bhutan power corporation limited tariff review · pdf fileapril 2013. the bpc submitted that...

TRANSCRIPT

Bhutan Electricity Authority

Bhutan Power Corporation Limited Tariff Review Report

October 2013

i

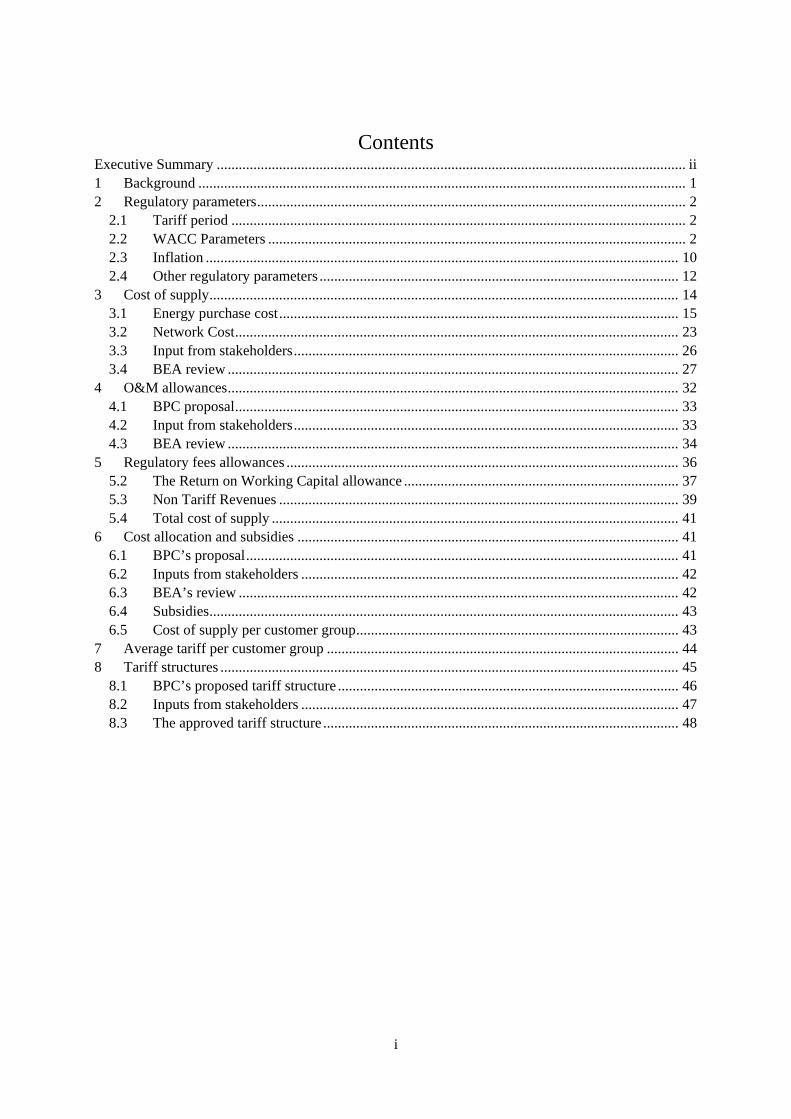

Contents

Executive Summary ................................................................................................................................ ii 1 Background ..................................................................................................................................... 1 2 Regulatory parameters ..................................................................................................................... 2

2.1 Tariff period ............................................................................................................................ 2 2.2 WACC Parameters .................................................................................................................. 2 2.3 Inflation ................................................................................................................................. 10 2.4 Other regulatory parameters .................................................................................................. 12

3 Cost of supply ................................................................................................................................ 14 3.1 Energy purchase cost ............................................................................................................. 15 3.2 Network Cost ......................................................................................................................... 23 3.3 Input from stakeholders ......................................................................................................... 26 3.4 BEA review ........................................................................................................................... 27

4 O&M allowances ........................................................................................................................... 32 4.1 BPC proposal ......................................................................................................................... 33 4.2 Input from stakeholders ......................................................................................................... 33 4.3 BEA review ........................................................................................................................... 34

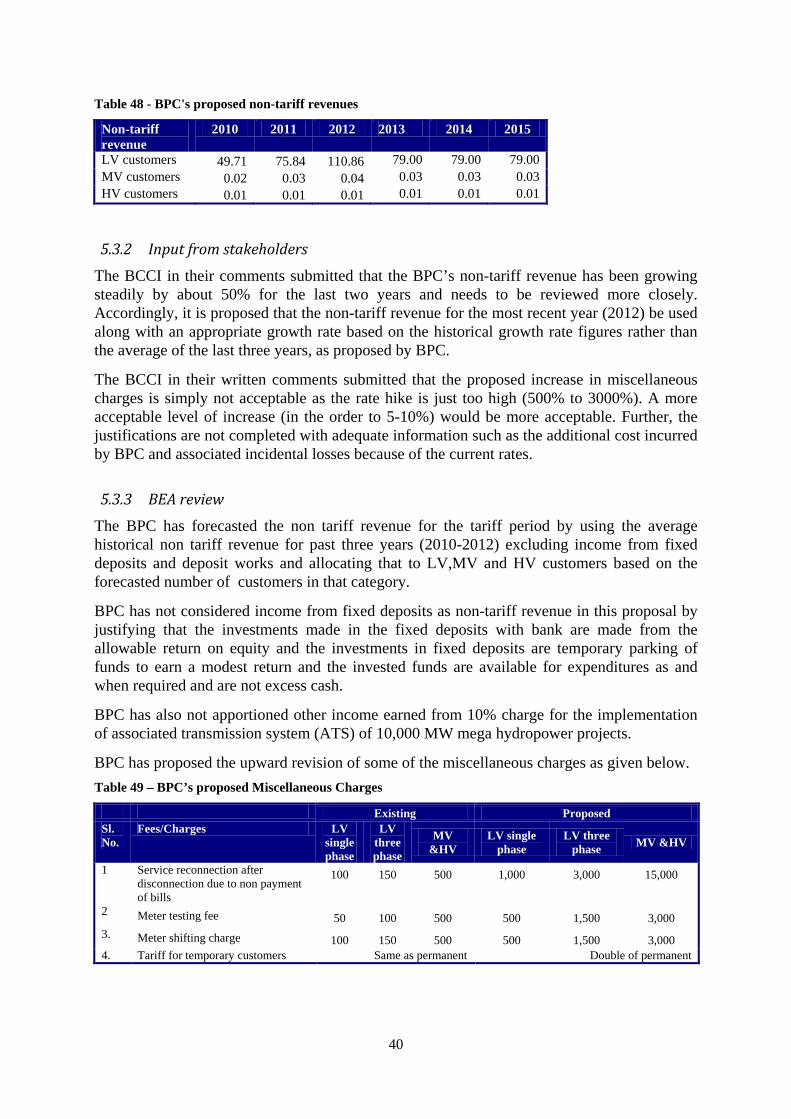

5 Regulatory fees allowances ........................................................................................................... 36 5.2 The Return on Working Capital allowance ........................................................................... 37 5.3 Non Tariff Revenues ............................................................................................................. 39 5.4 Total cost of supply ............................................................................................................... 41

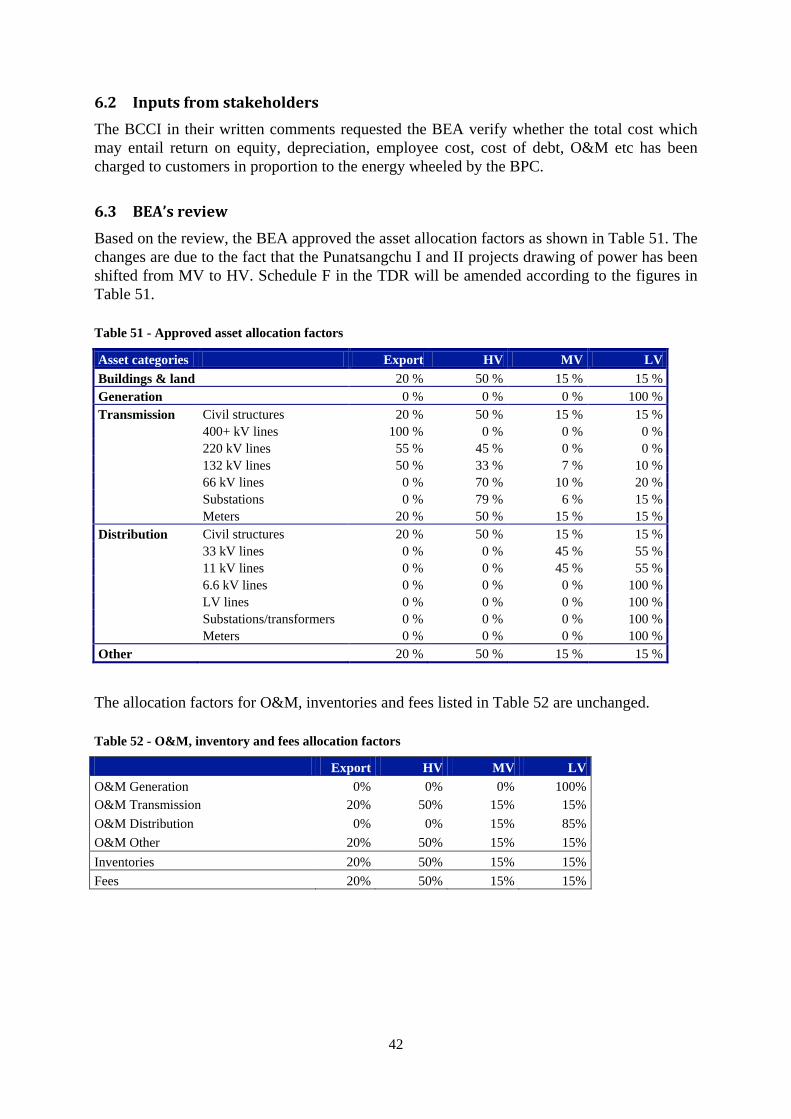

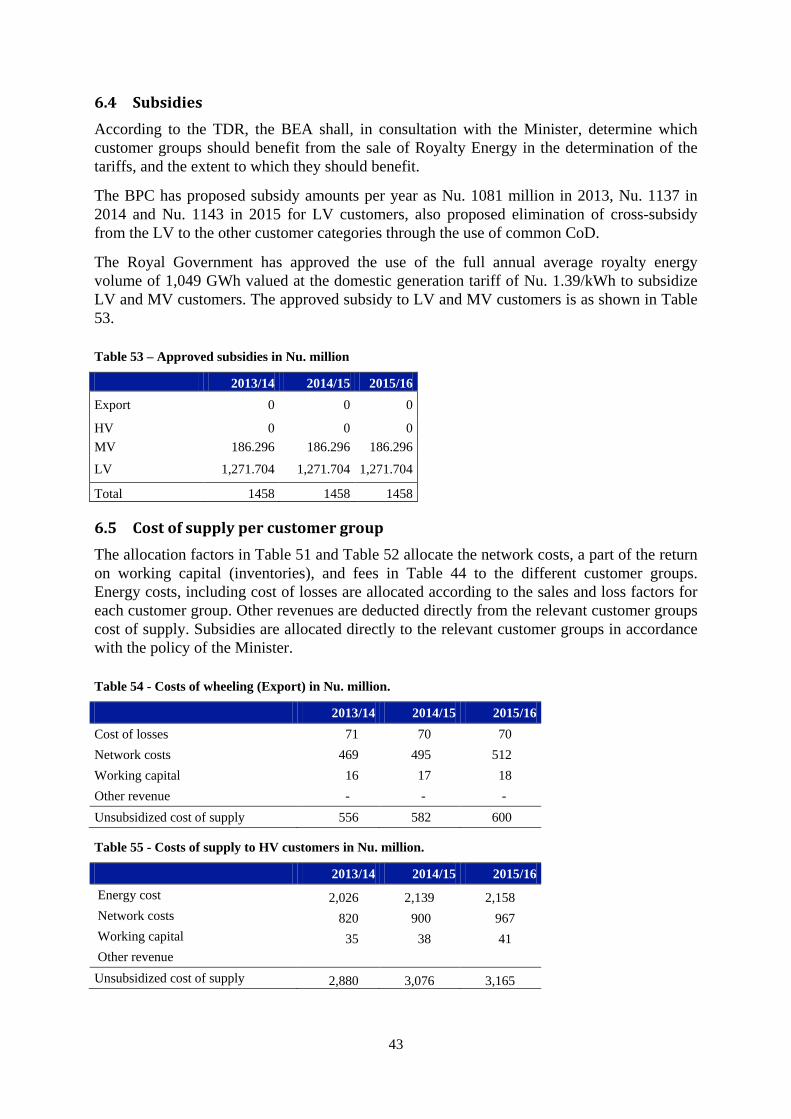

6 Cost allocation and subsidies ........................................................................................................ 41 6.1 BPC’s proposal ...................................................................................................................... 41 6.2 Inputs from stakeholders ....................................................................................................... 42 6.3 BEA’s review ........................................................................................................................ 42 6.4 Subsidies ................................................................................................................................ 43 6.5 Cost of supply per customer group ........................................................................................ 43

