional polymers***Total 58 million t (2013)*

bio-based:10 million t (2013)

(17% of total)

Full study available atwww.bio-based.eu/markets

Figure 2: Global production capacities of bioplastics (European Bioplastics 2014)

1 Market data graphics are available for download in English and German: http://en.european-bioplastics.org/press/press-pictures/labelling-logos-charts

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

6 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 7

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

In 2013 a distant second behind bio-based PET was bio-based PE, which was closely followed by polylactic acid (PLA), starch blends and biodegradable polyesters such as polybutylene succinate (PBS) and poly(butylene adipate-co-terephthalate) (PBAT). However, in 2018, PLA would be second, followed by biodegradable polyesters, starch blends and bio-based PE. This means that PLA’s production capacity could increase more than bio-based PE’s.

European Bioplastics’s selection of bio-based polymers and time span differ from nova-Institute’s. nova-Institute decided to cover further bio-based polymers by including bio-based thermosets (epoxies, polyurethanes (PUR) and ethylene propylene diene monomer rubber (EPDM) and cellulose acetate (CA) until 2020.

Figures 5 and 6 show the main results of nova-Institute’s survey. Production capacity of bio-based polymers will triple from 5.1 million tonnes in 2013 to nearly 17 million tonnes by 2020. The production capacity for bio-based polymers boasts very impressive development and annual growth rates, with a compound annual growth rate (CAGR) of almost 20% in comparison to petrochemical polymers, which have a CAGR between 3–4%. Due to their broader scope, nova-Institute’s projected production capacities are much higher than those projected by European Bioplastics.

The 5.1 million tonnes bio-based polymer production capacity represent a 2% share of overall structural polymer production at 256 million tonnes in 2013 and a bio-based polymer turnover of about €10 billion (5 Mio. t (production capacity) x €2.50/kg (estimated average bio-based polymer price) x 0,8 (capacity utilization rate)).

Figure 3: Global production capacities of bioplastics 2013 (by material type) (European Bioplastics 2014)

Figure 4: Global production capacities of bioplastics 2018 (by material type) (European Bioplastics 2014)

Full study available at www.bio-based.eu/markets-Institut.eu | 2015©

EPDMPEFPTTPETCAPUREpoxies

PLAStarch Blends

PHAPAPBATPBSPE

actual data forecast

5

10

15

20

Bio-based polymers: Evolution of worldwide production capacitiesfrom 2011 to 2020

2020201920182017201620152014201320122011 m

illion

t/a

Figure 5: Bio-based polymers: Evolution of worldwide production capacities from 2011 to 2020

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

8 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 9

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Polytrimethylene terephthalate (PTT) is 27% bio-based and made out of bio-based 1,3-propanediol (1,3-PDO) and currently petro-based TPA. PTT is similar to PET since both have TPA as precursor. Bio-based PTT and 1,3-PDO are produced by one leading company, DuPont. The market is well established and is not expected to grow much.

Polyethylene furanoate (PEF) is 100% bio-based and is produced out of bio-based 2,5-furandicarboxylic acid (2,5-FDCA) and MEG. PEF is a brand new polymer, which is expected to enter the market in 2017. Just as PTT, PEF is similar to PET. Both PEF and PET are used in bottle production, however PEF is said to have better properties, such as better barrier properties, than PET. Technology company Avantium is heavily involved in the development of PEF and is planning to introduce PEF to the market in 2017.

Ethylene propylene diene monomer rubber (EPDM) is made out of bio-based ethylene and can be 50% to 70% bio-based. Specialty chemicals company Lanxess is currently producing bio-based EPDM in Brazil. The market is small and is not expect to grow in the coming years.

Polyethylene (PE) is a 100% bio-based drop-in polymer. The bio-based building block needed is bio-based ethylene, which is made out of sugar cane. Brazilian petrochemical company Braskem produces bio-based PE in Brazil. Bio-based PE has been on the market for a few years but its production capacity has hitherto remained the same. Further developments have been slowed down because of the shale gas boom.

This bio-based share of overall polymer production has been growing over the years: it was 1.5% in 2011 (3.5 million tonnes bio-based for a global production of 235 million tonnes). With an expected total polymer production of about 400 million tonnes in 2020, the bio-based share should increase from 2% in 2013 to more than 4% in 2020, meaning that bio-based production capacity will grow faster than overall production.

The most dynamic development is foreseen for drop-in bio-based polymers, but this is closely followed by new bio-based polymers. Drop-in bio-based polymers are spearheaded by partly bio-based PET, whose production capacity was around 600,000 tonnes in 2013 and is projected to reach about 7 million tonnes by 2020, using bio-ethanol from sugar cane. Bio-based PET production is expanding at high rates worldwide, largely due to the Plant PET Technology Collaborative (PTC) initiative launched by The Coca-Cola Company. The second most dynamic development is foreseen for polyhydroxyalkanoates (PHA), which, contrary to bio-based PET, are new polymers, but still have similar growth rates to those of bio-based PET. PLA and bio-based PUR are showing impressive growth as well: their production capacities are expected to almost quadruple between 2013 and 2020.

