beyond the imf - unctadunctad.org/en/docs/gdsmdpbg2420071_en.pdf · beyond the imf devesh kapur and...

TRANSCRIPT

G-24 Discussion Paper Series

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT

UNITED NATIONS

Beyond the IMF

Devesh Kapur and Richard Webb

No. 43, February 2007

G-24 Discussion Paper Series

Research papers for the Intergovernmental Group of Twenty-Fouron International Monetary Affairs and Development

UNITED NATIONSNew York and Geneva, February 2007

UNITED NATIONS CONFERENCEON TRADE AND DEVELOPMENT

INTERGOVERNMENTALGROUP OF TWENTY-FOUR

Note

Symbols of United Nations documents are composed of capitalletters combined with figures. Mention of such a symbol indicates areference to a United Nations document.

*

* *

The views expressed in this Series are those of the authors anddo not necessarily reflect the views of the UNCTAD secretariat. Thedesignations employed and the presentation of the material do notimply the expression of any opinion whatsoever on the part of theSecretariat of the United Nations concerning the legal status of anycountry, territory, city or area, or of its authorities, or concerning thedelimitation of its frontiers or boundaries.

*

* *

Material in this publication may be freely quoted; acknowl-edgement, however, is requested (including reference to the documentnumber). It would be appreciated if a copy of the publicationcontaining the quotation were sent to the Publications Assistant,Division on Globalization and Development Strategies, UNCTAD,Palais des Nations, CH-1211 Geneva 10.

UNITED NATIONS PUBLICATION

UNCTAD/GDS/MDPB/G24/2007/1

Copyright © United Nations, 2007

All rights reserved

iiiBeyond the IMF

PREFACE

The G-24 Discussion Paper Series is a collection of research papers preparedunder the UNCTAD Project of Technical Support to the Intergovernmental Group ofTwenty-Four on International Monetary Affairs and Development (G-24). The G-24was established in 1971 with a view to increasing the analytical capacity and thenegotiating strength of the developing countries in discussions and negotiations in theinternational financial institutions. The G-24 is the only formal developing-countrygrouping within the IMF and the World Bank. Its meetings are open to all developingcountries.

The G-24 Project, which is administered by UNCTAD’s Division on Globalizationand Development Strategies, aims at enhancing the understanding of policy makers indeveloping countries of the complex issues in the international monetary and financialsystem, and at raising awareness outside developing countries of the need to introducea development dimension into the discussion of international financial and institutionalreform.

The research papers are discussed among experts and policy makers at the meetingsof the G-24 Technical Group, and provide inputs to the meetings of the G-24 Ministersand Deputies in their preparations for negotiations and discussions in the framework ofthe IMF’s International Monetary and Financial Committee (formerly Interim Committee)and the Joint IMF/IBRD Development Committee, as well as in other forums.

The Project of Technical Support to the G-24 receives generous financial supportfrom the International Development Research Centre of Canada and contributions fromthe countries participating in the meetings of the G-24.

BEYOND THE IMF

Devesh Kapur

Director

Centre for the Advanced Study of IndiaUniversity of Pennsylvania

Richard Webb

Director

Centre for Economic Research University of San Martin de Porres, Lima

G-24 Discussion Paper No. 43

February 2007

viiBeyond the IMF

Abstract

A consensus has developed that the International Monetary Fund (IMF) is not fulfilling

its role, prompting multiple proposals for reform. However, this paper argues that the

focus on reform should be complemented with an exploration of alternatives outside the

IMF which hold the potential to not only give developing countries greater bargaining

leverage with the Fund but also, by increasing competition, spurring the institution to

better performance. The paper argues that most of the IMF’s functions are being carried

out in part through alternative institutional arrangements. It focuses in particular on

the insurance role of the Fund and argues that developing countries are developing

alternative insurance mechanisms, from a higher level of reserves, to regional co-

insurance facilities to remittances as a counter-cyclical source of foreign exchange.

The de facto exit of its clientele has been driven by the high political costs associated

with Fund borrowing and now poses unprecedented challenges for the Fund, in particular

pressures on its income. The paper argues for a rapid restructuring and significant cuts

of the Fund’s administrative budget with the budget savings instead directed to lower

the interest rates charged to borrowers.

ixBeyond the IMF

Table of contents

Page

Preface ............................................................................................................................................ iii

Abstract ........................................................................................................................................... vii

A. Introduction .............................................................................................................................. 1

B. The Fund’s declining relevance .............................................................................................. 2

C. Alternatives to the Fund .......................................................................................................... 3

1. Global financial stability ...................................................................................................... 3

2. Insurance role ....................................................................................................................... 5

D. Organizational changes ........................................................................................................... 9

E. Implications ............................................................................................................................ 10

F. Conclusion ............................................................................................................................... 11

Notes ........................................................................................................................................... 11

References ........................................................................................................................................... 12

Annex ........................................................................................................................................... 13

A. Introduction

The drift away from the Bretton Woods para-digm, of a world where financial markets arecoordinated and disciplined by a central multilat-eral institution, continues. Industrialized countrieslong since removed themselves from IMF tutoring.When it lost its essential purpose, the Fund survivedas a developmental institution, dedicated to the fi-nancial stability of developing countries, moreconcerned with domestic than with internationalpolicies, and even joining the poverty alleviationcrusade. During the last decade, however, emergingmarket countries are also drifting away from theFund, prepaying debts to the institution, rejectingthe Fund’s role as a debt arbiter, building up inter-national reserves, and above all, reforming domesticpolicies to lessen the risk of financial crisis and de-pendence on the IMF. At the same time, the Fundhas been losing its financial capacity to provideemergency funding, and its human capital compara-tive advantage as an adviser. The principal reactionto this erosion of the Fund’s role has been to call for

IMF reform. A succession of ingenious proposalshave been put forward, designed to seduce the Fund’smain shareholders into an acceptance of the key stepsrequired for reform – a surrender of voting powerand the creation of new funding for the institution.

We argue that the focus on reform – which mayor may not happen – should be complemented bygreater attention to the reasons for the exodus fromthe Fund. Starting with a checklist of core IMF func-tions, one would find examples of both marketmechanisms and government interventions that insome measure are acting as substitutes for the IMF,including functions such as crisis resolution, exchangerate management, financial policy coordination andsurveillance. At the same time, exit from the Fund isalso being driven by high borrowing costs for Fundresources, as market rates decline relative to Fundcharges. Behind that trend is a cost crunch in theinstitution. A shrinking customer base means fallingrevenues, yet the institution has refused to adjust bycutting its administrative expenses. One reason fora closer look at the factors that are reducing demand

BEYOND THE IMF*

Devesh Kapur and Richard Webb

* This work was carried out under the UNCTAD Project of Technical Assistance to the Intergovernmental Group of Twenty-Four on International Monetary Affairs and Development with the aid of a grant from the International Development ResearchCentre of Canada.

2 G-24 Discussion Paper Series, No. 43

for IMF services is to assess the significance of adiminished IMF. How effective are those alterna-tive mechanisms? To what extent does the absenceof an IMF mean a more dangerous world? Anotherreason for the examination proposed here is to iden-tify opportunities for intervention that would reducefinancial vulnerability, not through the Fund, but bystrengthening the market and governmental substi-tutes for the IMF. The paper focuses in particular onthe insurance role of the Fund and argues that de-veloping countries are adopting alternative insurancemechanisms, from a higher level of reserves to re-gional co-insurance facilities to remittances as acounter-cyclical source of foreign exchange.

B. The Fund’s declining relevance

Over the last two years, respected internationalfinance experts have stated that the IMF is rudder-less and ineffective (Eichengreen and El-Erian,2005), that it is suffering from an identity crisis(Truman, 2005b), waning influence (Truman, 2005b)and a reduced role, that it is on the brink of irrel-evance (Wolf, 2006), that, as a result, the worldeconomy basically is not managed at all (Williamson,2005), that the IMF has long since lost its role as theworld’s central banker (Abdelal, 2005), has lost sightof where it wants to go (Truman, 2005b), and suf-fers from a mismatch between aspirations andauthority and instruments, and that no single stepwill restore the Fund to its prior respected position(Truman, 2005a).

In most cases the statement was followed by acall for IMF reform, and often by specific reformproposals. For several years, the reform debate hasconcentrated the attention of the international financecommunity. Meanwhile, however, markets and gov-ernments and civil associations have been buildingalternative solutions to the various functional defi-cits that result from the lack of an effective IMF.

In the late 1990s, the Fund appeared to be atthe zenith of its influence. Its attempt in 1997 tochange the Articles of Agreement to make capitalaccount liberalization a formal goal, and its subse-quent role in the financial crisis that began in Asiain 1997–98 and spread to the Russian Federation andBrazil in 1998–99 gave the Fund an unprecedentedglobal role. New forays such as the Poverty Reduc-

tion and Growth Facility (PRGF) drew the institu-tion into core development issues hitherto thepreserve of the multilateral development banks.These initiatives, however, did not reverse the under-lying trend to irrelevance of the institution, and thePRGF may have turned out to be a Pyrrhic victory.

