benchmarking quality: how medical device and diagnostics companies manage cost effectiveness while...

TRANSCRIPT

BEST PRACTICES,

®

LLC

Best Practices, LLC Strategic Benchmarking Research

Benchmarking Quality: How Medical Device & Diagnostics

Companies Manage Cost Effectiveness

while Ensuring Quality & Safety

BEST PRACTICES,

®

LLC

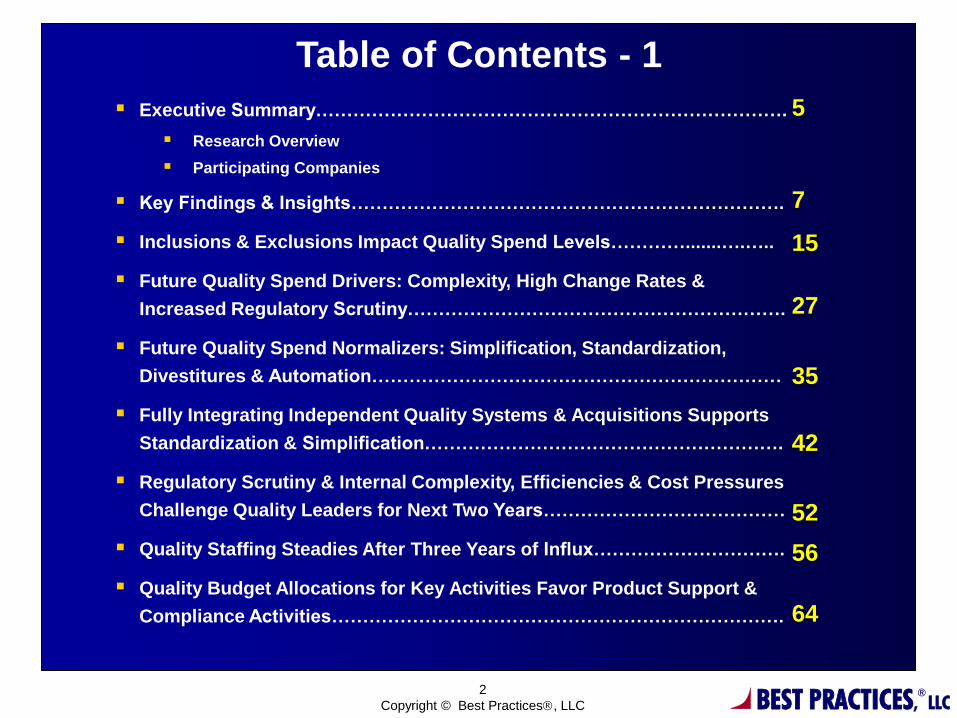

Table of Contents - 1

Executive Summary………………………………………………………………….

Research Overview

Participating Companies

Key Findings & Insights…………………………………………………………….

Inclusions & Exclusions Impact Quality Spend Levels………….......….…..

Future Quality Spend Drivers: Complexity, High Change Rates &

Increased Regulatory Scrutiny…………………………………………………….

Future Quality Spend Normalizers: Simplification, Standardization,

Divestitures & Automation…………………………………………………………

Fully Integrating Independent Quality Systems & Acquisitions Supports

Standardization & Simplification………………………………………………….

Regulatory Scrutiny & Internal Complexity, Efficiencies & Cost Pressures

Challenge Quality Leaders for Next Two Years…………………………………

Quality Staffing Steadies After Three Years of Influx………………………….

Quality Budget Allocations for Key Activities Favor Product Support &

Compliance Activities……………………………………………………………….

