basel ii overview (final review) -...

TRANSCRIPT

BASEL II OVERVIEWFEBRUARY 2017

BASEL II INTRODUCTION

3

BASEL – BACKGROUND

BASEL I Issued 1988

BASEL IIIssued 2006

BASEL IIIIssued 2010

u In the early 1980s, the onset of the Latin American debt crisis heightened the Committee’s concerns that the capital ratios of the main international banks were deteriorating at a time of growing international risks.

u Designed to achieve greater convergence in the measurement of capital adequacy.

u Results in broad consensus on a weighted approach to the measurement of risk, both on and off banks' balance sheets.

u Designed to improve the way regulatory capital requirements reflect underlying risks and to better address the recent financial innovation.

u The changes aimed at rewarding and encouraging continued improvements in risk measurement and control.

u Also to develop and expand the standardized rules set out in the 1988 Accord.

u Banking sector had entered the financial crisis with too much leverage and inadequate liquidity buffers.

u These defects were accompanied by poor governance and risk management, as well as inappropriate incentive structures.

u The dangerous combination of these factors was demonstrated by the mispricing of credit and liquidity risk, and excess credit growth.

u Some countries are already starting to execute capital requirements that go beyond current Basel III. Particularly, the US and some Europe countries are demanding banks to meet minimum capital ratios even after the effect of severe stress.

u UK and Switzerland have set a minimum level of leverage ratio at above 3%; other countries, are contending that “Pillar 2” add-on capital are met through highest quality capital.

Post Basel III (BASEL IV )After 2012

4

BASEL – KEY CONTENTS

u Focus on a single risk measure (Credit Risk)

u Insufficiently sensitive to risk (broad categories) - One size fits all

u Did not allow for use of Credit Risk Mitigation techniques such as Collateral, Guarantees etc.

u Introduced Minimal Capital Requirement pillar of at least 8% of its risk-weighted assets for sum of Tier 1 and Tier 2 capital

u Did not assess market risks - these came in the 1996 Market Risk Amendment

u Operational risks were ignored as a specific risk category

BASEL I Issued 1988

u Establish fixed risk weights corresponding to each supervisory category and makes use of external credit assessments

u Greater use of assessments of risk provided by banks’ internal systems as inputs to capital calculations

u Introduced capital charge for Operational Risk

u Introduced 2 new pillars

u Supervisory Review Process (Pillar 2)

u Market Discipline (Pillar 3)

BASEL IIIssued 2006

u Focussing on strengthening existing capital requirements and accompanying liquidity concerns

u Introducing Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR)

u Capital requirements for CCR based on stressed inputs

u Introducing bank liquidity and bank leverage

u Introducing Capital Conservation Buffer andcountercyclical buffer

u Introducing methodology to identify global systemically important financial institutions (SIFIs)

BASEL IIIIssued 2010

Post Basel III (BASEL IV )After 2012

u Restricting the advantages to banks of using internal models to calculate their capital requirements

u Requiring banks to meet a higher minimum leverage ratio

u Greater disclosure by banks

5

THE 3 PILLARS OF THE BASEL II ACCORD

Pillar 1 – Minimum Capital Requirements Pillar 2 – Supervisory Review Process Pillar 3 – Market Discipline

q Credit Risk§ Standardized approach§ Foundation internal ratings

based (F-IRB) approach§ Advanced IRB (A-IRB)

approach

q Market Risk§ Standardized approach (SA)§ Internal methods approach

(IMA)

q Operational Risk§ Basic indicator approach

(BIA)§ Standardized approach (SA)§ Standardized Measurement

Approach (SMA)

Minimum Capital Requirement

§ Board and Senior Management Oversight

§ Sound Capital Assessment and Planning

§ Comprehensive Assessment of Risks

§ Monitoring and Reporting§ Internal Control Review

Capital Adequacy Assessment

§ Annual comprehensive ICAAP Review

§ Stress Testing Review§ Material Risks Review

Supervisory Review Process

§ Guiding Principles§ Interaction with Accounting

Disclosures

General Considerations

§ General§ Scope of Application§ Capital Structure§ Capital Adequacy§ Credit Risk§ Market Risk§ Operational Risk§ Liquidity Risk§ Interest Rate Risk§ Other Material Risks

