banks, retailers, and fintech: reimagining payments ... · er: er-ure 3 retailer-bank relationships...

TRANSCRIPT

BANKS, RETAILERS, AND FINTECH: REIMAGINING PAYMENTS RELATIONSHIPS PART TWO: THE RETAILER PERSPECTIVE

Zilvinas Bareisis and Gareth Lodge January 2016

CONTENTS

Introduction.......................................................................................................................... 1

Key Research Questions ................................................................................................. 2

Retailer-Bank Relationships Under Pressure ..................................................................... 3

Back to Basics: Why Retailers Still Need Banks................................................................. 7

What’s Changing? And Why? ......................................................................................... 9

Do Retailers Still Need Banks in the 21st Century? Emphatically Yes .............................. 11

All That Glitters May Not Be Gold ................................................................................. 11

Glancing to the Future ....................................................................................................... 13

Working Together Generates Better Value For All ........................................................ 13

In an Ecosystem, Successful Evolution Relies on All Parties ....................................... 13

Retailers Have Never Had It So Good! ......................................................................... 14

Leveraging Celent’s Expertise .......................................................................................... 15

Support for Financial Institutions ................................................................................... 15

Support for Vendors ...................................................................................................... 15

Related Celent Research .................................................................................................. 16

INTRODUCTION

Imagine a family of three generations:

Of the two kids, one is in her late teens, and another in his early 20s. They are full of energy, optimism, and youthful exuberance. Technology is second nature for them, although they sometimes find it difficult to connect with people in the “physical space.” While incredibly smart, the teens occasionally display a hint of naiveté about how the real world works. Unencumbered by the past, they have visions of changing that world and writing history themselves.

Their parents are in their late 40s. They are doing well and hold respectable jobs, but feel hassled and harried by the pressures of life, “keeping up with the Joneses” and particularly, the speed of change around them. They also hold a bit of a grudge against the older generation; they don’t think parents have done enough for them, having spent most of their life “in it for themselves.”

It is true, the grandparents are still fairly wealthy, but they also have bills to pay. Those bodies are starting to creak a bit; their grandkids call it “a legacy challenge.” They never had the best of memories, and these days often find that their “right hand doesn’t know what the left one is doing.” The rapidly changing world frightens them; they don’t want to become irrelevant, and secretly hope that it’s all a fad that will just go away.

There is a rich uncle who likes nothing more than to indulge the kids and throw money at their latest ideas. He knows that many of those ideas will come to no good, but the thought that one of them just might change the world keeps him coming back for more.

There is also a mean uncle who has taken on the mission to keep the family in check and make sure they don’t misbehave. He takes his role rather seriously and meddles quite a bit, although not always consistently. As a result, none of the family like him that much, and most think he is against them.

Now, replace the kids with Fintech, the parents with retailers, the grandparents with banks, the rich uncle with venture capital and private equity firms, and the mean uncle with a regulator, and read the text again. Sound familiar? Indeed, just like a family is locked into a set of relationships, banks, retailers, and Fintech form a payment ecosystem that we believe is more symbiotic than many would want to admit.

As merchants that sell goods, retailers care about accepting payments efficiently and effectively. As corporates, they also have various other needs, from physical cash management to borrowing money and paying suppliers. Retailers traditionally have relied on banks to provide many of those services, although the relationship has often been strained. The merchants have long argued that the cost of payment acceptance is too high, and the silos between the retail and corporate sides of the bank have not helped to present a full picture of the relationship. Not surprisingly, retailers are increasingly susceptible to alternative solutions offered by technology firms.

Retail banks have been responsible for most of the payment instruments issued to consumers and used at the merchant tills. As cheques declined, the growth in card payments has been remarkable, even though the use of cash remains at stubbornly high levels in most countries. Yet, it is corporate banks that have the main relationship with retailers, and even though both sides may belong to the same universal bank, they often operate in silos. If the bank is also an acquirer, those operations would typically be in yet another siloed unit.

Chapte

r: I

ntr

oduction

2

Fintech firms sense the opportunity and are trying to insert themselves in a variety of ways. What will their growing presence mean to the relationship between banks and retailers? Will it prove to be a wedge further driving them apart or the glue that bonds everyone together?

Figure 1: Banks, Retailers, and Fintech — A Symbiotic Ecosystem?

Source: Celent

We believe it is time to reimagine the payments relationships between banks, retailers, and Fintech. Combative stances and door slamming will only result in lost opportunities for all.

To reimagine those relationships, it is helpful to start by understanding the perspectives of each party. Therefore, we have written three reports, with each exploring the perspective of a different stakeholder. This report looks at retailers and examines three research questions.