Here are some details on each bio-based polymer covered in the report:

Epoxies are approximately 30% bio-based (only bio-based carbon content2 considered in this report) and are produced out of bio-based epichlorohydrin. The market is well established and is not expected to grow much since epoxies have already long been partly bio-based.

Polyurethanes (PUR) can be 10% to 100% bio-based. PUR are produced from natural oil polyols (NOP). Bio-based succinic acid can be used to replace adipic acid. The global PUR market (including petro-based PUR) is continuously growing but the bio-based PUR market is expected to grow faster.

Cellulose acetate (CA) is 50% bio-based. This market is similar to that of epoxies: well established, for example cigarette filters are made from CA, with small growth.

Polyethylene terephthalate (PET) is currently 20% bio-based and produced out of bio-based monoethylene glycol (MEG) and terephthalic acid (TPA) as a drop-in bio-based polymer. TPA is currently still petro-based but subject to ongoing R&D. Bio-based TPA can be produced at pilot scale. Most bio-based PET and MEG are produced in Asia. Bio-based PET is one of the leaders of the bio-based polymers market and is slated to become the bio-based polymer with the biggest production capacity by far. This is largely due to the Plant PET Technology Collaborative (PTC) initiative launched by The Coca Cola Company.

Bio-based epoxies, PUR, CA and PET have huge production capacities with a well established market in comparison with other bio-based polymers. However, other bio-based polymers listed on Figure 6 show strong growth as well. Figure 6 shows the evolution of worldwide production capacities only for selected bio-based polymers (without bio-based epoxies, PUR, CA and PET). Some of these polymers are brand new bio-based polymers. That is why their markets are smaller and need to be developed correspondingly.

2 Bio-based carbon content: fraction of carbon derived in a product (EN 16575 Bio-based products from biomass– Vocabulary)

Full study available at www.bio-based.eu/markets-Institut.eu | 2015©

0.5

1

1.5

2

2.5

3

2020201920182017201620152014201320122011

EPDM

PHA

PEF

PA

PTT

PBAT PLA

PBS

Selected bio-based polymers: Evolution of worldwide productioncapacities from 2011 to 2020

actual data forecast

PE

Starch Blends

milli

on t/

a

Figure 6: Selected bio-based polymers: Evolution of worldwide production capacities from 2011 to 2020

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

10 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 11

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Bio-based building blocks as a precursor of bio-based polymersFor the first time, the production capacities of some major building blocks have been reported in the market study. The total production capacity of the bio-based building blocks reviewed in this study was 2 million tonnes in 2013 and is expected to reach 4.4 million tonnes in 2020, which means a CAGR of almost 12%. The most dynamic developments are spearheaded by succinic acid and 1,4-BDO, with MEG as a distant runner-up. Figure 7 shows the evolution of worldwide production capacities for some major building blocks.

Bio-based MEG, L-lactic acid (L-LA), ethylene and epichlorohydrin are relatively well established on the market. These bio-based building blocks cover most of the total production capacity. They are expected to keep on growing, especially bio-based MEG and ethylene, whereas L-LA and bio-based epichlorohydrin are projected to grow at lower rate. However, the most dynamic developments are spearheaded by succinic acid and 1,4-BDO. Both are brand new drop-in bio-based building blocks on the market. The first facilities are currently running and more will be built in the coming years.

Polybutylene succinate (PBS) is biodegradable and currently mostly fossil-based but could in theory be 100% bio-based. PBS is produced from 1,4-butanediol (1,4-BDO) and succinic acid. Both building blocks are available bio-based but 1,4-BDO is not commercially available yet; this is expected in 2015. PBS is currently produced exclusively in Asia. It is expected to grow and profit from the availability and lower cost of bio-based succinic acid.

Poly(butylene adipate-co-terephthalate) (PBAT) is also currently mostly fossil-based. PBAT is produced from 1,4-BDO, TPA and adipic acid. PBAT is biodegradable. PBAT can theoretically be up to 50% bio-based since bio-based adipic acid is not available yet. It is still at the research stage. PBAT has mostly been produced by one big company, BASF, but a new player, Jinhui ZhaolongHigh Technology, entered the market and another one, Samsung Fine Chemicals, which has a relatively small production capacity at the moment, is planning to extend its production capacity.

Polyamides (PA) are a big family since there are many different types of polyamides. This explains the wide range of bio-based carbon content: from 40% to 100%. Polyamides are generally based on sebacic acid, which is produced from castor oil. Evonik has recently developed a polyamide based on palm kernel oil. The market, which is expected to grow moderately, is headed by one big player, Arkema.

Polyhydroxyalkanoates (PHA) are 100% bio-based and biodegradable even in cold sea water. PHA are produced through a fermentation process mainly by specific bacteria. Many different companies are involved in the production of PHA. The market is currently very small but is expected to grow tremendously. The joint venture Telles, set by Metabolix and ADM in 2006, aimed at big capacity but hardly sold any PHA and subsequently collapsed in 2012. PHA are brand new polymers, which means their market still needs time to fully develop.

