basel iii pillar 3 disclosure year 2017 - voban.co.rs · basel iii pillar 3 disclosure 1 the nbs...

TRANSCRIPT

Basel III Pillar 3 Disclosure

BOARD OF DIRECTORS Number: 1.0-17742/8 Date: 30.05.2018.

Basel III Pillar 3 Disclosure

Year 2017

Basel III Pillar 3 Disclosure

Contents 1. General information .................................................................................................................................. 1

1.1. Basic information about the Vojvođanska banka a.d. Novi Sad ................................................... 1

2. Introduction ............................................................................................................................................... 2

2.1 Pillar 1 ............................................................................................................................................ 2

2.2 Pillar 2 ............................................................................................................................................ 3

2.3 Pillar 3 ............................................................................................................................................ 3

3. Overall risk and capital management ........................................................................................................ 4

3.1 Risk management strategy ............................................................................................................ 4

3.2 Risk management framework ....................................................................................................... 8

3.3 Risk governance structure ............................................................................................................. 9

3.4 Capital management ..................................................................................................................... 9

3.5 Risk types ..................................................................................................................................... 10

3.6 Monitoring and reporting ............................................................................................................ 10

4. Capital adequacy and ICAAP .................................................................................................................... 12

4.1 Capital adequacy ......................................................................................................................... 12

4.2 ICAAP considerations................................................................................................................... 12

5. Capital buffers ......................................................................................................................................... 16

6. Leverage ratio .......................................................................................................................................... 16

7. Credit risk ................................................................................................................................................. 17

7.1 Introduction ................................................................................................................................. 17

7.2 Credit risk management .............................................................................................................. 18

7.3 Capital requirement for credit risk .............................................................................................. 19

7.4 Quantitative information on the credit risk ................................................................................ 21

7.4.1 Gross and net credit exposure towards to asset classes .......................................................... 21

7.4.2 Credit exposure by geography/region ...................................................................................... 25

7.4.3 Credit exposure by sectors ........................................................................................................ 25

7.4.4 Credit exposure by maturity ..................................................................................................... 29

7.4.5 Distribution of exposures according to classification category, by types of counterparty, as

well as calculated scecific and needed reserves ................................................................................ 29

7.5 Exposures in default and impaired exposures ............................................................................ 32

7.6 Credit risk mitigation ................................................................................................................... 36

7.7 Related party and intra-group transactions ................................................................................ 37

Basel III Pillar 3 Disclosure

7.8 Equity investments held in banking book ................................................................................... 37

8. Market risk ............................................................................................................................................... 39

8.1 Introduction ................................................................................................................................. 39

8.2 Foreign exchange risk management ........................................................................................... 39

8.3 Commodity risk management ..................................................................................................... 40

8.4 CVArisk management .................................................................................................................. 40

8.5 Position risk of debt and equity instruments .............................................................................. 41

8.6 Capital requirement for market risk ............................................................................................ 41

9. Operational risks ...................................................................................................................................... 42

9.1 Introduction ................................................................................................................................. 42

9.2 Operational risk management ..................................................................................................... 43

9.3. Capital requirements for operational risk .................................................................................. 44

10. Exposures in the form of securitisation positions ................................................................................. 44

11. Other types of risk ................................................................................................................................. 45

11.1 Introduction ............................................................................................................................... 45

11.2 Liquidity risk............................................................................................................................... 45

11.3 Interest rate risk in the banking book ....................................................................................... 47

11.4 Concentration risk ..................................................................................................................... 48

11.5 Counterparty risk ....................................................................................................................... 48

11.6 Reputational risk........................................................................................................................ 49

11.7 Other risks ................................................................................................................................. 49

12. Appendix

Appendix 1: PI-KAP- Data on bank’s capital position

Appendix 2: PI-FIKAP - Data on main features of financial instruments included in calculation of bank’s

capital

Appendix 3: PI-UPK - Data on matching capital positions from the balance sheet with items from the PI-

KAP form

Appendix 4: PI-AKB - Data on total capital requirements and capital adequacy ratio

Appendix 5: PI-GR - Geographical Distribution of Exposures Relevant for the Calculation of the

Countercyclical Capital Buffer

Appendix 6: PI-KZS -Amount of Bank-Specific Countercyclical Capital Buffer

Basel III Pillar 3 Disclosure

1

The NBS regulations, by which Basel III standards are implemented, became effective on 30th June, 2017. Announcements incorporated in this Report have been prepared in accordance with the NBS requirements outlined in the Decision on disclosure of data and information by bank (RS Official Gazette 103/2016). This Basel III Pillar 3 Disclosure Report contains a description of the Bank’s risk management and capital adequacy practices and processes. The Disclosures in this Report are in addition to or in some cases, serve to clarify the disclosures set out in the Notes to the Financial Statements for the year ended 31 December 2017, presented in accordance with the NBS regulations, Financial Accounting Standards (FAS) and International Financial Reporting Standards (IFRS).

1. General information

1.1. Basic information about the Vojvođanska banka a.d. Novi Sad

Vojvođanska banka a.d. Novi Sad (hereinafter the “Bank”) was established on 31 December 1989. by the transformation of Vojvođanska banka – Udruzena banka (Associated Bank), Novi Sad. In 1995 the Bank changed its legal form into a joint stock company and became Vojvođanska banka a.d. Novi Sad. On 30 December 2001, in accordance with its Articles of Incorporation and the Decision of the Bank’s General Assembly, the Bank merged with Srpska razvojna banka a.d. Belgrade and Uzicka banka a.d. Uzice. In December 2006, in accordance with the terms of the Agreement on the Purchase and Sale of Share Capital, the National Bank of Greece, Athens became the major owner of the Bank by acquiring an equity interest of 99.43%. The aforementioned acquisition was duly registered with the Central Securities Depository and Clearing House on 12 December 2006. On 25 October 2007 the National Bank of Greece, Athens, conducted the mandatory purchase of the remaining 1,727 shares and became the sole owner of the Bank. On 7 December 2007, the Bank was excluded from the Belex list at its own request. The Bank is registered in the Republic of Serbia as a joint stock company for provision of banking services associated with payment transfers, credit and deposit activities in the country and abroad, and it operates in accordance with the Republic of Serbia’s Law on Banks. In accordance with the Decision brought by the Bank’s Assembly on 3 January 2008, the Bank merged with the National Bank of Greece a.d. Belgrade. The aforementioned status change of merger by absorption of the National Bank of Greece a.d. Belgrade was registered in the Serbian Business Registers Agency on 14 February 2008 under the number BD 6190/2008 (removal of the business entity – the National Bank of Greece a.d. Belgrade as the acquired bank), as well as the change in equity structure of the Bank (Decision number BD 6210/2008). The National Bank of Greece a.d. Belgrade was entirely owned by the National Bank of Greece, Athens and continued its operations under the name of Vojvođanska banka a.d. Novi Sad. As of 01 December 2017, OTP Bank Serbia a.d Novi Sad became 100% owner of Vojvođanska banka a.d Novi Sad. From 01 December Bank is member of OTP Group.

Basel III Pillar 3 Disclosure

2

The Bank’s Head Office is located in Novi Sad, 7, Trg Slobode. As of 31 December 2017, the Bank operated through its Head Office located in Novi Sad and 105 branches (31 December 2016: 106 branches). As of 31 December 2017, the Bank had 1,473 employees (31 December 2016: 1,468 employees). The Bank’s registration number is 08074313. Its tax identification number is 101694252. As of 31 December 2017, the Board of Directors consisted of the following members: - Gábor Kolics Director of Acquisitions and Coordination Department OTP Group - Imre Bertalan Managing Director of Human Resources Management Directorate of OTP Bank - Ferenc Böle IT Project management, IT subsidiary management and IT Architecture of OTP - Peter Bese Head of International Retail banking of OTP - Darko Spasic Lawyer, one of the owners of “Spasic i partneri” o.d. - Milan Parivodic Lawyer, “Foreign Investors Services” d.o.o. The Board of Directors’ members are elected by the General Assembly, in accordance with valid Statute of limitations. Members are elected for the period of 3 years with the re-election option.

