belgrade city report - bazabiur.pl · privreda posle dve uzastopne godine ekonomskog rasta, srpska...

TRANSCRIPT

REAL ESTATE

BELGRADE

Q2 2013

Izveštaj o BeograduT2 2013

on point

Belgrade City ReportQ2 2013

2 On Point • Belgrade City Report• Q2 2013

Economy/Investment

Economy

The very fragile economy in 2012 was reflected in Serbian GDP

figures. According to IHS Global Insight estimates, the country’s

economy contracted by 1.7% in 2012. However, real GDP increased

in the first quarter of 2013 compared to the corresponding period of

the previous year, amounting to 2.1%. By sector, the most

significant growth in the gross value added, in the first quarter of

2013, was registered as follows: information and communication

sector (8.1%), mining (6.6%), transportation and warehousing (

5.4%), electrical energy, gas and steam supply ( 3.2%) and

processing industry (2.4%). The most significant fall in the gross

value added was recorded in the section of construction (24.7%)

and trade (4.0%).

The Serbian government are heavily relying on FIAT’s production

and political stabilization in 2013. Therefore, the forecasted GDP

growth for 2013 is 2.1% (IHS Global insight forecast).

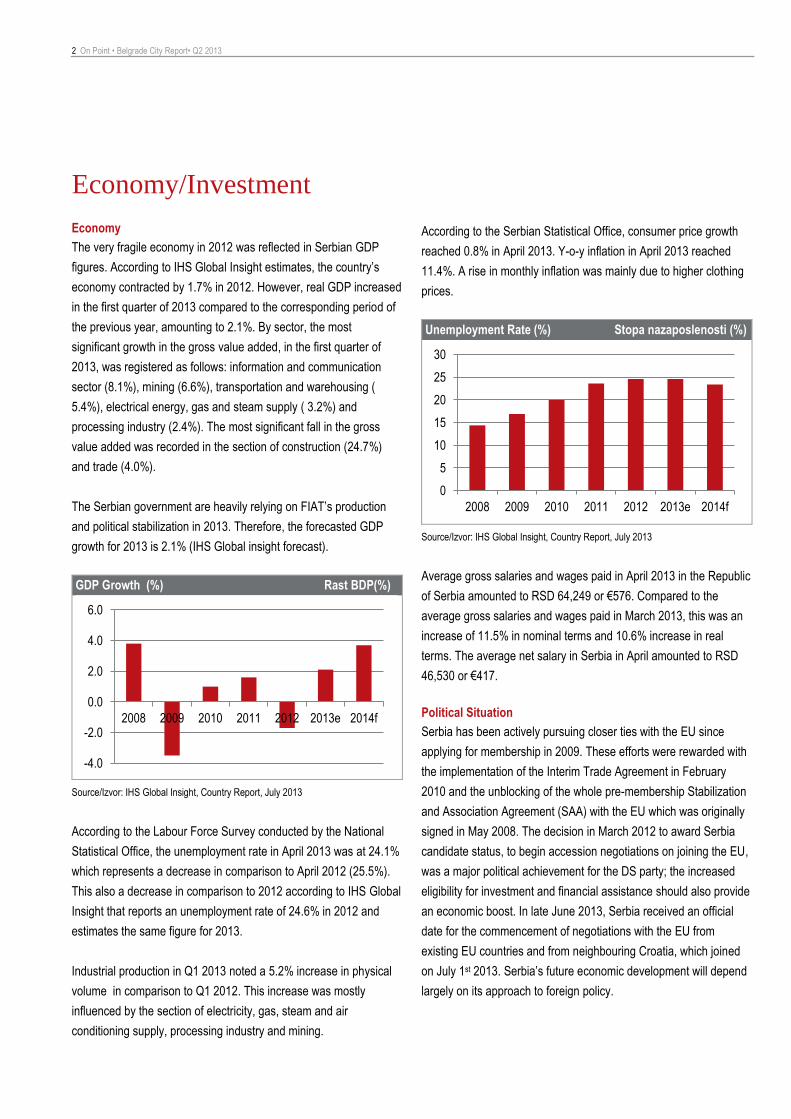

GDP Growth (%) Rast BDP(%)

Source/Izvor: IHS Global Insight, Country Report, July 2013

According to the Labour Force Survey conducted by the National

Statistical Office, the unemployment rate in April 2013 was at 24.1%

which represents a decrease in comparison to April 2012 (25.5%).