Nevertheless PHA producers and several new players are optimistic and see potential in PHA. Therefore, production capacity is expected to have grown tenfold by 2020.

Starch blends are completely biodegradable and 25% to 100% bio-based, with starch added to one or several biodegradable polymers. Many players are involved in the production of starch blends but Italian company Novamont is currently market leader. The market is expected to keep on growing, with production capacity projected to double between 2013 and 2020.

Polylactic acid (PLA) is 100% bio-based and biodegradable but only under certain conditions: PLA is industrially compostable. Produced by numerous companies worldwide, with NatureWorks as market leader, PLA is the most well established new bio-based polymer. However, the PLA market is still expected to grow further, with a projected fourfold growth between 2013 and 2020. PLA can already be found at near-comparable prices to fossil-based polymers.

In short, the most dynamic development is expected for bio-based PET, with a projected production capacity of about 7 million tonnes by 2020. Second in the drop-in polymers group are bio-based polyurethanes. Regardless, new bio-based polymers such as PLA and PHA are showing impressive growth as well: PLA production capacity is expected to almost quadruple and PHA production capacity is expected to grow tenfold between 2013 and 2020.

Detailed information on the development of bio-based PET and PLA and other polymers can be found in the full report.

Full study available at www.bio-based.eu/markets-Institut.eu | 2015©

D-LA2,5 FDCA2,3-BDOLactide1,3-PDO1,4-BDO

Succinic acidEpichlorohydrinEthyleneL-LAMEG

Selected bio-based building blocks: Evolution of worldwide production capacities from 2011 to 2020

actual data forecast

1

2

3

4

5

6

2020201920182017201620152014201320122011

milli

on t/

aFigure 7: Selected bio-based building blocks: Evolution of worldwide production capacities from 2011 to 2020

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

12 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 13

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Investment by regionMost investment in new bio-based polymer capacities will take place in Asia because of better access to feedstock and a favourable political framework. Figures 8 and 9 show the 2013 and 2018 global production capacities for bio-based polymers repartitioned by region. European Bioplastics published these market data, which take into account fewer types of bio-based polymers than nova-Institute. Due to the complexity of the manufacturing value chain structure of epoxies, PUR and cellulose acetate, the repartitions by region cannot be reliably determined for all bio-based polymers. As a result, a graph representing the repartition by region with nova-Institute’s scope is not provided in the report, but only for the subgroup selected by European Bioplastics.

Europe’s share is projected to decrease from 17.3% to 7.6%, and North America’s share is set to fall from 18.4% to 4.3%, whereas Asia’s is predicted to increase from 51.4% to 75.8%. South America is likely to remain constant with a share at around 12%. In other words, world

market shares are expected to shift dramatically. Asia is predicted to experience most of the developments in the field of bio-based building block and polymer production, while Europe and North America are slated to lose more than a half and just over three quarters of their shares, respectively.

Production capacities in EuropeFigure 10 shows the evolution of production capacities in Europe without bio-based thermosets (epoxies and PUR) and cellulose acetate.Europe’s position in producing bio-based polymers is limited to just a few polymers. Europe has so far established a solid position mainly in the field of starch blends and is expected to remain strong in this sector for the next few years. Nevertheless, a number of developments and investments are foreseen in Europe. PLA production capacities, especially starch blend production capacities, are predicted to grow. The growth of these increased production capacities for starch blends can be traced back to Italy’s Novamont, a leading company in this field.

Here are some details on each bio-based building block covered in the report:

Monoethylene glycol (MEG) is one of PET’s building blocks. Bio-based MEG is a drop-in which is mostly produced in Asia. The very fast increase in bio-based PET production has had a considerable impact on the production capacities of bio-based MEG. Bio-based PET actually leads the bio-based polymers group, which is largely due to the Plant PET Technology Collaborative (PTC) initiative launched by The Coca-Cola Company.

L-Lactic acid (L-LA) is PLA’s building block, together with D-lactic acid (D-LA). Both are optical isomers of LA. L-LA is much more common than D-LA since D-LA is more complicated to produce. Lactide is an intermediate between LA and PLA. It can be bought as such to produce PLA. A lot of different companies are involved in this business worldwide since most LA has long been used in the food industry as, among other things, a food preservative, pH regulator and flavouring agent. The production capacities do not only include LA used for polymer production, but also for the food industry. It is estimated that more than a half of LA is used by the food industry.

Ethylene is PE’s building block. Bio-based ethylene is currently made from sugar cane in Brazil. Further developments have slowed down because of a sudden extreme price drop in petro-based ethylene that happened due to the shale gas boom.

Epichlorohydrin is one of the building blocks of epoxies. Glycerin, which is a by-product of the production of biodiesel, is used as feedstock.

Succinic acid is a very versatile building block. Bio-based polymers such as PBS can be made of succinic acid but also other bio-based building blocks such as 1,4-BDO. It can be used as well in PUR to replace adipic acid. However, the market still has to be developed. Petro-based succinic acid is not a big market since petro-based succinic acid is relatively expensive. Bio-based succinic acid is actually cheaper than its petro-based counterpart. The first facilities have been running since 2013 and the next ones are already in the pipeline.