Disclosure Requirements

BASEL II PILLAR 1 OVERVIEW

7

CREDIT RWA CALCULATION

Bank’s capital ratio 8.00%= ³

Standardised Approach

• Classification of credits• External rating of credit quality• Allocation of fixed weights to each category• Calculation of credit risk as the sum of the

product of each exposure and respective weight

Internal Rating Based (IRB) Approaches

• Classification of credits and Internal rating of credit quality• Allocation to risk classes• Calculation of risk parameters per counterparty / exposure• Probability of default (PD) - What is the likelihood that a borrower defaults?• Loss given default (LGD) - How much of the exposure will be lost in event of default?• - Exposure at default (EAD) - What is your exposure to the borrower in case of default?• Quantification of credit risk as a function of PD, LGD, EAD, CCF, credit risk mitigation and effective maturity.• Only applied for certain exposure (new guideline issued on Mar 2016) (i.e. Not applicable for sovereign, banks, large corps, etc.)

IRB Foundation Approach IRB Advanced Approach

• Individual derivation of PD of each risk class

• LGD, EAD and time to maturitygiven by supervisory authorities

• Individual derivation of PD, LGD,and EAD for each risk class

• Consideration of time to maturityof each credit exposure

Total Capital

Credit RWA + Market RWA + Operational RWA

AAA A+ BBB+to AA- to A- to BBB -

Sovereigns 0% 20% 50% ...Option I 20% 50% 100% ...Option II 20% 50% 50% ...

Corporates 20% 50% 100% ...

...

SovereignsBanks

8

MARKET RWA CALCULATION

Bank’s capital ratio 8.00%= ³Total Capital

Credit risk + Market risk + Operational risk

Standardized Approach

Under this method market risk capital requirements are fixed based on predefined tables depending upon whether the exposures are:

•Long or short positions•Physical or derivative positions• Interest rate, Equity position, FX, Commodity or Option

risks•Subject to instrument specific or general market risks• Instrument maturity

Internal Models Approach

This method allows banks to use risk measures derived from their own internal risk management models, subject to seven sets of conditions, namely:

•certain general criteria concerning the adequacy of the risk management system

•qualitative standards for internal oversight of the use of models, notably by management

•guidelines for specifying an appropriate set of market risk factors (i.e., the market rates and prices that affect the value of banks' positions)

•quantitative standards setting out the use of common minimum statistical parameters for measuring risk

•guidelines for stress testing•validation procedures for external oversight of the use of

models•rules for banks which use a mixture of models and the

standardized approach

9

OPERATIONAL RWA CALCULATION

Bank’s capital ratio 8.00%= ³

Basic Indicator Approach

Operational risk seen as linear function of one unique risk measure (Gl) per bank:

KBIA = GI * awithKBIA = capital charge GI = exposure indicator,

provisionally averagegross income over past3 years

a = fixed percentage,set by Committee,relating the indus-try-wide level ofrequired capital tothe industry-widelevel of the indicator -actually 15%

Total Capital

Credit risk + Market risk + Operational risk

Standardized Approach

Operational risk seen as linear function of unique risk measures GEl1-8) per business unit:

KSTA = S(GI1-8 * b1-8)withb= fixed percentage, set by

Committee, for each of the8 business lines

Alternative Standardized Approach allows for special treatment of retail and commercial banking:KIRB = ßRetailBk. * m * LARetail Bk.withßRetailBk. = beta of business lineLARetailBk= loans and advancesm = multiplier (0.035)

Standardised Measurement Approach*

The SMA combines the Business Indicator (BI), a simple financial statement proxy of operational risk exposure, with bank-specific operational loss data (should use 10 years of good-quality loss data or minimum of five years of data).