2

Copyright © Best Practices, LLC

5

7

15

27

35

42

52

56

64

BEST PRACTICES,

®

LLC

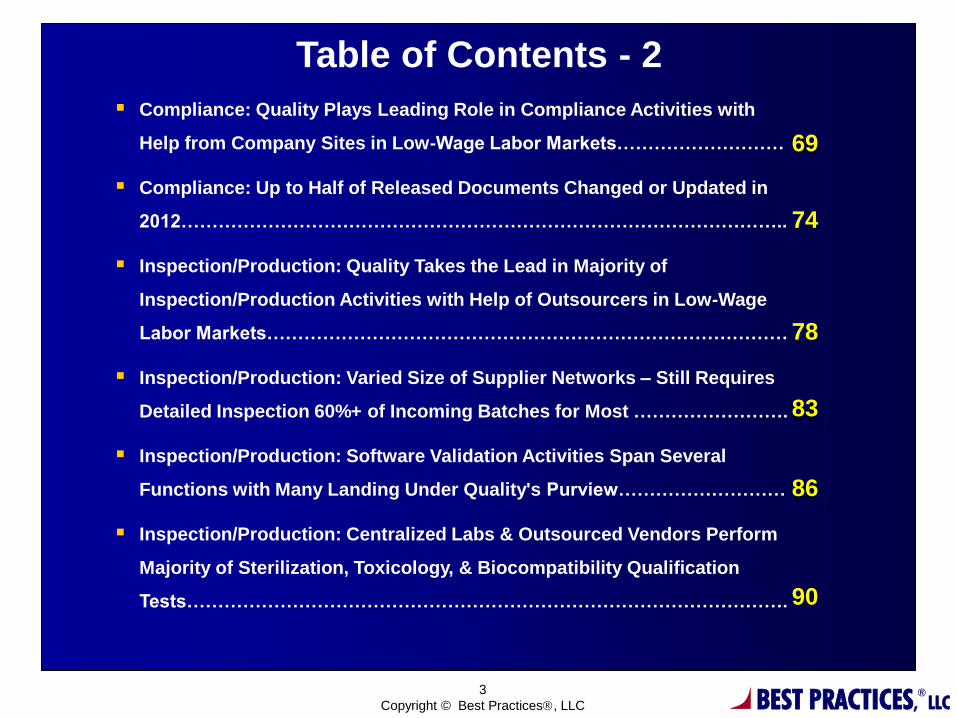

Table of Contents - 2

Compliance: Quality Plays Leading Role in Compliance Activities with

Help from Company Sites in Low-Wage Labor Markets………………………

Compliance: Up to Half of Released Documents Changed or Updated in

2012……………………………………………………………………………………..

Inspection/Production: Quality Takes the Lead in Majority of

Inspection/Production Activities with Help of Outsourcers in Low-Wage

Labor Markets…………………………………………………………………………

Inspection/Production: Varied Size of Supplier Networks – Still Requires

Detailed Inspection 60%+ of Incoming Batches for Most …………………….

Inspection/Production: Software Validation Activities Span Several

Functions with Many Landing Under Quality's Purview………………………

Inspection/Production: Centralized Labs & Outsourced Vendors Perform

Majority of Sterilization, Toxicology, & Biocompatibility Qualification

Tests…………………………………………………………………………………….

3

Copyright © Best Practices, LLC

69

74

78

83

86

90

BEST PRACTICES,

®

LLC

Table of Contents - 3

Non-Conforming: Quality Governs Non-Conforming Activities with Help

of Company Sites in Low-Wage Labor Markets………………………………...

Non-Conforming: Cycle Times for Processing CAPAs Can Take Up to A

Year or More…………………………………………………………………………..

Non-Conforming: Virtual Reviews & Automation Help Manage Thousands

of Annual Complaints ……………………………………………………………….

Product Support: Pre-Clinical & Clinical Quality Assurance Activities Not

Often Led by Quality…………………………………………………………………

Product Support: Quality Is Involved in Many Aspects of Design Control

& Cross-Charge Related Expenses……………………………………………

Additional Quality Activities: Quality Supports Many Additional Activities

with Use of Company Sites & Outsourced Vendors in Low-Wage Labor

Markets…………………………………………………………………………………

Universe of Learning: Key Demographics of Participating Companies …..

Appendix……………………………………………………………………………....