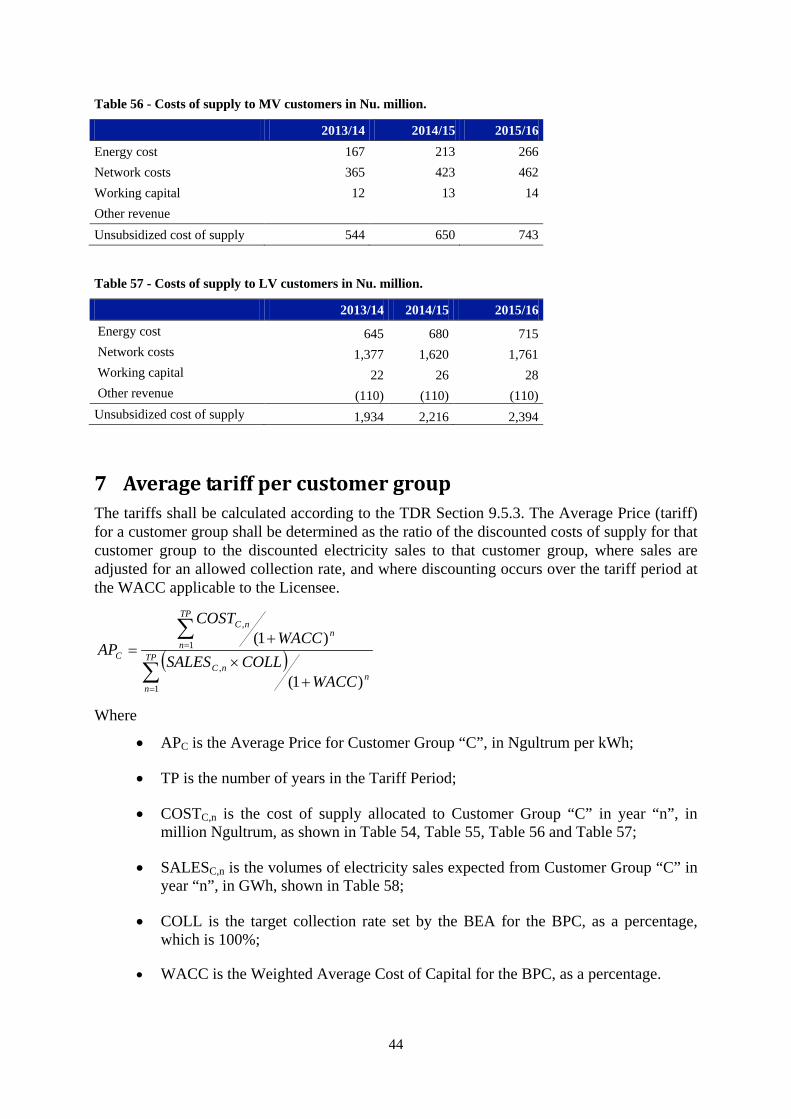

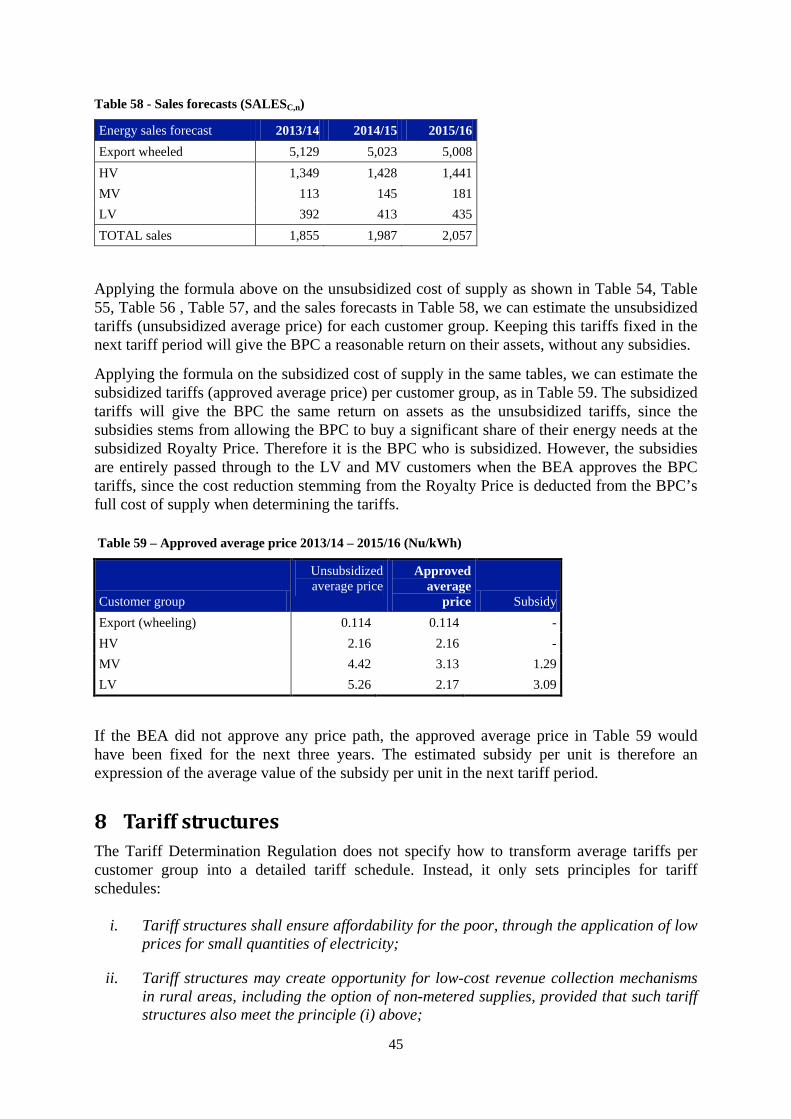

7 Average tariff per customer group ................................................................................................ 44 8 Tariff structures ............................................................................................................................. 45

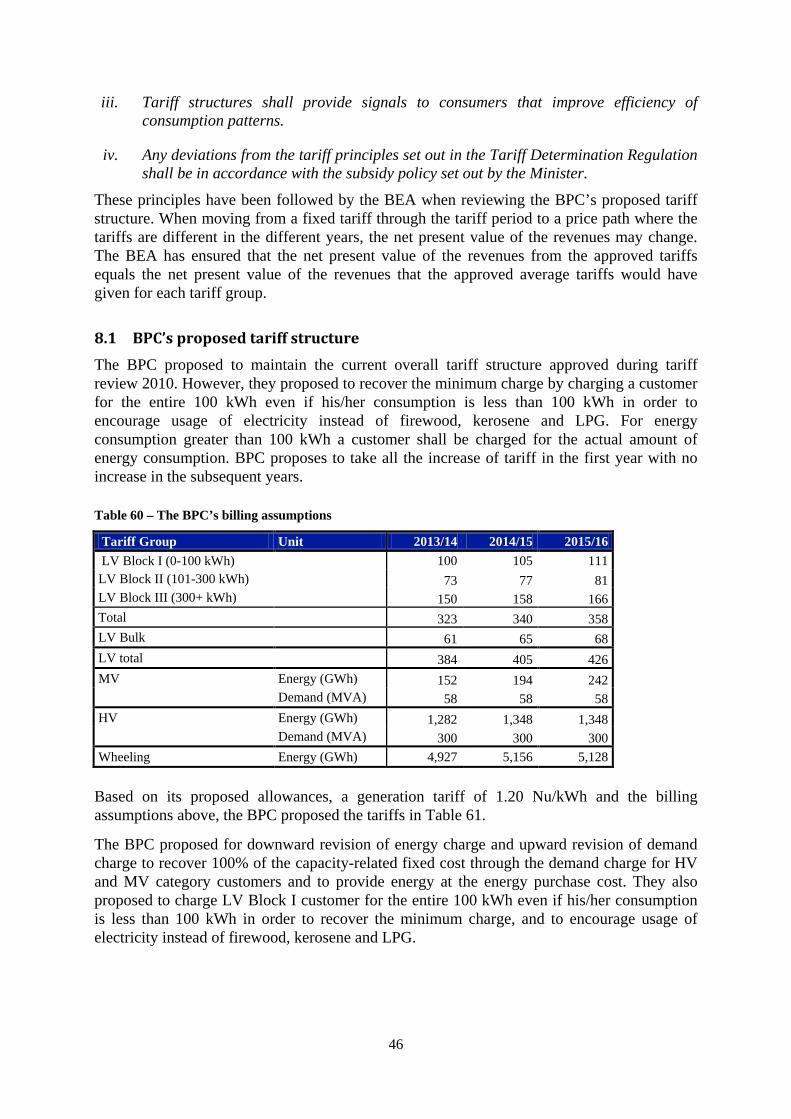

8.1 BPC’s proposed tariff structure ............................................................................................. 46 8.2 Inputs from stakeholders ....................................................................................................... 47 8.3 The approved tariff structure ................................................................................................. 48

ii

Executive Summary The Druk Green Power Corporation Limited (DGPC) generation tariff has been reviewed and set at Nu. 1.39/kWh. The annual average royalty energy volume of 1,049 GWh, which is 15% of the expected generation from Kurichhu, Basochhu, Tala and Chukha hydropower plants adjusted for auxiliary consumption has been approved by the Royal Government of Bhutan. The Bhutan Power Corporation Limited (BPC) tariff application has been reviewed and the allowed pre-tax Weighted Average Cost of Capital (WACC) is determined as 9.40 %, based on a 10 % after-tax cost of equity, a 2.06 % cost of debt, and a 40 % gearing ratio. The cost allowances have been set according to the provisions of the Tariff Determination Regulation. The BPC’s total costs of supply increase steadily over the tariff period, largely driven by new investments in transmission system. The BEA has determined an average cost of supply of Nu. 0.114/kWh for Wheeling, Nu. 2.16/kWh High Voltage (HV), Nu. 4.42/kWh for Medium Voltage (MV) and Nu. 5.26/kWh for Low Voltage (LV) consumers for the tariff period 2013/14 to 2015/16. The Royal Government approved the use of full annual average royalty energy volume of 1,049 GWh valued at the domestic generation tariff of Nu. 1.39/kWh and allocated an annual subsidy amount of Nu.1,271.704 million to LV consumers and an annual subsidy of Nu. 186.296 million to MV customers for the period 2013/14 to 2015/16. The HV customers will not be subsidized and will be paying the full cost of supply as per the Economic Development Policy 2010. Based on the approved subsidies and the annual average royalty energy volume, the BEA has approved the following tariff structure for the tariff period 1st October 2013 to 30th June 2016.

Customer Category Unit 2013/2014 2014/2015 2015/2016

Low Voltage (LV) LV Block I (Rural domestic) 0 – 100 kWh Nu./kWh 0 0 0

LV Block I (Others) 0-100 kWh Nu./kWh 0.98 1.12 1.28

LV Block II (All) >100-300 kWh Nu./kWh 1.86 2.13 2.45

LV Block III (All) >300 kWh Nu./kWh 2.46 2.82 3.23

LV bulk Nu./kWh 2.56 3.07 3.68 Medium Voltage (MV) Energy charge Nu./kWh 1.98 2.19 2.43 Demand charge Nu./kW/m 155 195 235 High Voltage (HV) Energy charge Nu./kWh 1.67 1.81 1.96 Demand charge Nu./kW/m 130 155 180

With the approved subsidies, the royalty energy price has been determined to be zero as per Section 8.2.3 of the Tariff Determination Regulation.

1

1 Background The Bhutan Power Corporation Limited (BPC) submitted their proposal for revision of domestic electricity tariffs vide letter no. 31/BPC/BEA/MD/2013/74 dated 5th April 2013.

The BPC submitted that an increase in the domestic electricity tariffs has become necessary due to substantial capital investments for establishing a reliable backbone transmission network and distribution infrastructure for:

• Ensuring availability and reliability of power supply to both the urban and rural areas.

• Extending and upgrading the existing transmission and distribution networks in both urban and rural areas.

• Expecting to incur increasing operational and maintenance expenditures considering the ageing infrastructure.

The BPC stated that an increase in the tariffs are necessary to ensure an adequate base for supporting their planned activities, which are in line with BPC’s 5-year investment plan (2013-2017), which in turn is in line with the RGoB’s 11th FYP for the energy sector in the country. In addition, BPC is expected to incur increasing operation and maintenance expenditures considering the significant expansion of rural distribution networks and the aging infrastructure base to ensure the desired level of quality and reliability of electricity supply to the customers.

The BPC also submitted some material changes in the forthcoming tariff period with an objective to reflect the true cost of electricity, encourage consumption of electricity by the rural customers to reduce dependence on other forms of energy and to reflect the operational constraints imposed on BPC:

• Downward revision of energy charge and upward revision of demand charge to reflect the true costs of generation, transmission, distribution, and supply of electricity, especially to the HV and the MV customers.

• Recover the minimum charge from LV life-line block (0-100 kWh), a customer shall be charged for the entire 100 kWh even if his/her consumption is less than 100 kWh in a month to encourage consumption of electricity by the rural customers thereby reducing dependence on other forms of energy, such as firewood, kerosene, and LPG.

• A separate Cost of Debt (CoD) for each customer category based on the nature of the loan, asset allocation and utilization factors to eliminate the cross-subsidies from the LV to other customer categories.

• Increase miscellaneous charges for some of the miscellaneous services to reflect the operational constraints imposed on BPC by the demand for such services.

As per the Tariff Determination Regulation, the BPC was required to submit their tariff proposals by 1st March 2010; however, the BPC has delayed their submission of their tariff proposal due to non finalization of the tariff proposals. The BPC tariff proposal was received on 5th April 2013.

2

As part of the tariff determination process, a public hearing was conducted on 18th July 2013 at the NRDCL Conference Hall, Thimphu. The BEA had initially planned to conduct the public hearing in May 2013, however the conduct of the public hearing was delayed due to the Election Commission of Bhutan’s directives to defer the public hearing to after the elections. Any written comments from the public were to be sent to the BEA Secretariat before 4 pm on 29th July 2013.

2 Regulatory parameters

2.1 Tariff period The length of the tariff period is not regulated in the Tariff Determination Regulation and is therefore to be determined as part of the tariff review.

The BPC tariff proposal is for a three year tariff period. The 2012 financial statements have been used as a reference for calculations of the proposed allowances.

The BEA’s view is that a three year tariff period is reasonable considering the prevailing uncertainties in the development of the electricity sector in the next few years. The tariff period is the same as proposed by the Druk Green Power Corporation (DGPC), which is necessary to avoid a new review of BPC’s tariffs in the middle of a tariff period. Therefore, the BEA recommends the proposed three year tariff period, starting from July 2013 and lasting until the end of June 2016. The new tariffs shall be valid from 1st October 2013 and to 30th June 2016.

2.2 WACC Parameters The WACC shall be calculated as the before-tax Weighted Average Cost of Capital in accordance with section 6.6.3 in the TDR:

GearingCoDTaxGearingCoEWACC ×+

−−×

=)1(

)1(

Where,

• WACC is the weighted average cost of capital, as a percentage;

• CoE is the cost of equity, as a percentage; as determined by the Authority for the Licensee;

• Gearing is the standard ratio of debt to total fixed assets, as determined by the BEA;

• CoD is the cost of debt, as a percentage, being the weighted average interest rate of the Licensee’s loans;

• Tax is the prevailing rate of company taxation, as a percentage.

