banking services: problems and perspectives

TRANSCRIPT

BA

NK

ING

SE

RV

ICE

S: P

RO

BLE

MS A

ND

PE

RSPE

CT

IVE

S

BANKING SERVICES:

PROBLEMS AND PERSPECTIVES

BANKING SERVICES:

PROBLEMS AND PERSPECTIVES

Papers presented at the National Seminar organized by

THE TAMIL NADU DR.AMBEDKAR LAW UNIVERSITY

CHENNAI

Shri.A.K.Venkata Subramaniam Chair of Excellence on Consumer Law and Jurisprudence

with financial support from the

Ministry of Consumer Affairs, Food and Public Distribution

(Department of Consumer Affairs), Government of India

on

23rd and 24th December, 2018.

BANKING SERVICES:

PROBLEMS AND PERSPECTIVES

Patron

Prof.(Dr.) T.S.N. Sastry

Vice-Chancellor

The Tamil Nadu Dr.Ambedkar Law University,

Chennai.

Chief Editors

Thiru. R. Santhanam, Honorary Director

Dr. Ranjit Oommen Abraham, Project Director

Associate Editors

Thiru.R. Karuppasamy, Project Manager

Tmt. Deepa Manickam, Assistant Professor

Thiru.V. Anandha Kumar, Research Associate

Published By

SHRI.A.K.VENKATA SUBRAMANIAM, CHAIR OF EXCELLENCE ON CONSUMER LAW AND JURISPRUDENCE (CECLJ),

THE TAMIL NADU DR. AMBEDKAR LAW UNIVERSITY, CHENNAI.

Funded by

MINISTRY OF CONSUMER AFFAIRS, FOOD AND PUBLIC DISTRIBUTION (Department of Consumer Affairs), GOVT. OF INDIA.

Year of Publication : 2019

ISBN No : 978-93-87882-83-6

Typeset and Aligned by:

A. Komathi, Junior Assistant, CECLJ, TNDALU.

©All Rights Reserved

Views expressed in these papers are the original views of the Authors. The

Editors are no way responsible for the authenticity of the facts or the contents

of the papers. Meticulous care has been taken in preparing this book to avoid

error. For subscription or any feedback, please write to us at

No part of the publication may be reproduced, stored in a retrieval system or

transmitted in any form or by any names, whether electronic, mechanical,

photocopying, recording or otherwise without prior permission of the Editors

and the Publisher.

PREFACE

In the context of economic liberalisation and globalisation,

various reforms in banking sectors have been introduced from time to

time in India to improve the operational efficiency and promote the

health and financial soundness of banks and make them achieve

internationally accepted standards of performance. Internet and mobile

banking, new products such as investment advisory services, cash

management services, tax advisory services etc. have increased the

popularity of banks. But there are a few problems that have been

plaguing the banking sector in our country- the problem of non-

performing assets (NPAs), the increasing number of bank frauds, the

threat of cybercrimes, the perception that banks cater more .to the

corporate houses and the urban elite than address the problems of the

rural poor etc. In this context the role of RBI as the regulator vis-à-vis

the Government’s policies has also come under public scrutiny.

The Banking Regulation Act 1949, which regulates all banking

firms in India, also gives RBI the power to regulate, control and inspect

all Indian Banks. Does the Act need a relook in the light of the

developments that have taken place in the banking sector in recent

years? To what extent has the Prevention of Money Laundering Act

2002 helped in tackling this serious problem? Do the provisions of the

Consumer Protection Act 1986 and the Information Technology Act

2000 have enough teeth to redress the grievances of consumers with

regard to banking services? These and other issues were discussed

threadbare at the two-day National Seminar on “Banking Services:

Problems and Perspectives” organized by the Shri.A.K.Venkata

Subramaniam Chair of Excellence on Consumer Law and Jurisprudence

of the Tamil Nadu Dr.Ambedkar Law University, Chennai on 23rd and

24th December, 2018 in which academicians, bank officials, consumer

related NGOs, research scholars and students participated.

Papers were invited on the following themes: (i) e-Banking and

the consumer (ii) Banking services - A SWOT analysis (iii) New trends

in bank-customer relationships (iv) Changing dimensions in loans and

advances (v) Money laundering as a major issue (vi) Privacy Issues in

Banking Transactions (vii) Efficient ways of controlling frauds in the

banking sector (viii) Non-performing assets (NPS) and ways to reduce

them. (ix) Do banking laws need major reforms? (x) Issues in e-wallet

(xi) Grievance redressal mechanism in banking sector and (xii) Role of

RBI in regulating banks. There was excellent response and about 80

papers on the above themes were presented over two days.

Some of the papers presented at the seminar have been edited and

selected for publication in this volume under the following sections:

Section-I : New trends in Banking.

Section-II : e-Banking and related issues.

Section-III : Grievance Redressal Mechanism in the Banking

Sector.

Section-IV : Banking Laws and Reforms.

Section-V : Prevention of Frauds in Banks.

Section-VI : Role of RBI in Regulating Banks.

We thank Prof. (Dr).T.S.N. Sastry, Vice-Chancellor of the

University for his guidance and support in organising the seminar and

bringing out the publication.

The editors record their deep sense of gratitude to the Hon’ble

Thiru Justice V.Ramasubramanian, Judge, Andhra Pradesh &

Telengana High Court for his insightful inaugural address at the

seminar and to Prof.(Dr).A.Rajendra Prasad, former Vice Chancellor,

Acharya Nagarjuna University, Guntur, Andhra Pradesh for his

thought provoking valedictory address. The Editors wish to thank the

contributors of the papers for their enthusiastic response. The views

expressed in the papers are of the respective authors only. The Editors

are no way responsible for the authenticity of facts or the contents of the

articles. We hope the readers will find this publication useful and

relevant.