KEY RESEARCH QUESTIONS

1 What is the current state of the retailer-bank relationship? 2 Why do retailers

need banks? 3 What does the future hold for the retailer-bank relationship?

Chapte

r: R

eta

iler-

Bank R

ela

tio

nship

s U

nd

er

Pre

ssure

3

RETAILER-BANK RELATIONSHIPS UNDER PRESSURE

Many years ago, the retailer/bank relationship was relatively straightforward. Both merchants and banks were much simpler organisations, existing in much simpler times. Today, however, much has changed, and it’s putting their relationship under pressure. Figure 2 highlights just a few of those changes.

Figure 2: Merchants Are Putting Banking Relationships Under Pressure

Source: Celent

Retailers Are Becoming More Sophisticated When banks set up their systems, they were often at the leading edge of technology. Swift, the network used for making cross-border payments, was pushing the boundaries of technology. However, as payments became increasingly seen as a utility, banks sought opportunities to reduce the cost in the value chain, not improve the value for all. As a result many banks’ payment systems are, at best, lagging the state of retailers’ systems, and in many cases ancient in comparison.

Retailers arguably have had to invest much more heavily in their IT. It’s not that they necessarily spend more; benchmarks suggest that banks often spend proportionally more on IT than many other industries. However, they have been facing an increase in the pace of change, particularly in channels and customer expectations. As a result, many retailers are becoming increasingly sophisticated in both their own skills and their requirements. A tipping point has been reached, with retailers continuing to evolve at a much faster pace than banks. This is one of the reasons that retailers have often turned to supply chain solutions such as GT Nexus or Hubwoo. Rather than being collections of financial products, solutions are designed around the procurement process. Banks today only sell what they build (which is limited to what they can deliver and support through their heritage technology), and these are typically packaged, point solutions. These new players are designed from the ground up around the end-to-end processes of a corporate, with APIs allowing the corporate to choose what services it takes, and how it integrates them.

Chapte

r: R

eta

iler-

Bank R

ela

tio

nship

s U

nd

er

Pre

ssure

4

Retailers Are Asserting Their Power The trend of retailers asserting themselves is perhaps no more evident than in the fees associated with accepting card transactions. Just about everywhere in the world, retailers are crying foul, claiming both that they are being overcharged and have been overcharged. In the UK, the British Retail Consortium state every year that they believe the cost of cards still to be too high,

1 going as far as to say:

“Cash remains the cheapest method of payment for retailers to process.”

There have been numerous examples of banks and bank-owned networks paying retailers substantial amounts of money for “historic overpayment of anti-competitive interchange fees.” In the UK in 2015, Tesco won $61 million from MasterCard, with at least 19 other cases still to be heard. In the US, Walmart launched a suit against Visa in 2014 for $5 billion, having pulled out of a wider class action which itself was settled for $5.7 billion.

Not only are the retailers taking a direct approach, they are also lobbying governments. The aforementioned British Retail Consortium is pushing the UK government hard to implement European interchange legislation immediately and save British retailers an estimated £480 million. In context, according to their estimates, that would be a halving of bank fees.

Regulators Seem to Be Siding with the Merchants Every business has to deal with regulation and laws, from tax to competition. Banks arguably have had more regulation than any other industry, particularly in the last 10 years. Although many of the regulations are designed to bring stability to the industry and to reduce risk, many interventions have been more structural in nature. For example, the Single Euro Payments Area (SEPA) was explicitly created to increase competition in the banking market. In particular, it created a common way of working for payments. In a SEPA country, corporates use the same payment message regardless of which country they are in, and receive the same basic levels of protection and service guarantee. As a result, instead of needing a bank in each country where the corporate operates, it just needs one, with the onus on that bank to be able to reach any other bank in Europe.

Furthermore, there are very obvious regulations and interventions around cards, from interchange reduction outlined above to the introduction of honour all cards. These are just the latest mandates being seen around the world; more are likely.

Greater Choice Is Increasing Competition for Retailers’ Business Based on the press from the last year, it would be easy to assume that banks were losing a war, and that Fintech companies, while perhaps not always going head-to-head with banks, are contributing to a rapid decline in their revenues. Changes on the horizon might accelerate that, with the Payment Services Directive 2 (PSD2) in Europe in particular set to radically change the landscape. With the Access to Account provisions (XS2A), any third party will be able to initiate a payment from a bank account. That opens up the payment market to a wide range of alternatives to the existing, primarily bank-owned, providers. While many banks have been assuming that third party will be a PayPal or other third party payment provider (TPP), there is nothing to stop that TPP being a retailer. A retailer can, on paper (the practicalities of it are evolving), initiate a payment directly from its shopper’s bank account, bypassing payment fees entirely.

