beyond savings –how to really help your clients plan for

TRANSCRIPT

Expand your capability. Expand your opportunities. Expand your income.

Beyond Savings – How to REALLY help your clients plan for College Costs

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies – low lying fruit

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies – low lying fruit

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

College is Expensive!

Years Public Private

Today $100,000 $320,000

Includes tuition, fees, and room & board, books and travel expenses

Source: *College Board. Annual 5% cost increase applied

CURRENT COST OF 4-YEAR COLLEGE EDUCATION

Over 500 colleges now charge more than $50,000/yearSource: College Board 2020 data analyzed by Collegiate Funding Solutions, Inc. Includes tuition, fees, room and board. Includes private and out-of-state public

Only 40% of freshmen enrolling in college graduate in four years

Source Dept. of Ed 2016

For one child!No wonder that 73% of parents with children under the age of 18

worry about college funding more than any other financial matter!

*Gallup Survey April 2015 – “U.S. Parents' College Funding Worries Are Top Money Concern”

Expand your capability. Expand your opportunities. Expand your income.

All demographics are impacted

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies – low lying fruit

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

Expand your capability. Expand your opportunities. Expand your income.

Expand your capability. Expand your opportunities. Expand your income.

Expand your capability. Expand your opportunities. Expand your income.

You need to be saving

$1,250/month to meet the projected cost of college. I

suggest…

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies – low lying fruit

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

Strategic College Planning Phase

l l l l l l l l l l l l l l l l l l l l l l

Tactical Planning

0 1 2 … 17 18

By helping your clients make smart and informed decisions at each step along the way, they’ll achieve a better outcome than they would

by going it alone and likely save money on college costs.

Birth >>> High School >>College Years

Dynamic College Planning

Expand your capability. Expand your opportunities. Expand your income.

The basics

Expected Family Contribution (EFC)

• Colleges use the EFC to determine your eligibility for financial aid• Parent and student income and liquid assets determine EFC• EFC is the minimum you are expected to contribute toward college costs

Financial & family info provided on the FAFSA (most public) / CSS Profile (many private) is used to calculate your EFC

How Financial Need is Determined

Expand your capability. Expand your opportunities. Expand your income.

AGI = $175,000

Liquid assets = $100,000

One child in college

Expected Family Contribution (EFC) = $45,000

Financial Need = Cost of Attendance - EFC

College Cost of Attendance - EFC = Financial Need

College A $52,000 - $45,000 $7,000

College B $65,000 $45,000 $20,000

EFC is the starting point for out-of-pocket college costs, not the Cost of Attendance of the college!

Example of financial need

With over 500 colleges that have a COA of > $50,000, many families with incomes > $150,000 will qualify for need-based financial aid

Expand your capability. Expand your opportunities. Expand your income.

Don’t assume your clients won’t qualify for financial aid

This is an actual student aid report for a family with an AGI of $290,000.

The EFC is $29,517

All of the schools selected by the family have a COA in excess of $50,000 year making them eligible for SIGNIFICANT amounts of need-based financial aid!

Expand your capability. Expand your opportunities. Expand your income.

Private College $65,000

Subtract EFC $45,000Financial Need $20,000Financial Aid Award: (scholarships and loans) $20,000Unmet Need (GAP) 0EFC + GAP $45,000

Total Cost to Parent $45,000

Many schools will not meet 100% of the financial need or fill most of the need with scholarships/grants versus loans

Your clients should know the schools’ history of allocating aid BEFORE they apply, not after they decide!

Example of financial need met

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies - low lying fruit

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

• Keep student’s income under the current protection allowance

• Avoid capital gains during your base years

• Postpone bonuses (raises if self-employed)

Income Tips

Familiarize yourself with

INCOMEstrategies that can effectively

lower EFC.

Expand your capability. Expand your opportunities. Expand your income.

(Excluded) Assets

• Retirement Accounts (401K, IRAs, SEPs, etc.)

• Personal Items (cars, furniture, etc.)

• Home Equity (except schools using Profile)

• Cash Value within life insurance policy

Asset Tips

Familiarize yourself with

ASSET strategies that can effectively

lower EFC.

Expand your capability. Expand your opportunities. Expand your income.