Chennai

21.05.2019. Editors

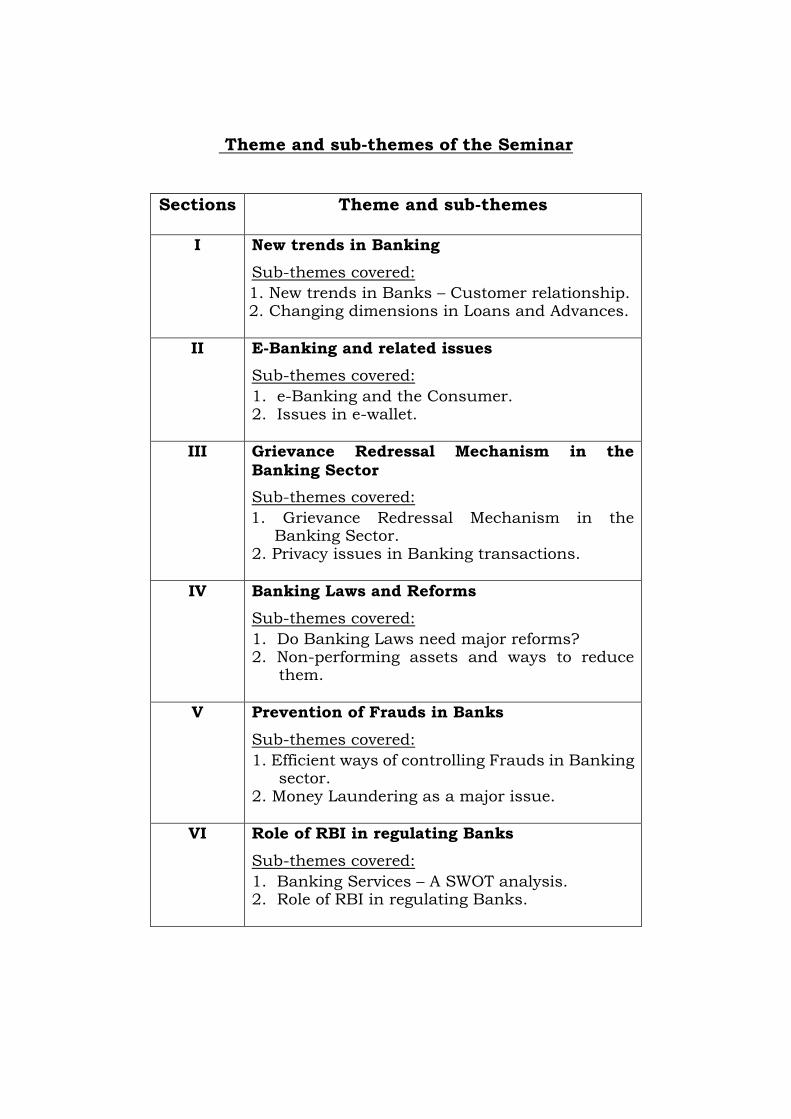

Theme and sub-themes of the Seminar

Sections Theme and sub-themes

I New trends in Banking

Sub-themes covered:

1. New trends in Banks – Customer relationship. 2. Changing dimensions in Loans and Advances.

II E-Banking and related issues

Sub-themes covered:

1. e-Banking and the Consumer. 2. Issues in e-wallet.

III Grievance Redressal Mechanism in the

Banking Sector

Sub-themes covered:

1. Grievance Redressal Mechanism in the Banking Sector.

2. Privacy issues in Banking transactions.

IV Banking Laws and Reforms

Sub-themes covered:

1. Do Banking Laws need major reforms? 2. Non-performing assets and ways to reduce

them.

V Prevention of Frauds in Banks

Sub-themes covered:

1. Efficient ways of controlling Frauds in Banking sector.

2. Money Laundering as a major issue.

VI Role of RBI in regulating Banks

Sub-themes covered:

1. Banking Services – A SWOT analysis. 2. Role of RBI in regulating Banks.

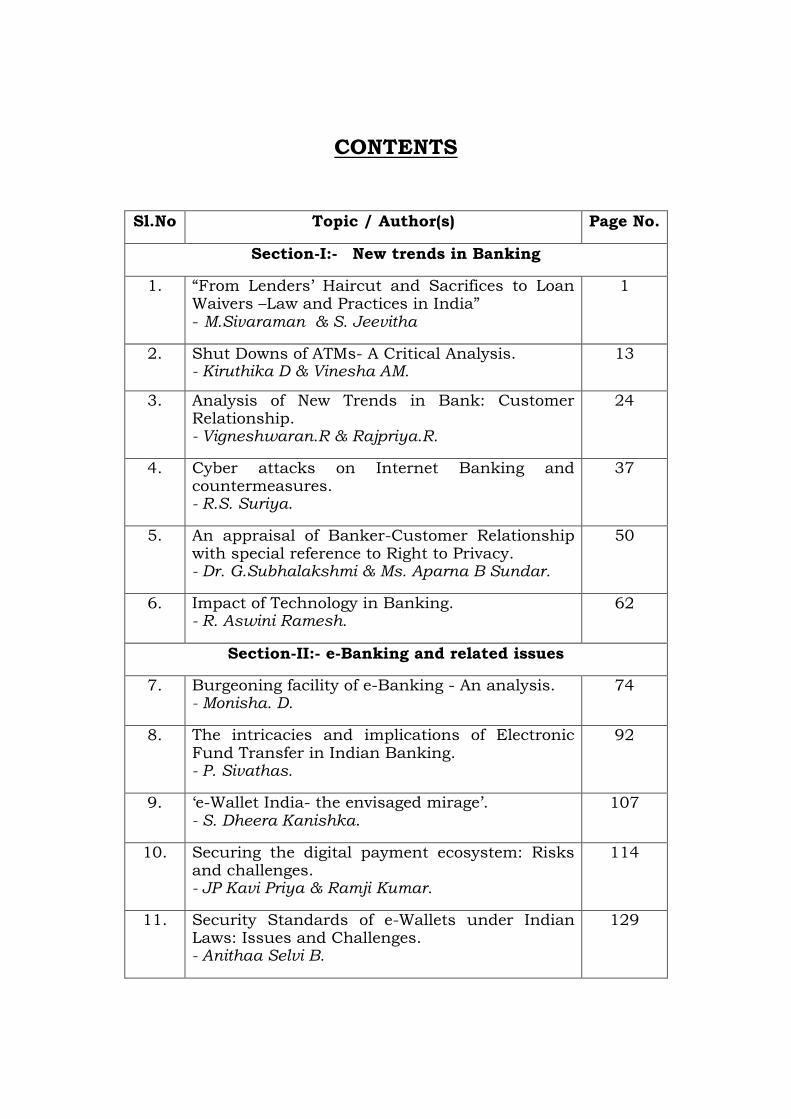

CONTENTS

Sl.No Topic / Author(s) Page No.