2. Introduction The Basel framework provides a more risk sensitive approach to assessment of risk and the calculation of regulatory capital. The Basel framework intends to strengthen the risk and capital management practices and processes within financial institutions. Given the NBS’s requirements the Bank has accordingly taken steps to comply with these requirements. The NBS’s risk and capital management framework, consistent with the Basel III framework, is built on three pillars: • Pillar 1: Calculation of the regulatory capital, risk weighted assets, capital requirements and capital adequacy ratio. • Pillar 2: The supervisory review process, including the Internal Capital Adequacy Assessment Process. • Pillar 3: Rules for the disclosure of risks management and capital adequacy data and information.

2.1 Pillar 1

Basel III Pillar 1 prescribes the basis for the calculation of the regulatory capital adequacy ratio. Pillar 1 defines the regulatory minimum capital requirements for each bank to cover the credit risk, market risk, operational risk and CVA risk. It also defines the methodology for measurement of these risks and the various elements of qualifying capital. Under Basel III standards, a bank shall calculate the following ratios:

- Common Equity Tier 1 capital ratio of the Bank is a ratio between the Bank’s Common Equity Tier 1 capital and Bank’s risk weighted assets.

- Tier 1 capital ratio of the Bank is a ratio between the Bank’s Tier 1 capital and Bank’s risk weighted assets.

- Capital adequacy ratio of the Bank is a ratio between the Bank’s capital and Bank’s risk weighted assets

Basel III Pillar 3 Disclosure

3

The table below summarizes the Pillar 1 risks and the approaches used by the Bank to calculating the RWAs in accordance with the NBS’s Basel III capital adequacy framework.

RISK TYPE APPROACH USED BY THE BANK

Credit risk Standardized Approach

Market Risk Standardized Approach

Operational Risk Basic Indicator Approach

CVA risk Standardized Approach

2.2 Pillar 2

Basel III Pillar 2 deals with the Supervisory Review and Evaluation Process (SREP). It also addresses the Internal Capital Adequacy Assessment Process (ICAAP) to be followed by banks to assess the overall capital requirements to cover all relevant risks (including those uncovered under Pillar 1). Under the NBS’s rules and Pillar 2 guidelines, each bank is to be individually assessed by the NBS and an individual minimum capital adequacy ratio could be prescribed as higher if the NBS assesses it is necessarily and is in interest of bank. The ICAAP incorporates a review and evaluation of risk management and capital relative to the risks to which the bank is exposed. The Bank has developed an ICAAP process which involves identification and measurement of risks to maintain an appropriate level of internal capital in alignment to the Bank’s overall risk profile and business plan. An ICAAP Policy has been developed to address major components of the Bank’s risk management, including risk types which are not covered under Pillar 1 and they are liquidity risk, credit fx risk, interest rate risk in the banking book, concentration risk, reputational risk and other risks.

2.3 Pillar 3

In the NBS’s Basel III framework, the Pillar 3 prescribes how, when, and at what level of data and information should be publicly disclosed about an institution’s risk management, governance and capital adequacy practices. The disclosures comprise detailed qualitative and quantitative information. The purpose of the Pillar 3 disclosure requirements is to complement the first two Pillars and the associated supervisory review process. The disclosures are designed to enable stakeholders and market participants to assess an institution’s risk appetite and risk exposures and to encourage all banks, via market pressures, to move towards more advanced forms of risk management. In accordance with NBS’s regulation, the Bank ordinarily annually and semi annually disclosed data and information about risk and capital management.

Basel III Pillar 3 Disclosure

4

3. Overall risk and capital management

3.1 Risk management strategy

The Bank perceives strong risk management capacities to be the strong foundation in delivering business results to customers, investors and OTP Group. In accordance with this, the Bank endeavors to develop the best international practices of risk management trying to provide the highest level of market discipline. Risk management and permanent control are an integral part of the Bank’s commitment to providing continuous returns to its shareholders. The delivery of superior shareholder returns depends on achieving the appropriate balance between risk and return, both in day-to-day business and in strategic management of the balance sheet and capital. To this effect, , the Bank has developed its own overall strategic direction, addressing the core issues regarding its fundamental attitude towards risk and risk management, driven by current balance sheet, business objectives and targeting shareholder value creation. The result of this process is the Bank’s Risk Strategy which lay the foundation on which the Bank builds

its risk culture, risk appetite, terminology, policies and procedures and constitutes its view on managing

the Bank’s risks, taking into account the local regulatory requirements and the international best

practices.

The purpose of the Risk Strategy is to describe Bank’s fundamental attitude towards risk as described by

risk principles and objectives, as well as the Bank’s risk appetite and risk tolerance, risk governance and

organization and key risk management capabilities. In particular, this document describes:

The Bank’s risk management mission and objectives

Definitions of risk types undertaken by the Bank

Guiding risk management principles

Definition of the Bank’s risk tolerance and appetite

The Bank’s risk management governance structure

Key Risk management capability goals

The overall objectives of the Bank’s Risk Management are to:

Establish a set of fundamental standards for risk management across the Bank in order to maximize earnings potential and exploit opportunities leading to shareholder value creation.

Support Bank’s business strategy by ensuring that business objectives are pursued in a risk-controlled manner in order to preserve earnings stability by protecting against unforeseen losses.

Improve the use and allocation of capital and enhance risk adjusted return on capital by incorporating risk into business performance measures.

Support decision making processes by providing the necessary risk related perspective.

Ensure consistency with best practices and compliance with local regulatory, quantitative and qualitative requirements.

Basel III Pillar 3 Disclosure

5

Ensure the cost-effectiveness of risk management by reducing overlaps and avoiding inappropriate, excessive or obsolete policies, processes, methodologies, models, controls and systems.

This document shall form the basis for the development of risk management policies, procedures,

guidelines and manuals for a particylar risk type.

Credit risk policies The Credit Policy regarding the Corporate Portfolio aims to provide the Bank’s personnel engaged in loan granting with the fundamental guidelines for the managing (identification, measurement, approval, monitoring and reporting) of the credit risk related to the Corporate Portfolio. The Credit Policy has been designed to meet the organizational requirements and the regulatory frameworks in the best possible way, as well as to allow the Bank to maintain and enhance its leading position in the market in align with adequate credit risk management. The Credit Policy has been approved and can be amended or revised by the Board of Directors and it is subject of periodical revision. This Board ratifies all exceptions from the Credit Policy initially approved by the Chief Credit Officer. All exceptions (and the rationale for each exception) should be recorded and have either an expiry date or a review date. Retail Banking Credit Policy and Small Business Banking Credit Policy sets the policies & risk acceptance criteria, which determine the framework for managing and minimizing the credit risks undertaken by the Retail Banking Products and Segments Division. Its main scope is to enhance, guide and regulate the effective and adequate management of retail and small business credit risk, thus achieving a viable balance between risk and reward. Both policies are orientated to serve three basic objectives: 1. Set the framework for the establishment of the basic credit criteria, instructions and procedures, 2. Assures compliance with regulatory and Group policy and 3. Establish a common approach for managing Retail Credit risks and Small Business Credit risks. Trading book policy The trading book Policy is related to market risks. Market risks arise from adverse effects on the financial result and equity on the valuation of balance sheet items and off-balance sheet items of the Bank arising from movements in market prices. Market risks include currency risk, price risk on debt securities and equity securities and commodity risk.

The Bank has no significant exposure to these risks, where there is a constant striving for their reduction to a minimum. Limits setting for market risks aims to risk managing, i.e. minimize risks that can have a negative impact on the operating results of the Bank.

In addition to the nominal limit for open positions, limits related to the indicators, the Bank has established VaR limits on open positions in major currencies. In the market risk management Department the Bank has established a number of different limits for transactions agreed on market, where internal limits are stricter than all the limits prescribed by the National Bank of Serbia.

