bee industry roadmap

DESCRIPTION

Bee industry for women entrepreneursTRANSCRIPT

Page 1

DRAFT BEE INDUSTRY ROADMAP:

2011-2015

Prepared in collaboration with:UPLB Bee Program

BEENET Philippines Foundation, Inc.Beekeepers Association of the Philippines, Inc.

Evelyn JuanilloCoordinator

DA- BAR

Page 2

I. INDUSTRY PROFILE

• Philippine annual honey production = 50-110 mt

• Equivalent to PhP21.8 M

• Average annual yield per colony is 0.022 mt

• Products: pollen, propolis, beeswax

• Value-added products: honey wine, honey and propolis soap, shampoo, honey cider and propolis ointment

Page 3

I. INDUSTRY PROFILE

• Honey production in Luzon – November to May

• Visayas – September to November; peaks from March to May

• Mindanao – year round

• Effects of climate change impact on local vegetation affects honey flow

Page 4

I. INDUSTRY PROFILE

• Phil. Honey was classified as either multi-floral or unifloral based on the Harmonized Methods of the European Commission and the Codex Alimentarius

• No color grading or classification

• Prices were dictated by market categories and supply and demand

Page 5

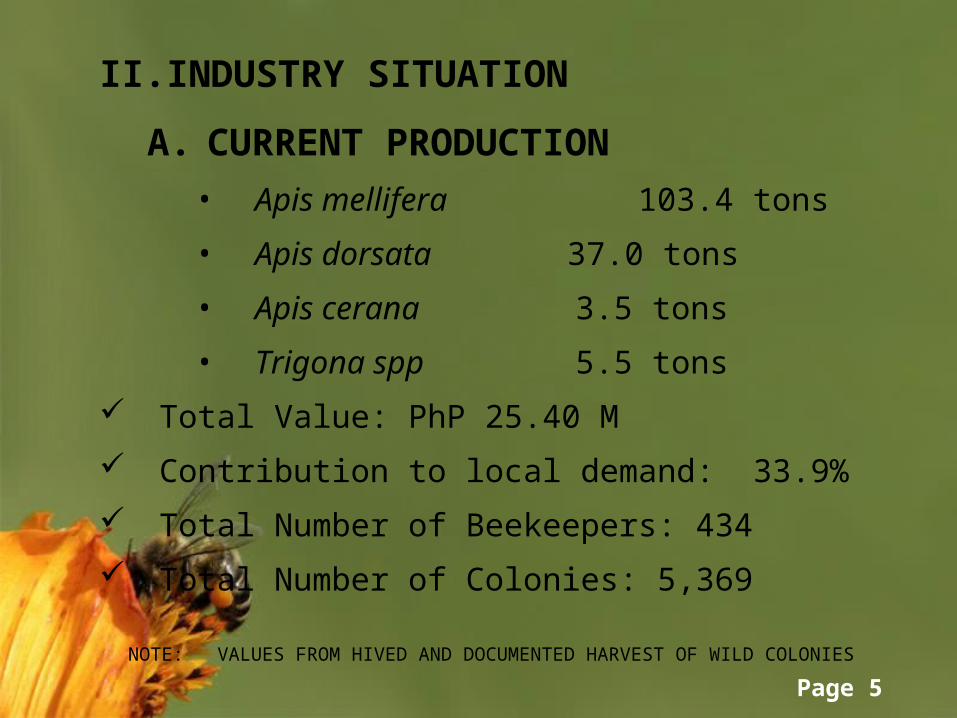

II. INDUSTRY SITUATION

A. CURRENT PRODUCTION

• Apis mellifera 103.4 tons

• Apis dorsata 37.0 tons

• Apis cerana 3.5 tons

• Trigona spp 5.5 tons

Total Value: PhP 25.40 M

