beyond panglossian theory: strategic capital investing …directory.umm.ac.id/data...

TRANSCRIPT

Beyond Panglossian theory: strategic capital investing in acomplex adaptive world

Tom Mouck*

Anderson Schools of Management, The University of New Mexico, Albuquerque, NM 87131-1221, USA

Abstract

Traditional capital budgeting theory (as an extension of ®nancial economics) is characterized as Panglossian because

of its suggestion that rational market outcomes produce the best of all possible worlds. During the last two decades,practice-oriented theorists have increasingly been moving from algorithmic capital budgeting techniques to a focus oncapital investment strategy. Also, during the last twelve years, economics researchers at the Santa Fe Institute (SFI)

have scrapped the dubious assumptions of neoclassical economics and have turned to complex adaptive systems theoryfor a more realistic portrayal of the economy. This paper explores various SFI studies and their implications for capitalinvestment theory and capital investment strategy. Brian Arthur's theory of increasing returns undermines the notion

that capital budgeting techniques can be counted on to generate economic e�ciency. His theory further suggests thatthe high tech, knowledge-based sectors of the economy inherently produce outcomes that are too unpredictable for themeaningful application of traditional capital budgeting techniques. Studies by David Lane and his colleagues suggestthat the identity of agents, the attributes of artifacts and the possibilities for action tend to be emergent phenomena

that are generated by the interactions of agents. These considerations suggest a form of strategic action that focuses onprocess. Finally, it is argued that the arti®cial life and other SFI types of computer simulation models are potentiallyuseful tools for the study of strategic capital investment decisions. # 2000 Elsevier Science Ltd. All rights reserved.

According to Jones and Smith (1982, p. 104),one of the ®rst published works dealing with theuse of present value calculations to assess non-®nancial investments was in 1887 by an Americancivil engineer concerned with the economics ofrailway construction. They also note that IrvingFisher's The rate of interest (originally publishedin 1907, but revised and published as The theory ofinterest in 1930) was the ®rst work in the Amer-ican economic literature to discuss net presentvalue as a criteria for appraisal of alternative

investments. They further note that the ®rst sig-ni®cant accounting publication dealing with capi-tal budgeting theory (CBT) was Bierman andSmidt's textbook, The capital budgeting decision(1960/1980).The landmark publications noted above focused

on the practical applications of CBT. But marketeconomists (including those who call themselvesacademic accountants) have never been satis®edwith merely practical applications; they havealways sought theoretical explanations purport-edly demonstrating that rational individuals and®rms acting to optimize their self interests in a freemarket economy will produce the best of all pos-sible worlds. In this sense, the market economist is

0361-3682/00/$ - see front matter # 2000 Elsevier Science Ltd. All rights reserved.

PI I : S0361-3682(99 )00049-5

Accounting, Organizations and Society 25 (2000) 261±283

www.elsevier.com/locate/aos

* Tel.: +1-505-277-6471; fax: +1-505-277-7108.

E-mail address: [email protected]

analogous to Dr. Pangloss in Voltaire's novelCandide (1759/1959).1 Thus, during the 1960s,with the development of the capital assets pricingmodel (CAPM), the e�cient markets hypothesis(EMH), and modern portfolio theory (MPT), thetheory of capital budgeting was rapidly integratedinto the Panglossian story of economic e�ciency.According to this story, individuals save andinvest in accordance with their preference for cur-rent versus future consumption and make invest-ment decisions that maximize return in accordancewith their own psychological aversion to risk; and®rms produce goods and services at the lowestpossible cost while maximizing pro®ts (i.e. thereturn to investors). With respect to new capitalinvestments, a ®rm will accept new investmentsthat have an expected rate of return in excess ofthe ®rm's cost of capital. Thus, in equilibrium the®rm's marginal rate of return would be equal tothe cost of capital.This story about the capitalinvesting decision was widely heralded as ``scien-ti®c''. The UK, in the 1960s, even publicized it as away of boosting the macro performance of theeconomy by linking macro-level investmentspending with ``e�cient'' decentralized micro-leveldecisions of individual ®rms (Miller, 1991).This story of capital budgeting and e�ciency

shares an a�nity with Voltaire's story of Candide.Recall how the young Candide encountered onemisfortune after another in his series of bizarreadventures, and how Dr. Pangloss reassured Can-dide after each disastrous event that, in spite ofappearances, this still must be the best of all pos-sible worlds. Why was Pangloss so insistent uponthis conclusion? Because it followed logically fromhis initial assumptions Ð never mind that theseassumptions were wishful thinking absurdities. Inlike fashion, the ®nancial economists who pro-mote the story of Panglossian capital budgetingtend to rely upon the unrealistic assumption ofglobal rationality, omnipresent equilibria, massivecognitive and computational capabilities, andunambiguous and readily available information.

As would be expected, the Panglossian story ofeconomic e�ciency has often been viewed by non-believers with an attitude of incredulity. Unfortu-nately, however, the non-believers were all too oftenintimidated by the ``scienti®c'' blu� and bluster ofthe economists, especially when couched in termsof highly abstract mathematical notations. The storyhas, accordingly, gone largely unchallenged in scien-ti®c and mathematical terms until quite recently,when a group of interdisciplinary economists andscientists at the Santa Fe Institute (SFI) Ð a privateresearch institute devoted to the study of complexadaptive systems Ð began to formulate an alter-native story about economic reality. Their alter-native story and its implications for capitalmarkets research in accounting has been discussedin Mouck (1998, pp. 206±210). The present paperexplores the implications of SFI economic theoryfor traditional capital budgeting theory and high-lights some of its implications for capital invest-ment in new technologies.Researchers in the SFI economics program

scrapped the neoclassical model of equilibriumbased on Newtonian mechanics and focusedinstead on an evolutionary model featuring con-tinual change, instability and adaptation. Stanfordeconomist Brian Arthur, who has been the drivingforce behind the SFI's economics research, haselaborated a theory of increasing returns whichradically contradicts the neoclassical emphasis ondecreasing returns, upward sloping supply curvesand market equilibrium analysis.2 The magnitudeof the challenge associated with increasing returnsis clearly manifested in the following quote:

Increasing returns are the tendency for thatwhich is ahead to get further ahead, for thatwhich loses advantage to lose further advan-tage. They are mechanisms of positive feedbackthat operate Ð within markets, businesses, andindustries Ð to reinforce that which gainssuccess or aggravate that which su�ers loss.Increasing returns generate not equilibriumbut instability: If a product or a company or

1 My use of the term ``Panglossian'' to describe the economic

theory of capital budgeting was inspired by Tony Tinker's 1988

article, ``Panglossian accounting theories: the science of apol-

ogizing in style''.

2 As noted by the Nobel prize winning economist Kenneth

Arrow (1994), Arthur's work on increasing returns set the stage

for a burgeoning literature on the subject.

262 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

a technology Ð one of many competing in amarket Ð gets ahead by chance or cleverstrategy, increasing returns can magnify thisadvantage, and the product or company ortechnology can go on to lock in the market(Arthur, 1996, p. 100)

With respect to Panglossian capital budgetingapplied to investing in new technologies, Arthur'stheory of increasing returns challenges the notionthat the most e�cient new technology will prevailin a free market. With respect to the practicalapplications of capital budgeting, Arthur's theoryimplies that future cash ¯ows associated with hightech investments may not be susceptible to mean-ingful estimation.Other SFI economists (Lane,Malerba,Max®eld &

Orsenigo, 1995) have mounted a powerful challengeto the Panglossian theory of rational choice, arguingthat economic action, in the most interestingsituations, emerges from processes of interactionbetween agents, rather than from choosing amonga pre-existing set of structured alternatives. Theirargument is contrary to traditional (Panglossian)capital budgeting theory, and it leads to a radi-cally di�erent perspective on strategic issues sur-rounding the development of new technologies(Lane & Max®eld, 1997).The hallmark of SFI research, however, is the

use of extraordinarily creative computer models tosimulate the complexity of real world conditions.Many of these models (ranging from simulationsof tra�c jams to arti®cial life) are discussed inJohn Casti's recent (1997) book entitled Would-beworlds: How simulation is changing the frontiers ofscience. One of the models discussed by Casti is anarti®cial stock market created by Brian Arthurand his colleagues. This computer-based arti®cialstock market is producing results that are surpris-ingly consistent with real world stock markets butquite inconsistent with the capital markets theoryof ®nancial economists. The results of this modelcontradict the basic theoretical notions associatedwith cost of capital in the Panglossian theory ofcapital budgeting, but the SFI approach to com-puter-based simulation models does shed someinteresting light on new directions that could betaken by capital investment theorists.

