beverage industry in thailand - propak asia

TRANSCRIPT

Beverage Industry in Thailand

By: Dr. Lackana LeelayouthayotinSept 1, 2020

Beverage industry situation

Carbonated drinks, energy drinks, beers and spirits are now becoming saturated or declined

Government issues many measurements to cut consumption of alcohols and beverages with high sugar content

Low purchasing power due to Covid-19 Non-carbonated drinks such as Vitamin drinks continue to

gain momentum due to health conscious attitude of consumers

VUCA worldVolatility Rate of Change is unpredictable Uncertainty Unclear about the present

Complexity Multiple key decision factors Ambiguity Lack of clarity about meaning of an event

(unknown unknows)

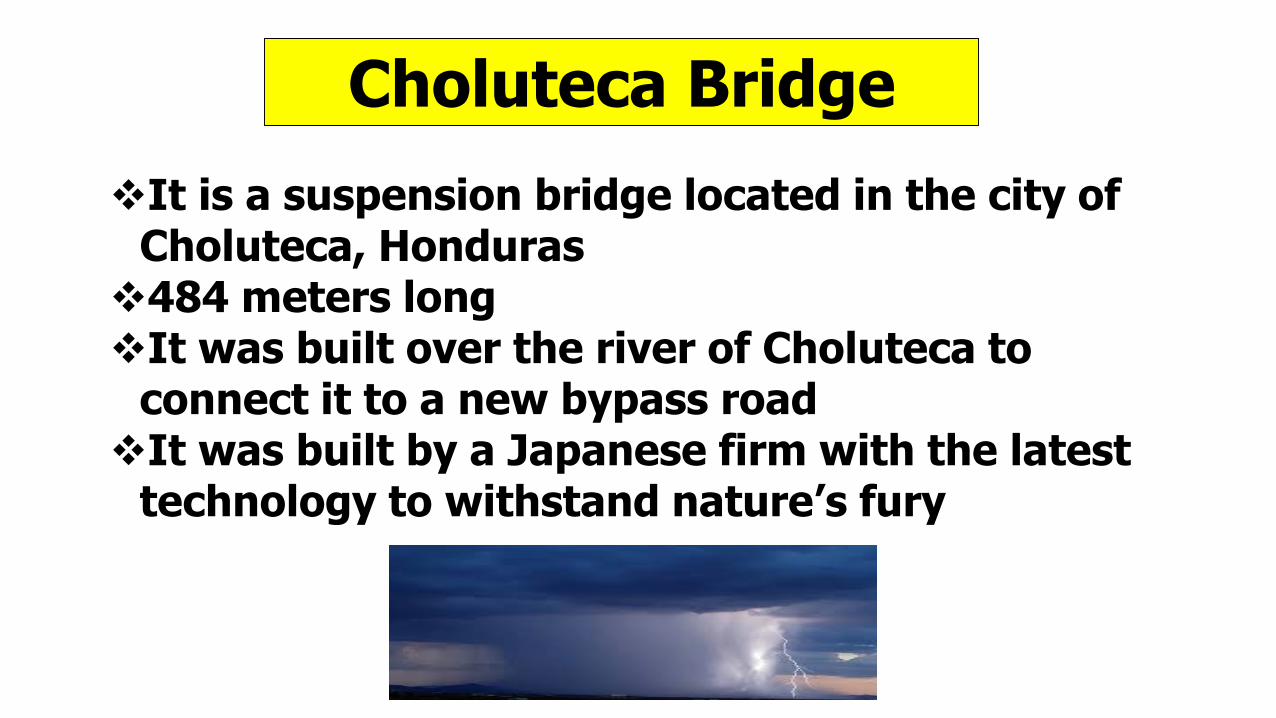

Choluteca BridgeIt is a suspension bridge located in the city of

Choluteca, Honduras484 meters longIt was built over the river of Choluteca to

connect it to a new bypass roadIt was built by a Japanese firm with the latest

technology to withstand nature’s fury

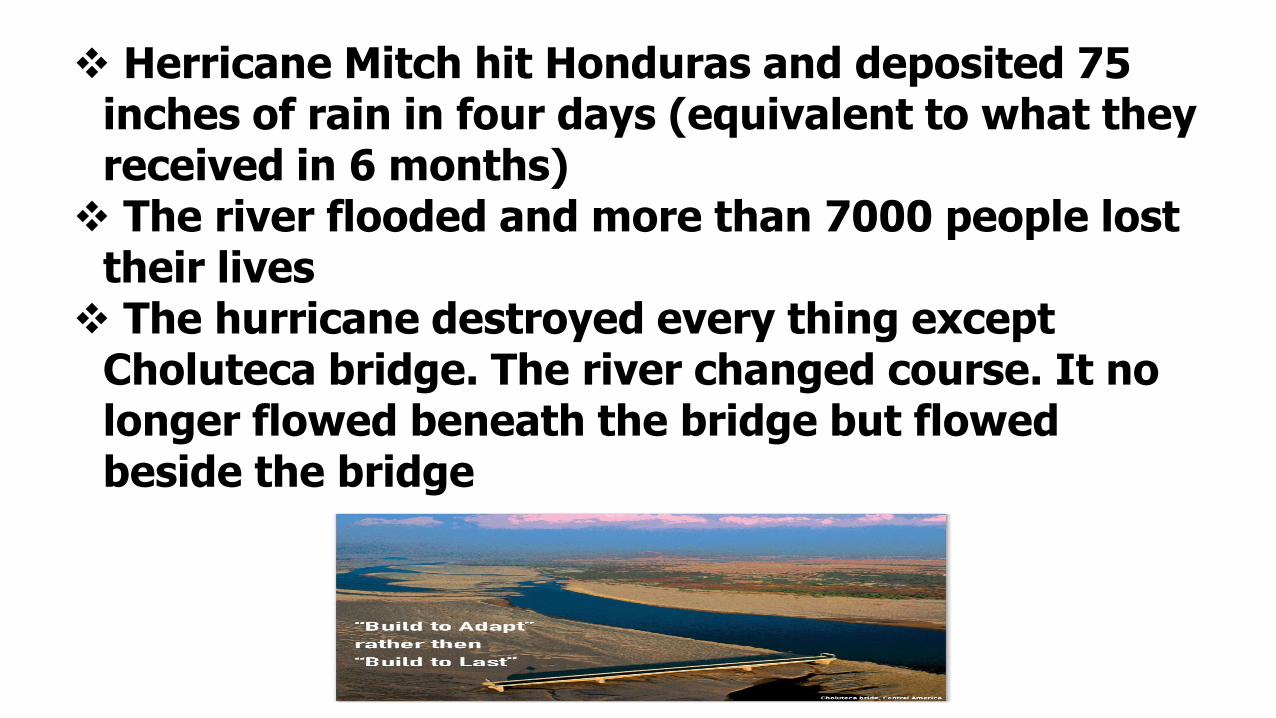

Herricane Mitch hit Honduras and deposited 75 inches of rain in four days (equivalent to what they received in 6 months) The river flooded and more than 7000 people lost

their lives The hurricane destroyed every thing except

Choluteca bridge. The river changed course. It no longer flowed beneath the bridge but flowed beside the bridge