Options

• School merit-based scholarships

• Need-based financial aid

• Tuition discounts – given to desirable students at the top of the applicant pool (test scores/GPA)

• Savings strategies• Cash flow strategies

• Funding strategies• Income and asset planning strategies• Strategies for business owners

• Strategies for grandparents• Tax credit strategies

• Gifting strategies

Source

Free Money

Gap/Shortfall

The big picture

• Savings strategies

• Cash flow strategies• Funding strategies• Income and asset planning strategies• Strategies for business owners

• Strategies for grandparents

• Tax credit strategies• Gifting strategies

Expand your capability. Expand your opportunities. Expand your income.

Savings strategies

Expand your capability. Expand your opportunities. Expand your income.

1. Funds for college2. Favorable for financial aid candidates?3. Use for college AND retirement - flexibility

SAVINGS STRATEGIES: Choosing the best option in light of the client’s circumstances

Expand your capability. Expand your opportunities. Expand your income.

HIGH LEVEL Comparison of common college funding vehicles

LiquidityTax Deferred

GrowthSelf-

FundingRisk

AverseFinancial Aid

Friendly

Flexibility (use &

Transfer)

529 QTP Savings Accounts X

Tax-Efficient Mutual Funds X X

Real Estate (rental property) X ? ?

HELOC (Home Equity) ? n/a ? X X

Savings Bonds, CD’s, TIPS X X X

Life Insurance (CV) X X X X X X

Consider benefits of alternatives to a 529 plan

Expand your capability. Expand your opportunities. Expand your income.

Consider the benefits of alternatives to a 529 plan

• Better liquidity

• Flexibility – multiple use (college and/or retirement)

• Less restrictions

• Avoids 529 glide path pitfalls (age-based portfolios)

• No coordination with education credits

• May be better option for asset managers – control/revenue

• State tax benefit on contributions of 529 may not be available or of negligible benefit.

• With right plan, LT capital gains will apply along with nominal dividend income

Example - using mutual fund for accumulation/funding

Expand your capability. Expand your opportunities. Expand your income.

529’s and Glide Path

Poor market returns in early years can DOOM 529 appreciation

“…age-based options within 529 college-savings plans have historically held the lion's share of assets” - Morningstar

Expand your capability. Expand your opportunities. Expand your income.

Business Owner Strategies

Expand your capability. Expand your opportunities. Expand your income.

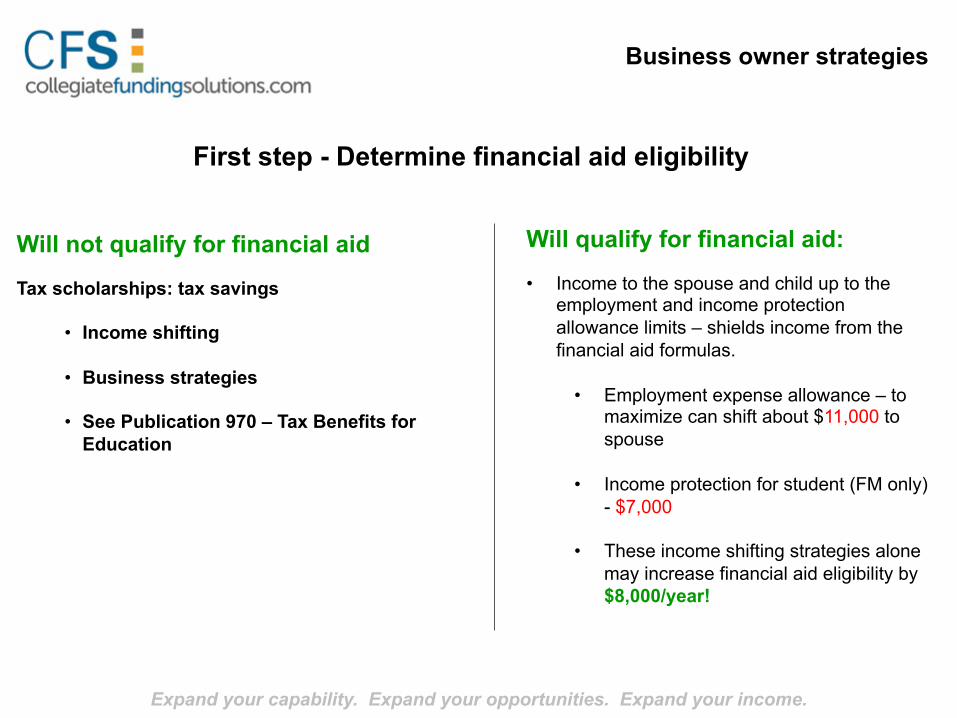

Business owner strategies

Will not qualify for financial aidTax scholarships: tax savings

• Income shifting

• Business strategies

• See Publication 970 – Tax Benefits for Education

First step - Determine financial aid eligibility

Will qualify for financial aid:• Income to the spouse and child up to the

employment and income protection allowance limits – shields income from the financial aid formulas.

