barclays americas select franchise conference 2013 - sallie mae

TRANSCRIPT

Barclays Americas Select Franchise Conference May 22, 2013

2

Forward-Looking Statements; Non-GAAP Financial Measures

The following information is current as of May 13, 2013 (unless otherwise noted) and should be read in connection with SLM Corporation’s Annual Report on Form 10-K for the year ended December 31, 2012

(the “2012 Form 10-K”), and subsequent reports filed with the Securities and Exchange Commission (the “SEC”). Definitions for capitalized terms in this presentation not defined herein can be found in the 2012

Form 10-K (filed with the SEC on February 26, 2013).

This Presentation contains forward-looking statements and information based on management’s current expectations as of the date of this presentation. Statements that are not historical facts, including

statements about our opinions, beliefs or expectations and statements that assume or are dependent upon future events, are forward-looking statements. Forward-looking statements are subject to risks,

uncertainties, assumptions and other factors that may cause actual results to be materially different from those reflected in such forward-looking statements. These factors include, among others, the risks and

uncertainties set forth in Item 1A “Risk Factors” and elsewhere in the 2012 Form 10-K, the Company’s first quarter Form 10-Q and subsequent filings with the SEC; increases in financing costs; limits on liquidity;

increases in costs associated with compliance with laws and regulations; changes in accounting standards and the impact of related changes in significant accounting estimates; any adverse outcomes in any

significant litigation to which we are a party; credit risk associated with our exposure to third parties, including counterparties to our derivative transactions; and changes in the terms of student loans and the

educational credit marketplace (including changes resulting from new laws and the implementation of existing laws). We could also be affected by, among other things: changes in our funding costs and

availability; reductions to our credit ratings or the credit ratings of the United States of America; failures of our operating systems or infrastructure, including those of third-party vendors; damage to our reputation;

failures to successfully implement cost-cutting and restructuring initiatives and adverse effects of such initiatives on our business; changes in the demand for educational financing or in financing preferences of

lenders, educational institutions, students and their families; changes in law and regulations with respect to the student lending business and financial institutions generally; increased competition from banks and

other consumer lenders; the creditworthiness of our customers; changes in the general interest rate environment, including the rate relationships among relevant money-market instruments and those of our

earning assets versus our funding arrangements; changes in general economic conditions; our ability to successfully effectuate any acquisitions and other strategic initiatives; and changes in the demand for debt

management services. The preparation of our consolidated financial statements also requires management to make certain estimates and assumptions including estimates and assumptions about future events.

These estimates or assumptions may prove to be incorrect. All forward-looking statements contained in this Presentation are qualified by these cautionary statements and are made only as of the date of this

Presentation. We do not undertake any obligation to update or revise these forward-looking statements to conform the statement to actual results or changes in our expectations.

The Company reports financial results on a GAAP basis and also provides certain core earnings performance measures. The difference between the Company’s core earnings and GAAP results for the periods

presented were the unrealized, mark-to-market gains/losses on derivative contracts and the goodwill and acquired intangible asset amortization and impairment. These items are recognized in GAAP but not in

core earnings results. The Company provides core earnings measures because this is what management uses when making management decisions regarding the Company’s performance and the allocation of

corporate resources. The Company’s core earnings are not defined terms within GAAP and may not be comparable to similarly titled measures reported by other companies. For additional information, see

“Core Earnings — Definition and Limitations” in the Company’s first quarter Form 10-Q for a further discussion and a complete reconciliation between GAAP net income and core earnings.

