bilal zia (world bank) shawn cole (hbs). impact evaluation in indonesia-results impact evaluation...

TRANSCRIPT

Bilal Zia (World Bank)Shawn Cole (HBS)

Impact Evaluation in Indonesia-Results Impact Evaluation in India - Ongoing Impact Evaluation in South Africa-Plans

Shawn Cole (Harvard University)Thomas Sampson (Harvard University)

Bilal Zia (World Bank)

Financial literacy is now a prominent feature of financial reform across the globe:

◦US: President’s Advisory Council on Financial Literacy

◦ Indonesia: 2008 was “Year of Financial Education”

◦ India: RBC has established Financial Literacy and Credit Counseling Centers

International and Private organizations are also pushing heavily for financial literacy programs:

◦ World Bank: $15 Million Russia Financial Literacy Program

◦ Citi Foundation: 4 years into a 10-year $200 Million global program on financial education, operating in 65 countries

Compelling survey evidence from developed countries shows strong positive correlation. HHs with low financial education:

◦ Tend not to plan for retirement (Lusardi and Mitchell, 2007a)

◦ Borrow at higher interest rates (Lusardi and Tufano, 2008; Stango and Zinman, 2006)

◦ Acquire fewer assets (Lusardi and Mitchell, 2007b)

◦ Participate less in the formal financial system (Alessie, Lusardi and van Rooij, 2007; Hogarth and O.Donnell, 1999).

But is this relationship causal?

But is this relationship causal?

Our paper addresses this question with a randomized evaluation

Piggy-backed experiment on a nationally representative household survey in Indonesia.

Unbanked households are our starting sample

Provided financial literacy training in groups at village level

Also provided financial incentives (to open bank accounts) (range $3-$14).

Demand for financial services is low because: ◦ Consumers rationally decide that value of

financial services is less than costOr◦ Services are not well understood

We find effect of financial literacy training only in subsets of sample.

We find significant effects of financial literacy training on uneducated population and those who possess low ex-ante financial literacy.

We do find a very strong and significant effect of financial incentives in the full sample.

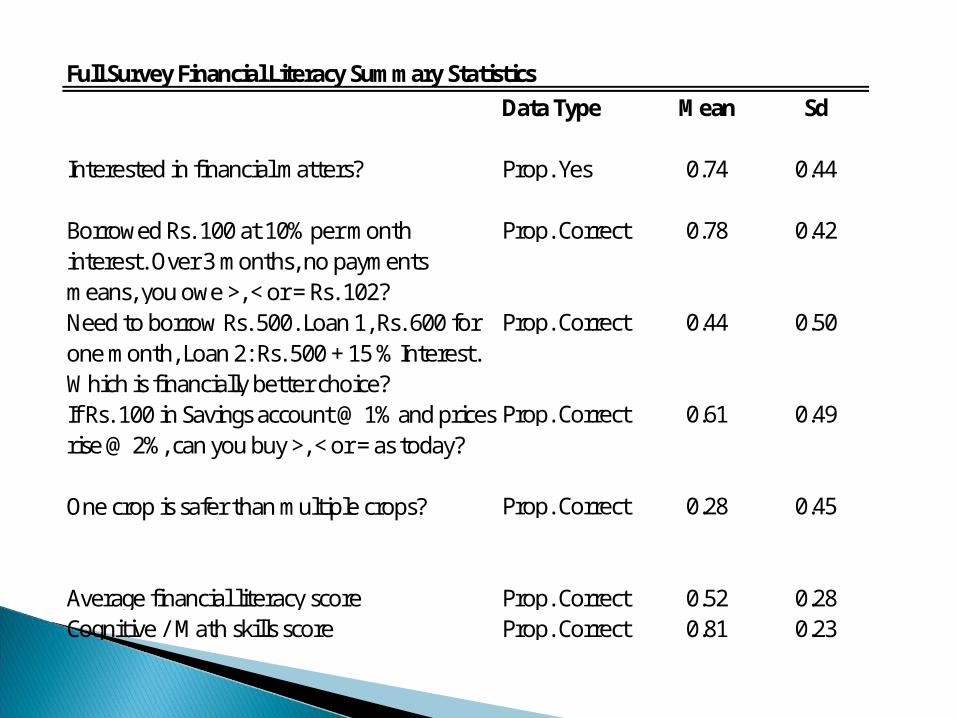

Full Survey Financial Literacy Summary StatisticsData Type Mean Sd

Interested in financial matters? Prop. Yes 0.74 0.44

Prop. Correct 0.78 0.42

Prop. Correct 0.44 0.50

Prop. Correct 0.61 0.49

Prop. Correct 0.28 0.45

Average financial literacy score Prop. Correct 0.52 0.28Cognitive / Math skills score Prop. Correct 0.81 0.23