Today, the Fund’s future appears much bleaker.Not only is demand for its resources at a historiclow, but major borrowers are prepaying the institu-tion. In 2003, Thailand finished paying off its obli-gations two years ahead of schedule while in 2004the Russian Federation prepaid its $3.3 billion debtto the IMF. In December 2005 and January 2006,Argentina and Brazil announced their decision torepay their entire debt to the Fund ($15.5 billion inthe case of Brazil and $9.8 billion in the case of Ar-gentina). Pakistan, which owes $1.5 billion and iscurrently the third-largest debtor, has said that it isseeking to cut its dependence on the Fund; Ukraine,the fourth largest debtor, has declined any furtherassistance; and Serbia has announced that it wouldnot increase its borrowings. In fiscal year 2005, justsix countries had Stand-by Arrangements – the low-est number since 1975. The volume of lending re-bounded in the current fiscal year, but almost entirelydue to one country – a $10 billion loan package toTurkey.

One possible interpretation is that the currentdecline in the demand for Fund resources is part ofa cyclical process. Barry Eichengreen has pointedout that the Fund is “a rudderless ship in a sea ofliquidity”, suggesting that the Fund’s raison d’êtrehas not changed. However, it is worth contrastingthe global payment systems in the aftermath of the oilprice shocks of 1973–74 and 1979–80 with 2005–06.In stark contrast to the earlier two shocks, whichcreated major global disequilibria and led many de-veloping countries to avail of the Fund’s facilities,there is little demand this time around. To be sure,this reflects structural and epistemic changes in de-veloping countries, in which the Fund has played animportant role. Greater liquidity in capital marketshas given many middle-income developing countriesalternatives, while low interest rates have made newfinancial emergencies less likely.

But there is more to the story. The Fund nolonger has the mystique, and its imprimatur no longercarries the weight previously associated with theinstitution, despite the continuing appearance of anall-powerful and non-accountable institution.

3Beyond the IMF

For some time there has been a broad consen-sus on the need to reform the IMF. Ideas for reformcover virtually every aspect of the Fund, from itssurveillance role to its role in debt management andemergency lending, to the nature of its advice andthe functions it needs to add or discard to its gov-ernance (for a recent elaboration see Akyüz (2005),Bryant (2004), Woods (1998; 2005) and Buira(2005). However, there is little agreement when itcomes to the details of the reforms. In the past quar-ter century, developing countries have beenperiodically afflicted by financial crisis. Each flurryof activity has resulted in an expansion in the scaleand scope of Fund itself. Mervyn King has pointedout that, instead of significant reform, the Fund’sprincipal shareholders have merely ensured that theinstitution be allowed to “evolve through a series ofever more bland communiqués and meaninglessstatements” (King, 2006).

But today the Fund faces perhaps its gravestcrisis, the result not of opprobrium but of irrelevance.The realization that if the Fund is not “kept up-to-date ... [it] risk[s] suffering a lengthy senescence”(Wolf, 2006), may well prompt real reforms. How-ever, as this paper argues, while developing countriesshould continue to press for reforms, they shouldtake heed of just how little change has resulted frompast calls for reform. Consequently, they mustcomplement the focus on reform with exploringalternatives outside the IMF which could eventuallyincrease the bargaining power of developing coun-tries with the Fund, while at the same time spurringthe institution to better performance by empower-ing competitive alternatives.

C. Alternatives to the Fund

Several factors have contributed to the devel-opment of alternative and supplementary mecha-nisms to carry out particular IMF functions. Perhapsthe most important has been the rapid growth of fi-nancial markets, and especially bond markets, whichin turn has driven the expansion of institutions thatmonitor and carry out continuous market surveil-lance, notably rating agencies and other private andgovernmental institutions that track financial condi-tions. A second factor has been an equally impres-sive expansion in networking and local or regionalcooperation and integration. Bryant (2004) has

pointed to the “Multiplicity of institutional venues –consultative groups and international organizations– [that are] involved in surveillance of financialstandards and prudential oversight. Similarly hetero-geneous and complex institutions are involved in thenascent supranational surveillance of all other typesof economic policies” (Bryant, 2004: 10–11). Cerny(2002) makes a similar point, speaking of the “pri-vatization of transnational regulation” through theexpansion of “webs of governance”, of “epistemiccommunities”, and “multi-level governance” involv-ing government and private sectors and civil asso-ciations. The conception of a more flexible networkedworld order that uses both the traditional verticalinternational organizations and new, horizontal “in-stitutions of globalization” has also been exploredby Anne Marie Slaughter (2004). The third devel-opment, closely related to the above, has been mod-ern communications technology which has broughtabout a multiplication in the volume, access andspeed of information, enormously facilitating sur-veillance by non-official actors. These contextualtrends help to explain the specific mechanisms, dis-cussed below, that are being used to complement orsubstitute for particular IMF functions.

1. Global financial stability

a. Crisis resolution

Although the Fund has been a pivotal player inmany debt and financial crises during the 1980s andthe 1990s, it began to be seen by developing coun-tries less as an impartial referee than as a debt col-lector for private creditors. In the late 1990s, the Fundproposed sovereign debt restructuring mechanisms(SDRM). Even if the Fund had been successful, theSDRM would have had limited utility since debtflows were becoming a much smaller part of totalfinancial flows. In any event the SDRM did not goanywhere as the international community chose topursue a more market-driven approach through theuse of collective active clauses (CAC) in bond con-tracts. Neither debtors nor creditors appear enthusi-astic about the Fund’s role in restructuring underCACs. In the end, with the advice and market sound-ings of a private investment bank, Argentina made aunilateral offer which was substantially accepted bythe market (Simpson, 2006). As the Argentinean andRussian defaults have shown, countries have real-ized that rather than perennial rounds of debt restruc-

4 G-24 Discussion Paper Series, No. 43

turing with the IMF playing a central role, countriesmay be better off simply ignoring the Fund. The re-sults (at least till now) don’t seem to indicate thatthese countries are any worse off than if they hadelected to use the offices of the IMF.

b. Managing the international monetarysystem

The primary role of the Fund on exchange ratemanagement had vanished with the collapse of theBretton Woods system. Consequently, its originalmandate notwithstanding, the Fund has been muchmore voluble on its member countries’ fiscal poli-cies than their exchange rate policies. Althoughrecent G-7 communiqués have emphasized the im-portance of flexibility in exchange rate systems,countries continue to peg their exchange rates andthere is not much that the Fund has been able to doabout it.

Williamson (2005) has emphasized the need forthe Fund to act as a referee on disputes over exchangerates and called for the institution to develop a systemof reference exchange rates to prevent unsustainableglobal imbalances. He argues that such a systemwould help secure global policy consistency. Themain problem with these arguments is that the risksto global financial stability are from the systemicallyimportant countries and regions, such as global im-balances caused by the huge United States currentaccount deficit, China’s system of exchange ratemanagement, or Europe’s rigid labour and productmarkets. But these are the very actors on whom theFund has little influence and who are least likely toallow the Fund to constrain their autonomy. It isunclear why moving from the current ambiguousguidelines to more well-defined rules (through asystem of reference exchange rates) would resolvethe enforcement problem. That depends critically onthe confidence of players in the institution itself,which in turn is singularly dependent on a percep-tion of presumed neutrality and a referee role of theinstitution that few emerging markets are willing toaccept given the current governance structure of theIMF.

Indeed even the SDR as a notional unit of ex-change now faces competition. In spring 2006, theAsian Development Bank (ADB) is planning tolaunch a notional unit of exchange, called the AsianCurrency Unit (ACU), which would help track the

relative values of Asian currencies. Modelled on theEcu (the forerunner of the Euro), the ACU would becalculated using a basket of 13 regional currencies,weighted according to the size of each economy. TheACU would allow monitoring of both the collectivemovement of Asian currencies against major exter-nal currencies, such as the dollar and the Euro, aswell as the individual movement of each Asian cur-rency against the regional average. Small borrowersare also expected to issue bonds denominated inACUs (rather than the SDR).