Section-I:- New trends in Banking

1. “From Lenders’ Haircut and Sacrifices to Loan Waivers –Law and Practices in India” - M.Sivaraman & S. Jeevitha

1

2. Shut Downs of ATMs- A Critical Analysis. - Kiruthika D & Vinesha AM.

13

3. Analysis of New Trends in Bank: Customer Relationship. - Vigneshwaran.R & Rajpriya.R.

24

4. Cyber attacks on Internet Banking and countermeasures. - R.S. Suriya.

37

5. An appraisal of Banker-Customer Relationship with special reference to Right to Privacy. - Dr. G.Subhalakshmi & Ms. Aparna B Sundar.

50

6. Impact of Technology in Banking. - R. Aswini Ramesh.

62

Section-II:- e-Banking and related issues

7. Burgeoning facility of e-Banking - An analysis. - Monisha. D.

74

8. The intricacies and implications of Electronic Fund Transfer in Indian Banking. - P. Sivathas.

92

9. ‘e-Wallet India- the envisaged mirage’. - S. Dheera Kanishka.

107

10. Securing the digital payment ecosystem: Risks and challenges. - JP Kavi Priya & Ramji Kumar.

114

11. Security Standards of e-Wallets under Indian Laws: Issues and Challenges. - Anithaa Selvi B.

129

Section-III:- Grievance Redressal Mechanism in the Banking

Sector

12. Grievance Redressal Mechanism in Banks. - Sanjay Pinto.

138

13. Grievance Redressal Mechanism in Banking Sector.

- Kumaresh .S.

153

14. Privacy issues in Banking Transactions – A Comparative Analysis. - U Shraddha Bhatt & Sreedevi Anand Nadig.

164

15. e-Banking: Security and Privacy Regulatory Environment. - R. Aswin & R.S. Bharathi.

175

16. Flaws in e-Banking – A prey to cyber hunters. - R.B. Rishabh & B. Yamuna Saraswathy.

188

17. Consumer Protection Act and Bank’s Liability – An Analysis. - J. James Jayapaul.

200

18. Privacy in Banking Transactions. - Yuvasree. P.

208

Section-IV:- Banking Laws and Reforms

19. “Crypto currencies - Indian Legal and Regulatory Nemesis” - M. Sivaraman & S. Jeevitha.

216

20. Legality of the “Naming and Shaming” Strategy Adopted by Banks Against Individual and Corporate Defaulters: Can the Bank Defame its Own Customers on the Ground of Wilful Defaults? - S. Mohammed Azaad.

225

21. Non-performing Assets and Measures to reduce it.

- Gadde Shareesh.

243

22. Digital India – A need for a Comprehensive Legal Code. - Bagavathy Vennimalai.

259

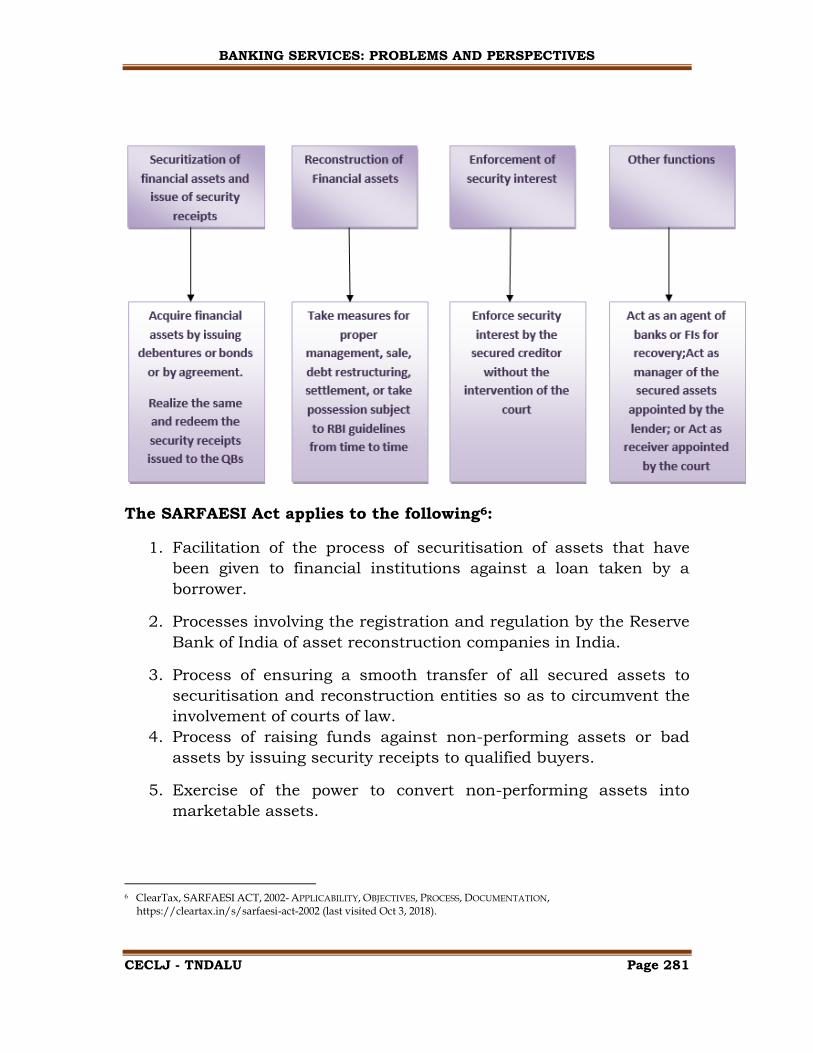

23. SARFAESI Act, 2002 – An overview. - Shreya Devaki.

275

Section-V:- Prevention of Frauds in Banks

24. Fugitive Economic Offenders Act, 2018 – A Critical analysis. - Balaji A.P.

286

25. Efficient ways to control fraud in Banking Sector. - Nivedha.P & Nandhini.P.

299

26. Analysis of Fugitive Economic Offender’s Act 2018 - A Stringent Step to curb Frauds. - Thraptthi Perumal.

318

27. Insurance Industry: An unexplored route to Money Laundering. - Gauri Sood.

329

28. Types of Bank fraud and some preventive measures.

- Divya. K.

