basic b volunteer training tax year 2014. federal nonrefundable and refundable credits new: premium...

TRANSCRIPT

Basic B volunteer training

Tax year 2014

• Federal nonrefundable and refundable credits

• NEW: Premium Tax Credit and related credit “reconciliation”

• Exemptions to the ACA insurance coverage requirement

• Other federal taxes and related tax issues

• Financial services at the tax site

BASIC B TRAINING OVERVIEW

Affordable Care Act (ACA) and the 2014 tax return

ACA THE BASICS• The ACA created the Health Insurance Marketplace –

Minnesota has it’s own marketplace, MNsure

• MNsure marketplace is where Minnesotans find information about health insurance options, purchase health insurance and enroll in public health plans

• Taxpayers must report whether he/she (and family) had insurance coverage for the year on their tax return

THE TAX RETURN

• A new tax credit, the Premium Tax Credit (PTC), is available to help eligible taxpayers pay for coverage

• Taxpayers could elect to claim the PTC throughout the year to help pay monthly insurance premiums – Advanced Premium Tax Credit (APTC)

• The ACA also includes the individual shared responsibility provision, which requires individuals to have health insurance coverage for their family

• Form 8962, Premium Tax Credit (PTC), Form 8965, Health Coverage Exemptions, and Form 1095-A, Health Insurance Marketplace Statement

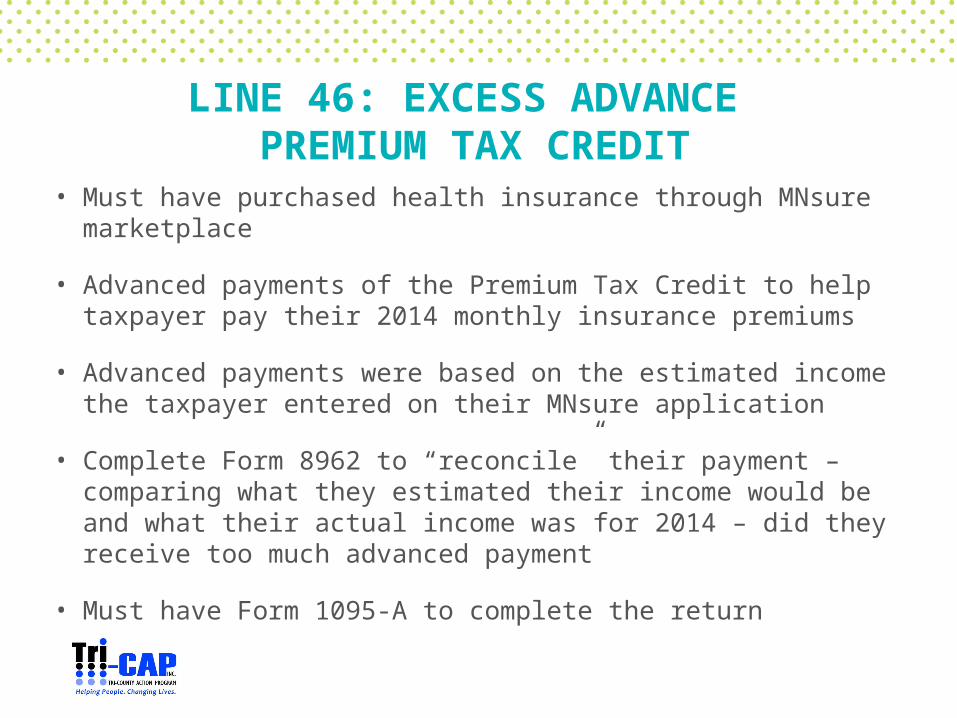

LINE 46: EXCESS ADVANCE PREMIUM TAX CREDIT

• Must have purchased health insurance through MNsure marketplace

• Advanced payments of the Premium Tax Credit to help taxpayer pay their 2014 monthly insurance premiums

• Advanced payments were based on the estimated income the taxpayer entered on their MNsure application

• Complete Form 8962 to “reconcile” their payment – comparing what they estimated their income would be and what their actual income was for 2014 – did they receive too much advanced payment