3

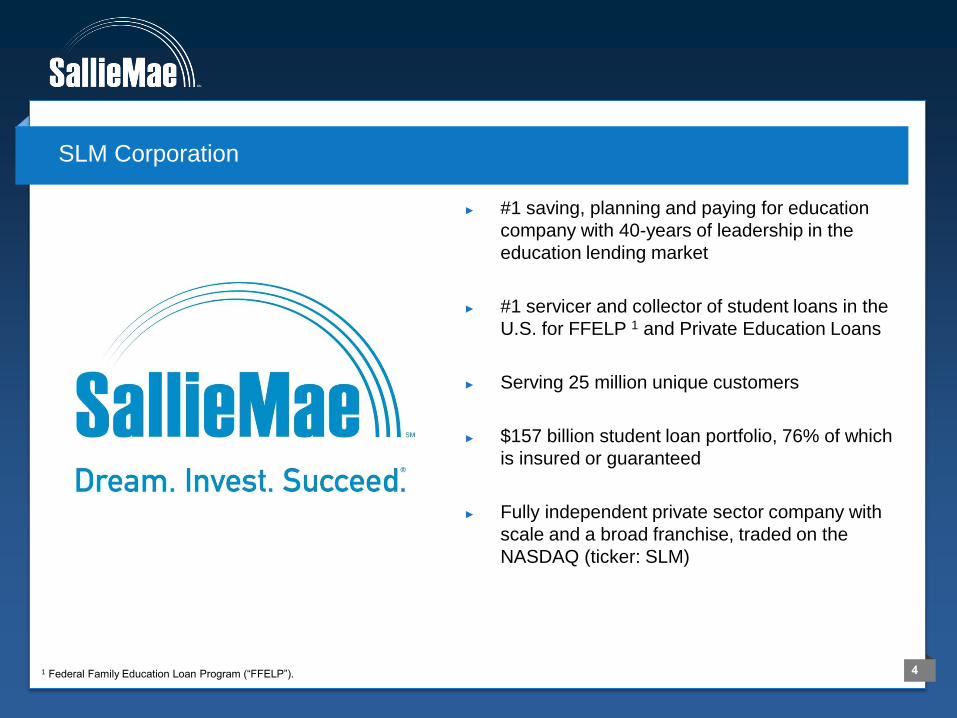

SLM Corporation Overview

4

► #1 saving, planning and paying for education

company with 40-years of leadership in the

education lending market

► #1 servicer and collector of student loans in the

U.S. for FFELP 1 and Private Education Loans

► Serving 25 million unique customers

► $157 billion student loan portfolio, 76% of which

is insured or guaranteed

► Fully independent private sector company with

scale and a broad franchise, traded on the

NASDAQ (ticker: SLM)

SLM Corporation

1 Federal Family Education Loan Program (“FFELP”).

5

Two Businesses

Legacy Business (as of 12/31/12)

FFELP Loans $124

Private Loans 31

Total $155

Intrinsic value: $22++ per share

$ in billions, except per share amounts (1) 2013 pro forma loan balance based on 2013 loan originations in excess of $4 billion (2) EPS Contribution based on approximately 450 million shares outstanding

Private Credit Growth Business (2013 Pro Forma)(1)