342

Section-VI:- Role of RBI in regulating Banks

29. Role of RBI in Regulating Banks. - K. Hari Priya & A. Lavanya.

357

30. RBI and its Role in Regulating Banks. - Ashirwad J. & Sobin Shaji.

367

31. SWOT Analysis. - R. Ajay.

380

32. Overregulation of Banks and Under Regulation of NPA: A Cause for Bank Mergers in India. - Dr. Fincy Pallissery & Mr. Ronak V. Chhabria.

387

Section-I

New trends in Banking

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 1

“FROM LENDERS’ HAIRCUT AND SACRIFICES TO LOAN WAIVERS –

LAW AND PRACTICES IN INDIA”

M. SIVARAMAN &

S. JEEVITHA

ABSTRACT:

Banks and lenders have always enjoyed discretion to either postpone

and/or scale down their recoveries of bad loan accounts. When the

loan repayments hit roadblocks arising out of genuine circumstances,

lenders have often permitted moratorium against recovery and even

took haircuts and sacrifices on their principal and interest receivables

with a view to reviving and rehabilitating the lenders. Traditionally,

under the voluntary route the lenders have acted through the non-

statutory mechanisms such as One Time Settlement, Roll Over,

Corporate Debt Restructuring, Strategic Debt Restructuring and

Sustainable Structuring of Stressed Assets schemes, until February

2018 when the Reserve Bank of India abolished such restructuring

schemes. Involuntarily, the banks were also, from time to time, enjoined

by popular governments to enforce crop loan and cooperative loan

waivers. In terms of statutorily recognized schemes envisaged by the

Sick Industrial Companies Act, Insolvency legislations and the

SARFAESI Act, the lenders are permitted to take haircuts and make

sacrifices in the loan recovery. In recent times, under the Insolvency

and Bankruptcy Code, the financial creditors end up making huge

sacrifices of the loans owed by corporate entities which are admitted

into Corporate Insolvency Resolution Process.

This paper critically examines the legal and regulatory challenges

associated with such loan waivers, sacrifices and haircuts. The relevant

international practices on this subject and the judicial pronouncements

on this subject will also be discussed.

Ph.D Scholar, The Tamil Nadu Dr. Ambedkar Law University, Chennai. II year B.A., LL.B (Hons), VIT School of Law, Chennai.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 2

General Obligations of Lenders towards Borrowers:

Once loan application is received and sanctioned for the

borrower, if the lender delays or refuses to actually disburse the loan

sanctioned, it can be compelled for specific performance of the contract

even through a writ court1 and banks may also end up in paying

damages and specific performance to release the sanctioned loan2.

Timely release of sanctioned loans is also one of their paramount

obligations3. Proper and correct statements of the loan accounts should

be rendered by the banks towards the borrowers4. Banks are to extend

fair, reasonable and non-discriminatory treatment to their borrowers5.

Excessive interest charging by lenders in violation of the Fair Practices

Code6 cannot be condoned or ignored by the Reserve Bank of India

(“RBI”) and in any case they cannot charge interests over interests7. Re-

scheduling or offering rehabilitation package to the borrowers has now

become well recognized and entrenched in our fiscal policy and law.

Banks and lenders cannot pursue plural remedies against their

borrowers8. They are under a duty to respond to the representations

received from the borrowers9. They can also be fastened by the

borrowers with counter-claims10. Any action taken by lenders for

attachment and sale of the secured assets cannot extinguish the right

of redemption vested with the borrowers11 which could remain open

until sale is completed through registration12. Even then, a borrower

may still challenge the auction sale on the basis that it did not fetch the

best possible deal vis-à-vis the one offered for settlement by the

borrower13. They should ensure that best possible price is realized for

1 Gujarat State Finance Corporation v. M/s. Lotus Hotels Pvt. Ltd. AIR 1983 SC 848 2 Indian Bank v. ABS Marine MANU/SC/2046/2006 : AIR2006SC1899 3 Mahesh Chandra v. Regional Manager, UP Financial Corporation AIR 1993 SC 935 4 Central Bank of India v. Ravindra & Ors. AIR 2001 SC 3095 5 See Gujarat State Finance Corporation v. M/s. Lotus Hotels Pvt. Ltd. AIR 1983 SC 848, Mahesh Chandra v. Regional Manager,

UP Financial Corporation AIR 1993 SC 935; State Financial Corpn. v. M/s. Jagdamba Oil Mills AIR 2002 SC 834; 6 A. R.Jeyarhuthran vs. The Union of India and Ors legalcrystal.com/1171472 decided on November 14, 2014 7 Central Bank of India v. Ravindra & Ors. AIR 2001 SC 3095 8 A.P. State Financial Corporation v. M/s. GAR Re-Rolling Mills AIR 1994 SC 2151 9 Maharashtra State Finance Corporation v. M/s. Suvarna Board Mills AIR 1994 SC 2657 and Mardia Chemicals Ltd. and Ors.

vs. the Union of India and Ors. 2004 SOL Case No.298 10 M.E. Industries Pvt. Ltd. v. Banaras State Bank Ltd. AIR 2000 All 181 11 Ganga Dhar v. Shankar Lal : [1959] 1 SCR 509; Maganlal v. M/s. Jaiswal Industries, Neemach AIR 1989 SC 2113 12 Mathew Varghese vs. M. Amritha Kumar and Ors. MANU/SC/0114/2014 13 Chairman and Managing Director, SIPCOT, Madras v. Contromix Pvt. Ltd. AIR 1995 SC 1632

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 3

the assets of the borrowers secured with them when they are sold14.

They cannot retain excess monies which remain with them after

satisfaction of all claims due by the borrowers and ought to return the

excess to the borrowers15. They cannot use strong-arm tactics and

forcibly recover the loans16and may even stand to face criminal

prosecution for such practices17. They cannot declare borrowers as

‘willful defaulters’ without following the due process of law18. They have

no escape and are obliged to act on the guidelines of RBI in extending

OTS in a non-discriminatory fashion, provided the borrower’s case falls

within the guidelines issued by RBI19. Banks can seek recompense only

if the assets released through OTS are sold by the borrowers within

three years of such settlement and there is no restriction for the

borrowers in raising money by creating third party interest over such

assets without selling the same20.