All of these challenges to Panglossian capitalbudgeting theory are explored in this paper, aswell as the implications for real world capitalinvesting issues, especially those surrounding thedevelopment of new, knowledge-intensive, tech-nologies. First, an overview is provided of tradi-tional capital investing theory, together with abrief sketch of some of the more salient alternativeperspectives that essentially move from capitalbudgeting theory to a theory of capital investmentstrategy. The next section outlines the main com-ponents of Arthur's theory of increasing returnsand the implications for economic e�ciency withrespect to new technologies. This is followed by asection which provides an overview of the argumentsof Lane et al. (1995) with respect to rational choicetheory, and an exploration of the implications forstrategic issues surrounding the development of new,knowledge-intensive technologies. Finally, I turn toan account of the SFI's stock market simulations,how they serve to undermine portfolio theory andthe Panglossian cost of capital concept, and howthe SFI simulation approach could play a pro-ductive role with respect to capital investmentstrategy.

1. From Panglossian capital budgeting to strategiccapital investing

To my knowledge, the earliest accounting paperdetailing the links between portfolio theory andcapital budgeting was Ball and Brown's ``Portfoliotheory and accounting'' (1969). In this article, theyweave the threads of the now familiar Panglossianstory in which ``the ®rm accepts the utility func-tions of investors, and by translating these into theinvestment decision it maximizes their utilities''(Ball & Brown, p. 309). The ®rm ``accepts the uti-lity functions of investors'' by requiring that theexpected value of the return on any new invest-ment project be at least equal to the cost of capi-tal. The cost of capital, according to the story, isthe expected rate of return on the ®rm's existingassets; i.e. the expected rate of return which theinvestor accepted by investing in the ®rmÐ keepingin mind, of course, that the investor's investmentdecision re¯ects the investor's preferences with

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 263

respect to current versus future consumption. Aswith other economics-based Panglossian stories, thisone relies upon the assumption of equilibrium in thecapital markets. As Ball and Brown point out,``Assumed equilibrium is necessary even to considerthe cost of capital as a normative variable since astate of disequilibrium in the capital market doesnot permit us to equate maximizing owners' utilitieswith maximizing the value of the ®rm'' (p 309).In the real world, of course, the purity described

by Panglossian theorists has never been achieved.But the model advocated by these theoristsbecame widely accepted by business schools, andit was formally adopted by large segments of thebusiness world. During the last two decades,however, the inadequacies of the capital budgetingmodel have been increasingly brought to light, andtheorists have increasingly been moving towardthe view that capital investing decisions are moreproperly considered as an inherent part of anadaptive, contextually-informed strategy than asthe outcome of contextually isolated algorithmicpresent value calculations. This trend was evidentby the early 1980s. Logue (1981), for instance,argues that traditional capital budgeting theory isinadequate for ``strategic investments'', which hedescribes as ``investments that take the ®rm in newdirections or that yield ®nancial bene®ts to the®rm undertaking them that are external to theinvestment itself'' (p. 88). An options model, hesuggests, would be more appropriate for evaluat-ing such investments. Coda and Dematte (1981)argue that the formulation of an overall businessstrategy constitutes the framework within whichspeci®c projects should be evaluated. If more thatone potential investment project ®ts within thestrategic game plan, then traditional capital bud-geting theory could be employed to determinespeci®cally which project is to be accepted (p.105). And Derkinderen and Crum (1981) note theemerging complexity of the business environmentat the beginning of the 1980s and suggest that,``Models with adequate predictive power underrelatively stable and well-understood conditionswill be less able to provide adequate guidance inthe more turbulent period of the 1980s'' (p. 8). Bythe 1990s a signi®cant literature had developedaround each of these suggestions.

Buckley (1996, Chapter 3) provides an overviewof the literature related to capital investmentoptions, a literature that was inspired largely bythe Black and Scholes (1973) option pricing model.As he points out, some types of capital investmentprojects may entail options to postpone the deci-sion until a later date. Other types of investmentprojects may entail an initial investment plusoptions to scale up or expand at a subsequentdate. Such options can be quite valuable, yet thesevalues are not considered in the traditional capitalbudgeting model. Buckley argues that treatinginvestment projects as options may be especiallyrelevant to projects involving research and devel-opment, projects involving natural resourceextraction, and projects involving expansion intonew marketing territories. In sum, the upshot ofthe investments options literature, ``is that the old-style capital appraisal techniques are more thanadequate in terms of dealing with cash cowinvestments but leave something to be desiredwhere there is operational ¯exibility or contingentopportunities for growth'' (Buckley, 1996, p. 53).Other directions in the strategic cost manage-

ment literature have been critical of the tendencyto evaluate investment projects too narrowly byfocusing only on the ``value-added'' (by the spe-ci®c ®rm); that is, by starting with the ®rm's pay-ments to suppliers and stopping at the expectedsales to customers. This narrow focus neglects thestrategic insights that could be gained by examin-ing the entire ``value chain'' of which the ®rm'svalue added is only one link. By developing theentire value chain, including not only the ®rm'simmediate suppliers and customers, but alsoincluding the supplier's suppliers and the custo-mer's customers, from raw materials to ultimateconsumer, the ®rm may gain insights into its ownbargaining power vis a vis suppliers and customersthat could alter the assumptions used in the capi-tal budgeting analysis. Shank and Govindarajan(1992), for example, discuss a case situation inwhich a value chain analysis yielded a signi®cantlydi�erent perspective on the investment optionsthan traditional capital budgeting analysis. Theyargue that speci®c projects should be consideredonly within the context of strategic options thathave been identi®ed by a full-¯edged value chain

264 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

analysis. This echoes Coda and Dematte's (1981)claim that ``the decision system of a company hasa box-within-box structure, where the singleinvestments are the smallest boxes and are hier-archically dependent on the business strategychoice. This latter structure gives the frameworkagainst which the single investment proposals areweighed and selected'' (pp. 104±105).Value chain analysis has received much of its

impetus due to the in¯uence of Porter's (1980,1985) books on competitive strategy which drawattention to strategies for cost leadership and dif-ferentiation leadership. Shank and Govindarajan(1992) note that ``. . .value chain analysis is essentialto determine exactly where in the ®rm's segment ofthe chainÐ from design to distributionÐ customervalue can be enhanced or costs lowered'' (p. 180). Inthis sense, value chain analysis has a certain degreeof a�nity with Japanese target costing. Whereas theformer is concerned with costs and values through-out the entire chain from raw materials to ®nalconsumer, the latter (target costing) focuses oncosts and values of new products from researchand development to completion of production.Whereas US ®rms pursuing a cost leadership

strategy have typically focused on the costs ofproduction, Japanese target costing is a strategythat focuses on cost reduction opportunities at theearliest conceptual stages of a new product, evenprior to production plans. As described by Kato(1993), ``Target costing is an activity which isaimed at reducing the life-cycle costs of new pro-ducts, while ensuring quality, reliability, and otherconsumer requirements, by examining all possibleideas for cost reduction at the product planning,research and development, and the prototypingphases of production'' (p. 36). As compared withthe traditional capital budgeting approach toevaluating the acceptability of a new project, arelatively passive approach that consists largely ofgathering information about available options andchoosing among them, Japanese target costing is ahighly active approach. Even in terms of expectedselling price, the target costing strategy requires anactive versus a passive approach. It attempts toidentify the functional elements of a product thatare valuable to consumers; elements such as``style, comfort, operability, reliability, quality,

attractiveness. . .''. (Kato, p. 38), and to assign avalue to each of these functions. The cumulativevalues associated with the functional elements of aproduct would constitute the expected sellingprice. With respect to costs, the procedures refer-red to as ``value engineering'' (VE) are relied uponto identify possible cost reductions. Kato notesthat VE requires an extensive support system,including ``cost tables, cost reduction databasesand cost reduction database management sys-tems'' (p. 43). These procedures underlie the cal-culation of the ``target cost'' which, in formulaterms, is the di�erence between ``expected salesprice'' and ``target pro®t'' (Kato, p. 38).None of these perspectives Ð target costing,

value chain analysis and capital investments trea-ted as options Ð necessarily negates the potentialusefulness of DCF-type capital budgeting techni-ques. They suggest variations for viewing thestrategic context and constructing assumptions,but they maintain a focus on speci®c projects Ðnew products, expansion to new territories, newproduction equipment, etc. Ð that does not ruleout the applicability of NPV analysis. By the early1990s, however, a new conception of strategy wasemerging; a conception that Stalk, Evans andShulman (1992) refer to as ``capabilities-basedcompetition'' (p. 57). The notion of capabilities-based competition is clearly a product of the``more turbulent period of the 1980s'' predicted byDerkinderen and Crum (1981, p. 8), and it hastriggered a radically di�erent approach to capitalinvestment decisions; an approach that is moreclearly attuned to the complex adaptive worlddescribed by the Santa Fe Institute economists.Baldwin and Clark (1992) have provided adetailed description of this new perspective. Theydescribe ``capabilities'' as:

. . .identi®able combinations of human skills,organizational procedures, physical assets,and information systems. Such complex com-binations of resources are achieved becausecompanies allocate resources (both humanand ®nancial) to their development in theexpectation of future reward. In this respect,capabilities are like any other investment(Baldwin & Clark, p. 69).