4

Copyright © Best Practices, LLC

92

97

101

106

111

115

120

128

BEST PRACTICES,

®

LLC

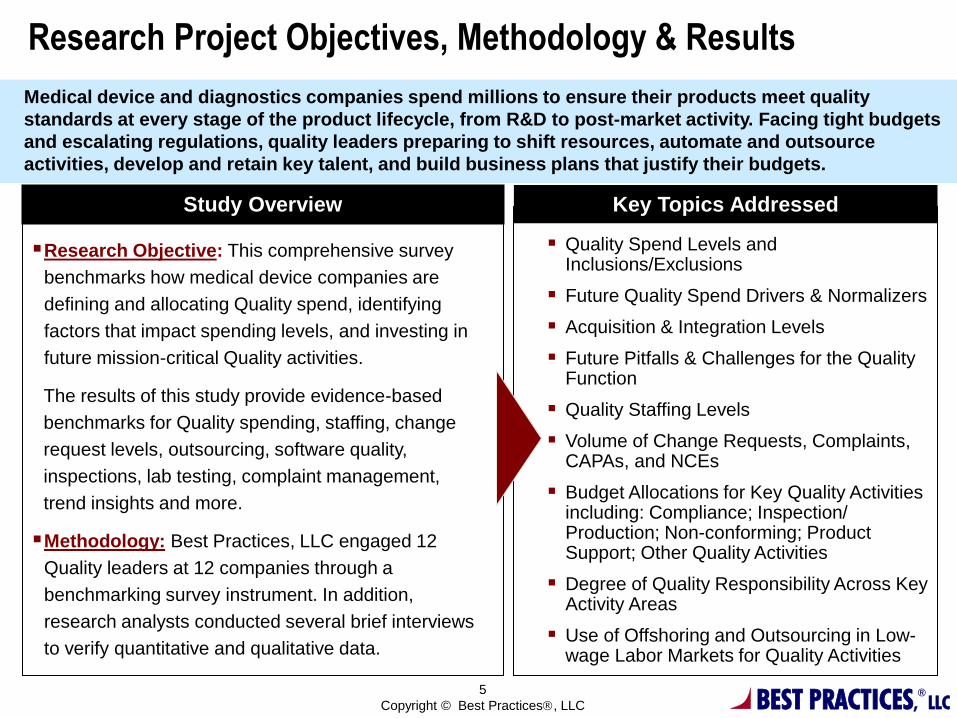

Key Topics Addressed Study Overview

Quality Spend Levels and Inclusions/Exclusions

Future Quality Spend Drivers & Normalizers

Acquisition & Integration Levels

Future Pitfalls & Challenges for the Quality Function

Quality Staffing Levels

Volume of Change Requests, Complaints, CAPAs, and NCEs

Budget Allocations for Key Quality Activities including: Compliance; Inspection/ Production; Non-conforming; Product Support; Other Quality Activities

Degree of Quality Responsibility Across Key Activity Areas

Use of Offshoring and Outsourcing in Low-wage Labor Markets for Quality Activities

Research Objective: This comprehensive survey

benchmarks how medical device companies are

defining and allocating Quality spend, identifying

factors that impact spending levels, and investing in

future mission-critical Quality activities.

The results of this study provide evidence-based

benchmarks for Quality spending, staffing, change

request levels, outsourcing, software quality,

inspections, lab testing, complaint management,

trend insights and more.

Methodology: Best Practices, LLC engaged 12

Quality leaders at 12 companies through a

benchmarking survey instrument. In addition,

research analysts conducted several brief interviews

to verify quantitative and qualitative data.

Research Project Objectives, Methodology & Results

5

Copyright © Best Practices, LLC

Medical device and diagnostics companies spend millions to ensure their products meet quality

standards at every stage of the product lifecycle, from R&D to post-market activity. Facing tight budgets

and escalating regulations, quality leaders preparing to shift resources, automate and outsource

activities, develop and retain key talent, and build business plans that justify their budgets.

BEST PRACTICES,

®

LLC

Benchmark Class:

6

Copyright © Best Practices, LLC

• Corporate Vice President, Quality and Regulatory

• Senior Vice President, Quality and Regulatory

• Vice President, Global Quality Systems

• Vice President, Quality Assurance Operations

• Vice President, Quality and Regulatory

• Vice President, Quality and Regulatory Affairs

• Senior Director, Global Quality Systems

• Senior Director, Global Quality and Regulatory

• Senior Director, Quality

• Director, Quality Systems

• Senior Manager, Quality and Quality Assurance

• Manager, Quality Assurance and

Regulatory Affairs

Job Titles of Respondents:

Universe of Learning: 12 Med Dev Orgs, 6 in Large Co. Segment

Twelve benchmark survey respondents participated in this research, nearly half of whom serve as vice presidents in Quality. Eleven of 12 benchmark companies represented are based in the United States. Two participants represent large business units instead of the entire company. The six circled companies make up the large company segment (LCS), with an average of $3.9 billion in 2012 revenue from medical device operations.