The Bank is continuously synchronized its assets and liabilities per currency. Monitoring of currency positions in each currency is done in order to have consistent position with the pre-established limits by currency and the total allowed open position of the Bank.

Basel III Pillar 3 Disclosure

6

Trading book policy defines the criteria for the allocation of balance sheet items and off-balance sheet items in the trading book and the banking book as well as a methodology for evaluating the trading book and the banking book.

The Trading book Policy contains a framework for the managing counterparty risk and determine the responsibility of participants staring with exposure, monitoring of exposure up to levels of decision making on limits for counterparty risk exposure.

Liquidity risk Policy The Liquidity risk Policy defines the basis framework, principles and metrics of liquidity risk management, which the Bank will adhere at any time to successfully satisfy its liquidity needs.

The main objective of liquidity management is to reduce the liquidity risk to a minimum by planning the inflow and outflow of funds and the adoption of appropriate measures to prevent and eliminate the causes of insolvency, or the avoidance of negative effects on the financial result and equity due to the inability of the Bank to meet its financial obligations .

The Bank strives in each moment to minimize liquidity risk. For the purposes of effective liquidity risk management and monitoring the Bank uses many reports on cash flows related to future planned activities including cyclical events that may affect the liquidity. The reports are used by the Treasury Division for daily liquidity management.

Except the prescribed reserve requirements, the Bank is establishing its own liquidity reserves with the aim to respond in anytime to unexpected demands and outflows of cash funds. The adequacy of liquidity reserves is monitored on a daily basis.

In order to mitigate liquidity risk, the Bank uses a limit system (internal and external), and a set of internal and external indicators. In addition of above stated, the Bank has set new indicators for liquidity reserve and acceptable levels of deposit outflows.

From 2017, in accordance with the NBS decision on Liquidity risk management, the Bank began to account and monitor the Liquidity Coverage Ratio (LCR) and established more stringent internal limits for this ratio.

In addition to the cash flows , the Bank also considers its liquidity position through liquidity GAP and conducts stress testing their liquidity position at least once every quarter and the results of stress testing are discussed at meetings of the ALCO Committee.

Policy for the management of interest rate risk in the banking book Interest rate risk is the risk of possible adverse effects on the financial result and capital arising from positions in the banking book due to changes in interest rates.

Policy for the management of interest rate risk in the banking book, the Bank is complied with the accepted level of risk exposure and targeted risk profile, as well as general and specific risk management principles set out in the Bank’s Risk Strategy.

The Bank assumes exposure to interest rate risk in accordance with the legal provisions and internal rules, where there is a constant striving to reduce this risk to a minimum.

Bank tends to maintain ratios between interest sensitive assets and liabilities within the established limits for specified intervals. Interest rate risk management is carried out for all currencies as well as at the level for particular major currencies.

Basel III Pillar 3 Disclosure

7

The basis for measuring interest rate risk exposure is to analyze mismatches in re-establishing the interest rate differential between interest-bearing assets and liabilities. Such mismatches are monitored monthly by the interest sensitive items of the balance and off-balance sheet distributed at certain time by intervals and upon such terms and on the basis of the next date of re-pricing instrument or the maturity date for instruments with fixed interest rates.

The Bank performs stress testing of interest rate GAP through a standardized shock of interest rate exposure to interest rate risk and through to the worst-case scenario change in interest rate monitors the effect on the economic value of equity and net interest income (NII).

Country Risk Management Policy Country risk is the risk that refers to the country of origin of the bank is exposed, the risk of negative effects on the financial result and equity due to the inability of banks to collect claims from individuals for reasons that are political, economic or social conditions in country of origin.

Policy for country risk management set out the key principles that are the basis of all business activities of the Bank, which include exposure to other countries and puts the focus on the Bank's approach to managing country risk arising from transactions with foreign counterparties.

The Bank has established limits on individual countries, by groups of countries, in accordance with rating and limits on certain regions of a country where they belong. The basis for determining the limits for exposure to other countries, make the ratings set forth by reputable agencies.

The Bank monitors daily the exposure to countries by all the aforementioned categories and maintains a level of exposure so that they are within established limits. Investment risk managment Policy The bank’s Investment risk is defined by the NBS and involves the investment risk in other legal entities and fixed assets. The Bank's investments in an entity who not belong in the financial sector should not exceed 10% of its capital, whereby under the investment is implied the investment that Bank has acquired the participation or shares of entity that not belong to the financial sector.

Total bank investments in entities outside the financial sector, in fixed assets and investment property must not exceed 60% of its capital, except that this limitation does not apply to the acquisition of shares for resale within six months from the date of acquisition.

In the Investments risk management Policy are determined the key principles related to the Bank's business activities that contributes in increasing the Bank's exposure to investment risk particular in part related to the investment relating to fixed assets. The Bank has established a system of control for all activities that contribute to incensement of investments as well as internal limits to prevent exceeding regulatory Ratios. The Bank calculates and monitors on monthly basis investment ratios to timely control planned investments and timely react in case of internal limits exceeding. Operational Risk Management Policy The Operational Risk Management Policy aim is to ensure that the entire Bank’s stakeholders, including the Board of Directors, Executive and Senior Management as well as Staff, manage operational risk within a formalized Framework aligned to business objectives.

Basel III Pillar 3 Disclosure

8

Operational risk is defined as the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. This definition includes legal and compliance risk, but excludes other risks such as strategic or reputational.

The main purpose of managing operational risk is to increase the awareness of operational risk, while creating the management structure which includes all organizational parts of the Bank and its employees as well as introducting the operational risk management tools.

The Policy gives the management structure for managing operational risk at the Bank level describing the role of every participant. 1. Collection of direct operational losses The Bank emphasizes on the collection of direct operational losses, for which the following definition has been adopted: ’All direct negative financial impacts on the Bank’s financial statements due to the occurrence of an operational risk event’. It is the Bank’s policy that all risk owners (the management of every organizational part of the Bank) report all incidents resulting in direct losses at the time of occurrence even if they are temporarily booked in transitory and/ or suspense accounts and not yet recognized in the P&L. 2. RCSA The RCSA methodology is conducted at the Bank level and in order to identify operational risks at the process level. The same methodology is used for the introduction of new products, activities, processes and systems, and it also assesses the activities entrusted to the third parties. The RCSA uses also the qualitative approach as well as the assessing of the relevant control environment. 3. KRI (key risk indicators) The purpose of KRIs is to assist in the identification of risk exposures before they crystallize into losses. 4. Action Plans By the term ’Action Plan’ we hereby mean all the necessary steps and measures intended to mitigate operational risks, after the acknowledgement of control inefficiencies or risk escalation.

3.2 Risk management framework The Bank has established a comprehensive and reliable system of risk management, integrated in all its business activities, which ensures that the Bank’s risk profile is always in line with already established propensity to risks. Risk management system is proportionate to the nature, volume and complexity of the Bank’s operations and/or its risk profile. The Bank’s risk management system encompasses: • Risk management strategy and policies, as well as procedures for risk identification and measurement and assessment and for managing risks • Adequate internal organizational structure • Effective and efficient process of management of all risk • Adequate internal controls system • Appropriate information system. The risk management framework of the Bank encapsulates the spirit of the following key principles for Risk Management as articulated by Basel III standards:

Basel III Pillar 3 Disclosure

9

• Management oversight and control • Risk culture and ownership • Risk recognition and assessment • Control activities and segregation of duties • Information and communication • Monitoring risk management activities and correcting deficiencies.

3.3 Risk governance structure

The Bank aims to adopt best practices regarding corporate governance, taking into account all relevant guidelines and regulatory requirements, as well as standards of best practices in this area

The Bank’s risk governance framework comprises a number of different constituents. A separate Compliance function is in charge of all internal and external compliance matters, such as standards, laws and regulations. The Internal Audit function, which reports directly to the Board of Directors level, through the Audit Committee, complements the risk management framework acting as the independent review layer, focusing on the effectiveness of the risk management framework and control environment.