Contribution to local demand: 33.9%

Total Number of Beekeepers: 434

Total Number of Colonies: 5,369

NOTE: VALUES FROM HIVED AND DOCUMENTED HARVEST OF WILD COLONIES

Page 6

II. INDUSTRY SITUATION

B. EXPORT• Total export 5,241 kilos• Total export value PhP 228,850.29

C. IMPORTS• Total imports 441.25 mt• Total value PhP 64.5 M

Note: export and import volumes are from the BTEP, 1st Q, 2009

Page 7

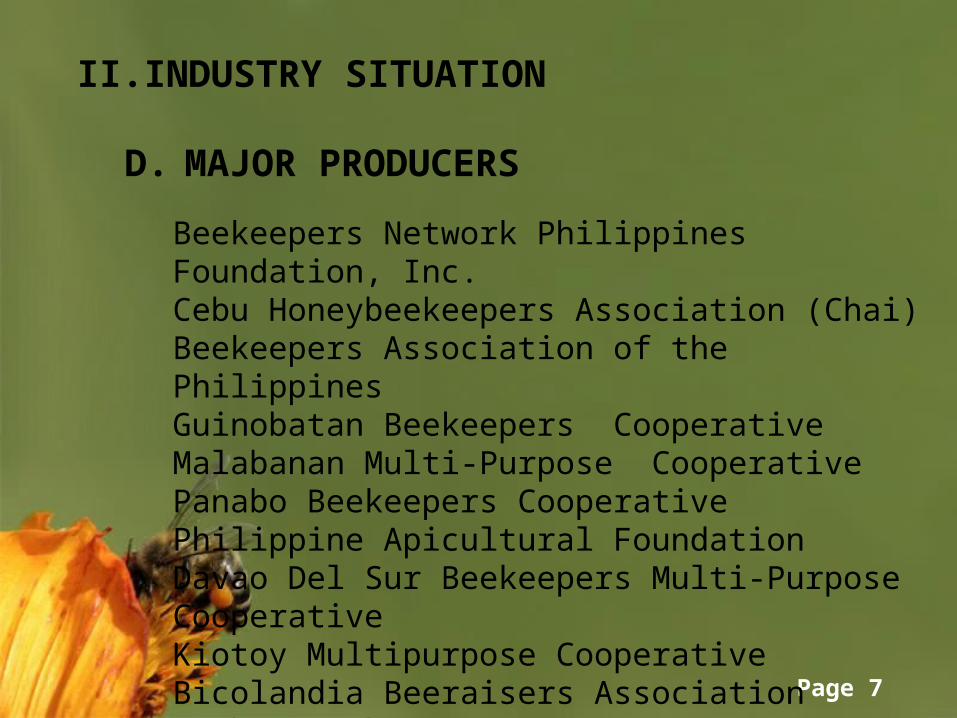

II. INDUSTRY SITUATION

D. MAJOR PRODUCERS

Beekeepers Network Philippines Foundation, Inc.Cebu Honeybeekeepers Association (Chai)Beekeepers Association of the PhilippinesGuinobatan Beekeepers CooperativeMalabanan Multi-Purpose CooperativePanabo Beekeepers CooperativePhilippine Apicultural FoundationDavao Del Sur Beekeepers Multi-Purpose CooperativeKiotoy Multipurpose CooperativeBicolandia Beeraisers AssociationBorbon Beekeepers Assn. Inc.

Page 8

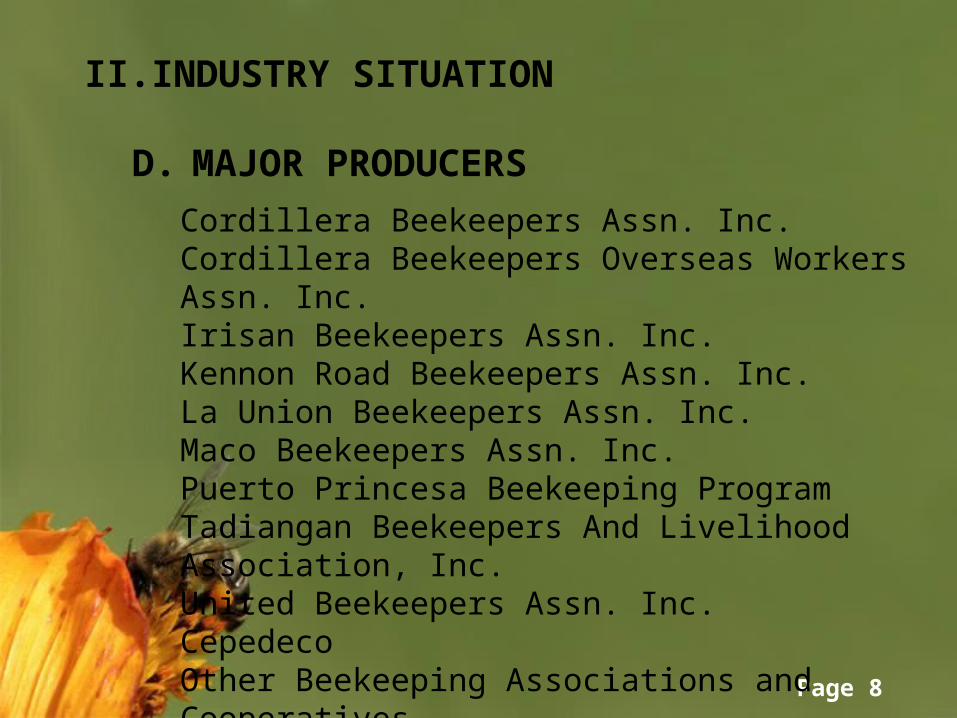

II. INDUSTRY SITUATION

D. MAJOR PRODUCERS

Cordillera Beekeepers Assn. Inc.Cordillera Beekeepers Overseas Workers Assn. Inc.Irisan Beekeepers Assn. Inc.Kennon Road Beekeepers Assn. Inc.La Union Beekeepers Assn. Inc.Maco Beekeepers Assn. Inc.Puerto Princesa Beekeeping ProgramTadiangan Beekeepers And Livelihood Association, Inc.United Beekeepers Assn. Inc.CepedecoOther Beekeeping Associations and Cooperatives