Retailers Are Encroaching on Bank Territory In many markets around the world, retailers have gradually moved into the banking market. Some offer only “entry level” financial services, such as credit cards or packaged insurance products, while others now offer retail deposit accounts and mortgages.

1http://www.brc.org.uk/brc_news_detail.asp?id=2831

Chapte

r: R

eta

iler-

Bank R

ela

tio

nship

s U

nd

er

Pre

ssure

5

Two aspects of this trend are noteworthy.

First, while some of these services were originally joint ventures, with the retailer partnering with a bank, increasingly retailers are going alone, with their own banking licences. This has often been because the banks have been forced to pull out, such as the Tesco/Royal Bank of Scotland partnership. Even those entities without banking licences are starting to encroach on bank territory, and it’s not solely a retail phenomenon. The use of in-house banks by large multinational corporates is a good example. Instead of each subsidiary (and potentially branch) holding accounts at a local level, they hold them with a central entity. This entity manages the accounts overall, and can make and receive payments on their behalf (POBO and ROBO — payments on behalf of and receipts on behalf of). They are not replacing the bank, but they are displacing at least part of the revenue-generating activity a bank would have undertaken.

Second, it’s not just that the retailers are competing, but often are competing in different ways, and for different reasons. For example, retailers have driven the consumerisation of insurance products. In many supermarkets it’s now possible to pop a “packet” of pet insurance into your basket. In a hugely complex, risk-driven market, this simplification of the product, making it easy to sell and easy to buy, has made it hugely successful, with some supermarkets now among the largest insurers in the market. The same applies to other financial products. According to Tesco’s 2014 annual report, since launching mortgage products in 2012, they have underwritten more than £1 billion in mortgages.

Yet, while the revenue from the insurance and other financial product sales is welcome, it can be almost a secondary consideration. The primary goal is to build and maintain a relationship with the customer, and to drive them to interact with a retailer property, whether real or virtual. They're looking to drive retail sales and increase share of spending. As a result, many of the products feature the loyalty scheme of that retailer, for rewards that have to be accessed via the retailer. While banks also seek to drive the same customer loyalty, most banks aren’t as sophisticated as a retailer in being able to do so. Furthermore, the bank does not operate in quite the same way, with financial intermediaries and money comparison sites, for example, driving disloyalty in effect.

Retailers Are Displacing Banks Where They Can Even retailers that don’t have aspirations to enter what they consider to be financial services are still displacing banks. Some are seeking to create their own emerging payments solutions; for example, MCX is a consortium of large merchants in the US that has developed CurrentC, a mobile wallet in pilot in Columbus, OH. Some retailers are seeking to create their own solution; Walmart recently announced plans for Walmart Pay.

Others have tried to compete much more directly (e.g., Europe’s Payfair payment card scheme). In response to the European regulator’s call for a third card scheme in Europe, and one preferably with European roots, Payfair was set up very much positioned as a “retailer friendly” scheme. As the Celent report In Search of a Third European Card Scheme: Time to Move On points out, success is unlikely for any of the schemes vying to be that third scheme; yet the very fact that the founder of Payfair was a board-level employee of Carrefour, one of the largest retailers in the world, is significant.

It should be noted, though, that while they may be trying to displace banks, both MCX and Payfair have struggled. It may not be as simple as the retailers think.

Chapte

r: R

eta

iler-

Bank R

ela

tio

nship

s U

nd

er

Pre

ssure

6

At a glance, perhaps there is nothing new in any of the points raised above. Yet taken together, and plotting the past trajectory forward, it’s plain that the traditional relationship has been under strain for a while. Neither party seems happy; the banks feel under attack, while the retailers believe that they aren’t obtaining what they want from a bank. So what does a retailer want?

Key Research Question

1

What is the current state of the retailer-bank relationship?

The pace of change in retailing has meant that merchants have often evolved far quicker than

banks, and that comes with significant consequences for banking.

Chapte

r: B

ack to B

asic

s:

Why R

eta

ilers

Still

Nee

d B

an

ks

7

BACK TO BASICS: WHY RETAILERS STILL NEED BANKS

Given the pressure that banks are feeling, it would seem at first glance that banks need retailers more than retailers need banks. Indeed, listening to some Fintechs, more of whom shortly, it has been suggested that banks will be replaced altogether by these agile new players. That poses the question: why does a retailer still need a bank, and where feasibly might a Fintech replace them?