c. Coordination role

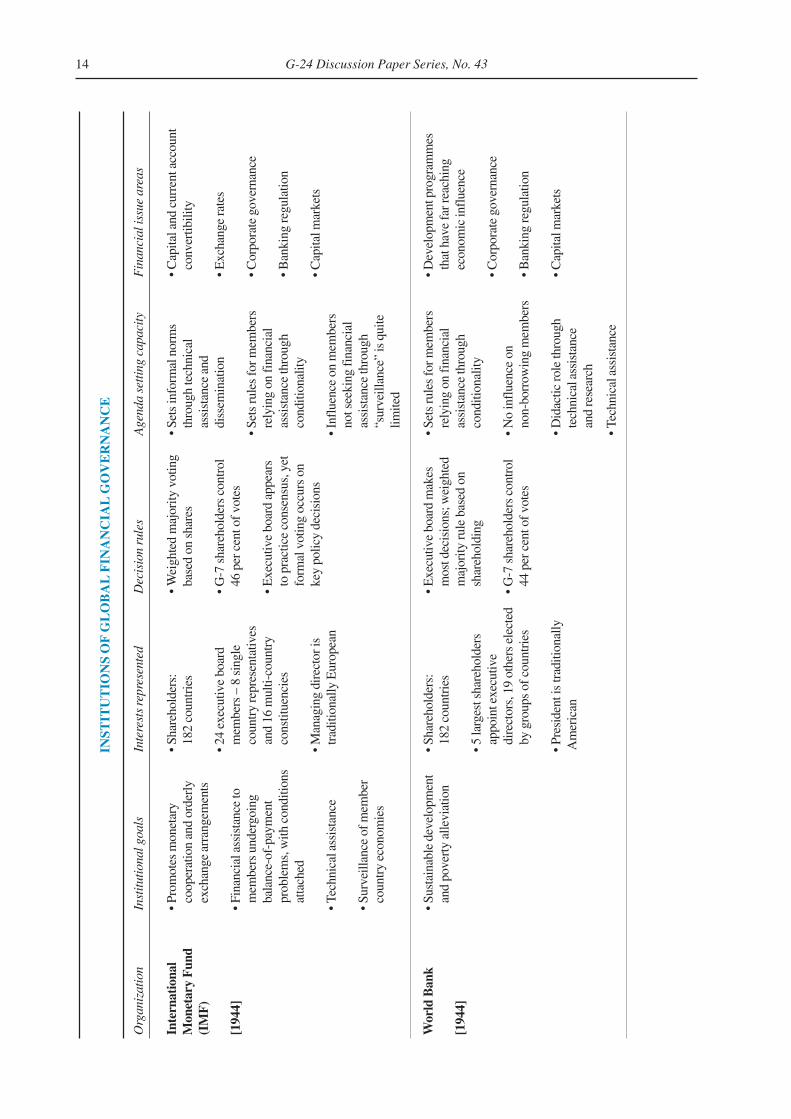

An important role of the Fund has been to func-tion as “a trusted, independent and expert secretariat”for policy makers around the globe. A very evidentsign of its failure (on perhaps all three attributes)has been the proliferation of alternatives. A varietyof institutional mechanisms are setting, interpreting,diffusing and enforcing rules on affecting global fi-nancial stability, ranging from purely governmentalto purely private, with complex public-private hy-brids added in. Ad hoc non-treaty intergovernmentalgroupings like the G-7, G-10, and G-20 are agendasetting and rule ratification institutions. Intergovern-mental organizations like the IMF, World Bank,International Finance Corporation (IFC), and Bankfor International Settlements (BIS) make some rules,but more importantly, serve as transmission and en-forcement mechanisms for rules developedelsewhere. Increasingly the rules underpinning glo-bal financial governance are being set by privateactors: the International Federation of Accountants(IFAC), Inter-Agency Standing Committee (IASC)and groupings of national regulatory institutions suchas International Organization of Securities Commis-sions (IOSCO) and International Association ofInsurance Supervisors (IAIS). The annex to this pa-per lists the goals, representation, decision rules, andagenda setting capacity of the principal institutionalunderpinnings of global financial governance.

Two features of this institutional mix are worthhighlighting. One, there is considerable variation informs of representation, goals, and authority. Two,there are overlapping jurisdictions in several areas,which is leading to the formation of “second gen-eration” emanation institutions (the Joint Forum onSupervision of financial conglomerates run jointlywith the Basle Committee on Banking Supervision,IOSCO and IASC, is an example). Developing coun-

5Beyond the IMF

tries should give greater emphasis to participatingin these multiple fora, rather than wringing theirhands about their marginalization in the Fund.

d. Surveillance function

Besides its insurance function (emergency lend-ing), surveillance has long been seen as the Fund’sother critical function. Compared to its early years,the very success of the Fund in ensuring greater trans-parency in countries’ macro accounts has meant that avariety of institutions (both private and public) play arole through their reports and analysis, which are simi-lar to those of the Fund. Moreover, a key weakness ofthe Fund’s surveillance is that issues in Article IVconsultations are negotiated ex ante with the sys-temically important countries, implying that the lat-ter exercise agenda control. The coverage of privaterating agencies has grown enormously, extending toboth sovereign and private debt, to most middle in-come countries and even many sub-Saharan nations.In addition to wide coverage and freedom from thepolitical inhibitions that limit the Fund, surveillancecarried out by the private sector is a source of fre-quent and up-to-date information, in contrast to therelative infrequency of Article IV consultationswhich occur only every 12–18 months and, in somecases, less frequently. The rating agencies have notimproved on the Fund’s prediction record, and,like the IMF, they can be suspected of conflict ofinterest, yet private surveillance is a growing indus-try.

Proposals to rescue Fund surveillance stress theneed to separate its surveillance and lending func-tions so as to avoid any perception of conflict ofinterest. The separation would apparently enhancethe independence and credibility of the Fund’s tech-nical judgment. However, enhanced surveillance ofthe global economy and a legal foundation for theinternational financial system require a tougher andmore independent role for the Fund, a delegation ofauthority that is not likely to be accepted by thenewly systemically important countries unless it istied to a fairer quota allocation.

Better surveillance could result if the Fund werereorganized to reflect the fact that much of what iscalled globalization is really regionalization. Tradeand exchange-rate policies are taking on an increas-ingly regional character, reflecting in part the factthat international trade has grown faster within re-

gions than between regions. The Fund could adoptan organizational structure akin to that of the Fed-eral Reserve System, with regional branches actingas the principal regional institutional mechanismsfor coordination and surveillance, leaving a smallercentral core to focus on global systemic issues.

2. Insurance role

For most developing countries, the Fund’s in-surance role – short-term balance-of-payments(BOP) support during times of crisis, when coun-tries cannot avail of any other sources of externalfinance – has been its most important function. Thatis when the Fund has most power, and where con-troversy over its use has been most manifest. Thus,finding alternatives to the Fund’s monopoly in thisarea will do more to change the relationship betweenthe IMF and developing countries than any other de-velopment.

Developing countries have several external fi-nancing options in the event of a balance-of-paymentscrisis. First, they could draw up credit lines on anongoing basis to preempt crises of illiquidity. Butthe volume depends on internal economic fundamen-tals, confidence in international markets, and thepredisposition of the G-7.1