The various statutory prescriptions, judicial pronouncements and

practices as highlighted above have seriously constrained the ability of

the banks and lenders to recover their loan receivables and have not

only led to the mounting of Non-Performing Assets (“NPA”), but, have

also jeopardized and eroded the capital adequacy of the banks and

financial institutions in India. Some of the means and mechanisms

through which banks and lenders invariably end up in NPAs and suffer

capital erosion are illustrated below.

Roll-over of Loans and Ever-greening:

Roll-over of loans is a legitimate process when the lender agrees

to extend the period of loan repayment of a borrower’s account for bona

fide business difficulties. However, ever-greening is an invidious

practice adopted by some banks to sanction fresh loans so as to settle

14 See J. Rajiv Subramaniyan and Ors. vs. Pandiyas and Ors. (14.03.2014 - SC) : MANU/SC/0207/2014 and Vasu P. Shetty

vs. Hotel Vandana Palace and Ors. (22.04.2014 - SC) : MANU/SC/0341/2014 15 See Swastic Automobiles, M/s. v. Bihar State Financial Corporation AIR 1989 SC 1551 and H.P. State Financial Corpn.,

Shimla v. Prem Nath Nanda AIR 2001 SC 5. 16 Manager, ICICI Bank Ltd.v. Prakash Kaur and Ors.III (2007) SLT 1=138 (2007) DLT 248 (SC); Citicorp Maruti Finance Ltd.

v. S. Vijayalaxmi reported in III (2007) CPJ 161 (NC). 17 See ICICI Bank vs. Shanti Devi Sharma and Ors. legalcrystal.com/677540 18 See Subhiksha Trading Services Limited, Chennai, Company Secretary, M.Rathinakumar vs. Kotak Mahindra Bank Limited,

and Ors. 2009 INDLAW MAD 1694 and Sudarshan Overseas Limited vs. Reserve Bank of India and Another 2009 INDLAW DEL 626

19 Sardar Associates and Ors. vs. Punjab and Sind Bank and Ors. (31.07.2009 - SC) : MANU/SC/1351/2009 20 Punjab and Sind Bank vs. Punjab Breeders Ltd. and Ors. (29.03.2016 - SC) : MANU/SC/0366/2016

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 4

the overdue loan accounts which would otherwise slip into NPA

defaults. Both these processes, however, have an effect of reduced or

doubtful recovery chances which over a period of time seriously affect

the lenders’ ability to collect chronic loan defaults.

Moratorium on Repayments and Recovery Proceedings:

Banks have discretion to effect a moratorium on the repayments

in case borrowers have genuine difficulties in servicing the loans. The

repayment is merely deferred and delayed in the case of moratorium of

repayment for a definite period as in the case of CDR and upon the

expiry of said moratorium period, the repayment installments would

commence. The loss of interests arising out of such moratorium erodes

the lender’s capital. Suspension of legal proceedings, including recovery

of loans, as envisaged under section 22 of the Sick Industrial

Companies Act, 1984 (“SICA”) was greatly abused by the borrowers in

our country resulting in the perpetual deferment of recovery

proceedings by lenders. The successor legislation to the SICA viz. IBC,

2016 which introduced moratorium under section 14 of IBC is limited

in duration to 180 days extendable by another 90 days which protects

only the corporate debtor and is no more available to the protection of

its guarantors21. This moratorium sometimes has the effect of not only

delaying, but also defeating the recovery possibilities of the loan

account causing losses to the banks.

One Time Settlement:

RBI guidelines as adopted by the individual scheduled

commercial banks policies hold the field in relation to entertaining of

borrower’s requests for approval of OTS, mostly in relation to the Micro,

Small and Medium Enterprises Sector22. Usually the banks seek to

realise at least the outstanding principal and in most circumstances the

banks forgo the interests where the borrowers have acted genuine and

have not resorted to either diversion or siphoning of the funds. In this

process, banks end up sacrificing the interests, costs and other charges

over the outstanding loans with the haircuts taken by the banks often

21 State Bank of India vs. V. Ramakrishnan and Ors. MANU/SC/0849/2018. 22 See RBI Circular No.RBI/2008-09/467 RPCD. SME & NFS. BC.No.102/06.04.01/2008-09 dated May 4, 2009.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 5

in the range of 40-60 per cent23 which even extend up to 90% of the

loan receivables24. RBI only lays down guidelines for such haircuts, but,

it is the prerogative of each commercial bank to decide on the quantum

of haircut it can take for its borrowers’ loans25. In this process, the only

advantage which accrues to the banks is the immediate liquidity of the

principal amount whose Net Present Value is better than the

uncertainties associated with recovery proceedings. OTS results in the

compromise and settlement of all pending cases and the relinquishment

of right to initiate any fresh cases against the borrowers.

Scheme of Arrangements:

The scheme of compromise with lenders and scheme of

arrangement by companies under section 391 to 394 of the erstwhile

Companies Act, 1956 was one of the most resorted practices which

resulted in the restructuring of companies with huge loan recasts,

deferments, moratorium and haircuts and sacrifices made by the banks

and financial institutions so as to revive the companies under schemes

which are approved by the High Courts.

Revival Scheme under SICA:

Most rehabilitation packages cast an obligation upon the

participating banks/creditors (who might be entitled to claim

outstanding dues from the sick company) to not only forego some part

of the interest liabilities or even accept a lump sum settlement, but also

to do something positive, i.e. to increase/enhance or continue with

recurring funding of a venture which otherwise would be wound-up26.