3

2.2.1 BPC proposal

The BPC has proposed an individual WACC for each customer category. In the proposal, BPC proposes a post-tax CoE of 16% and a gearing ratio of 44%, which is BPC’s actual gearing ratio as on 31st December 2012. The WACC parameters for export, HV, MV and LV customers are proposed as below:

Table 1 BPC Proposed WACC

Export HV MV LV Cost of Equity 16% 16% 16% 16%

Cost of Debt 9.43% 10.73% 1.38% 1.27%

Gearing 44% 44% 44% 44%

Tax 30% 30% 30% 30%

WACC 16.9% 17.5% 13.41% 13.36%

The BPC has proposed an individual Cost of Debt for each customer category. The CoDs are based on actual cost of assets allocated and used by each of the customer categories. BPC is of the view that a common CoD for all customer categories implies cross-subsidies between them, and the purpose of the proposal is to remove such cross-subsidies.

2.2.2 Inputs from stakeholders

The CEO of Druk Holding and Investment (DHI) expressed that a CoE of 10% is quite low compared to commercial debt in Bhutan during the public hearing and with such a low CoE, there is no incentive to invest in BPC. Therefore, he asked the BEA consider a CoE higher than 10%.

The BCCI in their written comments submitted while determining the CoE, it is not appropriate to equate the power scenario in Bhutan to that of India as the conditions prevailing in these countries are different. Firstly, India is currently experiencing a huge shortage in firm as well as peak power requirement and it is imperative to attract players in this sector so as to overcome the shortage. Secondly, a relatively high CoE would be admissible for private sector investments as the risks associated with transmission and distribution (T&D) of power is relatively high. However, in Bhutan’s case, allowing a high CoE for a state run monopoly with no associated risks is not warranted. Further, it was also submitted that a CoE of 10% is used and approved by the BEA during the last tariff period. Accordingly, it was recommended that the allowable CoE for BPC be reviewed and lowered to a more reasonable and acceptable figure.

The BPC in their written comments submitted that an increase in CoE from 10% to 16%, India is for ensuring reasonable returns to the shareholder in light of other competitive investment opportunities in the country where the return on investments are much higher than 16% for projects of comparable risks and social obligations. Accordingly, BPC proposed cost of equity of 16% for the next tariff period.

4

The BPC in their written comments submitted that the proposal to segregate the CoD as per customer category and elimination of cross subsidies from the LV to other customer categories are in line with Section 7.6 and Section 7.7 of the TDR. The BPC also stated that its weighted average CoD is much lower than the market CoD because of the inclusion of soft Rural Electrification loans under the grace period with 0% interest rate which are targeted for LV customers. Therefore, BPC stated that the inclusion of the RE loans in the calculation of CoD for the wheeling and HV customers will not be fair since they do not at all use the RE distribution assets. Accordingly, BPC proposed for separate CoD for each customer category based on the nature and usage of the outstanding and expected debt by each customer category.

2.2.3 BEA review

The WACC parameters are determined in the Tariff Determination Regulation Schedule C, but may be updated by the BEA from time to time. The parameters are discussed in the subsections below.

2.2.3.1 Tax The BEA has verified that the proposed tax rate is in accordance with the rate prescribed in the Income Tax Act of the Kingdom of Bhutan 2001 Chapter 9, section 45. The BEA has found no reasons to amend the proposed tax rate.

2.2.3.2 Cost of Debt The BPC has estimated a consolidated CoD of 2.76% based on the loan details in Table 2. The loan balances of 31.12.2012 have been used as the starting point to derive the loan balances at the end of each consecutive year.

Table 2 BPC’s calculation of average Cost of Debt – Loan Balance (Nu. mill) and interest rate

Particulars of Loan Interest

Rate 31.12.2012 31.12.2013 31.12.2014 31.12.2015

RE I 6 % 190.99 182.69 174.39 166.08

RE II 6 % 348.19 329.87 311.54 293.21

RE III 6 % 419.25 401.02 382.79 364.57

THP 9 % 659.83 549.86 439.89 329.92

RE JICA I 0 % 1,374.37 1,374.37 1,374.37 1,374.37

RE IV ADB 0 % 1,029.18 1,029.18 1,029.18 1,029.18

RE JICA II 0 % 575.27 979.81 979.81 979.81

RE V ADB 0 % 343.53 726.22 726.22 726.22

NPPF 9 % 503.13 461.20 419.28 377.35

ADA LOAN 0 % 40.73 255.32 277.94 277.94 Future Loan Transmission Programme) 13.32 % 18.60 1,100.09

Total 5,484.47 6,289.53 6,133.99 7,018.73

CoD per year 2.76 % 2.96 % 2.32 % 2.15 % 3.70 %

5

The BEA has verified the loan balance as of 31.12.2012 in the proposal against the loan balance in the audited balance sheet for 2012. The total loan balance for 2012 in the tariff proposal amounts to Nu 5,484 million, while in the audited accounts it amounts to Nu 5,720 million. The deviation of Nu 236 million is due to the JICA I loan, where BPC states that they will have a saving equal to this amount.

The BEA found that the proposed loan balance of 2012 for THP also includes IDC of Nu. 202.4 million. Since IDC is to be capitalized it should not be included in the estimated CoD. It is not clear what the IDC loan balance for the years 2013-2015 will be for the THPA loans. Based on a yearly payment of Nu 76.238 million on the THP without IDC, we have calculated a yearly payment of Nu 33.734 million for the IDC. The total payment each year will then be Nu 109.972 million, as described in the application.

The CoD proposed by BPC is the weighted average of the interest rate on existing loans as well as the loans that are envisaged to be taken during the tariff period, using the loan balance at the end of each year (i.e. in the middle of the tariff year) as weights.

The BEA has checked the interest rates and the proposed loan balances against the loan agreements, and found them to be correct.

For the future loans (Transmission Program) that is expected to be financed through a mix of debt and equity in the forthcoming tariff period, the BPC has assumed a gearing ratio of 70 % and an interest rate of 13.32 %. The interest rate is based on the weighted average interest rate of the interest rates offered by the domestic financial institutions (Bank of Bhutan & Bhutan National Bank) for a 10 year secured manufacturing/industry loan.

Due to the decreasing inflation, it is expected that the lenders interest rate will decrease as well. Further, it is assumed that BPC as a company owned by the RGoB will be able to borrow money at a lower interest rate than private companies. The only loan BPC has taken in the current tariff period is from NPPF, who offered the loan at an interest rate of 9%. The BEA viewed that the BPC should be able to take up similar loans also in the next tariff period at a slightly higher interest rate of 9.5%.

When estimating the future loan balances, BPC has inflated the capital drawdown amount each year for each project using a forecasted inflation index of 9% per year. BPC has allocated 70% of the inflated future capital drawdown to debt for the transmission investments that are to be financed through both equity and debt. Next, they have calculated an annual IDC of the debt financed capital drawdown. This is added to the outstanding loan balance for the tariff period. The outstanding loan is included in the loan balance when capitalized, where the BPC also includes the IDC. Since IDC is included in the investment schedule when capitalized and added to the asset value, it is not to be included in the loan balance. Further, the BEA has reduced the expected loan balance of future loans due to expectations of deferred investments compared to BPC’s proposed investment plan.

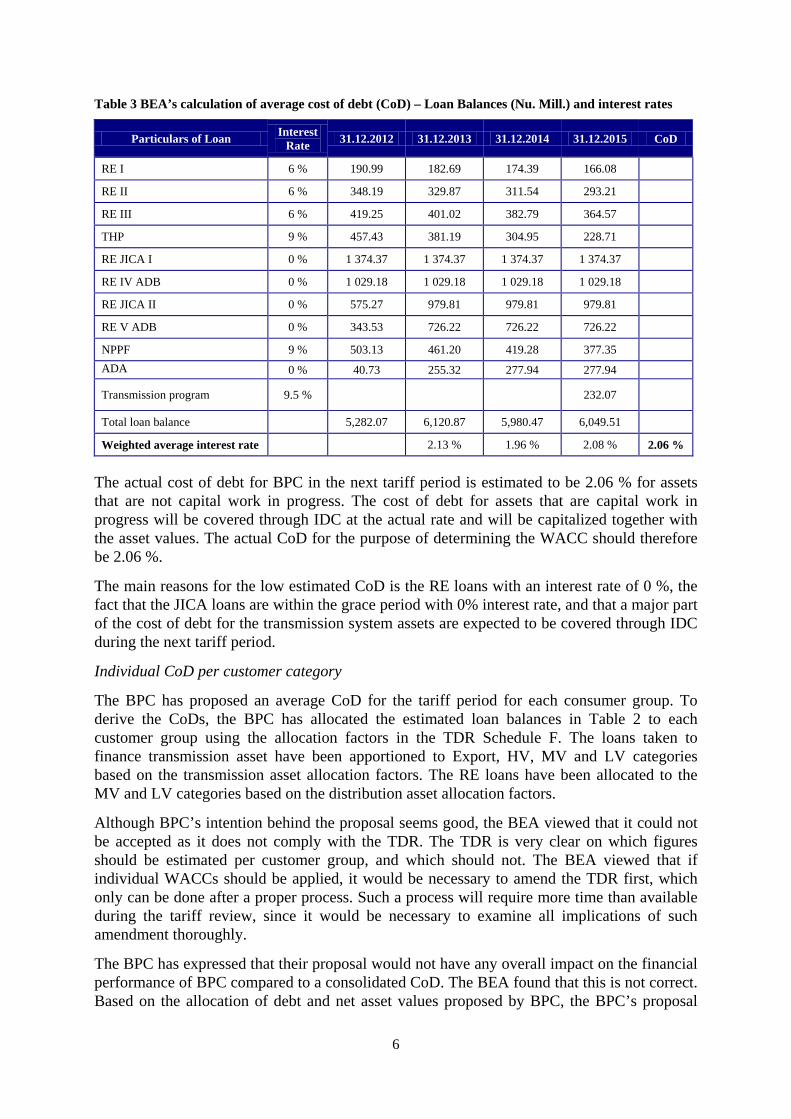

The interest rates and loan balances used by the BEA to estimate the regulatory CoD for the next tariff period are shown in Table 3. The weighted average interest rate per year is calculated using the estimated loan balances for each loan as weights. The CoD for the tariff period is calculated as the weighted average of the annual interest rate, using the total loan balances per year as weights. BEA has used a gearing of 70 % and an inflation of 7.94 % for future loans.

6

Table 3 BEA’s calculation of average cost of debt (CoD) – Loan Balances (Nu. Mill.) and interest rates

Particulars of Loan Interest Rate 31.12.2012 31.12.2013 31.12.2014 31.12.2015 CoD

RE I 6 % 190.99 182.69 174.39 166.08

RE II 6 % 348.19 329.87 311.54 293.21

RE III 6 % 419.25 401.02 382.79 364.57

THP 9 % 457.43 381.19 304.95 228.71

RE JICA I 0 % 1 374.37 1 374.37 1 374.37 1 374.37

RE IV ADB 0 % 1 029.18 1 029.18 1 029.18 1 029.18

RE JICA II 0 % 575.27 979.81 979.81 979.81

RE V ADB 0 % 343.53 726.22 726.22 726.22

NPPF 9 % 503.13 461.20 419.28 377.35 ADA 0 % 40.73 255.32 277.94 277.94

Transmission program 9.5 % 232.07

Total loan balance 5,282.07 6,120.87 5,980.47 6,049.51

Weighted average interest rate 2.13 % 1.96 % 2.08 % 2.06 %

The actual cost of debt for BPC in the next tariff period is estimated to be 2.06 % for assets that are not capital work in progress. The cost of debt for assets that are capital work in progress will be covered through IDC at the actual rate and will be capitalized together with the asset values. The actual CoD for the purpose of determining the WACC should therefore be 2.06 %.

The main reasons for the low estimated CoD is the RE loans with an interest rate of 0 %, the fact that the JICA loans are within the grace period with 0% interest rate, and that a major part of the cost of debt for the transmission system assets are expected to be covered through IDC during the next tariff period.

Individual CoD per customer category

The BPC has proposed an average CoD for the tariff period for each consumer group. To derive the CoDs, the BPC has allocated the estimated loan balances in Table 2 to each customer group using the allocation factors in the TDR Schedule F. The loans taken to finance transmission asset have been apportioned to Export, HV, MV and LV categories based on the transmission asset allocation factors. The RE loans have been allocated to the MV and LV categories based on the distribution asset allocation factors.

Although BPC’s intention behind the proposal seems good, the BEA viewed that it could not be accepted as it does not comply with the TDR. The TDR is very clear on which figures should be estimated per customer group, and which should not. The BEA viewed that if individual WACCs should be applied, it would be necessary to amend the TDR first, which only can be done after a proper process. Such a process will require more time than available during the tariff review, since it would be necessary to examine all implications of such amendment thoroughly.

The BPC has expressed that their proposal would not have any overall impact on the financial performance of BPC compared to a consolidated CoD. The BEA found that this is not correct. Based on the allocation of debt and net asset values proposed by BPC, the BPC’s proposal

7

would give an undue profit of approximately Nu. 180 million per year in the next tariff period. The reason for this is that introducing individual CoDs without also introducing individual gearing ratios is not a consistent way of dealing with the cost of capital. With individual gearing ratios, the differences in the individual WACCs would be significant higher than proposed by BPC. This emphasizes the importance of a thorough examination of all implications before it is decided to amend the WACC provisions in the TDR.

The BEA would like to add that it is not evident that a consolidated WACC implies any cross-subsidy, as in general the liabilities of a company are not tied to specific assets. Currently BPC is in a situation where the debt can be connected to specific investment projects. In the longer run this is not likely to be the case as new debt will be taken and old debt will be refinanced independently of any specific investment. Also under such circumstances the interest rates of a company’s loan portfolio can vary significantly.