The Bank’s risk management organization structure shall ensure the existence of clear lines of responsibility, the efficient segregation of duties and the prevention of conflicts of interest at all levels, including the Board of Directors, Executive Board and Directors of Divisions, as well as between the Bank, its related entities, its customers and any other stakeholders.

Within the Bank, risk management activities broadly take place at the following levels:

Strategic level – It encompasses risk management activities performed by the Board of Directors. These include the adoption of risk and capital strategies and policies, ascertaining the Bank’s risk definitions, profile and appetite, as well as, the risk reward profile.

Tactical level – It encompasses risk management activities performed by Executive Board and Directors of Divisions. These include proposing policies and adopting procedures for managing risks and establishing adequate systems and controls to ensure that the overall risk and reward relation remains within acceptable levels.

Operational (business line) level – It involves management of risks at the point where they are actually created. The relevant activities are performed by individuals who undertake risk on the organization’s behalf. Risk management at this level is implemented by means of appropriate controls incorporated into the relevant operational procedures and guidelines set by the Executive Board.

3.4 Capital management

The Bank’s policy is to maintain a strong capital base and meet the minimum capital requirements imposed by the regulator (NBS), so as to maintain investor, creditor and market confidence and to sustain future development of the business of the Bank. The impact of the level of capital on shareholders’ return is also recognized and the Bank recognizes the need to maintain a balance between the higher returns that might be achieved with lower relation of capital and obligations (financial leverage), and advantages and security afforded by high and stable capital position.

Basel III Pillar 3 Disclosure

10

The Bank’s capital management policy seeks to maximize return on risk adjusted capital while satisfying all the regulatory requirements.

3.5 Risk types The Bank is exposed to various types of risk.

Risks in Pillar 1

Credit risk (Counterparty credit risk; Delivery/Settlement risk for free delivery; CVA risk)

Delivery/Settlement risk for unsettled transactions

Market risk

Operational risk

Risks in Pillar 2

Liquidity risk

Residual risk

Credit fx risk

Concentration risk

Risk of possible underestimation of credit risk in the Standardized Approach

Risk of possible underestimation of operational risk in the Basic Indicator Approach

Credit risk induced by interest rate

Interest rate risk in banking book

Country risk

Investment risk

Strategic risk

Reputational risk

Other risks

The details of components of risks and how they are managed are presented in the following sections of this document.

3.6 Monitoring and reporting

The Risk Management Division provides that all types of risk are being measured and managed in accordance with internal act set by the Board of Directors anf Exsecutive Board. The Risk Management Division submits a quarterly report about risk management to responsible management bodies of the Bank. Under the market risk management, the Bank has established a number of internal reports, reports submitted to the OTP Group and the National Bank of Serbia. The Bank generates a daily report on the Foreign currency risk, the VaR, the compliance with the limits on open positions and report on the Bank's exposure to other counterparties, balance of goverment portfolio securities. Considering liquidity risk the Bank has established a series of reports that are related with daily liquidity risk management activities and that are presented to relevant functions and management bodies of the

Basel III Pillar 3 Disclosure

11

Bank, OTP Group and the National Bank of Serbia. Comprised are reports on liquidity ratio total for all currencies and per major currencies, narrow liquidity ratio, balance of planned cash inflows and outflows, balance of liquid assets and liabilities to other banks, on daily amount of liquidity buffer and deposits outflow the balance of the securities portfolio, balance of deposits and concentracion of deposits. Within the Country risk management the Bank has established series of internal reports as they are: a daily report on the Bank's exposure to other countries and usage of limits, the Bank's exposure to country risk by groups of quality rating and exposures presented by region. In addition to the daily, the monthly reports for ALCO Committee concerning market risk, interest rate risk in the banking book, liquidity risk and country risk, which include analysis of movement of relevant internal and external indicators, liquidity GAP's, interest rates GAP's, the results of stress tests and analysis of limit utilization and investment risk are prepared. The Bank is preparing a series of reports and on a monthly or quarterly basis that are included in the reports at OTP Group level. With respect to the credit risk and portfolio management, the Bank prepares reports related to credit risks and delivers them to the National Bank of Serbia, OTP Group, responsible bodies of the Bank and management of the Bank. Reports on credit risks are delivered quarterly and annually to responsible management bodies of the Bank and contain data on the quality of the credit portfolio, namely the volume of the portfolio towards segmentation of corporate clients and type of products for private individuals, debtor categorization, the largest exposures, indicators of the largest exposure, coverage of loans by provisions and collaterals and LTV for retail exposures. Also, to responsible divisions of the Bank the following reports are delivered on monthly basis: Watch list, Report on industry limits for corporate clients, Data on corporate portfolio – volume, segmentation, total exposure and maximum days of delinquency and Report on restructured loans. With respect to the credit risk and portfolio management to the OTP Group the following reports are delivered: Basel III, large exposures, portfolio of the Bank, restructured loans and collateral database.

The operational risk reporting of the appropriate functions and the Bank’s bodies it is conducted on the

quarterly and annual basis. The reports contain the operational risk events details, information about

taken measures in managing operational risk, the results of testing of the BCP (business continuity plan)

and other. Also, the Bank conducts quarterly reporting towards National bank of Serbia considering

calculated capital requirement for operational risk.

Regarding the Bank's capital, capital adequacy indicator and leverage ratio, the Bank has established a number of internal reports, reports submitted to the Group and the National Bank of Serbia. Reports which the Bank prepares (daily, monthly and quarterly) for National Bank of Serbia are submitted to certain forms in accordance with the timetable set by the Regulator.

Basel III Pillar 3 Disclosure

12

4. Capital adequacy and ICAAP

4.1 Capital adequacy

The NBS is a regulator/supervisor which subscribes and monitors minimum capital adequacy of the banks. Capital adequacy of the bank is measured as relation of capital and risk weighted assets of the bank. According to current regulations, the NBS requires from the banks to maintain capital adequacy ratios at the levels above the following: 1) 4.5%, for Common Equity Tier 1 capital ratio; 2) 6%, for Tier 1 capital ratio; 3) 8%, for capital adequacy ratio. Capital represents the sum of core and additional capital, where core capital represents the sum of Common Equity Tier 1 capital and additional Tier 1 capital. The mentioned types of regulatory capital differ in their quality in terms of availability for covering risk and losses from the bank’s business activity, and, therefore, core capital represents capital available for covering risk or losses during continual business activity (so-called going concern capital), while additional capital consists of elements for covering risk or losses in case of termination of business. Common Equity Tier 1 capital represents the part of core capital of the highest quality and may be used unconditionally, in total amount and without delay for covering risk or losses from business as soon as they emerge. As of 31.12.2017, the Bank disposes of the capital elements of the highest quality (i.e. Common Equity Tier 1 capital), and calculated capital adequacy ratios, including Common Equity Tier 1 capital, and core and total capital, are the same and in the amount of 21.34%. The mentioned ratio signifies adjustment with strategic goal of keeping strong capital position. The Bank’s regulatory capital structure is presented in Annex 1 of the report, and capital requirements and capital adequacy ratios are presented in Appendix 4 of the report.