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 265

The speci®c bene®ts associated with investing incapabilities arise from external integration, inter-nal integration, ¯exibility, the capacity to experi-ment, and the capacity to cannibalize, all of whichgenerate an ability to exploit emerging opportu-nities, to move creatively into new niches, andeven to create new niches. ``External integration isthe ability to link knowledge of customers with thedetails of engineering design in creating andimproving products'' (Baldwin & Clark, 1992,p. 70). Internal integration refers to the ability tocommunicate, plan, formulate strategy, and coor-dinate production activities across functional andorganizational units within the ®rm. Flexibilityrefers to the capability to switch from one productmix to another, from one level of operating capa-city to another, or even from one market toanother. Experimentation is intimately associatedwith organizational learning, and the capacity toexperiment is largely a function of investment incommunication and information systems thatfacilitate the generation and dissemination ofknowledge associated with diagnosis and testing.And ®nally the process of cannibalization Ðwhich refers to the development and promotion ofgoods or services that compete with or replacesome of the ®rms more pro®table products Ð isseen as a potentially valuable strategy for pre-venting entry by other ®rms. As Baldwin andClark point out, the capacity to cannibalize``requires a signi®cant investment in procedures,information systems, and human skills, as well asphysical assets'' (p. 73).Traditional capital budgeting may be appro-

priate for an economic environment in whichcompetition is for speci®c product lines or speci®cmarkets. But as Stalk et al. (1992) point out,today's complex economic environment is moreaptly characterized as a ``war of movement'' inwhich ``competitors move quickly in and out ofproducts, markets, and sometimes even entirebusinesses Ð a process more akin to an interactivevideo game than to chess'' (p. 62). In such anenvironment they argue that, ``The building blocksof corporate strategy are not products and mar-kets but business processes'' (p. 62). And this isprecisely where the work of SFI economist BrianArthur can expand and deepen our understanding

of issues involved in capital investment decisions. Hiswork on the phenomena of increasing returns sup-ports a radically di�erent understanding of businessand economic processes than the diminishing returnsand equilibrium processes underlying Panglossiancapital budgeting theory. His theory of increasingreturns supports neither the e�ciency claims nor theNPV techniques of Panglossian theory.

2. Increasing returns and economic (in)e�ciency

Arthur (1994, p. 1) points out that conventionaleconomic theory relies upon negative feedbackmechanisms (negative returns) to generate theequilibrium, harmony and stability that its propo-nents (Panglossians) associate with unimpededmarket forces. He further notes that, ``[a]ccordingto conventional theory, the equilibrium marks the`best' outcome possible under the circumstances:the most e�cient use and allocation of resources''(p. 1). The notion of positive returns has beenresisted by Panglossian economists because itthreatens to undermine their neat optimistic pic-ture of laissez-faire economic theory.

Diminishing returns imply a single equili-brium point for the economy, but positivefeedback Ð increasing returns Ð makes formany possible equilibrium points. There is noguarantee that the particular economic out-come selected from among the many alter-natives will be the `best' one. Furthermore,once random economic events select a parti-cular path, the choice may become locked-inregardless of the advantages of the alter-natives. (Arthur, 1994, p. 1).

Arthur's work on increasing returns in theeconomy is ®rmly grounded in a branch of prob-ability theory that focuses on ``nonlinear Polyaprocesses''. These are stochastic processes char-acterized by positive feedback, path dependency andsensitivity to initial conditions.3 Arthur, Ermoliev

3 Polya is the name of the mathematician who formulated

and worked out the detailed mathematical proofs for such

processes (Arthur, 1994, p.36).

266 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

and Kaniovski (1994, pp. 36±37) describe a veryrudimentary Polya process in terms of an urnwhich initially contains red and white balls inequal proportions. If a ball is drawn at random,say a white ball, then replaced, and a new ball ofthe color just drawn is added to the urn, then theproportion of white balls increases to greater than50% and the probability of drawing a white ballon the next round becomes greater than 50% Ð aclassic situation of increasing returns. If this pro-cess is repeated many times, the proportion ofwhite balls will eventually settle down to a stableamount somewhere between zero and 100%. Atthe outset, it is impossible to predict what thelong-run proportions will be, they depend on theprecise path taken during the early stages when anadditional ball of one color or the other makes asigni®cant di�erence in proportions. As thenumber of balls increases, the addition of anotherwhite ball tends to change the existing propor-tions by such a small amount that the probabilityof drawing another white ball tends to remainconstant. If a stable persistent proportion ofwhite balls is characterized as a ``structure'', thenone can say that a unique structure has emergedfrom a system ``with independent incrementssubject to random ¯uctuations'' (Arthur et al.,1994 p. 34).Arthur et al. (1994) discuss the generalization of

Polya processes beyond the simple urn example ofthe previous paragraph. Their generalizationapplies to processes involving more than two typesof things (i.e. ®rms in an industry, competingtechnologies, or industries locating in variousregions), and it extends to situations ``where theprobability of an addition to type j is an arbitraryfunction of the proportions of all types'' (p. 38).They also work out theorems that apply to classesof Polya processes, indicating which types ofPolya processes will be characterized by extremeattractor points (stable outcomes), which will becharacterized by both attractor points and repel-ling points (unstable outcomes), and which willhave multiple possible long-term outcomes. Thesigni®cance of this generalization for Arthur'seconomic work is that it allows him to specify theconditions under which a ``selected'' outcome will bestable and persistent. The various articles collected

in Arthur (1994) include applications of theseideas to industry locations, competing technolo-gies, and human learning and decision-making insituations with incomplete information. Theapplication to competing technologies is directlyrelevant to capital budgeting theory, since themost prominent capital investing decisions in thecurrent high-tech economy involve, directly orindirectly, competing technologies.With respect to new technological develop-

ments, Arthur (1988) 4 suggests that ``we can thinkof these methods or technologies as `competing'for a `market' of adopters'' (p. 590). And he pre-sents an analysis of the ways in which ``[i]ncreasedattractiveness caused by adoption. . . [i.e.]`increasing returns to adoption''' (Arthur, 1988,p. 590) can, under certain circumstances, culmi-nate in technological ``lock-in'' with no guaranteethat the prevailing technology is the best of thoseavailable. Notable sources of increasing returns toadoption include the following:

1. Learning by using. . . Often the more a tech-nology is adopted, the more it is used and themore is learned about it, therefore the moreit is developed and improved. . .

2. Network externalities. . . Often a technologyo�ers advantages to `going along' with otheradopters of it Ð to belonging to a networkof users. . .

3. Scale economies in production. Often, where atechnology is embodied in a product. . . thecost of the product falls as increased num-bers of units of it are produced. . .

4. Informational increasing returns. Often atechnology that is more adopted enjoys theadvantage of being better known and betterunderstood. . .

5. Technological interrelatedness. . . Often, as atechnology becomes more adopted, a num-ber of other sub-technologies and productsbecome part of its infrastructure. (Arthur,1988, p. 591).

4 Arthur (1988) is a somewhat condensed version of Chapter

2 in Arthur (1994).