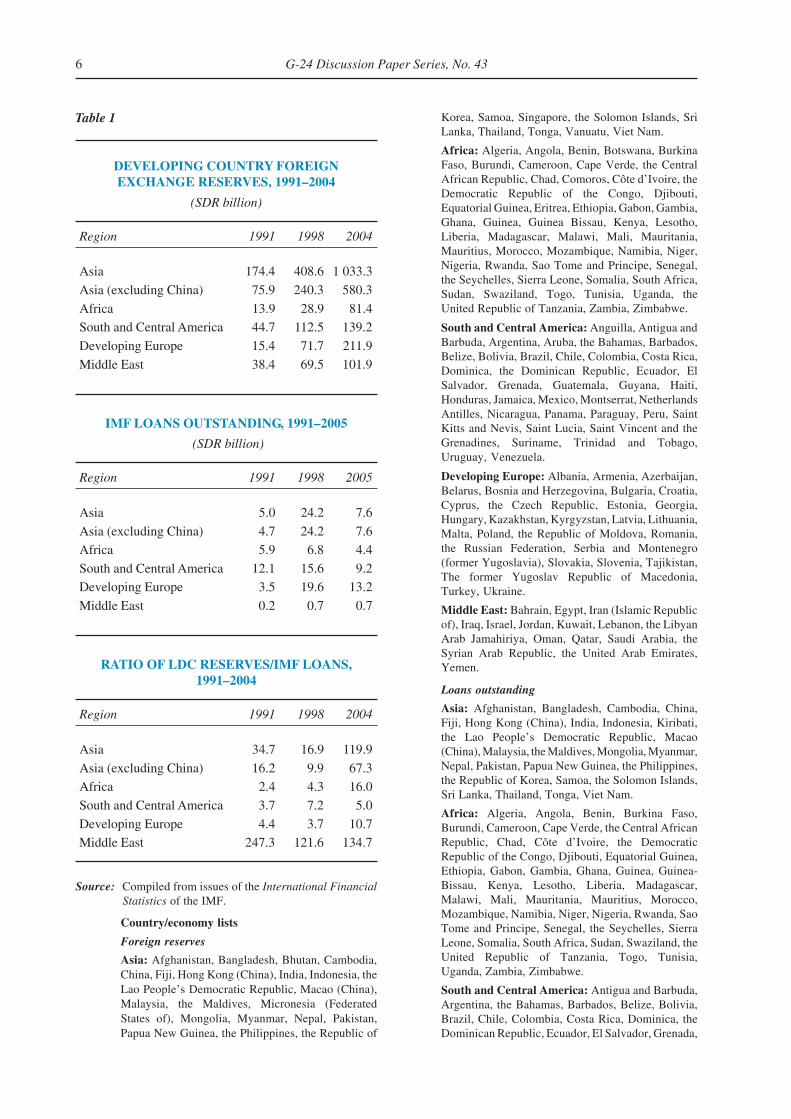

A second option is self-insurance. There are twomain possibilities here. The most obvious is thebuildup of reserves. Indeed the most significant signof dissatisfaction with the Fund is the very consciouschoice of developing countries to sharply increasetheir foreign exchange reserves in recent years (ta-ble 1). What is driving this? The demand for reservesis usually modelled on the lines of a buffer stockmodel, whereby the macroeconomic adjustmentcosts without reserves are balanced with the cost ofholding reserves. Another way of looking at a re-serve buildup is analogous to the precautionarymotive for savings traditionally put forward for ex-plaining individual consumption (and savings)behaviour (Aizenman and Lee, 2005). Kapur andPatel (2003), extend this line of thinking by stress-ing two additional factors: strategic considerationsarising from prevailing and likely geo-political re-alities, and the high prospective political price thatthe government of the day will have to pay if thecountry faces an external payments crisis (i.e. if thecountry runs out of foreign exchange reserves).

6 G-24 Discussion Paper Series, No. 43

Table 1

DEVELOPING COUNTRY FOREIGNEXCHANGE RESERVES, 1991–2004

(SDR billion)

Region 1991 1998 2004

Asia 174.4 408.6 1 033.3

Asia (excluding China) 75.9 240.3 580.3

Africa 13.9 28.9 81.4South and Central America 44.7 112.5 139.2

Developing Europe 15.4 71.7 211.9

Middle East 38.4 69.5 101.9

IMF LOANS OUTSTANDING, 1991–2005

(SDR billion)

Region 1991 1998 2005

Asia 5.0 24.2 7.6

Asia (excluding China) 4.7 24.2 7.6Africa 5.9 6.8 4.4

South and Central America 12.1 15.6 9.2Developing Europe 3.5 19.6 13.2

Middle East 0.2 0.7 0.7

RATIO OF LDC RESERVES/IMF LOANS,1991–2004

Region 1991 1998 2004

Asia 34.7 16.9 119.9

Asia (excluding China) 16.2 9.9 67.3Africa 2.4 4.3 16.0

South and Central America 3.7 7.2 5.0

Developing Europe 4.4 3.7 10.7Middle East 247.3 121.6 134.7

Source: Compiled from issues of the International FinancialStatistics of the IMF.

Country/economy lists

Foreign reserves

Asia: Afghanistan, Bangladesh, Bhutan, Cambodia,China, Fiji, Hong Kong (China), India, Indonesia, theLao People’s Democratic Republic, Macao (China),Malaysia, the Maldives, Micronesia (FederatedStates of), Mongolia, Myanmar, Nepal, Pakistan,Papua New Guinea, the Philippines, the Republic of

Korea, Samoa, Singapore, the Solomon Islands, SriLanka, Thailand, Tonga, Vanuatu, Viet Nam.

Africa: Algeria, Angola, Benin, Botswana, BurkinaFaso, Burundi, Cameroon, Cape Verde, the CentralAfrican Republic, Chad, Comoros, Côte d’Ivoire, theDemocratic Republic of the Congo, Djibouti,Equatorial Guinea, Eritrea, Ethiopia, Gabon, Gambia,Ghana, Guinea, Guinea Bissau, Kenya, Lesotho,Liberia, Madagascar, Malawi, Mali, Mauritania,Mauritius, Morocco, Mozambique, Namibia, Niger,Nigeria, Rwanda, Sao Tome and Principe, Senegal,the Seychelles, Sierra Leone, Somalia, South Africa,Sudan, Swaziland, Togo, Tunisia, Uganda, theUnited Republic of Tanzania, Zambia, Zimbabwe.

South and Central America: Anguilla, Antigua andBarbuda, Argentina, Aruba, the Bahamas, Barbados,Belize, Bolivia, Brazil, Chile, Colombia, Costa Rica,Dominica, the Dominican Republic, Ecuador, ElSalvador, Grenada, Guatemala, Guyana, Haiti,Honduras, Jamaica, Mexico, Montserrat, NetherlandsAntilles, Nicaragua, Panama, Paraguay, Peru, SaintKitts and Nevis, Saint Lucia, Saint Vincent and theGrenadines, Suriname, Trinidad and Tobago,Uruguay, Venezuela.

Developing Europe: Albania, Armenia, Azerbaijan,Belarus, Bosnia and Herzegovina, Bulgaria, Croatia,Cyprus, the Czech Republic, Estonia, Georgia,Hungary, Kazakhstan, Kyrgyzstan, Latvia, Lithuania,Malta, Poland, the Republic of Moldova, Romania,the Russian Federation, Serbia and Montenegro(former Yugoslavia), Slovakia, Slovenia, Tajikistan,The former Yugoslav Republic of Macedonia,Turkey, Ukraine.

Middle East: Bahrain, Egypt, Iran (Islamic Republicof), Iraq, Israel, Jordan, Kuwait, Lebanon, the LibyanArab Jamahiriya, Oman, Qatar, Saudi Arabia, theSyrian Arab Republic, the United Arab Emirates,Yemen.

Loans outstanding

Asia: Afghanistan, Bangladesh, Cambodia, China,Fiji, Hong Kong (China), India, Indonesia, Kiribati,the Lao People’s Democratic Republic, Macao(China), Malaysia, the Maldives, Mongolia, Myanmar,Nepal, Pakistan, Papua New Guinea, the Philippines,the Republic of Korea, Samoa, the Solomon Islands,Sri Lanka, Thailand, Tonga, Viet Nam.

Africa: Algeria, Angola, Benin, Burkina Faso,Burundi, Cameroon, Cape Verde, the Central AfricanRepublic, Chad, Côte d’Ivoire, the DemocraticRepublic of the Congo, Djibouti, Equatorial Guinea,Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea-Bissau, Kenya, Lesotho, Liberia, Madagascar,Malawi, Mali, Mauritania, Mauritius, Morocco,Mozambique, Namibia, Niger, Nigeria, Rwanda, SaoTome and Principe, Senegal, the Seychelles, SierraLeone, Somalia, South Africa, Sudan, Swaziland, theUnited Republic of Tanzania, Togo, Tunisia,Uganda, Zambia, Zimbabwe.

South and Central America: Antigua and Barbuda,Argentina, the Bahamas, Barbados, Belize, Bolivia,Brazil, Chile, Colombia, Costa Rica, Dominica, theDominican Republic, Ecuador, El Salvador, Grenada,

7Beyond the IMF

While in some cases (most notably in EastAsia), countries have been building up their reservesto prevent appreciation of their currency, in the vastmajority of cases the primary motive has been “self-insurance”. To guard themselves against externalshocks, developing countries can either seek somesort of joint insurance or attempt to obtain self-in-surance. The institutional mechanism for the formerhas been the IMF, and for the latter foreign exchangereserves. The trade off between the two has beenbetween political and financial costs. While borrow-ing from the Fund has lower financial costs, thepolitical costs have been high. As conditionalitiesmounted so did the political costs. In retrospect, theAsian financial crisis was the turning point. Policymakers are well aware of the humiliation heapedon East Asian economies in the course of their Fundprogrammes during the East Asian crisis from 1997–99.Although the Fund has changed tack since then, itsperceived lack of independence means that policymakers would be understandably risk-averse. De-veloping countries appear to be prepared to pay ahigh financial cost (estimated to be about one per-cent of GDP of developing countries taken as awhole) to preempt the prospect of a ruinous politi-cal cost (Rodrik, 2006).2

Thus, the high costs of holding reserves not-withstanding, they are still a more attractive optionrelative to availing of any contingent credit line, ei-ther from markets or the IMF. For one, the very actof securing contingent credit facilities may trigger adownward spiral of confidence that a governmentwould want to avoid in the first place. Moreover,once a crisis builds up it is exceedingly difficult toeither predict or control its momentum. High levelsof uncertainty enhance the case for the status quo

option (i.e. hold high reserves and pay a financialpremium). This is even more the case given currentgeopolitical realities where economic pressure,whether through international financial institutionsor on trade policies or even something as seeminglymundane as travel advisories, means a high level ofreserves is essential for a country to maintain policyautonomy. Large reserves also help to reassure for-eign investors that the likelihood of default on foreigncurrency denominated liabilities is extremely small.

