become ifrs ready with oracle e-business suite release … · · 2012-03-05become ifrs ready with...

TRANSCRIPT

Become IFRS Ready with Oracle E-Business

Suite Release 12.1

Presented by: Humberto Lopez

What is IFRS

IFRS - International Financial Reporting Standards are a series of accounting

standards developed by the International Accounting Standards Board (IASB),

that is becoming the global standard for the preparation of public company financial

statements.

IFRS focuses on the standardization of financial reporting standards across

international borders. This standardized reporting practice provides a uniform view of

a corporations accounting statements.

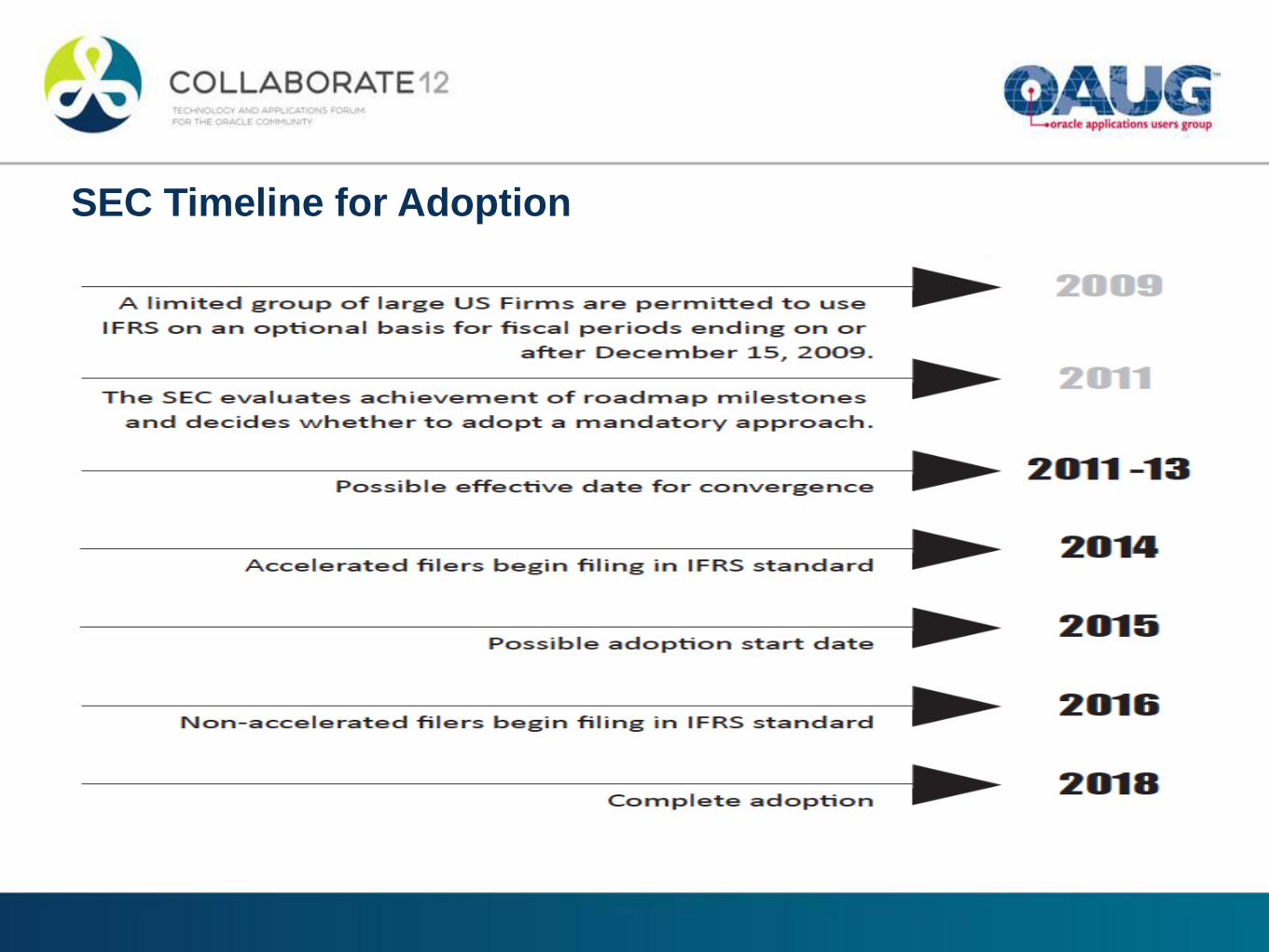

The US Securities and Exchange Commission is weighing a five-year work plan that

would lead to conversion of all US public companies to IFRS. This is in response to

global demand from regulators, investors, businesses and auditors for a single set of

accounting standards.

While support for maintaining US GAAP remains strong in the U.S., it is clear that

multinational corporations or corporations that simply do business internationally will

need to begin preparing for IFRS one way or another.