Borrowed Rs. 100 at 10% per month interest. Over 3 months, no payments means, you owe >, < or = Rs. 102?Need to borrow Rs. 500. Loan 1, Rs. 600 for one month, Loan 2: Rs. 500 + 15 % Interest. Which is financially better choice?If Rs. 100 in Savings account @ 1% and prices rise @ 2%, can you buy >, < or = as today?

One crop is safer than multiple crops?

1 2 3 4

Dependent Var: Opened Bank Account?Financial Literacy Invite? -0.020 -0.022

[0.027] [0.028]Incentive==75000 0.054 0.048

[0.024]** [0.026]*Incentive==125000 0.092 0.088

[0.026]*** [0.029]***

Constant 0.097 -0.444 0.035 -0.447[0.020]*** [0.319] [0.014]** [0.327]

Household Controls YES YES

Experimental Results: The Effect of Financial Literacy Education and Incentives on Opening of Bank Accounts

Financial literacy training has no effect on the likelihood of opening a bank account

Financial incentives have a very large effect: ◦ Compared to the baseline of $3, a $14 incentive

increase probability of opening a bank account from 3.5% to 12.7% -- an almost three-fold increase

4 5 6

Dependent Var: Opened Bank Account?

Financial Literacy Invite? -0.049 -0.048 -0.051[0.034] [0.036] [0.035]

Incentive==75000 0.060 0.051 0.036[0.039] [0.040] [0.040]

Incentive==125000 0.100 0.098 0.100[0.030]*** [0.034]*** [0.033]***

Below Median Financial Literacy * Financial Literacy Invite 0.100 0.087 0.092[0.044]** [0.043]** [0.043]**

Below Median Financial Literacy * Incentive==75000 -0.016 -0.008 0.008[0.060] [0.058] [0.057]

Below Median Financial Literacy * Incentive==125000 -0.024 -0.031 -0.035[0.049] [0.055] [0.054]

Constant 0.067 -0.377 -0.409[0.027]** [0.331] [0.307]

Household Controls YES YES

Enumerator Fixed Effects YES

Experimental Results: Heterogeneous Effects of Financial Literacy Education and Incentives on Opening of Bank