Estimated Average Balance of

Smart Option Loans

$10 Billion

ROA 2.4%

Capital 12 – 15%

ROE 16 – 20%

Growth 20%++

Est. 2013 EPS Contribution (2) $0.55

6

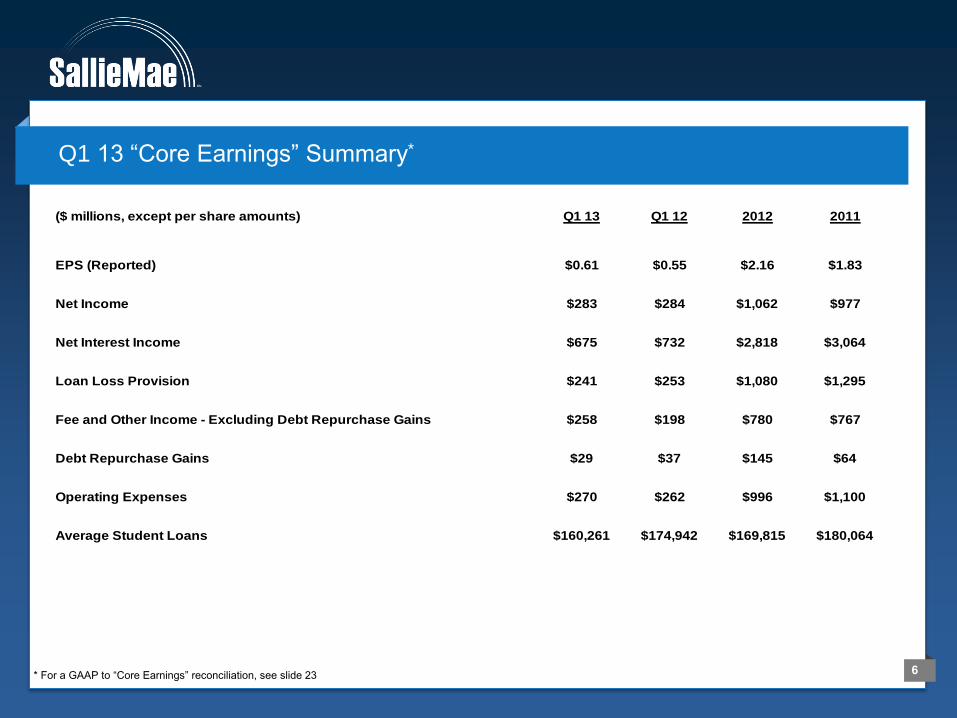

Q1 13 “Core Earnings” Summary*

* For a GAAP to “Core Earnings” reconciliation, see slide 23

($ millions, except per share amounts) Q1 13 Q1 12 2012 2011

EPS (Reported) $0.61 $0.55 $2.16 $1.83

Net Income $283 $284 $1,062 $977

Net Interest Income $675 $732 $2,818 $3,064

Loan Loss Provision $241 $253 $1,080 $1,295

Fee and Other Income - Excluding Debt Repurchase Gains $258 $198 $780 $767

Debt Repurchase Gains $29 $37 $145 $64

Operating Expenses $270 $262 $996 $1,100

Average Student Loans $160,261 $174,942 $169,815 $180,064

7

► Estimates for academic year 2011-12 project that 21 million students will enroll in higher education and incur costs of over $436 billion; $7 billion of which is funded by private education loans

► Private Education Loan products bridge the funding gap between the cost of a college education and funds available through U.S. Department of Education (ED) programs, grants, and other sources

Role of Private Education Loans

Source: Trends in College Pricing.© 2012 The College Board,. www.collegeboard.org,

U.S. Department of Education 2012

Cost of College (Based on a Four-Year Term) Total Cost of Education (in billions)

2011/2012 Academic Year

$113

$116

$200

$7

Federal

Family Contributions

Grants

Private Education

Loans

Source: U.S. Department of Education, President’s 2013 Budget & Company analysis

$17,125 $17,125 $27,000 $27,000

$78,299

$19,003

$124,884

$41,544

Full-TimePrivate School

Full-TimePublic School

Full-TimePrivate School

Full-TimePublic School

ED Lending Limit Cost of attendance gap

Cost of

attendance

gap

Cost of

attendance

gap

AY 2001-2002 AY 2011-2012

$95,424

$36,128

$151,884

$68,544

8

► 2011-12 academic year market share approximately 47%

Private Education Loan Industry Originations

Source: Trends in Student Aid.© 2012 The College Board,. www.collegeboard.org, industry data is preliminary. Based on current dollars. Data reported by academic year, SLM quarterly data converted to academic year basis.

► Private Education Loan originations declined from their peak as a result of an increase in federal student loan limits, an overall increase in the use of federal student loans, an increase in federal grants, and tighter underwriting standards.

$3.8 $4.8

$7.1 $7.7 $7.7

$4.8

$2.3 $2.5 $3.0

$11.6

$15.5

$18.5

$21.1 $22.9

$10.6

$7.1 $6.2 $6.4

03-04 04-05 05-06 06-07 07-08 08-09 09-10 10-11 11-12

SLM vs. Industry Originations (billions)