4.2 ICAAP considerations One of the key elements of the Basel standard adopted by National Bank of Serbia is the requirement for an Internal Capital Adequacy Assessment Process (ICAAP) of the Bank. In accordance with the NBS regulation the Bank is obligated to implement the Internal Capital Adequacy Assessment Process, i.e. determine total internal capital requirements in accordance with its risk profile, as well as determine available internal capital and perform its allocation. The ICAAP incorporates a review and evaluation of risk management and capital relative to the risks to which the Bank is exposed. The Bank has developed its own ICAAP framework which involves identification and measurement of all material risks and calculation of internal capital requirements, to maintain an appropriate level of internal capital in alignment to the Bank’s overall risk profile and business plan. An ICAAP document has been developed in order to primarily meet regulatory requirements, and secondary to complement its ongoing improvement of risk (including risk types which are not covered under Pillar 1 including liquidity risk, fx credit risk, credit risk induced by interest rate

Basel III Pillar 3 Disclosure

13

risk, interest rate risk in the banking book, concentration risk, residual risk, strategic risk, reputational risk and other risks) and capital management approaches. The Bank implements the Internal Capital Adequacy Assessment Process with the purpose to identify all materially significant risks to which the Bank is exposed in its business activities and in that respect to ensure that the Bank at all times has sufficient capital (or in wider terms available financial resources) to cover all these risks. The Bank have developed adequate capabilities that are utilized for internal assessment of capital adequacy which are primarily related to effective and efficient risk and capital management. These capabilities are continuously enhanced and formalized so as to address regulatory requirements but also reap business benefits and support the strategic aspirations of the Bank. The key objective of ICAAP is to ensure that the Bank has sufficient capital (or in wider terms available financial resources) to cover all materially significant risks to which the Bank is exposed in its business activities. A number of already existing capabilities and activities in the Bank may be, to a greater or lesser extent, considered as components of the ICAAP in its broadest sense. These include: -Overall business strategy and objectives of the Bank -Governance, particularly governance in regard to risk and capital management in the Bank -Business planning and budgeting -Risk Management, including risk identification, measurement, assessment, mitigation, monitoring and control of individual risks -Regulatory capital, available internal capital and the Bank funding management -Performance management -Overall internal control system. Thus, the ICAAP is a process that leverages and integrates into these elements mainly from the point of view of available internal capital adequacy assessment, taking into account regulatory requirements. In particular, the ICAAP can be perceived as related to the further integration of risk management, capital management and performance management across the Bank, and thus serves the further implementation of the strategic direction of the Bank. This integration represents best international practice and aims at addressing challenges across capital, risk and performance management in a way that optimally addresses the fundamental relationship between capital, risk and performance. The ICAAP represents process of assessment of all materially significant risks to which the Bank is exposed or could be exposed in its banking activities. In accordance with NBS regulation rules, the Bank has developed ICAAP which contains next phases: -Identification, mapping and assessment of materially significant risks; -Calculation (assessment) of internal capital requirements for individual risks; -Calculation (assessment) of aggregated capital requirements; - Comparison of regulatory and available internal capital; comparison of regulatory and internal capital requirements for individual risks; comparison of aggregated regulatory and aggregated internal capital requirements. Overall assessment of internal capital adequacy (ICAAP), as one of the base assumptions has the assessment of materiality of risks to which the Bank is exposed to, in order to determine the need for calculation of internal capital requirements for individual risk the Bank has identified as materially significant. For all risks identified on the level of the Bank during the risk identification phases, the Bank performs materiality assessment. In accordance with ICAAP Policy, materiality assessment of each risk is

Basel III Pillar 3 Disclosure

14

performed by applying the following methodology, i.e. approaches depending on risk nature, as well as NBS requirement. For all assessed risks recognized as materially significant, the Bank calculates internal capital requirement applying adopted methodology and stress testing. Short description of methodologies (approaches) for calculating internal capital requirement for individual risks: Credit risk, CVA risk, counterparty risk and Settlement/Delivery risk for free delivery The Bank applies standardized approach (prescribed by the Decision on Capital Adequacy of Banks); Approach of the method of current exposure and Approach prescribed by the Decision on Capital Adequacy of Banks, respectively. Risk of possible underestimation of credit risk in the SA The Bank applies its own methodology based on the assumption of deterioration of credit risk for

exposures classified in past due items class from risk weight 100% in risk weight 150%.

Internal capital requirement for credit risk in line with methodology is the sum of the capital requirement calculated by Standardized approach and capital requirement for underestimation risk due to Standardized approach. Market risk (price) The Bank applies standardized approach (prescribed by the Decision on Capital Adequacy of Banks). Market risk (fx) The Bank applies standardized approach (prescribed by the Decision on Capital Adequacy of Banks). Settlement/Delivery risk for unsettled transactions The Bank applies Approach prescribed by the Decision on Capital Adequacy of Banks. Operational risk The Bank applies Basic indicator Approach (prescribed by the Decision on Capital Adequacy of Banks). Credit FX risk The level of credit risk caused by changing foreign exchange earned has already been reflected in the capital requirement for credit risk. For this reason, for the purpose of determining the capital requirement for credit-foreign exchange risk the Bank does not evaluate its substantive significance in quantitative terms, but it is considered material and more involved in the internal capital requirements for credit risk. In assessing the internal capital requirement for credit risk uses the assumption of change of problematic placements using the elasticity coefficient and estimate of the expected maximum change in the value of dinar in relation to the main currencies relevant for the Bank's credit exposure is used. Country risk The Bank applies approach of weighting exposure derived from net assets and off balance sheet items towards other countries by applying risk weights which are differed for each group depending on credit rating in which underlined country is classed along with stress testing.

Basel III Pillar 3 Disclosure

15

Residual risk The Bank applies approach of measuring volatility of market value of collaterals in form of non-financial property which are accepted regarding standardized approach used for credit risk mitigation along with stress testing. Risk of possible underestimation of operational risk in the BIA Bank uses its own methodology based on the comparisons between capital charges calculated under the application of BIA and result obtained from stress testing of actual losses from operational risk.

Liquidity risk The Bank uses its own methodology based on consideration of the ratio of liquidity assets and total liabilities. Credit risk induced by interest rate risk

The level of credit risk caused by interest rate change in the year for which the calculated internal capital

requirements have already been reflected in the capital requirement for credit risk. For the purpose of

determining the capital requirement for credit risk induced by interest rate risk, the Bank does not

evaluate its substantive significance in quantitative terms, but it is considered material. Credit risk

induced by interest rate risk is calculated on portfolio of unsecured consumer loans in RSD with variable

interest rate, which constituter’s greatest part of portfolio exposed to this risk. In assessing the internal

capital requirement for interest rate risk, the assumption of change in problematic placements using the

coefficient of elasticity and standardized interest rate shock is used.

Interest rate risk in banking book The Bank applies the methodology of standardized interest rate shock. Investment risk The Bank uses its own methodology based on comparison of the balance of the investments in other related entities and fixed assets with the balance in the previous period. Credit concentration risk The Bank applies approach of assessing material concentration of individual exposures (according to obligor - title) and material concentration of industrial sectors (according to sector) using the approach of the Bank of Spain based on the Herfindahl-Hirschman Index (HHI). Other risks which cannot be precisely quantified (strategic risk, reputational risk and other risks) For risks which cannot be quantitatively presented, and are qualified as material The Bank allocates capital requirement in the amount of 0.01% of the total net assets as cover for each single risk. Total amount of internal capital requirement with stress test of the Bank is calculated as the simple sum of internal capital requirements for every type of risk provided through applied methodologies for calculating internal capital requirements and stress testing results. The Bank does not take into account the effects of diversification between different types of risk.

Basel III Pillar 3 Disclosure

16

In its ICAAP Report 2017 the Bank has, in addition to risks from Pillar 1, calculated internal capital requirements for interest rate risk in the banking book, credit fx risk, credit risk induced by interest rate concentration risk, strategic risk and reputational risk.

5. Capital buffers

Capital buffers are additional Common Equity Tier 1 capital that banks are obliged to maintain above the prescribed regulatory minimum. Capital buffers introduction has several advantages: the buffers increase the resilience of banks to losses, reduce excessive or underestimated exposures and restrict the distribution of capital. These macroprudential instruments should limit systemic risks in the financial system, which can be cyclical (capital conservation buffer and countercyclical capital buffer) or structural (capital buffer for a systemically important bank and systemic risk buffer).

The following capital buffers are used in the Republic of Serbia:

Capital conservation buffer

Countercyclical capital buffer

Capital buffer for a systemically important bank

Systemic risk buffer.

The capital buffers are calculated in accordance with the with the NBS regulations.