BEST PRACTICES,

®

LLC

Key Findings & Insights: Quality Spend Trends & Drivers

The following key findings and insights emerged from this study.

Quality Spending Trends: Nearly half of participating companies saw spending increase for the Quality

function over the past three years with an average amount of increase in spending of 6% for the full

benchmark class and for the large companies within it. Regulatory requirements, business expansion/new

products, and economic conditions are commonly cited forces for increased Quality spend.

Factors Increasing Quality Support Spend: Complexity in product mix, product family, and

manufacturing network received the highest impact ratings when it comes to prompting investment

increases in Quality spend. The total benchmark class also spotlights high change rates for design and

manufacturing processes – along with standardization initiatives – as other sources of increasing Quality

Support spending in the next two years. The large company segment indicated that the impact of

Regulatory infractions on Quality Support spend increases is much higher than did the overall benchmark

class. Half of large companies ranked consent decrees as having high impact on costs compared to only

25% of the overall benchmark class.

Future Quality Spend Normalizers: The overall benchmark class spotlights product simplification,

network optimization, standardization initiatives, and divestitures as key drivers expected to decrease

Quality Support spending requirements in the next 24 months. Large companies rank divestitures as being

twice as likely to lower costs compared to the overall benchmark class. Locating plants in low-cost

markets, automation, and decreasing change rates for product design and manufacturing all have at least

some positive impact on reducing support spending needs. A minority of companies did suggest that

Regulatory factors will help reduce costs – possibly because Regulatory actions have prompted

improvements that lead to lower support cost requirements.

7

Copyright © Best Practices, LLC

BEST PRACTICES,

®

LLC

(n=11)

Q12. How has the total spend of your company's medical device Quality function changed over the past three

years (2010-2012)?

8

Copyright © Best Practices, LLC

Spend Change Trend: Cost Changes Over Past 3 Years in

Medical Devices Quality Function

(n=6)

45% 50%

36% 33%

18% 17%

Total BenchmarkClass

Large CompanySegment

Increased Remained the same Decreased

Total %

Change in

Quality spend

in past 3 years

Max 30%

75th Percentile 10%

Mean 6%

Median 0%

25th Percentile 0%

Min -8%

(n=5)

Large Company Segment:

Total %

Change in

Quality spend

in past 3 years

Max 30%

75th Percentile 8%

Mean 6%

Median 0%

25th Percentile 0%

Min -10%

(n=10)

Total Benchmark Class:

45% of Participants Increased Quality Spending in Past 3 Years

Nearly half of participating companies saw spending increase for the Quality function over the past three

years. The average amount of increase in spending for the Quality function was 6% for both the full

benchmark class and the large companies within it.

BEST PRACTICES,

®

LLC

0

2

4

6

8

10

12

0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

Quality Cost / Revenue

Finding Your Zone of Optimal Competitiveness (Core Quality Costs Excluding Various Support Services)

Company A

Company B

Company C

Company D

Company E

Company F

Company G

Company H

Company I

Company J

Company K

Entering Zone of Competitiveness for Quality “Core Costs”

On average, companies spend about 1.8% of revenue on the Quality function. For large companies, the average was lower at 1.7%. However, with Quality spend increasing by an average of 6-10% overall, companies are moving toward an optimal zone of competition where spend lands between 1.5% - 3% of total revenue. Most companies exclude a host of Support Services & Functions in the calculation of Quality core costs.