The answer lies in a number of areas.

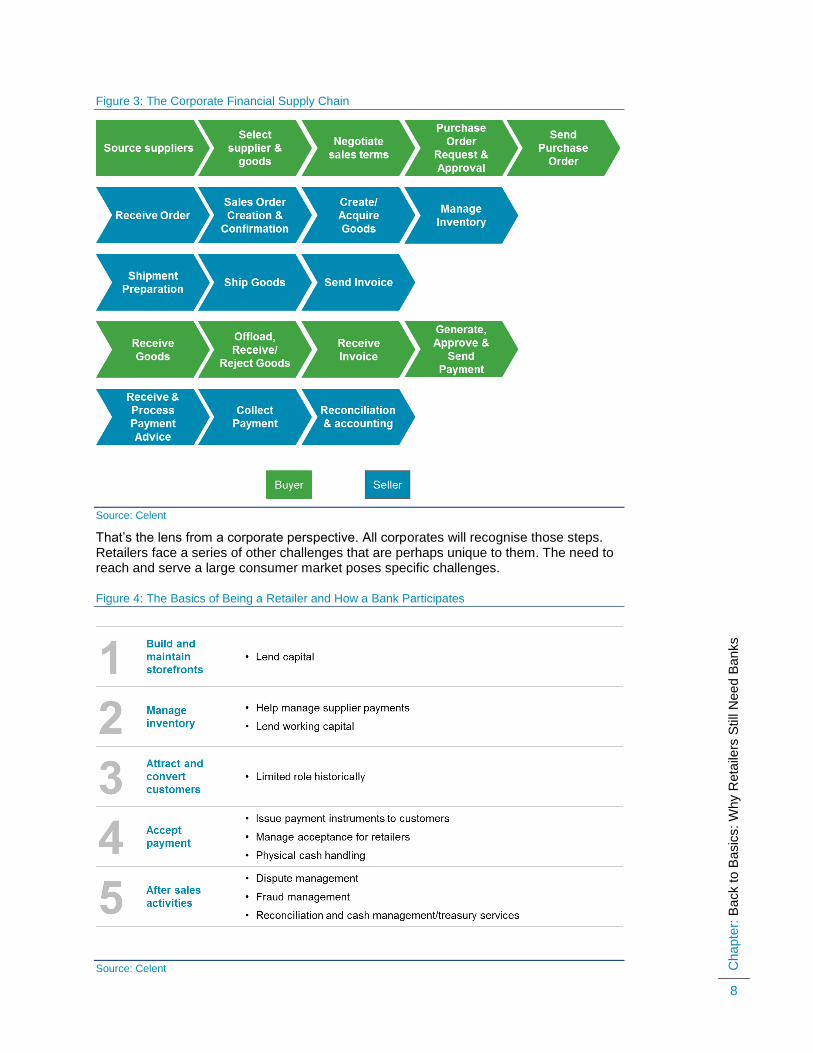

Fundamentally, all corporates have two parts to their financial operations: accounts payable (AP) and accounts receivable (AR). Given that they are intrinsically linked, there are functions that straddle both: liquidity management, cash forecasting, etc.

Even then, there are two distinct lenses that can be applied. Figure 3 shows a typical financial supply chain process. Payments are obviously a vital part of the supply chain, but they are virtually the last process in it, and banks are aware of this. At many points in the value chain, banks offer services — letters of credit, shipping insurance, invoice financing, etc. But few, if any, banks offer services in every step, nor do they integrate them across the value chain.

Key Research Question

2

Why do retailers need banks?

Retailers focus on managing the supply chain – banks play a vital role in the financial supply

chain for a retailer, including regulated activities a Fintech can’t supply.

Chapte

r: B

ack to B

asic

s: W

hy R

eta

ilers

Still

Nee

d B

an

ks

8

Figure 3: The Corporate Financial Supply Chain

Source: Celent

That’s the lens from a corporate perspective. All corporates will recognise those steps. Retailers face a series of other challenges that are perhaps unique to them. The need to reach and serve a large consumer market poses specific challenges.

Figure 4: The Basics of Being a Retailer and How a Bank Participates

Source: Celent

Chapte

r: B

ack to B

asic

s: W

hy R

eta

ilers

Still

Nee

d B

an

ks

9

Figure 4 shows a simplified view of the basics of being a retailer. It’s less a value chain and more a statement of how they operate. Broadly, a retailer needs a store (virtual or physical) that has goods to sell (requiring the acquisition and management of goods for sale). They then need to attract customers into the store and (hopefully!) accept the payment as a result of a sale, and finally manage anything that might happen when things don’t go as smoothly as planned.