*According to d355, Advanced Measurement Approach to be replaced by SMA - the proposed SMA framework would be applied to internationally active banks on a consolidated basis. Supervisors retain discretion to apply the SMA framework to non-internationally active institutions.ILDC: Interest, Lease and Dividend Component; SC: Services Component; FC: Financial Component; Avg: Average of the items at the years: t, t-1 and t-2

BASEL II PILLAR 1 – CREDIT RISK STANDARDIZED APPROACH

1 1

CREDIT RWA CALCULATION PROCESS

u Approach Determination - Defines approach to be adopted (Standardized, Foundation IRB or Advanced IRB) for each credit portfolio

u Single View of Customer (SVC) - Creates a consolidated view of all credit exposures to a customer, including identifying material customer relationships for purposes of defining a customer group

u Asset Classification - Identifies the asset class of the exposure

u Risk Weight Assignment/ PD calculation: Depends on different methods (SA/ IRB), Risk Weight Assignment (applicable for SA) or Internal PD calculation (applicable for both F-IRB and A-IRB) will be performed.

u Exposure / Exposure at Default (EAD) - Calculates the potential exposure at the point when customer defaults

u Credit Risk Mitigation (CRM) - Recognises the mitigating effects of collaterals, guarantees, etc in reducing the exposure amount and / or LGD

u Maturity calculation: Determines Supervisory Maturity (applicable for F-IRB) or internally calculate Maturity (applicable for A-IRB)

u Risk Weighted Assets (RWA) Calculation - Calculates the credit RWA of the exposure based on rules specific to the approach adopted