SLM Total Market

9

Low Risk = Smart Option, Legacy Traditional Cosigned, and Law/MBA/MED/CT/Other

Moderate Risk = Legacy Traditional Non-Cosigned

Elevated Risk = Non-Traditional

Consumer Lending Segment – High Quality Portfolio

10

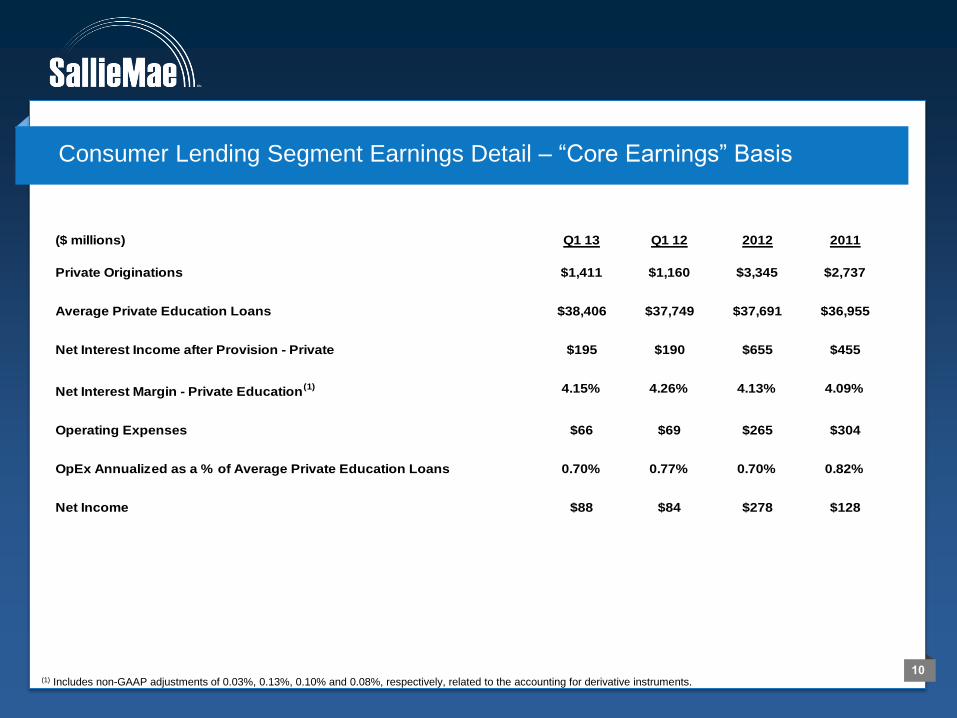

Consumer Lending Segment Earnings Detail – “Core Earnings” Basis

($ millions) Q1 13 Q1 12 2012 2011

Private Originations $1,411 $1,160 $3,345 $2,737

Average Private Education Loans $38,406 $37,749 $37,691 $36,955

Net Interest Income after Provision - Private $195 $190 $655 $455

Net Interest Margin - Private Education(1) 4.15% 4.26% 4.13% 4.09%

Operating Expenses $66 $69 $265 $304

OpEx Annualized as a % of Average Private Education Loans 0.70% 0.77% 0.70% 0.82%

Net Income $88 $84 $278 $128

(1) Includes non-GAAP adjustments of 0.03%, 0.13%, 0.10% and 0.08%, respectively, related to the accounting for derivative instruments.

11

FFELP Loan Segment Earnings Detail – “Core Earnings” Basis

($ millions) Q1 13 Q1 12 2012 2011

Average FFELP Loans $121,855 $137,193 $132,124 $143,109

Net Interest Income after Provision - FFELP $245 $286 $1,092 $1,361

Net Interest Margin - FFELP(1) 0.83% 0.85% 0.84% 0.98%

Operating Expenses $157 $185 $702 $760

OpEx Annualized as a % of Average FFELP Loans 0.52% 0.53% 0.53% 0.53%

Net Income $104 $80 $307 $434

(1)Includes non-GAAP adjustments of (0.40%), (0.27%), (0.31%) and (0.34%), respectively, related to the accounting for derivative instruments.

12

Business Services Segment – “Core Earnings” Basis

(in millions) Q1 13 Q4 12 Q1 12

Net Income $124 $134 $137

Servicing Revenue $212 $218 $236

Contingency Revenue $99 $95 $90

Department of Education Accounts Serviced 4.8 4.3 3.7

13

Funding Diversity and Liquidity

14

FFELP

► Issued $2.5 billion of FFELP ABS

► Sold residual interest in two FFELP securitization trusts totaling $5.8 billion of assets

► Refinanced $787 million of FFELP reset rate notes to term

Private Credit

► Issued $2.5 billion of Private ABS

Unsecured Debt

► Issued $1.5 billion of long term unsecured debt

► Repurchased $800 million of outstanding debt through tender offers

Capital Management

► Returned nearly $200 million to shareholders through share repurchases(1)

► Maintained excess capital at Bank and SLM Corporation

2013 Capital Markets Summary

(1) As of March 31, 2013.