• Employment expense allowance – to maximize can shift about $11,000 to spouse

• Income protection for student (FM only) - $7,000

• These income shifting strategies alone may increase financial aid eligibility by $8,000/year!

Expand your capability. Expand your opportunities. Expand your income.

Strategies for Grandparents

Expand your capability. Expand your opportunities. Expand your income.

1. Grandparents play a significant role in college funding

2. College costs (via the EFC) are a impacted by parents & grandparents actions

3. Common strategies that grandparent employ may have negative consequences that drive up cost

4. Educational opportunity for the advisor

5. Create unique value for the entire family – across the generations thereby maintaining and expanding relationships and business through generations

Expand your capability. Expand your opportunities. Expand your income.

Common Grandparent College Funding Strategies

1. Gifting money directly to the student or parents to be used for college costs

2. Sending the money directly to the college to be applied to the bill

3. Saving for grandchild using 529 plan

Each of these options may DECREASE financial aid eligibility and INCREASE the family’s out-of-pocket college cost!.

Result:Grandparent contribution may be diluted/offset by the increase in college costs due to decreased financial aid eligibility!

Expand your capability. Expand your opportunities. Expand your income.

Grandparents

Method Alternative

Gift to student Wait until after college to gift money to pay down loans

Gift to parents Wait until after college to gift money to pay down loans

Send money directly to college Wait until student’s senior year to make payment.

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies low lying fruit

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

Mistakes that cost families thousands of dollars in financial aid and tuition discounts

Mistake #1 “I make too much money!”

Mistake #2 Rushing through the process

Mistake #3 Applying to fewer than six schools

Mistake #4 Picking the wrong schools

Mistake #5 Assuming all financial aid is the same

Expand your capability. Expand your opportunities. Expand your income.

Mistake #6 Not knowing the formulas

Mistake #7 Not applying at all

Mistake #8 “My CPA/tax preparer will do it”

Mistake #9 Responding to a colleges offer too soon

Mistake #10 Forgoing expert help

Mistakes that cost families thousands of dollars in financial aid and tuition discounts

Expand your capability. Expand your opportunities. Expand your income.

Every family should apply for financial aid

• You WANT the school to see their ability to pay

• Schools WANT full-pay clients. Use tuition discounts to get them

• These parents contribute to endowments/booster programs, etc.

• Highly desirable to colleges and they’ll compete for them

• The forms are the means for the family getting the best deal

• Federal loans and some merit-based scholarships require form filing

Here’s Why:

Expand your capability. Expand your opportunities. Expand your income.

Dynamic College Planning

l l l l l l l l l l l l l l l l l l l l l l0 1 2 … 17 18

Birth >>> High School >> College Years

By helping your clients make smart and informed decisions at each stepalong the way you’ll help them achieve the goals

Right CollegeRight Reasons

Right Price

Putting it all together

College Admissions and Financial Aid

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies for Affluent Clients

• Big mistakes families make that can be costly

• Example

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

Example – Facts of the case

• Small business owner

• Family size = 5

• AGI = $215,000

• SAT = 1,400 GPA = 4.0

• Non-qualified assets = $300,000

Facts of the case:

Expand your capability. Expand your opportunities. Expand your income.

Test Case - Results• COA = $64,000

• EFC = $46,000

• Family contribution = $48,000 ($46K + $2K gap)/year

• Four-year projected cost of $192,000

Benefits of advance planning:

• Used $100K of non qualified assets to pay down mortgage

• Shift income to spouse and student of $15,000

Result:

• Family Contribution = $38,000/year• Four-year projected cost = $152,000• Four year savings = $40,000

Savings on sticker price of $26,000/year

Impact on retirement savings outlook? HUGE!

Expand your capability. Expand your opportunities. Expand your income.

Agenda

• Current college cost landscape

• The college funding/retirementsavings dilemma

• Covering the basics

• Strategies for Affluent Clients

• The college admissions andforms minefield

• Test case review

• Summary/Conclusion

Expand your capability. Expand your opportunities. Expand your income.

Contact:

Phone: 919-469-1996

Email: [email protected]

Website: www.collegiatefundingsolutions.com