banks ratio analysis

DESCRIPTION

Everest bank limitedTRANSCRIPT

CHAPTER - IINTRODUCTION

2.2 Background commercial bank

A bank is a commercial or state institution that provides financial services, including

issuing money in various forms, receiving deposits of money, lend money and

processing transactions and the creating of credit A commercial bank accepts deposits

from customers and in turn makes loans, even in excess of the deposits; a process

known as fractional-reserve banking. Some banks (called Banks of issue) issue

banknotes as legal tender. Many banks offer ancillary financial services to make

additional profit; for example, most banks also rent safe deposit boxes in their

branches. In other words, Bank is a financial institution, which accepts deposits from

the public and in turns advances loan by creating credit. Bank is a manufacturer, of

credit and machine fix facilitying exchanges bank are those financial organization that

offer credit;, saving and payment services and perform the widest range of financial

function of any firm in the economy.

A bank generates a profit from the differential between the level of interest it pays for

deposits and other sources of funds, and the level of interest it charges in its lending

activities. This difference is referred to as the spread between the cost of funds and the

loan interest rate.

According to US law “Any kind of business offering deposits subject to withdrawal

on demand and making loan of commercial or business nature is a bank.”

According to Geoffary Crowther, “A banker is a dealer in debt in his own and other

peoples; the banker business is them to take debt of other people to offer his own in

exchange and thereby to credit money.”

“The banker’s business is to take the debts of other people to offer his own exchange,

and thereby create money”. G. Crowther.

According to nature and function perform the bank are categories in to different types.

There are different types of bank are Central Bank, Commercial Bank, Development

Bank, joint Venture Bank and Cooperative Banks. Different types of banks are

established for different function to be done. According to the function, perform by

them it is categories in to different types. Central bank is the supreme bank in the

1

country. It keeps the monetary system stable in the country, provide loan to

government, control all the banks and financial institution registered in central bank,

and it issue notes and control credit of money.

Commercial banks are established to improve people’s economic welfare and facility,

provide loan to the commercial and industrial sector and to provide other banking

sector in the country. In the context of English banking system the term “joint stock

bank” and “commercial bank” are interchangeable. The joint venture bank, are those

banks, which are established under joint investment with the foreign investor. The

almost joint venture banks established in Nepal are commercial bank.

3.2 Definitions of commercial bank are as followings

“Commercial bank means a bank authorized to receive both demand and time

deposits, to engage in trust services, to issue letter of credit, to rent time deposits

boxes, and to provide similar services.” Black’s laws Dictionary.

“Commercial Bank means a bank which operates currency exchanges transactions,

accepts deposit, provide loans; perform dealings, relating to comers expert the banks

which have been specified for cooperative, agricultural, industry of similar other

specific objective.” Commercial Bank Act 2031.

In the context of Nepal, one of the developed sectors is banking sector. More investor

is attracted in the banking sector for the investment. The only stock exchange of

Nepal also shows the growth of financial sector. Banking sector plays leading role in

Nepal stock Exchange (NEPSE). The fluctuation in the price of share in banking

sector will bring fluctuation in overall NEPSE index.

Simply bank can be defined as a financial institution, which provides a host of

financial service beside taking deposits and making loan. Basically a bank is an

institution whose principle operations are concerned with the accumulation of the

temporarily idle money of the general public for the purpose of advancing to other for

expenditure.

The origin of the word ‘Bank’ is linked to Italian word ‘Banko’ which means a Bench, Latin

word “Benkus” Meaning a joint stock company, French word “Banque” meaning a bench and

England word ‘Bank’. Bank of Venice in Italy in 1157, which is regarded as the first modem

bank.

2

4.2 Development of Banking System

The history of bank is too long in the ancient period the function of bank is performed

by merchant, moneylender, and gold smith. Merchant used to exchange gold, silver and

valuable ornament. The receipt given by them are considering to be equivalent to amount

exchange. Moneylenders provide loan to borrower in terms of written repayment note with

extra amount. The goldsmith was the third ancestor of the modem banks. The goldsmith used

to give receipts, which were known as a goldsmith note.

The history of banking developed from established of Case de Giorgio in Genoa in 1148.

After that bath of Venice in 157, Bath of Barcelona in l40l. The modern banking started and

takes rapid speed of forming and functioning from 17th

century. Bank of Manila, bank of

Florence and Bank of Amsterdam was established in Holland. Bank of Hamburg was

established in Germany in 1610 and Bank of England was established in England.