2.2.3.3 Cost of Equity BPC has applied for a CoE of 16 %, referring to the CERC norms for Cost of Equity (CoE) in the Indian power sector. In India the regulated CoE is 15.5 %, plus 0.5 % if the investment project is commissioned according to the plan. The BPC’s view is that the CoE of the power sector in Bhutan should be equal to or higher than the CoE of the Indian power sector, considering the integrated nature of the two sectors. The BEA viewed that despite the close links between India and Bhutan, the CoE for the two sectors are not directly comparable mainly due to differences in gearing ratios and the investors’ perspective.

The CoE can be estimated in many ways, but the Capital Asset Pricing Model (CAPM) is widely used. According to the CAPM model the CoE should be estimated as:

(1)

is the Equity Risk Premium, which normally is measured as the extra return that stocks have to offer relative to Government bonds to compensate for the higher risk of investing in stocks. is the risk free rate, and normally is the return on the Government bond the ERP is measured against. The is the only sector specific variable in the formula, and is a measure of the systematic risk for the sector compared to the risk of a balanced portfolio on the stock market. Higher the risk compared to the stock market, higher the .

The is normally estimated based on the correlation between a company’s or sector’s return and the return on a balanced stock market portfolio. If the return of the company correlates perfectly with the market portfolio, is 1. If the return of the company is more volatile than the return on the market portfolio is higher than 1, and if it is less volatile then it is less than 1. If there is no correlation between the company’s return and the return on the market portfolio, is 0. If there is a negative correlation, is less than 0, and this implies that the company’s return will increase if the return on the stock market decreases. The is not a measure of the total risk of investing in only the specific company or sector, but a measure of the risk that the investor cannot remove through diversification of his investment in a well balanced portfolio. Traditionally the is much lower for the power sector than other sectors listed on the stock exchange, due to the low covariance between return on assets between the power sector and the market portfolio. This is also the reason for why investments in the power sector are attractive to investors despite the lower return on assets. The investor can reduce its risk by adding power sector investments to its portfolio.

8

is the levered beta, which take the capital structure (gearing) of the company into account. If two companies with the same systematic risk (represented by the unlevered beta, ) have different gearing, they will have different . The transformation from the unlevered beta to the levered beta, taking the Debt/Equity-ratio (D/E) into account, is done by most practitioners according to the following formula:

(2)

Whether the CERC CoE norm of 16 % is relevant in Bhutan or not is depends on whether the risk free rate, the equity risk premium and levered beta is the same or not. If all parameters are the same in both countries, the answer is yes. It any of the parameters are different, the answer is most likely no. Whether it should be higher or lower will depend on the differences in the factors.

If investors in Bhutan have access to the same Government bonds and stock markets as Indian investors, we can assume that the risk free rate and the equity risk premium are the same in both countries. However, the BEA viewed that the equity risk premium should be lower due to differences in the investors’ perspective between India and Bhutan. DHI as an investor will most likely have limitations in its investment possibilities compared to an Indian private investor. Due to such limitations, the BEA viewed that the ERP should be lower for DHI than for Indian investors. Regarding the levered beta, the BEA viewed that there should be differences due to different gearing ratios. The differences in gearing between Indian and Bhutanese companies will give differences in , and therefore also in the CoE.

To exemplify the view of the BEA, we have calculated the differences assuming that a CoE of 16 % is a reasonable level in India. Given that the underlying factors in the CoE formula is relevant for the power sector in Bhutan, the CoE can be recalculated to a level suitable for Bhutan if we know two out of the three parameters in formula (2).

In an article on the CoE in India from June 2010, it is argued that the CoE for Indian investors should be 15.5 %1, the same as the CERC norm. The article is written by Saurabh Mukherjea, Head of Equities, Institutional Equities, Ambit Capital. He assumed the risk free rate to be 7.4 % (expected return on 10-year Government bond), the levered beta to be 1.1, and the ERP to be 7.25 %. From formula (2) we get:

(3)

Since he assumed to be 1.1, and we know that the CERC gearing norm is 70% debt and 30% equity, we can apply formula (2) to calculate the .

(4)

DGPC has a gearing of around 40 percent. By applying formula (2) on , which we for this calculation assume to be the same in India and Bhutan, we get a for the BPC like:

(5)

1 http://www.vccircle.com/byinvitation/2010/06/14/what-real-cost-equity-india

9

By replacing the of 1.1 (India) with 0.56 (Bhutan), we get the following CoE for Bhutan:

(6)

Under the assumptions in Mukherjea’s calculations the Indian CoE adjusted for the BPC’s gearing ratio is 11.5 %, which could be a benchmark used in the tariff review. However, the BEA viewed that both the and the ERP assumptions are too high in Mukherjea’s example.

One of the few sources for assessing the CoE using CAPM on the power sector of India is Professor of Finance, Aswath Damodaran at the Stern School of Business at the New York University. He is an authority in corporate finance and equity evaluation, and has done many studies of equities throughout the world. Also in the Indian power sector. Much of his work and data is available at his website2.

Professor Damodaran calculates CoE in USD, with the return on as 10-year US Government bond as a risk free rate of return. His updated figures for 2013 regarding the CoE estimation for the Indian power sector are:

• Risk free rate: 1.76 % (10 year US Government bond)

• ERP: 8.8 percent, based on an ERP of 5.8 % for mature markets and a country risk premium for India of 3 %.

• Unlevered beta, : 0.4657, estimated for the Indian power sector.

Adjusting the unlevered beta to a levered beta at 40 % gearing, using formula (4), gives a of 0.7762. Inserting these figures into formula (2) we get:

(7)

However, this CoE is in USD. To transform the CoE into other currencies, Professor Damodaran suggests adjusting the CoE with the difference between the inflation in that currency and the USD. The difference in inflation between India and US has been approximately 4.7 % the last 10 years, but the 2009 and 2010 figures were quite extreme. The average difference in the inflation forecast for the next 3 years is around 3 %3. Adjusting the result in (7) for expected differences in the inflation, we get an estimated CoE for Bhutan of 11.6 %. The BEA viewed that also the and ERP used by Professor Damodaran was too high for Bhutan.

The BEA viewed that the best estimate of CoE could be obtained using the CAPM model on the updated data of Professor Damodaran, adjusting the and the ERP, and applying the differences in the expected inflation between the US and India. None of the figures are accurate, but the BEA viewed that the should be in the interval 0.3 – 0.4, the ERP in the interval 7.2% – 8.8% and the inflation in the interval 3% - 4%. The reason for adjusting the was that the more frequent tariff reviews reduces the impact of recessions in Bhutan compared to India, and hence reduces the systematic risk too.

Regarding the ERP, DHI is an investor with limitations in its investment portfolio compared to a private international investor. Such limitations will result in an expected return on investments that is lower than the one assumed by professor Damodaran. It is quite common to assume that Governments in general should expect a lesser return on assets than investors on stock exchange, though there might be examples of the opposite. 2 http://pages.stern.nyu.edu/~adamodar/ 3 www.tradingeconomics.com

10

The BEA has found it difficult to estimate the differences in inflation between the US and India exactly. Based on the historic differences it should be more than 4 %. Based on the current expectations it should be less than 3%. BEA expects it to be between 3 and 4 %.

Based on the expected intervals of the , the ERP and the inflation the BEA viewed that a CoE of 10 % should be appropriate for investors in BPC equity.

2.2.3.4 Gearing The BPC proposed a gearing ratio of 44%, which the BPC states is the company’s actual gearing ratio as on 31st December 2012. The BPC also states that BPC would have preferred adoption of different gearing ratios for the individual customer category to reflect true cost of supply.

BEA viewed that the gearing ratio should be assessed using the average debt over the next tariff period over the average net asset value for the same period.

According to BPC’s proposal the average loan balance in the next tariff period is expected to be Nu. 6,481 million, whilst the net asset value used for determining the tariffs is expected to be Nu. 16,371 million. This gives a gearing ratio of 39.6%.

Using BEA’s reviewed figures, the average loan balance as of 31.12.2015 in the next tariff period is expected to be Nu. 6,059 million, whilst the net asset value used for determining the tariffs is expected to be Nu. 15,191 million. This gives a gearing ratio of 39.8%. The BEA therefore viewed that the gearing ratio of 40% should be used, as prescribed in the TDR Schedule C.

The BEA would like to point out that the relatively low gearing of BPC has a negative impact on the BPC tariffs. Due to the low share of debt, the tariffs are higher than necessary. The impact on the tariffs of reducing the debt will be the opposite of what some of the customers stated during the public hearing. If the debt is reduced, the cost of supply will increase. The reason is that the CoE is higher than the CoD. A post-tax CoE of 10% is equal to a pre-tax CoE of 14.3%. The BEA is of the view that the BPC should move towards an optimal gearing, which probably is in the range of 60-70% debt. If a change in gearing is not observed towards the next tariff review, the BEA may have to review the practice of using a gearing close to the observed one. In India they use a gearing of 70% in the regulatory WACC, independently of the actual gearing of the companies.

2.2.3.5 The WACC Using a CoD of 2.06 %, CoE of 10 %, Gearing ratio of 40 % and a Tax Rate of 30 % the BEA has estimated the WACC to be 9.40 %.

2.3 Inflation The historical inflation rates are used for calculation of historical costs in 2012-values, which is the base year for this tariff review. The forecasted inflation rate is used for the calculation of the forecasted costs (allowances) and investments in each of the years in the tariff period.

11

2.3.1 BPC proposal

The BPC has proposed the realized inflation rates for the prevailing tariff period as estimated by the National Statistics Bureau as shown in the Table 4 below. The BPC states that the Authority approved an average inflation rate of 5% against BPC’s proposed forecast of 5.96% in 2010. The realized inflation rate for the period has been significantly higher (around 10% for the 4th quarter of 2012) than the approved figure which has adversely impacted BPC on O&M costs and return on assets.

Table 4 Historical inflation rates

2010 2011 2012 Average

Inflation 7.0 % 8.8 % 10.9 % 8.9 %

The average inflation rate for the next tariff period is proposed by BPC to be 8.9% based on the arithmetic average of the realized inflation rates for 2010, 2011 and 2012.

2.3.2 Input from stakeholders

The BCCI in their written comments submitted that for inflation, a more realistic figure should be used based on the forecast made by the International Monetary Fund (IMF).

The BPC in their written comments submitted that the consistent and uniform application of the inflation forecast mechanism would be fair rather than convenient change in the applied mechanism resulting in lower recoveries, always impacting the financial performance of the Licensee.

2.3.3 BEA review

The BEA has verified that the inflation rates for the years of 2010 to 2012 are consistent with the official figures from National Statistics Bureau. These figures should be used when inflating historical figures to 2012 values in this tariff review.

The BPC has not used any forecasts when estimating the future inflation rate, but has proposed the average inflation over the three past years. The BEA does not find the methodology appropriate for the tariff review. The BEA has checked that the World Economic Outlook International Monetary Fund (IMF) for the forecasted inflation for the period 2013 to 2016. The IMF forecasts are shown in Table 5. The ADB Asian Development Outlook 2013 from April 2013 has forecasted the inflation of 2013 to 9.3% and expects 7.4% in 2014.

The BEA recognized that forecasting the inflation is very difficult, and that different sources will have different estimations. However, the BEA viewed that the IMF forecast should be used as basis for the determination of the expected inflation in the next tariff period, as it was done in the last review. The average of the forecasts for the period 20013-2016 is 7.94%. The BEA therefore determined the annual inflation to be used when determining the tariffs should be 7.94 % per year in the next tariff period.

12

Table 5 Inflation forecast4

Year IMF*

2013 9.33% 2014 8.16%

2015 7.68% 2016 6.57% Average 2013-2016 7.94%

The BEA has approved an average historical inflation rate of 8.9% and the forecasted inflation rate of 7.94 % to be used in this tariff review.

Using an annual inflation rate of 7.94 % instead of 8.9 % has an impact on all of the allowances proposed by the BPC, except for the energy cost. It has an impact on the allowances for return on assets and depreciations through reduced capitalized investment amounts and estimated depreciations.

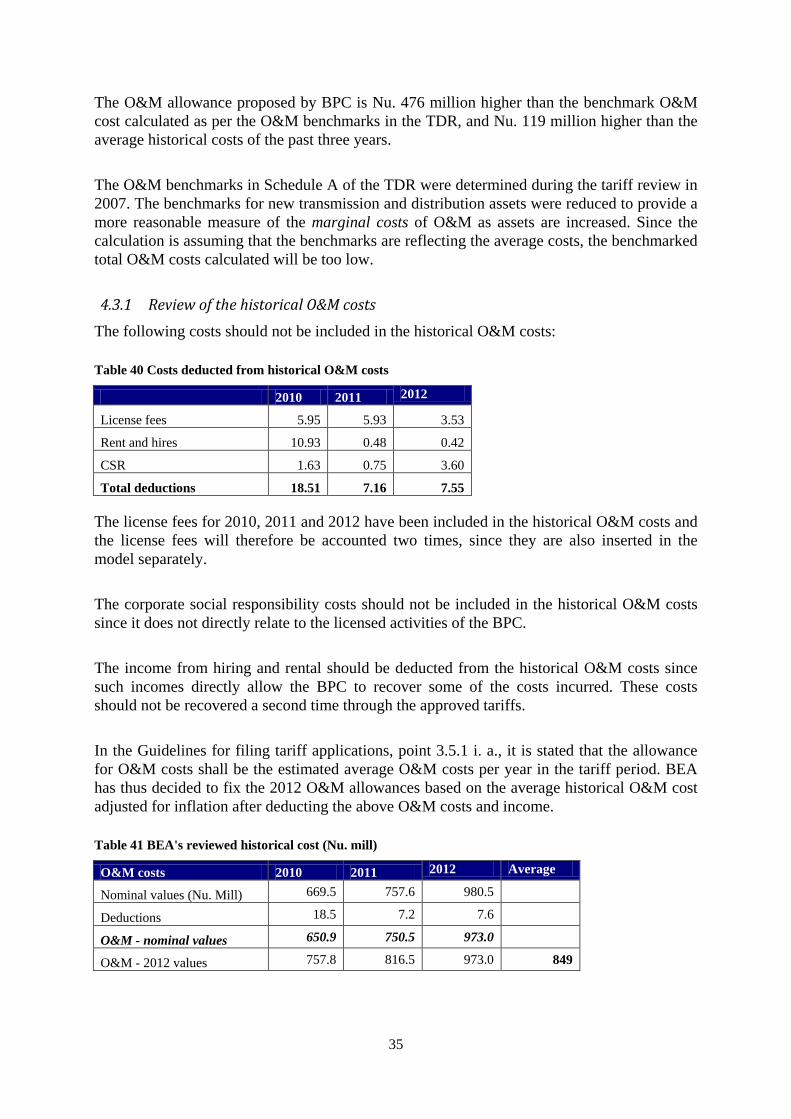

2.4 Other regulatory parameters The O&M benchmark parameters are determined in the Tariff Determination Regulation Schedule A, but may be updated by the BEA from time to time. These parameters are discussed in section 4.3.2. The O&M efficiency gain parameters are discussed in 4.3.3. The technical loss allowances are discussed in section 2.4.1, and the commercial loss allowances are discussed in section 2.4.2. The collection rate is discussed in section 2.4.3. These regulatory parameters are determined in the Tariff Determination Regulation Schedule E, but may be updated by the BEA from time to time.