• Must have Form 1095-A to complete the return

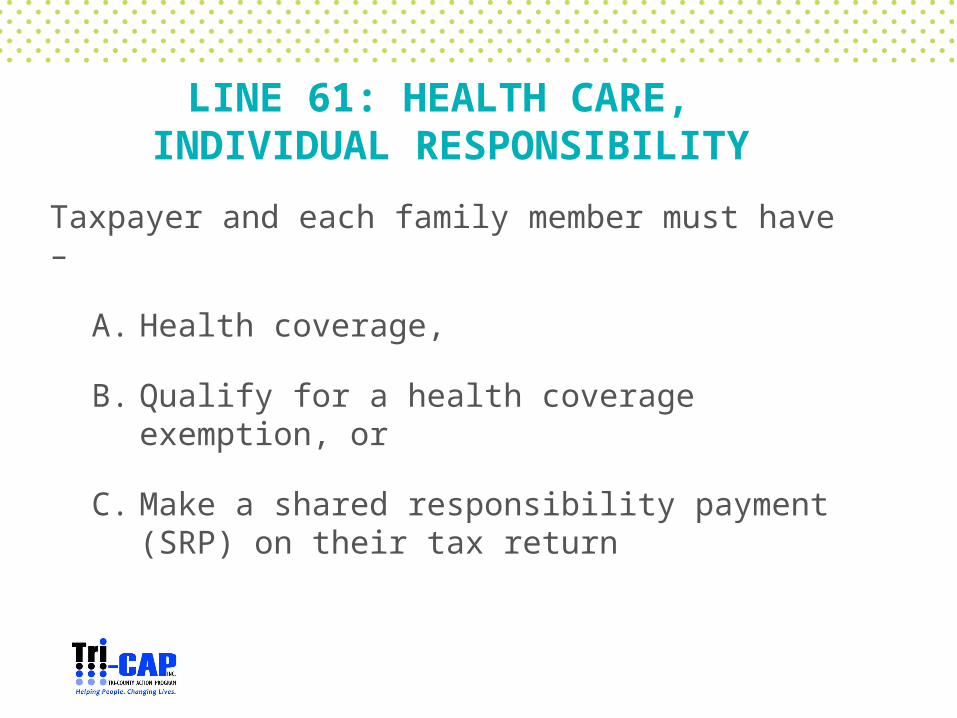

LINE 61: HEALTH CARE, INDIVIDUAL RESPONSIBILITY

Taxpayer and each family member must have –

A. Health coverage,

B. Qualify for a health coverage exemption, or

C. Make a shared responsibility payment (SRP) on their tax return

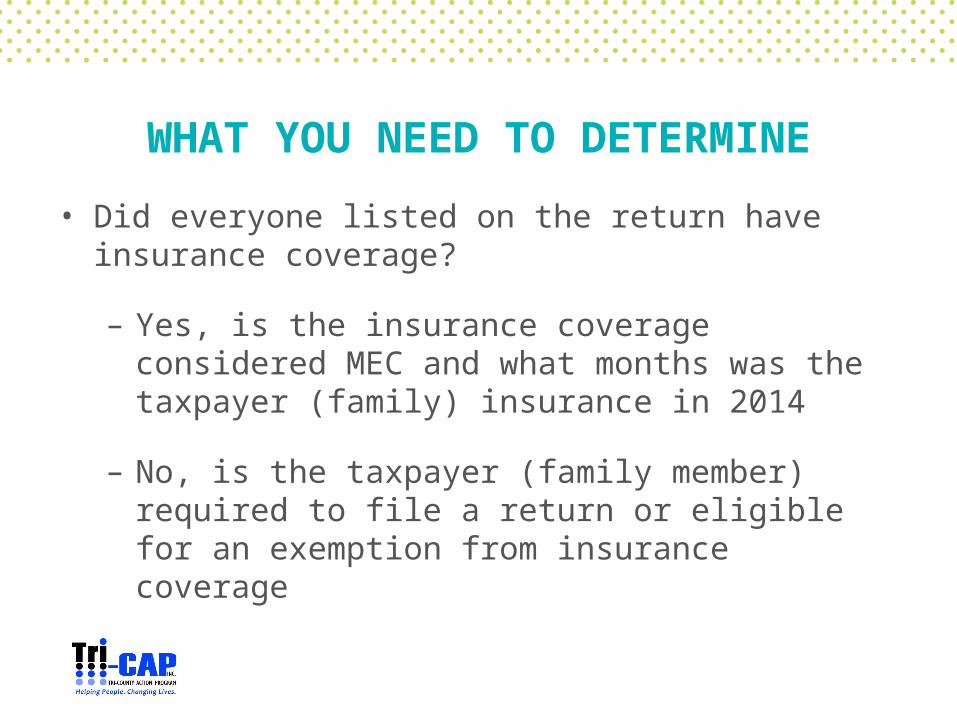

WHAT YOU NEED TO DETERMINE

• Did everyone listed on the return have insurance coverage?