This also a decrease in comparison to 2012 according to IHS Global

Insight that reports an unemployment rate of 24.6% in 2012 and

estimates the same figure for 2013.

Industrial production in Q1 2013 noted a 5.2% increase in physical

volume in comparison to Q1 2012. This increase was mostly

influenced by the section of electricity, gas, steam and air

conditioning supply, processing industry and mining.

According to the Serbian Statistical Office, consumer price growth

reached 0.8% in April 2013. Y-o-y inflation in April 2013 reached

11.4%. A rise in monthly inflation was mainly due to higher clothing

prices.

Unemployment Rate (%) Stopa nazaposlenosti (%)

Source/Izvor: IHS Global Insight, Country Report, July 2013

Average gross salaries and wages paid in April 2013 in the Republic

of Serbia amounted to RSD 64,249 or €576. Compared to the

average gross salaries and wages paid in March 2013, this was an

increase of 11.5% in nominal terms and 10.6% increase in real

terms. The average net salary in Serbia in April amounted to RSD

46,530 or €417.

Political Situation

Serbia has been actively pursuing closer ties with the EU since

applying for membership in 2009. These efforts were rewarded with

the implementation of the Interim Trade Agreement in February

2010 and the unblocking of the whole pre-membership Stabilization

and Association Agreement (SAA) with the EU which was originally

signed in May 2008. The decision in March 2012 to award Serbia

candidate status, to begin accession negotiations on joining the EU,

was a major political achievement for the DS party; the increased

eligibility for investment and financial assistance should also provide

an economic boost. In late June 2013, Serbia received an official

date for the commencement of negotiations with the EU from

existing EU countries and from neighbouring Croatia, which joined

on July 1st 2013. Serbia’s future economic development will depend

largely on its approach to foreign policy.

-4.0

-2.0

0.0

2.0

4.0

6.0

2008 2009 2010 2011 2012 2013e 2014f

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013e 2014f

On Point • Belgrade City Report • Q2 2013 3

Privreda/Investicije

Privreda

Posle dve uzastopne godine ekonomskog rasta, srpska privreda

belezi značajan pad od 1,7% u 2012, uglavnom zbog izbora koji su

se dogodili sredinom godine kao I zbog slabe poljoprivredne sezone

i opšte ekonomske krize u drugim delovim Evrope. Na osnovu

zvaničnih podataka koje je objavio Statistički zavod Repubilike

Srbije, zabeležen je privredni pad od 2,0% u odnosu poslednji

kvartal 2012. godine. Najveći pad zabeležen je u građevinskom

sektoru (24,7%) i sektoru snabdevanja električnom energijom,

gasom i parom (7,1%). Sektori koji su zabeležili rast i uspešno

završili tromesečje su: sektor informisanja i komunikacija (11,4%),

sektor finansijskih delatnosti i delatnosti osiguranja (5,9%) i sektor

prerađivačke industrije (4,9%). IHS Global Insight za 2013. godinu

predviđa oporavak privrede i porast BDP od 2,1%. Ova prognoza

deluje prilično optimistično, a verovatno je zasnovana na

očekivanom porastu industrijske proizvodnje predvođene FIAT-om,

koji u ovom trenutku predstavlja jedinu nadu za Srbiju.

CPI (%) Inflacija (%)

Source/Izvor: IHS Global Insight, Country Report, July 2013

U aprilu 2013 prema Anketi o radnoj snazi koju sprovodi Republički

zavod za statistiku, stopa nezaposlenosti je iznosila 24,1%, što

predstavlja pad u odnosu na april 2012 ( 25,5 % ) , kao ismanjenje

u odnosu na 2012 u skladu sa ekonomskim izvodrima HIS Global

Insight koji sugerišu stopu nezaposlenosti od 24,6% u 2012, a

procenjuju istu figure u 2013.

Industrijska proizvodnja u prvom tromesečju 2013. beleži rast

fizičkog obima od 5,2% u odnosu nan a prvo tromesečje 2012. Ovaj

pad najviše je uticao na sektor proizvodnje elekrtične energije, gasa,

pare i klimatizacije.