For many poorer developing countries whoseexports are insufficient to build reserves, the needfor insurance has been reduced by growing cashflows from their citizens abroad. Remittances haveemerged as an important (in some cases, critical)source of financial flows for many developing coun-tries (figure 1). These flows come without a plethoraof conditionalities, are unrequited transfers (andtherefore do not require repayment), and increase intimes of shocks. They are allowing many develop-ing countries to cover their trade deficits andtherefore avoid the cycle of unsustainable externalborrowings to cover high current account deficits,thereby necessitating an IMF programme.

But a country’s diaspora can be a financial re-source not just through accretion in the currentaccount (in the form of remittances) but in the capi-tal account as well. For instance in 1998, when Indiafaced sanctions and global financial markets werein turmoil, the country raised $4.2 billion throughIndia Resurgent Bonds (IRBs) and again in 2000,apprehensive about its balance-of-payments pros-pects, India raised another $5.5 billion through theIndia Millennium Deposit (IMD) scheme. Whileboth issues (especially the latter) were expensive,they were much less costly than any other alternative.And the experience underscored a new possibility:a country with a large overseas diaspora could raisesignificant resources at relatively short notice, with-out having to go to the Fund. Nonetheless there areclear limits as to the amount of money that can beraised through this route.

Political motivations have also led to emer-gency financing between countries, as illustrated byVenezuela’s recent offer to Argentina to buy $3.4 bil-lion of Argentinean government bonds, of which$1.1 billion has been disbursed thus far. Similar fi-nancing has been a long established practice betweenoil-rich and needy Muslim nations in the Middle Eastand Africa.

Guatemala, Guyana, Haiti, Honduras, Jamaica,Mexico, Nicaragua, Panama, Paraguay, Peru, SaintKitts and Nevis, Saint Lucia, Saint Vincent and theGrenadines, Suriname, Trinidad and Tobago,Uruguay, Venezuela.

Developing Europe: Albania, Armenia, Azerbaijan,Belarus, Bosnia and Herzegovina, Bulgaria, Croatia,Cyprus, Czech Republic, Estonia, Georgia, Hungary,Kazakhstan, Kyrgyzstan, Latvia, Lithuania, Poland,the Republic of Moldova, Romania, the RussianFederation, Serbia and Montenegro (formerYugoslavia), Slovakia, Slovenia, Tajikistan, Theformer Yugoslav Republic of Macedonia, Turkey,Ukraine.

Middle East: Bahrain, Egypt, Iran (Islamic Republicof), Iraq, Israel, Jordan, the Syrian Arab Republic,Yemen.

8 G-24 Discussion Paper Series, No. 43

Developed countries had already developedself- and joint-insurance systems. It was the estab-lishment of the General Agreements to Borrow (theGAB) among the G-10 in 1964 that undermined theFund’s raison d’être for the industrialized countries.Following the onset of the Asian crisis, the UnitedStates shot down the idea of an Asian MonetaryAuthority and severely criticized the Asian Devel-opment Bank when it attempted to adopt a positiondifferent from the prescriptions of the IMF. In thelast few years Asian countries have renewed effortsat establishing swap facilities between the region’scentral banks to pool resources against a specula-tive attack (under the so-called Chiang MaiInitiative), and efforts to develop a region-wide mar-ket for local currency bonds. In the medium-term,the swap arrangements (now around $70 billion) posea singular challenge to the Fund. If growing coopera-tion among central banks in the region (exemplifiedby central bank swap facilities) leads to an Asianequivalent of a GAB, the Fund’s importance to theregion will diminish for the same reason that it hasall but disappeared in the industrialized countries.

The strong development of regional monetaryand financial arrangements has been pointed out byHenning (2005) and Cohen (2003). “Cohen counts

four full-fledged monetary unions, involving 37 coun-tries, thirteen fully dollarized countries, five near-dollarized countries, and ten bimonetary countries”(Henning, 2005: 1). Henning also notes that the Ex-change Stabilization Fund of the United States hasentered into nearly 120 agreements since its intro-duction in 1934.

Some developing countries are seeking insur-ance by coming under the umbrella of a major power.The EU will effectively provide insurance for newCentral and East European members through theERM2. The liquidity provided to these countries willcome from the European Central Bank rather thanfrom the IMF.

The Cold War powerfully shaped the lendingof the Bretton Woods Institutions in two distinctways. First, the prospect of a country turning to theSoviet Bloc made the market for lending contestable.Second, allies of major shareholders could alwaysexpect their economic transgressions to face less op-probrium. For a while the collapse of the Soviet Unionseemed to remove any political competition, but thewar on terrorism and the rise of China has changedthat. In Asia, Africa, and Latin America, China hasmounted a charm offensive, with economic deals that

Figure 1

GROWING IMPORTANCE OF REMITTANCES

Number of countries where remittances are greater than:

0

20

40

60

80

100

120

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Num

ber

of c

ount

ries Trade deficit

Net private capital inflows

Net official development assistance

9Beyond the IMF

eschew advice and hectoring. Its demand for rawmaterials from the latter two regions in particularhas fuelled a new commodity boom and led Chinato stake strategic partnerships. China’s volume oftrade with Africa has quadrupled in the past five years(to reach about $37 billion).3 And the pragmaticChinese policies are a much less constraining phi-losophy than that of the Fund’s major shareholders.Thus, even as Zimbabwe defaulted on its obligationsto the Fund, Beijing rolled out the red carpet forPresident Mugabe.

Table 2 summarizes the variety of mechanismsreviewed above that supplement the IMF or reducethe demand for insurance, and points out the princi-pal mechanisms used in each region.

D. Organizational changes

The drift away from the Fund is also a conse-quence of the growing access by emerging marketsto private finance and the rising relative cost of Fundloans. At the same time, the Fund is not respondingto the loss of competitive advantage by reducing itsadministrative expenses. The resulting de facto exitof its clientele, driven by the combination of highpolitical costs associated with Fund borrowing andgrowing availability of alternatives, now poses anunprecedented challenge for the Fund, in particularpressures on its income. This paper examines theoptions available to the Fund if it is to reverse itsloss of clientele.

In particular, in addition to governance reform,the Fund’s future seems to require significant cutsin its administrative budget, using budget savings tolower borrower interest rates. The recent decisionof Argentina and Brazil to prepay their IMF debtshas meant that the Fund income will decline by$116 million in 2006. Apart from a short period in1990, the IMF’s loan book is at its lowest in the pastquarter century. One option that the Fund is consider-ing to augment its shrinking income is a proposal toinvest some of its reserves in higher yielding longer-term securities, while another option would find away to generate income from its gold holdings.

One alternative that does not seem to be on thecards is to cut the Fund’s administrative expenses.The Fund like the IBRD is cost-plus lender and there-

fore has had little incentive to make the sorts of hardchoices that are forced on its clients. In recent years,the cost of borrowing has increased and along withhigh administrative expenditures, the financial costsof IMF loans are high. When added to the politicalcosts, it is hardly surprising, therefore, that coun-tries are prepaying loans.

Unlike the Bank, which has undergone severalmajor and wrenching organizational changes, theFund has enjoyed a charmed existence. The onlyfundamental reform occurred in the aftermath of thecollapse of the Bretton Woods system in the early1970s, but even that had very modest organizationaleffects. However, as discussion above has sought todemonstrate, the Fund’s current financial situationis not the result of temporary circumstances, but isbeing driven instead by longer-term structural fac-tors. The income pressures facing the Fund will notbe resolved by tinkering with the budget. The un-derlying cause of this predicament is that the Fundis losing rents that it enjoyed as a monopolist, butwhich are dissipating as alternative sources of in-surance and counter-cyclical flows become availableto developing countries. Consequently, the revenueshortfalls facing the Fund are of a more permanentnature than the management appears willing toacknowledge. We believe that the Fund has little

Table 2

ALTERNATE RISK MANAGEMENTMECHANISMS FOR LDCs

Region Insurance mechanism

Central America(incl. Mexico) Remittances

East Asia Reserves, swap facilities

East Europe ECB (through EU membership)

Latin America Reserves

Middle East andNorth Africa Remittances

Russian Federation Reserves

South Asia Remittances, reserves

Sub-Saharan Africa Assistance from Asia

10 G-24 Discussion Paper Series, No. 43

alternative but to swallow some if its own medicine,tightening its belt and reducing administrative ex-penditures. We believe there is considerable scopefor doing that, though the Fund’s recent strategicreview avoided any serious consideration of thematter. The standard cost-cutting steps required areto overhaul compensation policies, develop moreflexible (internal) labour markets, greater decentrali-zation and outsourcing to lower cost locations.

The biggest anomaly in the Fund’s compensa-tion is its pensions. The anomaly is both in terms oflevel and structure. On level, a comparison of thepension of the median Fund staffer with other com-parable places (e.g. universities) is revealing of theextent to which the Fund has gone overboard. It issimply over the top. The present value of the pen-sion due to a Fund staffer who retires at B3–B4 levelafter about 25 years at the Fund is about $5–6 mil-lion.

