becoming a homeowner module 11 instructor guide - freddie mac

TRANSCRIPT

2 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

This page intentionally left blank.

3 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

CreditSmart® Module 11: Becoming a Homeowner

Table of Contents

Welcome to Freddie Mac’s CreditSmart® Initiative ......................................................................... 6

Program Structure ....................................................................................................................... 6

Using the Instructor Guides ......................................................................................................... 7

Lesson Concepts and Icons ............................................................................................................... 8 How to Access the WBT ............................................................................................................... 8

Tips for Instructors ........................................................................................................................... 9 Workshop Preparation Tips ......................................................................................................... 9

Before the Workshop Begins ....................................................................................................... 9

Adult Learning Tips .................................................................................................................... 10

Instructor Training ..................................................................................................................... 10

Introduction to Module 11: Becoming a Homeowner ................................................................... 11 Module Overview ....................................................................................................................... 11

Glossary ..................................................................................................................................... 11

Topic 1: Is Homeownership Right for You? .................................................................................... 12 Overview .................................................................................................................................... 12

Is Homeownership Right for You? .............................................................................................. 12

Start the Discussion ................................................................................................................... 12

Activity ....................................................................................................................................... 14

Topic 2: Why Own a Home? ........................................................................................................... 15 Overview .................................................................................................................................... 15

Why Own a Home? .................................................................................................................... 15

Start the Discussion ................................................................................................................... 15

Build Equity ................................................................................................................................ 17

Gain Tax Advantages .................................................................................................................. 18

Rely on Monthly Principal and Interest Payment Stability ......................................................... 19

Gain a Sense of Community ....................................................................................................... 20

Rent or Buy?............................................................................................................................... 21

Knowledge Check ....................................................................................................................... 22

Topic 3: Buying a Short Sale or REO/Bank-Owned Property ........................................................... 23 Overview .................................................................................................................................... 23

Buying a Short Sale or Bank-Owned Property ............................................................................ 23

Start the Discussion ................................................................................................................... 23

Short Sales: What You Need to Know ........................................................................................ 24

4 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

What is a Short Sale? ................................................................................................................. 25

Am I a Good Candidate for a Short Sale? ................................................................................... 26

What is the Buying Process for Short Sales? .............................................................................. 26

REO and Bank-Owned Properties .............................................................................................. 27

What is a REO or Bank-Owned Property? .................................................................................. 27

What Should I Know About Buying an REO Home? ................................................................... 28

What is the Buying Process for REO Properties ......................................................................... 28

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs ................................................ 29 Overview .................................................................................................................................... 29

Down Payments, Mortgage Insurance, Closing Costs ................................................................ 29

Start the Discussion ................................................................................................................... 29

Activity ....................................................................................................................................... 31

Down Payments ......................................................................................................................... 33

Mortgage Insurance ................................................................................................................... 34

Closing Costs .............................................................................................................................. 36

Other Costs ................................................................................................................................ 37

Activity ....................................................................................................................................... 37

Section Conclusion ..................................................................................................................... 38

Topic 5: Finding a Mortgage Lender ............................................................................................... 39 Overview .................................................................................................................................... 39

Finding a Mortgage Lender ........................................................................................................ 39

Start the Discussion ................................................................................................................... 39

Types of Mortgages ................................................................................................................... 42

Fixed-Rate Mortgages ................................................................................................................ 43

Adjustable-Rate Mortgage ......................................................................................................... 44

Mortgage Shopping Tips ............................................................................................................ 46

Affordable, Low Down Payment Mortgages .............................................................................. 47

Activity ....................................................................................................................................... 48

Topic 6: Finding a Real Estate Agent .............................................................................................. 50 Overview .................................................................................................................................... 50

Finding a Real Estate Agent ........................................................................................................ 50

Start the Discussion ................................................................................................................... 50

Questions to Ask a Real Estate Agent ........................................................................................ 52

Homeownership Education and Credit Counseling .................................................................... 53

Section Conclusion ..................................................................................................................... 55

Module Conclusion ......................................................................................................................... 56

5 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Module Summary....................................................................................................................... 56

Appendix A: Glossary ...................................................................................................................... 57

6 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Welcome to Freddie Mac’s CreditSmart® Initiative

This consumer financial education and outreach initiative is designed to help

consumers build and maintain better credit, make sound financial decisions, and understand the steps to successful long-term homeownership. In this guide, you’ll find everything you need to lead participants through real-life scenarios, group discussions and activities that will encourage them to apply these lessons to their daily lives. By sharing the CreditSmart resources with others, you’ll help them increase their financial understanding, gain life-long money management skills, and show them how to avoid costly mistakes.

Program Structure

The CreditSmart Curriculum includes 12 complete financial education modules that can be completed in two ways – self-paced online or in a classroom setting.

Module Title

1 Your Credit and Why It Is Important

2 Managing Your Money

3 Goal Setting

4 Banking Services: An Important Step

5 Establishing and Maintaining Credit

6 Understanding Credit Scoring

7 Thinking Like a Lender

8 Avoiding Credit Traps

9 Restoring Your Credit

10 Planning For Your Future

11 Becoming a Homeowner

12 Preserving Homeownership: Protecting Your Home Investment

Continued on next page

7 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Welcome to Freddie Mac’s CreditSmart® Initiative, Continued

Using the Instructor Guides

The Instructor Guides can be used alone or as an adjunct to the Web-Based Training (WBT) program. Even if participants choose not to experience the program online, gaining familiarity with the WBT will help you present the material more effectively. The most up to date content can always be found online at www.freddiemac.com/creditsmart/consumer_training.html. Each of the twelve CreditSmart modules has its own Instructor Guide which follows the organization of the Web-Based Training (WBT) available online, and includes much of the same content. Each Instructor Guide includes:

A glossary of all the relevant terms introduced in the module

A module introduction which includes

An overview

Learning objectives

Sample discussion questions to start the lesson

“The Basics” – a list of bullet points outlining the key concepts of the lesson

A lesson summary of all the key concepts in the lesson

Activities, knowledge checks, discussion questions, and handouts

8 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Lesson Concepts and Icons

Each module topic will present several key concepts. These concepts are introduced

to your participants in a variety of ways described in the table below.

Activity An activity usually involves class participation, whether it is a game, exercise, or worksheet completion. Typically after an activity you will have the opportunity to lead a discussion.

Discussion

Discussions allow you to introduce key concepts while involving your participants in the conversation and making the information relevant to them. Sample questions are included in each lesson to help you guide the discussion.

Knowledge Check

There are short knowledge checks throughout each topic designed to start discussions or quickly test participants’ knowledge of certain concepts.

How to Access the WBT

The CreditSmart Web-Based Training (WBT) is available free of charge in both English and Spanish and can be accessed online at www.freddiemac.com/creditsmart/consumer_training.html.

9 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Tips for Instructors

The following tips and suggestions will help to ensure the successful delivery of the

CreditSmart curriculum.

Workshop Preparation Tips

Select handouts and exercises for each topic in advance to help enhance your presentation and discussion with participants.

Determine if you will need other instructional materials such as overhead transparencies, slides, flip charts, handouts, and videos.

Arrive at the workshop location early to set up.

Decide how the room should be set up (e.g., classroom style, lecture).

Make sure that all of the necessary equipment, such as a computer and projector is available and working.