Under section 19 of the SICA when any scheme is sanctioned by BIFR it

had required lenders to provide further financial assistance to a sick

industrial company by way of loans, advances or guarantees or reliefs

or concessions or sacrifices which led to the frittering away of the

financial resources of the banks in our country. In the case of BIFR

scheme the sick industries are given financial assistance by way of

23 See https://www.thehindubusinessline.com/money-and-banking/banks-have-to-take-up-to-50-haircut-on-

stressed-debt-of-rs-50000-cr-under-ice-framework-study/article24933342.ece as accessed on 16.11.2018 24 See https://www.financialexpress.com/industry/banking-finance/idbi-bank-default-cases-settled-with-90-pct-

haircut-malvika-steel-to-usha-ispat-see-how-surprisingly-low-settlement-was/950181/ as last accessed on 16.11.2018 25 See https://www.thehindubusinessline.com/money-and-banking/banks-not-rbi-will-decide-size-of-badloan-

haircuts/article9686869.ece as accessed on 16.11.2018

26 IndusInd Bank Ltd. vs ITI Limited and Ors. decided by Delhi High Court on 11 July, 2014

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 6

loans, advances or guarantees or reliefs or concessions or sacrifices by

Government, banks public financial institutions and other authorities27.

Corporate Debt Restructuring:

CDR was introduced by RBI as a voluntary non-statutory

arrangement by banks to restructure the accounts of borrowers who are

not classified as willful defaulters and whose accounts do not involve

any frauds. Several corporates in our country have availed CDR and

some of them even availed CDR twice. The CDR cell has approved

restructuring of stressed loans worth Rs.4 trillion since its inception in

2001, of which Rs.84,677 crore worth of loans exited the CDR cell

successfully while Rs.1.84 trillion exited without success and now

nearly Rupees 1.32 trillion worth of bad loans are presently undergoing

restructuring in the cell28. In a typical case of CDR, the lenders agree to

a moratorium, sacrifice of loan principal and interest receivables,

recasting the loans, extending the repayment schedule and in some

cases releasing of additional and fresh loans to help revive the borrower

companies. In some CDR cases, the lenders may also agree to convert

their debt into equity in the borrower company thereby reducing the

quantum of loans and in return may seek a right of recompense which

is very illusory. In all instances of CDR, there is a huge write-off and

loss to the receivables of a bank, by way of hair-cuts and sacrifices.

Courts have held that CDR package also binds the non-member banks

of a borrower29 and with a view to ensuring revival of the CDR

companies they were exempted from onerous financial obligations30

while in some instances injunction against invocation of bank

guarantees were issued to help such companies31, and even

governments were directed to support the obligations undertaken to be

discharged by them in terms of the CDR scheme32. The implementation

of CDR schemes by the Indian banking sector had resulted in draining 27 Deputy Commercial Tax Officer and Ors. vs. Corromandal Pharmaceuticals and Ors. MANU/SC/1598/1997 28 See https://www.livemint.com/Industry/k2S0MIBwJ1Imv7x6PXPxSJ/RBI-moves-to-wind-up-CDR-system.html as

accessed on 12.12.2018 29 Yes Bank Limited Vs. A2z Maintenance and Engineering Services Ltd. and Ors Delhi High Court decision dated July 30,

2014 legalcrystal.com/1159118 30 IDBI Trusteeship Services Ltd. and anr Vs. Arch Pharmalabs Ltd. and ors Delhi High Court decision dated August 24, 2014

legalcrystal.com/1162953 31 Geodesik Techniques Private Limited vs. Larsen and Tourbro Madras High Court decision dated March 28, 2014

legalcrystal.com/1136543 32 AIDQUA Holdings Mauritius Incvs. Tamil Nadu Water Investment Co. Ltd. Madras High Court decision January 31, 2014

legalcrystal.com/1124006

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 7

their resource pool so much that the banks are requiring re-

capitalisation today.

Assignment to Asset Reconstruction Companies:

With the enactment of the SARFAESI Act, 2002, the banks and

financial institutions were permitted to assign and sell their loans to

Asset Reconstruction Companies (“ARC”) in terms of section 5 thereof,

at huge discounts. This enabled the banks and financial institutions to

quickly get rid of their sticky loans and NPAs to ARCs and realise only a

part of the value of the outstanding loan receivables of its borrowers.

ARCs remit only a small upfront money and subsequently settle a

heavily discounted consideration to the banks for such assignment and

the same was neither considered to be against public policy nor the

receipt of only a meagre portion of their loan receivables from the

ARCs33struck down by our courts. Worse such assignment of loans

were also attracting huge stamp duty, which now stands exempted in

terms of the amendment made to section 5 of SARFAESI Act in 2016.

The banks and financial institutions lost heavily on these assignments

of loans, but, in the process only managed to clean-up their balance-

sheets.

Loan Write-off and Waivers:

As per the RBI data on global operations, public sector banks

have written off, including compromise, an amount of Rs.241,911

crores from 2014-15 till September 201734 which amount stood at

Rs.3,16,500 crore as on April 201835. Government of India has clarified

that “writing off of loans is done, inter alia, for tax benefit and capital

optimization. Borrowers of such written off loans continue to be liable for

repayment. Recovery of dues take place on ongoing basis under

applicable legal mechanisms. Therefore, write-off does not benefit

borrowers36.”

33 See ICICI Bank vs. Official Liquidator of APS Star Ltd. AIR 2011 SC 1521 34 See https://www.businesstoday.in/current/economy-politics/govt-has-written-off-rs-2.4-lakh-crore-bad-loans-in-

three-years/story/274077.html as accessed on 12.12.2018 35 See https://www.financialexpress.com/industry/banking-finance/explained-loan-write-off-is-not-the-same-as-loan-

waiver-what-you-should-know/1335139/ as accessed on 12.12.2018 36 The Press Release dated March 28, 2018 of the Ministry of Finance, Government of India.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 8

On the other hand, our judiciary holds that a bank may exercise

their "right of waiver" unilaterally to absolve the debtor from its liability

to repay and upon such exercise, in which event the debtor is deemed

to be absolved from the liability of repayment of loan subject to the

conditions of waiver37. The last debt waiver scheme viz. Agricultural

Debt Waiver and Debt Relief Scheme, 2008 (ADWDRS,

2008) announced by the Union Government was implemented in the

year 2008, where under the debt waiver portion of the ADWDRS, 2008

was closed by its due date i.e. 30.6.2008, while the debt relief portion of

the Scheme was closed on 30.6.2010, with its benefits having been

extended to 3.73 crore farmers to an extent of Rs.52,259.86 crore38.