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 267

One of Arthur's main points is that, with respectto the ``e�cient harmony'' that Panglossian econ-omists presume to be guaranteed by the unfetteredplay of market forces, there is in fact no guaranteethat the most economically e�cient technologywill prevail. His analysis suggests that the bene®tsfrom adopting one of two competing technologi-cal alternatives will be an emerging function of thesequence of adoptions, i.e. it will be path-dependent.Suppose, for instance, that a ®rm has initiallydetermined that technology A (say a new computersoftware system) will be more cost e�ective thantechnology B (a competing software system). It isaltogether likely that this same ®rm would changeits assessment if adoptions of technology B beganto outrun the adoptions of technology A to theextent that the ``returns to adoption'' (networkexternalities, scale economies in production, tech-nological interrelatedness, etc.) associated with Bbegan to dwarf those associated with A.The ``dynamics of adoption'', accordingly, are

of primary importance in Arthur's theory of com-peting technologies, and he illustrates the implica-tions in several models of varying sophisticationand generalizability. A review of all his models isneither possible nor desirable within the scope ofthe present paper, but a brief overview of his basicmodel should prove helpful. The basic modelinvolves two competing new technologies, (A andB) and two types of adopters (R and S). R-typesare assumed to have a ``natural'' preference fortechnology A and S-types have a ``natural'' pre-ference for technology B. However, with increas-ing cumulative adoptions of one technology versusthe other the ``returns to adoption'' (discussedabove) begin to outweigh natural preferences.Thus, if one of the technologies (say technologyA) accumulates su�cient adoptions, then bothtypes of adopters will begin to choose that tech-nology and the competition will be over. TechnologyA, in this case, will have achieved ``lock-in''.In Arthur's basic model the adopters, R-types

and S-types, are assumed to arrive at the ``adop-tion window'' in a random order so that anytimeprior to lock-in the probability that the nextadopter will choose A (or B) is 50%, the prob-ability of heads versus tails in a coin toss. If thepattern of cumulative adoptions is charted, the

result will be a ``random walk with absorbingbarriers'' (Arthur, 1988, p. 594) as illustrated inFig. 1. The hypothetical graph in Fig. 1 shows thedi�erence in adoptions of A versus B on the ver-tical axis with time on the horizontal axis. Thedashed lines represent the ``absorbing barriers'',the di�erences beyond which one of the two tech-nologies achieves lock-in. Between the barriers R-types will choose A and S-types will choose B, butas indicated, once the cumulative adoptions pushthe di�erence beyond either barrier both types ofadopters will choose the same technology resultingin technological lock-in. ``The important factabout a random walk with absorbing barriers isthat absorption occurs eventually with certainty''(Arthur, 1988, p. 594). Thus, in the long-run,according to this model, ``the economy must lockin to monopoly of one of the two technologies, Aor B, but which technology is not predictable inadvance'' (Arthur, 1988, p. 594).``Real world'' competition, of course, is rarely as

passive as suggested in this basic model. As Arthurpoints out, the possibility of ``winner-take-all'' in atechnological competition creates powerful incen-tives for strategic competition. The incentive forstrategic competition, however, is not unique towinner-take-all situations Ð and Arthur (1988)does include a model which results in a sharedmarket. In any case, it is the fact of increasingreturns to adoption that motivates aggressivecompetition among technologies. This is whyArthur claims that ``competition between technol-ogies usually becomes competition between band-wagons, and adoption markets display both acorresponding instability and a high degree ofunpredictability'' (1988, p. 590).Arthur calls attention to several actual case his-

tories involving competing technologies. One ofthe most straight-forward case histories is theearly VCR market.

The VCR market started out with two com-peting formats selling at about the same price:VHS and Beta. Each format could realizeincreasing returns as its market shareincreased: large numbers of VHS recorderswould encourage video outlets to stock moreprerecorded tapes in VHS format, thereby

268 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

enhancing the value of owning a VHS recor-der and leading more people to buy one. (Thesame would, of course, be true for Beta-for-mat players.) In this way, a small gain inmarket share would improve the competitiveposition of one system and help it furtherincrease its lead (Arthur, 1994, p. 2).

The VCR market is a clear-cut example ofincreasing returns. It also illustrates a Polya processthat results in lock-in to one of the alternatives.

Such a market is initially unstable. Both sys-tems were introduced at about the same timeand so began with roughly equal marketshares; those shares ¯uctuated early onbecause of external circumstance, `luck', andcorporate maneuvering. Increasing returns onearly gains eventually tilted the competitiontoward VHS: it accumulated enough of anadvantage to take virtually the entire VCRmarket. Yet it would have been impossible atthe outset of the competition to say whichsystem would win, which of the two possibleequilibria would be selected. Furthermore, ifthe claim that Beta was technically superioris true, then the market's choice did not

represent the best economic outcome. . .(Arthur, 1994, p. 2).

Other competing technology examples cited byArthur (1994) include: the QWERTY keyboardversus other possible keyboards; gasoline versussteam and electric power for automobiles; alliumarsenide versus doped silicon in the semiconductorindustry; computer software; nuclear versus othertechnologies for the generation of electricity; andlight-water versus gas-cooled technologies fornuclear reactors (1994, pp. 15, 16, 25).It must be noted that Arthur does not deny a

role for negative returns and the analytical techni-ques of conventional economics. He fully acceptstheir applicability with respect to ``the parts of theeconomy that are resource-based (agriculture,bulk goods production, mining)'' (1994, p. 3). Theincreasingly dominant sectors of the con-temporary economy, however, are associated withthe production of high-value, knowledge-basedgoods and services such as ``computers, pharma-ceuticals, missiles, aircraft, automobiles, software,telecommunications equipment, or ®ber optics''(Arthur, 1994, p. 3). These sectors are, accordingto Arthur, ``largely subject to increasing returns''(1994, p. 3,).

Fig. 1. Increasing returns and technological lock-in. Adapted from Fig. 3 of Arthur (1994, p. 23).

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 269

These sectors dealing in high-value, knowledge-based goods and services are also the sectors forwhich, according to Lane et al. (1995), the neo-classical economists' conception of economicaction breaks down, as the importance of rationalchoice is superseded by the importance of net-works of interaction between various agents andartifacts. In these sectors increasing returns plays aunique role in the competition for adopters since,in the words of Lane and Max®eld (1997, p. 185),new con®gurations in agent/artifact space breedfurther con®gurations. . .'', generating what theyrefer to as ``complex foresight horizons'' (a notiondiscussed in detail in the next section) and radi-cally altering the nature of strategic competition.

3. Beyond ``rational choice''

A fundamental presumption of neoclassicaleconomics generally Ð a presumption that isincorporated into traditional capital budgetingtheory Ð is that all economic action is the resultof structured choices made by rational, optimizingagents. Lane et al. (1995) summarize this rationalchoice (RC) presumption as follows:

RC1 Universality: Every signi®cant economicaction is the result of a choice.

RC2 Context representation: To choose whatcourse of action to take, the agent must construethe context in which the action is to takeplace in terms of a choice situation. A choicesituation consists of a speci®cation of a set ofavailable acts and, associated with each availableact, a set of consequences that describe whatmight happen should the agent choose that act.

RC3 Rationality: The agent must select an acton the basis of a calculation of the value ofthe consequences associated with it. Thealgorithm guiding the calculation must besuch that the agent obtains some pre-speci®edmeasure of value from the chosen act. Thevalue may be speci®ed in absolute terms, orrelative to what can be attained from theother available acts.

It should be noted that this description of RC isbroad enough to encompass the notion of boundedrationality as well as the strict rationality of neo-classical economics models. This description of RC isalso consistent with the old-fashioned business schooloptimization approach to strategy in which ``A strat-egy speci®ed a precommitment to a particular courseof action. . . [and] choosing a strategy meant opti-mizing among a set of speci®ed alternative coursesof action, on the basis of an evaluation of the valueand the probability of their possible consequences''(Lane & Max®eld, 1997, pp. 169±170). This viewof strategy presumes that agents can foresee thealternative courses of action and their con-sequences, if not with certainty, then at least withenough clarity to assign probabilities. A capitalinvestment strategy, from this perspective, wouldessentially amount to a precomittment to tradi-tional capital budgeting theory. Suppose, how-ever, that the consequences of alternative coursesof action include contingencies that are unknownbut will unfold with some degree of clarity in thefuture. In such situations, an options-type capitalinvesting strategy, or value chain analysis, may beappropriate as a modi®cation of traditional capi-tal budgeting theory. But suppose that the invest-ment situation involves too many other agents andtoo many possible consequences for rational eva-luation. To use the words of Lane and Max®eld,your foresight horizons ``have become complicated''(p. 170), and traditional capital budgeting and itsstrategic variations are no longer applicable.

If you cannot even see a priori all the impor-tant consequences of a contemplated courseof action, never mind carrying out expectedgain calculations, you must constantly andactively monitor your world and react quicklyand e�ectively to unexpected opportunitiesand di�culties as you encounter them. As aresult, an essential ingredient of strategy inthe face of complicated foresight horizonsbecomes the organization of processes ofexploration and adaptation. (Lane & Max®eld,1997, p. 170).