Yields % Stope prinosa %

Source/Izvor: Jones Lang LaSalle, July2013

Prema podacima Republičkog zavoda za statistiku , rast potrošačkih

cena dostigao 0,8 % u aprilu 2013., a inflacija u aprilu 2013 je

dostigla 11,4% . Rast mesečne inflacije je uglavnom zbog vec e

cene odec e .

Prosečna bruto zarada isplac ena u aprilu 2013 u Republici Srbiji

iznosila je 64,249 dinara ili 576 € . odnosu na prosečnu bruto

zaradu isplac enu u martu 2013 , to je povec anje od 11,5%

nominalno i 10,6 % realno povec anje . Prosečna neto zarada u

Srbiji u aprilu iznosila je 46,530 dinara ili 417 € .

Politička situacija

Srbija je aktivno sprovodi što bliže veze sa E od podnošenja

zahteva za članstvo u 2009. Ovi napori su nagrađeni sa primenom

Prelaznog trgovinskog sporazuma u februaru 2010. i deblokadi

prethodnog članstva za stabilizaciju i pridruživanju (SSP ) sa E ,

koji je prvobitno potpisan u maju 200 . Odluka u martu 2012 da

dodeli Srbiji status kandidata za početak pregovora o pristupanju o

Evropskoj uniji je veliki politički uspeh za DS ,povec ana moguc nost

za investicije i finansijsku pomoc treba da obezbedi ekonomski

podsticaj . rajem juna 2013 , Srbija je dobila zvaničan datum za

početak pregovora sa E iz postojec ih zemalja EU i iz susedne

Hrvatske , koja se pridružila 1. Juli 2013. Budići ekonomski razvoj

Srbije ce u velikoj meri zavisiti od sprovođenja spoljne politke.