As Figure 4 highlights, banks play a role in each of these areas, but have traditionally done little in the customer segment. One could argue that loyalty schemes for cards, such as a card issued by a retailer which offers greater rewards for using the card in specific stores. is the closest that many banks have achieved.

It should be noted that banks should also understand at least several aspects of this process — after all, running a branch network is retailing financial services products.

WHAT’S CHANGING? AND WHY? Now consider that same figure, but looking at how Fintechs fit in. As Figure 5 demonstrates, each stage has many, many potential alternatives to banks, whether it’s a service or a software solution designed to enable the retailer to undertake the activity. Fintechs typically focus on one aspect of the value chain, and, having been able to build from scratch using modern technology, many of them could be considered best in class in terms of their functionality. Traditionally, most banks have only been as good (or as bad!) as the next bank, which will have had similar issues. For example, when Metro Bank launched in the UK, it stated it was the first new bank in more than 100 years.

Figure 5: The Basics of Being a Retailer and How a Nonbank Can Service Them

Source: Celent

For a retailer then, it’s not just choice, but the fact that the choices now being offered in some cases are decades more advanced than what was being offered by the banks.

Chapte

r: B

ack to B

asic

s: W

hy R

eta

ilers

Still

Nee

d B

an

ks

10

This conundrum is something that puzzles many retailers. Given that this is the banks’ core business, how can they be so far behind?

What many merchants don’t realise is that, while they may have a single relationship with a bank, the products being provided are from an organisation that is far from integrated. The services highlighted in Figure 4 all come from different divisions within a bank. Indeed, in many cases, the product varies significantly within one of those divisions depending on channel, brand, or country. Take card issuance as an example. Debit cards, credit cards, and commercial cards usually fall in different divisions of the bank, not even sharing the same P&L line, let alone technology. The reasons for this are numerous, but are largely historical. Many banks have seen technology as a utility. That is, it is a tool and a means to an end. Given that banks were large, early adopters of technology, the systems they bought were leading edge — then. However, many banks have chosen to maintain the technology, rather than do large periodic overhauls. It’s too simplistic to describes the reason as “If it ain’t broke, don’t fix it,” but that is perhaps broadly true.

Second, many banks are a product of many years of mergers and acquisitions. The banks may have many core banking systems, but they’re likely to have even more dozens of overlapping payment systems. For example, Royal Bank of Scotland publicly stated

2 in 2014 that it had 80 payment systems, which they were seeking to rationalise to

around 10. Multiply those systems by the increasing number of channels, and it’s no wonder that banks don’t have a single, integrated service.

At face value, it would seem that the role of the bank is under severe threat. Not only are they not engineered to deliver the services the retailer wishes, but there are many entrants who are able. Does this spell the end of the need for banks?

2 http://www.computerweekly.com/news/2240215168/RBS-rationalises-IT-systems-to-improve-customer-

service-and-cut-costs

Chapte

r: D

o R

eta

ilers

Still

Need B

anks in t

he 2

1st C

entu

ry? E

mph

atically

Yes

11

DO RETAILERS STILL NEED BANKS IN THE 21ST CENTURY? EMPHATICALLY YES

Given the pressures outlined, the Fintechs waiting in the wings, and the difficulties for many banks to respond, it is not surprising that some might think banks are threatened. Indeed, it has become fashionable to pronounce that banks have no future, with several, such as TransferWise, actively stating in their advertising that banks rip clients off. An analogy that has been made is that this is a gold rush, with many Fintechs flooding to the market to seek their fortunes.

Celent does not subscribe to that school of thought. Doing so would risk ignoring the rich history of developments in banking, from the Medici family in the 14th century and beyond, and banks certainly are responding.

Of course, we acknowledge the disruption and recognise that banking is changing. We simply don’t agree that banks will disappear, at least not all of them, nor do we think that retailers actually want that.

What is clear is that the ecosystem is shifting. Ecosystems evolve, and every part of the ecosystem evolves, albeit at differing speeds. This section highlights why and how.

ALL THAT GLITTERS MAY NOT BE GOLD It’s worth noting the reality of what happens in a gold rush. It brings to mind a well-known saying: “All that glitters is not gold.” Something may look great but not actually be great. Celent believes this applies to Fintech. We believe that Fintech presents many opportunities and is undoubtedly shaping the future, yet it also poses some risks, including several in the short term. Although no one risk should stop a retailer using Fintech, the pitfalls are many and varied, and retailers should exercise caution.