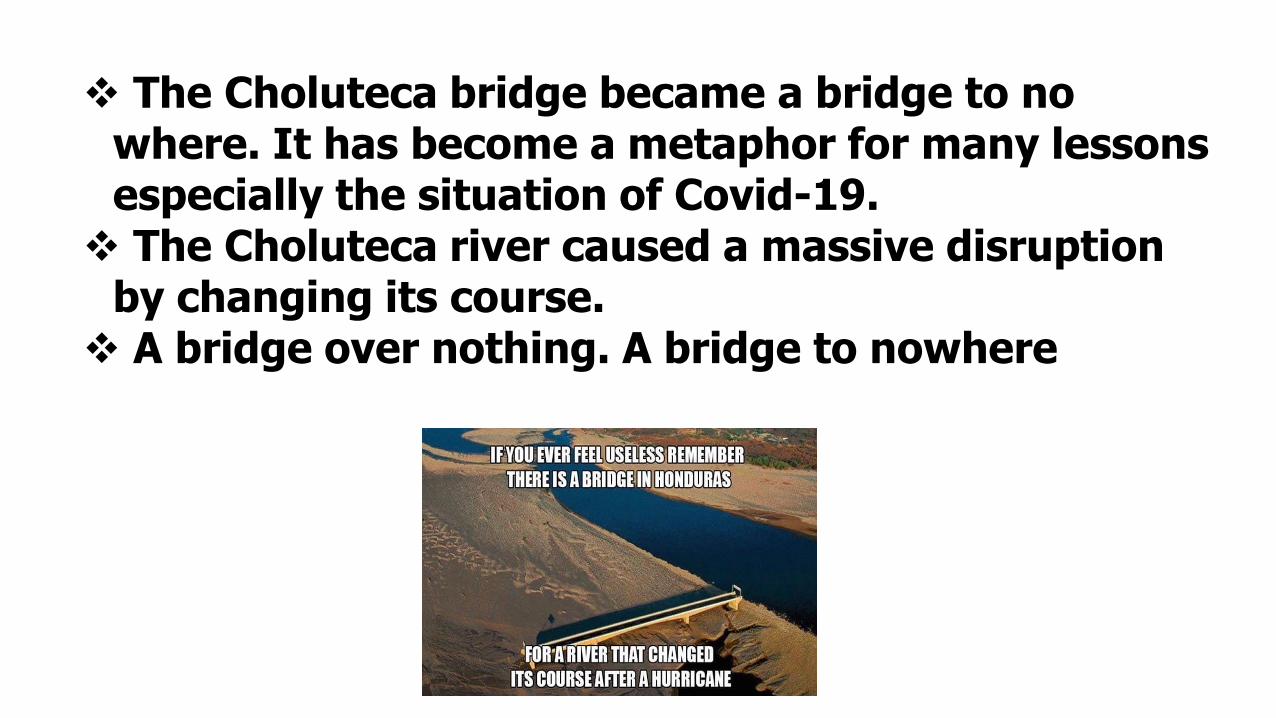

The Choluteca bridge became a bridge to no where. It has become a metaphor for many lessons especially the situation of Covid-19. The Choluteca river caused a massive disruption

by changing its course. A bridge over nothing. A bridge to nowhere

“Build to Adapt” rather than “Build to Last”

Impact from Covid 191. Financial impact

Most of businesses and people faced at least 25% income decreased. Normally Thai people were not have well plan savings. Therefore, they have to cut non-essential items, reduce their spending, etc.

2. Emotional Disturbance

People feel depressed due to the social lockdown and social distancing. People are very scare of catching the Covid virus.

3. Personal Hygiene

Thais are cautious about hygiene. 89% of Thai people use gel or handwash and 95% use mask.

4. Purchasing Power Drop

Thai people cut down and/or trade down items. They focus on the day-to-day items, less stocking and save cash.

Key strategies to survive after Covid

TouchlessWe have to adapt our business model to serve them. Food

court in Thailand do not leave fork and spoon for users but it will be sealed and packed them for individual usage in a plastic bag. Hygiene is become a key factor for consumers to buy or consume products. Products and services must meet this requirement

Cashless Try to avoid using cash. Mobile payment is becoming very important. More than 50 m of Thais use Internet and they spend more than 10 hours online. Mobile commerce is about half of total e-commerce and grew double digit every year.

selflessPeople want to do something good for the society and be good for other people. CSR become part of the important strategy for the organization

It is not the strongest of the species that survive,nor the most intelligentbut the one most responsive to change

Charles Darwin

New and Now!!