1,4-Butanediol (1,4-BDO) is also a versatile building block. At the moment no facility able to produce commercial quantities is running but the first one is expected in 2015. 1,4-BDO can directly be produced from biomass or indirectly from succinic acid. Since bio-based succinic is relatively new to the market, this partly explains why 1,4-BDO is still not commercially available. 2,3-Butanediol (2,3-BDO) is another isomer of butanediol. Global Bio-Chem Technology Group, based in China, is currently producing 2,3-BDO, which they obtain by processing corn.

1,3-Propanediol (1,3-PDO) is one of PTT’s building blocks. 1,3-PDO is mostly produced from corn by DuPont. The market is well established and is not expected to grow much.

2,5-Furandicarboxylic acid (2,5-FDCA) can be combined with MEG to produce polyethylene furanoate (PEF). 2,5-FDCA is a brand new building block which is expected to come to the market in 2017. Avantium is deeply involved in 2,5-FDCA but others are also showing interest.

Detailed information on the development of bio-based building blocks can be found in the full report.

Figure 8: Global production capacities of bioplastics in 2013 (by region) (European Bioplastics 2014)

Figure 9: Global production capacities of bioplastics in 2018 (by region) (European Bioplastics 2014)

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

14 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 15

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Market segmentsThe packaging industry consumes most petro-based polymers. For bio-based polymers, the same trend can be observed: the major part of this as rigid packaging (bottles for example) and the rest as flexible packaging (films for example). These uses cannot come as a surprise, since bio-based PET is one of the biggest bio-based polymers in terms of capacity and is mostly used for the production of bottles. On the other hand, the packaging industry has a considerable interest in biodegradability since packaging is only needed for short times but in big quantities, which contributes to the accumulation of waste. It should be understood that not all bio-based polymers are biodegradable but some important ones are, e.g. PHA, PLA and starch blends. This feature is also interesting for agriculture and horticulture applications (mulch films for example). However, bio-based polymers are also

used in many different other market segments. Figures 11 and 12 show the global production of bio-based polymers by market segment in 2013 and in 2018.

The order of importance of the market segments is expected to stay approximately the same between 2013 and 2018. Rigid packaging is supposed to keep its first place by growing tremendously with an almost sevenfold growth in only five years. This is again due to the very fast development of bio-based PET. However, the automotive sector is projected to gain faster importance than consumer goods and agriculture sectors. Automotive is actually the second most dynamic after rigid packaging and is followed by electronics, a sector which is still very small, followed by textiles, which is already well established on the global market.

One noteworthy finding of other studies is that Europe shows the strongest demand for bio-based polymers, while production tends to take place elsewhere, namely in Asia. In Europe, bio-based polymer production facilities for PLA are not only small in size but also small in number. On the other hand, bio-based PA and CA production is based in Europe and is likely to continue supplying for the growing markets of the building and construction and automotive sectors. Europe does have industrial production facilities for PBAT which is still fully fossil-based. However, judging by industry announcements and the ever-increasing capacity of its bio-based precursors, PBAT is expected to be increasingly bio-based, with a projected 50% share by 2020. Housing the leading chemical corporations, Europe is particularly strong and has great potential in the fields of high value fine chemicals and building blocks for the production

of inter alia bio-based PA, PUR and thermosets. However, only few specific, large-scale plans for bio-based building blocks incorporating concrete plans for the production of bio-based polymers have been announced to date.The European Union’s relatively weak position in the production of bio-based polymers is largely the consequence of an unfavourable political framework. In contrast to bioenergy and biofuels, there is no European policy framework to support bio-based polymers, whereas bioenergy and biofuels receive strong and ongoing support during commercial production (quotas, tax incentives, green electricity regulations, market introduction programs, etc.). Without comparable support, bio-based chemicals and polymers will suffer further from underinvestment by the private sector. It is currently much safer and much more attractive to invest in bio-based polymers in Asia, South America and even North America.

Full study available at www.bio-based.eu/markets-Institut.eu | 2015©

Bio-based polymers: Evolution of production capacities in Europefrom 2011 to 2020 (without thermosets and cellulose acetate)

0.2

0.4

0.6

1

0.8

2020201920182017201620152014201320122011

PLAStarch Blends PEF PAPBAT

milli

on t/

a

0

200000

400000

600000

800000

1000000

2020201920182017201620152014201320122011

actual data forecast

Figure 10: Bio-based polymers: Evolution of production capacities in Europe from 2011 to 2020 (without thermosets and cellulose acetate)

Figure 11: Global production capacities of bioplastics 2013 (by market segments) (European Bioplastics 2014)

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

16 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 17

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Content of the full reportThis 500-page report presents the findings of nova-Institute’s market study, which is made up of three parts: “market data”, “trend reports” and “company profiles”.The “market data” section presents market data about total production capacities and the main application fields for selected bio-based polymers worldwide (status quo in 2013, trends and investments towards 2020). Due to the lack of 100% reliable market data about some polymers, which is mainly due to the complexity of their manufacturing value chain structure (namely thermosets and cellulose acetate) or their pre-commercial stage (CO2-based polymers), this section contains three independent articles by experts in the field who present and discuss their views on current and potential market development. However, this part not only covers bio-based polymers, but also investigates the current bio-based building block platforms.