2.4.1 Technical transmission and distribution losses

The technical transmission and distribution losses are losses due to resistance in the network lines, cables and transformers and cannot be fully avoided. Since these losses are requiring the BPC to purchase more energy than they sell, they have an impact on the tariffs. The higher the technical losses, the more energy must be purchased per unit sold, and hence the tariff will increase.

2.4.1.1 BPC’s proposal The BPC has proposed technical losses of 2% for HV, 2.5% for MV, 12% for LV which is as per Schedule E of the TDR.

2.4.1.2 BEA review The BEA reviewed the historical losses for BPC and as per the calculations the global losses for BPC are as in Table 6.

4 Inflation, end of period prices from http://www.imf.org/external/pubs/ft/weo/2013/01/weodata/download.aspx

13

Table 6 – Global technical losses - % of energy purchase

2010 2011 2012 Global losses 5.07% 4.99% 4.26%

Based on the historical losses of the BPC, it is recommended that the technical loss allowances be fixed as shown in Table 7.

Table 7 – BEA’s approved technical losses

Losses HV 2.0 % MV 2.5 % LV 12.0 %

2.4.2 Commercial losses

The commercial losses are mainly due to low metering efficiency and electricity theft. According to the Tariff Determination Regulation section 5.7 and 6.8 the commercial losses shall be taken into consideration when determining the tariffs.

2.4.2.1 BPC’s proposal The BPC has proposed the commercial losses of 0.5% for HV, 1% for MV and 5% for the LV customers considering that a commercially lossless system cannot be expected. According to the Tariff Determination Regulation schedule E the commercial losses are calculated considering 5% losses of LV sales and 0 % for MV and HV.

Table 8 – BPC’s proposed commercial loss factors

2010 2011 2012 Commercial losses: 1.49 % 1.49 % 1.51 %

2.4.2.2 BEA’s review As BPC should have achieved 100 % metering and the commercial losses mainly relates to electricity theft. Therefore, a commercial loss allowance of 0.5% and 1% for HV and MV are high since BPC has confirmed that there were no historical case of electricity theft from HV and MV lines and none are reported to BEA for consideration. Therefore commercial loss has been calculated considering of 0% for HV and MV sales and 5% for LV sales as per the TDR Schedule E will be used for calculation of the commercial losses in Table 9.

Table 9 – BEA’s approved commercial loss factors

2013 2014 2015 Commercial losses: 1.06% 1.04% 1.06%

2.4.3 Collection rates

The collection rate is the rate of billed energy sales that is actually paid by the customers. The rate will be less than 100 % if any of the customers never pays an electricity bill and the security deposits do not fully cover the unpaid bill. To avoid the BPC from having an

14

economic loss due to unpaid bills, the expected losses are borne by the other customers, as determined in the Tariff Determination Regulation sections 6.9 and 9.5.3.

2.4.3.1 BPC’s proposal The BPC has proposed the collection rates of 98% (LV=91%, MV=98% and HV=100%) based on the BPC’s actual weighted average collection rate for the year 2012. As per the Tariff Determination Regulation Schedule E the collection rates are 100 % for all the customer categories (HV, MV and LV).

2.4.3.2 BEA’s review The BEA has scrutinized the collection rate calculation, books of accounts and other information provided by the BPC, but cannot find any evidence justifying a weighted average collection rate of 98 %. The outstanding bills of 2011 and 2012 are used to compute the collection efficiency and BPC has not reported any outstanding bills earlier than 2011. Therefore BEA assumes that there are no outstanding bills other than the 2011 and 2012. According to the books of accounts only small amount of bad debt stemming from unpaid bills is written off every now and then.

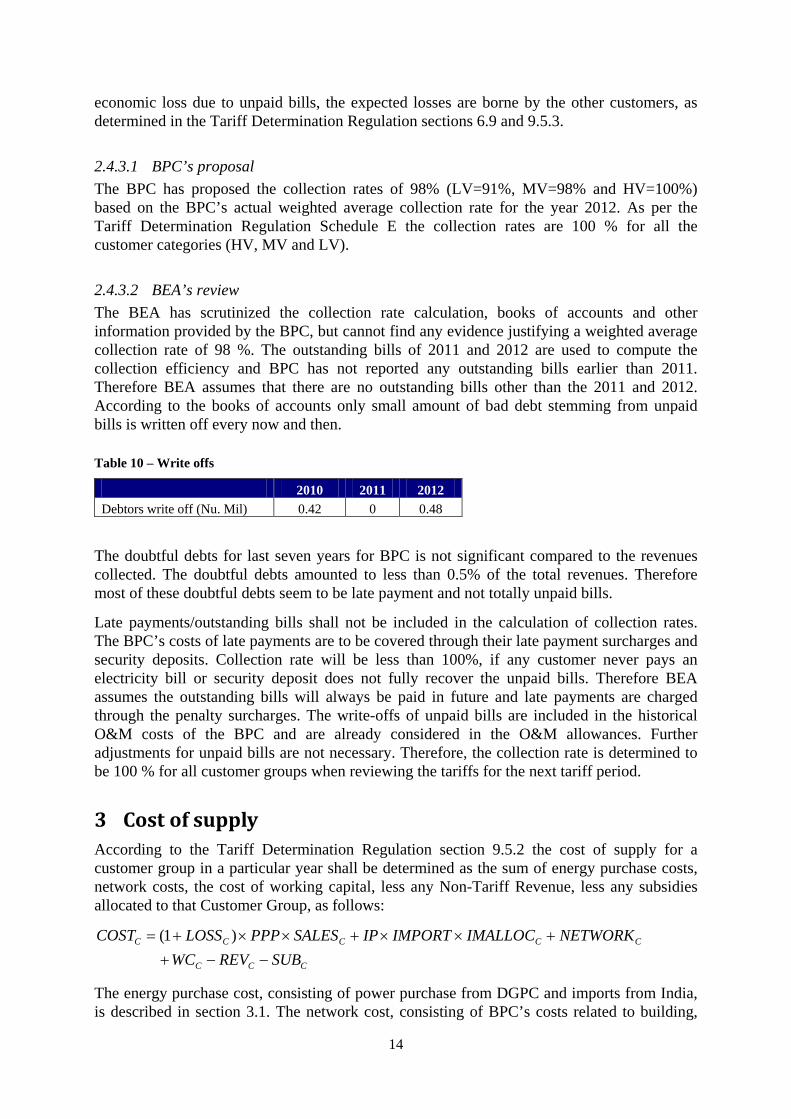

Table 10 – Write offs

2010 2011 2012 Debtors write off (Nu. Mil) 0.42 0 0.48

The doubtful debts for last seven years for BPC is not significant compared to the revenues collected. The doubtful debts amounted to less than 0.5% of the total revenues. Therefore most of these doubtful debts seem to be late payment and not totally unpaid bills.

Late payments/outstanding bills shall not be included in the calculation of collection rates. The BPC’s costs of late payments are to be covered through their late payment surcharges and security deposits. Collection rate will be less than 100%, if any customer never pays an electricity bill or security deposit does not fully recover the unpaid bills. Therefore BEA assumes the outstanding bills will always be paid in future and late payments are charged through the penalty surcharges. The write-offs of unpaid bills are included in the historical O&M costs of the BPC and are already considered in the O&M allowances. Further adjustments for unpaid bills are not necessary. Therefore, the collection rate is determined to be 100 % for all customer groups when reviewing the tariffs for the next tariff period.

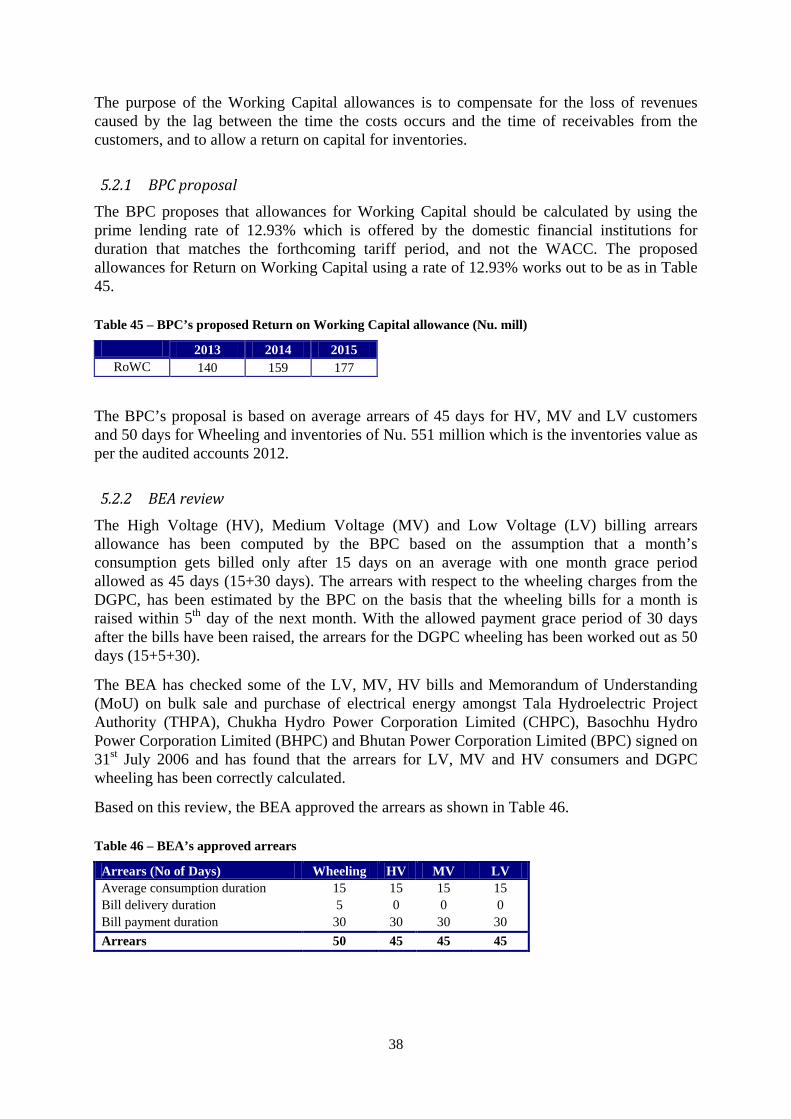

3 Cost of supply According to the Tariff Determination Regulation section 9.5.2 the cost of supply for a customer group in a particular year shall be determined as the sum of energy purchase costs, network costs, the cost of working capital, less any Non-Tariff Revenue, less any subsidies allocated to that Customer Group, as follows:

CCC

CCCCC

SUBREVWCNETWORKIMALLOCIMPORTIPSALESPPPLOSSCOST

−−++××+××+=

)1(

The energy purchase cost, consisting of power purchase from DGPC and imports from India, is described in section 3.1. The network cost, consisting of BPC’s costs related to building,

15

operating and maintaining their network, is described in section 3.2. The cost of working capital is described in section 5.2. The non-tariff revenues are described in section 5.3. The subsidies are described in section 4.4.

3.1 Energy purchase cost The Energy cost is the cost incurred by the BPC for purchasing the energy from DGPC and India for supply to the customers which is determined as per the following equation:

CCCC IMALLOCIMPORTIPSALESPPPLOSS ××+××+= )1(Cost PurchaseEnergy

Where

• Energy Purchase CostC is the cost for Customer Group “C”, in million Ngultrum;

• LOSSC is the sum of technical and commercial losses allocated to Customer Group “C”, as a percentage;

• PPP is the Power Purchase Price, which is the Additional Price determined for the DGPC, in Ngultrum per kWh;

• SALESC is the sales for the year attributed to Customer Group “C”, in GWh.

• IP is the average import price in Ngultrum per kWh;

• IMPORT is the volume of electricity imported, in GWh;

• IMALLOCC is the allocation of import costs to Customer Groups, for which the high voltage customer group equals one (100 %) and for other customer groups equals zero (0 %).

3.1.1 Power purchase from DGPC

The power purchase cost for a specific customer group is the sales adjusted for the loss factor multiplied with the power purchase price.

3.1.1.1 Power purchase price For the purchase of power from the DGPC’s various generating plants, the BPC has proposed a royalty energy price of Nu. 0.13/kWh for energy drawn within the royalty limit and an additional energy price of Nu. 1.2/kWh for energy drawn above the royalty limit. However, BPC submits that as permitted by regulation, any revisions of the prevailing generation tariffs will be incorporated in this proposal and requests the BEA to consider allowing these costs as determined by the BEA to factor in while determining the final tariffs.

3.1.1.2 Sales forecasts The sales forecasts are used to estimate the power purchase costs of the BPC and also for estimating the average cost of supply per unit sold. The sales forecasts have therefore a large impact on the determined tariffs.

16

3.1.1.2.1 BPC’s proposal The BPC has forecasted the sales volumes for each customer category as detailed in Table 11.

Table 11 – BPC’s sales forecasts per customer category

Sales forecast (GWh) 2012 (actual) 2013 2014 2015 LV 378 392 413 435 MV 124 155 198 247 HV 1267 1,307 1,376 1376 Total domestic sales 1769 1,855 1,987 2,057 Wheeling 4938 4,927 5156 5128

3.1.1.2.2 Input from stakeholders The BCCI in their written comments recommended that the energy sales forecast for HV and MV customers should be made based on the historical trend of energy sales and the projected drawal of power by new customers. The demand in MW can then be estimated by assuming a load factor also based on the historical trend. Estimating a more realistic MW for the HV and MV customer category is important as it will have a major bearing on the demand charge calculated for the two customer categories.