For example, how much can retailers rely on Fintech firms, and on which ones? Technology barriers falling away has meant that there are generally few areas of financial services that don’t have multiple providers all competing for the same business, and with new ones springing up almost every day. As a result, the offerings are evolving rapidly as they respond to their competitors’ innovations. Therefore, how can a retailer be sure that they’re choosing the right vendor? While in some segments dominant players are emerging, they may not necessarily be the best ones.

Furthermore, given that many Fintechs have been in business less than three years, a question must be whether they will still be in business in a year’s time. It’s not just the size or age of the business that is the factor; many large, established businesses such as

Key Research Question

3

What does the future hold for the retailer-bank relationship?

Rather than being the end of banking, this is a pivotal moment to redefine the bank-retailer relationship for the better. Yet, retailers are

unlikely to need those banks which aren’t able to change.

Chapte

r: D

o R

eta

ilers

Still

Need B

anks in t

he 2

1st C

entu

ry? E

mph

atically

Yes

12

Verifone and Amazon have entered Fintech markets — and then left within a few years or less. An additional element is that many are so new and disruptive that they are seeking to disrupt business models as well.

There is also the more traditional risk. Are the entities regulated, and what is your redress should something go wrong? Many Fintech services are cheaper than banks because of the technology they use; equally, their lack of the burden of regulatory compliance plays a large part. Many Fintechs are highly aware of regulation, and actively seek to draw the boundaries around their services to ensure that they don’t move into regulated areas. This implies that there is an expectation that regulated bodies still exist in the ecosystem. Which in turn leads to the question: “Who will meet those requirements?”

The final point supports the belief that the new solutions may not necessarily be better. Technology novelty does not necessarily equate to superiority. After all, in many cases these new solutions are bound by some of the processes that already exist. Banking has existed for hundreds of years, with many processes that would be familiar to bankers from previous centuries. Here lie two truths.

First, for banking to work, processes have to be standardised and backwardly compatible. Banks are intermediaries, and so any change has to be applied to every party, across the entire value chain. Some customers are slow to change, and the bank is usually not able (for a range of reasons) to force the customer to change. It therefore must continue to accommodate the laggards while also meeting the needs of the early adopters.

Second, the processes have evolved to where they are today for a reason. There are a few examples where Fintechs imply they have a viable alternative, yet miss out vital parts of the value chain, making it unsuitable for certain types of transactions; or they require significant changes in the market for them to work. For example, a number of the blockchain use cases in cross-border payments only address part of the value chain. For a transaction of a few dollars, that costs a fraction of a comparable banking product, you may be willing to forgo the certainty of when the transaction is completed and the message saying that it’s been delivered. For a multi-million dollar transaction, with FX involved, those elements are suddenly absolutely critical.

Chapte

r: G

lancin

g to

the

Futu

re

13

GLANCING TO THE FUTURE

Many now realise that the only constant is change; yet many of those changes aren’t quite as unique as we may have first thought. While we talk about the impact that the Internet has had on bank branches, it equally has had an impact on retailers. And just as some banks see the opportunity, the Internet has transformed some retailers. Celent thinks then that Fintech, rather than the end of banking, is the trigger point for the next evolution of the banking industry.

WORKING TOGETHER GENERATES BETTER VALUE FOR ALL Fintechs are beginning to realise the benefits of working with banks, rather than trying to replace them. And banks realise the value Fintechs can bring, and are now figuring out ways to work with them. This is explored in the Fintech report in this series, but at its most simple, take blockchain. R3CEV is a consortium of banks (as at November 2015, 30 of the largest banks in the world) that are exploring blockchain’s potential. R3CEV is funded by banks but draws heavily on technology expertise from nonbanks, and is seeking to create standards for the use of blockchain. From the technology being little heard of until recently, this collaborative effort is likely to see it being used in mainstream banking in the very near future.

Working together therefore has potentially massive benefits. Examples of this practice with retailers already exist. Previously, “industry” standards were formed by banks and imposed on the industry. However, the emerging Nexo card standards in Europe are a good example of how a collaborative approach can bring significantly better results for all.

To date card standards have been designed with the card networks in mind – what information needs to flow to whom, where? ISO8583 is the dominant standard globally, but it has many variations where it has been adapted for local purposes. Over 200 variations exist in Europe alone. They may only be minor in many cases, but it does mean that the end-to-end process does differ country by country.