TB

C A

ve

rag

e =

1.8

%

9

Copyright © Best Practices, LLC

BEST PRACTICES,

®

LLC

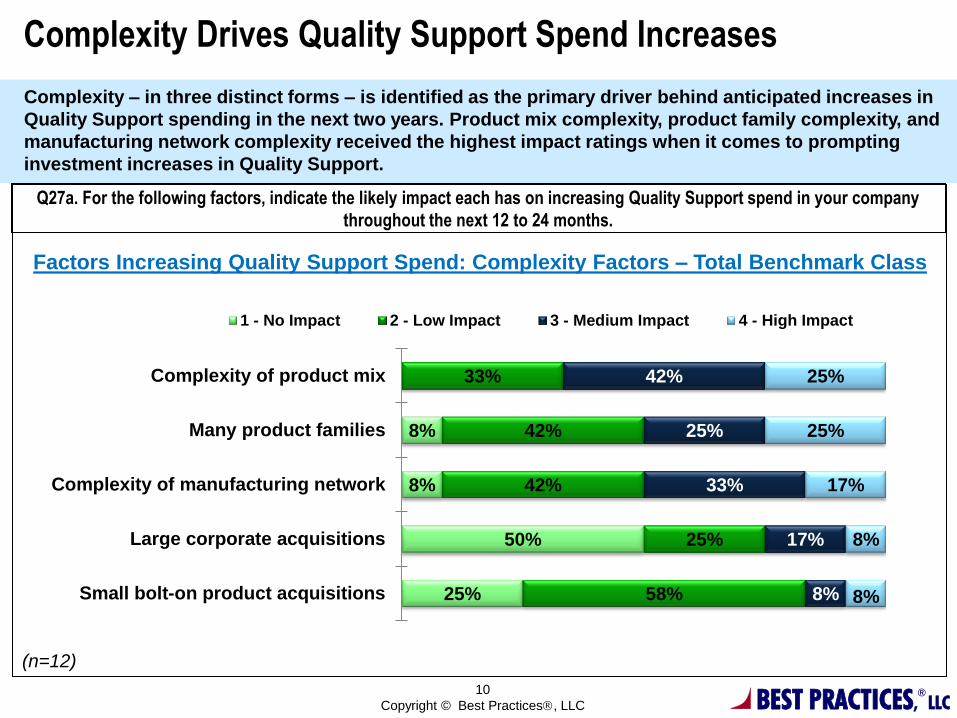

Complexity Drives Quality Support Spend Increases

Complexity – in three distinct forms – is identified as the primary driver behind anticipated increases in

Quality Support spending in the next two years. Product mix complexity, product family complexity, and

manufacturing network complexity received the highest impact ratings when it comes to prompting

investment increases in Quality Support.

(n=12)

Q27a. For the following factors, indicate the likely impact each has on increasing Quality Support spend in your company

throughout the next 12 to 24 months.

10

Copyright © Best Practices, LLC

Factors Increasing Quality Support Spend: Complexity Factors – Total Benchmark Class

8%

8%

50%

25%

33%

42%

42%

25%

58%

42%

25%

33%

17%

8%

25%

25%

17%

8%

8%

Complexity of product mix

Many product families

Complexity of manufacturing network

Large corporate acquisitions

Small bolt-on product acquisitions

1 - No Impact 2 - Low Impact 3 - Medium Impact 4 - High Impact

BEST PRACTICES,

®

LLC

Less Than Half of Quality Systems at Acquired Companies Are Fully Integrated into Existing Standards The total benchmark class has fully integrated only 38% of acquired sites into existing Quality standards.

Conversely, 29% of deals remain stand-alone and 34% pursue only partial integration with parent

company Quality standards. All companies plan for future integration.

Q35. Based on the past 3 years (2010-2012) of acquisitions, estimate the % of acquired facilities where Quality staff and

systems have been fully integrated into your corporate Quality standards.

11

Copyright © Best Practices, LLC

(n=7)

Quality Integration for Acquired Sites – Total Benchmark Class:

Percentage of total

acquisitions fully

Integrated, 38%

Percentage of total

acquisitions remaining

stand-alone (no

integration), 25%

Percentage of total

acquisitions with some integration but not all

sites/ systems,

34%

• All companies plan for future integration.

• Two companies in the total benchmark class indicate that they have already

fully integrated, therefore their data were omitted from the calculations.

Currently

% of total

acquisitions

fully inte-

grated

% of total

acquisitions

remaining

stand-alone

% of total

acquisitions

with some

integration

Max 75% 100% 100%

75th Percentile 65% 50% 40%

Mean 38% 29% 34%

Median 50% 0% 31%

25th Percentile 5% 0% 13%

Min 0% 0% 0%

Average Degree Current

Acquisition Integration:

BEST PRACTICES,

®

LLC

12

Structure

People

Products

Custom-ers

Sales Forces

Facilities

Suppliers

Quality Systems

Technol-ogy

Integration

Center of

Excellence

Integration Centers of Excellence Help Achieve M&A

Productivity Targets Many acquisitions and decentralized culture have permitted many quality systems not to be fully integrated. Fully integrating quality systems across acquired companies and assets offer greater efficiencies. Some companies employ Integration Centers of Excellence to accomplish this.