This was followed up several state governments extending their own

loan waiver schemes as part of their election manifestos which resulted

in huge losses to the cooperative and rural banks, despite objections by

RBI39 and it is estimated that if every state were to waive even 50% of

their agricultural debt, it would cost 1% of India’s GDP in terms of

2016-17 price40.

In the Debt Relief Scheme issued by the Government of India,

when eligibility for loan waivers had not been defined exhaustively, but

only a few examples were mentioned, which can be extended up to a

number of other activities which have not been explicitly mentioned as

the term ‘etc.’ our judiciary extended relief to borrowers who were

affected by militancy41. The Madras High Court has ruled that the

denial of benefit of waiver of crop loans to the farmers who had

cultivated lands exceeding 5 acres is a clear discrimination violating

Article 14 of the Constitution of India and directed that the benefit of

crop loan waiver scheme should be extended to farmers holding more

than 5 acres as well42. But, this decision of the Madras High Court was

eventually stayed by the Supreme Court in July 201743.

37 The Commissioner vs. Mahindra and Mahindra Ltd. (24.04.2018 - SC) : MANU/SC/0513/2018 38 The Press Release dated March 28, 2018 of the Ministry of Finance, Government of India. 39 See https://www.orfonline.org/expert-speak/are-loan-waivers-breeding-a-defaulter-nation/ accessed on 12.12.2018 40 NilanjanBanik, Are Loan Waivers a Panacea for Rural Distress?, Economic & Political Weekly, Vol. LIII No.47, December

1, 2018 41 Jammu Rural Bank vs. Mohd. Din and Ors. (29.08.2008 - SC) : MANU/SC/3674/2008 42 National South Indian vs The Government of Tamil Nadu Madras High Court decision dated 04.04.2017

https://indiankanoon.org/doc/61680939/ 43 See https://www.thehindu.com/news/national/tamil-nadu/sc-stays-madras-hc-order-directing-tn-govt-to-waive-

all-crop-loans/article19202600.ece as accessed on 12.12.2018

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 9

Lenders’ Sacrifices under IBC, 2016:

In terms of IBC, 2016, financial creditors are entitled to CIRP

against corporate debtors under section 7 which may be admitted by

NCLT under section 13 which will include declaration of a moratorium

under section 14 and the appointment of interim resolution

professional. Unlike SICA, the moratorium period and the CIRP period

is also limited in duration and cannot extend indefinitely and therefore

resolution of insolvency of corporate debtors is time-bound. Under IBC,

2016, the financial creditors will constitute a Committee of Creditors

which will evaluate and recommend a resolution plan submitted by the

applicant for approval by NCLT. Once the resolution plan is approved

by NCLT under section 31, it will be binding on the corporate debtor, its

employees, members, creditors, guarantors and other stakeholders

involved in the resolution plan. In case there is no approval of any

resolution plan, then, the corporate debtor proceeds for liquidation in

which case the right of the financial creditor to receive the distribution

of the assets of the company is regulated by section 54 of IBC, which

ranks secured creditors ahead of the unsecured creditors.

Although the provisions of IBC, 2016 are much more effective and

time-bound than those in SICA, yet, its actual implementation remains

dogged with the resolution plans approved by NCLT involving huge

haircuts and sacrifices by the banks44. It has been held by our Supreme

Court and NCLAT that initiation of CIRP is not a recovery proceeding

against borrowers and is aimed at only resolving the corporate

insolvency of a corporate debtor45 and quite recently Limitation Act has

also been held to be applicable to such proceedings. The Supreme Court

has further ruled that if there are pre-existing disputes and if the debt

is disputed then, CIRP cannot be ordered by NCLT46 which rulings will

affect the ability of banks to initiate proceedings against corporate

debtors who may dispute such debt liability. Recently, the RBI had

issued a circular in February 2018 disbanding all CDR schemes and

urging banks to evolve a resolution plan within 180 days for those

44 See https://www.thehindubusinessline.com/money-and-banking/bankruptcy-code-babysteps-towards-recovery-

of-bad-loans/article10002680.ece visited on 16.11.2018. Also, see https://www.rediff.com/business/report/why-banks-are-uncomfortable-with-bankruptcy-code/20171004.htm as accessed on 16.11.2018

45 B.K. Educational Services Private Limited vs. Parag Gupta and Associates MANU/SC/1160/2018 46 Transmission Corporation of Andhra Pradesh Limited vs. Equipment Conductors and Cables Limited MANU/SC/1192/2018

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 10

borrowers who have cumulative exposure of more than Rs.2000 crores

borrowings47 and upon its failure to initiate proceedings against such

borrowers under the provisions of IBC, 2016. The Bombay High Court

refused to stay this direction of RBI48, while the Allahabad High Court

had stayed its operation in relation to power producing companies49

and the Supreme Court has also refused to vacate the said stay while

its application to other borrowers has been upheld by it.

Recent Practices & Conclusion:

Several laudable steps and measures have been initiated by the

Government and regulators like RBI to arrest the mounting NPAs and

losses accruing to the banks. Section 35 AA was inserted in the

Banking Regulation Act, 1949 by way of an ordinance passed in

2017enabling the Government of India to authorize the RBI to issue

directions to banks to initiate the resolution process with respect to a

default under the provisions of IBC, 2016, while section 35 AB (1) was

inserted to enable RBI to issue directions to banks from time to time for

resolution of stressed assets, and Section 35 AB (2) enables the RBI to

specify one or more authorities or committees and appoint or approve

their members, to advise banks on resolution of stressed assets. The

change in section 35 AB (2) is aimed at reducing the ‘fear factor’,

particularly, of the public sector banks in taking decisions on hair-cuts

for the stressed assets for disposing them off or for a OTS. At the same

time, to deal with willful defaulters the provisions were made stringent

by RBI through its master circular which paves way for initiation of not

only recovery proceedings, but also criminal proceedings50. It also

created a mechanism to investigate and report on frauds committed by

borrowers51. Meanwhile, section 211 and 212 of the Companies Act,

2013 paved the way for creation of a statutory authority viz. Serious

Fraud Investigation Office to effectively go into the corporate frauds by

borrowers etc. Legislations like the Prevention of Money-Laundering

Act, 2002, the Black Money (Undisclosed Foreign Income and Assets)

and Imposition of Tax Act, 2015 and the Fugitive Economic Offenders

47 RBI/2017-18/131DBR.No.BP.BC.101/21.04.048/2017-18 dated February 12, 2018 48 JayaswalNeco Industries Limited and Ors. vs. Reserve Bank of India and Ors. MANU/MH/0406/ 49 Independent Power Producers Association of India and Ors. vs. Union of India and Ors. MANU/UP/2966/2018 50 RBI Master Circular No. RBI/2015-16/100DBR.No.CID.BC.22/20.16.003/2015-16 dated July 1, 2015 51 RBI Master Circular No. RBI/2015-16/75DBS.CO.CFMC.BC.No.1/23.04.001/2015-16 dated July 1, 2015