The need to standardise is clear. Yet the approach generated even further value. By extending the Nexo stakeholder group for the design process to retailers and others, the resulting standard is much better, and has clearer benefit to all parties. Research by the Nexo consortium

3 suggests that retailers will generate cost savings in excess of 20%,

reduce implementation time by at least four months and cut payment processing charges and POS terminal prices. Even the regulator is happy because it makes the market more efficient, but also allows greater competition.

IN AN ECOSYSTEM, SUCCESSFUL EVOLUTION RELIES ON ALL PARTIES Our assertion that banking is changing and that banks simply will not disappear is an important one. It is clear that banks have managed to retain nearly all the trust that customers have in them, with few actually switching banks. Some of it may be down to inertia, but much of it is built on relationships based on providing core services, safely and securely, over many years. Celent believes that the smartest banks are going to leverage those trusted relationships to stay relevant to their customers and expand a range of services which they are well placed to deliver, such as instant financial advice or identity management services.

Retailers need them to evolve. If they don’t, banks will become increasingly commoditized, or will choose which businesses to remain in. Just as a retailer will close

3http://www.cartes-bancaires.com/IMG/pdf/nexo_-_Press_Release_EDC_White_Paper_final_-2.pdf

Chapte

r: G

lancin

g to

the

Futu

re

14

an underperforming store or drop a line that isn’t selling, so might a bank. There is already evidence of this among some of the larger global transaction banks, as they reduce the products and countries that they serve. Furthermore, in some countries, banks have fired clients as they saw the potential risks of that client outweighing their profitability. Retailers need to ensure that banks remain relevant and motivated, yet ensuring mutual benefit.

Fintechs need the banks to evolve as well, given that they are reliant on someone to deliver those regulated services. A simple analogy illustrates the point. In the Californian Gold Rush of the nineteenth century, a few prospectors made their fame and fortune. It changed the landscape of America. Yet the organisations that really benefited provided the infrastructure and tools. As Mark Twain said:

“During the gold rush it’s a good time to be in the pick and shovel business.”

The payment rails in particular are the foundation for the Fintech Gold Rush. The majority of Fintechs use existing bank payment rails. ApplePay is currently an initiation device only for bank cards, running on card rails; PayPal uses ACH, cards, and real-time payment networks to deliver their services. Yet, would those Fintechs believe that the rails work exactly how they’d like them to? Probably not. Working more closely with the “shovel makers” means the Fintechs should get better shovels. Working with banks more closely will create better results for retailers and Fintechs too.

RETAILERS HAVE NEVER HAD IT SO GOOD! Retailers currently have the best of both worlds, and arguably have never had it so good on the whole. The fact that banking is changing — and recognises that it needs to change — presents a unique opportunity for retailers. By engaging with banks to build better and tighter relationships, they have the opportunity to help shape the bank of the future. In reality, all the members of the family outlined in the introduction have a role to play. It’s difficult to perceive the best outcome being achieved without most or all parties being involved.

Was this report useful to you? Please send any comments, questions, or suggestions for upcoming research topics to [email protected].

Chapte

r: L

evera

gin

g C

ele

nt’s E

xpert

ise

15

LEVERAGING CELENT’S EXPERTISE

If you found this report valuable, you might consider engaging with Celent for custom analysis and research. Our collective experience and the knowledge we gained while working on this report can help you streamline the creation, refinement, or execution of your strategies.

SUPPORT FOR FINANCIAL INSTITUTIONS Typical projects we support related to cards and payments include:

Vendor short listing and selection. We perform discovery specific to you and your business to better understand your unique needs. We then create and administer a custom RFI to selected vendors to assist you in making rapid and accurate vendor choices.

Business practice evaluations. We spend time evaluating your business processes, particularly in issuing, acquiring, and product development. Based on our knowledge of the market, we identify potential process or technology constraints and provide clear insights that will help you implement industry best practices.

IT and business strategy creation. We collect perspectives from your executive team, your front line business and IT staff, and your customers. We then analyze your current position, institutional capabilities, and technology against your goals. If necessary, we help you reformulate your technology and business plans to address short-term and long-term needs.

SUPPORT FOR VENDORS We provide services that help you refine your product and service offerings. Examples include:

Product and service strategy evaluation. We help you assess your market position in terms of functionality, technology, and services. Our strategy workshops will help you target the right customers and map your offerings to their needs.

Market messaging and collateral review. Based on our extensive experience with your potential clients, we assess your marketing and sales materials—including your website and any collateral.