The “trend reports” section contains a total of eleven independent articles by leading experts in the field of bio-based polymers and building blocks. These trend reports cover in detail every recent issue in the worldwide bio-based building block and polymer market.The final “company profiles” section includes company profiles with specific data including locations, bio-based building blocks and polymers, feedstocks and production capacities (actual data for 2011 and 2013 and forecast for 2020). The profiles also encompass basic information on the companies (joint ventures, partnerships, technology and bio-based products). A company index by bio-based building blocks and polymers, with list of acronyms, follows.

Updates to the reportnova-Institute will provide annual updates of the report based on the existing report and the continuously updated data. The trend reports will be updated every second year at least.

Figure 13 shows the worldwide shares of bio-based polymers production in different market segments in 2013 and 2020 for nova-Institute’s scope of bio-based polymers (with thermosets and cellulose acetate).

The same statement can be made regarding the packaging sector: packaging (rigid and flexible together) is the leader, with a clear advantage for rigid packaging, which is slated to grow strongly. On the other hand, automotive, building and construction, textiles and consumer goods are much bigger because bio-based epoxies, polyurethanes and cellulose acetate are used in these sectors. The smallest market segments are agriculture and functional. In agriculture, applications are mostly limited to biodegradable polymers (mulch films), which

are clearly not a market leader in terms of capacities – but depending on future policy on plastic microparticles, mulch films and other biodegradable applications could grow strongly. Functional polymers are used for coatings, adhesives, paint and ink applications, which require relatively small quantities of polymers.

Figure 12: Global production capacities of bioplastics 2018 (by market segments) (European Bioplastics 2014)

Full study available at www.bio-based.eu/markets-Institut.eu | 2015©

Worldwide shares of bio-based polymers production in differentmarket segments in 2013 and 2020

Packaging - rigid(incl. food serviceware)

Functional

Packaging - flexible

Automotive and transports

Textiles (incl. non-woven and fibres)

Electrical andelectronic (incl. casing)

Consumergoods

Agriculture andhorticulture

Building andconstruction

Others

52%

2013 2020

15% 14%

4%

16%

18%

18%

9% 40%

6%8%

16%

13%

11%

2%3%

1%

2%

2%2%

Figure 13: Worldwide shares of bio-based polymers production in different market segments in 2013 and 2020

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

18 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 19

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

9 Bio-based building blocks – Rainer Busch (18 pages, 27 tables and figures)

9.1 Introduction9.2 Selected monomers9.3 Perspectives

10 Asian markets for bio-based chemical building blocks and polymers – Wolfgang Baltus (36 pages, 33 tables and figures)

10.1 Introduction10.2 Asian markets for bio-based polymers10.3 Asia-Pacific region in numbers10.4 Feedstock – Key to success in Asia-

Pacific10.5 Policy development10.6 Market growth factors10.7 Selected biopolymer families –

limitations, challenges and chances in Asia-Pacific

10.8 Case Study: The National Bioplastics Roadmap in Thailand – Situation and outlook after 6 years in operation

11 Brand views and adoption of bio-based polymers – Harald Käb (26 pages, 19 tables and figures)

11.1 Introduction – Why read this?11.2 Summary11.3 Brand Strategies – Branch Aspects11.4 Individual Brand Strategies (selection,

alphabetic order) for packaging applications

11.5 Summary table

12 GreenPremium prices along the value chain of bio-based products – Michael Carus, Asta Eder and Janpeter Beckmann (16 pages, 6 tables and figures)

12.1 Initial questions12.2 Methodology12.3 Definition of “GreenPremium” prices12.4 GreenPremium prices do exist12.5 Results of the LinkedIn survey in the

bio-based community

12.6 GreenPremium price ranges – the full picture

12.7 Examples of GreenPremium Prices12.8 Main drivers for emotional and strategic

performance12.9 GreenPremium in the automotive sector12.10 Some actors fail to receive a

GreenPremium12.11 GreenPremium for Biofuels?12.12 Summary – GreenPremium prices along

the value-added chain from bio-based chemicals to products

12.13 References

Bio-based plastics and environment13 Environmental evaluation of bio-based

polymers and plastics – Roland Essel and Christin Liptow (20 pages, 14 tables and figures)

13.1 Introduction13.2 Results from recent life cycle

assessments13.3 Feedstock supply and use of by-

products13.4 Genetically modified organisms13.5 Biodiversity13.6 Land use13.7 Conclusion

14 Microplastic in the environment – sources, impacts and solutions – Roland Essel (8 pages, 4 tables and figures)

14.1 Introduction14.2 Defining microplastic14.3 Sources of microplastic14.4 Impacts of microplastics14.5 Can bio-based plastics be a solution?14.6 Conclusions14.7 References

Table of contents(474 pages and 202 tables and figures)

1 Executive summary (26 pages, 16 tables and figures)

1.1 Introduction1.2 Study background1.3 Methodology1.4 Main results1.5 Content of the full report1.6 Authors of the study1.7 Figures