BANK OF BARSILONA 1401

BANK OF GENOA 1407

BANK OF AMSTERDAM 1609

BANK OF ENGLAND 1694

BANK OF HINDUSTAN 1770

5.2 History and Development of Banking System in Nepal

In Nepalese context the development of banking sector is not too long. In the era of

the great hero King Pritivi Narayan Shaha the coin Mohar was used in his Name. In

1989 the “Taksar” the institution which used to issue coin was established. In ancient

time there was practice of taking and giving of loan for purpose of trade and other

various purposes.

In 1933 BS “Tejarat Adda” Was established in the reign of King Ranodip Singh. The

main purpose of the Adda was to provide loans to the government offices and the

people against the deposit of gold and silver. It has also established its branches

outside the Kathmandu valley.

Nepal bank limited is the first bank of Nepal. It was established 1937 AD which

marked the beginning of an era of formal banking in Nepal. Its initial authorized

capital was 10 million rupees and issued capital was 25 lakes, Paid up capital was 8

lakes and 42 thousand rupees, Which was established under the Nepal Rastra Bank

3

Act 1956 (2012 BS). After that in 2000 (2058 BS) Nepal Rastra Bank Act has been

revealed by parliament. There after government has established the Rastrya Banijaya

Bank and Agriculture Development Bank in 1966 (2022 BS) and 1968 (2024 BS)

respectively.

Up to 1983, the development of banking sector in Nepal is not satisfactory,

government give emphasis to new technology and capital transfer from the foreign

- country’. Thus some joint venture banks were established. The first joint venture

bank was Nepal Arab Bank Limited (NABIL) in 1985 (2041BS). After that many

commercial bank were established they are “Nepal Investment Bank” in 1985 (2042

BS), Standard Chartered Bank Limited in 1986 (2043 BS), “Himalayan Bank

Limited” in 1992 (2049BS), “Nepal SBI Bank Limited” in 1993 (2050BS), “Nepal

Bangladesh Bank Limited” in 1994 (2051 BS), “Everest Bank limited” in 1994 (2051

BS), “Bank of Kathmandu limited” in l994(2O5IBS), “Nepal Credit and Commerce

Bath” were established. Till the date there are 20 banks are in operation in Nepal

including Agriculture Development Bank Limited. Citizen International bank and

Global Bank Limited is the latest and youngest bank of Nepal.

6.2 Function of commercial Bank

Commercial bank is directly related to the people and institution. The commercial

banks are operating to gain profit although it helps to accelerate people and economic

welfare and facility, to provide loan to industry and commerce and to provide banking

service to the public and state. There are different functions performed by commercial

bank some of the function are as given as followings.

To Accept Deposit

Accepting deposit is the main function of commercial bank. Mainly three kind

of account are allows by the bank for accepting deposit. They are Current,

Saving and Fixed Account. People and institution can deposit their money in

any account as required. In current account interest is not given for deposits.

To provide loan

There are different kind of loan are provided by commercial bank like

Business loan, home loan, education loan, vehicle loan and other different type

of loan. Bank charges different interest rate for different type of loan.

4

To perform Agency function

Another function of commercial bank is agency function, carries the works for

its customer in the following ways.

Transfer the money from one place to another.

Payment of rent of the house premium of the insurance income tax etc

on the behalf of the customer.

General Utility Function

A commercial bank discharges the function of general utility which are as

following:

Exchange of foreign currency.

Issue of travelers’ cheque.

Providing information and other services.

To provide security for the valuables goods and documents by providing

locker system and providing economic and professional advice.

7.2 Introduction of Everest bank Limited

Everest bank limited (EBL) was establish in 1994 and stated its operations with a

view and objective of extending professionalized and efficient banking service to

various segment of the society. EBL joined hands with Punjab National Bank

(PNB), India as its joint venture partner in 1997. PNB is the largest sector Bank of

India having 110 years of banking history with more than 4600 branch office

allover India and is known for its strong systems and procedures and a distinct

work culture.

Drawing its strength from its joint venture partner, EBL has been steadily growing

in its size and operation ever since its inception and today it has establish itself as

a leading private sector bank of the nation, reckoned as one of the fastest growing

commercial bank of the country.

The bank paid-up capital has increased to Rs 1,03,04,67,300.00 against the

authorized capital of 1,25,00,00,000.00. The local Nepalese promoters hold 50%

5

share in the bank’s equity while 20% of the equity is contributed by joint venture

partner PNB whereas remaining 30% is held by the public.