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 2013e 2014f

Sektor/Sektor

Yield/

Stopa prinosa

%

Changes on previous quarter/

Promene u odnosu na

prethodno tromesečje

Offices/Kancelarijski prostori 9.25% ↕

Retail/Maloprodajni prostori

Shopping Centers/tržni

centri

9.00% ↕

Logistics/Logistički objekti 10.25% ↕↕

↕

4 On Point • Belgrade City Report• Q2 2013

Office Market

Supply

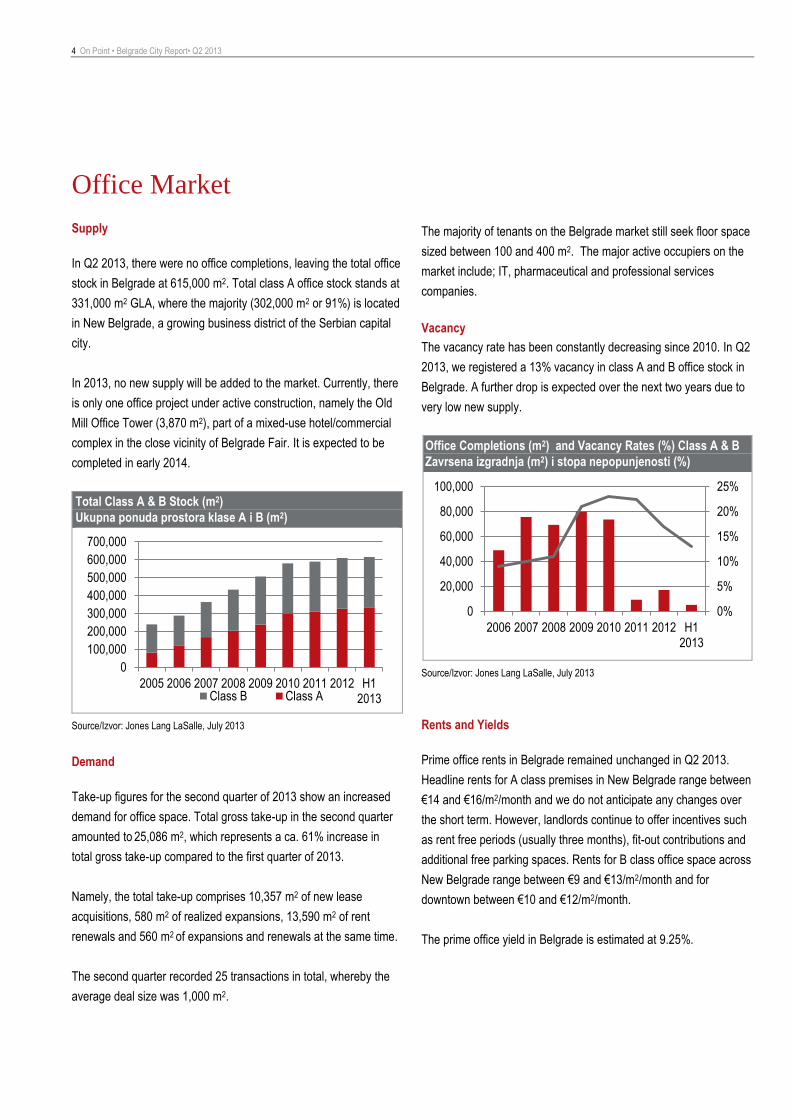

In Q2 2013, there were no office completions, leaving the total office

stock in Belgrade at 615,000 m2. Total class A office stock stands at

331,000 m2 GLA, where the majority (302,000 m2 or 91%) is located

in New Belgrade, a growing business district of the Serbian capital

city.

In 2013, no new supply will be added to the market. Currently, there

is only one office project under active construction, namely the Old

Mill Office Tower (3,870 m2), part of a mixed-use hotel/commercial

complex in the close vicinity of Belgrade Fair. It is expected to be

completed in early 2014.

Total Class A & B Stock (m2)

Ukupna ponuda prostora klase A i B (m2)

Source/Izvor: Jones Lang LaSalle, July 2013

Demand

Take-up figures for the second quarter of 2013 show an increased

demand for office space. Total gross take-up in the second quarter

amounted to 25,086 m2, which represents a ca. 61% increase in

total gross take-up compared to the first quarter of 2013.

Namely, the total take-up comprises 10,357 m2 of new lease

acquisitions, 580 m2 of realized expansions, 13,590 m2 of rent

renewals and 560 m2 of expansions and renewals at the same time.

The second quarter recorded 25 transactions in total, whereby the

average deal size was 1,000 m2.

The majority of tenants on the Belgrade market still seek floor space

sized between 100 and 400 m2. The major active occupiers on the

market include; IT, pharmaceutical and professional services

companies.

Vacancy

The vacancy rate has been constantly decreasing since 2010. In Q2

2013, we registered a 13% vacancy in class A and B office stock in

Belgrade. A further drop is expected over the next two years due to

very low new supply.

Office Completions (m2) and Vacancy Rates (%) Class A & B

Zavrsena izgradnja (m2) i stopa nepopunjenosti (%)

Source/Izvor: Jones Lang LaSalle, July 2013

Rents and Yields

Prime office rents in Belgrade remained unchanged in Q2 2013.

Headline rents for A class premises in New Belgrade range between

€14 and €16/m2/month and we do not anticipate any changes over

the short term. However, landlords continue to offer incentives such

as rent free periods (usually three months), fit-out contributions and

additional free parking spaces. Rents for B class office space across

New Belgrade range between €9 and €13/m2/month and for

downtown between €10 and €12/m2/month.

The prime office yield in Belgrade is estimated at 9.25%.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2005 2006 2007 2008 2009 2010 2011 2012 H12013Class B Class A

0%

5%

10%

15%

20%

25%

0

20,000

40,000

60,000

80,000

100,000

2006 2007 2008 2009 2010 2011 2012 H12013

On Point • Belgrade City Report • Q2 2013 5

Kancelarijski prostori

Ponuda

U drugom tromesečju 2013. godine nije zabelezena izgradnja

novog kancelarijskog prostora.Ukupna ponuda kancelarijskog

prostora klase A i B u drugom tromesečju 2013. godine iznosi

615.000 m2. Ukupna ponuda prostora klase A iznosi 331.000 m2,

gde se većina (302.000 m2 ili 91%) nalazi na Novom Beogradu,

poslovnom centru Beograda koji se neprestano razvija.

2013. godini tržište će dobiti veoma malu ponudu

novoizgradjenog poslovnog prostora. Trenutno je samo jedan

projekat u fazi aktivne izgradnje čiji se završetak planira do kraja

godine. U pitanju je Stari Mlin (3.870 m2), deo mešovitog hotelsko-

komercijalnog prostora u neposrednoj blizini Beogradskog sajma.