Chapte

r: R

ela

ted C

ele

nt R

esearc

h

16

RELATED CELENT RESEARCH

Breaking the Payments Dam: External Forces Transforming the Payments Ecosystem

November 2015

Payments Tokenisation Evolution: Glancing into the Future October 2015

Top Trends in Retail Payments: A Year in Review. 2015 Edition January 2015

Defining a Digital Financial Institution: What “Digital” Means in Banking December 2014

Apple in Payments: What to Expect? March 2014

Copyright Notice

Prepared by

Celent, a division of Oliver Wyman, Inc.

Copyright © 2016 Celent, a division of Oliver Wyman, Inc. All rights reserved. This report may not be reproduced, copied or redistributed, in whole or in part, in any form or by any means, without the written permission of Celent, a division of Oliver Wyman (“Celent”) and Celent accepts no liability whatsoever for the actions of third parties in this respect. Celent and any third party content providers whose content is included in this report are the sole copyright owners of the content in this report. Any third party content in this report has been included by Celent with the permission of the relevant content owner. Any use of this report by any third party is strictly prohibited without a license expressly granted by Celent. Any use of third party content included in this report is strictly prohibited without the express permission of the relevant content owner This report is not intended for general circulation, nor is it to be used, reproduced, copied, quoted or distributed by third parties for any purpose other than those that may be set forth herein without the prior written permission of Celent. Neither all nor any part of the contents of this report, or any opinions expressed herein, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other public means of communications, without the prior written consent of Celent. Any violation of Celent’s rights in this report will be enforced to the fullest extent of the law, including the pursuit of monetary damages and injunctive relief in the event of any breach of the foregoing restrictions.

This report is not a substitute for tailored professional advice on how a specific financial institution should execute its strategy. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisers. Celent has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Information furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified, and no warranty is given as to the accuracy of such information. Public information and industry and statistical data, are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the information without further verification.

Celent disclaims any responsibility to update the information or conclusions in this report. Celent accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages.

There are no third party beneficiaries with respect to this report, and we accept no liability to any third party. The opinions expressed herein are valid only for the purpose stated herein and as of the date of this report.

No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or conditions, which occur subsequent to the date hereof.

For more information please contact [email protected] or:

Zilvinas Bareisis [email protected]

Gareth Lodge [email protected]

AMERICAS EUROPE ASIA

USA

200 Clarendon Street, 12th Floor Boston, MA 02116

Tel.: +1.617.262.3120 Fax: +1.617.262.3121

France

28, avenue Victor Hugo Paris Cedex 16 75783

Tel.: +33.1.73.04.46.20 Fax: +33.1.45.02.30.01

Japan

The Imperial Hotel Tower, 13th Floor 1-1-1 Uchisaiwai-cho Chiyoda-ku, Tokyo 100-0011

Tel: +81.3.3500.3023 Fax: +81.3.3500.3059

USA

1166 Avenue of the Americas New York, NY 10036

Tel.: +1.212.541.8100 Fax: +1.212.541.8957

United Kingdom

55 Baker Street London W1U 8EW

Tel.: +44.20.7333.8333 Fax: +44.20.7333.8334

China

Beijing Kerry Centre South Tower, 15th Floor 1 Guanghua Road Chaoyang, Beijing 100022

Tel: +86.10.8520.0350 Fax: +86.10.8520.0349

USA

Four Embarcadero Center, Suite 1100 San Francisco, CA 94111

Tel.: +1.415.743.7900 Fax: +1.415.743.7950

Italy

Galleria San Babila 4B Milan 20122

Tel.: +39.02.305.771 Fax: +39.02.303.040.44

China

Central Plaza, Level 26 18 Harbour Road, Wanchai Hong Kong

Tel.: +852.2982.1971 Fax: +852.2511.7540

Brazil

Av. Doutor Chucri Zaidan, 920 – 4º andar Market Place Tower I São Paulo SP 04578-903

Tel.: +55.11.5501.1100 Fax: +55.11.5501.1110

Canada

1981 McGill College Avenue Montréal, Québec H3A 3T5

Tel.: +1.514.499.0461

Spain

Paseo de la Castellana 216 Pl. 13 Madrid 28046

Tel.: +34.91.531.79.00 Fax: +34.91.531.79.09

Switzerland

Tessinerplatz 5 Zurich 8027

Tel.: +41.44.5533.333

Singapore

8 Marina View #09-07 Asia Square Tower 1 Singapore 018960

Tel.: +65.9168.3998 Fax: +65.6327.5406

South Korea

Youngpoong Building, 22nd Floor 33 Seorin-dong, Jongno-gu Seoul 110-752 Tel.: +82.10.3019.1417 Fax: +82.2.399.5534