Provide a sign-in sheet and allow space (e.g., side table, counter, etc.) for handouts and resource materials.

Set up refreshments, if provided.

Provide adequate signs directing participants to the workshop location.

Greet and welcome participants individually as they arrive.

Begin the workshop promptly.

Distribute and collect evaluation forms before the end of each workshop.

Confirm that all participants have signed the sign-in sheet to ensure credit for attending the workshop.

Before the Workshop Begins

Welcome participants and introduce yourself.

Review logistics (session length, restroom location, breaks, etc.).

Provide a brief history of the CreditSmart curriculum, which you can find a www.freddiemac.com/creditsmart.

Provide an overview of workshop materials.

10 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Tips for Instructors, Continued

Adult Learning Tips

Adults learn in different ways; therefore, you will want to use different techniques, vary your presentation style, and be sensitive to how your students are responding.

Relate the content to what your students already know. Doing so will make your workshop more effective and will help to ensure participants retain more information.

Be sensitive to those with special needs and/or learning disabilities.

Use ice breakers, activities, exercises, and/or videos to break up the flow of your presentation.

Supply handouts and local and/or national articles that highlight the topic being presented.

Poll the audience to gauge participants’ level of knowledge of the topic being presented.

Research available community credit counseling resources in advance to ensure that consumers have access to appropriate referrals, as necessary.

Instructor Training

Freddie Mac provides CreditSmart instructor training for anyone who is interested in teaching the CreditSmart curriculum. Select one of the options below:

Contact Freddie Mac by emailing: [email protected].

Attend a CreditSmart Train-the-Trainer workshop hosted by Freddie Mac. This instructor training series includes a comprehensive review of the CreditSmart curriculum, plus instruction on best practices in conducting effective classroom training. Visit http://www.freddiemac.com/creditsmart/for more information.

11 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Introduction to Module 11: Becoming a Homeowner

Module Overview

This module will help participants understand the benefits, decisions and the costs involved with buying a home. This module is divided into the following sections:

1. Is Homeownership Right for You? 2. Working With Your Lender

Learning Objectives

After completing this module, participants should be able to:

Determine if they are ready to buy a home

Describe ways to prepare to purchase and own a home

List the advantages of buying versus renting a home

List and explain the variety of expenses involved in purchasing and maintaining a home

Module Topic:

Is Homeownership Right for You?

Why Own a Home?

Buying a Short Sale or REO/Bank-Owned Property

Down Payments, Mortgage Insurance, and Closing Costs

Finding a Mortgage Lender

Finding a Real Estate Agent

This topic includes activities to help simulate real-world scenarios with your participants.

Glossary

A Glossary is included in Appendix A of this guide, and contains definitions and descriptions of terms and phrases related to this module. A Glossary is also included in the Participant Presentation. Encourage your participants to use the Glossary during and after the class to become more familiar with the terminology.

12 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 1: Is Homeownership Right for You?

Overview In this section, participants will be able to determine if homeownership is right for

them. They will also discuss ways that they can prepare to buy and own their own home. They will learn about the advantages of buying versus renting a home and how to determine their readiness to buy a home.

Time 20 minutes

Is Homeownership Right for You?

The Basics

Buying a home is one of the largest purchases you will ever make.

Homeownership offers many benefits.

Before buying a home, you need to address any concerns and seek accurate information from a reliable source.

It is important to get started early with a HUD-approved counseling agency that can address your concerns.

Start the Discussion

To start the discussion with your participants, ask some open-ended questions. Here are some examples to get you started:

How many people do you think own their own home (about two-thirds)?

What steps would you take to determine if you are ready, financially or otherwise, to own your own home?

What are some of the benefits of owning your own home? What are some of the risks?

Continued on next page

13 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 1: Is Homeownership Right for You?, Continued

Start the Discussion (continued)

Is Homeownership Right for You?

Is Homeownership Right for You? (cont.)

14 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 1: Is Homeownership Right for You?, Continued

Activity Instructor note:

Ask participants to turn to page 8 of the Participant Presentation to complete the “Are You Ready to Buy a Home?” questionnaire. Explain that this questionnaire will help them determine their readiness to buy a home. Read each question out loud and ask participants to answer each question by selecting “Yes” or “No” in the column to the right. See instructor copy below.

Questionnaire: Are You Ready to Buy a Home?

15 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?

Overview This topic discusses reasons for owning a home.

Time 15 minutes

Why Own a Home?

The Basics

Some people rent a home because they think they can’t afford to buy one.

When you rent, you can live in a neighborhood for as little or as long as you want.

There are fewer maintenance responsibilities when you rent.

There are many benefits to owning a home including the opportunity to build equity.

Owning a home is an opportunity to settle down and gain a sense of belonging in a community.

The value of your home can increase over time, making your investment grow.

Most homeowners receive tax breaks, because interest paid on a home mortgage and real estate taxes are almost always tax deductible.

Deciding whether to rent or buy is a personal decision. Each option offers different advantages.

Start the Discussion

To start the discussion with your participants, ask some open-ended questions. Here are some examples to get you started:

What are some of the benefits of owning a home versus renting?

What are some of the main differences between owning a home and renting?

What impact can owning a home have on your credit rating?

16 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Start the Discussion (continued)

Why Own a Home?

Instructor note:

Define the following term:

Term Definition

Equity Equity is the value in your home above the total amount of the liens against your home. If you owe $100,000 on your house, but it is worth $130,000, you have $30,000 of equity.

Continued on next page

17 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Build Equity

Why Own a Home? (cont.)

Instructor note:

Define the following terms:

Term Definition

Mortgage

A mortgage is a document that is signed by a borrower when a home loan is obtained and gives the lender the right to take possession of the property if the borrower fails to make loan payments.

Interest Interest is a charge for using someone else's funds. Interest is typically indicated as a percentage of the amount borrowed.

Principal

Principal is the actual amount of money borrowed or the remaining amount of the loan that has not yet been paid back to the lender. The principal balance of a loan is the borrower’s debt.

Amortization

Amortization is the term used to describe the gradual reduction of the outstanding balance of the loan as the amount of the loan is gradually paid down over a predetermined period of time at a specific interest rate.

Continued on next page

18 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Build Equity (continued)

Term Definition

Appreciation Appreciation is the term used to describe an increase in the market value of a home due to changing market conditions and/or home improvements.

Gain Tax Advantages

Why Own a Home? (cont.)

19 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Rely on Monthly Principal and Interest Payment Stability

Why Own a Home? (cont.)

Instructor note:

Define the following terms:

Term Definition

Homeowner’s Insurance

Homeowner’s insurance is a policy that protects you and the lender from losses resulting from things like fire or flood, which may damage the structure of the house, create liability (such as injury to a visitor to your home), or cause damage to or theft of your personal property (such as to furniture, clothes, or appliances).

Inflation Inflation is an increase in the general level of prices.

20 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Gain a Sense of Community

Why Own a Home? (cont.)

21 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Rent or Buy?

Rent or Buy?

Rent or Buy? (cont.)

22 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 2: Why Own a Home?, Continued

Knowledge Check

Instructor note:

Ask participants to turn to page 16 of the Participant Presentation to identify reasons why you might want to own a home.

Knowledge Check 1

Instructor note:

After participants have answered the question, review the following correct answers:

Opportunity to build equity

May gain a tax advantage

Stable monthly payments

23 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 3: Buying a Short Sale or REO/Bank-Owned Property

Overview This topic discusses short sales and REO/bank-owned properties.