Mr. Nutthakorn UtensuteDirector of Tax Planning Bureau

Excise Department

Policies & Regulations to Promote Functional Beverages Industry

2

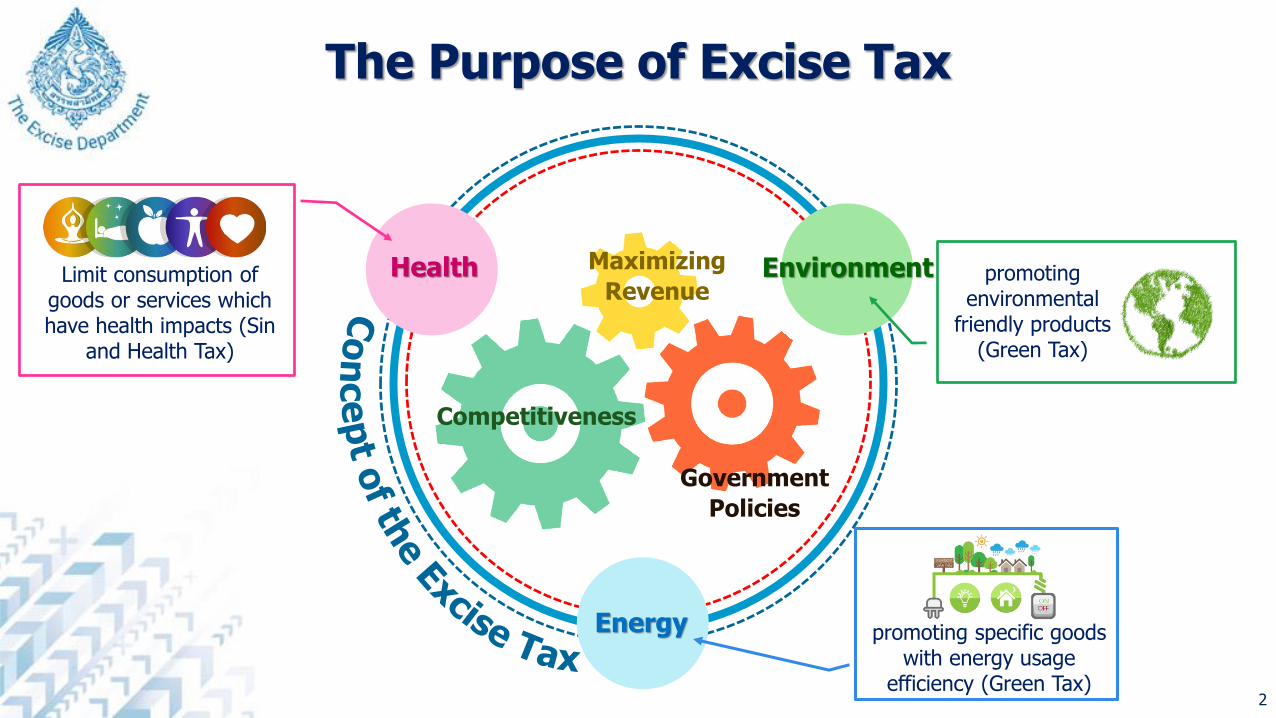

Maximizing

Revenue

Competitiveness

Government

Policies

Health Environment

Energy

Limit consumption of goods or services which have health impacts (Sin

and Health Tax)

promoting specific goods with energy usage

efficiency (Green Tax)

The Purpose of Excise Tax

promoting environmental

friendly products (Green Tax)