The banks provides a wide range of banking facilities through a wide network of

41 branches covering all the 5 regions of the county and over more than 250

reputed correspondent banks across the global. All the branches are

interconnected through anywhere branch banking services (ABBS) facility which

enables its customers to do banking transitions from any of this branch in

respective of their having account in the other branch.

Being a pioneer in opening a representative office in New Delhi, India EBL has

successfully taken another historical step in the banking history of the county. Its

representative office facilities the remittance of Nepalese workers residing in India

by opening accounts from the identified branches of Joint Venture Partner, Panjab

National Bank, India and also attracts Indian remittance to Nepal.

EBL is playing a pivotal role in arranging remittance of funds to and India through

instant transfer facility in addition to the drafts thawing arrangement with 4600

branches of PNB allover India. The bank is also offering cash management

system for managing the funds from India from 250 locations of India. EBL in

order to help Nepalese citizens working abroad has entered into arrangements

with banks and finance companies in different countries which enables quick

remittance of funds by the Nepalese citizens in countries like UAE, Kuwait,

Bahrain, Qatar, Saudi Arabia, Malaysia, Singapore and UK.

Not to be left behind in technology advancement, a continuous review and

upgrading of the technology is undertaken for the convenience of its customers.

The bank has also introduced “EBL Debit Card”. The bank has more than 40

ATM machine all over the Nepal. The bank has tied up with Smart Choice

Technology (SCT) for ATM. The banks also provide 365 banking services from

New Road and New Baneshwor Branch. For providing banking services to remote

area, the bank has introduced branchless banking services named “FINO”.

Further, the bank has introduced the Bank on Wheel service from its Birtamod

Branch. Considering latest technology development, the bank has recently

launched Mobile Banking Facility and e-banking. For customer value added, the

bank has offering utility bill payment services for NTC postpaid and prepaid

6

mobile, UTL bill payment, QFX Cinema ticket booking, online ticket booking of

Yeti airlines.

Recognizing the value of offering a complete range of services not only to

corporate but also to individuals EBL has pioneered in the banking sectors in

extending various customer friendly products like home loan, education loan, flexi

loan, loan against future lease rentals and home equity loan ,car loan, loan against

shares and loan against insurance policies etc.

Serving the valued customers and the society for 16 years means knowing each

other better, building relationship, bonding as partners in progress and will

continue working with each other by meeting its customers expectations. Thus the

outstanding performance and the commitment to customer satisfaction have

earned us the reputation of being “THE NAME YOU CAN BANK UPON.”

8.2 Board of Directors

1) Mr. B.K. Shrestha Chairman

2) Mr. Ved Krishna Shrestha Director

3) Mr. Arun Man Sherchan Director

4) Mr. Dr. Hal Gopal baidhya Director

5) Mr. B.L Gupta Director

6) Mr. P.K. Mahapatra Director (CEO)

7) Mr. Muskan Shrestha Director

8) Mr. Shiv Saran K.C Director

1.8 Objective of Fieldwork

The main objectives of the study study are listed as followings:

Getting Information about deposit condition of EBL

To know about the saving scheme of EBL

1.9 Methodology used

While conducting this report d4ta.and other information collection it by methods.

Interview method

While preparing this report I used interview method. I communicated orally

and got information from the Branch Manager of Bhairahawa Branch of Mr.

Surendra Nath Shanna, Credit Officer Mr. Nabin Regmi and Operation Officer

Mr. Biswa Raj Shakya. They help me and cooperate with me. They provided

7

all necessary date & other valuable suggestions for this report. By the

internship period I knew the added facility of this bank & difference between

other banks. I got many information about the saving plan in which I have

prepared this report.

Field observation report

In the duration of writing this report, I observed different department &

sections to gain different information & facts, transaction activities& operation

methods of different department & unit.

1.10 Scheme of Everest Bank Limited

Organization has a two scheme

i) Deposit scheme

ii) Loan scheme

i) Deposit scheme

Under this scheme customer of Everest Bank Limited can deposit their money

safely with certain rate of interest. Everest Bank Limited provided different

saving scheme to the customer according to their need and requirements.