Time 15 minutes

Buying a Short Sale or Bank-Owned Property

The Basics

If you are not able to maintain payments a short sale allows you to sell your home and use the proceeds to pay off the mortgage, even if the home’s market value is less than the total amount owed.

In a short sale, the lender and all parties involved agree to sell a property at a price that is below the mortgage balance owed by the borrower – and the borrower is permitted to sell the home at or near the current market value.

A short sale allows both delinquent and current borrowers to avoid foreclosure.

When purchasing a short sale, it is important to find a real estate professional with experience in short sale transactions.

Purchasing a short sale requires patience and flexibility.

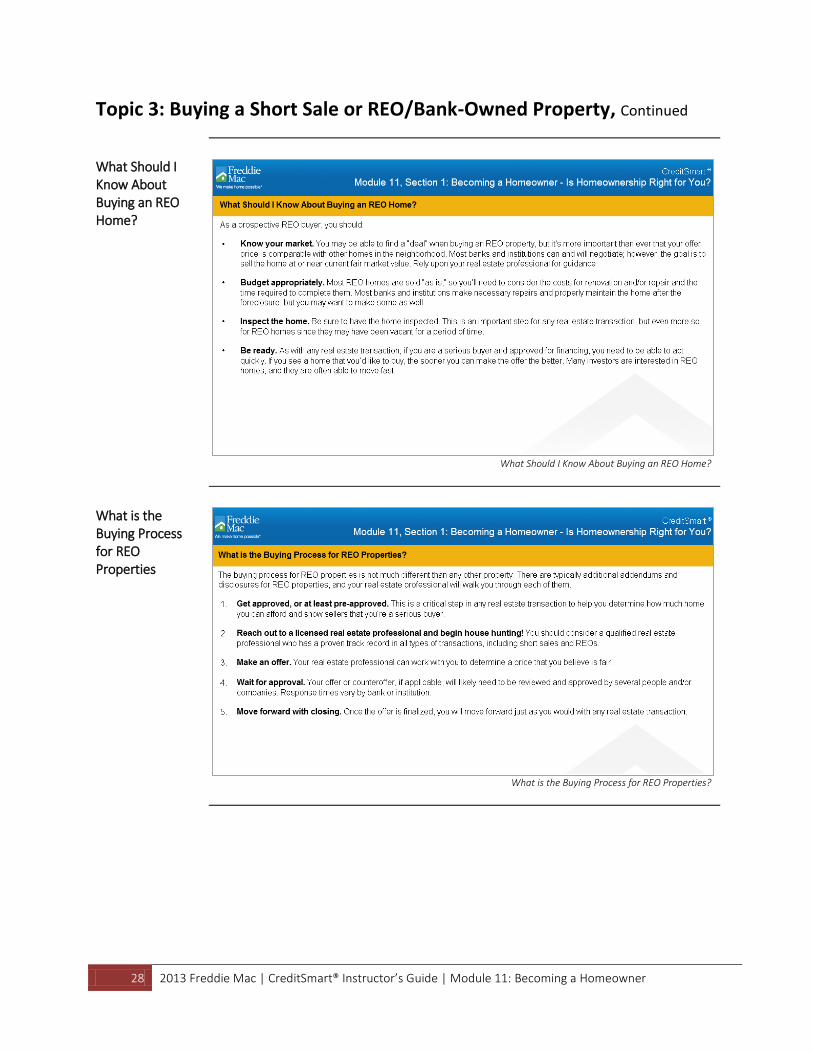

REO or bank-owned properties are homes that have been through the entire foreclosure process and are now owned by the lender.

As with any real estate transaction, if you are a serious buyer and approved for financing, you need to be able to act quickly. If you see a home that you’d like to buy, the sooner you can make the offer the better. Many investors are interested in REO homes, and they are often able to move fast.

Start the Discussion

To start the discussion with your participants, ask some open-ended questions. Here are some examples to get you started:

How do you know if buying a short sale is right for you?

What are some of the benefits to buyers of purchasing a short sale?

Why do you think it is important to work with a real estate agent who has experience with short sales?

24 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 3: Buying a Short Sale or REO/Bank-Owned Property, Continued

Start the Discussion (continued)

Buying a Short Sale or REO/Bank-Owned Property

Short Sales: What You Need to Know

Short Sales: What You Need to Know

25 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 3: Buying a Short Sale or REO/Bank-Owned Property, Continued

What is a Short Sale?

What is a Short Sale?

What is a Short Sale? (cont.)

26 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 3: Buying a Short Sale or REO/Bank-Owned Property, Continued

Am I a Good Candidate for a Short Sale?

Am I a Good Candidate for a Short Sale?

What is the Buying Process for Short Sales?

What is the Buying Process for Short Sales?

27 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 3: Buying a Short Sale or REO/Bank-Owned Property, Continued

REO and Bank-Owned Properties

REO and Bank-Owned Properties: What You Need to Know

What is a REO or Bank-Owned Property?

What is a REO or Bank-Owned Property?

28 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 3: Buying a Short Sale or REO/Bank-Owned Property, Continued

What Should I Know About Buying an REO Home?

What Should I Know About Buying an REO Home?

What is the Buying Process for REO Properties

What is the Buying Process for REO Properties?

29 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs

Overview This topic discusses the costs associated with buying a home.

Time 20 minutes

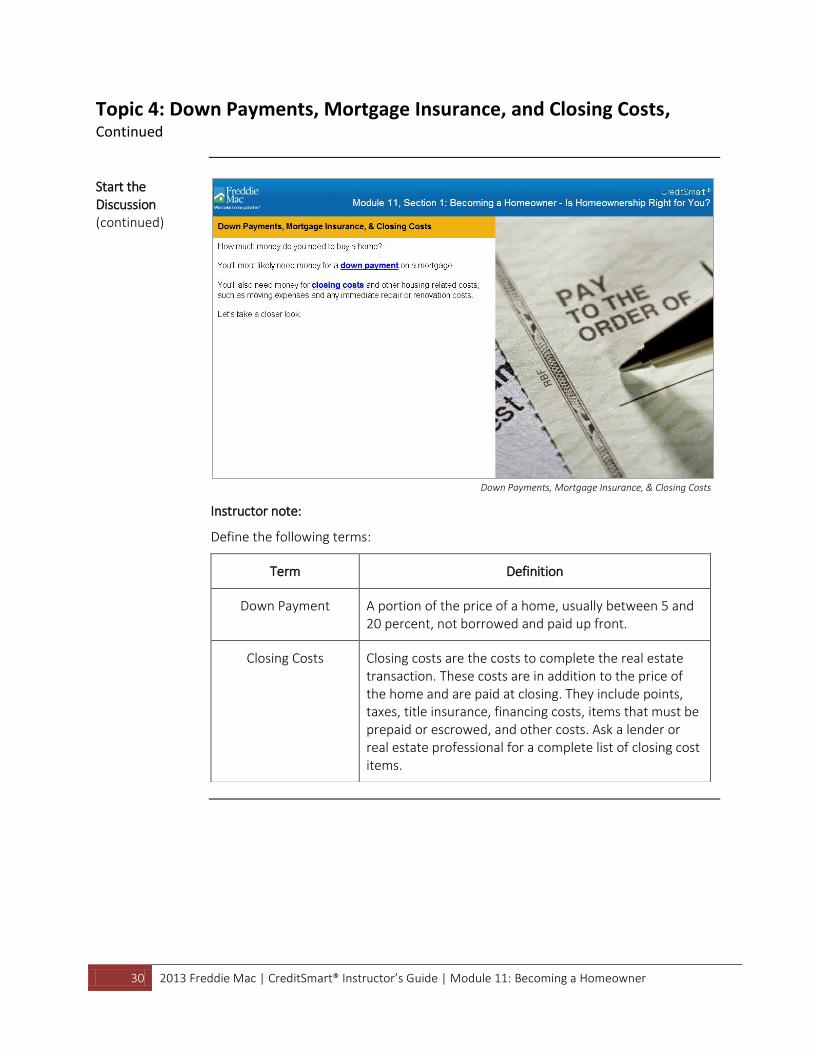

Down Payments, Mortgage Insurance, Closing Costs

The Basics

You will most likely need money for a down payment on a mortgage. A down payment is a percentage of the value of the property and is determined by the type of mortgage you choose.