15

Non-Consolidation FFELP Non-Consolidation FFELP Consolidation FFELP

Issue $1,246M SLM Trust 2013-2 $1,249M SLM Trust 2013-1 $1,527M SLM Trust 2012-8

Pricing Date April 3, 2013 February 5, 2013 December 13, 2012

Collateral US Govt. Guaranteed or Insured

FFELP Stafford and Plus Loans

US Govt. Guaranteed or Insured

FFELP Stafford and Plus Loans

US Govt. Guaranteed or Insured

FFELP Consolidation Loans

Prepayment

Speed (1) 6% Constant Prepayment Rate 6% Constant Prepayment Rate 4% Constant Prepayment Rate

Tranching

Moody’s Amt WAL(1) Pricing(2)

A Aaa $1,211 4.4 L+45

B Aa1 $35 8.8 L+210

Moody’s Amt WAL(1) Pricing(2)

A-1 Aaa $280 1.0 L+17

A-2 Aaa $396 3.3 L+25

A-3 Aaa $538 6.8 L+55

B A1 $35 8.6 L+225

Moody’s Amt WAL(1) Pricing(2)

A Aaa $1,485 7.8 L+90

B A1 $43 17.4 L+360

Recent SLM FFELP ABS Transactions

(1) Estimated based on a variety of assumptions concerning loan repayment behavior, as more fully described in the related prospectus, which may be obtained at

http://www2.salliemae.com/investors/debtasset/slmsltrusts/. Actual average life may vary significantly from estimates.

(2) Pricing represents the yield to expected call.

16

Projected Cash Flows From FFELP Portfolio*

Assumptions

No Floor Income, CPR/CDR = Stafford & Plus (4.0%), Consolidation (3.0%)

Excludes assets and excess spread associated with FFELP Trust 2006-2

* These projections are based on internal estimates and assumptions and are subject to ongoing review and modification. These projections may prove to be incorrect.

($ in Millions)

► Total Cash Flows from Projected Excess Spread = $8.8 Billion

► Total Cash Flows from Projected Servicing Revenues = $4.7 Billion

as of 3/31/13 2013 2014 2015 2016 2017 2018 2019 2020

Projected FFELP Average Balance $111,462 $103,233 $93,609 $84,153 $75,164 $66,443 $58,342 $50,786

Projected Excess Spread $701 $866 $793 $727 $807 $733 $661 $586

Projected Servicing Revenue $466 $579 $527 $477 $426 $374 $325 $279

Projected Total Revenue $1,167 $1,445 $1,320 $1,204 $1,232 $1,107 $985 $865

2021 2022 2023 2024 2025 2026 2027 2028 - 2033

Projected FFELP Average Balance $43,800 $37,404 $31,931 $27,454 $23,245 $19,234 $15,441 $6,246

Projected Excess Spread $517 $449 $364 $306 $275 $238 $202 $536

Projected Servicing Revenue $237 $198 $165 $141 $120 $100 $82 $206

Projected Total Revenue $754 $647 $528 $447 $396 $338 $284 $742

17

High Percentage of Student Loans Funded to Term

$157 Billion Student Loan Portfolio* as of March 31, 2013

* Gross loans, Numbers may not add due to rounding.

Funded to Term, $118 Bn

► FFELP Consolidation Term ABS, $70 Bn

► FFELP Non-Consolidation Term ABS, $28 Bn

► Private Term ABS, $20 Bn

Fixed Spread Liabilities, $25 Bn

Conduits, $14 Bn

► Straight A Conduit, $7 Bn

► FFELP ABCP Conduit & FHLB, $7 Bn

► Private ABCP Conduit, $0.4 Bn

18

$1.6

$2.5

$1.5 $2.3

$1.8

$2.8

$0.2

$1.6

$3.7

$0

$5

$10

As of March 31, 2013 (par value, $ in billions)

Note: Does not include Sallie Mae Bank or Subsidiary funding

► Total unsecured debt outstanding of $18.1 billion

Unsecured Debt Maturities

19

► Bank charter

– Utah based ILC regulated by FDIC and Utah Department of Financial Institutions (UDFI)