For situations with such complicated foresighthorizons, the capabilities-based capital budgeting

270 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

strategy discussed above would seem appropriatesince it highlights the processes of exploration andadaptation.Suppose, however, that foresight horizons are

not merely complicated, but are literally complexin the full richness of that term as it is used incomplex adaptive systems theory. According toLane and Max®eld (1997), this is the decision-making situation for large segments of the con-temporary economy, especially those segmentsthat deal in high-value, knowledge-based goodsand services. It is clearly a situation in which therational choice perspective outlined above is notapplicable. Neither, therefore, is traditional capitalbudgeting theory applicable. But the claim of Laneand Max®eld is more radical yet. They argue thatsituations involving complex foresight horizonsrequire a new conceptualization of strategy. Beforeexamining their arguments regarding strategy,however, it may be useful to explore brie¯y whatthey mean by ``complex foresight horizons''.The situations of concern to Lane and Max®eld

involve networks of relationships between agents andartifacts. They use the term ``agent/artifact space'' tocharacterize such networks, and they use the term``structure'' to refer to a speci®c set of agent/artifactrelationships. Agent/artifact relationships in generalare a function of the attributions that various agentsassign to each other and to artifacts; ``[a]ttributionsabout what an artifact `is' and what agents`do'. . .'' (Lane & Max®eld, 1997, p. 182). Suchattributions play a crucial role in economic actions.

The meaning that agents give to themselves,their products, their competitors, their custo-mers, and all the relevant others in theirworld, determine their space of possibleactions Ð and, to a large extent, how they act.In particular, the meaning that agents con-struct for themselves constitute their identity:what they do, how they do it, with whom andto whom (Lane & Max®eld, 1997 p. 182).

``Complex foresight horizons'', according toLane and Max®eld, result from processes bywhich an agent's actions generate changes in thenetwork of agent/artifact relationships which, inturn, generate changes in the agent's identity.

Contrary to the rational choice model of neo-classical economics, their perspective focuses onthe interactions of agents. It is the interactions ofagents that generate changes in attributions,changes in structure of agent/artifact networks,changes in the structure of the agent's world, andchanges in the agent's identity. Following Lane etal. (1995), they use the term ``Generative Rela-tionships'' (GRs) to refer to the relationshipsamong agents that have the potential to generatesuch changes. ``The attributions, competences andentities that are constructed from GR interactionscannot be predicted from a knowledge of thecharacteristics of the participating agents alone,without knowledge of the structure and history ofthe interactions that constitute the GR'' (Lane etal., p. 15). The world constructed by interactionsforms the context within which an agent acts, butat the same time an agents actions may trigger achange in that world. Thus, not only does theagent experience ambiguity with respect to theconsequences of an action, the agent experiencesambiguity with respect to his or her own identityand the structure of the world within which s/heacts.The structure of the agent's world, i.e. thenetworks of agent/artifact relationships, is thusappropriately characterized as an emergent phe-nomena,5 a characterization that is central to Laneand Max®eld's notion of complex foresighthorizons. . . ``Emergent structure and cognitiveambiguity generate complex foresighthorizons. . .'' (Lane & Max®eld, 1997 p. 174).Lane and Max®eld (1997) support their views

about agent/artifact networks and GRs byrecounting how a small computer company oper-ating in California's silicon valley in the early1970s elected to enter the PBX market and withina few years became one of the three ®rms dom-inating the industry, with a market share that wasexceeded only byATT. The small computer company

5 In the language of complex systems theory, ``emergent

phenomena'' refers to phenomena that exhibit features that are

not to be found in any of their constituent parts. Emergent

phenomena result from the interaction or organization of the

parts. Consciousness is thus an emergent phenomena in that

the neurons that collectively produce consciousness are, indivi-

dually, totally devoid of consciousness.

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 271

was ROLM,6 and the opening they perceived wasa direct result of a 1968 decision by the US Fed-eral Communication Commission (in the Carter-phone case). Prior to this FCC decision, localtelephone companies enjoyed monopoly statuswith respect to PBX systems, the systems thatmanage the routing of incoming calls to an orga-nizations internal telephone system. The FCCs1968 decision ended the monopoly of local phonecompanies. New ®rms immediately began enteringthe PBX business. ``In particular, a whole newkind of business was created: the interconnect dis-tributors who con®gured, installed, and main-tained business communication systems'' (Lane &Max®eld, p. 176). But until ROLM entered thebusiness the basic technology employed in PBXsystems did not change signi®cantly. ``Most PBXsstill used electromechanical switching technologyand had only a few `convenience' features like call-forwarding'' (Lane & Max®eld, p. 175).In 1973, ROLM determined that it was both

technically possible and economically feasible toproduce and sell PBX systems that employeddigital switching and computer-based control.``Digital switching would provide the means tointegrate voice and data into a single system, whilecomputer control would make possible such addi-tional functions as least-cost routing of long-dis-tance calls, automatic dialing, and call-detailrecording Ð and would permit an organization tomove telephone numbers from o�ce to o�ce justby typing commands at a keyboard, rather thanby ripping out and rewiring cable'' (Lane & Max-®eld, 1997, p. 176). The success of their idea isindicated by the fact that, in 1973 ROLM hadannual revenues of $4 million, but 5 years after theinstallation of their ®rst PBX they had annualrevenues of over $200 million.At ®rst glance, it might appear that the expla-

nation of ROLM's success was essentially due to

their technological breakthrough. But Lane andMax®eld (1997) challenge that explanation: ``Wethink the right explanation is social, not tech-nological. . .'' (p. 176). They point out that,although the Carterphone decision broke themonopoly of local phone companies, it did noth-ing to alter the established patterns of interactionamong relevant agents. So, even 5 years after the1968 FCC decision, when the telecommunicationsmanager (TM) of a large company needed toorder a new PBX system, s/he typically simplycontacted the local phone company for informa-tion about the available options and followed thephone company's recommendation. Lane andMax®eld point out that, ``. . .TMs tended to be ex-telephone company employees, with little incentiveto be creative Ð or training or experience in howto be creative managers, even if the will werethere'' (p. 177). Nor did the 1968 decision do any-thing to alter the attributions assigned to PBXsystems. The suppliers of PBXs, the higher levelmanagement of ®rms, and the TMs all tended toshare the same notion about a PBX: ``. . .in parti-cular, that a PBX is just a switchboard connectedto telephone sets at one end and an outside line atthe other; and that managing a PBX means mak-ing sure that there is a serviceable telephone oneach desk where one is needed'' (Lane & Max®eld,p. 177).What ROLM did, in addition to their technolo-

gical innovation, was to change the pattern ofinteractions; a move which fortuitously facilitatedthe development of generative relationships, newproduct attributions, and new identities.

When ROLM contracted with an inter-connect distributor, it required the dis-tributor's sales people to attend a ROLMtraining program, sta�ed by instructorsrecruited from IBM and Xerox. Second,ROLM sought to establish direct relation-ships with the TMs of large ®rms such asGeneral Motors, Allied Stores, and IBM. Itdid this by creating a group of ``nationalaccounts'' representatives, ROLM employeeswhose mandate was to provide ``liaison andsupport'' to major customers. But the repre-sentatives' ®rst task was to start talking to

6 Lane and Max®eld (1997) had access to detailed informa-

tion about ROLM and the sequence of events they relate. They

note that, ``Our version of the story relies on various ROLM

marketing and strategy documents currently in possession of

one of us (RM), a cofounder of ROLM who led its PBX divi-

sion, and material collected in a Stanford Graduate School of

Business case prepared by Professor Adrian Ryans'' (p. 175,

n. 12).

272 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

their targeted TMs, to let them know whatthe ROLM technology would be able to dofor them, to ®nd out what their problemswere, and to ®gure out how ROLM couldhelp solve them. (Lane & Max®eld, 1997, pp.178±179).