US GAAP vs. IFRS

SEC Timeline for Adoption

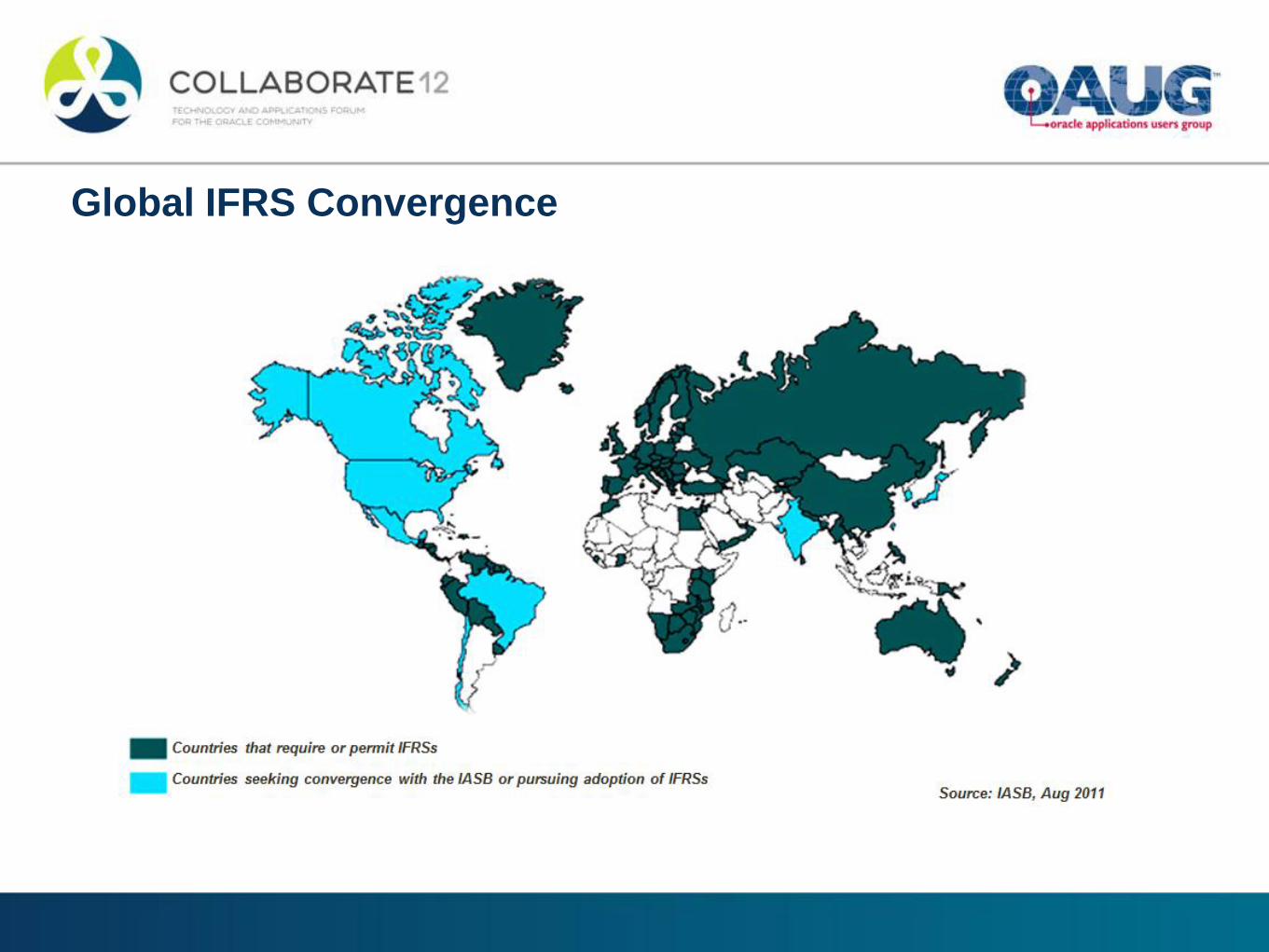

Global IFRS Convergence

There are quite a few similarities between IFRS and US GAAP because the convergence project

between IASB and FASB (the standard setters responsible for IFRS and US GAAP respectively) has

been going on for a while (since 2003 actually).