7

Internal PD Calculation

Internal EAD Calculation

Internal LGD Calculation

Internal Maturity Calculation

RWA Calculation

CRM CRM

CRM CRMSVC Asset

Classification

Internal PD Calculation

Supervisory EAD

CRM & Supervisory

LGD

Supervisory Maturity1

SVC Asset Classification Risk Weight Assignment

Exposure Calculation

Credit Risk Mitigation

RWA Calculation

Approach determination

1 2 3 4 5 7

2

3 4 5 6

3 4 5 6IRB Approach

Standardized ApproachFoundation

Advanced

0

0

1

2

4

5

7

3

6

1 2

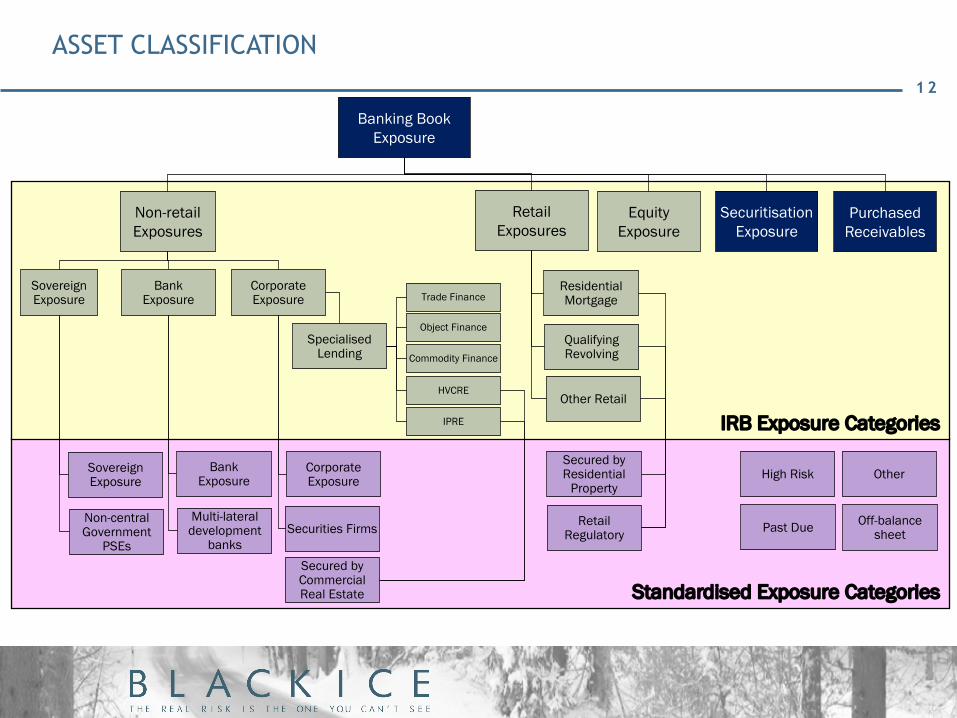

ASSET CLASSIFICATION

Standardised Exposure Categories

IRB Exposure Categories

Banking Book Exposure

Corporate Exposure

BankExposure

SovereignExposure

Retail Exposures

EquityExposure

SecuritisationExposure

Non-central Government

PSEs

Multi-lateral development

banks

Secured by Residential

Property

Securities Firms

Secured by Commercial Real Estate

Past Due

High Risk Other

Off-balance sheet

Non-retail Exposures

Purchased Receivables

Specialised Lending

SovereignExposure

Retail Regulatory

Corporate Exposure

BankExposure

Residential Mortgage

Qualifying Revolving

Other RetailHVCRE

IPRE

Object Finance

Commodity Finance

Trade Finance

1 3

KEY PARAMETERS ACROSS APPROACHES

Standardized Approaches IRB Approaches

Exposure Calculation

EADExposure

Foundation Retail

RWA x min. 8 %Capital

Calculation

Credit Risk Mitigation

HairCuts (Collateral, Currency, Maturity)

Effective Maturity

Customer Risk Customer PDSupervisory Values, dependent on external ratings

Effective MaturityEffective Maturity

CCF

Eligible Financial Collateral

AdvancedSimple Comprehensive

CCF

Pool PD Customer PD

HairCuts (Currency, Maturity)

Internally CalculatedRegulator Defined

Eligible Collateral

Haircuts (Currency, Maturity)

Exposure LGD Exposure LGDPool LGD

EAD

Bank‘s Collateral

HairCuts (Currency, Maturity)

HairCuts (Currency, Maturity)

Eligible Financial Collateral

Supervisory Risk weights

1 4

CREDIT RISK MITIGATION – RESIDUAL RISK

E* = MAX {0; [E * (1+HExposure) - C * (1 - HCollateral – HFX)]}

Legend: E* = Exposure value after risk mitigation, E = Current exposure value (before mitigation), C = Current value of collateral received, w = Specific risk weight

Maturity Mismatch Market Risk

• Exposure and collateral possess a different time to maturity: Usually the collateral is not pledged for the life of the exposure

• This maturity mismatch causes a forward credit risk

• Supervisory measures:- Collateral must be pledged for

at least one year- Consideration of maturity

adjustment: Adjusted Protection= C*

= C * (1 - HCollateral – HFX) *

• Value of exposure and collateral depends on different market risk factors

• This can cause a diverging development of the respective value

• Application of haircuts to allow for- volatility of price of exposure- volatility of price of collateral- volatility of exchange rate, if

FX-mismatch exists

tT

1 5

CREDIT RISK MITIGATION – DERIVATION OF HAIRCUTS IN THE COMPREHENSIVE APPROACH

E* = MAX {0; [E * (1+HExposure) - C * (1 - HCollateral – HFX)]}

Legend: E* = Exposure value after risk mitigation, E = Current exposure value (before mitigation), C = Current value of collateral received, w = Specific risk weight

Standard Supervisory Haircuts Own Estimates Haircuts based on VaR-models

• Derivation based on internal estimates of price and FX volatility

- 99th percentile one-tailed confidence interval

- Consideration of illiquidity- Historical observation period of

at least 1 year- Update at least every 3 months

• Derivation of haircut for each category of exposure; else individually

- Debt securities are rated BBB-(A-3) or higher

- Categorisation according to type of issuer or issue, its rating, its maturity and its modified duration

• Use VaR-approach to reflect price volatility of exposure and collateral of repo-style transactions

- Repo-style transactions covered by a bilateral netting agreement on a counterparty-by-counterparty basis

- Requires supervisory approval of internal model according to 1996 Market Risk Amendment

- Same statistical parameters as in market risk measurement, except for 5 business day holding period