Different types of available saving scheme are shown below.

a) Fixed deposit

b) Saving deposit

c) Call deposit

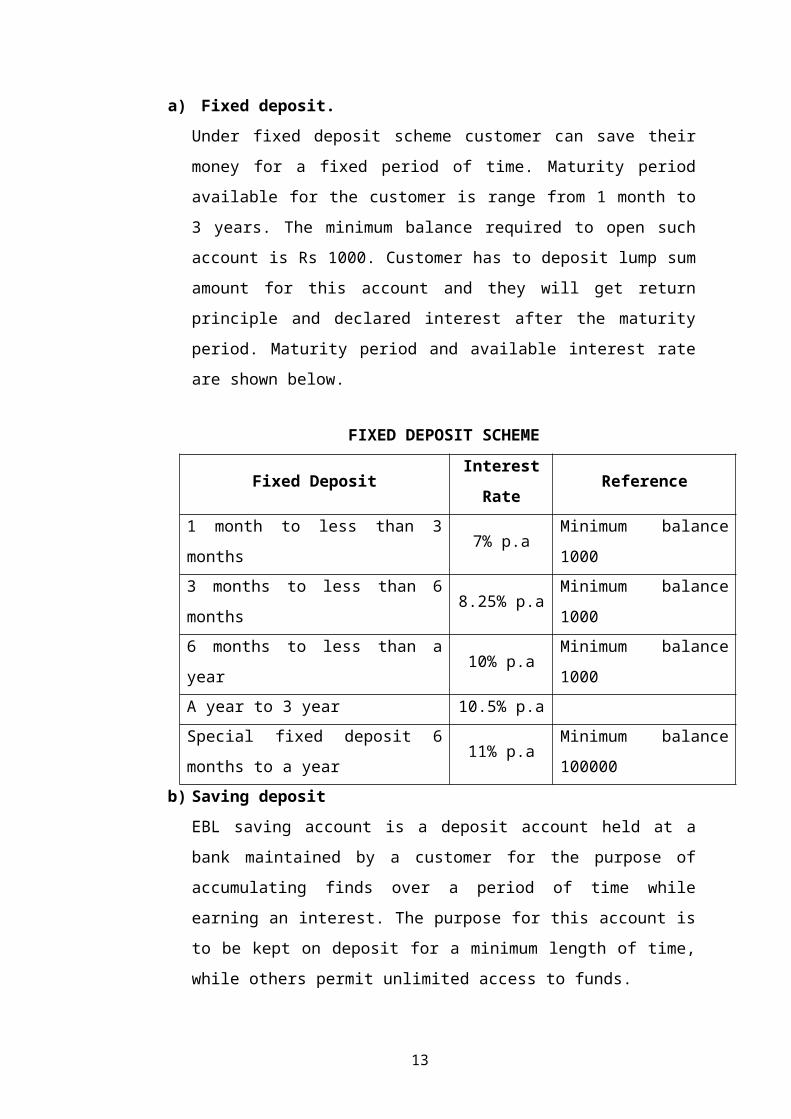

a) Fixed deposit.

Under fixed deposit scheme customer can save their money for a fixed period

of time. Maturity period available for the customer is range from 1 month to 3

years. The minimum balance required to open such account is Rs 1000.

Customer has to deposit lump sum amount for this account and they will get

return principle and declared interest after the maturity period. Maturity period

and available interest rate are shown below.

FIXED DEPOSIT SCHEME

Fixed DepositInterest

RateReference

1 month to less than 3 months 7% p.a Minimum balance 1000

3 months to less than 6 months 8.25% p.a Minimum balance 1000

8

6 months to less than a year 10% p.a Minimum balance 1000

A year to 3 year 10.5% p.a

Special fixed deposit 6 months to a year 11% p.a Minimum balance 100000

b) Saving deposit

EBL saving account is a deposit account held at a bank maintained by a

customer for the purpose of accumulating finds over a period of time while

earning an interest. The purpose for this account is to be kept on deposit for a

minimum length of time, while others permit unlimited access to funds.

Saving account can be opened in NPR and for the Nepalese citizen and USD

for foreign citizens with valid password and job appointment letter. Nepalese

citizen who have foreign currency source of income they can open foreign currency

account.

Interest rate is calculated on Daily Closing balance and payable .on quarterly basis.

The main objective of such saving is to encourage and mobilize small and scattered

money. There is various kind of scheme under this deposit which is listed below.

i) Normal saving Deposit

ii) Special saving Deposit:

Super Saving

Saving Premium

Remit Saving

Student Saving account

Everest Narri Bachat

Everest Baal Bachat

i) Normal Saving Account

This account is specially design for those customers who have to maintain

regular saving and to those who wants to save small amount in a regular time

basis. They can save money in such account at any time during office hour of

the organization. Saving can be made daily, weekly, monthly or in a lump sum

basis. In daily saving customer gets 3% interest compounding daily balance.