US GAAP vs. IFRS Similarities

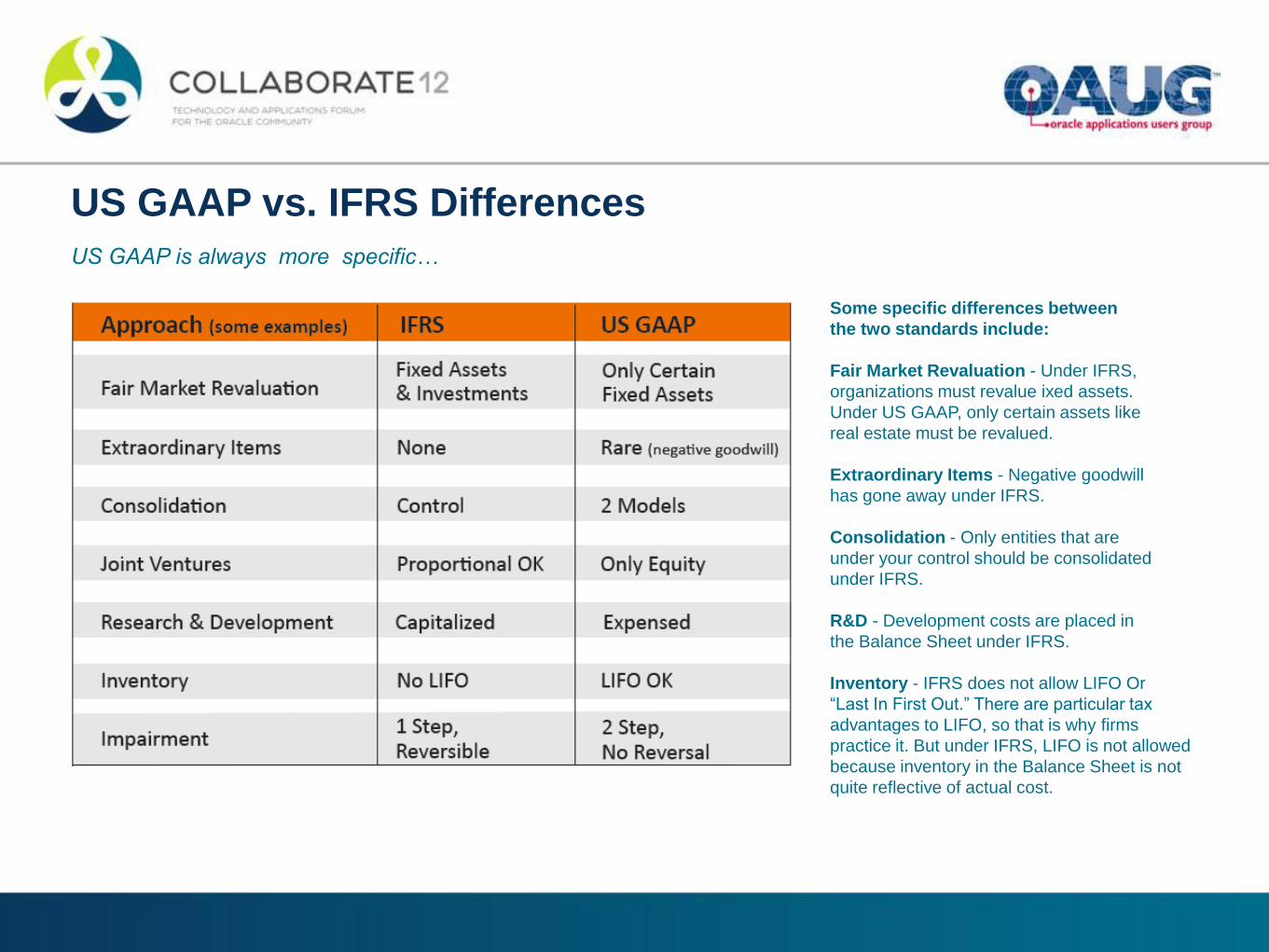

US GAAP is always more specific…

US GAAP vs. IFRS Differences

Some specific differences between

the two standards include:

Fair Market Revaluation - Under IFRS,

organizations must revalue ixed assets.

Under US GAAP, only certain assets like

real estate must be revalued.

Extraordinary Items - Negative goodwill

has gone away under IFRS.

Consolidation - Only entities that are

under your control should be consolidated

under IFRS.

R&D - Development costs are placed in

the Balance Sheet under IFRS.

Inventory - IFRS does not allow LIFO Or

“Last In First Out.” There are particular tax

advantages to LIFO, so that is why firms

practice it. But under IFRS, LIFO is not allowed

because inventory in the Balance Sheet is not

quite reflective of actual cost.