3

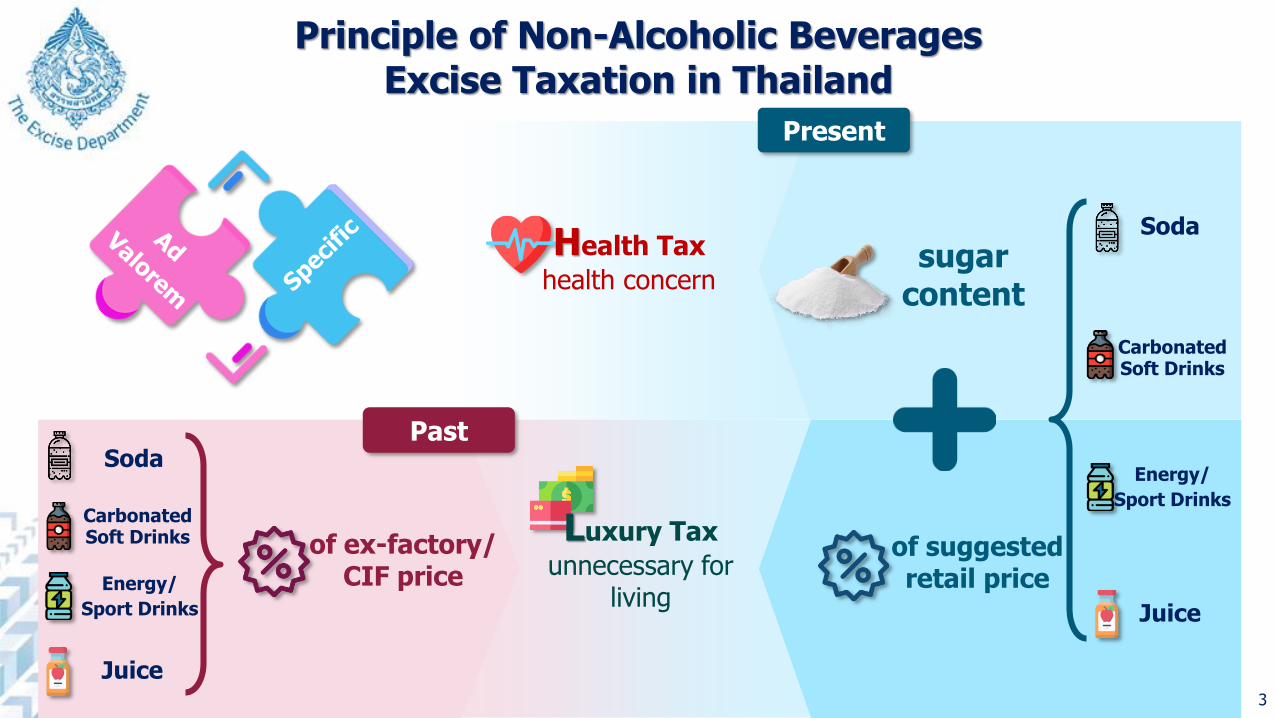

Principle of Non-Alcoholic Beverages Excise Taxation in Thailand

PastSoda

Carbonated Soft Drinks

Energy/

Sport Drinks

Juice

Soda

Carbonated Soft Drinks

Energy/

Sport Drinks

Juice

Present

Health Tax

health concern

of ex-factory/CIF price

of suggested retail price

sugar content

Luxury Tax

unnecessary for living

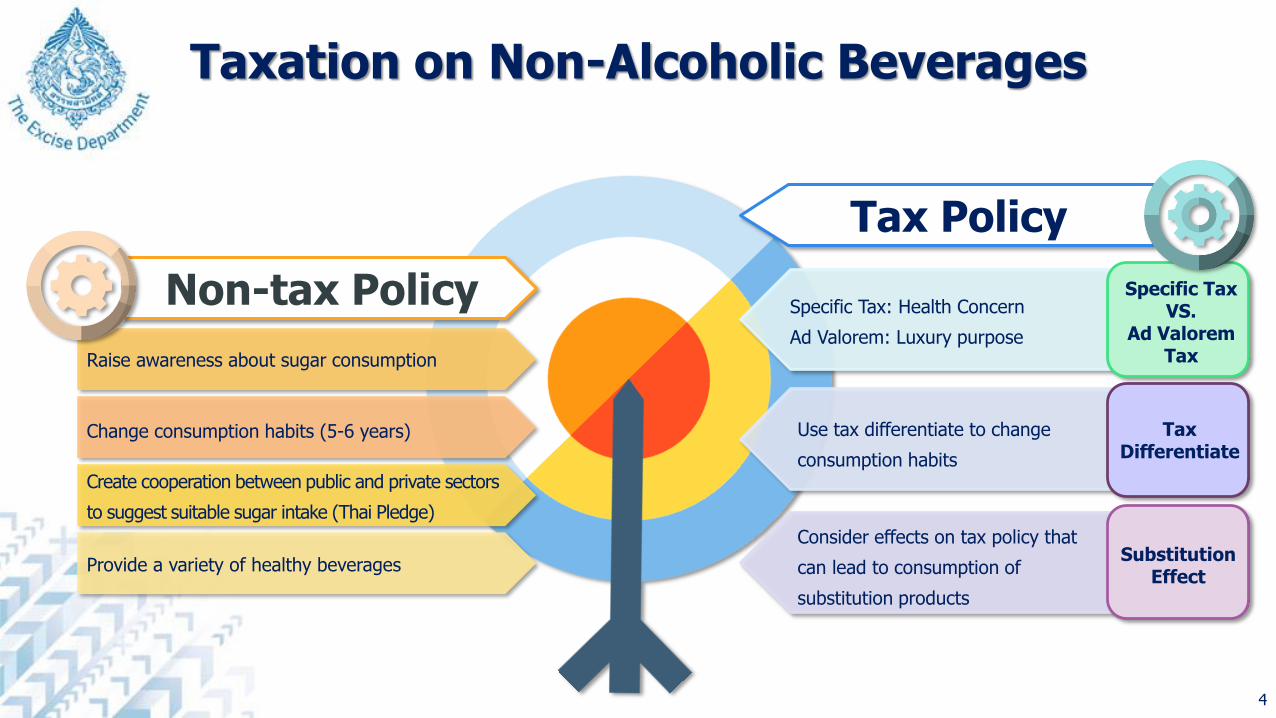

Taxation on Non-Alcoholic Beverages

4

Raise awareness about sugar consumption

Change consumption habits (5-6 years)

Create cooperation between public and private sectors

to suggest suitable sugar intake (Thai Pledge)

Provide a variety of healthy beverages

Non-tax Policy

Tax Policy

Specific Tax: Health Concern

Ad Valorem: Luxury purpose

Use tax differentiate to change

consumption habits

Consider effects on tax policy that

can lead to consumption of

substitution products

Specific Tax VS.

Ad Valorem Tax

Tax Differentiate

Substitution Effect

5

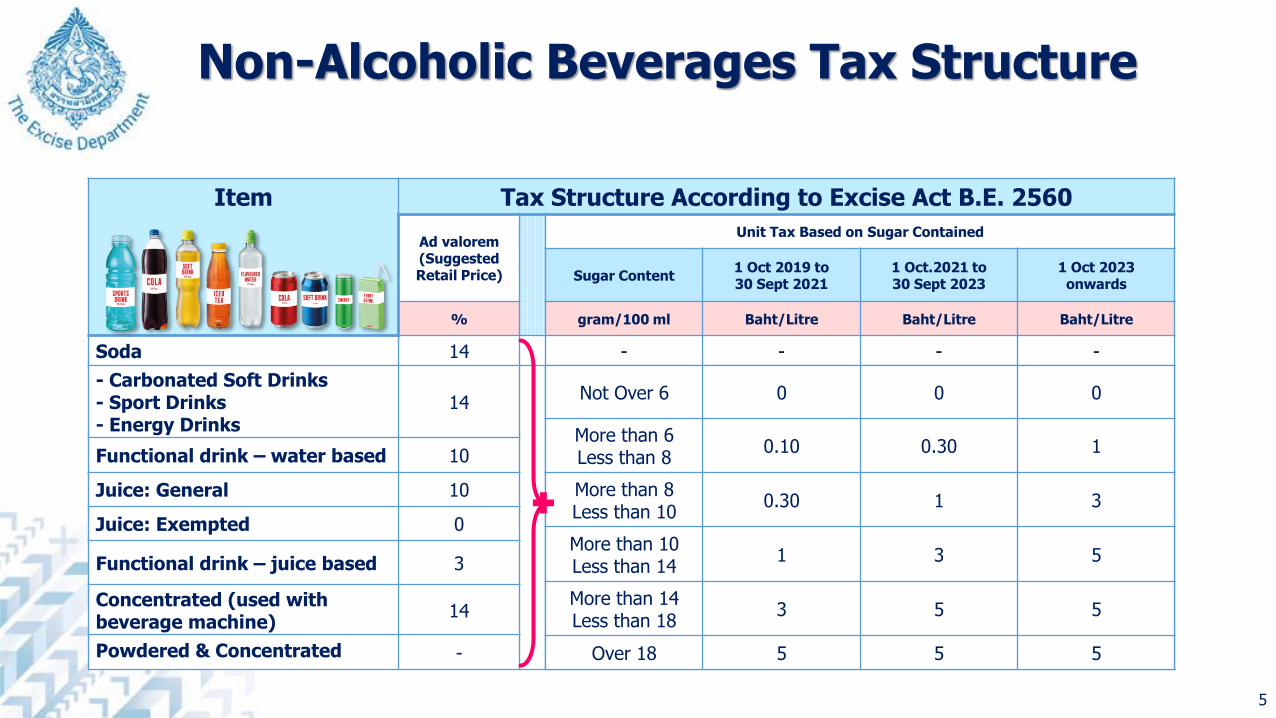

Item Tax Structure According to Excise Act B.E. 2560

Ad valorem(Suggested Retail Price)

Unit Tax Based on Sugar Contained

Sugar Content1 Oct 2019 to30 Sept 2021

1 Oct.2021 to30 Sept 2023

1 Oct 2023onwards

% gram/100 ml Baht/Litre Baht/Litre Baht/Litre

Soda 14 - - - -

- Carbonated Soft Drinks - Sport Drinks - Energy Drinks

14

Functional drink – water based 10

Juice: General 10

Juice: Exempted 0

Functional drink – juice based 3

Concentrated (used with beverage machine)