– Charter granted October 2005

► Current bank activity

– Total assets of $9.4 billion at March 31, 2013

– Originates Sallie Mae’s Private Education Loans

– Funded through affiliate, brokered and direct retail deposits

– 14.8% Total Risk-based Capital at March 31, 2013

– Dividends of $120 million paid 2013 YTD

► Deposit taking activities

– Deposits totaled $8.0 billion at March 31, 2013

• $5.1 billion Brokered Deposits

• $2.9 billion Direct Retail and other affiliate and non-affiliate Deposits

– Brokered Deposit term portfolio has a weighted average maturity of 21.1 months

– Total deposits increased by 29% over Q112 and 3% over Q412

Sallie Mae Bank

20

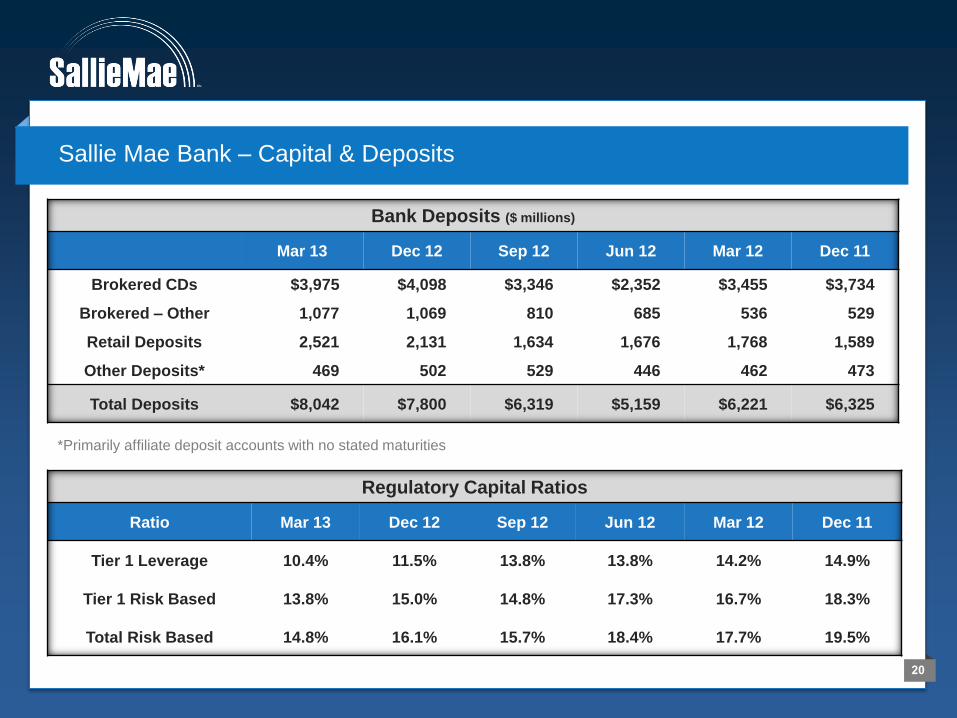

Sallie Mae Bank – Capital & Deposits

*Primarily affiliate deposit accounts with no stated maturities

Bank Deposits ($ millions)

Mar 13 Dec 12 Sep 12 Jun 12 Mar 12 Dec 11

Brokered CDs $3,975 $4,098 $3,346 $2,352 $3,455 $3,734

Brokered – Other 1,077 1,069 810 685 536 529

Retail Deposits 2,521 2,131 1,634 1,676 1,768 1,589

Other Deposits* 469 502 529 446 462 473

Total Deposits $8,042 $7,800 $6,319 $5,159 $6,221 $6,325

Regulatory Capital Ratios

Ratio Mar 13 Dec 12 Sep 12 Jun 12 Mar 12 Dec 11

Tier 1 Leverage 10.4% 11.5% 13.8% 13.8% 14.2% 14.9%

Tier 1 Risk Based 13.8% 15.0% 14.8% 17.3% 16.7% 18.3%

Total Risk Based 14.8% 16.1% 15.7% 18.4% 17.7% 19.5%

21

Q & A

22

Appendix

23

GAAP to “Core Earnings” Reconciliation

($ in millions, except per share amounts) Quarters Ended

March 31, 2013 December 31, 2012 March 31, 2012

Dollars Diluted EPS Dollars Diluted EPS Dollars Diluted EPS

GAAP net income 346$ $0.74 348$ $0.74 112$ $0.21

Adjustment from GAAP to "Core Earnings"

Net impact of derivative accounting (110) (128) 264

Net impact of goodwill and acquired intangible assets 4 14 5

Total "Core Earnings" Adjustments before net tax effect (106) (114) 269

Net tax effect 43 23 (97)

Total "Core Earnings" Adjustments (63) (91) 172

"Core Earnings" $283 $0.61 $257 $0.55 $284 $0.55