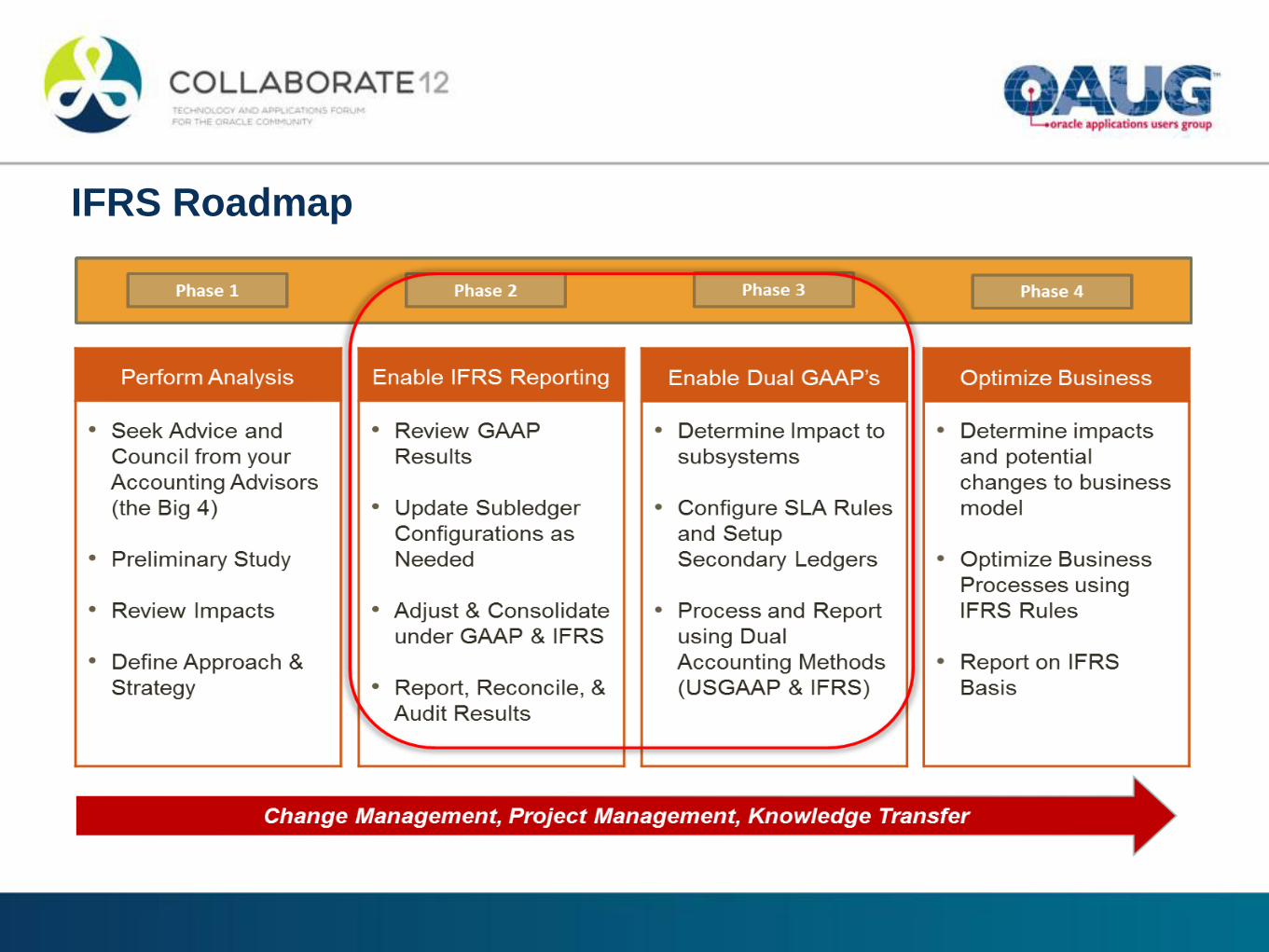

IFRS Roadmap

Which Approach is Right for You?

11i vs. R12 Comparison

Let’s Discuss How to manage Dual GAAP Reporting Using

Release 11i….

R11i: General Ledger - Adjusting Company Method

Reporting on US GAAP and IFRS simultaneously

requires different results to be displayed from the same

accounting base. Using this option, IFRS adjustment

journals are created and posted in a separate adjusting

company or balancing segment that shares the same

chart of accounts, calendar, and currency as the main

operating company.

There exists 11i capability at the subledger level that

can be used to address multi-GAAP reporting

requirements. For example, the requirement for

componentized fixed assets per IFRS can be addressed

by setting up a secondary Fixed Asset Ledger where the

componentized child assets can be separately

depreciated per IFRS, while the parent asset remains in

the primary FA Ledger to be depreciated as usual per

US GAAP rules and regulations.

US GAAP reports are generated in the main operating

company. Oracle’s capability of consolidating multiple

sets of books can be leveraged to obtain IFRS reports

from the consolidated entity as illustrated in the

diagram.