Note: export and import volumes are from the BTEP, 1st Q, 2009

Page 9

II. INDUSTRY SITUATION

E. R & D INSTITUTIONS

Benguet State UniversityCamarines Sur State Agricultural CollegeCavite State UniversityDon Mariano Marcos Memorial State UniversityMariano Marcos State UniversityPhilippine Normal UniversitySaint Louis UniversityUniversity of the Philippines Los Baños

Page 10

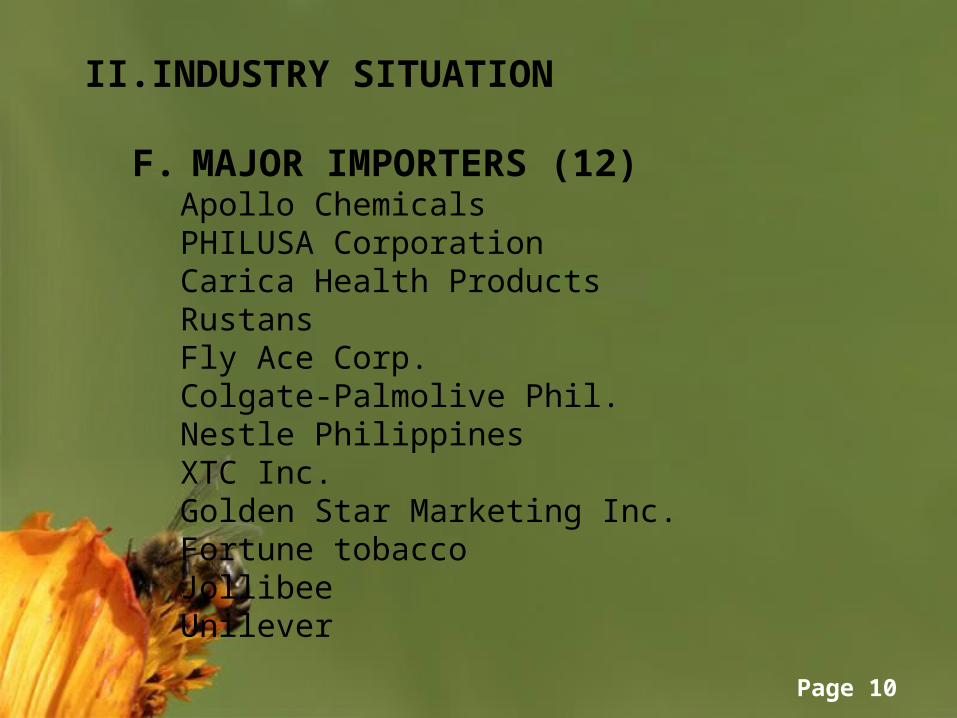

II. INDUSTRY SITUATION

F. MAJOR IMPORTERS (12)Apollo ChemicalsPHILUSA CorporationCarica Health ProductsRustansFly Ace Corp.Colgate-Palmolive Phil.Nestle PhilippinesXTC Inc.Golden Star Marketing Inc.Fortune tobaccoJollibeeUnilever

Page 11

II. INDUSTRY SITUATION

G. SAFETY NETS

Product quality; applying international standards for local and imported produce.

Honey and pollen analysis. Pathological and chemical residue analysis. Self-monitoring and reporting among

various beekeeping organizations. Coordination of R&D institutions with concerned government agencies like BFAD, FNRI and DTI.

Page 12

II. INDUSTRY SITUATION

G. SAFETY NETS

Bees and equipment

Quarantine of imported queens and other bee species. Restrictions on source and importation of Apis spp. colonies Pathological tests on local colonies. Quarantine and certification for migratory colonies.