• Backtesting required

t <= 1 yr 0,5 1,0 1 yr < t <= 5 yr 2,0 4,0

5 yr < t 4,0 8,0 t <= 1 yr 1,0 2,0

1 yr < t <= 5 yr 3,0 6,0 5 yr < t 6,0 12,0

BB+ to BB- 15,0 - Main index equities and gold

UCITS / Mutual FundsCash in same currency 0,0

Highest haircut applicable

15,0

25,0

AAA to AA-

A+ to BBB- and unrated bank securities

Other equities listed on recognized exchanges

Issue rating for debt securities

Residual Maturity

Sovereign Issuers

Other Issuers

- Haircuts expressed as percentage- Haircuts based on 10 day holding period assumption

1 6

CREDIT RISK MITIGATION – TECHNIQUES

Collateral• Financial collateral• Physical collateral

- Receivables- Corporate or Residential Real Estate

Guarantees and Credit Derivatives• Specific characteristics

- Direct claims on protection provider- Explicitly referenced to specific exposures- Irrevocable and unconditional

• Certain range of eligible protection providers- Sovereign entities, PSE, banks and securities firms with lower risk weight

than counterparty- Other entities rated A- or better

On-Balance Sheet Netting AgreementsConsideration of net exposure of loans and deposits:• Assets (loans) treated as exposure• Liabilities (deposits) treated as collateral

Credit Risk Mitigation Techniques

1 7

CREDIT RISK MITIGATION – TYPES OF COLLATERAL ELIGIBLE

Collateral

Financial Collateral Physical Collateral

•Receivables•Real Estate

Collateral- Commercial

Real Estate (CRE)

- Residential Real Estate (RRE)

•Any other physical collateral

• Cash• Gold• Debt securities rated by ECAIs

- Sovereign or PSE exposure rated BB- or better- Other exposure rated BBB- or better- Short-term rating of A-3/P-3 or better

• Debt securities not rated by ECAIs- Issued by banks and listed on exchange- Qualifies as senior debt- Other issues of same seniority rated BBB- (A-

3/ P-3) or better- Counterparty not expected to be rated below

BBB-• Equities included in a main index• Equities not included in a main index but listed on a

recognized exchange

StandardApproach

StandardApproach

IRB FoundationApproach

Selected Fin. Collateral

Simple Approach:Substitution of Risk

Weights

Selected Fin. Collateral

Comprehensive Approach:

Reduction of Exposure

All collateral types

Comprehensive Approach:

Reduction of Exposure

Impact on capital chargeApproach

IRBAdvancedApproach

All collateral types

Collateralisation reflected in derivation of Loss Given Default

(LGD)

BASEL II PILLAR 1 – MARKET RISK STANDARDIZED MEASUREMENT APPROACH

1 9

Market Risks

u Risk of losses in on- and off-balance sheet positions arising from movements in market prices

u The risks subject to this requirement are:

- The risks pertaining to interest rate related instruments and equities in the trading Book

- Foreign exchange risk and commodities risk throughout the bank

Trading Book

u A trading book consists of positions in financial instruments and commodities held either with trading intent or in order to hedge other elements of the trading book.

u To be eligible for trading book capital treatment, financial instruments must either be free of any restrictive covenants on their tradability or able to be hedged completely.

u In addition, positions should be frequently and accurately valued, and the portfolio should be actively managed.

u Trading book positions are more vulnerable to short-term changes in their value and therefore warrant a capital charge against market risk.

u Positions held with trading intent are those held intentionally for short-term resale and/or with the intent of benefiting from actual or expected short-term price movements or to lock in arbitrage profits, and may include for example proprietary positions, positions arising from client servicing (e.g. matched principal broking) and market making.

WHAT ARE MARKET RISKS ?

2 0

INTEREST RATE RISK

Specific Risk General Risk

Definitions Adverse movement in the price of an individual security owing to factors related to the individual issuer

Risk of loss arising from changes in market interest rates

Exposures 1. Absolute gross market value of long and short debt securities positions

2. Offsetting is restricted to matched positions in the identical issue

Net short or long market value of debt securities positions by currency

MeasurementMethod

Specific risk capital charge according to counterparty type and credit ratings

General risk capital charge for the followings:-1. Net position charge2. Basis risk charge3. Yield curve risk chargeMeasured using one of the following methods:-1. Maturity Method2. Duration Method

Parameters 1. Counterparty type2. Credit ratings3. Residual term to final maturity

1. Coupon rate2. Residual term to maturity

Interest rate risk capital charge is the total of both specific and general risk capital charges

2 1

EQUITY RISK

Specific Risk General Risk

Definitions 1. Gross equity positions (i.e. the sum of all long equity positions and of all short equity positions)

2. Long and short positions in the same issue may be reported on a net basis

1. Difference between the sum of the longs and the sum of the shorts (i.e. the overall net position in an equity market)

2. The long or short position in the market must be calculated on a market-by-market basis, i.e. a separate calculation has to be carried out for each national market in which the bank holds equities.