3.1.1.2.3 BEA’s review BPC has projected the sale for rural LV domestic customers by considering the forecasted Rural Electrification (RE) customers and historical average energy consumption of 92 kWh per household and the average consumption growth rate of 1.9% for RE fill in customers. The LV industrial sale has been assumed to increase at the rate of 1 %. The LV sales forecast for other customers in the LV category was projected based on the historical consumption trend for the period 2004- 2012.

The BEA found that LV sales forecast follows a trend that was found to be realistic, as can be seen from

Figure 1.

Figure 1 – Historical and forecasted LV energy sales in GWh

The MV sales forecast consists of the sales forecast for the MV industries and the hydropower construction power. The MV industries sales consider the MV contracted demand and average load factor for the past two - three years (2010-2012). For the new industries which are expected to come online in 2013, a load factor of 0.1 (2013) and 0.2 (2014) was proposed

17

considering the trend in consumption pattern of new industries during initial start up phase. A load factor of 0.27 is used for 2015-2016 which is the average load factor of all MV industries. The MV industries sales forecast follows a trend that was found to be realistic.

The hydropower construction power forecast includes the construction power requirement for Punastangchhu I and II, Mangdechhu, Dagachhu, Sankosh, Kuri-Gongri, Chamkharchhu, Kholongchhu, Wangchhu, Bunakha, Amochhu, Nikachhu, Druk Bindu and existing hydropower projects with a load factor of 0.50.

Table 12 –Forecast Hydropower Construction Power

Demand (MW)

Energy(GWh) Project 2013 2014 2015 2016 2013 2014 2015 2016 Punatsangchhu I 8.0 9.0 10.0 9.0 35.04 39.42 43.80 39.42 Punatsangchhu I 1.5 3.0 5.0 6.0 6.57 13.14 21.90 26.28 Mangdechhu 1.0 2.5 4.0 5.0 4.38 10.95 17.52 21.90 Dagachhu 1.4 0.5 - - 6.13 2.19 0.00 4.38 Sankosh - 1.5 3.0 5.0 6.57 13.14 8.76 Kuri-Gongri - - 0.2 1.0 0.88 6.57 Chamkharchhu - 0.2 1.0 2.0 0.88 4.38 6.57 Kholongchhu - 0.5 1.0 1.5 2.19 4.38 4.38 Wangchhu - 0.5 1.0 1.5 2.19 4.38 6.57 Bunakha - 0.2 0.5 1.0 0.88 2.19 8.76

Amochhu - 0.5 1.0 1.5 2.19 4.38 Nikachhu - 0.2 1.0 2.0 0.88 4.38 Total 2.4 6.6 12.7 20.5 10.51 28.91 55.63 67.89

The BEA found that Punatsangchu I and II projects are drawing power at 66 kV and therefore, the demand and energy forecast should be deducted from the MV customers and included under HV customers.

The BEA asked the DGPC and the Department of Hydropower and Power Systems (DHPS) to verify the hydropower construction power forecast submitted by the BPC. It was found that the DHPS projections are much higher and optimistic than the BPC projections. However, based on the historical consumption pattern of the hydropower projects under construction, BPC’s projection seems more realistic. Based on the above, the BEA decided on the hydropower construction power estimate given in Table 13. The energy forecasts are estimated using load factors of 0.5. The total MV sales forecast in each tariff year will be as in Table 13. The MV sales forecasts are illustrated in

18

Figure 2.

Table 13 – BEA's MV sales forecast (GWh)

2013/14 2014/15 2015/16 MV industries 102.9 116.5 125.7 HP construction power 10.5 28.9 55.6 Total MV Sales 113 145 181

19

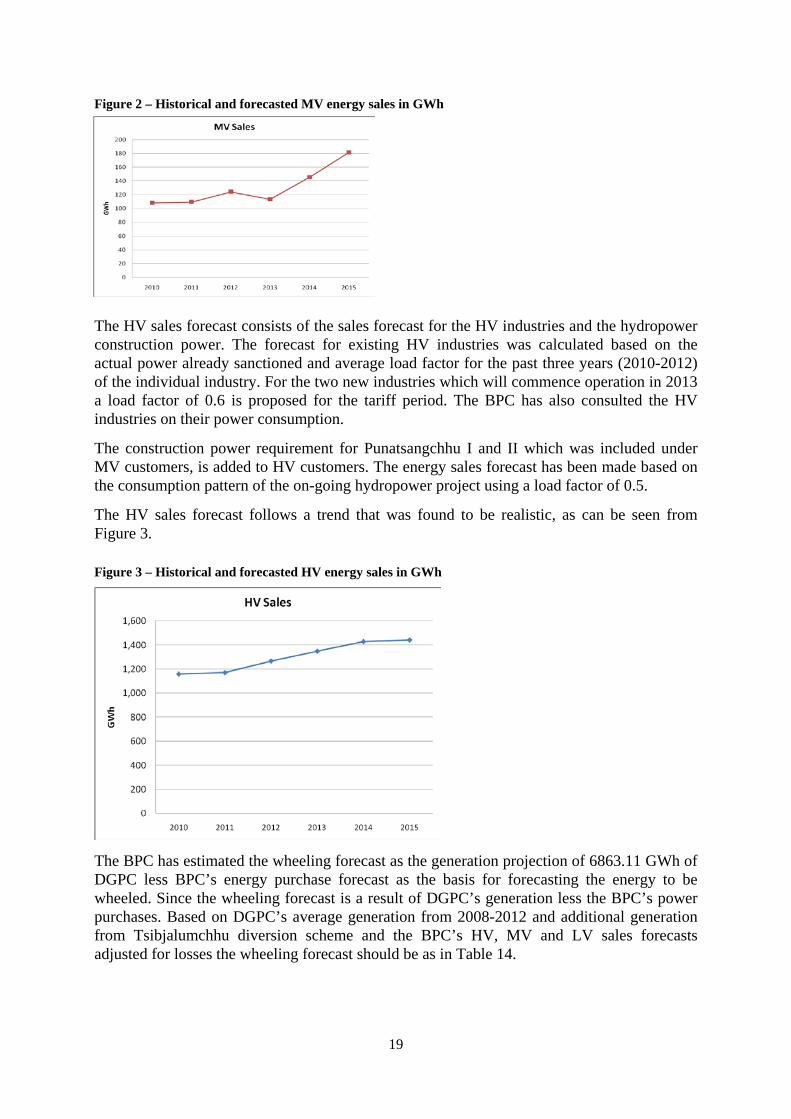

Figure 2 – Historical and forecasted MV energy sales in GWh

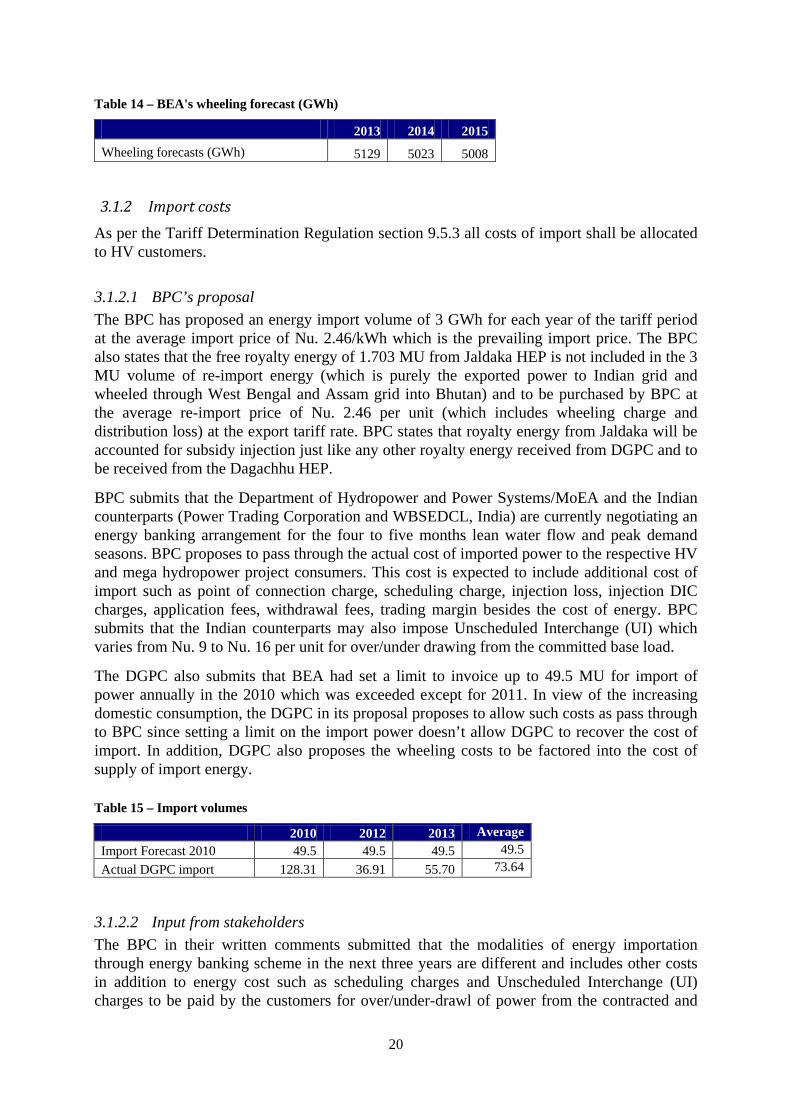

The HV sales forecast consists of the sales forecast for the HV industries and the hydropower construction power. The forecast for existing HV industries was calculated based on the actual power already sanctioned and average load factor for the past three years (2010-2012) of the individual industry. For the two new industries which will commence operation in 2013 a load factor of 0.6 is proposed for the tariff period. The BPC has also consulted the HV industries on their power consumption.

The construction power requirement for Punatsangchhu I and II which was included under MV customers, is added to HV customers. The energy sales forecast has been made based on the consumption pattern of the on-going hydropower project using a load factor of 0.5.

The HV sales forecast follows a trend that was found to be realistic, as can be seen from Figure 3.

Figure 3 – Historical and forecasted HV energy sales in GWh

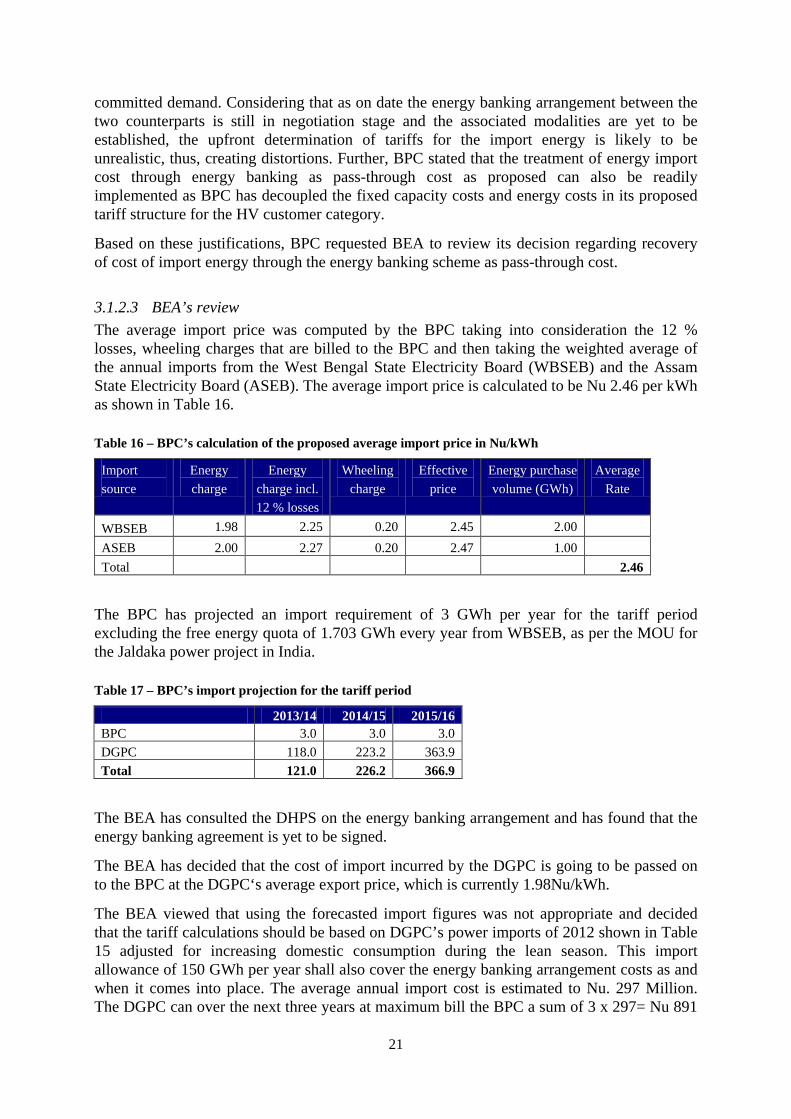

The BPC has estimated the wheeling forecast as the generation projection of 6863.11 GWh of DGPC less BPC’s energy purchase forecast as the basis for forecasting the energy to be wheeled. Since the wheeling forecast is a result of DGPC’s generation less the BPC’s power purchases. Based on DGPC’s average generation from 2008-2012 and additional generation from Tsibjalumchhu diversion scheme and the BPC’s HV, MV and LV sales forecasts adjusted for losses the wheeling forecast should be as in Table 14.

20

Table 14 – BEA's wheeling forecast (GWh)

2013 2014 2015 Wheeling forecasts (GWh) 5129 5023 5008

3.1.2 Import costs

As per the Tariff Determination Regulation section 9.5.3 all costs of import shall be allocated to HV customers.