Market data2 Market data

(28 pages, 44 tables and figures)2.1 Bio-based Building Blocks2.2 Bio-based Polymers

3 Qualitative analyses of selected bio-based polymers (12 pages, 6 tables and figures)

3.1 Cellulose Acetate (CA)3.2 Carbon dioxide as chemical feedstock:

Polymers and plastics from CO2 3.3 Thermosets

Trend reports

Policy on bio-based polymers4 Policies impacting bio-based plastics

market development – Dirk Carrez, Jim Philp and Lara Dammer (40 pages, 6 tables and figures)

4.1 Introduction4.2 Policy issues4.3 Bio-based plastics within a bioeconomy4.4 General bioeconomy strategies and

policies4.5 References

5 Plastic bags – their consumption and regulation in the European market and beyond – Constance Ißbrücker, Kristy-Barbara Lange and Hasso von Pogrell (12 pages, 3 tables and figures)

5.1 Introduction5.2 Common types of carrier bags5.3 The bio-based plastics alternative –

commercially available5.4 The bag market in Europe and beyond5.5 European regulation on lightweight

plastic bags – a complex negotiation process

5.6 Possible bag market developments in EU Member States

6 Bagislation in Europe – a (good?) case for biodegradables – Harald Käb (8 pages, 7 tables and figures)

7 Standards, norms and labels for bio-based products – Lara Dammer and Michael Carus (8 pages, 6 tables and figures)

7.1 Introduction7.2 Activities of CEN/TC 411 7.3 Bio-based labels in Europe7.4 Certification of the sustainability of wood

as a raw material – FSC and PEFC7.5 New certification systems for

sustainable biomass7.6 References

Bio-based building blocks and polymers market8 Bio-based polymers, a revolutionary

change – Jan Ravenstijn (70 pages, 11 tables and figures)

8.1 Introduction8.2 Market trends8.3 Technology trends8.4 Environmental trends8.5 Selected bio-based polymer families8.6 Customer views8.7 New business concepts8.8 New value chain8.9 Lessons learnt 8.10 Acknowledgements

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

20 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 21

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

15.79 Surakshit Parivar Biotech Pvt. Ltd.15.80 Synbra Technology B.V.15.81 Teijin Limited15.82 TerraVerdae BioWorks Inc.15.83 The Dow Chemical Company15.84 The Woodbridge Group15.85 ThyssenKrupp AG15.86 Tianan Biologic Material Co., Ltd.15.87 Tianjin GreenBio Materials Co., Ltd.15.88 TMO Renewables Limited15.89 ttz Bremerhaven15.90 Uhde Inventa-Fischer AG15.91 Veolia Water Technologies15.92 Verdezyne, Inc.15.93 Wuhan Sanjiang Space Gude Biotech

Co, Ltd.15.94 Yunan Fuji Bio-Material Technology Co.,

Ltd.15.95 Zhejiang Hangzhou Xinfu

Pharmaceutical Co., Ltd.15.96 Zhejiang Hisun Biomaterials Co., Ltd.

16 Company product index (9 pages)

17 List of acronyms (3 pages)

Authors of the study

Florence Aeschelmann (MSc) (Germany), materials engineer, is a staff scientist in the Technology & Markets department at nova Institute. Her main focus is on bio-

based materials, especially bio-based polymers. She is well acquainted with the global market for bio-based polymers and building blocks as she is one of the authors of the market study “Bio-based Building Blocks and Polymers in the World – Capacities, Production and Applications: Status Quo and Trends Towards 2020”. She is also in charge of the overall organization of the International Conference on Bio-based Materials.

Michael Carus (MSc) (Germany), physicist, founder and managing director of the nova-Institute, has worked in the field of Bio-based Economy for over 20 years. This

includes biomass feedstock, processes, bio-based chemistry, polymers, fibres and composites. His work deals with market analysis, techno-economic and ecological evaluation as well as the political and economic framework for bio-based processes and applications (“level playing field for industrial material use”). Carus is part of an extensive, worldwide network, which enabled nova-Institute to make use of leading experts in the field for its market study.

Wolfgang Baltus (PhD) (Thailand) worked for BASF for 15 years and was responsible for the business development of environmental friendly coatings in Asia. From 2008

until 2014, Baltus worked for the National Innovation Agency (NIA) in Bangkok. In October 2014, he started work as a consultant for the Precise Corporation, a group of Thai companies specialized in the field of electrical power distribution equipment, project and service for substations, renewable energy and supervisory systems. His main target is to assist Precise get

Company data15 Company profiles

(129 pages, 96 company profiles)15.1 AnoxKaldnes15.2 Anqing Hexing Chemical Co., Ltd.15.3 Arizona Chemical Company LLC15.4 Arkema SA15.5 Attero15.6 Avantium Technologies B.V.15.7 BASF SE15.8 Bayer MaterialScience15.9 Bio-on Srl15.10 BioAmber Inc.15.11 BioBased Technologies LLC15.12 BioMatera Inc.15.13 Bioplastech Ltd.15.14 BIOTEC Biologische Naturverpackungen