Capital buffers of the Bank as of 31.12.2017. year:

In RSD thousands

Capital buffers In RSD thousands

% of Risk weighted assets

Combined buffer requirement 3,328,353 4.11%

-Capital conservation buffer 2,025,147 2.5%

-Countercyclical capital buffer 0 0%

- Capital buffer for a systemically important bank 0 0%

- Systemic risk buffer 1,303,206

1.61%

6. Leverage ratio

The Leverage ratio represents relation of the core capital, which is generated as the sum of the common

equity tier 1 capital and additional tier 1 capital in accordance with the decision regulating capital

adequacy of the bank, and the amount of the bank's exposure generated (calculated) in line with the

Basel III Pillar 3 Disclosure

17

Methodology of the National Bank of Serbia for producing reports on leverage ratio and it is expressed as

percentage. This ratio represents addition to capital adequacy ratio, and, compared to adequacy ratio,

signifies the level of financial leverage that is not based on the property risk level, considering it is

calculated as relation of core capital and assets of the bank which is not risk level weighted.

In accordance with valid regulations of the National Bank of Serbia, minimum required level is not

determined for leverage ratio, only obligation of calculation and monitoring of the same.

The Leverage ratio of the Bank as of 31th December, 2017 was at the level of 11.42%.

7. Credit risk

7.1 Introduction

Credit risk is the risk of suffering financial loss, should any of the Bank’s customers or market counterparty fail to fulfill their contractual obligations, and arises mainly from the Bank’s placements to corporate and retail customers. These placements arise in the ordinary course of its commercial banking activities and are usually transacted with collateral or other credit risk mitigants.

Short description of credit risk (categories)

Credit risk –the current or prospective risk to earnings and capital arising from the counterparty’s failure

to meet the terms and obligations deriving from any credit agreement with the bank or its failure to

otherwise act as agreed. It also includes:

Residual risk - the current or prospective risk to earnings and capital arising from the fact that recognized risk measurement and mitigation techniques (collaterals, guarantees, netting agreements) used prove less effective than expected.

Credit FX risk – Risk of the loss to which the bank is additionally exposed due to approving placements in foreign currency or dinars with foreign currency clause, which arises from debtors exposure to currency risk, since influence of dinar exchange rate change affects the debtor’s financial standing and creditworthiness.

Credit risk induced by interest rate risk – Risk of the loss to which the bank is additionally exposed due to changes in reference interest rates to which loan repayment is connected that has an influence on credit ability of clients to repay obligations.

Underestimation of credit risk in the SA – defined as the current or prospective risk to earnings and capital arising from activities in case of underestimation of credit risk due to implementing standardized approach (Pillar I) considering that standardized approach to credit risk capital requirement calculation does not adequately encompass all credit risk components.

CVA risk – Risk of loss arising from a change in the amount of the CVA due to the change in the credit margin of the other counterparty, on account of a change in the counterparty’s credit quality.

Basel III Pillar 3 Disclosure

18

Concentration risk – It is acknowledged that the key source of concentration risk is credit concentration risk, which is the current or prospective risk to earnings and capital arising from excessive exposure places with one counterparty or group of related counterparties whose likelihood of default is driven by common underlying factors, e.g. economic sector, industry, geographical location, instrument type.

Country risk: the current or prospective risk to earnings and capital, caused by events in a particular country which are at least to some extent under the control of the government but definitely not under the control of a private enterprise or individual. Possible events include deterioration of economic conditions, political and social upheaval, nationalization and expropriation of assets and disruptive currency depreciation or devaluation. This definition includes all forms of cross-border lending in a country whether to the government, a bank, a private enterprise or an individual. It also includes:

- Sovereign risk, where the government cannot service its own debt because it does not have the required amount of foreign exchange or is unwilling to service its debts or enters in renegotiation and rescheduling schemes or any other form of technical default. Country risk assessment does not only involve an assessment of willingness of the state to fulfill its obligations, as other factors can also cause losses. In practice, sovereign risk and country risk are highly correlated, however, as the government is the major factor in sovereign and country risk affairs.

- Transfer risk, defined as the inability of private agents to fulfill their obligations due to government actions. One example of transfer risk is when the government has imposed prohibitive exchange restrictions, which may make it impossible for private agents to transfer payments.

- Convertibility risk, defined as the inability of private agents to fulfill their obligations due to government/central bank actions. One example of convertibility risk is when the central bank has imposed prohibitive foreign exchange controls, which may make it impossible for private agents to convert local to foreign currency payments and vice versa.

7.2 Credit risk management The Bank has an established internal process for assessing credit risk through Credit Policies. Credit Policy for the Corporate Portfolio The Credit Policy ensures equal treatment for all obligors. The Bank's customers (including related

obligors) are subject to equal treatment in line with procedures that do not entail discriminations,

excluding those regarding credit risk and ability to pay. The assessment of credit rating and ability to pay

obligations is carried out on the basis of a single set of criteria (including obligor risk rating, financial

data, collateral, type and duration of credit risk, industry).

The management of the credit risk in the Corporate Portfolio lies with the Chief Credit Officer in

cooperation with the Chief Risk Officer for issues falling under their respective responsibility, as well

as the Corporate Banking Division Director and the Director of the Trouble Assets Management Division

(for issues falling under their respective responsibility). The above are supported by other senior officers

designated by the Bank’s appropriate Administrative Bodies.

Basel III Pillar 3 Disclosure

19

The credit control mechanism of the Corporate Portfolio consists of:

An independent credit risk management functions.

Multiple level Credit Approving Bodies.

Internal Audit Divisions.

The Loan Administration Department.

Retail Banking Credit Policy and Small Business Banking Credit Policy Credit Policy, as most important document in managing of credit risk in retail and small business,

represents set of selected criteria, guidelines and authorities by which is being implemented strategy of

credit risk protection. The main idea is minimization and determining the acceptable credit risk, with

the aim of reaching an adequate portfolio structure by using of adopted criteria.

Retail Policies/Procedures and Credit Portfolio Management Unit is in charge of preparing and

submitting of Retail Banking Credit Policy and Small Business Banking Credit Policy to the Board of

Directors for adoption, in whose jurisdiction is approval of the same.

These Credit Policies are subject of periodic review. By updating of the document, all approved changes

of the Policies, which have been made since the last review, are incorporated in the same. Unit is under

the responsibility of Chief Credit Officer.

Retail Credit Initiation Department is performing processing of application by applying valid Retail

Banking Credit Policy and Small Business Credit Policy. All overrides of the valid policies have to be

approved in accordance with Override Policies which are defined in the Credit Policies. Department is

under the responsibility of Chief Credit Officer.

7.3 Capital requirement for credit risk The Bank uses the Standardized Approach, defined by the National Bank of Serbia in the Decision on Capital Adequacy of Banks, for calculating the credit risk weighted assets. The Bank’s credit risk weighted assets are the sum of the values of balance sheet assets and off-balance sheet items multiplied by the corresponding credit risk weights. The Bank applies the credit risk mitigation techniques in the manner and under the terms prescribed by the Decision on Capital Adequacy of Banks. The Bank allocates all the exposures from the banking book, exposures from the trading book for which it has to calculate capital requirement for counterparty risk and other exposures from the trading book into one of the following classes: 1) Exposures to central governments or central banks; 2) Exposures to territorial autonomies or local government units; 3) Exposures to public administrative bodies; 4) Exposures to multilateral development banks; 5) Exposures to international organisations; 6) Exposures to banks; 7) Exposures to companies;