14

Powdered & Concentrated -

Not Over 6 0 0 0

More than 6 Less than 8

0.10 0.30 1

More than 8 Less than 10

0.30 1 3

More than 10 Less than 14

1 3 5

More than 14 Less than 18

3 5 5

Over 18 5 5 5

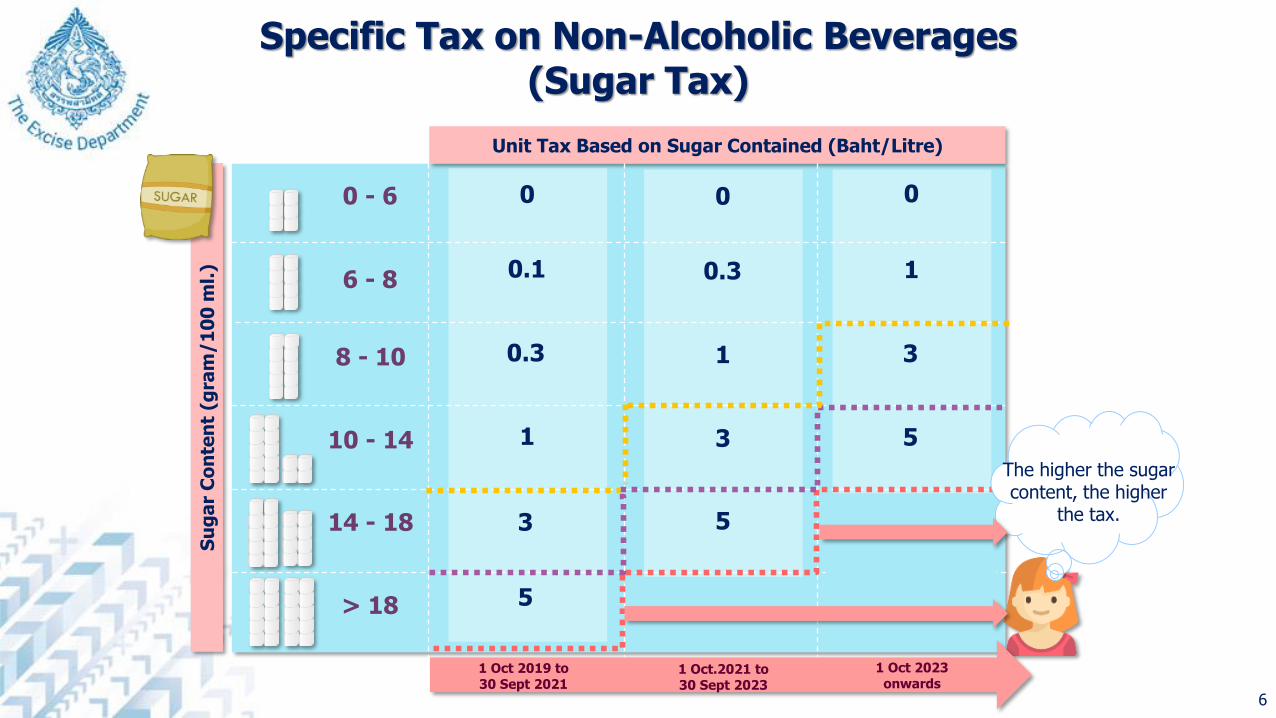

Non-Alcoholic Beverages Tax Structure

Su

ga

r C

on

ten

t (g

ram

/1

00

ml.

) 0 - 6

6 - 8

8 - 10

10 - 14

14 - 18

> 18

Unit Tax Based on Sugar Contained (Baht/Litre)

0 0 0

0.1 0.3 1

0.3 1 3

1 3 5

3 5

5

The higher the sugar content, the higher

the tax.

Specific Tax on Non-Alcoholic Beverages (Sugar Tax)

1 Oct 2019 to30 Sept 2021

1 Oct.2021 to30 Sept 2023

1 Oct 2023onwards

6

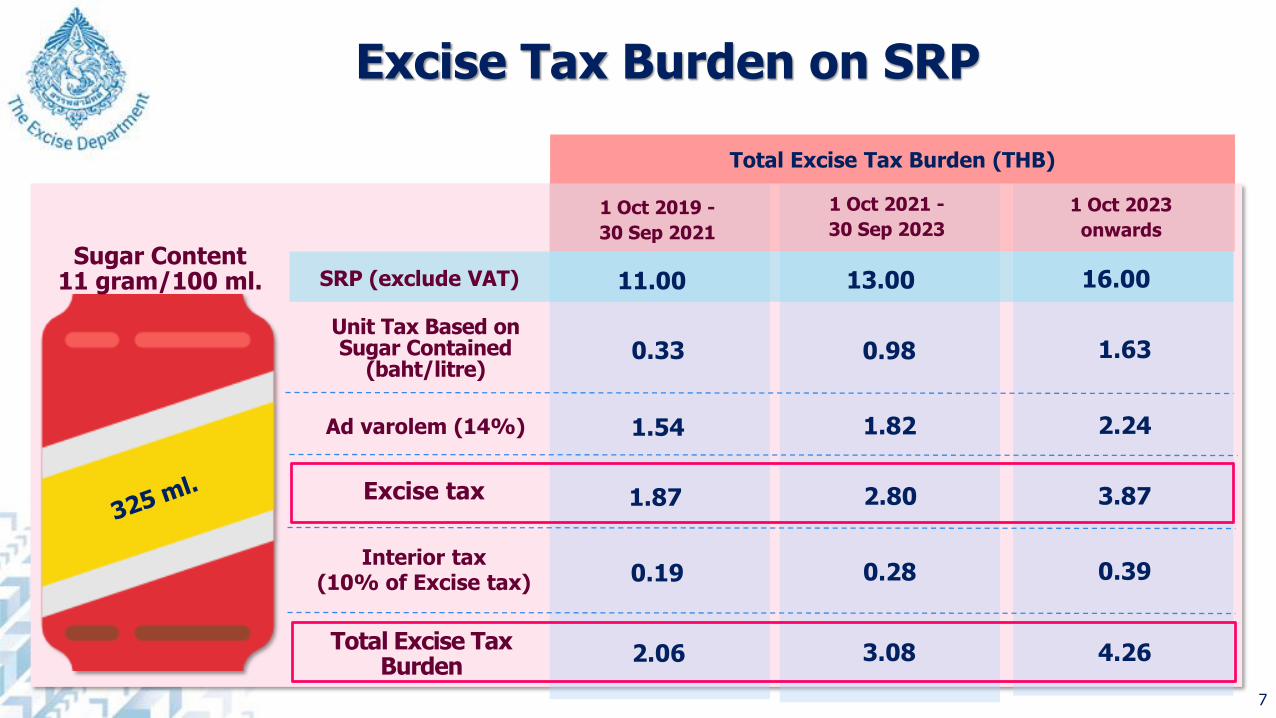

Sugar Content11 gram/100 ml.

1 Oct 2019 -

30 Sep 2021

1 Oct 2021 -

30 Sep 2023

1 Oct 2023

onwards

Total Excise Tax Burden (THB)