You’ll also need money for closing costs and other housing-related costs, such as moving expenses and any immediate repair or renovation costs.

Loans with less than 20 percent down typically have some type of additional mortgage insurance-related costs.

Mortgage insurance helps to protect lenders from losses in the event that you default on your mortgage and lose your home to foreclosure.

Closing costs generally range from 3% to 7% of the mortgage amount depending upon the loan program.

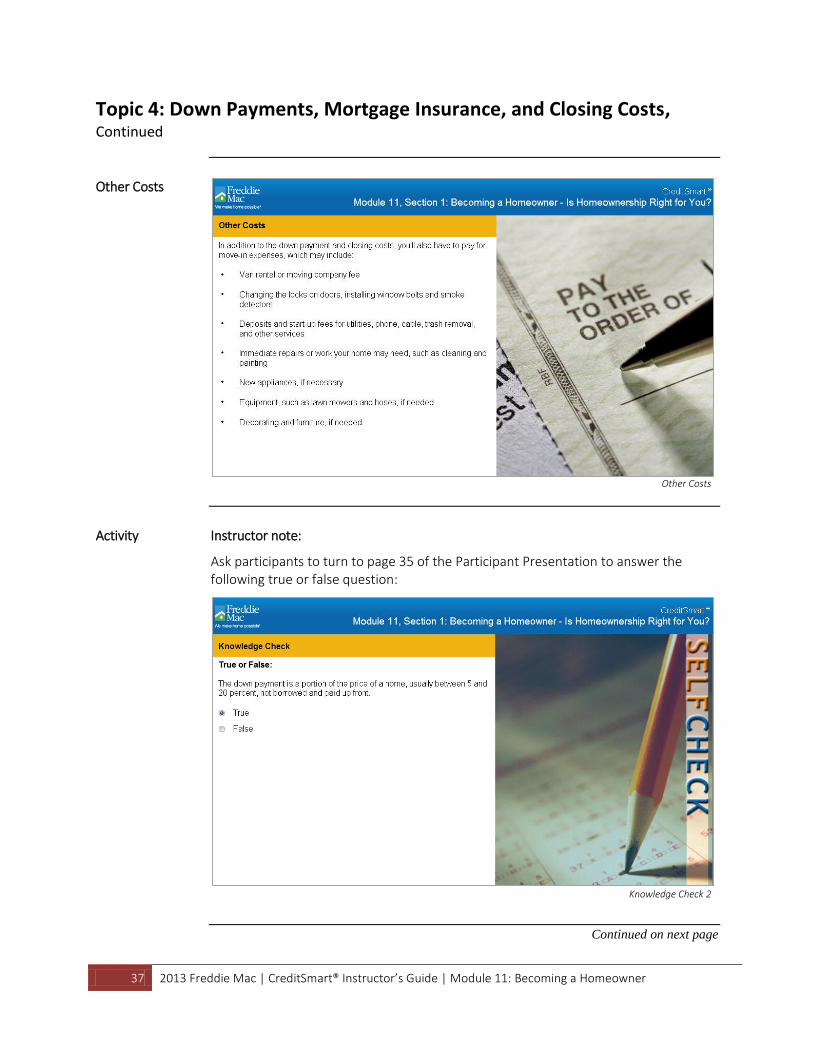

In addition to the down payment and closing costs, you’ll also have to pay for moving expenses which may include van rental fee, changing the locks on doors, deposits and start-up fees for utilities, new appliances, and decorating and furniture, if needed.

Start the Discussion

To start the discussion with your participants, ask some open-ended questions. Here are some examples to get you started:

What does it mean to default on your mortgage?

What is a Good Faith Estimate? What types of costs are included?

What other costs are associated with moving and how can you prepare for them?

Continued on next page

30 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Start the Discussion (continued)

Down Payments, Mortgage Insurance, & Closing Costs

Instructor note:

Define the following terms:

Term Definition

Down Payment A portion of the price of a home, usually between 5 and 20 percent, not borrowed and paid up front.

Closing Costs Closing costs are the costs to complete the real estate transaction. These costs are in addition to the price of the home and are paid at closing. They include points, taxes, title insurance, financing costs, items that must be prepaid or escrowed, and other costs. Ask a lender or real estate professional for a complete list of closing cost items.

31 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Activity Instructor note:

Ask participants to turn to page 29 of the Participant Presentation to complete “The Costs of Homeownership” exercise. Ask participants to work in groups to match the correct cost of homeownership phrase in the Word Bank with its correct description. After they have completed the exercise, review each cost and description. See instructor copy on the next page.

Word Bank

Foreclosure

Down Payment

Closing Costs

Private Mortgage Insurance (PMI)

Escrow

Good Faith Estimate

Mortgage Insurance Premium (MIP)

Lenders

Default

Points

Title Insurance

Continued on next page

32 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Cost Description

Default Failure to meet a payment or fulfill a credit obligation.

Mortgage Insurance Premium (MIP)

The cost of the insurance which the Federal Housing Administration (FHA) provides to lenders and is paid by the individual homebuyer.

Escrow The holding of money or documents by a neutral third party prior to closing. It can also be an account held by the lender (or servicer) into which a homeowner pays money for taxes and insurance.

Down Payment A portion of the price of a home, usually between 5 and 20 percent, not borrowed and paid up front.

Foreclosure A legal process in which collateral property is sold in an attempt to satisfy the outstanding debt of a mortgage.

Closing Costs Costs to complete the real estate transaction. These costs are in addition to the price of the home and are paid at closing. They include points, taxes, title insurance, financing costs, items that must be prepaid or escrowed, and other costs.

Points Points are a one-time charge by a lender to lower the interest rate of a loan. One point is equal to 1 percent of the loan amount.

Lender Lender is the term used for the person or entity that is providing credit or a loan to a borrower at specific terms and conditions. The term lender can generally be used interchangeably with the term creditor.

Continued on next page

33 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Cost Description

Good Faith Estimate A written statement itemizing the approximate costs and fees for the mortgage.

Title Insurance Insurance that protects lenders and homeowners against loss of their interest in the property because of legal problems with the title.

Private Mortgage Insurance (PMI)

Private Mortgage Insurance or PMI is a type of insurance which helps to protect lenders from losses in the event that a homeowner defaults on his or her mortgage and loses his or her home to foreclosure.