Prime Office Yields %

Stopa prinosa prvoklasnog prostora %

Source/Izvor: Jones Lang LaSalle, April 2013

Potražnja

Transakcije zabeležene u drugom tromesečju 2013. godine ukazuju

na povećanu tražnju za kancelarijskim prostorom. kupan bruto

zakup u drugom tromesečju iznosio je 25.086 m2, što predstavlja

oko 61% povećanja u odnosu na ukupan bruto zakup u prvom

tromesečju 2013. godine.

Od ukupne bruto kvadrature, 10.357 m2 se odnosi na nove

transakcije, 5 0 m2 na proširenja postojećeg prostora, 13.590 m2

predstavljaju obnove postojećih ugovora o zakupu, dok se 560 m2

odnosi na obnovu postojećih ugovora o zakupu uz istovremeno

proširenje postojećeg prostora. kupno je zabeleženo 25

transakcija na tržištu, sa prosečnom zakupljenom kvadraturom od

1.000 m2.

Analizom pojedinačnih transakcija zakupa, zaključujemo da su

zakupi kancelarijskog prostora preko 1.000 m2 i dalje retki na tržištu,

a u drugom kvartalu ove godine oni su iznosili 15% od ukupnog

broja transakcija.

Većina zakupaca u Beogradu i dalje traži kancelarijske prostore od

100 do 400 m2. Zakupci koji su uzimali prostore su bile IT

kompanije, farmaceutske kuće I kompanije koje se bave pružanjem

profesionalnih usluga.

Raspoloživi prostor

Stopa nepopunjenog prostora je u stalnom padu od 2010. godine. U

drugom tromesečju 2013. godine stopa praznog prostora u

poslovnim zgradama klase A I B u Beogradu iznosila je 13%.

Očekuje se dalji pad u naredne dve godine zbog slabe ponude

novoizgrađenog kancelarijskog prostora.

Prime Rents €/m2/month

Cene zakupa prvoklasnog prostora €/m2/mesečno

Source/Izvor: Jones Lang LaSalle, April 2013Cene zakupa i stope prinosa

Visine zakupa i stope prinosa

Cene zakupa prvoklasnog prostora u Beogradu ostale su

nepromenjene u drugom tromesečju 2013.godine. Cene zakupa

kancelarijskog prostora klase A na Novom Beogradu kreću se od

€14 do €16/m2/mesečno i ne očekujemo nikakve promene u

kratkoročnom periodu. Ipak, vlasnici prostora i dalje nude podsticaje

poput rent-free perioda (obično 3 meseca), dodatna parking mesta

bez naknade, učešće zakupodavca u troškovima završnih radova.

Cene zakupa za kancelarijski prostor klase B na Novom Beogradu

iznose između €9 do €13/m2/mesečno a centru grada od €10 do

€12/m2/mesečno. Procenjuje se da stopa prinosa za prvoklasne

kancelarijske prostore u Beogradu iznosi 9,25%.

8.00%

8.25%

8.50%

8.75%

9.00%

9.25%

9.50%

9.75%

Q12009

Q32009

Q12010

Q32010

Q12011

Q32011

Q12012

Q32012

Q12013

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 Q12013

Q22013

6 On Point • Belgrade City Report• Q2 2013

Retail Market

Supply

In April, we witnessed the completion of Stadium Center at

Voždovac, adding 30,000 m2 to the market. Therefore, the

shopping centre stock in Belgrade increased in the second

quarter of 2013 to 188,700 m2 GLA. Prime shopping centers in

Belgrade remained at 128,000 m2 GLA. Translated into shopping

centre density figures, Belgrade remains at the lowest position of

the European shopping centre scale, with only 78 m2 of retail

space in modern shopping centres per 1,000 inhabitants.

Although the scheme has been operating since Q3 2012, the

official opening of Karaburma Shopping Center (12,000 m2 GLA)

took place in March 2013. The first retailers to enter the shopping

centre are Roda supermarket, DM and Merkur. Jysk opened its

store in November 2012, and the official opening saw the

entrance of Sport Vison, Takko Fashion, Deichmann, C&A,

BigBang and Cotton4Family.

Shopping Center Stock in Belgrade (m2)

Ponuda tržnih centara u Beogradu (m2)

Source/Izvor: Jones Lang LaSalle, July 2013

In terms of new supply, there are no further shopping centre

schemes under construction or any planned with a definitive

completion date. Large sized pipeline projects in Belgrade

include: Delta Planet (75,000 m2 GLA) which has already signed

agreements with hypermarket and multiplex cinema operators;

Višnjička Plaza (40,000 m2 GLA) that is negotiating with anchors

and Ada Mall (30,000 m2 GLA).