Minimum amount required to open such account is Rs 500. EBL saving A/c

holder can enjoy the following benefits.

Free cheque Book

Free statement on demand

Unlimited Withdrawn

9

Evening counter facility

365 days banking

Pay bill Facility

I banking Facility

ii) Special Saving Deposits

Any customer can open this account with as per various minimum balance

determine by the bank. The customer can deposit their money in regular basis like

daily, monthly, or in lump sum basis. And withdrawn can be made with cheque.

The bank is providing 6 - 6.75% interest in this account. It is rare to find interest

rate in such kind of account. Special saving deposit includes the following

deposit, which is explaining below.

a) Super Saving

Any customer can open this account minimum balance of Rs 1,00,000.00

The account holder can get the better interest rate i.e. 6.5% which is

greater than the rate of normal saving account. The super saving account

holder enjoys the following facilities with Everest bank ltd.

Free cheque Book

Free statement on demand

Unlimited Withdrawn

Evening counter facility

365 days banking

Pay bill Facility

I banking Facility

Free ATM card

50% discounts annual locker charge.

Free any branch banking system

b) Saving Premium

Any customer can open this account but the minimum balance of this

account inside valley branch Rs 1,00,000.00 and outside the valley is Rs

50,000.00

The account holder can get the 6% interest with said account. The saving

premium account holder enjoys the following facilities with Everest bank

ltd.

Free cheque Book

10

Free statement on demand

Unlimited Withdrawn

Evening counter facility

365 days banking

Pay bill Facility

I banking Facility

Free ATM card

50% discounts annual locker charge

Free any branch banking system

Additional benefits.

Issuance of Everest Bank Saving Premium Card.

Exclusive Service for the Saving Fund Premium accounts holder.

No commission on Demand Draft up to Nrs. 1 lac in a month.

No Security deposit for locker facility.

For small lockers 50% discount and if it is not available 15%

discount on other lockers.

Personal Accidental Death Insurance for Rs. 3 lac.

c) Remit Saving

With the inception of carrying out remittance activities, the bank

joined hands with various exchange companies especially in the

Middle East due to higher concentration of Nepalese in these areas.

Identifying the ever increasing volume of remittance from the

Middle East and equally prospering informal channels of remitting

hinds known as Hundi, EBL felt the need to take initiative to bring

remittance in to the official fold. With the aim EBL developed its

own web-based remittance product known as “Everest Remit” and

officially launched the same from UAE on 25th July 2006.

Currently EBE receives remittance payment from different

Exchanges house covering countries such as UAE, Quarter,

Bahrain, Malaysia and UK. From above exchange house the

customers can open the Remit saving account with minimum

balance of Rs 200.

The remit saving account holder able the withdrawn the deposited

11

amount after coming the concern branch or give debit authority to

relatives. The remit saving account holder enjoys the following

facilities with Everest Bank limited.

Free cheque Book

Free statement on demand

Unlimited Withdrawn

Evening counter facility

365 days banking

Pay bill Facility

I banking Facility

ATM Card

ABBS facilities

d) Student Saving Account

Over 30% of the population in Nepal is youngsters and most of them are

student. This product is target to the college and university student. The

minimum balance of this account is Rs 100. The student account holder

enjoys the following facilities with Everest bank ltd.

Free cheque Book

Free statement on demand

Unlimited Withdrawn

Evening counter facility

365 days banking

Pay bill Facility

I banking Facility

ATM Card free

ABBS facilities

e) Everest Naari Bachat

With the objective to encourage the small saving of women household

and professions the bank has introduced Naari Bachat Khata, where the

customer can make small saving and get the higher interest rate. The

minimum balance of this account is Rs 5,000.00 inside valley and Rs.

2500.00 outside valley.

The facility offer in this account is as under

Interest Rate: 6.75% p.a (Daily Balance Basis)

Issuance and renewal of Debit Card at NPR 50/-

Issuance of Free Cheque Book

12

Pay Bill Registration Facility

25% discount on Annual locker rent (Small Locker Only)

e-Banking (Internet Banking) service facility

Free cheque Book

Free statement on demand

Unlimited Withdrawn

Evening counter facility

365 days banking

f) Everest Bal Bachat

With the objective to make the children future secure, EBL

introduce Baal Bachat Kbata where the parents! Guardian makes

the saving in their children name and the bank pays higher interest

on this account. The minimum balance of this account is Rs

5000.00 inside valley and Rs, 2500.00 outside valley.