Exposures 1. Absolute gross market value of long and short debt securities positions

2. Offsetting is restricted to matched positions in the identical issue

Net short or long market value of debt securities positions by currency

MeasurementMethod

8%, unless the portfolio is both liquid andwell-diversified, in which case the charge will be 4%.

8%

Parameters 1. Counterparty type2. Credit ratings3. Residual term to final maturity

1. Coupon rate2. Residual term to maturity

Equity risk capital charge is the total of both specific and general risk capital charges

2 2

FOREIGN EXCHANGE RISK

General Risk

Definitions Risk of holding or taking positions in foreign currencies, including gold

Exposures 1. The net spot position (i.e. all asset items less all liability items, including accrued interest, denominated in the currency in question)

2. The net forward position (i.e. all amounts to be received less all amounts to be paid under forward foreign exchange transactions, including currency futures and the principal on currency swaps not included in the spot position)

3. Guarantees (and similar instruments) that are certain to be called and are likely to be irrecoverable

MeasurementMethod

Short hand method:-1. 8% of the higher of either the net long currency positions or the net short currency positions

and 2. 8% of the net position in gold

Parameters Currency code

2 3

COMMODITIES RISK

General Risk

Definitions The risk of holding or taking positions in commodities, including precious metals, but excluding gold

Exposures 1. Long and short positions in each commodity may be reported on a net basis for the purposes of calculating open positions

2. Positions in different commodities will as a general rule not be offsettable in this fashion

MeasurementMethod

Commodity risk capital charge captures the following risks:1. Directional Risk (15% of net position)2. Basis Risk, Interest Rate Risk and Forward Gap Risk (3% of gross position)Commodity risk capital charge can be measured using one of the following methods:-1. Simplified Approach2. Maturity Ladder Approach

Parameters Commodity type

BASEL II – PILLAR 1 OPERATIONAL RISK BASIC INDICATOR APPROACH

2 5

OPERATIONAL RISK BIA MEASUREMENT

• Operational Risk capital charge under the BIA is calculated as follows:

• Average over the previous three years of a fixed percentage (denoted alpha, i.e. 15%) of positive annual gross income

• Figures for any year in which annual gross income is negative or zero should be excluded from both the numerator and denominator when calculating the average

• The charge may be expressed as follows:

where:

KBIA = the capital charge under the Basic Indicator Approach

GI = annual gross income, where positive, over the previous three years

N = number of the previous three years for which gross income is positive

α = 15%

2 6

DEFINITION OF GROSS INCOME

• Gross income is defined as follows:-

• Net interest income plus net non-interest income

• Gross of any provisions (e.g. for unpaid interest)

• Gross of operating expenses, including fees paid to outsourcing service providers

• Exclude realized profits/losses from the sale of securities in the banking book

• Exclude extraordinary or irregular items as well as income derived from insurance

BASEL II – PILLAR 2 SREP & ICAAP OVERVIEW

2 8

ICAAP FRAMEWORK

CreditRisk (inc.

Concentr. & residual risk)

MarketRisk

OperationalRisk

Interest rateRisk in theBanking

Book

OtherRisks

(Strategic,Reputation)

CapitalCharge

Board & Senior Management Oversight

CapitalCharge

CapitalCharge

CapitalCharge*

CapitalCharge*

Use of ICAAP

Monitoring, Reporting and Review

ICAA

P M

easu

rem

ent

ICAA

P M

anag

emen

t

Key Requirements

Risk Aggregation

§ Establish rigorous corporate governance and senior management oversight

§ Establish risk-based strategy including defining and setting the bank’s appetite and tolerance for risk

§ Assess and measure all material risks inherent in Group’s business

§ Review, monitor, control and report on all material risks

§ Demonstrate that ICAAP forms an integral part of day-to-day management process and decision making culture of the Group

§ Relate capital to level of risk and ensure capital adequacy using scenario analysis and stress testing methods

2 9

What is Risk Appetite?