– Yes, is the insurance coverage considered MEC and what months was the taxpayer (family) insurance in 2014

– No, is the taxpayer (family member) required to file a return or eligible for an exemption from insurance coverage

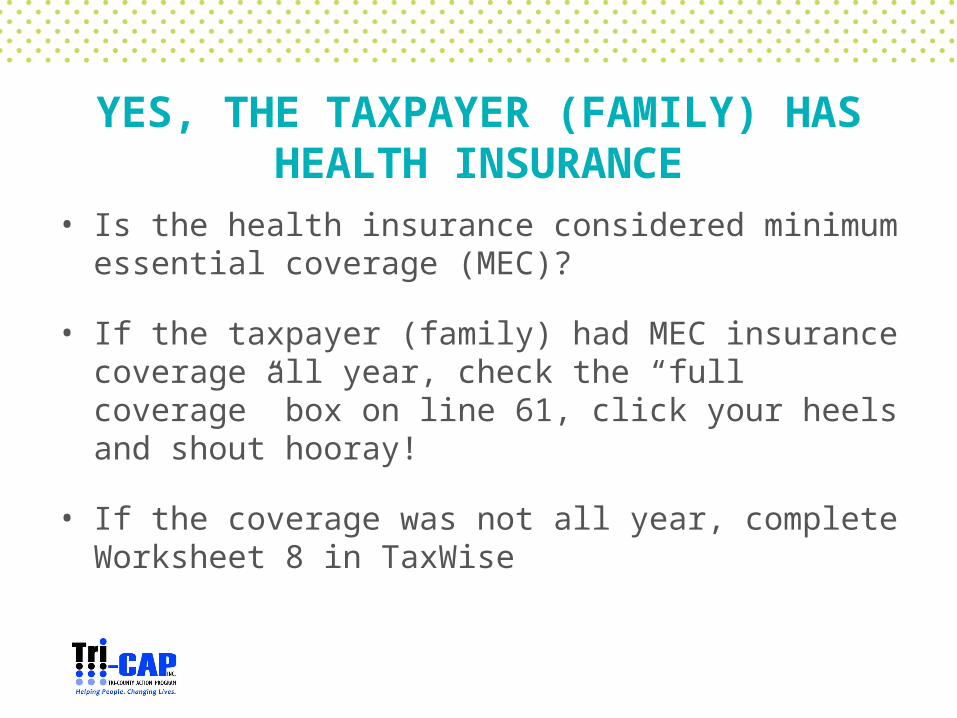

YES, THE TAXPAYER (FAMILY) HAS HEALTH INSURANCE

• Is the health insurance considered minimum essential coverage (MEC)?

• If the taxpayer (family) had MEC insurance coverage all year, check the “full coverage” box on line 61, click your heels and shout hooray!

• If the coverage was not all year, complete Worksheet 8 in TaxWise

NO, THE TAXPAYER (FAMILY) DID NOT HAVE HEALTH INSURANCE

• Check the federal filing requirement threshold to determine whether the taxpayer is required to file a return

• Determine whether the taxpayer (family) may qualify for an exemption from the penalty

MINIMUM ESSENTIAL COVERAGE

• Insurance through employer

• Insurance purchased through private company

• Insurance purchased through MNsure marketplace – must have Form 1095-A to complete the return

• Student health plans

• Government-sponsored

EXEMPTIONS TO THE PENALTY

• Taxpayer (family) may be eligible for more than one exemption

• Find the exemption that is least complicated

• Undocumented taxpayers are exempt from the penalty (exemption code C)

• Some exemptions require approval from the federal marketplace

• Taxpayer can elect to take the penalty without claiming an exemption

LINE 69: NET PREMIUM TAX CREDIT

• Credit based on MAGI and family size

• To be eligible must have purchased insurance through MNsure marketplace

• Must have Form 1095-A from MNsure

• If taxpayer elected to receive the APTC, then the portion used during the year will be deducted from the calculated PTC amount