Benefits Of Integration

Specialists

Specialists can organize quickly

Have experience with past

integrations

Employ “due diligence” mindset to

integration

Drive early synergy actions

Avoid common mistakes

Remain focused on integration for

full cycle

Don’t have line operation

responsibilities that distract

Get to back-end opportunities:

Quality, Technology, et al.

BEST PRACTICES,

®

LLC

Quality Staffing over Med Device Employees – Shown as %

13

Copyright © Best Practices, LLC

Medical Device Quality Staffing:

Quality FTEs/ Medical

Device FTEs

Max 10.2%

75th Percentile 7.7%

Mean 5.9%

Median 5.8%

25th Percentile 3.3%

Min 2.6%

Quality FTEs/ Medical

Device FTEs

Max 10.2%

75th Percentile 7.7%

Mean 5.4%

Median 4.7%

25th Percentile 3.3%

Min 1.6%

(n=10) (n=6)

Total Benchmark Class: Large Company Segment:

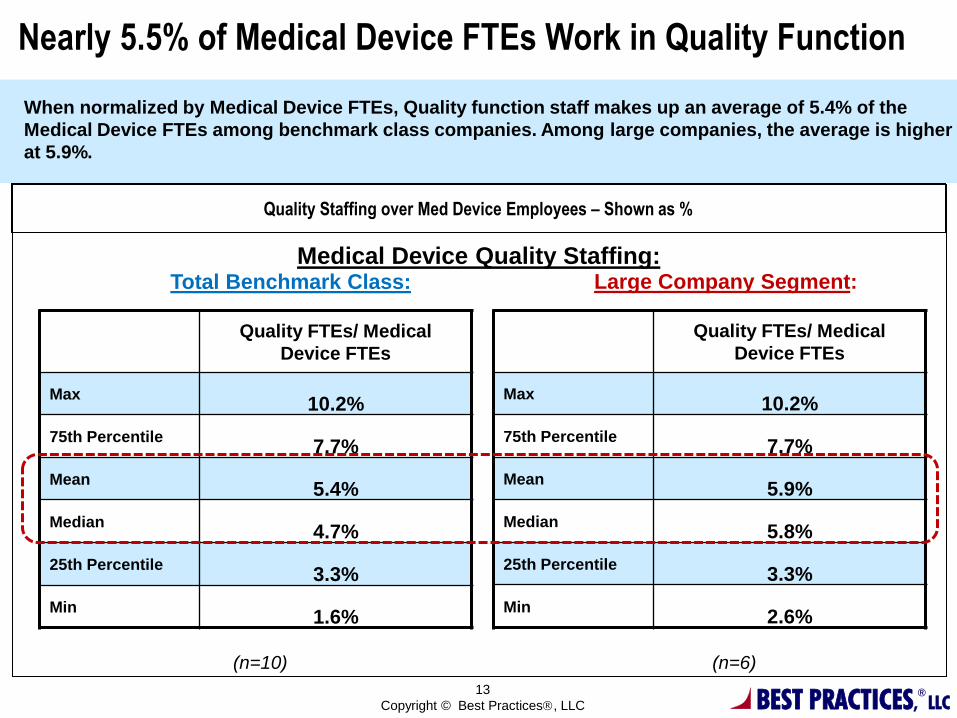

Nearly 5.5% of Medical Device FTEs Work in Quality Function

When normalized by Medical Device FTEs, Quality function staff makes up an average of 5.4% of the

Medical Device FTEs among benchmark class companies. Among large companies, the average is higher

at 5.9%.

BEST PRACTICES,

®

LLC

Majority Changed Less than 50% of Released & Effective Docs

Forty percent of the total benchmark class indicated that their Quality functions changed or updated

between 31-50% of released and effective documents in 2012. One large-company representative

achieved the lowest change/update rate of 11-15% in the benchmark class.

(n=10)

Q37. What percentage of your company's released and effective documents were changed or updated in 2012?

14

Copyright © Best Practices, LLC

Document Change Levels:

Total Benchmark Class: Large Company Segment:

(n=5)

11-15%, 10%

16-20%, 10%

21-30%, 30%

31-50%, 40%

More than 50%, 10%

11-15%, 20%

31-50%, 60%

21-20%,

20%

BEST PRACTICES,

®

LLC

Q26d. Please estimate the percentage of Quality Assurance activities that are done in low-wage markets at company sites vs.

via third-party outsourcers.