Demand

New international retailers to enter the Belgrade market include:

Bagatt (Italian shoe retailer) and Desigual (a Spansh fashion

brand) who have signed up for retail space in Delta City and

šće Shopping Center respectively. In addition, a local retailer

opened the playground „Dream Land“ over 2,000 m2 in Stadium

Shopping Center. In addition, another playground of 1,200 m2 is

planned for Septemebr in Delta City, also by local retailer - Ultra

Kanal.

Total Annual Spend in € per Capita in Belgrade

Source/Izvor: Statistical Office of the Republic of Serbia

The demand from international retailers for modern retail

schemes continues to be very strong; the main obstacle for new

entrants or retailers looking to expand is the limited supply of

modern shopping centres.

The vacancy rate in prime shopping centres is close to zero and

the majority of current vacant space is largely due to tenant mix

changes.

Rents and Yields

Prime rents and yields remained unchanged in Q2. Prime

shopping center rent for a 100 to 200 m2 retail unit stands at

€65/m2/month, while rent for such a unit on Knez Mihajlova

Street is € 0/m2/month. Average rents in prime shopping centres

in Belgrade range between €27 and €29/m2/month. The prime

shopping centre yield stands at 9%.

0

50,000

100,000

150,000

200,000

2007 2008 2009 2010 2011 2012 2013f

1,900

1,950

2,000

2,050

2,100

2,150

2,200

2,250

2,300

2009 2010 2011 2012

On Point • Belgrade City Report • Q2 2013 7

Maloprodajni prostori

Ponuda

Iako je završetak izgradnje Stadion centra na Voždovcu bio

planiran za kraj marta, zvanično otvaranje je odloženo za

poslednju nedelju aprila. Tako je ukupna ponuda maloprodajnog

prostora u tržnim centrima u Beogradu u drugom tromesečju

2013. iznosi 188.700 m2. Maloprodajni prostor u prvoklasnim

centrima u Beogradu smešten je u četiri objekta i njegova

površina iznosi 128.000 m2. Po glavi stanovnika, Beograd nudi 78

m2 modernog prodajnog prostora u tržnim centrima, zbog čega se

nalazi na najnižem mestu na evropskoj skali tržnih centara.

Iako ovaj tržni centar radi od trećeg tromesečja 2012, tržni centar

araburma je zvanično otvoren u martu 2013. Zakupci koji su prvi

ušli u tržni centar su Roda supermarket, DM i Merkur. Jysk je

otvorio svoj maloprodajni prostor u novembru 2012., a sa

zvaničnim otvaranjem ušli su Sport Vision, Takko Fashion,

Deichmann, C&A, Big Bang, Cotton4Family.

Prime Shopping Center Yields

Stopa prinosa prvoklasnih tržnih centara

Source/Izvor: Jones Lang LaSalle, July 2013

U aprilu 2013. je otvoren Stadion centra na Voždovcu, što je

povećalo ponudu tržnih centara u Beogradu na 188.700 m2. Osim

ovog projekta koji je nedavno otvoren, u Beogradu neće biti

izgrađeno novih tržnih centara.

Veliki projekti koji su planirani u Beogradu su: Delta Planet

(75.000 m2) koji već ima potpisan ugovor o zakupu sa

hipermarketom i bioskopom, Višnjička Plaza (40.000 m2) koja

pregovara sa ankorima i Ada Mall (30.000 m2).

Potražnja

Novi brendovi koji su se na tržištu pojavili su Bagatt, italijanski

modni brend za obuću i Desigual, španski modni brend, koji su

zakupili lokale u tržnom centru Delta City, odnosno šću. Na

površini od 2.000 m2 u Stadion Shopping Centru je otvorena

decija igraonica Dream Land. Takodje u shopping centru Delta

City za septembar 2013. godine je planirano otvaranje decije

igraonice na 1,200 m2.

Prime rents €/m2/month

Cene zakupa prvoklasnog prostora €/m2/mesečno

Source/Izvor: Jones Lang LaSalle, July 2013

Potražnja stranih brendova za modernim prodajnim prostorom je i

dalje snažna; glavna prepreka brendovima koji nisu prisutni na

tržištu ili već postojećim koji žele da prošire svoju mrežu jeste

nedovoljna ponuda maloprodajnog prostora u modernim tržnim

centrima. Stopa nepopunjenog prostora u tržnim centrima je

skoro jednaka nuli a prazne lokale koje posetioci vide su samo

naizgled prazni, zbog promene zakupaca.