10 MINUTE BREAK

Topic 7: Nonrefundable Credits

LINE 48: FOREIGN TAX CREDIT

• Enter the amount shown in box 6 of 1099-DIV or 1099-INT directly on line 48

• If required to use Form 1116 then it is out-of-scope

LINE 49: CHILD AND DEPENDENT CARE CREDIT

• Max credit: $3,000 for 1 qualifying person, $6,000 for 2+qualifying persons

• Cannot be married filing separately

• Must have earned income

• Expenses must be paid by the taxpayer to work or look for work

• Form 2441

QUALIFYING PERSON

• Child under age 13 and claimed as an exemption

• Person who is physically/mentally incapable of self-care and couldn’t be claimed as exemption because income was $3,950+

• Spouse who is physically/mentally incapable of self-care

QUALIFYING EXPENSES

• Paid by the taxpayer (spouse) to work or look for work

• Child in nursery school or pre-school for children below level of KG qualify for the credit

• Overnight camp does not qualify

• Day camp may qualify if the camp specializes in a particular activity such as computers or soccer

QUALIFYING PROVIDER• Payments cannot be made to the

taxpayer’s (spouse) dependent

• If payments are made to a taxpayer’s (spouse) child, he/she cannot be a dependent and must be age 19 or older by the end of the year

• If the provider refuses to give EIN/TIN, the taxpayer can still claim the credit, see Pub 17, “provider refusal”

LINE 50: EDUCATION CREDITS

• American opportunity credit, max credit $2,500 per student

• Lifetime learning credit, max credit $2,000 per return

• Cannot use both credits for the same student

• Form 8863

CANNOT CLAIM THE CREDIT

• Claimed as a dependent on another person’s tax return, such as the taxpayer’s parent

• Filing status is married filing separately

• Was a nonresident alien for any part of 2014 (nonresidents are out-of-scope for Tri-CAP)

EDUCATION DOCUMENTATION

• Can be shown on Form 1098-T or annual statement from the institution or receipts for books and equipment

• Reduce expenses by amounts received from scholarships and grants shown in box 5 of Form 1098-T

AMERICAN OPPORTUNITY CREDIT• 40% of the credit may be refundable

• Available for the first 4 years of post secondary education

• Pursuing a degree or recognized educational credential

• Enrolled at least half time

• No felony drug convictions

NOT ELIGIBLE FOR THE REFUNDABLE AMERICAN OPPORTUNITY CREDIT

1. Taxpayer is (a) under age 18; or (b) age 18 and their earned income was less than ½ of their support; or (c) FT student over age 18 and under 24 and earned income was less than ½ of their support; AND

2. At least one of his/her parents was alive at the end of the year; AND

3. Taxpayer is not filing a joint return

LIFETIME LEARNING CREDIT

• Nonrefundable

• Available for an unlimited number of years

• Do not to be pursuing a degree

• Can take one or more courses

• Felony drug convictions are permitted

EXPENSES• Qualifies: tuition, required enrollment fees and

course-related materials such as books, supplies and equipment

• American opportunity credit: books, supplies and equipment do not have to be purchased from the school

• Lifetime learning credit: books, supplies and equipment must be purchased from the school

• Does not qualify: computer tech fees, student activity or athletic fees, insurance, room and board, transportation

CALCULATING EXPENSES

Scenario 1

Tuition $12,500

Course-related materials $650

Scholarships and Grants ($5,000)

Eligible expenses for credit $8,150

LINE 51: RETIREMENT SAVINGS CREDIT

• Taxpayers qualify if they made contributions to an eligible plan

• Contributions to employer-sponsored plan are shown in box 12, Form W-2

• Contributions to a traditional IRA or Roth IRA

• Must be age 18 or older and cannot be a FT student

• Form 8880

LINE 52: CHILD TAX CREDIT

• Nonrefundable credit up to $1,000 per child

• Taxpayers not claiming the full amount may be eligible for the refundable Additional Child Tax Credit

• Must have a Qualifying Child, determined by info entered on TaxWise Main Information Sheet

• Form 8812

LINE 53: RESIDENTIAL ENERGY CREDITS

• Expired provision

Topic 8: Other taxes

• Line 57: self-employment tax

• Line 59: additional tax on IRAs, other qualified retirement plans – early distributions subject to 10% penalty

• Line 60b: 1st time homebuyer credit repayment

• Line 61: health care, individual responsibility

10 MINUTE BREAK