Risk Appetite is the amount and type of risk that an organization is able and willing to accept in pursuit of its business objectives. It can be set qualitatively (“high”, “moderate”, “very low”) or quantitatively (e.g. through at-risk measures) for broad groups of risks.

It does not seek to prevent risk taking. It aims to establish an understanding of the risk exposure’s implications and establish tolerable thresholds that guide the business to optimize risks-returns.

Implicit Risk Appetite Explicit Risk Appetite

Implied statement of acceptable risk taking or behaviour by an organization in the pursuit of its corporate objectives

Statement that is explicitly defined by the organisation and used internally to management and monitoring purpose

RISK APPETITE OVERVIEW

3 0

RISK ADJUSTED RETURN ON CAPITAL (RAROC)

Introduction to RAROC - Components

RAROC best practice is to adjust net income for expected losses due to credit risk and adjust capital for unexpected losses due to risks

Risk-Adjusted Return

Risk-Adjusted CapitalRAROC=

Net Interest Income

Interest income

Funds chargeInterestexpense

Funds credit

Non Interest Income

Non Interest Expense

Direct

Indirect

Overhead

Taxes

Expected Loss

(for credit risk)

Earnings on Capital

Risk-AdjustedProfit & Loss

Capital allocated for unexpected losses

Risk-AdjustedCapital

Credit Risk Market Risk

Operational Risk

Other Risks

3 1

LINKING RAROC TO VALUE

BU 1

20 % 15 % 10 %

BU 2 BU 3

Total BankHurdle Rate = 15%1

Capital allocated according to risk, with an expectation of meeting or exceeding the hurdle rate 400m 600m 1000m

20m 0 <50m>RAROCEcon. Profit2 ($)

Application of RAROC

♦ Creates a level playing field that supports identification of value (e.g. economic profit), when compared against the bank-wide hurdle rate, or the minimum return expected by shareholders

♦ Enables better understanding of where capital should beallocated and the associated returns, contributing to decision making

♦ Provides a uniform and comparable measure of the risk-adjusted rate of return across all lines of business or products, enabling relative rankings for performance evaluation

Hurdle Rate = 15%+5%

-5%

“Value adding”

“Value destroying”

Econ. Profit ($)

ILLUSTRATIVE

1 In this simplified example the hurdle rate for each business is assumed to be the same as the overall hurdle rate for the bank

2 Economic Profit = (RAROC - Hurdle Rate) x Allocated Capital

BASEL II – PILLAR 3 MARKET DISCIPLINE OVERVIEW

3 3

CONCEPTUAL OVERVIEW

Guiding Principles

u Complements Pillars 1 and 2

u Should be consistent with how senior officers actually manage risks in the bank

Achieving appropriate disclosure

u Pillar 3 helps give supervisors a level playing field for disclosure, but actual implementation is left to country supervisors

Interaction with Account Disclosures

u Similar to, but different from, accounting disclosures – Pillar 3 has a narrower scope of capital adequacy reporting

u Location of disclosure is not specified – but management must try to keep all disclosure in same place

3 4

CONCEPTUAL OVERVIEW (CONTINUED)

Banks must decide whether the information is material – but there is guidance on what information is material

Frequency of disclosure

u Mostly on semi-annual basis

u Risk Policies etc. on an Annual basis

u Large international banks must disclose on quarterly basis

Proprietary and confidential information

u Banks should determine which information is proprietary before disclosure – issue of discussion with supervisor

u E.g. Methodologies, parameter estimates etc.

This presentation and content are property of BlackIce Enterprise Risk Management Inc. and may not be reproduced or copied without express consent.

BlackIce Enterprise Risk Management Inc.#310 – 207 West Hastings St.Vancouver BC, Canada V6B 1H7

Visit Us at www.blackiceinc.comContact at [email protected]