Visine zakupa i stope prinosa

Zakupi i stope prinosa prvoklasnih prostora ostali su nepromenjeni

u drugom tromesečju 2013.godine. Visina zakupa prvoklasnog

maloprodajnog prostora površine od 100 do 200 m2 u modernim

tržnim centrima iznosi €65/m2/mesečno, dok se isti takav prostor u

nez Mihajlovoj ulici može iznajmiti za € 0/m2/mesecno.

Prosečne visine zakupa u prvoklasnim tržnim centrima u

Beogradu kreću se od €27 do €29/m2/mesečno. Stopa prinosa za

prvoklasne tržne centre iznosi 9%.

8.75%

9.00%

9.25%

9.50%

9.75%

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

0

20

40

60

80

100

120

Q1

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q12

012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

High Street Shopping Centers

8 On Point • Belgrade City Report• Q2 2013

Market Practice

Leasing Market Practice

Lease length

• Average lease length is 5 years, 3 – 5 years are common in

the city centre and 5 (rarely 7) years on the outskirts

• In a few cases longer leases can be agreed

• 3 year break options are becoming more common

Payment Terms

• Rents are quoted in € and paid monthly in advance in either €

or RSD according to the exchange rate on the day of the

payment

Rental Deposit

• It is common to agree on a cash deposit or bank guarantee

equal to 3 months rent for all types of premises (office, retail

and industrial)

• Indexation is annually in line with European CPI

Other Charges

• Service and energy charges (Utilities and direct consumption

are paid separately)(offices and industrial)

• Service charges and marketing costs (retail)

Insurance

• The landlord covers costs of building insurance (recovered by

service charges). The tenant covers insurance of own

premises, contents and civil liabilities

Incentives

• Offered by the landlords in form of 3 month rent free period, fit-

out contributions and free of charge additional parking space

Tržišna praksa zakupa prostora

Dužina zakupa

• Prosečna dužina zakupa je 5 godina - uglavnom se prostori u

centru grada zakupljuju na 3 – 5 godina, a na periferiji na 5

(retko 7 godina)

• malom broju slučajeva se vrši zakup prostora na duži period

• Sve su češće mogućnosti raskida ugovora nakon 3 godine

Uslovi plaćanja

• Cene zakupa se navode u € a plaćaju se mesečno unapred ili u

€ ili u RSD prema valutnom kursu na dan plaćanja

Depozit

• Praksa je da se depozit plaća u kešu ili bankarskom garancijom

u iznosu od tri mesečne rente za sve vrste prostora

(kancelarijski, maloprodajni i industrijski)

• Indeksacija se vrši godišnje i usklađena je sa evropskim rastom

potrošačkih cena

Ostali troškovi

• Troškovi usluga i potrošnje električne energije (troškovi

održavanja i direktne potrošnje plaćaju se posebno)

(kancelarijski i industrijski prostori)

• Troškovi usluga i marketinga (maloprodajni prostori)

Osiguranje

• Vlasnik prostora pokriva troškove osiguranja zgrade (naplaćuje

se od naknade za troškove usluga). Zakupac plaća osiguranje

za sopstvene prostorije, pokretnu imovinu i civilna lica

Podsticaji

• Vlasnici prostora prilikom izdavanja mogu davati i podsticaje u

vidu izdavanja prostora na period od 3 meseca bez naknade,

uređenja prostora o sopstvenom trošku ili dodatna parking

mesta gratis

Jones Lang LaSalle offices

Belgrade

Bulevar Mihajla Pupina 6, 11070 Novi Beograd

Serbia

+ 381 11 22 00 101

+ 381 11 22 00 102

Contacts

Andrew Peirson

Managing Director

Jones Lang LaSalle

Serbia

+381 11 22 00 103

www.joneslanglasalle.com

Belgrade City Report Q2 2013

OnPoint reports from Jones Lang LaSalle include quarterly and annual highlights of real estate activity, performance and specialised

surveys and forecasts that uncover emerging trends.

www.joneslanglasalle.com

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of

Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We

would like to be told of any such errors in order to correct them.

.