The resulting interactions culminated in a seriesof new shared understandings of what ROLM'sPBX technology could do (new attributions thatwent far beyond what the ROLM engineers andrepresentatives originally were aware of) and whatkinds of revenue-enhancing/cost-saving measurescould be proposed by TMs to their higher man-agement (measures that went far beyond what theTMs were originally aware of). In short, theinteractions initiated by ROLM culminated notjust in a technologically improved PBX, they cul-minated in a series of new products; the PBXbecame a new artifact, playing a completely dif-ferent role in agent/artifact networks. ``In time,the very idea that users had about a PBX waschanged Ð from a telephone system, to an intelli-gent interface between a company and outsiders,to a tool that could be adapted to solve a widerange of `line-of-business' voice-based applica-tions, providing productivity improvements inmany aspects of customers' operations'' (Lane &Max®eld, p. 180). Among other things the ROLMtechnology was reprogrammed to become anautomatic call distribution (ACD) system whichcould be used for ``order processing, customerservice, account information, and so on'' (Lane &Max®eld, p. 180). The ROLM PBX could also bemodi®ed to provide ``what came to be called Cen-tralized Attendant Service'' (Lane & Max®eld,p. 180), a service which allowed an organization touse a centralized bank of operators to process callsto any number of outlets or stores at di�erentlocations.Not only did ROLM bene®t from these new

attributions to its PBX technology, in their own®rms many of the TMs who initiated the purchaseand implimentation of the new technologyacquired a new status with new roles, newresponsibilities and a new structure of rewards.``From a relatively low-level `custodian' of a com-pany's telephonic system, the TM began to be

perceived as a major factor in the ability of acompany to enhance its productivity and torespond to customers. In many companies, the posi-tion became equal in importance to the informationsystems manager, often with a vice-presidencyattached'' (Lane & Max®eld, 1997 p. 180). Fur-thermore, Lane and Max®eld (p. 180) note thatmany of the TMs developed an intense loyalty toROLM, sometimes exceeding their loyalty to theirown employers, a fact which further enhanced thesuccess of ROLM. As described by Lane andMax®eld, many of the TMs were members of theInternational Communications Association whichheld an annual convention. ``At these conventions,ROLM backers in the association gave formalpresentations describing productivity-enhancingapplications of the ROLM system Ð and after-wards, over drinks in the bar, talked about thepersonal rewards and recognition they had wonfor championing ROLM inside their companies.As a result, other TMs actively sought out ROLMand its distributors'' (Lane & Max®eld, p. 181).Within 5 years of installing their ®rst PBX system,ROLM controlled 23% of the US PBX market(Lane & Max®eld, p. 182).So, what are the implications of all this for strat-

egy? From Lane and Max®eld's (1997) frameworkof foresight horizons, three relatively distinct stagesof strategic focus can be delineated. First, whenforesight horizons are relatively clear, strategy canbe described as an attempt to control outcomes.This view of strategy was widely relevant when, inthe words of Stalk et al. (1992), the economywas``characterized by durable products, stablecustomer needs, well-de®ned national and regionalmarkets, and clearly de®ned competitors. . .''.(p.62). This is the perspective in which traditionalcapital budgeting theory is more or less applicable.But when new products proliferate, customerwants and needs change rapidly, and markets andcompetitors can no longer be clearly de®ned, thenin the words of Lane and Max®eld, ``foresighthorizons have become complicated'', outcomes areno longer predictable, let alone controllable, andtraditional capital budgeting theory is no longerapplicable. With complicated foresight horizons,the emphasis of strategy shifts from outcomes toprocesses, and the emphasis of capital budgeting,

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 273

according to Stalk et al. (1992), should shift to acapabilities perspective, which focuses on the pro-cesses of exploration and adaptation. But whenforesight horizons are not merely complicated, butare complex, in the sense indicated above, Lane andMax®eld argue that strategy should focus on a dif-ferent set of processes, the processes of interaction.Noting that ``strategy'' is usually situated

``within a suite of concepts'' that includes vision,mission, goals, and tactics, Lane and Max®eld(1997, p. 189) customize these concepts to ®t theirlanguage. They suggest that a ®rm's vision andmission culminate in ``directedness in agent/arti-fact space''. That is, vision and mission specify thekinds of artifacts the ®rm intends to create, iden-ti®es the agents to whom the ®rm wishes to sellthose artifacts, and establishes the direction ofchange in agent/artifact space that the ®rm wishesto initiate. They expand the usual notion of goals(in terms of desired outcomes) to include desired``recon®gurations of agent/artifact space''. Theyuse the term ``tactics'' in the conventional sensehaving to do with the process of executing theactions they decide upon. They then locate ``strat-egy'' as follows:

Strategy lies between directedness and execu-tion. It lays down ``lines of action'' that the®rm intends to initiate and that are supposedto bring desired outcomes. Since outcomesdepend on the interactions with and betweenmany other agents (inside and outside the®rm's boundaries), strategy really representsan attempt to control a process of interactions,with the ®rm's own intended ``lines of action''as control parameters (Lane & Max®eld, pp.189±190).

The attempts to control the process of interac-tions suggests ``a set of practices, which are partlyexploratory, partly interpretive, and partly opera-tional'' (Lane & Max®eld, 1997 p. 191). Lane andMax®eld particularly emphasize two kinds ofpractices that they characterize as ``populating theworld'' and ``fostering generative relationships''. The®rst of these has to do with the fact that the rapidlychanging structure of agent/artifact relationshipstends to render original assumptions about agents

and artifacts obsolete. ``Hence, the strategic needfor practices that help agents `populate' theirworld: that is, to identify, criticize, and reconstructtheir attributions about who and what are there''(Lane & Max®eld, p. 191). These are essentiallydiscursive practices of ongoing interpretation andreinterpretation of agent/artifact attributions andrelationships. Lane and Max®eld (pp. 191±193)o�er several observations regarding the detailedcharacteristics of such practices, but they sum-marize succinctly as follows: ``. . .it ought to be topmanagement's strategic responsibility to makesure that interpretive conversations go on at allrelevant levels of the company Ð and that su�-cient cross-talk between these conversations hap-pens so that attributions of the identities of thesame agents and artifacts made by people orgroups with di�erent experiences and perspectivescan serve as the basis for mutual criticism andinspiration to generate new and more useful attri-butions'' (p. 193).They suggest, however, that ongoing interpreta-

tion of emerging structure is, by itself, too passive.The ®rm can attempt to control the processes ofinteraction more aggressively if it engages in prac-tices designed to selectively encourage certaintypes of relationships. These are the practices thatthey characterize as ``fostering generative rela-tionships''. And the relationships that should beencouraged are those with the greatest potentialfor generating new attributions and new structuresof agent/artifact relationships. Presumably, if the®rm is in on the ground ¯oor with respect toattributional shifts, and is actively engaging ininterpretive practices, then it will be at a strategicadvantage in responding to those changes. Agentsshould, accordingly, be encouraged to actively``monitor relationships for generativeness'' (Lane& Max®eld, 1997, p. 197). And such monitoring islikely to be more e�ective if agents can identifyand recognize indicators of generative potential.Lane and Max®eld thus discuss the following assome of the ``essential preconditions of genera-tiveness'' (pp. 194±195):

. Aligned directedness The participants in therelationship need to orient their activities in acommon direction in agent/artifact space. . .

274 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

. Heterogeneity . . .generativeness requires thatthe participating agents di�er from oneanother in key respects. They may have dif-ferent competencies, attributions or access toparticular agents or artifacts. . ..

. Mutual directedness Agents need more thancommon interests and di�erent perspectivesto form a generative relationship. They alsomust seek each other out and develop arecurring pattern of interactions out of whicha relationship can emerge. . ..

. Permissions Discursive relationships arebased on permissions for the participants totalk to one another about particular themesin particular illocutionary modes (requests,orders, declarations, etc.). These permissionsare granted explicitly or implicitly by super-ordinate agents and social institutions.Unless potential participants in a relation-ship have appropriately matched permis-sions, or can arrogate these permissions tothemselves, the generative potential of therelationship is blocked.

. Action opportunities . . ..Engaging in jointaction focuses talk on the issues and entitiesof greatest interest Ð those around whichthe action is organized. And action itselfreveals the identities of those engaged in it.In addition, new competencies emerge out ofjoint action, and these competencies canchange agents' functionality and, hence,identity Ð even leading to the formation of anew agent arising from the relationship itself(Lane & Max®eld, pp. 194±195).