15

Copyright © Best Practices, LLC

Managing QA Labor Costs across Global Markets

(n=4-5)

Large Companies Use Low-Wage Markets for Quality Engineering & Design Assurance for Commercial Products

All participants in the large company segment perform at least some Quality Engineering and Design Assurance for Commercial Products support activities at company sites in low-wage markets. Up to 40% also use third-party vendors in these markets for some Quality Engineering activities.

Companies performing activities in low-wage

markets at company sites

Companies using 3rd-party outsourced vendors to

conduct activities in low-wage markets

Quality

Engineering

Pre-Clinical

Quality

Assurance

Clinical

Quality

Assurance

Design

Assurance

for New

Products &

Commercial

Products

Quality

Engineering

Pre-Clinical

Quality

Assurance

Clinical

Quality

Assurance

Design

Assurance

for New

Products &

Commercial

Products

0% 0% 25% 75% 20% 0% 60% 75% 100% 80% 80%

1-15% 0% 75% 25% 60% 0% 40% 0% 0% 20% 20%

16-30% 40% 0% 0% 0% 40% 0% 0% 0% 0% 0%

31-50% 40% 0% 0% 0% 20% 0% 0% 0% 0% 0%

51-100% 20% 0% 0% 20% 40% 0% 25% 0% 0% 0%

Large Company Segment – Product Support Activities:

%

Activities

Performed

BEST PRACTICES,

®

LLC

(n=11)

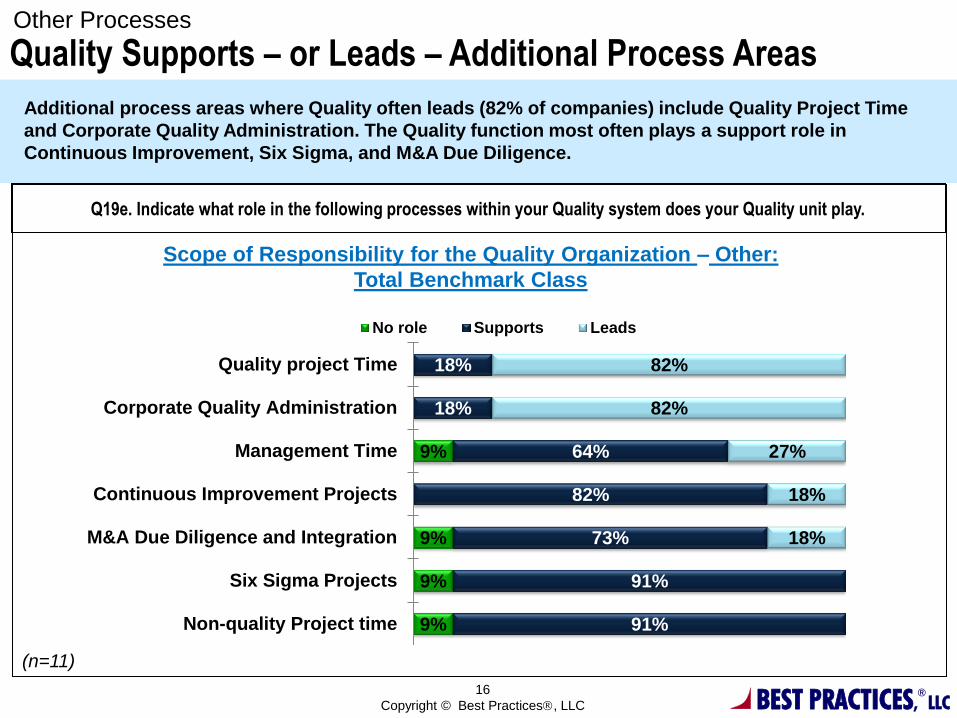

Q19e. Indicate what role in the following processes within your Quality system does your Quality unit play.

16

Copyright © Best Practices, LLC

Scope of Responsibility for the Quality Organization – Other:

Total Benchmark Class

Quality Supports – or Leads – Additional Process Areas

Additional process areas where Quality often leads (82% of companies) include Quality Project Time

and Corporate Quality Administration. The Quality function most often plays a support role in

Continuous Improvement, Six Sigma, and M&A Due Diligence.