PMI is generally required by lenders when a homebuyer pays less than 20 percent as a down payment on a loan. PMI coverage will cost approximately 1 percent of the loan amount up front, plus an additional .50 percent annual premium paid monthly.

Down Payments

Down Payments

Continued on next page

34 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Mortgage Insurance

Mortgage Insurance

Instructor note:

Define the following terms:

Term Definition

Private Mortgage Insurance (PMI)

Private Mortgage Insurance or PMI is a type of insurance which helps to protect lenders from losses in the event that a homeowner defaults on his or her mortgage and loses his or her home to foreclosure.

PMI is generally required by lenders when a homebuyer pays less than 20 percent as a down payment on a loan. PMI coverage will cost approximately 1 percent of the loan amount up front, plus an additional .50 percent annual premium paid monthly.

Continued on next page

35 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Mortgage Insurance (continued)

Term Definition

Mortgage Insurance Premium (MIP)

A mortgage insurance premium or MIP is the cost of the insurance which the Federal Housing Administration (FHA) provides to lenders and is paid by the individual homebuyer.

MIP is made up of two parts: up front mortgage insurance premium (UFMIP), and annual insurance premium, which is collected in monthly installments.

Lender

Lender is the term used for the person or entity that is providing credit or a loan to a borrower at specific terms and conditions. The term lender can generally be used interchangeably with the term creditor.

Default A default is a failure to meet a payment or fulfill a credit obligation.

Foreclosure A legal process in which collateral property is sold in an attempt to satisfy the outstanding debt of a mortgage.

36 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Closing Costs

Closing Costs

Instructor note:

Define the following terms:

Term Definition

Points Points are a one-time charge by a lender to lower the interest rate of a loan. One point is equal to 1 percent of the loan amount.

Title Insurance Insurance that protects lenders and homeowners against loss of their interest in the property because of legal problems with the title.

Escrow

The holding of money or documents by a neutral third party prior to closing. It can also be an account held by the lender (or servicer) into which a homeowner pays money for taxes and insurance.

Good Faith Estimate (GFE)

A written statement itemizing the approximate costs and fees for the mortgage.

37 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Other Costs

Other Costs

Activity Instructor note:

Ask participants to turn to page 35 of the Participant Presentation to answer the following true or false question:

Knowledge Check 2

Continued on next page

38 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 4: Down Payments, Mortgage Insurance, and Closing Costs, Continued

Section Conclusion

Section Conclusion

39 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender

Overview This topic discusses how to prepare to get a mortgage.

Time 20 minutes

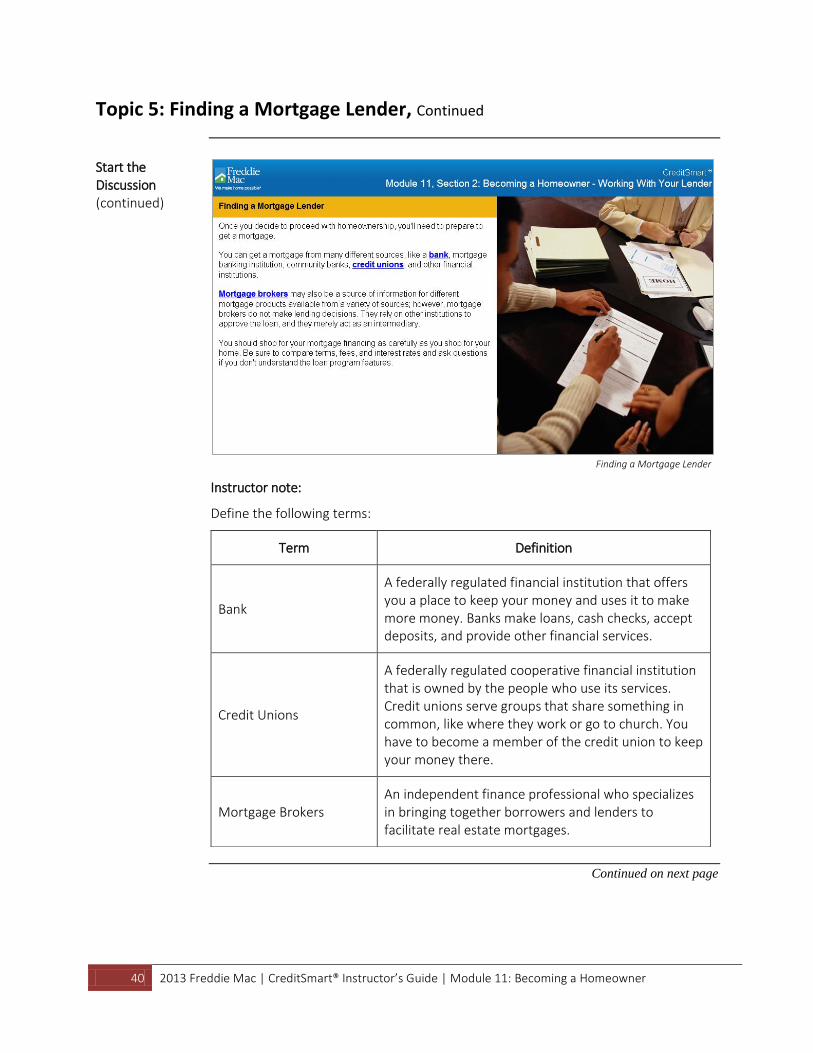

Finding a Mortgage Lender

The Basics

You can get a mortgage from many different sources like a bank, mortgage banking institution, community banks, credit unions, and other financial institutions.

Mortgage brokers may also be a source of information for different mortgage products available from a variety of sources.

There are many different types of mortgages. It is important to shop around to find the mortgage that is right for you.

Saving enough money for a down payment can be hard. However, many mortgage lenders offer low down payment mortgages and programs with flexible underwriting guidelines to help people in these types of financial situations.

Some mortgages offer a lower down payment along with paid or financed closing costs.

Always be careful when selecting a lender because there are a few you should watch out for.

A responsible lender can help you gain financial flexibility and achieve your goals.

Start the Discussion

To start the discussion with your participants, ask some open-ended questions. Here are some examples to get you started:

What are the steps you should take to determine how much mortgage you can afford?

In addition to mortgage payments, what other costs should you consider when figuring out how much you can afford?

What things do you think are most important to lenders when they review a home loan application?

What are some benefits of getting pre-approved for a mortgage?

40 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Start the Discussion (continued)

Finding a Mortgage Lender

Instructor note:

Define the following terms:

Term Definition

Bank

A federally regulated financial institution that offers you a place to keep your money and uses it to make more money. Banks make loans, cash checks, accept deposits, and provide other financial services.

Credit Unions

A federally regulated cooperative financial institution that is owned by the people who use its services. Credit unions serve groups that share something in common, like where they work or go to church. You have to become a member of the credit union to keep your money there.

Mortgage Brokers An independent finance professional who specializes in bringing together borrowers and lenders to facilitate real estate mortgages.

Continued on next page

41 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Start the Discussion (continued)

Finding a Mortgage Lender (cont.)

Instructor note:

Define the following terms:

Term Definition

Checking Account

An account that lets you write checks to pay bills or to buy goods. The financial institution takes the money from your account and pays it to the person named on the check. The financial institution sends you a monthly record of the deposits made and the checks written.