3.1.2.1 BPC’s proposal The BPC has proposed an energy import volume of 3 GWh for each year of the tariff period at the average import price of Nu. 2.46/kWh which is the prevailing import price. The BPC also states that the free royalty energy of 1.703 MU from Jaldaka HEP is not included in the 3 MU volume of re-import energy (which is purely the exported power to Indian grid and wheeled through West Bengal and Assam grid into Bhutan) and to be purchased by BPC at the average re-import price of Nu. 2.46 per unit (which includes wheeling charge and distribution loss) at the export tariff rate. BPC states that royalty energy from Jaldaka will be accounted for subsidy injection just like any other royalty energy received from DGPC and to be received from the Dagachhu HEP.

BPC submits that the Department of Hydropower and Power Systems/MoEA and the Indian counterparts (Power Trading Corporation and WBSEDCL, India) are currently negotiating an energy banking arrangement for the four to five months lean water flow and peak demand seasons. BPC proposes to pass through the actual cost of imported power to the respective HV and mega hydropower project consumers. This cost is expected to include additional cost of import such as point of connection charge, scheduling charge, injection loss, injection DIC charges, application fees, withdrawal fees, trading margin besides the cost of energy. BPC submits that the Indian counterparts may also impose Unscheduled Interchange (UI) which varies from Nu. 9 to Nu. 16 per unit for over/under drawing from the committed base load.

The DGPC also submits that BEA had set a limit to invoice up to 49.5 MU for import of power annually in the 2010 which was exceeded except for 2011. In view of the increasing domestic consumption, the DGPC in its proposal proposes to allow such costs as pass through to BPC since setting a limit on the import power doesn’t allow DGPC to recover the cost of import. In addition, DGPC also proposes the wheeling costs to be factored into the cost of supply of import energy.

Table 15 – Import volumes

2010 2012 2013 Average Import Forecast 2010 49.5 49.5 49.5 49.5 Actual DGPC import 128.31 36.91 55.70 73.64

3.1.2.2 Input from stakeholders The BPC in their written comments submitted that the modalities of energy importation through energy banking scheme in the next three years are different and includes other costs in addition to energy cost such as scheduling charges and Unscheduled Interchange (UI) charges to be paid by the customers for over/under-drawl of power from the contracted and

21

committed demand. Considering that as on date the energy banking arrangement between the two counterparts is still in negotiation stage and the associated modalities are yet to be established, the upfront determination of tariffs for the import energy is likely to be unrealistic, thus, creating distortions. Further, BPC stated that the treatment of energy import cost through energy banking as pass-through cost as proposed can also be readily implemented as BPC has decoupled the fixed capacity costs and energy costs in its proposed tariff structure for the HV customer category.

Based on these justifications, BPC requested BEA to review its decision regarding recovery of cost of import energy through the energy banking scheme as pass-through cost.

3.1.2.3 BEA’s review The average import price was computed by the BPC taking into consideration the 12 % losses, wheeling charges that are billed to the BPC and then taking the weighted average of the annual imports from the West Bengal State Electricity Board (WBSEB) and the Assam State Electricity Board (ASEB). The average import price is calculated to be Nu 2.46 per kWh as shown in Table 16.

Table 16 – BPC’s calculation of the proposed average import price in Nu/kWh

Import source

Energy charge

Energy charge incl. 12 % losses

Wheeling charge

Effective price

Energy purchase volume (GWh)

Average Rate

WBSEB 1.98 2.25 0.20 2.45 2.00 ASEB 2.00 2.27 0.20 2.47 1.00 Total 2.46

The BPC has projected an import requirement of 3 GWh per year for the tariff period excluding the free energy quota of 1.703 GWh every year from WBSEB, as per the MOU for the Jaldaka power project in India.

Table 17 – BPC’s import projection for the tariff period

2013/14 2014/15 2015/16 BPC 3.0 3.0 3.0 DGPC 118.0 223.2 363.9 Total 121.0 226.2 366.9

The BEA has consulted the DHPS on the energy banking arrangement and has found that the energy banking agreement is yet to be signed.

The BEA has decided that the cost of import incurred by the DGPC is going to be passed on to the BPC at the DGPC‘s average export price, which is currently 1.98Nu/kWh.

The BEA viewed that using the forecasted import figures was not appropriate and decided that the tariff calculations should be based on DGPC’s power imports of 2012 shown in Table 15 adjusted for increasing domestic consumption during the lean season. This import allowance of 150 GWh per year shall also cover the energy banking arrangement costs as and when it comes into place. The average annual import cost is estimated to Nu. 297 Million. The DGPC can over the next three years at maximum bill the BPC a sum of 3 x 297= Nu 891

22

Million for recovery of import costs. The weighted average import price is estimated to be 1.97 Nu/kWh for the total import volume for both the BPC and the DGPC imports and the import volumes will be as in Table 18 below.

Table 18 – Expected import volumes

2013/14 2014/15 2015/16 BPC import 4.703 4.703 4.703 DGPC import 150 150 150 Total 154.703 154.703 154.703

3.1.3 Total energy costs

The BPC has proposed to meet the above power purchase requirement through purchase from the DGPC, the BPC’s mini and micro hydro generation and through imports as shown in Table 19.

Table 19 – BPC’s proposed power purchase scheme in GWh

2013 2014 2015

Own generation 15 15 15 Imports 3 3 3 Royalty 1,011 1,063 1,069 Additional Energy 1,055 1,147 1,219 Total energy purchase forecast 2,083 2,228 2,306

The actual embedded generation has gradually decreased from 25 MU in 2009 to 15 MU in 2012 due to wear and tear of equipments and damage caused due to floods. Considering the on-going rehabilitation works, embedded generation forecast of 15 MU for the tariff period has been used.

BPC has calculated the royalty energy from DGPC as 15% of DGPC’s aggregated forecasted generation after adjusting for the auxiliary consumption and plant availability of 98%, however as per the TDR, the generation is adjusted only for auxiliary consumption. The contribution of royalty energy from DGPC has not taken into account the additional generation available from the Tsibjalumchhu diversion scheme from 2014 onwards.

The review has resulted in amendments of the import, royalty energy and purchase from the DGPC which is shown in the Table 20 below.

Table 20 – BEA’s calculated power purchase scheme in GWh

2013 2014 2015 Own generation 15 15 15

BPC Imports 4.703 4.703 4.703 Royalty Energy 1,043 1,048 1,057

Purchase from DGPC 865 998 1,065

DGPC imports 150 150 150

Total energy purchase forecast 2,078 2,215 2,292

23

These costs of power purchase from the DGPC adjusted for the losses are allocated to the HV, MV and LV customers. The cost of imports is allocated to the HV customers as per the Tariff Determination Regulation.

The total energy cost for the different customer categories are estimated by BPC as in Table 21, using a generation tariff of 1.20 Nu/kWh.

Table 21 – BPC’s estimated energy costs per customer category (Million Nu.)

2013 2014 2015 Wheeling 59 62 62 HV 1621 1705 1706 MV 198 252 315 LV 568 598 629 Total 2446 2617 2710

The changes given in Table 20 have an impact on the power purchase costs, and the BEA estimates of the energy costs per customer group using the approved generation tariff of Nu. 1.39/kWh as shown in Table 22.

Table 22 – BEA’s estimated energy costs per customer category (Million Nu.)

2013 2014 2015 Wheeling 71 70 70 HV 2,026 2,139 2,158 MV 167 213 266 LV 645 680 715 Total 2,909 3,102 3,209

3.2 Network Cost The annual network costs allocated to each Customer Group shall comprise a share of each element of the total annual network costs, where the sum of allocations across all Customer Groups shall equal the total annual network costs referred to in subsection 9.3.2 in the Tariff Determination Regulation.

[ ] [ ][ ] C

iCii

iCii

iCiiC

FALLOCFEESOMALLOCOM

AALLOCDEPAALLOCASSETWACCNETWORK

×+×+

×+××=

∑

∑∑

,

,,

Where

• NETWORKC is the network cost allocated to Customer Group “C”, in million Ngultrum;

• WACC is the Weighted Average Cost of Capital for the Licensee, determined in accordance with Section 6.6 in the TDR, as a percentage.

• ASSETi is the net historical value of assets in asset category “i”, in million Ngultrum;

24

• DEPi is the depreciation allowance for assets in asset category “i”, in million Ngultrum;

• OMi is operating and maintenance allowance for cost category “i” , in million Ngultrum;

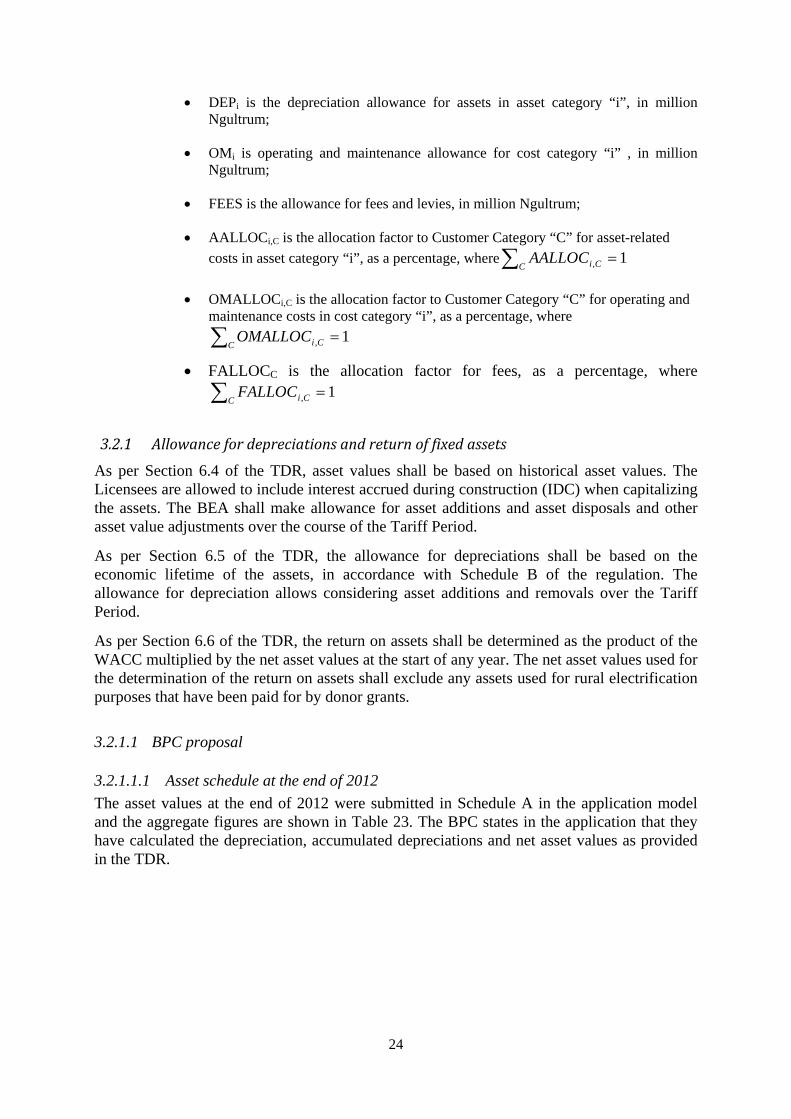

• FEES is the allowance for fees and levies, in million Ngultrum;

• AALLOCi,C is the allocation factor to Customer Category “C” for asset-related costs in asset category “i”, as a percentage, where∑ =

C CiAALLOC 1,

• OMALLOCi,C is the allocation factor to Customer Category “C” for operating and maintenance costs in cost category “i”, as a percentage, where

∑ =C CiOMALLOC 1,

• FALLOCC is the allocation factor for fees, as a percentage, where ∑ =

C CiFALLOC 1,

3.2.1 Allowance for depreciations and return of fixed assets

As per Section 6.4 of the TDR, asset values shall be based on historical asset values. The Licensees are allowed to include interest accrued during construction (IDC) when capitalizing the assets. The BEA shall make allowance for asset additions and asset disposals and other asset value adjustments over the course of the Tariff Period.

As per Section 6.5 of the TDR, the allowance for depreciations shall be based on the economic lifetime of the assets, in accordance with Schedule B of the regulation. The allowance for depreciation allows considering asset additions and removals over the Tariff Period.

As per Section 6.6 of the TDR, the return on assets shall be determined as the product of the WACC multiplied by the net asset values at the start of any year. The net asset values used for the determination of the return on assets shall exclude any assets used for rural electrification purposes that have been paid for by donor grants.

3.2.1.1 BPC proposal

3.2.1.1.1 Asset schedule at the end of 2012 The asset values at the end of 2012 were submitted in Schedule A in the application model and the aggregate figures are shown in Table 23. The BPC states in the application that they have calculated the depreciation, accumulated depreciations and net asset values as provided in the TDR.

25

Table 23 BPC’s proposed Non-granted assets at end of 2012 (Nu. mill)

Gross value Acc. Dep Net value Dep

Buildings & land 1,620.6 402.1 1,218.5 52.9

Generation 710.7 389.3 321.4 34.3

Transmission 7,462.0 1,495.2 5,966.8 233.5

Distribution 6,051.2 1,066.9 4,984.3 192.8

Vehicles 230.0 134.1 95.9 22.3

Office equipment 649.4 340.0 309.3 90.0

Tools 183.0 95.7 87.3 12.7

Total 16,906.8 3,923.3 12,983.5 638.5

BPC stated in their proposal that any grants received by the RGoB were passed on to BPC as equity, and their view was that none of their assets should be treated as granted. The figures in Table 23 therefore contain all fixed assets of BPC.

3.2.1 Investments

The proposed investment schedule is, according to the BPC, in line with BPC’s 5-year investment plan drawn for the period 2013-2017, which in turn is in line with the RGoB’s proposed 11th FYP for the energy sector in the country. The BCP states that the investments in the next five years are geared towards network augmentation to meet increased demand for power; renewal of ageing assets to deliver better reliability in the future and to meet safety requirements; and building transmission network for the evacuation of power from the upcoming hydropower projects. The programs have been divided into two major areas – “Plan works” and “Out of plan works”. The latter one will be taken up by BPC on behalf of others agencies, but these investments are not included in the submitted investments figures in the tariff application. The estimated total annual capital outlays in 2012 costs for BPC’s investments are shown in Table 24.

Table 24 BPC’s planned capital outlay for investments in Nu. Million. 2012 values.