Even as the Fund’s advice recommends thatcountries move from defined benefit-regime to de-fined contribution-system, its own compensationpolicy remains wedded to a defined benefit pensionsystem, one of the last bastions in the world. Evenworse, the defined benefits are linked to a staffer’slast three years salary, a perverse incentive from thepoint of view of another favourite Fund recommen-dation, labour market flexibility. Its pension systemactually encourages immobility because pensionsincrease disproportionately with years of service: infact there are two major career kinks, when the pen-sion jumps discontinuously, so a staffer within sightof these kinks simply drops anchor. The Fund’s jus-tifies this policy with references to the importanceof factors such as experience and institutionalmemory. The Fund, however, stands out from otherorganizations that require similar skills.

A second problem with the Fund’s compensa-tion policies is wage compression. The Fund’sstandard prescription is to argue for wage decom-pression to allow more flexibility to hire staff withspecial skills, especially at senior levels. Sadly, heretoo the Fund has failed to follow its own advice.Unlike most of its member states, senior Fund staffis well compensated. The wage compression arisesfrom the fact that junior staff is compensated muchtoo handsomely, especially when one adds in mu-nificent expatriate benefits: home leave, education,the G-5; (ability to “import” domestic help and pen-sions). These high salaries do not compensate for

greater risk, since it is virtually impossible to bedownsized from the Fund.

A third issue is the need for greater transpar-ency in salary structure. IMF staff receives a rangeof benefits in non-monetized form from educationfor children to home leave travel allowances. TheFund’s message to its civil service clients aroundthe world has been a consistent one – monetize allbenefits so that they are clear and transparent. A com-parison of lower level total emoluments (includingthe present value of pension liabilities), with his/hercounterpart in comparable private/public institutionswould be telling.

Developing countries have a strong interest inpushing for organizational changes in the Fund, andin particular a major overhaul of the Fund’s person-nel and compensation policies, in line with what theinstitution advocates everyone else. Since personnelexpenses amount to about 70 per cent of the Fund’sbudget (which is approaching nearly $900 million),there is simply no alternative but to address the sizeof staff and the structure of compensation. Recentattempts to reform the Fund’s pension plan werescuttled when Executive Directors from some indus-trialized countries bowed to pressure from staff.4

These countries feel that few nationals from theircountries would be willing to join the Fund if thecompensation package were less attractive. Currentpolicy, however, means that developing countries aresubsidizing the ability of rich countries to have na-tionals on the staff.

E. Implications

The lack of voice in the IMF has been a peren-nial complaint of developing countries. CurrentlyEurope (including the Russian Federation) accountsfor 40 per cent of the IMF’s voting share and up to10 of the 24 seats on the Executive Board. Japan,China and India and other East Asian countries ac-count for only 16 per cent of the vote share and5 chairs. Current discussions indicate that Europemight be willing to give up 2 per cent of its voteshare (and perhaps one seat), which will do little toaddress the structural imbalance.

However, as Hirschman has pointed out,“voice” is not the sole source of legitimacy for an

11Beyond the IMF

organization. If membership is voluntary, and “exit”does not impose onerous costs, then governance byvoice is not necessary for legitimacy. Private firmsare not democratic but nonetheless enjoy societallegitimacy when factor and product markets are com-petitive, since competition gives both input suppliersand output buyers exit options. Even where factorand product markets are not competitive, legitimacycan exist if markets are “contestable” (that is, entrycosts are low), or where viable anti-trust and regu-latory institutions exist.

Consequently the possibility of exit even in theabsence of voice could give the Fund greater legiti-macy. Unfortunately, for virtually all developingcountries exit was not a viable option. The “market”for international organizations is, for the most part,not contestable except in the few areas where bothregional and global institutions exist. Thus in devel-opment projects borrowers had some choice betweena regional development bank, the World Bank, and(to varying degrees) the private sector. In some casescountries can engage in forum-shopping – for in-stance Canada, Mexico and the United Nations canchose between the North American Free TradeAgreement (NAFTA) and the World Trade Organi-zation (WTO) dispute settlement mechanisms incases of trade dispute resolution. But in many im-portant areas this has not been true, especially in thecase of functions and services supplies by the IMF –until now.

Among the public goods that the Fund provides,including information, analysis, advice to individualgovernments, advice on co-ordination of policies,management of defaults and emergency lending,viable alternatives now exist for many more devel-oping countries than ever before.

F. Conclusion

We find a variety of initiatives and develop-ments outside the Fund that complement or supple-ment the IMF’s financial coordination, insurance andsurveillance functions. It seems highly likely thatthe cumulative effect of those initiatives has been,in some degree, to reduce the risk and potential costsof financial instability, in short, to make the worldsafer, though it is difficult to arrive at a more preciseassessment due to the lack of systematic data, to the

heterogeneous nature of the initiatives, and to thefact that many have an informal character. However,the evidence suggests a growing trend that is drivenboth by the growth and diversification of financialmarkets, and by the increasing complexity of globaland national governance. A September 2004 reportto the IMF Board, The Fund’s Strategic Direction,opens with a reference to the “tectonic shifts in theground the IMF is directed to tend”, and acknowl-edging that “in some important measures, the Fundhas lagged rather than led” (IMF, 2004). Those lagsare part of the explanation for the surge in non-Fundinitiatives aimed at reducing financial vulnerability,whether as a direct intent, as in the case of regionalinsurance arrangements, higher reserve holdings, andincreased market-based surveillance, or as an indi-rect effect of other governance objectives, especiallythe rapid growth of bilateral and regional trade agree-ments. However, this paper has argued that the re-sort to non-Fund alternatives is also driven in partby the increasing cost of Fund resources, largelyexplained by its very high administrative budget.

Further analysis is needed to explore the ex-tent to which these developments can be integratedinto a new model for the management of financialinstability in the world, a model that will comple-ment the centralized decision and rule-makingcapacities of an IMF with the more flexible, and moreparticipatory, decentralized governance that is be-ing generated through the combined action ofnational governments, regional arrangements, mar-ket institutions, and civil associations.

Notes

1 In 1995, in the aftermath of Mexico’s crash Argentinafaced a liquidity crisis and entered into $6.7 billion worthof “reverse repo” arrangements with 14 internationalbanks that gave it access to liquidity in the event of asudden large capital flight. The banks charged Argen-tina a fee together with Argentine bonds as collateral.

2 Generally these costs are calculated as the difference be-tween short term borrowing abroad and yield of liquidforeign assets (e.g. the United States Treasuries) in whichreserves are usually invested. One puzzle (highlightedby Rodrik) is why countries in their quest to insulatethemselves from financial crises choose to increase theirforeign reserves rather than reduce their short term li-abilities. Rodrik notes that developing countries have re-sorted to the former but the optimal solution is in fact acombination of the two measures. This would not onlydecrease this social cost of holding excess foreign re-

12 G-24 Discussion Paper Series, No. 43

serves, but also increase liquidity to respond to externalshocks. The issue is also examined by Aizenman andMarion (2004).

3 Details of official Chinese policy can be found in “Chi-na’s African Policy”. The so-called “Five Principles ofPeaceful Co-existence” enshrine mutual territorial re-spect, non-aggression and non-interference in each oth-er’s internal affairs The white paper promises that theChinese Government will now “vigorously encourage”Chinese enterprises to take part in building African in-frastructure and help Africa to build its own capacity.

4 The IMF can learn a little from its sister institution, theWorld Bank, which moved toward defined contributionpension schemes and more transparent, monetized ben-efits since 1997.

References

Abdelal R (2005). Comment at IIE Conference on IMF Re-form. 23 September.

Aizenman J and Lee J (2005). International Reserves: Precau-tionary versus Mercantilist Views, Theory and Evidence.NBER Working Paper, 11366. Cambridge, MA, NationalBureau of Economic Research (NBER).

Aizenman J and Marion N (2004). International Reserve Hold-ings with Sovereign Risk and Costly Tax Collection. TheEconomic Journal, 114: 497. Oxford, UK, July.

Akyüz Y (2005). Reforming the IMF: Back to the DrawingBoard, G-24 Discussion Paper, 38. New York and Ge-neva, United Nations Conference on Trade and Devel-opment (UNCTAD).

Bryant RC (2004). Crisis Prevention and Prosperity Manage-ment for the World Economy. Washington, DC, TheBrookings Institution.

Buira A (2005). The Bretton Woods Institutions: Governancewithout Legitimacy? In: Buira A, ed. Reforming theGovernance of the IMF and the World Bank. London,Anthem Press: 7–44.

Cerny PG (2002). Globalizing the Policy Process: From IronTriangles to Golden Pentangles? Manchester Papers inPolitics: CIP Series 7/2002. Manchester, UK, March.

Cohen B (2003). Monetary Governance in a World of RegionalCurrencies. In: Kahler M and Lake DA, eds. Govern-ance in a Global Economy: Political Authority in Tran-sition. Princeton, NJ, Princeton University Press.