If an agent is aware of these preconditions, thensteps can be taken to strengthen the ones that existand/or to promote one that is missing. Withrespect to the ROLM case, for instance, thedevelopment of user groups promoted hetero-geneity and aligned directedness, the promotion ofaccount representative/TM relationships fosteredmutual directedness and action opportunities.And with respect to permissions, it is fair to saythat much of ROLM's success was due to the factthat the ®rm actively facilitated the exchange ofproblems, ideas, information, requests, etc.between account representatives and TMs, and

between account representatives and ROLM's engi-neers. A more hierarchically compartmentalizedcompany would have missed some of the key oppor-tunities that ROLM was able to take advantage ofas a result of providing permission for discursiveexchanges between di�erent groups within the ®rmas well as between the ®rm's representatives andagents from other ®rms. In summary, as Lane andMax®eld (1997) demonstrate with the ROLMcase, ``[t]o realize generative potential, relationshipparticipants must have the right permissions, time,and space to talk; they must do work together;and that work must facilitate their coming toshared understandings about each others' compe-tencies and attributions of identity; and their rela-tionship must be embedded in a network of otherrelationships that can amplify whatever possibi-lities emerge from their joint activities'' (p. 196).All of this has clearly moved miles (in con-

ceptual strategic space) from the rational choicemodel of Panglossian capital budgeting theory.But it brings us much closer to the computersimulation models that are fundamental to theSanta Fe Institute's research program. Just asagent based interactions were at the heart of Laneand Max®eld's (1997) ROLM story, interactionsbetween arti®cial agents are at the heart of theSFI's most heralded computer simulation models,models that are generally characterized as arti®ciallife models. ``Arti®cial life (alife) is the bottom upstudy of basic phenomena commonly associatedwith living organisms, such as self-replication,evolution, adaptation, self-organization, parasit-ism, competition, and cooperation'' (Tesfatsion,1997, p. 534). In his provocatively titled article,``How Economists can get Alife'', Tesfatsion refersto the numerous ways in which arti®cial life simu-lations are enhancing our understanding of com-plex issues in evolutionary economics. Could alifesimulation models also shed light on some of thecomplex issues in capital investing theory?

4. Should capital investment theorists get ``alife''?

The usefulness of computer-based simulationwith respect to capital investment decisions hasbeen argued by some theorists for at least 35 years.

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 275

Following the pioneering work of Hertz (1979,1968), most of these approaches have relied uponnormal probability statistical methods to simulaterates of return for projects when various factors(that are subjectively believed to in¯uence returns)are randomly selected and combined. Repeatedsimulations with di�erent combinations of rele-vant factors yields, according to Hertz (1968), a``risk-based pro®le'' for the project at issue. Suchsimulation models are variously referred to as``Hertz-type risk simulation'' or simply as``sophisticated risk analysis'' (Ho & Pike, 1991,1998).Using the language of Lane and Max®eld, these

types of computer-based simulation models maybe useful in situations with complicated foresighthorizons, but they fail to ®ll the bill with respect tothe increasing returns sectors of the economy inwhich the macro structure of economic and ®nan-cial reality tend to be emergent phenomena thatresult from the interactions of agents who are act-ing in accordance with their respective subjectivebeliefs which, in turn, are largely emergent phe-nomena. The SFI view of economic agents' sub-jective beliefs and their role in economic activityhas been described by Arthur (1995, p. 20) as fol-lows:

Economic agents make their choices basedupon their current beliefs or hypotheses. . .about future prices, or future interest rates, orcompetitors' future moves, or the futurecharacter of their world. And these choices,when aggregated, in turn shape the prices,interest rates, market strategies, or worldthese agents face. The beliefs or hypothesesthat agents form in the real economy are lar-gely individual and subjective. They are oftenprivate. And they are constantly tested in aworld that forms from their and others' sub-jective beliefs. Thus at a sub-level, we canthink of the economy ultimately as a vastcollection of beliefs or hypotheses, constantlybeing formulated, acted upon, changed anddiscarded; all interacting and competing andevolving and co-evolving; forming an oceanof ever-changing, predictive models-of-the-world. This view is useful, I believe, because it

forces us to think about how beliefs createeconomic behavior Ð and how economicoutcomes create beliefs. And it leads to dif-ferent insights. Beyond the simplest problemsin economics, this ecological view of theeconomy becomes inevitable; and it leads to aworld of complexity.

Arthur and his SFI colleagues have used thegenetic algorithms and Classi®er Systems devel-oped by John Holland (1975, 1986) to create anarti®cial stock market that re¯ects the interplay ofsubjective expectations. The results of their stockmarket simulations pose fundamental challengesto Panglossian capital budgeting theory.Investors in the SFI's arti®cial stock market are

arti®cially intelligent agents who continually create``market hypotheses'' (``expectational schemas'')about future dividend and price movements. Someof the schemas relate to fundamental accountingand economic expectations and some relate to``technician-oriented'' expectations about pricepatterns. Arthur (1995) points out that the simu-lation is typically run with 100 agents, each ofwhich is endowed with a portfolio of 60 expecta-tional schemas. ``Thus there are at any time 6,000expectational models'' (Arthur, 1995, p. 24). Theseschemas, however, are not ®xed and immutable;genetic algorithms have been used to allow muta-tion, thus facilitating the formation of new sche-mas. As agents try out various schemas, theythrow out the ones that perform poorly and stickwith the ones that pay o�.The simulation runs of this market produce an

arti®cial time series that can be studied visually (interms of price patterns) or statistically. The modelhas produced results that are in accordance withconventional (Panglossian) portfolio theory, butonly when the simulation is started with parametersettings that re¯ect conventional theory: ``If westart our traders o� with identical, fundamental-value expectations (by setting the parameters of alltheir expectational models to reproduce prices thatvalidate these expectations), we ®nd that deviat-ing, nonfundamentalist expectations cannot get afooting'' (Arthur, 1995, p. 24). However, when theresulting time series generated under these specialcircumstances is compared with actual stock market

276 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

price movements, the arti®cial market looksextremely bland and unrealistic: ``The market in asense in this regime is essentially `dead''' (Arthur,1995, p. 25).On the other hand, when a simulation run

begins with heterogeneous expectational schemas,the market ``comes to life'' (Arthur, 1995, p. 25).Trends emerge when expectational schemas bychance produce price movements that become self-reinforcing, often producing price bubbles thatmove prices signi®cantly away from fundamentalvalues. The market also occasionally producescrashes when trends reverse. When expectationsbegin to converge, the market may enter a periodof stability. But this stability never lasts becausesome of the expectational models begin to exploit thepattern of stability. ``Then there will be swift changesof gestalt, swift readjustments in expectations thatchange the market itself and cause avalanches offurther change'' (Arthur, 1995, p. 25). Thus, theresulting time series often exhibits periods of rela-tive price stability followed by prolonged periodsof high volatility.In sum, the SFI's arti®cial stock market bears a

remarkable resemblance to the stock market asdescribed by John Maynard Keynes: ``. . .it is, soto speak, a game of Snap, of Old Maid, of MusicalChairs Ð a pastime in which he is victor who saysSnap neither too soon nor too late, who passes theOld Maid to his neighbor before the game is over,who secures a chair for himself when the musicstops'' (1936, pp. 155±156). It is a game infusedwith ``animal spirits'' (Keynes, pp. 161±162). It is agame in which ``we devote our intelligences toanticipating what average opinion expects theaverage opinion to be'' (Keynes, p. 156).The SFI's arti®cial stock market is a prime

example of an alife model that is relevant to thecritique of traditional capital investment decisiontheory. But given the discussions, in previous sec-tions, of the strategic aspects of capital investmentdecisions, a more important question is whethersuch models can be used to shed light on issuesrelated to capital investment strategy. I suggestthat the answer to this question is ``yes''.Consider a model reported by Dalle (1998) that