Savings Account An account where you keep money for safekeeping or as an investment that earns interest.

Real Estate Professional

An individual who provides services in buying and selling homes. The real estate professional is paid a percentage of the home sale price by the seller.

Unless you have signed an agreement with the real estate agent to be a buyer's agent, the real estate professional represents the interest of the property seller.

Continued on next page

42 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Start the Discussion (continued)

Term Definition

Homeownership Education

Offered through community service organizations, it provides information on the mortgage approval process, home selection elements, financing and closing processes, mortgage delinquencies, and foreclosures.

Types of Mortgages

Types of Mortgages

Instructor note:

Define the following terms:

Term Definition

Balloon Mortgage

A mortgage with monthly payments based on a 30- year amortization schedule and the unpaid principal balance due in a lump sum payment at the end of a specific period (usually 5 or 7 years) earlier than 30 years. The mortgage contains an option to reset the interest rate to the current market rate and to extend the maturity date provided certain conditions are satisfied.

Continued on next page

43 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Types of Mortgages (continued)

Term Definition

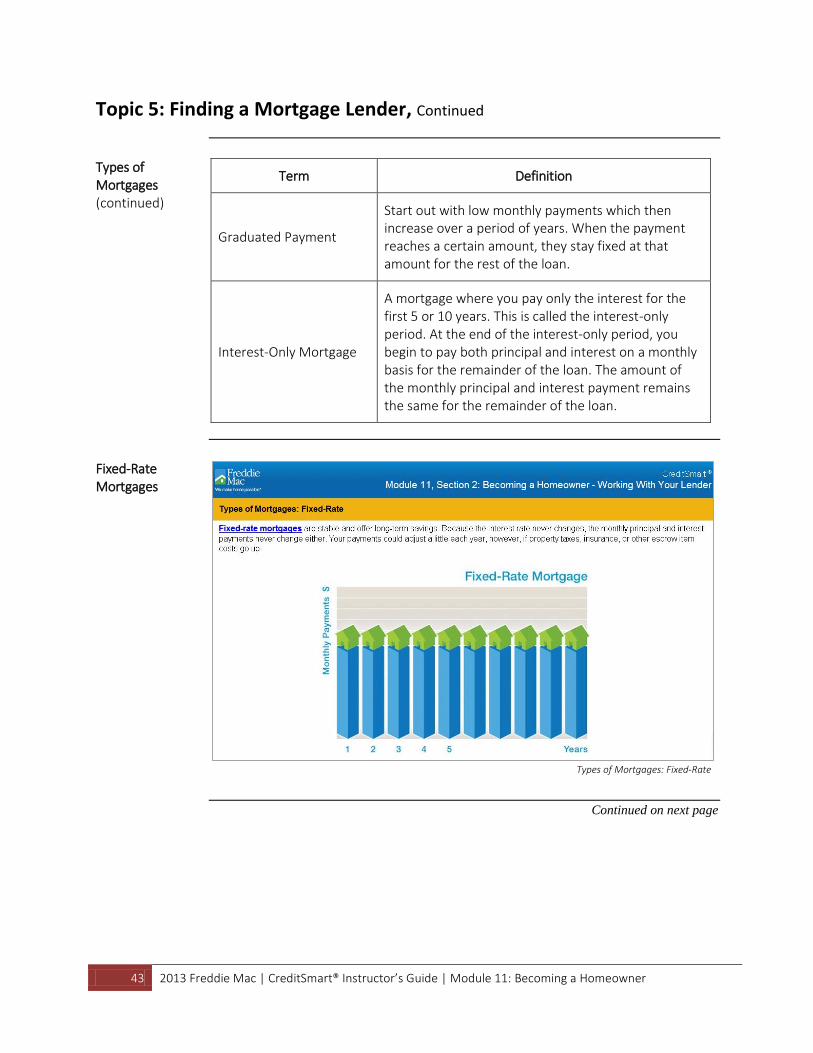

Graduated Payment

Start out with low monthly payments which then increase over a period of years. When the payment reaches a certain amount, they stay fixed at that amount for the rest of the loan.

Interest-Only Mortgage

A mortgage where you pay only the interest for the first 5 or 10 years. This is called the interest-only period. At the end of the interest-only period, you begin to pay both principal and interest on a monthly basis for the remainder of the loan. The amount of the monthly principal and interest payment remains the same for the remainder of the loan.

Fixed-Rate Mortgages

Types of Mortgages: Fixed-Rate

Continued on next page

44 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Fixed-Rate Mortgages (continued)

Instructor note:

Define the following term:

Term Definition

Fixed-Rate Mortgage A mortgage with an interest rate that does not change during the entire term of the loan.

Adjustable-Rate Mortgage

Types of Mortgages: Adjustable-Rate

Continued on next page

45 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Adjustable-Rate Mortgage (continued)

Instructor note:

Define the following term:

Term Definition

Adjustable-Rate Mortgage

Also known as a variable-rate loan, ARMs usually offer a lower initial rate than fixed-rate loans. The interest rate can change at specified time periods based on changes in an interest rate index that reflects current finance market conditions, such as the LIBOR index or the Treasury index.

The ARM promissory note states maximum and minimum rates. When the interest rate on an ARM increases, the monthly payments will increase and when the interest rate on an ARM decreases, the monthly payments will be lower.

Types of Mortgages: Adjustable-Rate (cont.)

46 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Mortgage Shopping Tips

Mortgage Shopping Tips

Instructor note:

Define the following terms:

Term Definition

Terms The provisions, conditions, and requirements pertaining to the loan as stated in the loan agreement.

Annual Percentage Rate (APR)

The APR (annual percentage rate) is the cost of credit expressed at a yearly rate which includes the interest and certain fees that a borrower is required to pay for a loan. The APR tells the annual cost of borrowing money based on the loan amount, interest rate, added fees, and term; thus, it may be higher than an advertised interest rate.

Continued on next page

47 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Mortgage Shopping Tips (continued)

Mortgage Shopping Tips (cont.)

Affordable, Low Down Payment Mortgages

Affordable, Low Down Payment Mortgages

Continued on next page

48 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Affordable, Low Down Payment Mortgages (continued)