Eichengreen B and El-Erian M (2005). Comments by BarryEichengreen and Mohammed El-Erian, Conference onIMF Reform, Institute for International Economics, Sep-tember, cited in IMF Survey, October: 305.

Henning RC (2005). Regional Arrangements and the IMF. Pa-per prepared for the Conference on Reform of the Inter-national Monetary Fund. Washington, DC, AmericanUniversity, Institute for International Economics, Sep-tember.

IMF (2004). The Fund’s Strategic Direction – PreliminaryConsiderations. Report by The Secretary to the Interna-tional Monetary Committee on the Fund’s Strategic Di-rection, 30 September: 2.

Kapur D and Patel U (2003). Large foreign currency reserves:Insurance for domestic weaknesses and external uncer-tainties? Economic and Political Weekly, XXXVIII (11).15–21 March: 1047–1053.

King M (2006). Governor, Bank of England, quoted in Finan-cial Times, 21 February.

Rodrik D (2006). The Social Cost of Foreign Exchange Re-serves. NBER Working Paper, 11952. Cambridge, MA,National Bureau of Economic Research.

Simpson L (2006). Role of the IMF in Debt Restructuring: LIAPolicy, Moral Hazard, and Sustainability Concerns. Pa-per prepared for the Technical Group Meeting of G-24.Geneva, 16–17 March: 12–17, 36–37.

Slaughter AM (2004). A New World Order. Princeton, NJ,Princeton University Press.

Truman T (2005a). Background paper prepared for the IIEConference on IMF Reform. 23 September: 1.

Truman T (2005b). Interview in Finance and Development.31 October: 321.

Williamson J (2005). Reforms to the International MonetarySystem to Prevent Unsustainable Global Imbalances. In:The International Monetary Fund in the 21st Century:Interim Report of the International Monetary Conven-tion Project. Switzerland, World Economic Forum: 22.

Wolf M (2006). The world needs a tough and independentmonetary Fund. Financial Times, 22 February.

Woods N (1998). Governance in international organizations:The case for reform in the Bretton Woods institutions.In: UNCTAD, International Monetary and Financial Is-sues for the 1990s, Vol. IX. United Nations publication,sales no. E.98.II.D.3. New York and Geneva.

Woods N (2005). Making the IMF More Accountable. In: BuiraA, ed. Reforming the Governance of the IMF and theWorld Bank. London: Anthem Press: 149–170.

13Beyond the IMF

ANNEX

14 G-24 Discussion Paper Series, No. 43

INST

ITU

TIO

NS

OF

GL

OB

AL

FIN

AN

CIA

L G

OV

ER

NA

NC

E

Org

aniz

atio

nIn

stitu

tiona

l goa

lsIn

tere

sts r

epre

sent

edD

ecis

ion

rule

sA

gend

a se

tting

cap

acity

Fin

anci

al is

sue

area

s

Inte

rnat

iona

l•

Prom

otes

mon

etar

y•

Shar

ehol

ders

:•

Wei

ghte

d m

ajor

ity v

otin

g•

Sets

info

rmal

nor

ms

•C

apita

l and

cur

rent

acc

ount

Mon

etar

y F

und

coop

erat

ion

and

orde

rly

182

coun

trie

sba

sed

on s

hare

sth

roug

h te

chni

cal

conv

ertib

ility

(IM

F)

exch

ange

arr

ange

men

tsas

sist

ance

and

•24

exe

cutiv

e bo

ard

•G

-7 s

hare

hold

ers

cont

rol

diss

emin

atio

n•

Exc

hang

e ra

tes

[194

4]•

Fina

ncia

l ass

ista

nce

tom

embe

rs –

8 s

ingl

e46

per

cen

t of v

otes

mem

bers

und

ergo

ing

coun

try

repr

esen

tativ

es•

Sets

rule

s fo

r mem

bers

•C

orpo

rate

gov

erna

nce

bala

nce-

of-p

aym

ent

and

16 m

ulti-

coun

try

•E

xecu

tive

boar

d ap

pear

sre

lyin

g on

fina

ncia

lpr

oble

ms,

with

con

ditio

nsco

nstit

uenc

ies

to p

ract

ice

cons

ensu

s, y

etas

sist

ance

thro

ugh

•B

anki

ng re

gula

tion

atta

ched

form

al v

otin

g oc

curs

on

cond

ition

ality

•M

anag

ing

dire

ctor

iske

y po

licy

deci

sion

s•

Cap

ital m

arke

ts•

Tech

nica

l ass

ista

nce

trad

ition

ally

Eur

opea

n•

Infl

uenc

e on

mem

bers

not s

eeki

ng fi

nanc

ial

•Su

rvei

llanc

e of

mem

ber

assi

stan

ce th

roug

hco

untr

y ec

onom

ies

“sur

veill

ance

” is

qui

telim

ited

Wor

ld B

ank

•Su

stai

nabl

e de

velo

pmen

t•

Shar

ehol

ders

:•

Exe

cutiv

e bo

ard

mak

es•

Sets

rule

s fo

r mem

bers

•D

evel

opm

ent p

rogr

amm

esan

d po

vert

y al

levi

atio

n18

2 co

untr

ies

mos

t dec

isio

ns; w

eigh

ted

rely

ing

on fi

nanc

ial

that

hav

e fa

r rea

chin

g[1

944]

maj

ority

rule

bas

ed o

nas

sist

ance

thro

ugh

econ

omic

infl

uenc

e•

5 la

rges

t sha

reho

lder

ssh

areh

oldi

ngco

nditi

onal

ityap

poin

t exe

cutiv

e•

Cor

pora

te g

over

nanc

edi

rect

ors,

19

othe

rs e

lect

ed•

G-7

sha

reho

lder

s co

ntro

l•

No

infl

uenc

e on

by g

roup

s of

cou

ntri

es44

per

cen

t of v

otes

non-

borr

owin

g m

embe

rs•

Ban

king

regu

latio

n

•Pr

esid

ent i

s tr

aditi

onal

ly•

Did

actic

role

thro

ugh

•C

apita

l mar

kets

Am

eric

ante

chni

cal a

ssis

tanc

ean

d re

sear

ch

•Te

chni

cal a

ssis

tanc

e

15Beyond the IMF

INST

ITU

TIO

NS

OF

GL

OB

AL

FIN

AN

CIA

L G

OV

ER

NA

NC

E (

cont

inue

d)

Org

aniz

atio

nIn

stitu

tiona

l goa

lsIn

tere

sts r

epre

sent

edD

ecis

ion

rule

sA

gend

a se

tting

cap

acity

Fin

anci

al is

sue

area

s

Inte

rnat

iona

l•

Supe

rvis

e m

anag

emen

t•

Sam

e as

Exe

cutiv

e B

oard

•C

onse

nsus

but

wei

ghte

d•

Adj

ustm

ent p

roce

ss•

Inte

rnal

mon

etar

y sy

stem

Mon

etar

y an

dan

d ad

apta

tion

of in

ter-

of th

e IM

Fin

favo

ur o

f G-7

Fin

anci

alna

tiona

l mon

etar

y an

d•

Glo

bal l

iqui

dity

•Sy

stem

ic c

risi

sC

omm

itte

efi

nanc

ial s

yste

m(f

orm

erly

Int

erim

•IM

F po

licie

sC

omm

itte

e )

[199

9]

Inte

rnat

iona

l•

Loa

n an

d eq

uity

•Sh

areh

olde

rs:

•B

oard

of D

irec

tors

•C

apita

l Mar

ket D

evel

opm

ent

Fin

ance

fina

ncin

g fo

r pri

vate

174

coun

trie

sco

mpo

sed

of W

orld

Ban

kC

orpo

rati

on (I

FC

)se

ctor

pro

ject

s in

Exe

cutiv

e D

irec

tors

•In

vest

men

t pol

icie

s,(A

ffili

ate

ofde

velo

ping

cou

ntri

eses

peci

ally

FD

IW

orld

Ban

k)•

Wei

ghte

d m

ajor

ity ru

le;

•A

dvis

ory

and

tech

nica

lG

-7 s

hare

hold

ers

cont

rol

•C

orpo

rate

gov

erna

nce

[195

6]as

sist

ance

for b

usin

ess

52 p

er c

ent o

f vot

e (t

hean

d go

vern

men

tU

nite

d St

ates

con

trol

s24

per

cen

t)

Ban

k of

•Fo

rum

of c

entr

al b

anke

rs•

Unt

il ea

rly

1990

s•

Boa

rd o

f Dir

ecto

rs:

•Se

ts s

tand

ards

for

•B

anki

ng s

tand

ards

and

Inte

rnat

iona

lfo

r int

erna

tiona

l mon

etar

y11

cou

ntri

es fr

om G

-10

21 m

embe

rs. 2

eac

h fr

omin

dust

rial

ized

sta

tes

regu

latio

n (B

asel

sta

ndar

ds)

Sett

lem

ents

(BIS

)an

d fi

nanc

ial c

oope

ratio

n,(i

ndus

tria

lized

sta

tes)