The facility offer in this account is as under

Interest Rate: 6.75% p.a (Daily Balance Basis)

Issuance and renewal of Debit Card at NPR 50/-

Issuance of Free Cheque Book

Pay Bill Registration Facility

25% discount on Annual locker rent (Small Locker Only)

e-Banking (Internet Banking) service facility

Free cheque Book

Free statement on demand

Unlimited Withdrawn

Evening counter facility

365 days banking

g) Call deposit

In deposit terminology the term call deposit refers to a specific

type of interest bearing investment account that allows a person to

withdraw their money from the account without penalty. In many

cases the money can be withdrawn from call deposit account

without prior notification to the bank.

A call deposit account holder allows the holder instant access to

their account and the ability to withdrawn their money at any time

13

without having to pay an early withdrawn penalty or inform the

bank in advance of their intention to withdraw their funds. A

person a call deposit account besides earning a favorable rate of

interest also has considerably more access to their money than

people with their money invested in other types of account. This

kind of account can be open by those customers who want to

maintain regular deposit and large amount. Saving can be made in

daily, monthly or in lump sum basis. The bank is providing annual

interest rate range between 7% to 10% according which is greater

than the rate of saving account.

iii) Loan scheme

This scheme is provided to those members or customer who wants loan

for different economic, education, agriculture, social and business

purposes. Bank charges certain interest in such kind of loan. And this

depends upon the nature of the loan. Bank has many varieties of loans

for customer according to their requirement. Only customer of company

can take a loan from the Bank also provides different suggestions

guidance to the member for their financial planning.

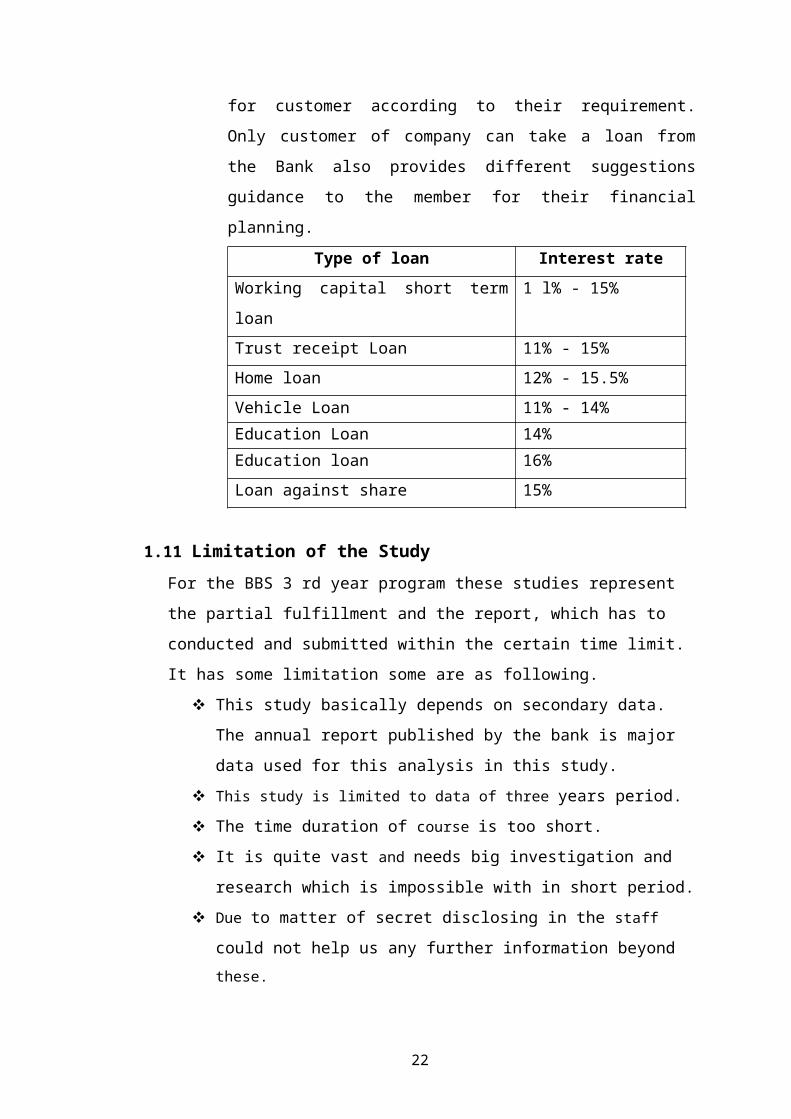

Type of loan Interest rate

Working capital short term loan 1 l% - 15%

Trust receipt Loan 11% - 15%

Home loan 12% - 15.5%

Vehicle Loan 11% - 14%

Education Loan 14%

Education loan 16%

Loan against share 15%

1.11 Limitation of the Study

For the BBS 3 rd year program these studies represent the partial fulfillment and

the report, which has to conducted and submitted within the certain time limit. It

has some limitation some are as following.