GmbH & Co. KG15.15 Braskem S.A.15.16 Cargill Inc.15.17 Cathay Industrial Biotech, Ltd.15.18 Cellulac15.19 Chengdu Dikang Biomedical Co., Ltd.15.20 China New Materials Holdings Ltd.15.21 Chongqing Bofei Biochemical Products

Co., Ltd.15.22 Corbion Purac15.23 DaniMer Scientific LLC15.24 DSM N.V.15.25 DuPont15.26 DuPont Tate & Lyle Bio Products

Company, LLC15.27 Evonik Industries AG15.28 Far Eastern New Century Corporation15.29 Futerro15.30 Galactic15.31 Genomatica, Inc.15.32 Global Bio-Chem Technology Group

Co., Ltd.15.33 Henan Jindan Lactic Acid Technology

Co., Ltd.15.34 Hubei Guangshui National Chemical

Co., Ltd.15.35 Hunan Anhua Lactic Acid Company15.36 India Glycols Limited15.37 Indorama Ventures Public Company

Limited

15.38 Jiangsu Clean Environmental Technology Co., Ltd.

15.39 Jinhui Zhaolong High Technology Co., Ltd.

15.40 Kaneka Corporation15.41 Kingfa Sci. & Tech. Co., Ltd.15.42 KNN Bioplastic15.43 LANXESS AG15.44 Limagrain Holding S.A.15.45 Lukang Pharmaceutical Co., Ltd.15.46 Mango Materials15.47 Meredian Holdings Group15.48 Merquinsa S.A.15.49 Metabolix Inc.15.50 Mitsubishi Chemical Corporation (MCC)15.51 Musashino Chemical Laboratory, Ltd.15.52 Myriant Corporation15.53 Nafigate Corporation15.54 Nantong Jiuding Biological Engineering

Co., Ltd.15.55 NatureWorks LLC15.56 Newlight Technologies LLC15.57 Novamont S.p.A.15.58 Novomer Inc.15.59 Paques15.60 PHB Industrial S.A.15.61 Plaxica Ltd.15.62 PolyFerm Canada Inc.15.63 PTT MCC Biochem Co., Ltd.15.64 Rennovia Inc.15.65 Reverdia15.66 Rodenburg Biopolymers B.V.15.67 Roquette15.68 Samsung Fine Chemicals Co., Ltd.15.69 Shandong Fuwin New Material Co., Ltd.15.70 Shanghai Tong-Jie-Liang Biomaterials

Co., Ltd.15.71 Shantou Liangyi15.72 Shenzhen Bright China Biotechnological

Co., Ltd.15.73 Shenzhen Ecomann Biotechnology Co.,

Ltd15.74 Showa Denko K.K.15.75 Solvay SA15.76 Succinity GmbH15.77 Sulzer Chemtech AG15.78 SUPLA Material Technology Co., Ltd

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

22 © 2015 nova-Institut GmbH, Version 2015-05 © 2015 nova-Institut GmbH, Version 2015-05 23

www.bio-based.eu/markets Bio-based Building Blocks and Polymers in the World

Kristy-Barbara Lange (Germany) is Deputy Managing Director at European Bioplastics and heads the communications division of the association. Since 2010 she has

been responsible for all of the association’s communications, internally and externally, including media relations and corporate publishing. Since she joined managing team in early 2015, her further focus areas now include EU policy and membership development. She holds a Master of Political Sciences from Heidelberg University, Germany. Before joining European Bioplastics, Kristy worked in international PR-agencies for several years, with a focus on the infrastructure and (renewable) energy industry sectors.

Jim Philp (PhD) (France) is a microbiologist who has been a policy analyst at the Organisation for Economic Cooperation and Development (OECD) in Paris

since 2011, where he specializes in industrial biotechnology, synthetic biology and biomass sustainability. He has been an academic for about sixteen years, researching environmental and industrial biotechnology: bioremediation, biosensors, wastewater science and engineering. He was involved in various UK government initiatives in biotechnology, such as Biotechnology Means Business, and BioWise. He was coordinator of the LINK Bioremediation Programme, at the academic-industrial interface, for about six years. He spent a total of eight and a half years working as an oil biotechnologist for Saudi Aramco in Saudi Arabia, investigating field problems related to chemistry and microbiology, and developing biotechnology solutions for improved oil recovery and exploitation. He has authored over 300 articles. In 2015 he was inducted into Who’s Who.

Jan Ravenstijn (MSc) (The Netherlands) has more than 35 years of experience in the chemical industry with Dow Chemical and DSM, including 15 years in executive

global R&D positions in engineering plastics, thermosets and elastomers. He is currently a visiting professor and consultant to CEOs of biopolymer companies and has published several papers and articles on the market development of bio-based polymers. Jan Ravenstijn is regarded as one of the world’s leading experts in his field.