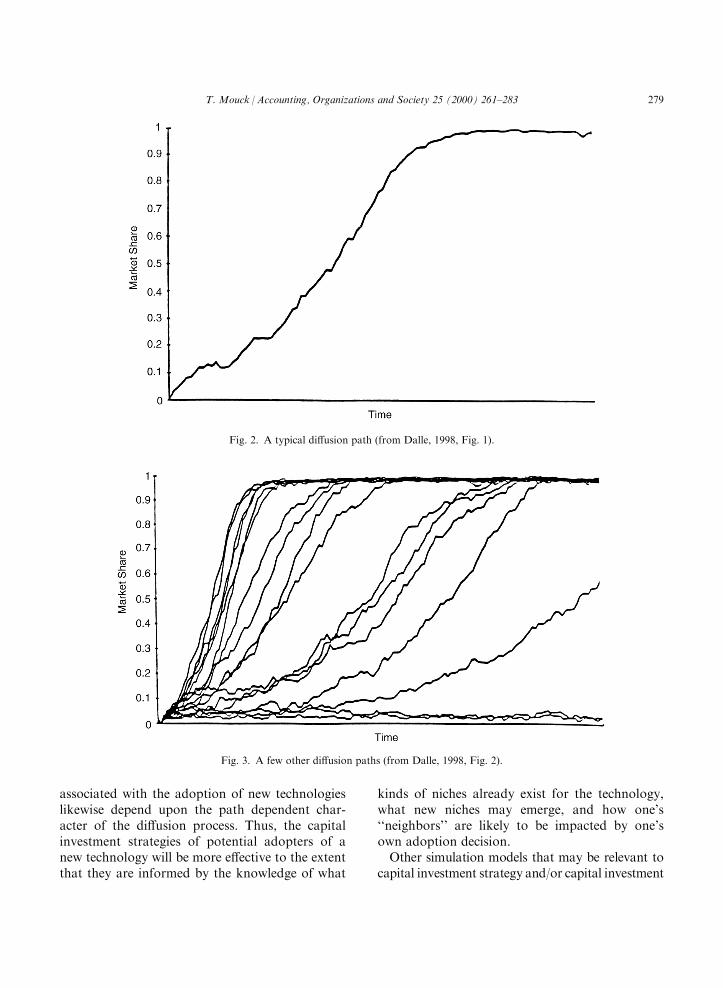

simulates the di�usion of a new technology. In thismodel, the potential adopters of a new technology

are heterogeneous ®rms. Each ®rm has an adop-tion decision rule that is a function of adoptioncosts (including the costs of switching from the oldtechnology) versus the potential pro®t and risksassociated with the new technology. The adoptiondecision rules di�er from ®rm to ®rm as a result ofdi�erences in products, markets, size, organiza-tion, knowledge base, learning processes, etc. Butdespite these di�erences, each ®rm is part of a``local interaction structure'', explained by Dalle(p. 245) as follows:

When one of the `neighbors' of a ®rmadopts the technology, this contributes toreducing the adoption costs and risks for this®rm, or indeed increases the costs and risksassociated with the decision not to adopt.There are many reasons for this. . ., notablyrelated to problems of technological compat-ibility and accessibility to knowledge andspeci®c information acquired by others,which therefore reduce adoption costs andrisks. Technological adoptions are thereforelocally cumulative: the adoption decision ofeach agent. . . take[s] into account the deci-sions of a certain number of other agents, i.e.his `relevant neighbors'. . . with whom he isinteracting. We can therefore attribute toeach of these agents a neighborhood, that isto say a group of agents with whom he isinteracting: if we then assume that theseneighborhoods are interconnected. . ., weobtain what we propose to call a connectedlocal interaction structure.

The simulations reported by Dalle (1998) arebased on interaction structures in which eachagent has four immediate neighbors. Statisticalbehavior functions are speci®ed with respect to theprobability that a given ®rm will adopt the newtechnology if zero, one, two, three, or four of itsneighbors, respectively, have already adopted thetechnology. On the assumption that networkexternalities (Arthur's positive returns to adoptiondiscussed earlier) will reduce the costs and risksassociated with the new technology as it is adop-ted by more and more of a ®rms neighbors, ahigher probability of adoption is speci®ed if one

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 277

neighbor has adopted than if no neighbors haveadopted. A still higher probability is speci®ed if twoneighbors have adopted than if only one neighborhas adopted, and so forth. The simulation protocolemployed by Dalle ``involves simulating trajec-tories obtained by drawing randomly, at each timestep, one agent from the population whose adoptionprobability as a function of his neighborhood isgiven by F [a statistical probability function]'' (p.247).The results indicate that heterogeneity (of

adopting ®rms) and local interactions are su�cientto account for the logistic, ``S-shaped'', di�usionpath of a new technology. A typical di�usion pathgenerated by Dalle's (1998) computer simulation isshown in Fig. 2. Dalle's simulations also indicatethat the time it takes a new technology to ``¯oodthe market'' of potential adopters is highly sensi-tive to the likelihood of early adoption. The di�u-sion path in Fig. 2 was generated by assigning 0.05and 0.10, respectively, as the probability of a ®rmadopting if none of its neighbors had adopted andthe probability of adoption if one of its neighborshad already adopted the new technology. Thesensitivity of the di�usion path, with respect toearly adoptions, was studied by altering theseprobabilities of early adoption. The variation inthe resulting di�usion paths is shown in Fig. 3.The steeper di�usions paths (the ones that repre-sent a faster ¯ooding of the market) were asso-ciated with higher probabilities of early adoption;the ¯atter di�usion paths were associated withlower probabilities of early adoption.An even more interesting ®nding, however, is that

``The taking into account of local interactions. . .provides an explanation for the formation of techno-logical niches and enclaves'' (Dalle, 1998, p. 251).There are various factors, such as size, the avail-ability of technical support, etc., which tend toreduce the adoption costs of a ®rm relative to itsneighbors, thus increasing its likelihood of earlyadoption. but the fact that adoption costs includethe costs of switching from the currently usedtechnology, suggests that some ``neighborhoods'',in which the ®rms are using the same, moreestablished technology with its own local external-ities, may as a group be more likely (or less likely,as the case may be) to adopt a new technology than

other neighborhoods which may be using a di�er-ent established technology. Such local interactionfactors account for the appearance of ``technolo-gical niches''.

The ®rst niches to appear initially growslowly, or even fail to survive, because thetechnology which is gradually being aban-doned is itself still subject to strong localexternalities which incite its users to continueto exploit it: the switching costs are still sta-tistically high, and all the more so if the ®rmis dealing with others who exploit the sametechnology. This growth then becomes muchmore rapid: due to the growth of one or moreof the niches, the remaining potential adoptershave statistically an ever increasing numberof neighbors who have already adopted it,which renders their own adoption more andmore likely. ®nally the di�usion graduallybecomes complete as the number of adoptersstill not having adopted slowly decreases: itactually tends to zero as the probability thatan adopter of the new technology returns tothe former becomes extremely weak when thequasi-totality of his neighbors have alsoadopted the new technology. (Dalle, 1998, pp.251±252)

As Dalle (1998) points out, this simulationmodel o�ers some signi®cant insights that arerelevant to capital investment strategy. If newtechnologies spread from niche to niche, and if thespeed of the di�usion process is signi®cantlyin¯uenced by early adoption behavior, then itwould behoove the producers of new technologiesto identify the potential niches with the highestlikelihood of early adoption and develop theirpromotional strategy accordingly: ``it is thereforeto these potential clients that a ®rm must initiallypay the more attention, not only because it wantsto sell, but also, so it seems, because the futuresuccess of its technology will often depend greatlyon its success in these niches, as the future adopterswill actually be greatly in¯uenced by these ®rst ones''(Dalle, p. 253). It should be noted, however, that thestrategic implications are not limited to producers ofnew technologies. The potential bene®ts and risks

278 T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283

associated with the adoption of new technologieslikewise depend upon the path dependent char-acter of the di�usion process. Thus, the capitalinvestment strategies of potential adopters of anew technology will be more e�ective to the extentthat they are informed by the knowledge of what

kinds of niches already exist for the technology,what new niches may emerge, and how one's``neighbors'' are likely to be impacted by one'sown adoption decision.Other simulation models that may be relevant to

capital investment strategy and/or capital investment

Fig. 2. A typical di�usion path (from Dalle, 1998, Fig. 1).

Fig. 3. A few other di�usion paths (from Dalle, 1998, Fig. 2).

T. Mouck /Accounting, Organizations and Society 25 (2000) 261±283 279

theory include the information contagion model(ICM) reported by Lane (1997) and the trade net-work game (TNG) reported by Tesfatsion (1997).The ICM allows for computer simulation ofagent's sequential selections of either product A orproduct B, based on their knowledge of the per-formance characteristics of A and B, respectively.The agents' knowledge of relevant performancecharacteristics comes from two sources, publiclyavailable (but incomplete) information and infor-mation gained from privately polling a sample ofprevious adopters of A or B. The cumulativeinformation about A and B is strongly pathdependent depending largely upon relatively smalldi�erences in the pattern of early adoptions and/or the chance di�erences in early polling results.Lane (p. 105) makes an apt comparison with theprocess of deciding what movie to see.

Suppose you are thinking about seeing amovie. Which one should you see? Even ifyou keep up with the reviews in the news-papers and magazines you read, you willprobably also try to ®nd out which moviesyour friends are seeing Ð and what theythought of the ones they saw. So which movieyou decide to see will depend on what youlearn from other people, people who alreadywent through the same choice process inwhich you are currently engaged. And afteryou watch your chosen movie, other peoplewill ask you what ®lm you saw and what youthought of it, so your experience will helpinform their choices and hence their experi-ences as well.