Bel

gium

, Ita

ly, F

ranc

e,fi

nanc

ial s

ervi

ces

for

Ger

man

y, th

e U

nite

d•

The

se s

tand

ards

bec

ome

•C

orpo

rate

gov

erna

nce

[193

0]ce

ntra

l ban

ks•

Maj

or e

xpan

sion

in 1

999

Kin

gdom

and

the

Uni

ted

the

yard

stic

k fo

r all

othe

rto

incl

ude

45 c

entr

al b

anks

Stat

es);

9 o

ther

s el

ecte

dco

untr

ies

•Fi

nanc

ial C

ongl

omer

ates

•Im

plem

enta

tion

offr

om O

EC

D a

nd la

rger

(cur

rent

ly n

o de

velo

ping

thro

ugh

Join

t For

um w

ithin

tern

atio

nal f

inan

cial

LD

Cs

coun

try

on th

e bo

ard)

IOSC

O a

nd IA

ISag

reem

ents

•G

ener

al m

anag

er,

trad

ition

ally

Eur

opea

n

16 G-24 Discussion Paper Series, No. 43

Org

anis

atio

n•

Clu

b of

like

-min

ded

•29

cou

ntri

es; i

nitia

lly•

Cou

ncil

is o

verr

idin

g•

Info

rmat

ion

and

anal

ysis

•C

orpo

rate

gov

erna

nce

for

Eco

nom

icco

untr

ies

in a

n ad

vanc

edfr

om w

este

rn c

ount

ries

inco

mm

ittee

Co-

oper

atio

nst

age

of e

cono

mic

Eur

ope

and

nort

h A

mer

ica,

•D

evel

opm

ent a

ssis

tanc

e•

Tax

have

nsan

d D

evel

opm

ent

deve

lopm

ent;

foru

m fo

rre

cent

ly e

xpan

ded

to•

Spec

ializ

ed c

omm

ittee

s fo

rco

mm

ittee

to c

oord

inat

e(O

EC

D)

coor

dina

tion

of p

olic

yin

clud

e M

exic

o, th

e R

ep.

spec

ific

pol

icy

area

s (t

rade

,do

nor p

rogr

amm

es•

Cor

rupt

ion

deve

lopm

ent

of K

orea

, Pol

and,

Hun

gary

deve

lopm

ent a

ssis

tanc

e et

c.)

[196

1]an

d th

e C

zech

Rep

ublic

•D

evel

opm

ent A

ssis

tanc

eC

omm

ittee

con

sist

s of

Par

isba

sed

dele

gate

s of

OE

CD

and

perm

anen

t obs

erve

rs:

IMF,

UN

DP,

Wor

ld B

ank

Lon

don

Clu

b•

Foru

m fo

r com

mer

cial

•Pr

ivat

e fi

nanc

ial i

nter

ests

,•

Con

sens

us•

Res

truc

turi

ng o

f pri

vate

ly•

Term

s of

rest

ruct

urin

gho

lder

s of

sov

erei

gn d

ebt

espe

cial

ly la

rge

bank

she

ld s

over

eign

deb

tpr

ivat

ely

held

sov

erei

gn d

ebt

•Pr

essu

re o

n go

vern

men

ts o

fco

untr

y of

ori

gin

(mai

nly

G-7

) on

sove

reig

n de

btre

late

d is

sues

Par

is C

lub

•Fo

rum

for b

ring

ing

toge

ther

•M

ainl

y O

EC

D•

Con

sens

us•

Res

truc

turi

ng o

f off

icia

lly•

Term

s of

rest

ruct

urin

gde

btor

s an

d of

fici

al c

redi

tors

gove

rnm

ents

(sec

reta

riat

held

sov

erei

gn d

ebt

offi

cial

ly h

eld

sove

reig

n de

bt[1

956]

in a

uni

fied

neg

otia

ting

prov

ided

by

Fren

chfr

amew

ork;

to a

void

trea

sury

dep

t.)de

faul

t on

debt

Gro

up o

f Sev

en•

Foru

m fo

r dis

cuss

ion

of•

Seve

n in

dust

rial

ized

•C

onse

nsus

•M

ost i

nflu

entia

l glo

bal

•B

road

infl

uenc

e in

(G-7

)ec

onom

ic a

nd fi

nanc

ial

coun

trie

s (C

anad

a, F

ranc

e,bo

dy b

ut in

flue

nce

over

arch

ing

rule

s of

glo

bal

issu

es a

mon

g th

e m

ajor

Ger

man

y, It

aly,

Jap

an,

over

whe

lmin

gfi

nanc

ial a

rchi

tect

ure

[197

4]in

dust

rial

cou

ntri

esth

e U

nite

d K

ingd

oman

d th

e U

nite

d St

ates

)

INST

ITU

TIO

NS

OF

GL

OB

AL

FIN

AN

CIA

L G

OV

ER

NA

NC

E (

cont

inue

d)

Org

aniz

atio

nIn

stitu

tiona

l goa

lsIn

tere

sts r

epre

sent

edD

ecis

ion

rule

sA

gend

a se

tting

cap

acity

Fin

anci

al is

sue

area

s

17Beyond the IMF

INST

ITU

TIO

NS

OF

GL

OB

AL

FIN

AN

CIA

L G

OV

ER

NA

NC

E (

cont

inue

d)

Org

aniz

atio

nIn

stitu

tiona

l goa

lsIn

tere

sts r

epre

sent

edD

ecis

ion

rule

sA

gend

a se

tting

cap

acity

Fin

anci

al is

sue

area

s

Gro

up o

f Ten

•Fo

rum

for c

onsu

ltatio

n an

d•

11 in

dust

rial

ized

cou

ntri

es•

Foru

m fo

r exc

hang

e of

•R

epor

ts th

at h

ave

an a

gend

a(G

-10)

coop

erat

ion

on e

cono

mic

,(G

-7 p

lus

Bel

gium

,id

eas;

no

expl

icit

pow

ers

setti

ng c

apac

ity fo

r oth

er in

ter-

mon

etar

y, a

nd fi

nanc

ial

Net

herl

ands

, Sw

eden

,na

tiona

l ins

titut

ions

(IM

F an

d[1

963]

mat

ters

Switz

erla

nd)

•M

eets

twic

e a

year

inB

IS in

par

ticul

ar)

conj

unct

ion

with

IMF

•C

ompo

sed

of fi

nanc

ein

teri

m c

omm

ittee

mee

tings

;m

inis

ters

and

cen

tral

ban

kin

add

ition

mee

ts in

sm

alle

rgo

vern

ors

grou

ps re

gula

rly

thro

ugh

the

year

Gro

up o

f 20

•Fo

rum

for d

iscu

ssin

g an

d•

Fina

nce

and

Trea

sury

•U

ncle

ar –

pro

babl

y•

Rep

orts

and

del

iber

atio

ns•

Rul

es a

nd s

tand

ards

for

(suc

cess

or to

G-2

2)fo

rmin

g co

nsen

sus

onof

fici

als

of G

-7 a

ndco

nsen

sus

coul

d ha

ve a

gend

a se

tting

aver

ting

and

deal

ing

with

avoi

ding

and

dea

ling

with

syst

emic

ally

impo

rtan

tca

paci

ty; t

oo e

arly

to te

llfi

nanc

ial c

rise

s[1

999]

fina

ncia

l cri

ses

deve

lopi

ng e

cono

mie

s pl

usE

U, I

MF

and

Wor

ld B

ank

•C

reat

ed b

y U

S Tr

easu

ry to

limit

Eur

opea

n in

flue

nce

Fin

anci

al S

tabi

lity

•Fo

rum

for d

iscu

ssin

g an

d•

Rep

rese

ntat

ives

from

G-7

•Fo

rum

for e

xcha

nge

•R

epor

ts a

nd re

com

men

da-

•C

ompe

ndiu

m o

f bes

t pra

ctic

eF

orum

form

ing

cons

ensu

s on

coun

trie

s (t

reas

ury,

sup

er-

of id

eas

tions

from

wor

king

gro

ups

stan

dard

s fo

r fin

anci

al in

stitu

-av

oidi

ng a

nd d

ealin

g w

ithvi

sory

, and

cen

tral

ban

k);

and

foru

ms

have

age

nda

tions

[199

9]fi

nanc

ial c

rise

sW

orld

Ban

k, IM

F, B

IS,

setti

ng c

apac

ityO

EC

D, B

asel

Com

mitt

ee,

IOSC

O, I

AIS

•C

reat

ed in

199

9 ou

t of

a G

-7 in

itiat

ive

Uni

ted

Nat

ions

• C

omm

on p

ract

ice

on•

UN

mem

bers

hip

•C

onse

nsus

•To

geth

er w

ith In

tern

atio

nal

•B

ankr

uptc

y, e

spec

ially

Com

mis

sion

on

Inte

r-cr

oss-