US GAAP Operating Company

AP AR FA

Sub-ledgers

IFRS Adjusting Company

Consolidated Entity

Transactions

IFRS Adjusting J/E’s

US GAAP Reporting

IFRS Reporting

Secondary FA Ledger

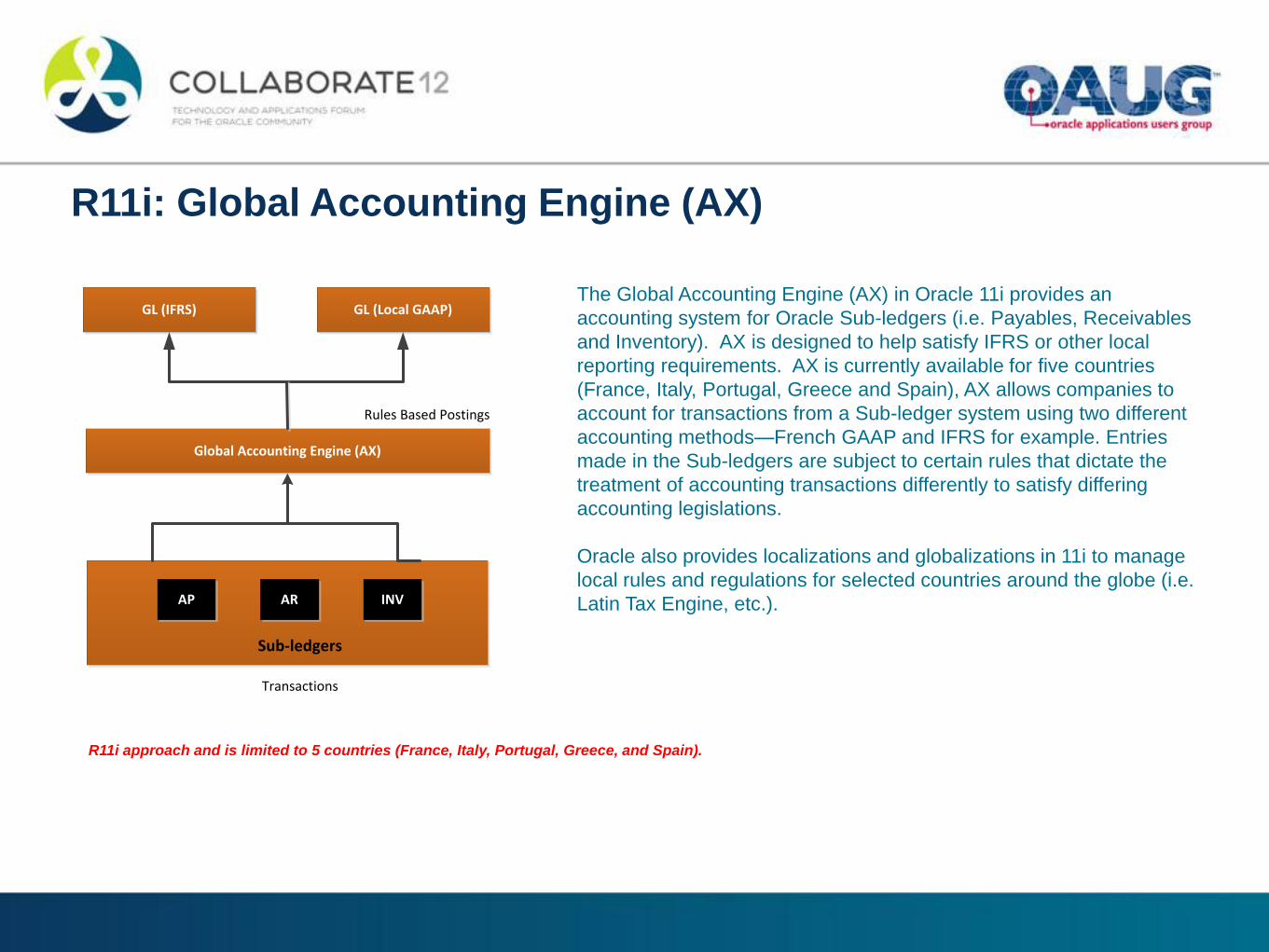

R11i: Global Accounting Engine (AX)

The Global Accounting Engine (AX) in Oracle 11i provides an

accounting system for Oracle Sub-ledgers (i.e. Payables, Receivables

and Inventory). AX is designed to help satisfy IFRS or other local

reporting requirements. AX is currently available for five countries

(France, Italy, Portugal, Greece and Spain), AX allows companies to

account for transactions from a Sub-ledger system using two different

accounting methods—French GAAP and IFRS for example. Entries

made in the Sub-ledgers are subject to certain rules that dictate the

treatment of accounting transactions differently to satisfy differing

accounting legislations.

Oracle also provides localizations and globalizations in 11i to manage

local rules and regulations for selected countries around the globe (i.e.

Latin Tax Engine, etc.).

R11i approach and is limited to 5 countries (France, Italy, Portugal, Greece, and Spain).

GL (IFRS)

AP AR INV

Sub-ledgers

GL (Local GAAP)

Global Accounting Engine (AX)

Transactions

Rules Based Postings

Let’s Discuss How to Enable Dual GAAP Reporting Using

Release 12….

National vs. Parent/Group Compliance

National Parent and Group Resulting Problem

Statutory & Transaction Tax

regulations drive bookkeeping

IAS/IFRS or US GAAP drive

balance definition & disclosure

Eg: Billing not equal to Recognizable

Revenue

Invoice & document basis

(Sales Tax & VAT rules)

Reality & Market basis

(Accrual & Mark-to-Market)

Under-accrued,

Under-provided

Arms Length Values

(Landed cost, tax mark-up)

Intercompany Eliminated

(Lower of Cost & Market)

Inventory over-valued,

OOB Intercompany

National and Local

Chart of Accounts

External Reporting & Management

COA

Inconsistent Roll Up

minibus: T&E or HR expense

Local practice forces

classifications

Home country practice

assumes classifications

False mapping:

Exempt=from military service

“Not legal in my country” Simply book the entry… Discrepancies,

reporting errors

Use a Ledger for each LE, or use BSVs?

Limitation

Many LEs use

the same Ledger

Ledger not

owned by a LE

When

Compliance

Single LE uses

one Ledger

• No Legal Entity

Context

in Subledger

Transactions

• AGIS not available

• Not for Legal Entity

Legal Reporting

• Good for Adjustments

• Management

Reporting

• GL-only

implementation

Generally,

One OU per Ledger -

Requirement is:

Preserve LE’s privacy

vis-à-vis VAT auditor

Independent Doc

Sequencing,

VAT Controls,

Statutory COA, etc

Countries that regulate

individual LEs

e.g France, Italy

Many OUs per ledger

if desired:

Requirement is:

No privacy vis-à-vis

State Tax inspectors

No Autonomous Doc

Sequencing and Tax

Per Legal Entity

Countries that regulate

at the Group level

e.g US, Canada

Comment

Maintain Multiple Accounting Representations with

Secondary Ledgers

Source: Oracle Corporation, 2005

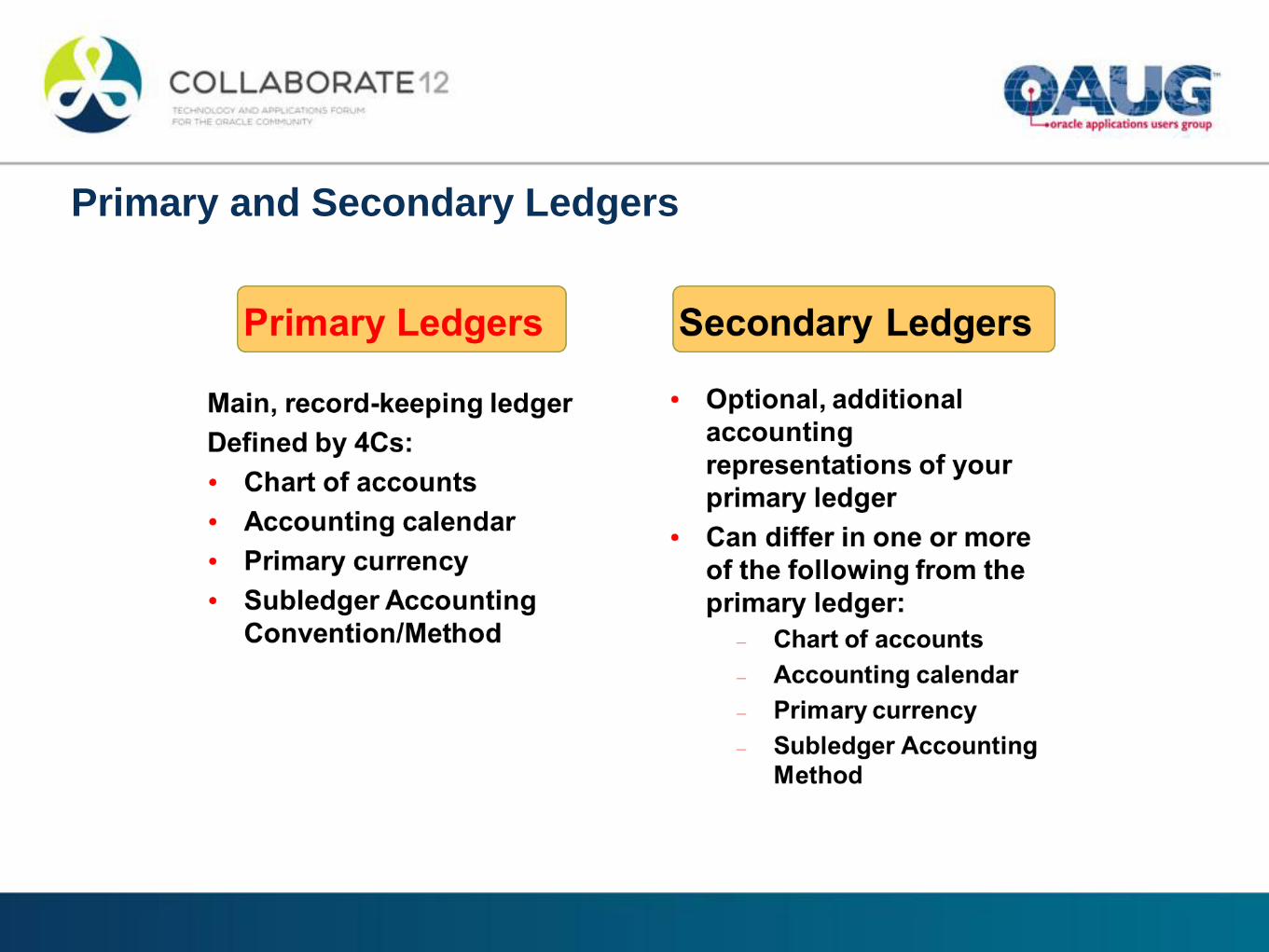

Primary and Secondary Ledgers

Secondary Ledgers

• For global companies that must comply with different countries’ legal requirements

• Useful for supplementary purposes, such as consolidation or management reporting

• Provides a complete accounting picture within itself or a partial picture to be grouped with other ledgers to provide a complete picture

• More Flexibility!

• Represent legal entity(s) accounting information in a different:

• Accounting Method

• Chart of Accounts

• Calendar

• Subledger Accounting Method

• Maintain 4 Different Levels

When to use a Secondary Ledger, an Adjustment Segment,

or an Adjustment Ledger

Adjusting

Segment

Adjusting

Ledger

Secondary

Ledger

Corp. wants GL balances per Parent

GAAP

Corp. wants “Just the adjustments,

thank you”

Corp. wants a complete Parent GAAP

& Currency edition of the Sub’s books

Subsidiary books are pretty similar to

parents

Mapping gets us most of the way to

Parent

Subsidiary books are quite alien to

parents

No inventory Inventory is the big difference Inventory is one of the big differences

National chart of accounts is clearly

related to IAS IFRS or GAAP

balances

Manageable series of

reclassifications

National chart of accounts is radically

different from corporate

National Controllership

- Corp GAAP known

Regional Controllership

- Corp GAAP administered

Parent Controllership

Mexico plant, US parent

Balances are enough

(Full drill down available)

See they’ve been properly adjusted to

our rules Every petty cash slip

Thick or Thin Secondary Ledgers

Source: Oracle Corporation, 2005

Corporate GAAP - IAS/IFRS or National Regulation

Primary?

National ‘GAAP’ Primary,

Corporate ‘GAAP” Secondary

Corporate ‘GAAP’ Primary,

National ‘GAAP’ Secondary

Country regulates intensely Country is easy going

Country regulations differ from US GAAP

or IAS/IFRS

Country regulations similar to US GAAP or

IAS/IFRS

You have lots of in-country transactions

with local companies

Most of your transactions are with HQ or

are exports

You are in a regulated industry with local

oversight

You are in a regulated industry with

corporate oversight

Your national staff don’t know Corporate

culture

Your national staff know what you need

them to do. (Expatriates)

Reporting Currencies vs. Secondary Ledgers - Which to

Use?

Source: Oracle Corporation, 2005

If you use Reporting Currency, you decide on the level of

detail you need

Source: Oracle Corporation, 2005

Four Options to “Consolidate” Information - Why and

When?