2013 2014 2015 2016 2017 Total

”Plan works” outlay 2,406 3, 011 1,839 1,855 1,258 10,370

”Out of plan works” outlay 5,306 9 ,484 9,273 9,124 6,083 39,270

Total annual outlay 7,712 12,495 11,112 10,979 7,341 49,640

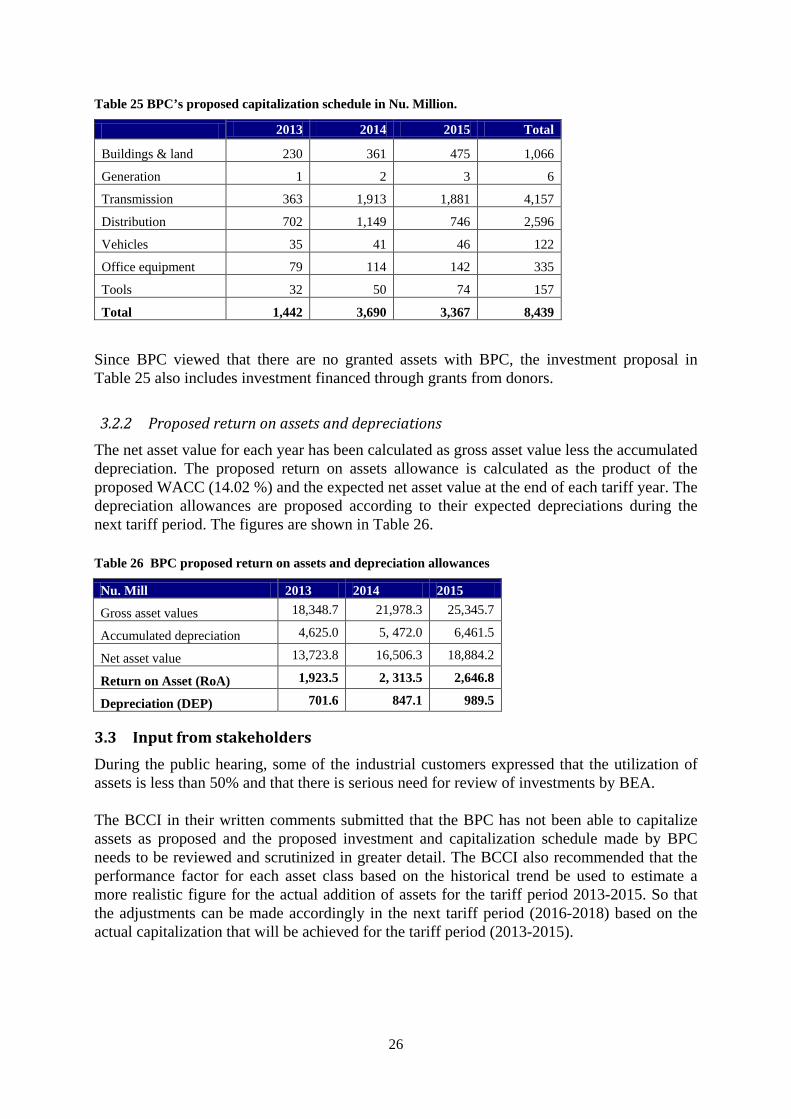

The investment schedule for the next tariff period as proposed by the BPC in the tariff application form is shown in Table 25. The total figures for 2014 and 2015 in the tariff application form are slightly different from the figures in BPC’s proposal write-up. The investments are the capitalized amounts of the “Plan works” outlays including IDC for the projects completed in each year. For calculation of IDC BPC used an interest rate of 13.32%. The figures are based on the BPC’s investment plan for the period 2013-2017, which are in 2012 values, and have been inflated to the different capitalization years using an annual inflation rate of 8.9%.

26

Table 25 BPC’s proposed capitalization schedule in Nu. Million.

2013 2014 2015 Total

Buildings & land 230 361 475 1,066

Generation 1 2 3 6

Transmission 363 1,913 1,881 4,157

Distribution 702 1,149 746 2,596

Vehicles 35 41 46 122

Office equipment 79 114 142 335

Tools 32 50 74 157

Total 1,442 3,690 3,367 8,439

Since BPC viewed that there are no granted assets with BPC, the investment proposal in Table 25 also includes investment financed through grants from donors.

3.2.2 Proposed return on assets and depreciations

The net asset value for each year has been calculated as gross asset value less the accumulated depreciation. The proposed return on assets allowance is calculated as the product of the proposed WACC (14.02 %) and the expected net asset value at the end of each tariff year. The depreciation allowances are proposed according to their expected depreciations during the next tariff period. The figures are shown in Table 26.

Table 26 BPC proposed return on assets and depreciation allowances

Nu. Mill 2013 2014 2015

Gross asset values 18,348.7 21,978.3 25,345.7

Accumulated depreciation 4,625.0 5, 472.0 6,461.5

Net asset value 13,723.8 16,506.3 18,884.2

Return on Asset (RoA) 1,923.5 2, 313.5 2,646.8

Depreciation (DEP) 701.6 847.1 989.5

3.3 Input from stakeholders During the public hearing, some of the industrial customers expressed that the utilization of assets is less than 50% and that there is serious need for review of investments by BEA. The BCCI in their written comments submitted that the BPC has not been able to capitalize assets as proposed and the proposed investment and capitalization schedule made by BPC needs to be reviewed and scrutinized in greater detail. The BCCI also recommended that the performance factor for each asset class based on the historical trend be used to estimate a more realistic figure for the actual addition of assets for the tariff period 2013-2015. So that the adjustments can be made accordingly in the next tariff period (2016-2018) based on the actual capitalization that will be achieved for the tariff period (2013-2015).

27

The BPC in their written comments submitted that the investment in T&D assets are mainly driven by the policies of RGoB for the energy sector in the country and all the investments are approved by the relevant departments like DHPS and DRE. The same, after being vetted by these departments, are put up to BEA for approval, before the same are implemented.

The BCCI in their written comments submitted that the depreciation that was approved by BEA for the last tariff period far exceeded the actual depreciation costs incurred by BPC. Accordingly, it is recommended that this over-recovery made by BPC needs to be adjusted in the forthcoming tariff period.

The BPC in their written comments submitted that the over recovery of depreciation as submitted by BCCI is not correct as it works out to Nu. 76.95 million only as per BPC. Further, BPC stated that there isn’t any such provision in the TDR 2010 that allows adjustment in the next tariff for the over or under recovery in the previous tariff period. If this be the case, BPC should rightfully be allowed for the under recovery on account of the estimation of the energy sales forecasts which was purely done on the basis of the contracted power withdrawal of the HV customers.

The BCCI also stated that the BPC’s proposal also includes a return on assets for granted assets that were provided by the Austrian Government for electrification of Phobjikha valley. It is accordingly recommended that the asset classes funded by the Austrian Government for rural electrification works in Phobjikha valley be adjusted in determining the tariff for 2013 to 2015.

3.4 BEA review

3.4.1 Asset schedule at the end of 2012

Since BPC was of the view that all its assets should be treated as equity, BPC sought the clarification on the treatment of the funds released for Rural Electrification from the Ministry of Economic Affairs (MoEA). The MoEA in turn sought clarification from the Ministry of Finance (MoF) on the subject. The MoF vide letter No. MoF/PED/30/2013/3497 dated May 20, 2013 clarified that assets acquired through grants maybe treated as capital reserve in the book of accounts and the capital cost recovery should be as per the BEA Tariff Determination Regulation.

Based on the clarification provided by the MoF, BPC has submitted gross and net asset values, accumulated and annual depreciation for the granted assets, as shown in Table 27. The BEA has shifted these values from non-granted assets to granted assets. These assets will therefore not contribute to any return on assets, as determined in section 6.6.2 in the TDR.

Table 27 Granted fixed assets at the end of 2012 (Nu. mill)

Gross value Acc. Dep. Net value Dep

RE Distribution 1,147.4 180.4 967.0 42.5

28

Table 28 BEA reviewed non-granted fixed assets at end of 2012 (Nu. mill)

Gross value Acc. Dep. Net value Dep

Buildings and land 1,620.6 402.1 1,218.5 52.9

Generation 710.7 389.3 321.4 34.3

Transmission 7,462.0 1,495.2 5,966.8 233.5

Distribution 4, 905.7 886.8 4,018.9 150.6

Vehicles 229.2 134.0 95.2 22.1

Office equipment 649.1 340.0 309.2 90.0

Tools 182.1 95.5 86.5 12.7

TOTAL 15 ,759.4 3 ,742.9 12,016.5 596.0

3.4.2 Investments

The BPC’s total budget requirement to implement the “Plan works” in the Five Year Investment Plan (2013 – 2017) amounts to Nu. 10,369 million (2012 figures). In addition the BPC is planning to undertake investments called “Out of plan works” for an amount of Nu. 39,270 million, but these investments are not included in BPC’s proposal.

The BPC has derived the investment schedule from the Investment Plan firstly by adding expected IDC to the debt drawdown amounts, secondly by capitalizing the estimated IDC and annual capital drawdown figures in the expected year of completion, thirdly by inflating the capitalized amounts from the start of the project to the year of capitalization. BPC used an inflation rate of 8.9 %, and an interest rate of 13.32%.

The BEA found that the treatment of capital work in progress (CWIP) at the end of 2012 was not clear. At the end of 2012 the CWIP balance of BPC was Nu. 6,665 million. Further, BEA found that capitalized amounts of granted assets had to be submitted separately. Due to the huge amount of proposed investments, the BEA found it necessary to go through the investment plan with the BPC project managers to evaluate the priorities, risks and status related to each project.

Due to these issues, a meeting was held at BPC office on11/07/2013. The BPC informed that they had not included the relevant CWIP balance in the investment schedule. Out of the CWIP balance of Nu. 6,665 million, Nu 3,445 million was related to “Plan works” and should have been included in the proposal. BPC expected to capitalize Nu. 2,483 million in 2013 and Nu. 962 million in 2014. During the meeting, BPC proposed to defer several of their investment by 1 to 2 years. On 16/07/2013 the BEA received new information about investments where capitalized CWIP was included, the investment schedule was updated according to the deferred investments, and the investments in granted assets were reported separately. After correcting some minor errors in the spreadsheet model submitted by BPC, BEA asked BPC to confirm that the new figures was in line with BPC’s investment schedule. BPC confirmed this on 17/07/2013. BPC’s updated investment schedule, including also 2016, is shown in Table 29 and

Table 30.

29

Table 29 Proposed capitalization of non-granted assets, in Nu. Mill.

2013 2014 2015 2016 Total

Buildings and land 498 361 475 198 1,532

Generation 19 2 3 3 27

Transmission 1,264 835 2,382 2,202 6,683

Distribution 1,833 1,565 462 535 4,394

Vehicles 35 41 46 53 175

Office equipment 112 150 509 245 1,015

Tools 43 62 87 111 303

TOTAL 3,805 3,015 3,963 3,346 14,129

Table 30 Proposed capitalization of granted assets, Nu. Mill.

2013 2014 2015 2016 Total

Distribution 255 474 - - 729

During the 2010 tariff review, the BEA found that the actual capital expenditures in 2008 and 2009 were less than 50% of the proposed amounts, and around 57% of the approved amounts. The actual capitalized amount in 2009 was around 41% of the proposed amount and 59% of the approved amount. During the review BPC expressed that it was more optimistic about the performance for the tariff period 2010/11-2012/13.

The BEA has compared the actual capitalization in the years 2010-2013 with the figures proposed by the BPC in 2010 and the reviewed figures used by the BEA when determining the tariffs for 2010/11-2012/13.

30

Table 31 Capitalized investments compared to BPC’s proposal and BEA’s review in 2010

2010 2011 2012 20135 Total Performance

Buildings & land (Nu. Mil) BPC Proposal 256 290 266 106 918 90%

BEA Review 178 200 181 71 630 131%

Annual accounts 201 214 143 264 822 Generation (Nu. Mil)

BPC Proposal 54 31 7 06 92 19%

BEA Review 48 27 6 0 82 22%

Annual accounts 0 -1 0 19 18 Transmission (Nu. Mil)

BPC Proposal 468 910 1,299 1, 688 4,365 45%

BEA Review 395 736 1,043 1,358 3,533 55%

Annual accounts 440 -54 760 800 1,947 Distribution (Nu. Mil)

BPC Proposal 2,655 626 2,033 2,690 8,004 58%

BEA Review 2,406 499 1,678 2, 417 6,999 67%

Annual accounts 230 1,560 1,018 1,855 4,663 Vehicles, office equipment and tools (Nu. Mil)

BPC Proposal 86 499 359 360 1, 304 52%

BEA Review 60 183 223 122 588 116%

Annual accounts 90 271 274 46 681 Total (Nu. Mil)

BPC Proposal 3,519 2,356 3,964 4,844 14,683 55%

BEA Review 3,086 1,645 3,131 3, 970 11,832 69%

Annual accounts 960 1,991 2,195 2,984 8,130

From the table above it is evident that the BPC’s proposed investment schedule has been far too optimistic in the tariff period 2010/11 – 2012/13 as it was in the previous tariff period. Therefore, the total cost of supply of BPC was estimated too high due to corresponding high provision for depreciations and return on assets. One might think that this also caused that the tariffs was determined too high. However, since the tariffs are estimated as the total cost of supply per customer group divided on total consumption per customer group (discounted values), also the consumption forecast errors must be taken into consideration.

The BEA has performed a rough assessment of the impact of the forecast errors on the tariffs by inserting the actual consumption, actual capitalized investments and average inflation of 8.9% in the tariff model from 2010. The LV consumption forecasts were quite good, whereas the HV and the MV were far too high. Since wheeling is estimated as the total generation less

5 The expected annual account figures for 2013 are based on the BEA’s review. Some of the figures BPC has proposed are higher. BPC proposed Nu. 498 million for buildings and land, Nu. 1,264 million for transmission, and Nu. 191 million for vehicles, office equipment and tools. In total BPC proposed Nu. 3,805 million to be capitalized in 2013, compared to the Nu. 2,984 million reviewed by the BEA. With BPC’s estimate the overall performance would be 76%, and for transmission 68%. 6 The figure is not including investments of Nu. 2,477 million in Druk Bindu and Begana hydroelectric projects proposed by BPC, but regarded as not relevant for the tariff review by the BEA.

31