This study basically depends on secondary data. The annual report

published by the bank is major data used for this analysis in this study.

This study is limited to data of three years period.

The time duration of course is too short.

14

It is quite vast and needs big investigation and research which is

impossible with in short period.

Due to matter of secret disclosing in the staff could not help us any further

information beyond these.

CHAPTER – II

15

PRESENTATIONS AND ANALYSIS OF DATA

2.1 Presentation and Analysis of Fixed Deposit

Table 2.1 Year wise Fixed Deposit Position

Year Amount

2064/065 7049978230.00

2065/066 15061938201.00

2066/067 13007478505.00

Fig. 2.1 Year wise Fixed Deposit Position

2064/065 2065/066 2066/067 -

2,000,000,000.00 4,000,000,000.00 6,000,000,000.00 8,000,000,000.00

10,000,000,000.00 12,000,000,000.00 14,000,000,000.00 16,000,000,000.00

Fixed Deposit

Fixed Deposit

Analysis

We can clearly see that the fixed deposit trend is increasing year by year. A person

that means this scheme is attracting more and more customers. Since their

participation in this scheme is in increasing trend. Fixed deposit during year 065/066

has been increased by 9.37% and fixed deposit has increased by 19.33% in financial

year 066/067.

2.2 Presentation and Analysis of Saving Deposit

Table 2.2 Year wise Saving Deposit Position

Year Amount

2065/066 11883857171.00

2066/067 13039108920.00

2067/068 17269289330.00

Fig. 2.2 Year wise Saving Deposit Position

16

2064/065 2065/066 2066/067 -

2,000,000,000.00

4,000,000,000.00

6,000,000,000.00

8,000,000,000.00

10,000,000,000.00

12,000,000,000.00

14,000,000,000.00

16,000,000,000.00

Fixed Deposit

Fixed Deposit

Analysis

We can clearly see that money in saving deposit of the company is volatile. We can

see that saving Deposit from 2066/067 is increased by 24.39% and in financial year

2067/068, it was decreased by 9.62% due to the competition in banking sectors.

2.3 Presentation and Analysis of Call Deposit

Table 2.3 Year wise Call Deposit Position

Year Amount

2065/066 2780647781.00

2066/067 7550045393.00

2067/068 12952163592.00

Fig. 2.3 Year wise Call Deposit Position

2064/065 2065/066 2066/067 -

2,000,000,000.00

4,000,000,000.00

6,000,000,000.00

8,000,000,000.00

10,000,000,000.00

12,000,000,000.00

14,000,000,000.00

16,000,000,000.00

Fixed Deposit

Fixed Deposit

Analysis

17

The above chart and table clearly shows us how the call deposit scheme is attracting

the customer in the organization. Deposit in this account has been increased by

126.35% during year 066/067 and during year 067/068, deposit has been increased by

33.66% than previous year.

2.4 Presentation and Analysis of overall Deposit Scheme

Table 2.4: Amount of deposit collected in three different years

Deposit 2065/066 2066/067 2067/068

Fixed deposit 6446181289.00 15061938201.00 13007478505.00

Saving deposit 11883857171.00 13039108920.00 17269289330.00

Call deposit 2780647781.00 7550045393.00 12952163592.00

Fig. 2.4: Amount of deposit collected in three different years

2065/066 2066/067 2067/0680.00

2,000,000,000.00

4,000,000,000.00

6,000,000,000.00

8,000,000,000.00

10,000,000,000.00

12,000,000,000.00

14,000,000,000.00

16,000,000,000.00

18,000,000,000.00

20,000,000,000.00

Fixed depositSaving depositCall deposit

2.5 Study Result

After Studying about the topic we can say that BANKING BUSINEESS has been

growing BUT THE COMPETETION IS ALSO HIGH IN MARKET. And after

studying the saving scheme of this organization I come to the following conclusion.