Ledger Sets GCS DBI FCH

Objective Manage Ledgers,

Balances

Non-Complex

Consolidation

“Barn door

is open –

close it”

Complex

Consolidation &

analysis

IAS/IFRS &

US GAAP

Use GCS to

eliminate

By Design Daily

Decisions

By Design

Internal control GL Controls, OICM GL Controls,

OICM

OICM on

subledger

Processes

OICM

Integration

Frequency Once Posted Monthly Daily Once Run

Source GL from SLA GL from SLA GL, SLA, Sub

Ledgers

GL from SLA, SAP,

E, etc.

Reporting FSG

send to FCH

FSG

send to FCH

Portal as Delivered EPB + Excel

Interface

R12: Convergence vs. Compliance

The Compliance approach requires the configuration

of accounting rules in SLA to reflect the duality of

accounting treatments for certain classes of

transactions. In this model, US GAAP accounting

would take place in the Primary Ledger and where

IFRS would be generated out of the Secondary Ledger.

With this approach, adjustment entries for IFRS need

not be created separately. SLA allows organizations to

define two sets of business rules for certain

transactions. Thus, at the transaction level, two SLA

records are maintained, thereby minimizing the back-

end work to adjust US GAAP to IFRS and allowing drill-

down to the source of the transaction.

The concept of “Ledger Sets” in R12 enables

transactions to be recorded with dual views, stream-

line month-end processes for Primary and Secondary

Ledgers, and reports to be generated based on dual

accounting treatments for the comparative year(s).

Note, definition of SLA rules are limited to certain classes of transactions. For instance, SLA

cannot be used to generate two sets of inventory cost accounting entries.

R12: Convergence vs. Compliance

The Convergence approach also requires the

configuration of accounting rules in SLA to reflect the

duality of accounting treatments for certain classes of

transactions. In this model, IFRS accounting would

take place in the Primary Ledger and where US GAAP

would be generated out of the Secondary Ledger.

With this approach, adjustment entries for IFRS need

not be created separately. SLA allows organizations to

define two sets of business rules for certain

transactions. Thus, at the transaction level, two SLA

records are maintained, thereby minimizing the back-

end work to adjust US GAAP to IFRS and allowing drill-

down to the source of the transaction.

The concept of “Ledger Sets” in R12 enables

transactions to be recorded with dual views, stream-

line month-end processes for Primary and Secondary

Ledgers, and reports to be generated based on dual

accounting treatments for the comparative year(s).

Note, definition of SLA rules are limited to certain classes of transactions. For instance, SLA

cannot be used to generate two sets of inventory cost accounting entries.