Hasso von Pogrell (Germany) has been Managing Director of European Bioplastics since March 2009. Upon completion of his education in Germany and a two-year term of

military services, he studied Economics at the University of Cologne, where he graduated in 1994.He began his political career as a lobbyist in 1995, when he joined the Germany Industry Association for Optical, Medical and Mechatronical Technologies. There he was responsible for public relations and economics. After a two-year stint as General Manager at the Federal Association of the German Medium and Large Retail Enterprises, he returned to the industry sector. As Head of Department for Foreign Affairs at the Association of the German Construction Industry and Assistant Director of the European International Contractors (EIC), he served the construction industry for seven years from 2000 to 2007. He directed the affairs of the Association of the German Sawmill Association as its Managing Director between 2007 and 2009.

a foothold in the biorefinery business, introducing smart community concepts in Thailand.He is regarded as one of the leading experts on bio-based polymer markets and policy in Asia.

Howard Blum (BSChem, MBA) (Philadelphia-USA) is a B2B chemical industry professional with more than 30 years experience working in the chemical and polymer field.

Previously with Conoco Oil, Chem Systems and Kline, he now runs his own firm Chemicals & Plastics Advisory, focusing on biopolymers and biorenewable solutions. The firm’s mission is to provide business development services for quickly identifying new markets, technologies and opportunities, with ‘real-time’ implementation to speed up the marketing and sales process and minimize revenue-limiting activities.His clients include multi-national companies that require assistance in market and technology analysis, new business development and project management. In addition to the chemical and plastics industry, he has assisted clients from the oil & gas, catalysts, packaging, automotive and healthcare-pharma industry sectors.

Rainer Busch (Dr.rer.nat.) (Germany) is a chemist with 24 years of experience in the chemical industry. He worked in various positions in R&D with Dow Chemical, mainly in technology

scouting and intellectual asset management. After his industrial career, he founded a consulting firm and focused on the chemical aspects of the industrial material use of biomass. He is currently scientific advisor to the leading edge cluster BioEconomy in central Germany and also visiting professor at the paper centre Gernsbach near Karlsruhe (Germany). Rainer has published and co-authored several papers and articles on the use of renewable resources in the chemical industry.

Dirk Carrez (PhD) (Belgium) is one of the leading policy consultants on a Bio-based Economy in Brussels. He was Director Industrial Biotechnology at EuropaBio, the European

Association for Bioindustries, until 2011. He is now Managing Director of Clever Consult, Brussels. In 2013 he became the Executive Director of the new industrial association BIC (Bio-based Industries Consortium), which is the private partner in the Biobased Industries Initiative (BBI JU), a new PPP between the EU Commission and more than 70 bio-based economy companies.

Constance Ißbrücker (Germany) has been working as Environmental Affairs Manager for European Bioplastics since February 2013. She is responsible for issues related to the

compostability, sustainability, and standardization of bioplastics. Constance Ißbrücker holds a degree in chemistry from the University of Jena in Germany with a specialization in Bioorganic and Macromolecular Chemistry. Before joining the association she worked in different research groups at universities in Berlin and Jena. Her research background is in polysaccharide chemistry, in particular cellulose dissolution, modification and analytics.

Harald Käb (PhD) (Germany) is a chemist and has an unblemished 20-year “bio-based chemistry and plastics” track record. From 1999 to 2009 he chaired the board

and developed “European Bioplastics”, the association that represents the bioplastics industry in Europe. Since 1998 he has been working as an independent consultant, helping green pioneers and international brands to develop and implement smart business, media and policy strategies for bio-based chemicals and plastics.

Bio-based Building Blocks and Polymers in the World www.bio-based.eu/markets

24 © 2015 nova-Institut GmbH, Version 2015-05

nova-Institute

The nova-Institut GmbH was founded as a private and independent institute in 1994. It is located in the Chemical Park Knapsack in Huerth, which lies at the heart of the chemical industry around Cologne (Germany).For the last two decades, nova-Institute has been globally active in feedstock supply, techno-economic and environmental evaluation, market research, dissemination, project management and policy for a sustainable bio-based economy.

Key questions regarding nova activitiesWhat are the most promising concepts and applications for Industrial biotechnology, biorefineries and bio-based products? What are the challenges for a post petroleum age – the Third Industrial Revolution?

Order the full report

The full report can be ordered for 3,000 € plus VAT at www.bio-based.eu/markets

nova-Institut GmbH

Chemiepark KnapsackIndustriestraße 30050354 Hürth, Germany

T +49 (0) 22 33 / 48 14-40F +49 (0) 22 33 / 48 14-50

Bio-based EconomyBio-based Chemicals & Materials •

Biorefi neries • Industrial BiotechnologyCarbon Capture & Utilization

Sustainability

Technology & Markets

EnvironmentalEvaluation

Life Cycle Assessments (LCA)Life Cycle InventoriesMeta-Analyses of LCAs

Raw Material SupplyAvailability & Prices

Sustainability

Market ResearchVolumes & Trends

Competition AnalysisFeasibility and

Potential Studies

Techno-Economic Evaluation (TEE)

Process EconomicsTarget Costing Analysis

Dissemination & Marketing SupportB2B communication

Conferences & WorkshopsMarketing Strategies

Political Framework & Strategy

System AnalysisStrategic Consulting