Ad varolem (14%) 1.54 1.82 2.24

Excise tax 1.87 2.80 3.87

Unit Tax Based on Sugar Contained

(baht/litre)0.33 0.98 1.63

Interior tax(10% of Excise tax) 0.19 0.28 0.39

Total Excise Tax Burden

2.06 3.08 4.26

SRP (exclude VAT) 11.00 13.00 16.00

7

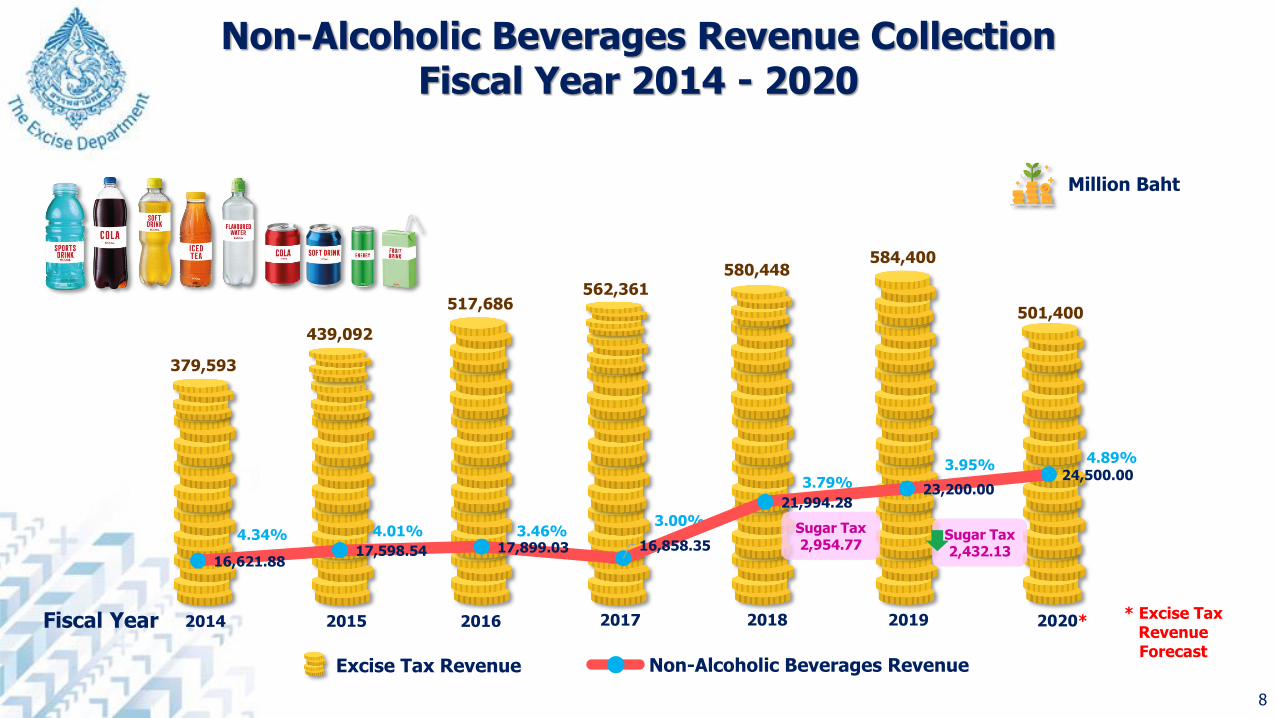

Excise Tax Burden on SRP

2014 2015 2016 2017 2018 2019

Million Baht

Fiscal Year 2020*

4.34% 4.01% 3.46%3.00%

3.79%3.95%

379,593

439,092

517,686562,361

580,448

501,400

584,400

* Excise Tax Revenue Forecast

Excise Tax Revenue Non-Alcoholic Beverages Revenue

Non-Alcoholic Beverages Revenue Collection Fiscal Year 2014 - 2020

8

4.89%

16,621.8817,598.54 17,899.03 16,858.35

21,994.2823,200.00

24,500.00

Sugar Tax2,954.77

Sugar Tax2,432.13

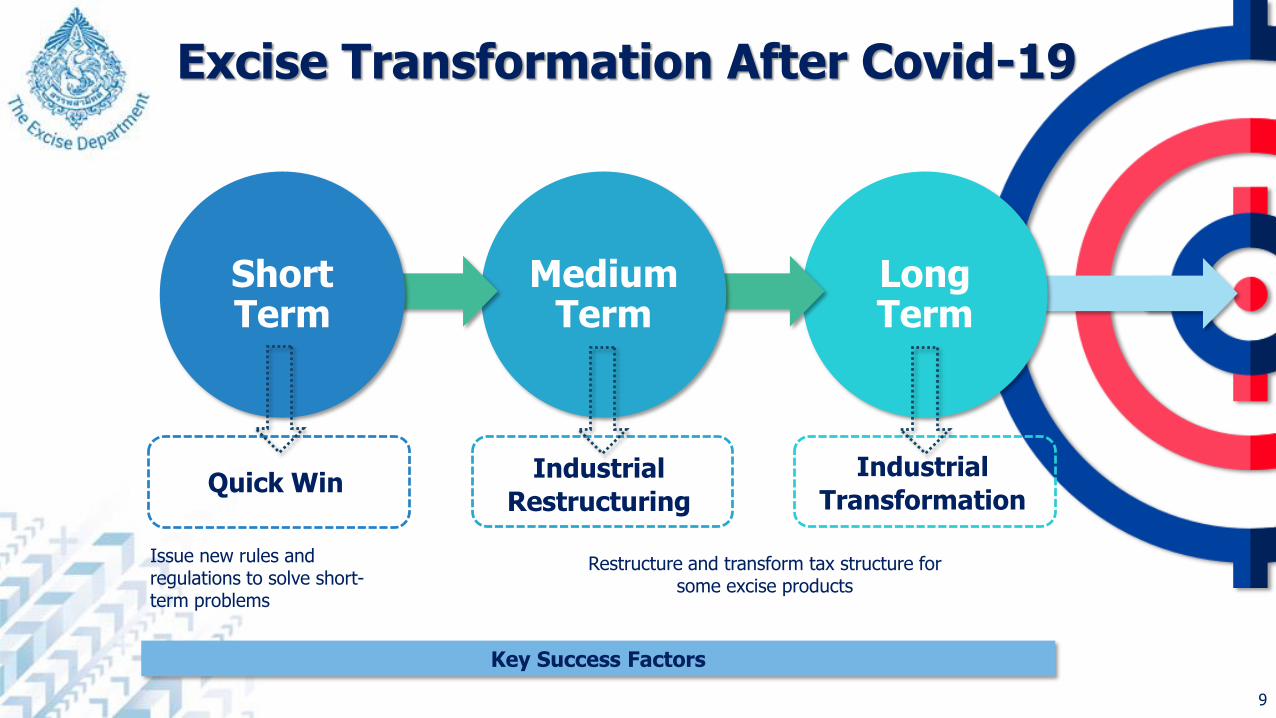

Long Term

Medium Term

Short Term

Quick Win Industrial

Restructuring

Industrial

Transformation

Key Success Factors

Issue new rules and regulations to solve short-term problems

Restructure and transform tax structure for some excise products

9

Excise Transformation After Covid-19

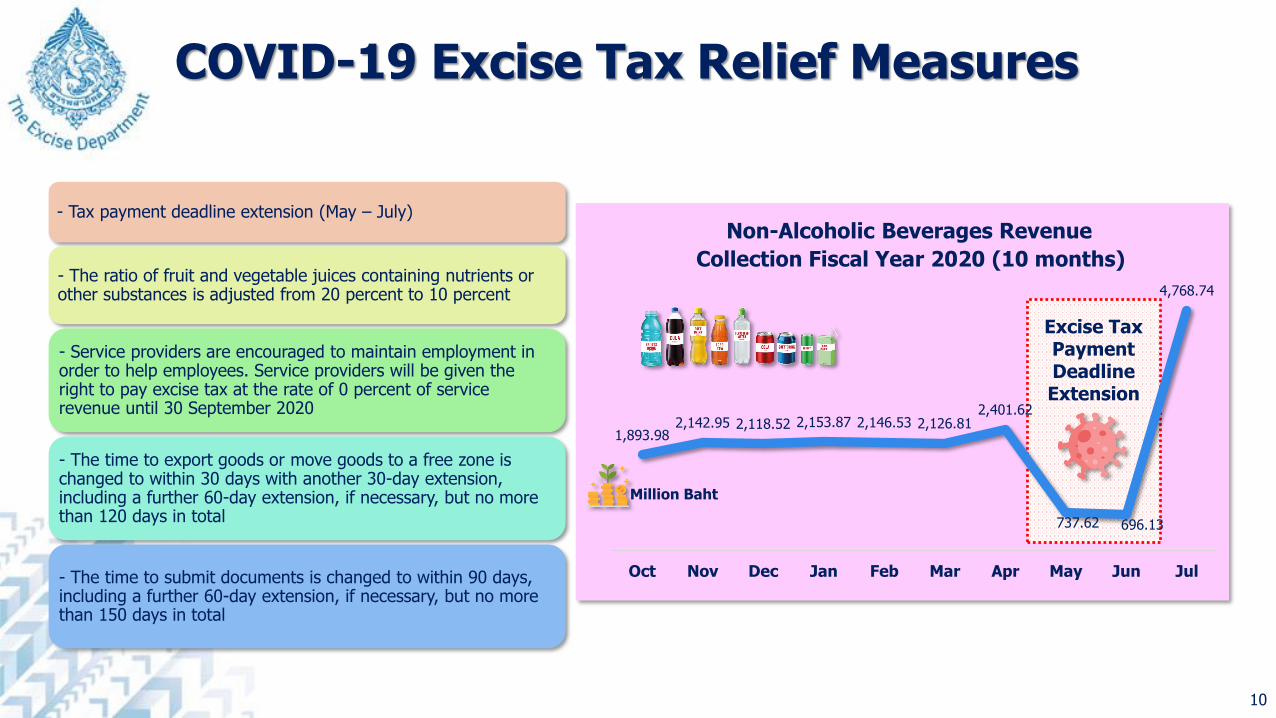

10

Excise Tax Payment Deadline Extension

Non-Alcoholic Beverages Revenue

Collection Fiscal Year 2020 (10 months)

1,893.982,142.95 2,118.52 2,153.87 2,146.53 2,126.81

2,401.62

737.62 696.13

4,768.74

Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Million Baht

- Tax payment deadline extension (May – July)