Other Processes

9%

9%

9%

9%

18%

18%

64%

82%

73%

91%

91%

82%

82%

27%

18%

18%

Quality project Time

Corporate Quality Administration

Management Time

Continuous Improvement Projects

M&A Due Diligence and Integration

Six Sigma Projects

Non-quality Project time

No role Supports Leads

BEST PRACTICES,

®

LLC

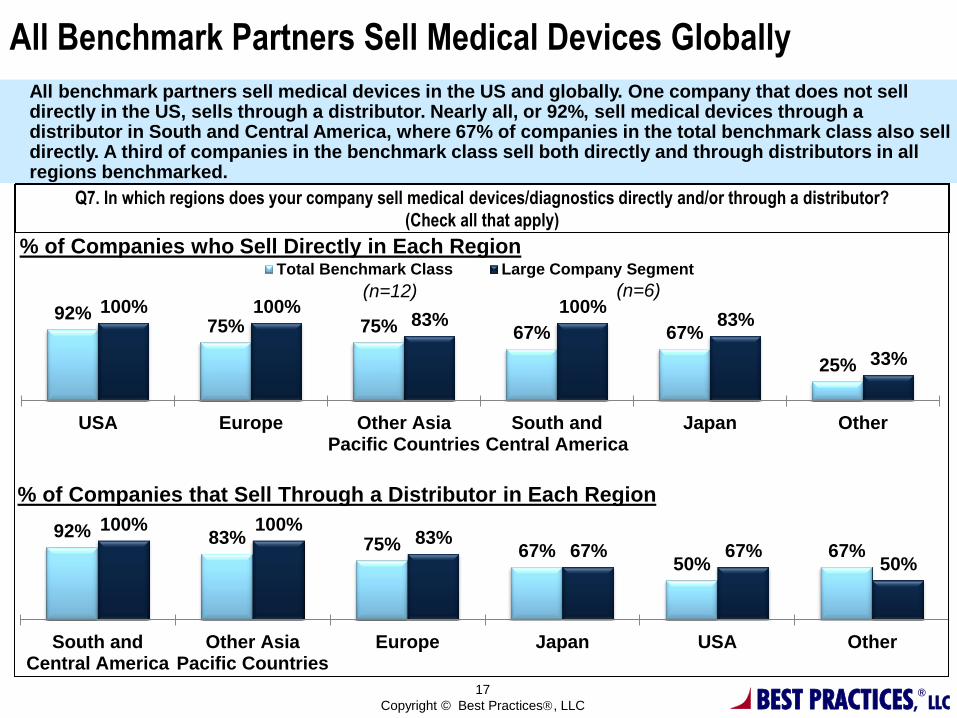

Q7. In which regions does your company sell medical devices/diagnostics directly and/or through a distributor?

(Check all that apply)

17

Copyright © Best Practices, LLC

% of Companies who Sell Directly in Each Region

(n=12) (n=6)

92% 75% 75% 67% 67%

25%

100% 100% 83%

100% 83%

33%

USA Europe Other AsiaPacific Countries

South andCentral America

Japan Other

Total Benchmark Class Large Company Segment

92% 83% 75% 67% 50%

67%

100% 100% 83%

67% 67% 50%

South andCentral America

Other AsiaPacific Countries

Europe Japan USA Other

% of Companies that Sell Through a Distributor in Each Region

All Benchmark Partners Sell Medical Devices Globally

All benchmark partners sell medical devices in the US and globally. One company that does not sell directly in the US, sells through a distributor. Nearly all, or 92%, sell medical devices through a distributor in South and Central America, where 67% of companies in the total benchmark class also sell directly. A third of companies in the benchmark class sell both directly and through distributors in all regions benchmarked.

BEST PRACTICES,

®

LLC

18

Copyright © Best Practices, LLC

Best Practices, LLC is a research and consulting firm that conducts work

based on the simple yet profound principle that organizations can chart a

course to superior economic performance by studying the best business

practices, operating tactics and winning strategies of world-class

companies.

Best Practices, LLC

6350 Quadrangle Drive, Suite 200, Chapel Hill, NC 27517

919-403-0251

www.best-in-class.com

About Best Practices, LLC