The bank is offering various deposit schemes for attracting deposit from

various segment of society.

Deposit has been good in overall aspects.

It has been seen that saving in all scheme is not in parallel.

During studied period, the fixed deposit of the bank was increasing year by

year and it was due to offering higher interest rate.

18

During studied period, the saving deposit of the bank was increased in

2066/067. However; it was decreased in 2068/069 due to high competition in

banking market and entry of other financial player.

Saving in call deposit has been increasing trend but in recent years the growth rate

was decreased to 33.66% from 126.35%.

Best scheme for organization is saving deposit because this scheme is low cost for

the organization.

19

CHAPTER - III

SUMMARY, CONCLUSION AND RECOMMENDATION

3.1 Summary & Conclusion

The Everest bank limited has head office is Katmandu city but is covered the all f

region of all over the Nepal. It has been performing qualitative work from its starting

period. It has succeeded to develop its financial transaction and awarding the people

business man about the importance of saving. It has developed the utility of skills and

knowledge for those who have the skill and honesty by providing loan in a favorable

rate of interest. It has also provided employment opportunity to more the 650 person

directly, to do its transaction. It has helped its customer for saving, by provoking

different kinds of saving scheme with an attractive interest rate. Between bank and

financial institution it has established its own premises and good will. All the scheme

of this organization is attracting and motivating customer for saving.

Everest bank limited has succeeded to gather people from all the classes and level of

the society. In present, almost bank and financial companies are unable to reach the

financial sector of the small merchants and lower class in all over the Nepal. In this

situation this bank has taken policy to reach and give financial services to the people

of those classes and level in all over the nation and different types of programs have

been introduced to solve such problems. Over all, saving priority given by this

organization is appreciable. Its scheme is not sufficient to collect all the scattered

money in its area. Organization has to come with other attractive scheme in recent

future.

3.2 Recommendation

The Study discloses some weakness of Everest Bank Ltd. therefore the following

recommendation are submitted.

i) The bank should increase the interest rate in saving deposit to attract and to

inspire the customers to save theft find.

ii) Likewise other joint venture commercial bank, the main concentration of

Everest Bank Ltd. is limited to Kathmandu Valley and major cities like

Biratnagar, Birgunj and Butwal. However the major parts of Nepalese

people are livings in village or where they are highly exploited by Sahu and

Mahajans by manipulating principal amount the overall economic

development of the country is almost impossible until and unless the

20

programmers are matched with those people requirement. Therefore it is

suggested to them to expand its branches in rural areas for the economic

enlistment of poor people who live in villages.

iii) Though Everest Bank is formulating different new schemes but it is similar

to many other banks. Therefore it is recommended to them to formulate new

schemes which are unique & profitable for the customer.

4. Being a part of society, it has a great responsibility in the social

development; therefore it is recommended to Everest Bank Ltd. To

participate in social events such as in education, health programmed and

environment protection etc.

iv) Everest Bank is charging Anywhere Branch Banking Services (ABB 5)

commission to its customer which may distract the customer. Therefore it is

recommended to them not to take the service charge from the customer.

Bibliography

21

Bajracharya, B.C. (2061). Business Statistics.: M.K. Publishers & Distributors,

Kathmandu.

Dhital, Shristi. (2011). Deposit Scheme of Everest Bank Limited. Unpublished

Bachelor Reports, Tribhuvan University, Buddha Jyoti College.

Everest Bank Limited (2063/064-2068/069) Annual Report Bhairahawa, Everest

Bank Limited

Faculty of Management (2009). BBS: Courses of Study: Office of the Dean,

Faculty of Management, Tribhuvan University, Kathmandu.

Pant P.R. (2009), Social Science research & thesis writing (5th Ed): Buddha

Academic Enterprises, Kathmandu.

Paudel, B.R. Baral, J.K., Gautam, RAt & Rana, B.S. (2009). Corporate Finance

(5th ed.): Asmita Publications, Katbmandu.

Pradhan Radhe S. (2003). Research in Nepalese Finance: Buddha Academic

Publishers & Distributors Pvt. Ltd., Kathmandu.

Pradhan Surendra (1992). Basis of Financial Management: Educational

Enterprises Pvt. Ltd, Katbmandu.

Shrestha, M.K. Bhandari, D.B. (2007). Financial Markets & Institutions; Asniita

Publication, Kathmandu.

Thapa, K. (2007). Fundamentals of investment (5th ed): Asmita Books Publication,

Kathmandu.

22