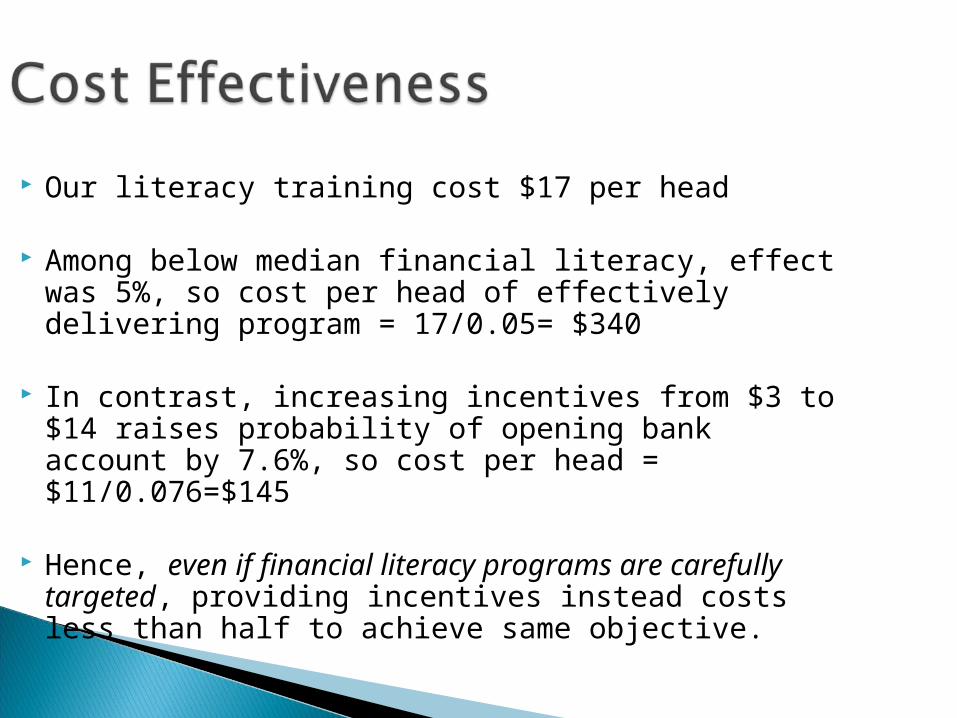

These results suggest financial literacy programs should be carefully targeted

However…

Our literacy training cost $17 per head

Among below median financial literacy, effect was 5%, so cost per head of effectively delivering program = 17/0.05= $340

In contrast, increasing incentives from $3 to $14 raises probability of opening bank account by 7.6%, so cost per head = $11/0.076=$145

Hence, even if financial literacy programs are carefully targeted, providing incentives instead costs less than half to achieve same objective.

Financial education may have extra benefits that households may reap in the future (such as better internal savings, saving more informally, etc.)

We do not measure these benefits – to do in future follow-up survey

This paper focuses on extensive margin

Shawn Cole (Harvard University, J-PAL, IPA)Jeremy Shapiro (Yale University, IPA)

Bilal Zia(WB)

Video-Based Financial Literacy: ◦ Detailed, engaging modules on savings, credit, insurance and budgeting◦ Local actors and good production firm hired for these videos (though not

Bollywood!)◦ Lab setup for screenings◦ Low-cost, scalable intervention

Financial Counseling◦ Unbiased consultation to discuss household budgeting, borrowing and savings

options

Outcomes◦ Measured financial literacy◦ Real-world type savings and investment questions with financial

consequences◦ Follow-up household survey

Further Test Some Behavioral Theories:◦ Do people respond (financially) to deadlines?◦ Do people (investors) respond to de-biasing ?

Shawn Cole (Harvard University, J-PAL, IPA)Jeremy Shapiro (Yale University, IPA)Kartini Shastry (Wellsley College, IPA)

Workers in mining houses in South African exhibit low levels of financial literacy◦ May make poor savings and expenditure

decisions◦ Financial stresses may hinder work performance◦ Financial habits may contribute to absenteeism

Avoid coming to work on payday, to avoid moneylender

May “celebrate” the evening after payday, and miss work in subsequent days

Provide customized, two-day, experiential financial education module emphasizing:◦ Financial planning◦ Savings choices◦ Lending choices◦ Insurance◦ Hire Purchase◦ Legal rights◦ Remittances

Financial Education Foundation◦ Funding and technical support

Goldfields and AngloGold Ashanti◦ Two of world’s largest mining firms

TEBA Bank◦ Cooperative bank serving mine workers

Innovations for Poverty Action◦ Technical support and research direction

Ikhumiseng Consulting ◦ Provide financial literacy education

Treatment assigned at individual level Sample size

◦ 10,000 workers in treatment◦ 10,000 in control

Administrative Data◦ Financial data (Teba)◦ Productivity and absenteeism (Mining Houses)

Survey data◦ 1,500 household surveys

Baseline Endline (one year later)

Knowledge / awareness of financial tools Numeracy and budgeting skills More savings accounts, more savings Decreased use of moneylenders Reduced absenteeism Improved debt management

Baseline surveying:◦ Starting January 2010◦ 30 individuals / week for one year

Financial intervention◦ 200 individuals / week for one year

Administrative data collection:◦ Periodically throughout study, and beyond

Endline surveying:◦ Beginning January 2011

Study completion:◦ December 2011

Non-profit/private partnership◦ Mining houses contributing 20,000 person-days of

labor◦ FEF funding training costs of 10,000 workers

If success demonstrated, mining houses may scale up to all workers

Individual-level randomization and large sample size allow detection of ‘small’ effects

Range of experiments designed to understand importance of financial literacy◦ India, Indonesia, South Africa◦ Videos, Classroom, Community-Based

Taken together, along with a dozen other experiments conducted by colleagues around the world, will soon learn:◦ What works, what doesn’t◦ How financial literacy education works?◦ What is most cost-effective◦ Lead to: educational reforms, regulatory reform,

new private markets