Basel III Pillar 3 Disclosure

20

8) Retail exposures; 9) Exposures secured by mortgages on immovable property; 10) Exposures in default; 11) Exposures associated with particularly high risk; 12) Exposures in the form of covered bonds; 13) Exposures in the form of securitisation positions; 14) Exposures to banks and companies with a short-term credit assessment; 15) Exposures in the form of units or shares in open-ended investment funds; 16) Equity exposures; 17) Other items. Exposure ratings and risk weights While calculating the credit risk weighted assets in 2017, the Bank used the credit risk weigths defined in the Decision on Capital Adequacy of Banks. The Bank did not use the obligors’ credit risk weights assigned by the selected credit rating agencies, but it rather used credit risk weights of a country based on the credit rating of a country established by Export Credit Agency applying the methodology of the OECD (credit rating is allocated into one of the eight categories of the lowest export credit insurance premiums). As For exposures to banks, corporates, territorial autonomies and local government entities, public administrative bodies, private individuals, overdue claims, exposures secured by mortgages on real estate and other exposures, the credit risk weights defined in the Decision on Capital Adequacy of Banks have been used. The Bank allocated the credit risk weight of 0% to exposures towards Republic Serbia and National bank of Serbia. The credit risk analysis per exposure classes calculated for the purpose of the regulatory capital adequacy as of 31st December 2017 is provided hereinafter. The overview of capital requirements for cedit risk, counterparty risk and delivery/settlement risk for free delivery per exposure classes as of 31st December 2017 is presented in the following table: In RSD thousands

Exposure classes Capital requirements

Governments and central banks 0

Territorial autonomies and local government entities

242

Public administrative bodies 49

International development banks 0

International institutions 0

Basel III Pillar 3 Disclosure

21

Banks 67,839

Corporate 1,961,336

Private individuals 2,026,611

Exposures secured by mortgages 718,956

Default 217,031

High risk exposures 0

Exposures to covered bonds 0

Exposures of securitisation position 0

Exposures to banks and companies with short-term credit assessment

0

Exposures to investments in open investment funds

0

Equity exposures 8,610

Other exposures 416,796

Total 5,417,470

7.4 Quantitative information on the credit risk

7.4.1 Gross and net credit exposure towards to asset classes

The gross exposures presented in all the tables below include balance sheet assets and off-balance sheet items before applying the credit conversion factor, but do not include off-balance sheet items that are not subject to classification according to the NBS Decision on the Classification of Bank Balance Sheet Assets and Off-Balance Sheet Items, while the exposure with respect to financial derivatives is presented by using the current exposure method. The gross exposures to credit risk before applying the credit risk mitigation techniques, allowances for impairments, provisions, specific credit risk adjustments, necessary reserves and net exposure as of 31st December 2017 are provided in the following table:

Basel III Pillar 3 Disclosure

22

In RSD thousands

Exposure classes Gross exposures

Impairments, provisions

and specific credit risk

adjustments Needed reserve

Net exposure prior to

implementation of credit

protection

Risk weighted

assets

Governments and central banks 23,886,444 16,178 0 23,870,267 0

Territorial autonomies and local government entities 15,136 2 0 15,134 3,027

Public administrative bodies 3,047 0 0 3,047 609

Banks 4,250,745 10,805 0 4,239,941 847,988

Corporate 31,181,576 53,573 0 31,128,003 24,516,700

Private individuals 38,100,920 216,223 0 37,884,698 25,332,640

Exposures secured by mortgages 16,930,241 105,296 0 16,824,945 8,986,947

Exposures in default 7,226,379 4,815,028 0 2,411,351 2,712,890

Equity exposures 416,583 308,952 0 107,630 107,630

Other exposures 24,554,334 5,654,950 0 18,899,384 5,209,943

Total 146,565,405 11,181,007 0 135,384,400 67,718,374

amount of deductions from capital 381,838

The gross exposures to credit risk before applying the credit risk mitigation techniques per credit risk weights and exposure classes, as of 31st December 2017, are presented in the following table:

In RSD thousands

CREDIT RISK WEIGHTS

Exposure classes Gross

exposures 0% 20% 35% 50% 75% 100% 150%

Governments and central banks 23,886,444 23,886,444 0 0 0 0 0 0

Territorial autonomies and local government entities 15,136 0 15,136 0 0 0 0 0

Public administrative bodies 3,047 0 3,047 0 0 0 0 0

Banks 4,250,745 0 4,250,745 0 0 0 0 0

Corporate 31,181,576 0 20,176 0 0 0 31,161,400 0

Private individuals 38,100,920 0 0 0 0 38,100,920 0 0

Exposures secured by mortgages 16,930,241 6,555 592 10,419,550 1,129,233 735,154 4,639,157 0

Basel III Pillar 3 Disclosure

23

Exposures in default 7,226,379 0 0 0 0 0 6,558,863 667,516

Equity exposures 416,583 0 0 0 0 0 416,583 0

Other exposures 24,554,334 13,707,744 0 0 0 0 10,846,590 0

Total 146,565,405 37,600,743 4,289,696 10,419,550 1,129,233 38,836,074 53,622,593 667,516

amount of deductions from capital 381,838

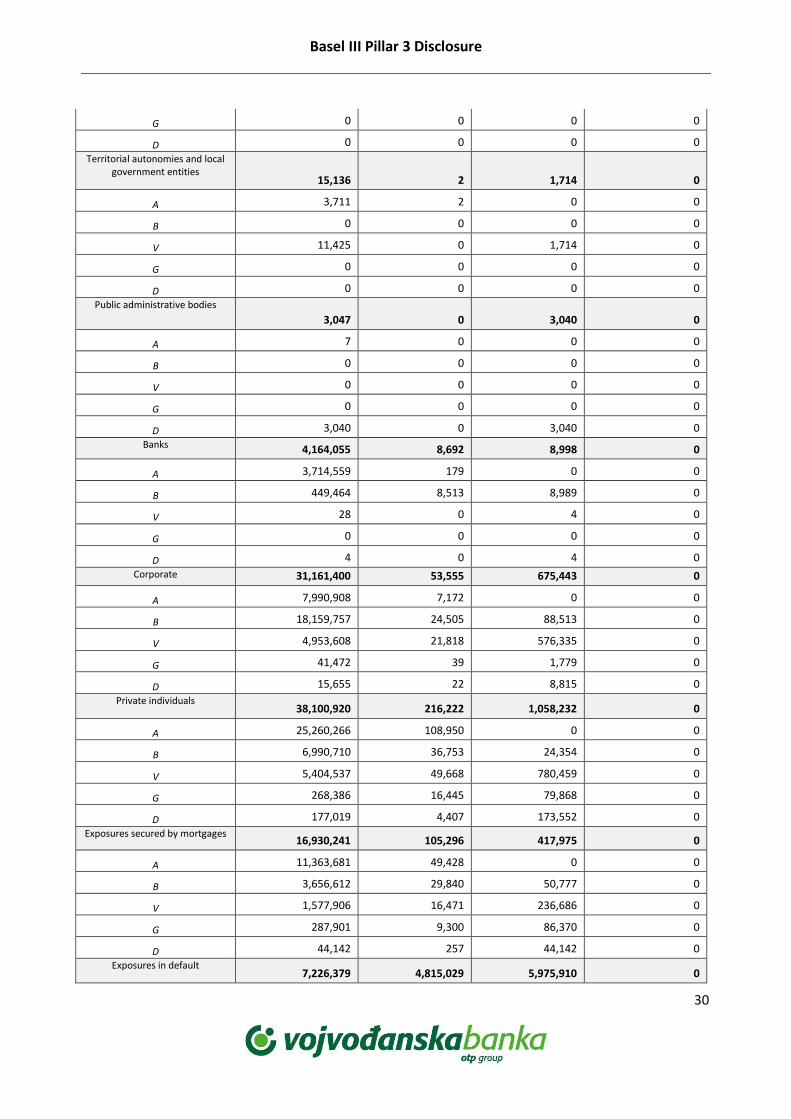

The net exposures to credit risk before applying the credit risk mitigation techniques per credit risk weights and exposure classes, as of 31st December 2017, are presented in the following table: In RSD thousands

Exposure classes Net

exposures

CREDIT RISK WEIGHTS

0% 20% 35% 50% 75% 100% 150%

Governments and central banks 23,870,267 23,870,267 0 0 0 0 0 0

Territorial autonomies and local government entities 15,134 0 15,134 0 0 0 0 0

Public administrative bodies 3,047 0 3,047 0 0 0 0 0

Banks 4,239,941 0 4,239,941 0 0 0 0 0

Corporate 31,128,003 0 20,156 0 0 0 31,107,847 0

Private individuals 37,884,698 0 0 0 0 37,884,698 0 0

Exposures secured by mortgages 16,824,945 6,553 592 10,367,215 1,128,331 707,482 4,614,772 0