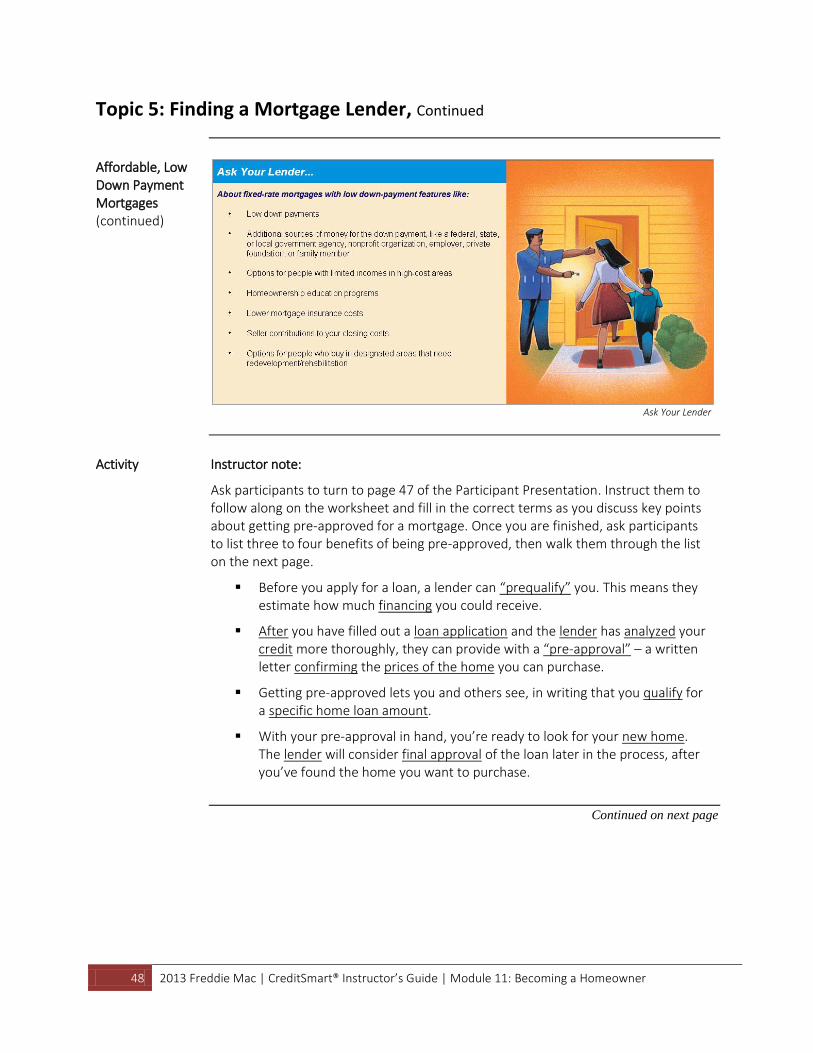

Ask Your Lender

Activity Instructor note:

Ask participants to turn to page 47 of the Participant Presentation. Instruct them to follow along on the worksheet and fill in the correct terms as you discuss key points about getting pre-approved for a mortgage. Once you are finished, ask participants to list three to four benefits of being pre-approved, then walk them through the list on the next page.

Before you apply for a loan, a lender can “prequalify” you. This means they estimate how much financing you could receive.

After you have filled out a loan application and the lender has analyzed your credit more thoroughly, they can provide with a “pre-approval” – a written letter confirming the prices of the home you can purchase.

Getting pre-approved lets you and others see, in writing that you qualify for a specific home loan amount.

With your pre-approval in hand, you’re ready to look for your new home. The lender will consider final approval of the loan later in the process, after you’ve found the home you want to purchase.

Continued on next page

49 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 5: Finding a Mortgage Lender, Continued

Activity (continued)

Instructor note:

Ask your participants to list three to four benefits of being pre-approved. After they have come up with their list, review the following benefits below:

You’ll discover how much you can confidently offer when you find the right home.

Pre-approval could open doors to homes and neighborhoods you didn’t realize you could afford.

Getting pre-approved will save you time and effort by eliminating properties beyond your price range.

Find out if you have any credit issues and clear up any problems before you get started.

Learn your best financing options from a professional mortgage banker.

Pre-approval can help you win a bidding war against others who may not qualify.

You will be considered a more serious homebuyer than someone who is “just looking.”

Source: The Benefits of Mortgage Pre-Approval, JT Realty

50 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 6: Finding a Real Estate Agent

Overview This topic discusses steps to take and questions to ask when looking for a real estate

agent.

Time 10 minutes

Finding a Real Estate Agent

The Basics

A good real estate agent can help you define what you want in a home, search for homes in neighborhoods that meet your needs, and provide you with data on recent home sales in the area.

Real estate agents earn their living matching homebuyers with sellers. They are licensed by the state where they live and have taken classes in subjects such as real estate law and finance.

You’ll want to choose a real estate agent who makes you feel comfortable and can provide knowledge and services you need.

Real estate agents are paid commission by the seller of the house when the sale closes. The buyer does not pay the real estate agent.

Start the Discussion

To start the discussion with your participants, ask some open-ended questions. Here are some examples to get you started:

Do you know any real estate agents? Have you ever talked to them about the home purchase process?

What’s important to you when selecting a real estate agent?

What are some good resources to assist you in finding a real estate agent?

Continued on next page

51 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 6: Finding a Real Estate Agent, Continued

Start the Discussion (continued)

Finding a Real Estate Agent

Finding a Real Estate Agent (cont.)

52 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 6: Finding a Real Estate Agent, Continued

Questions to Ask a Real Estate Agent

Finding a Real Estate Agent (cont.)

For example…

53 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 6: Finding a Real Estate Agent, Continued

Homeownership Education and Credit Counseling

Homeownership Education and Credit Counseling

Homeownership Education

Continued on next page

54 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 6: Finding a Real Estate Agent, Continued

Homeownership Education and Credit Counseling (continued)

Credit Counseling

Homeownership Education and Credit Counseling (cont.)

55 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Topic 6: Finding a Real Estate Agent, Continued

Section Conclusion

Section Conclusion

56 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Module Conclusion

Module Summary

Summarize this module by reviewing the key points below with your participants.

Key points from Module 11: Becoming a Homeowner:

Module11 Summary

57 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Appendix A: Glossary

Term Definition

Adjustable Rate Mortgage (ARM)

Also known as a variable-rate loan, ARMs usually offer a lower initial rate than fixed-rate loans. The interest rate can change at specified time periods based on changes in an interest rate index that reflects current finance market conditions, such as the LIBOR index or the Treasury index. The ARM promissory note states maximum and minimum rates. When the interest rate on an ARM increases, the monthly payments will increase and when the interest rate on an ARM decreases, the monthly payments will be lower.

Amortization Amortization is the term used to describe the gradual reduction of the outstanding balance of the loan as the amount of the loan is gradually paid down over a predetermined period of time at a specific interest rate.

Annual Percentage Rate (APR)

The APR (annual percentage rate) is the cost of credit expressed at a yearly rate which includes the interest and certain fees that a borrower is required to pay for a loan. The APR tells the annual cost of borrowing money based on the loan amount, interest rate, added fees, and term; thus, it may be higher than an advertised interest rate.

Appreciation Appreciation is the term used to describe an increase in the market value of a home due to changing market conditions and/or home improvements.

Balloon Mortgage

A mortgage with monthly payments based on a 30- year amortization schedule and the unpaid principal balance due in a lump sum payment at the end of a specific period (usually 5 or 7 years) earlier than 30 years. The mortgage contains an option to reset the interest rate to the current market rate and to extend the maturity date provided certain conditions are satisfied.

Bank A federally regulated financial institution that offers you a place to keep your money and uses it to make more money. Banks make loans, cash checks, accept deposits, and provide other financial services.

Checking Account

An account that lets you write checks to pay bills or to buy goods. The financial institution takes the money from your account and pays it to the person named on the check. The financial institution sends you a monthly record of the deposits made and the checks written.

58 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Appendix A: Glossary, Continued

Term Definition

Closing Costs

Closing costs are the costs to complete the real estate transaction. These costs are in addition to the price of the home and are paid at closing. They include points, taxes, title insurance, financing costs, items that must be prepaid or escrowed, and other costs. Ask a lender or real estate professional for a complete list of closing cost items.

Credit Union

A federally regulated cooperative financial institution that is owned by the people who use its services. Credit unions serve groups that share something in common, like where they work or go to church. You have to become a member of the credit union to keep your money there.