- The ratio of fruit and vegetable juices containing nutrients or other substances is adjusted from 20 percent to 10 percent

- Service providers are encouraged to maintain employment in order to help employees. Service providers will be given the right to pay excise tax at the rate of 0 percent of service revenue until 30 September 2020

- The time to export goods or move goods to a free zone is changed to within 30 days with another 30-day extension, including a further 60-day extension, if necessary, but no more than 120 days in total

- The time to submit documents is changed to within 90 days, including a further 60-day extension, if necessary, but no more than 150 days in total

COVID-19 Excise Tax Relief Measures

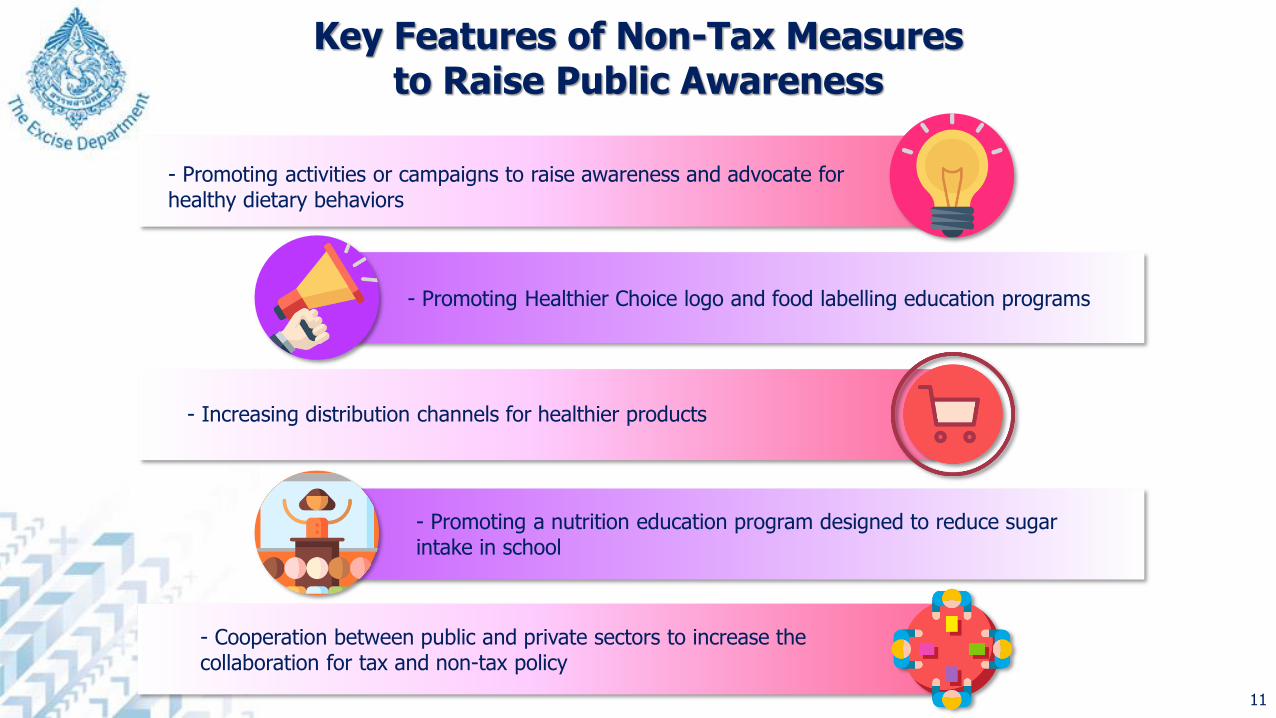

- Promoting activities or campaigns to raise awareness and advocate for healthy dietary behaviors

- Promoting Healthier Choice logo and food labelling education programs

- Promoting a nutrition education program designed to reduce sugar intake in school

- Increasing distribution channels for healthier products

- Cooperation between public and private sectors to increase the collaboration for tax and non-tax policy

11

Key Features of Non-Tax Measures to Raise Public Awareness

12

Specific Rate

Ad valorem Rate

Health

Luxury

Future Direction of Non-Alcoholic Beverages Tax

Promote health awareness as a key of excise tax development

and tax innovation

Encourage the beverage industry to reformulate their products according to the low sugar content