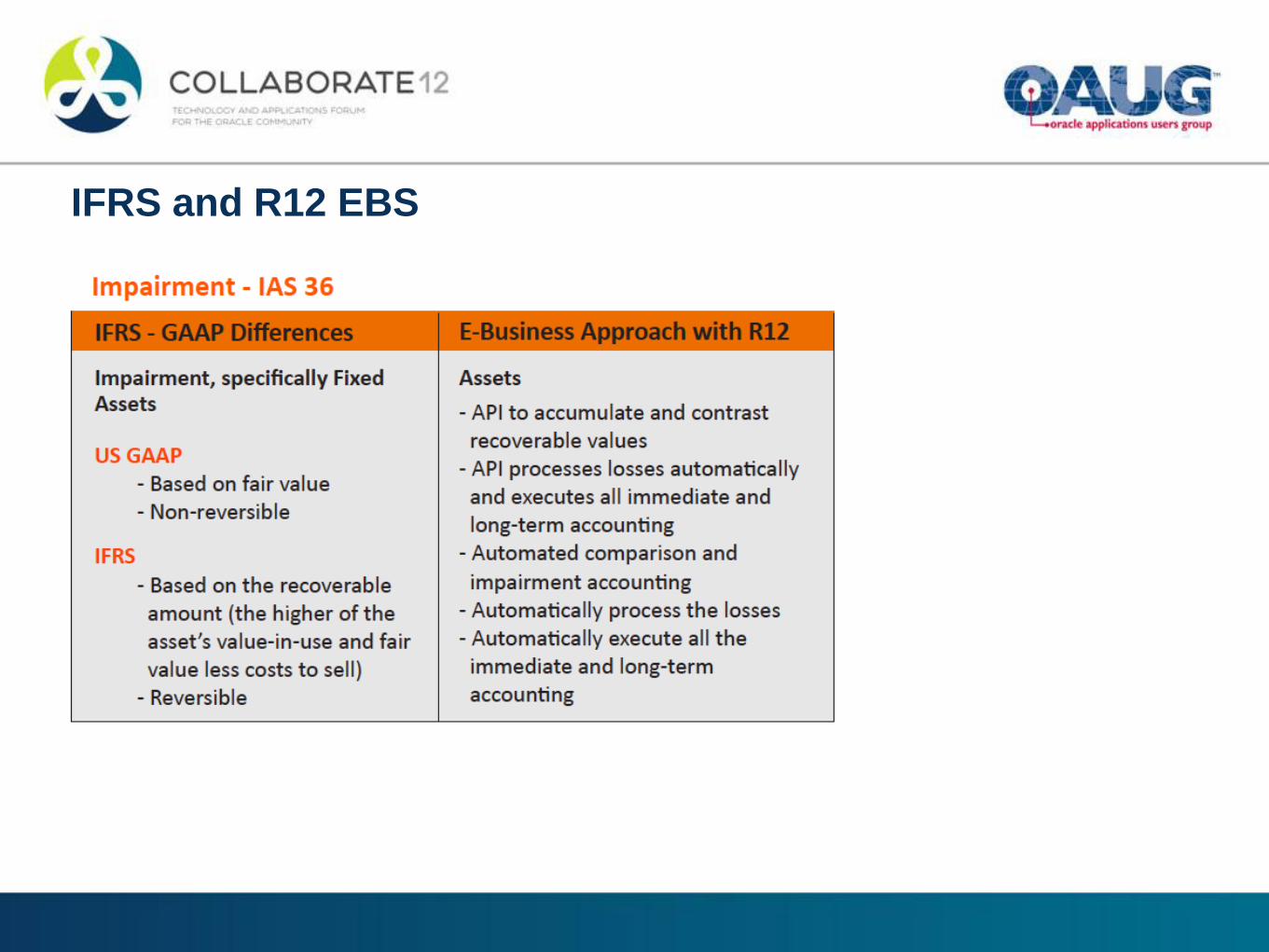

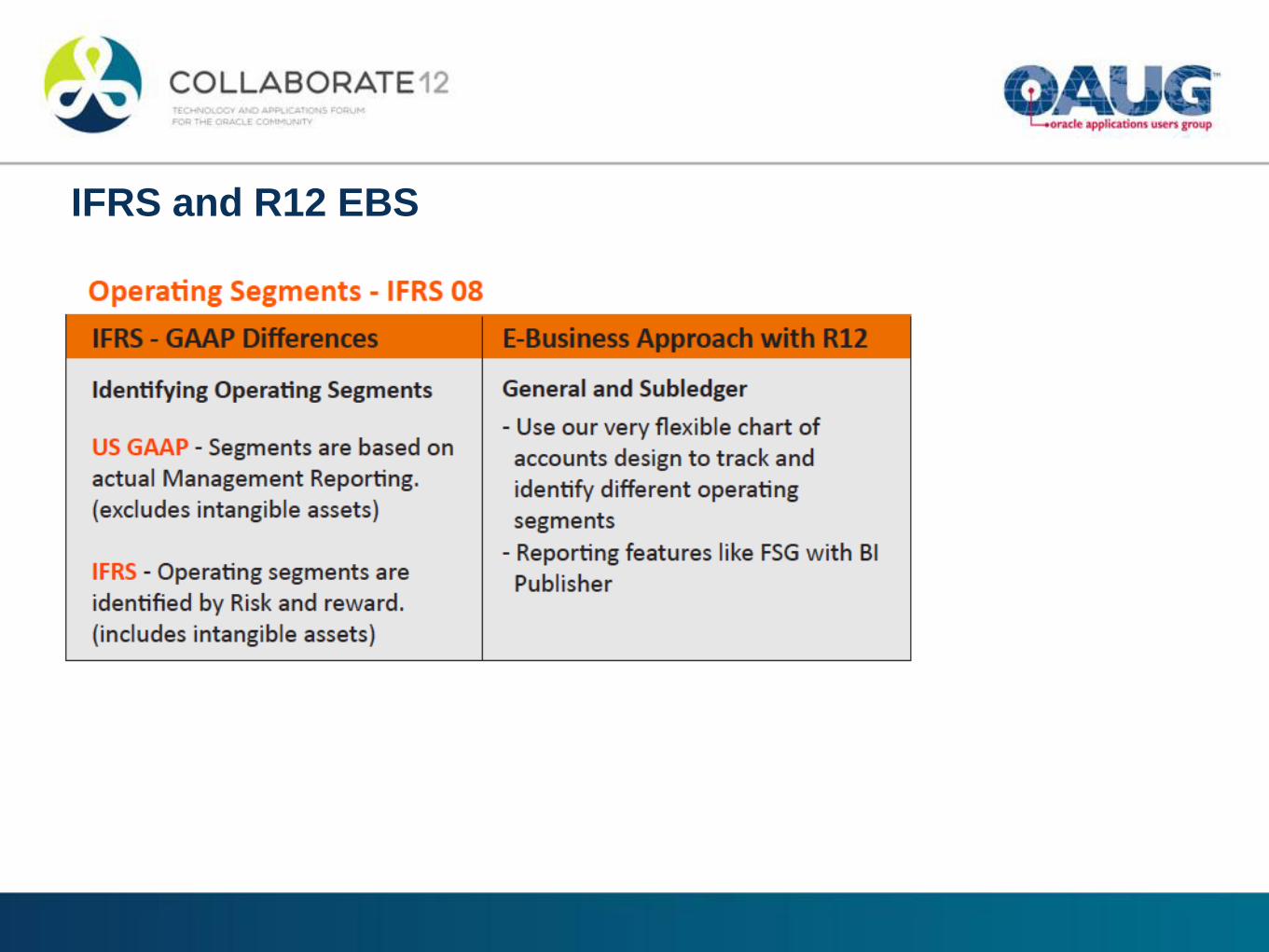

IFRS and R12 EBS

IFRS and R12 EBS

IFRS and R12 EBS

IFRS and R12 EBS

IFRS and R12 EBS

IFRS and R12 EBS

• IFRS will impact many areas of your business

• IFRS conversion will be a multi-year effort

• The need to capture more transactional data at a more granular level

may impact existing chart of account designs

• The conversion effort will be more than an accounting exercise

• Parallel reporting will be required under the current SEC roadmap

• Will require robust change management championed by top company

leadership

Conversion Considerations

• Start Early…

• Leverage Technology (R12 and SLA)…

• Optimize Your Business Model…

Key Takeaways!