Default A default is a failure to meet a payment or fulfill a credit obligation.

Down Payment A portion of the price of a home, usually between 5 and 20 percent, not borrowed and paid up front.

Equity Equity is the value in your home above the total amount of the liens against your home. If you owe $100,000 on your house, but it is worth $130,000, you have $30,000 of equity.

Escrow The holding of money or documents by a neutral third party prior to closing. It can also be an account held by the lender (or servicer) into which a homeowner pays money for taxes and insurance.

Fixed-Rate Mortgage A mortgage with an interest rate that does not change during the entire term of the loan.

Foreclosure A legal process in which collateral property is sold in an attempt to satisfy the outstanding debt of a mortgage.

Good Faith Estimate (GFE)

A written statement itemizing the approximate costs and fees for the mortgage.

Graduated Payment Start out with low monthly payments which then increase over a period of years. When the payment reaches a certain amount, they stay fixed at that amount for the rest of the loan.

59 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Appendix A: Glossary, Continued

Term Definition

Homeowner’s Insurance

Homeowner’s insurance is a policy that protects you and the lender from losses resulting from things like fire or flood, which may damage the structure of the house, create liability (such as injury to a visitor to your home), or cause damage to or theft of your personal property (such as to furniture, clothes, or appliances).

Inflation Inflation is an increase in the general level of prices.

Interest Interest is a charge for using someone else's funds. Interest is typically indicated as a percentage of the amount borrowed.

Interest Only Mortgage

A mortgage where you pay only the interest for the first 5 or 10 years. This is called the interest-only period. At the end of the interest-only period, you begin to pay both principal and interest on a monthly basis for the remainder of the loan. The amount of the monthly principal and interest payment remains the same for the remainder of the loan.

Lender Lender is the term used for the person or entity that is providing credit or a loan to a borrower at specific terms and conditions. The term lender can generally be used interchangeably with the term creditor.

Margin The amount (expressed as a percentage) added to the index for an ARM to establish the interest rate on each adjustment date.

Mortgage A mortgage is a document that is signed by a borrower when a home loan is obtained and gives the lender the right to take possession of the property if the borrower fails to make loan payments.

Mortgage Broker An independent finance professional who specializes in bringing together borrowers and lenders to facilitate real estate mortgages.

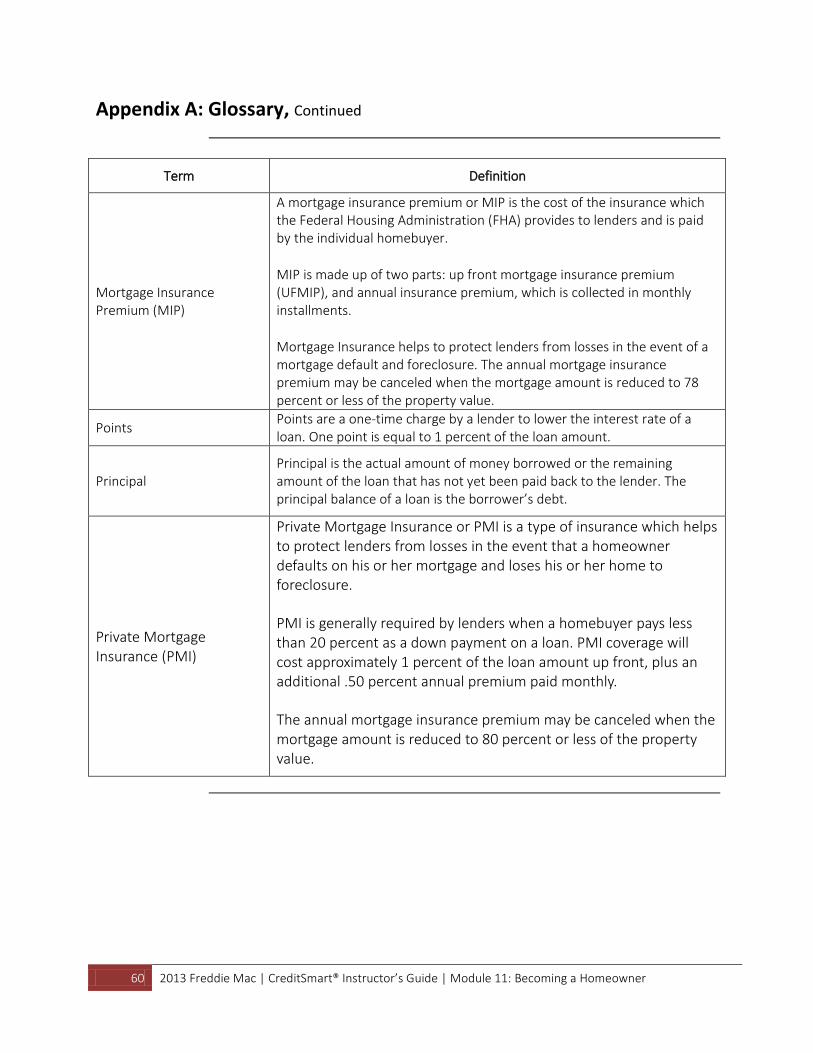

60 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Appendix A: Glossary, Continued

Term Definition

Mortgage Insurance Premium (MIP)

A mortgage insurance premium or MIP is the cost of the insurance which the Federal Housing Administration (FHA) provides to lenders and is paid by the individual homebuyer.

MIP is made up of two parts: up front mortgage insurance premium (UFMIP), and annual insurance premium, which is collected in monthly installments.

Mortgage Insurance helps to protect lenders from losses in the event of a mortgage default and foreclosure. The annual mortgage insurance premium may be canceled when the mortgage amount is reduced to 78 percent or less of the property value.

Points Points are a one-time charge by a lender to lower the interest rate of a loan. One point is equal to 1 percent of the loan amount.

Principal Principal is the actual amount of money borrowed or the remaining amount of the loan that has not yet been paid back to the lender. The principal balance of a loan is the borrower’s debt.

Private Mortgage Insurance (PMI)

Private Mortgage Insurance or PMI is a type of insurance which helps to protect lenders from losses in the event that a homeowner defaults on his or her mortgage and loses his or her home to foreclosure.

PMI is generally required by lenders when a homebuyer pays less than 20 percent as a down payment on a loan. PMI coverage will cost approximately 1 percent of the loan amount up front, plus an additional .50 percent annual premium paid monthly.

The annual mortgage insurance premium may be canceled when the mortgage amount is reduced to 80 percent or less of the property value.

61 2013 Freddie Mac | CreditSmart® Instructor’s Guide | Module 11: Becoming a Homeowner

Appendix A: Glossary, Continued

Term Definition

Real Estate Professional

An individual who provides services in buying and selling homes. The real estate professional is paid a percentage of the home sale price by the seller.

Unless you have signed an agreement with the real estate agent to be a buyer's agent, the real estate professional represents the interest of the property seller.

Real estate professionals may be able to refer you to local lenders or mortgage brokers, but are generally not involved in the lending process.

Savings Account An account where you keep money for safekeeping or as an investment that earns interest.

Spending Plan A spending plan is an itemized list of all of one's expenses. Spending plans are tools commonly used to measure or gauge expenses against income.

Terms The provisions, conditions, and requirements pertaining to the loan as stated in the loan agreement.

Title Insurance Insurance that protects lenders and homeowners against loss of their interest in the property because of legal problems with the title.