Make sugar-free drinks cheaper and increase

more healthier products to the consumers

13

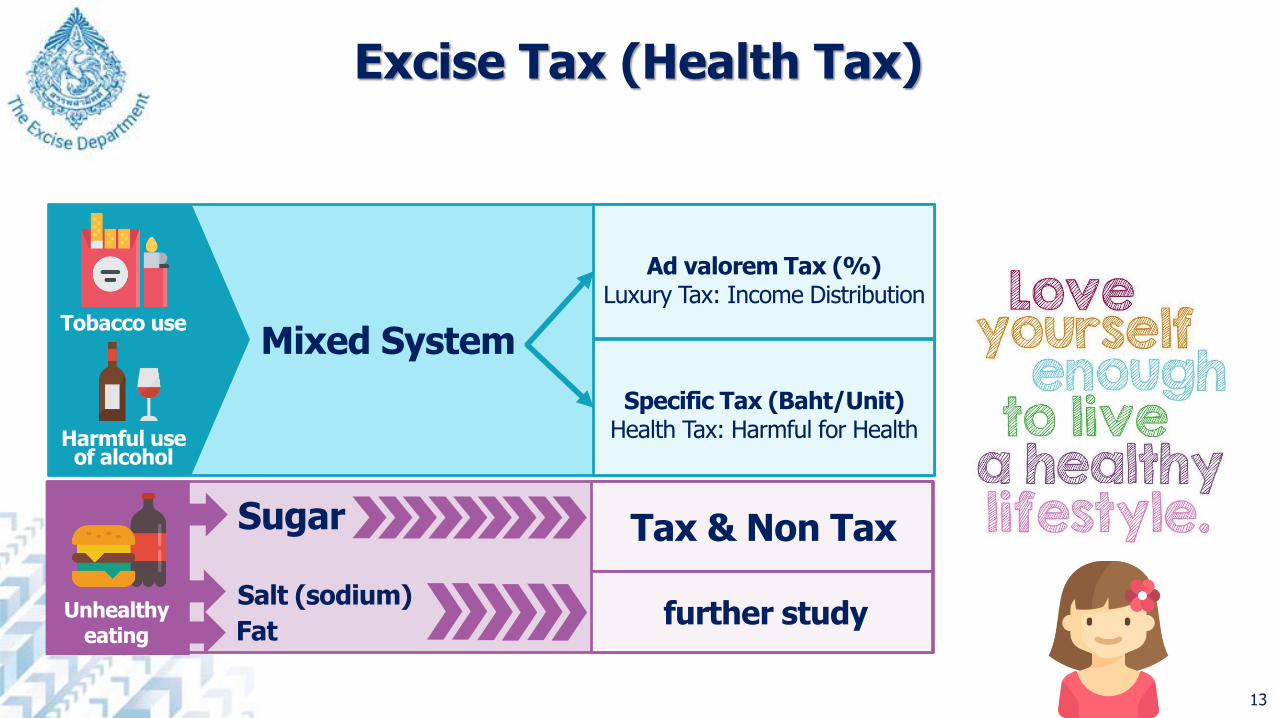

Excise Tax (Health Tax)

Tobacco use

Harmful use of alcohol

Specific Tax (Baht/Unit)Health Tax: Harmful for Health

Mixed System

Ad valorem Tax (%)Luxury Tax: Income Distribution

Unhealthy eating

Sugar

Salt (sodium)

Fat

Tax & Non Tax

further study

14

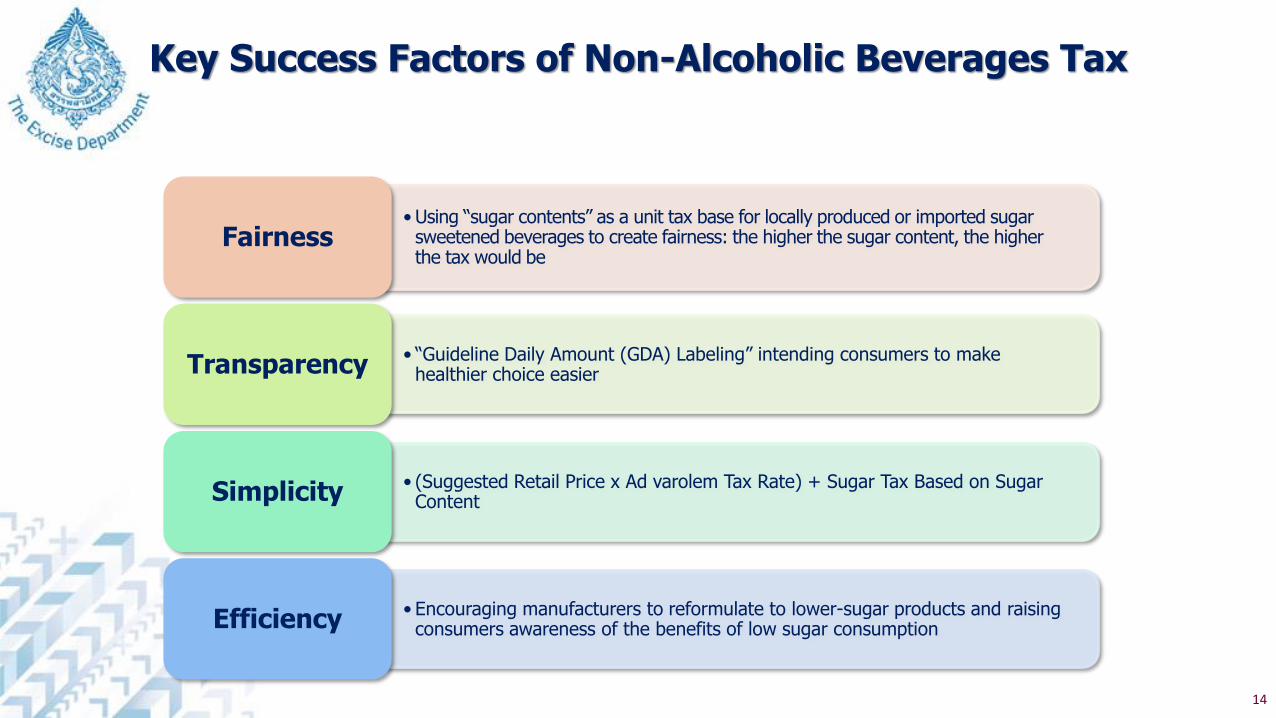

• Using “sugar contents” as a unit tax base for locally produced or imported sugar sweetened beverages to create fairness: the higher the sugar content, the higher the tax would be

Fairness

• “Guideline Daily Amount (GDA) Labeling” intending consumers to make healthier choice easierTransparency

• (Suggested Retail Price x Ad varolem Tax Rate) + Sugar Tax Based on Sugar ContentSimplicity

• Encouraging manufacturers to reformulate to lower-sugar products and raising consumers awareness of the benefits of low sugar consumptionEfficiency

Key Success Factors of Non-Alcoholic Beverages Tax