Exposures in default 2,411,351 0 0 0 0 0 1,771,675 639,676

Equity exposures 107,630 0 0 0 0 0 107,630 0

Other exposures 18,899,384 13,707,744 0 0 0 0 5,191,640 0

Total 135,384,400 37,584,564 4,278,870 10,367,215 1,128,331 38,592,180 42,793,564 639,676

The net exposures to credit risk after applying the credit risk mitigation techniques per credit risk weights and exposure classes, as of 31st December 2017, are presented in the following table:

Basel III Pillar 3 Disclosure

24

In RSD thousands

Exposure classes Net

exposures

CREDIT RISK WEIGHTS

0% 20% 35% 50% 75% 100% 150%

Governments and central banks 24,017,181 24,017,181 0 0 0 0 0 0

Territorial autonomies and local government entities 15,134 0 15,134 0 0 0 0 0

Public administrative bodies 3,047 0 3,047 0 0 0 0 0

Banks 4,317,151 0 4,317,151 0 0 0 0 0

Corporate 30,499,538 0 0 0 0 0 30,499,538 0

Private individuals 37,309,737 0 0 0 0 37,309,737 0 0

Exposures secured by mortgages 16,824,945 6,553 592 10,367,215 1,128,331 707,482 4,614,772 0

Exposures in default 2,411,351 0 0 0 0 0 1,771,675 639,676

Equity exposures 107,630 0 0 0 0 0 107,630 0

Other exposures 19,878,686 14,574,307 112,739 0 0 0 5,191,640 0

Total 135,384,400 38,598,041 4,448,663 10,367,215 1,128,331 38,017,219 42,185,255 639,676

The gross exposures to credit risk per exposure classes before applying the credit risk mitigation techniques, as of 31st December 2017 and average exposures per exposure classes during 2017 are displayed in the following table: In RSD thousands

Exposure classes

Exposures before implementation of

credit protection as at 31.12.2017

Average gross exposure before

implementation of credit protection

Governments and central banks 23,886,444 27,512,139

Territorial autonomies and local government entities 15,136 12,748

Public administrative bodies 3,047 29,336

Banks 4,250,745 3,825,820

Basel III Pillar 3 Disclosure

25

Corporate 31,181,576 33,204,526

Private individuals 38,100,920 34,572,326

Exposures secured by mortgages 16,930,241 18,691,456

Exposures in default 7,226,379 10,863,804

Equity exposures 416,583 534,816

Other exposures 24,554,334 24,435,028

Total 146,565,405 153,681,999

7.4.2 Credit exposure by geography/region

The geographical distribution of gross exposures before applying the credit risk mitigation techniques, per exposure classes and according to the materially significant areas, as of 31st December 2017, was as follows:

In RSD thousands

Exposure classes Credit risk exposure

Serbia European

Union the rest of

Europe the rest of the

world

Governments and central banks 23,886,444 23,886,444 0 0 0

Territorial autonomies and local government entities 15,136 15,136 0 0 0

Public administrative bodies 3,047 3,047 0 0 0

Banks 4,250,745 7,806 2,885,894 162,611 1,194,434

Corporate 31,181,576 30,374,847 512,811 0 293,918

Private individuals 38,100,920 38,064,887 24,167 5,380 6,486

Exposures secured by mortgages 16,930,241 16,921,080 9,161 0 0

Exposures in default 7,226,379 7,209,564 16,361 361 93

Equity exposures 416,583 211,018 187,510 18,055 0

Other exposures 24,554,334 24,554,334 0 0 0

Total 146,565,405 141,248,163 3,635,904 186,407 1,494,931

7.4.3 Credit exposure by sectors

The distribution of gross exposures before applying the credit risk mitigation techniques, per exposure classes and sectors, as of 31st December 2017, was as follows:

Basel III Pillar 3 Disclosure

26

In RSD thousands

Exposure classes

Credit risk

exposure

Fin

ance

an

d in

sura

nce

Pu

blic

co

mp

anie

s

Co

rpo

rate

Entr

epre

neu

rs

Pu

blic

sec

tor

Ret

ail

Pri

vate

ho

use

ho

lds

wit

h

emp

loye

d in

div

idu

als

and

regi

ster

ed a

gric

ult

uri

sts

Fore

ign

per

son

s

Oth

er c

lien

ts

Oth

er

Governments and central banks

23,886,444 7,708,812 0 0 0 16,177,632 0 0 0 0 0

Territorial autonomies and local government entities

15,136 0 0 0 0 15,136 0 0 0 0 0

Public administrative bodies

3,047 0 0 0 0 3,047 0 0 0 0 0

Banks 4,250,745 7,806 0 0 0 0 0 0 4,242,939 0 0

Corporate 31,181,576 2,490,830 3,793,015 24,091,002 0 0 0 0 806,729 0 0

Private individuals

38,100,920 120,924 83,058 8,610,683 858,285 0 28,205,399 42,903 36,033 143,635 0

Exposures secured by mortgages

16,930,241 0 0 5,374,051 33,371 0 11,496,029 1,747 9,161 15,882 0

Exposures in default

7,226,379 16,407 8,355 2,262,854 514,744 106,919 2,809,018 10,934 16,814 1,480,334 0

Equity exposures

416,583 96,146 87,251 27,621 0 0 0 0 205,565 0 0

Other exposures

24,554,334 0 0 0 0 0 22438 0 0 0 24,531,896

Total 146,565,405 10,440,925 3,971,679 40,366,211 1,406,400 16,302,734 42,532,884 55,584 5,317,241 1,639,851 24,531,896

The table below indicates gross exposures before applying the credit risk mitigation techniques with respect to which allowances for impairments or provisions were made for off-balance sheet items per sectors or types of counterparties, per exposure classes, as of 31st December 2017.

In RSD thousands

Exposure classes Credit risk exposures with impairments or provisions

Impairments or provisions

Governments and central banks 0 0

Finance and insurance 0 0

Public companies 0 0

Corporate 0 0

Entrepreneurs 0 0

Public sector 0 0

Retail 0 0

Private households with employed individuals and registered agriculturists

0 0

Foreign persons 0 0

Other clients 0 0

Territorial autonomies and local government entities 2 2

Finance and insurance 0 0

Basel III Pillar 3 Disclosure

27

Public companies 0 0

Corporate 0 0

Entrepreneurs 0 0

Public sector 2 2

Retail 0 0

Private households with employed individuals and registered agriculturists

0 0

Foreign persons 0 0

Other clients 0 0

Public administrative bodies 0 0

Finance and insurance 0 0

Public companies 0 0

Corporate 0 0

Entrepreneurs 0 0

Public sector 0 0

Retail 0 0

Private households with employed individuals and registered agriculturists

0 0

Foreign persons 0 0

Other clients 0 0

Banks 242,650 10,733

Finance and insurance 0 0

Public companies 0 0

Corporate 0 0

Entrepreneurs 0 0

Public sector 0 0

Retail 0 0

Private households with employed individuals and registered agriculturists

0 0

Foreign persons 242,650 10,733

Other clients 0 0

Corporate 30,815,540 53,539

Finance and insurance 2,490,605 10,545

Public companies 3,792,829 1,439

Corporate 24,020,843 35,823

Entrepreneurs 0 0

Public sector 0 0

Retail 0 0

Private households with employed individuals and registered agriculturists

0 0

Foreign persons 511,263 5,732

Other clients 0 0

Private individuals 37,669,658 216,222

Finance and insurance 65,543 25

Public companies 83,057 50

Corporate 8,465,227 17,960

Entrepreneurs 851,091 2,524

Public sector 0 0

Retail 28,012,956 194,855

Private households with employed individuals and registered agriculturists

42,901 380