Page 13

II. INDUSTRY SITUATION

H. BENEFITS

Generates employment – local and foreign job generation

Increases agricultural productivity – food security

Market of bees and bee products – income generation

Enhances biodiversity

Page 14

CROPS MEAN % YIELD INCREASE

Coconut ( Native San Ramon) 35-70

Cotton (Deltapine 16) 35

Tomato * 35

Cucurbits

Watermelon 73.9

Cucumber 76.5

Squash 88.9

Gourd 84.3

Luffa 85.1

Bitter gourd 98.7

Sunflower 30.0

Pechay 90.0

Chinese mustard 45.3

Passion fruit ^ 100.0

Sweet potato 17.0

Philippine lemon 56.0

Radish 22.0

Yield increase of some agricultural crops pollinated by beesSource: UPLB Bee Program.2004.* - pollinated by bumble bee^- pollinated by carpenter bee

Page 15

II. INDUSTRY SITUATION

I. INDUSTRY OPPORTUNITIES

Market led

Climatic and geographical advantage

Prospects for pollination

Diversified bee products

High honey prices

Page 16

II. INDUSTRY SITUATION

I. INDUSTRY OPPORTUNITIES

High consumer preference for local honey and

other bee products

Manpower exportation of beekeepers

Ecotourism

Page 17

III. INDUSTRY RISK

A. IMMEDIATE CONCERNS

Quality control of bees and bee products

Increase production

Security – quarantine, insurance, financing

R & D needs on genetic diversity, bee breeding, pollination and socio-economic constraints in technology adoption

Advocacy and legislation

Community development

Page 18

III. INDUSTRY RISK

B. HIGH IMPACT THREATS

Critical pests and diseases

Further decrease in access to native flora resources

Page 19

IV. THE BEE INDUSTRY ROADMAP

A. VISION

“A profitable bee industry that supports agriculture, forestry and biodiversity conservation and capable of supplying quality bees and bee products to local and foreign markets”

Page 20

IV. THE BEE INDUSTRY ROADMAP

B. MISSION

“To provide a collaborative forum for industry, funding agencies, and RD and E providers to lead research, innovation and adoption to benefit the Philippine bee industry”

Page 21

IV. THE BEE INDUSTRY ROADMAP

C. GOALS Strengthen the multi-disciplinary RDE programs

Training and capacity development

Support enterprise development

Integrate apiculture in the farming systems

Conserve and manage indigenous bee species

Institutionalize policies on importation and quarantine

Page 22

IV. THE BEE INDUSTRY ROADMAP

D. OBJECTIVES Establish regional centers for beekeeping, accredit

one service laboratory for each region

Generate R&D apiculture technologies

Promote standardization of bee products

Develop and strengthen policies to promote organic agriculture by integrating apicultural technologies

Promote apitourism

Establish information hub for DA-HVCDP

Page 23

IV. THE BEE INDUSTRY ROADMAP

E. TARGETS Continuous supply of quality queen bees and bee

stocks

Increased production of quality bees and bee products

Strict quarantine of imported queen bees and bee products

Page 24

IV. THE BEE INDUSTRY ROADMAP

E. TARGETS Designation of bee inspectors per region

Available channels for financing of industry and research needs

Development of human resource for R&D in beekeeping and for entrepreneurial income generating endeavor

Page 25

IV. THE BEE INDUSTRY ROADMAP

F. STRATEGIES

Major Strategies Key Institutions

Enhancement of and increasing funding for RD&E• biodiversity and genetic studies• bee product development• management and conservation• pollination• technology adoption

Page 26

IV. THE BEE INDUSTRY ROADMAP

F. STRATEGIES

Major Strategies Key Institutions

Improving access to quality and reasonably priced inputs• Queens• Nucleus colonies• Equipment

Page 27

IV. THE BEE INDUSTRY ROADMAP

F. STRATEGIES

Major Strategies Key Institutions

Linkages with or partnership with various industry support mechanisms (i.e. strong links between beekeepers, buyers and inter-agency and private-public partnerships

Page 28

IV. THE BEE INDUSTRY ROADMAP

F. STRATEGIES

Major Strategies Key Institutions

Enhancement of bees and bee product quality and classification standards

Enhancement of marketing structure facilities (i.e. access roads, processing centers, eyc.)

Page 29

IV. THE BEE INDUSTRY ROADMAP

F. STRATEGIES

Major Strategies Key Institutions

Human resource development

Export market development

Policy analysis and advocacy

Page 30

IV. THE BEE INDUSTRY ROADMAP

G. EXTERNAL AND AGRICULTURE PRIORITIES

Priorities for the bee industry roadmap need to be integrated and coordinated with the:

• Broader national RD & E thrust of the Philippine government including the initiatives set by the DA under the HVCDP and DA-BAR

• Regional agreements and initiatives

• International bee research trends

• Investment by other associated industries

Page 31

IV. BEE ROADMAP WORKPLAN SCHEDULE

Page 32

Thank you.

Evelyn JuanilloDA- BAR