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 11

Ordinance, 2018 were some welcome legislative initiatives which, inter-

alia, seek to identify, recover, tax and prosecute bank fraudsters and

defaulters who flew the country without settling their bank repayments

obligations or secretly hoarding them in tax heavens. Naming and

shaming of the borrowers is also now well recognized by our judiciary.

The Central Vigilance Commission had examined the modus operandi of

top 100 banks frauds, identified the loopholes and had suggested

systemic improvements in its recent report submitted in October

201852.

However, at the same time, both the Government and the

regulators like the RBI have been fighting shy to reveal the extent of

NPAs, extent of loans written-off, CDR impacts and the details of money

stashed away by Indian corporates and others in tax heavens despite

the receipt of and availability of such data. Information under RTI on

the total extent of loans and sacrifices made by banks under the CDR

schemes were refused by the Central Information Commission by

holding that the CDR scheme is not a public authority53. The Supreme

Court has reminded that RBI has a statutory duty to uphold the

interest of the public at large, the depositors, the country's economy

and the banking sector and thus it ought to act with transparency and

not hide information that might embarrass individual banks and

therefore under the provisions of the RTI Act it should disclose the

information on the NPAs and loan sacrifices extended to corporate

borrowers54. Despite the same, as neither the Government nor RBI were

disclosing such details, the CIC castigated RBI and the PMO for their

refusal to share the details of NPA brought about by willful defaulter

and the action taken by the PMO on the letter sent to it by Raghuram

Rajan, the then Governor of RBI on the subject55. Sadly, the RBI had

filed writ petitions challenging this CIC order which forced the outgoing

CIC to write to the President of India on 4th December 2018 that the

Government and its regulators like RBI are intimidating the CIC against

the directions issued “to implement orders of Supreme Court confirming

orders of CIC for disclosure of wilful defaulters of Banks, etc. in 11

second appeals in 2011, just to protect the names of those rich men and

52 Analysis of Top 100 Bank Frauds, Report dated October 15, 2018 of the Central Vigilance Commission, New Delhi 53 Shailesh Gandhi and Ors. vs. CDR Cell, Mumbai (16.09.2016 - CIC) : MANU/CI/0482/2016 54 Reserve Bank of India and Ors. vs. Jayantilal N. Mistry and Ors. (16.12.2015 - SC) : MANU/SC/1463/2015 55 Sandeep Singh Jadoun vs. CPIO, DGEAT (16.11.2018 - CIC) : MANU/CI/0774/2018

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 12

bodies, who duped India and Indians to the tune of lakhs of crores of

Rupees56”. When the Apex Court was approached to regulate the matter

of waivers, write-offs, rescheduling of repayments, moratoriums and

one-time settlements by banks which result in loss of substantial

amount of public funds, it failed to judicially legislate as it did in the

Vishaka and Ors. v. State of Rajasthan and Ors.

(MANU/SC/0786/1997), but lost the opportunity and merely proceeded

to flag the issue for consideration by the Committee of Experts under

the Chairmanship of Shri Vepa Kamesam, Ex-Deputy Governor of

Reserve Bank of India57. Quite recently, the Government of India

seemed to be apparently seeking to obtain from RBI a part of over

Rs.3.6 lakh crores of its reserves so as to apply the same for its populist

policies which was viewed as an invasion into its autonomy resulting in

serious resistance from RBI58 and also leading to recent resignation of

the RBI Governor.

Although we appear to be in a tumultuous phase in relation to

banking industry and there appears to be half-hearted or lackluster

support from the Government and some regulators, yet the efforts

under the Fugitive Economic Offenders Ordinance is paying some

dividends and there is an overwhelming resolve amongst all

stakeholders now to urgently arrest the continuance of NPAs, revamp

the recoveries and bring to justice the fugitive economic offenders,

which in the long-run will lead to improving not only the credit system

but also promote honest borrowing in our country.

56 Letter dated December 4, 2018 of Prof Dr. M Sridhar Acharayalu, who retired as Central Information Commissioner

on 20 November 2018 addressed to the President of India, copy as available in https://www.moneylife.in/article/government-regulators-are-intimidating-cic-by-filing-writ-petitions-says-prof-sridhar-acharyulu/55863.html accessed on 12.12.2018.

57 Common Cause (A Regd. Society) vs. Union of India (UOI) and Ors. (18.08.2010 - SC) : MANU/SC/0615/2010 58 Speech of Dr. Viral V Acharya, Deputy Governor, Reserve Bank of India delivered in the A. D. Shroff Memorial

Lecture in Mumbai on October 26, 2018

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 13

SHUT DOWNS OF ATMs- A CRITICAL ANALYSIS

KIRUTHIKA D

&

VINESHA AM

ABSTRACT

The banking sector is said to be the lifeblood of economic activities. This

sector has changed its dimensions in various forms at lightning speed.

One of the major milestones of banking sector was the introduction of

Automated Teller Machine (ATM). ATM marked the first step for the

digital banking in India. ATM is one of the e-banking outlets that allow

customers to carry out basic transactions without the aid of any

representatives. ATM is commonly called as the cash dispenser and

acquired a touch point with the customers. ATMs are known to be more

than machine, which would help the account holder to perform banking

and withdraw money by inserting card rather than visiting the bank.

The industry of ATM outsourcing has been growing exponentially in

India. The ATM industry continues to move from bank’s managed

services to end-to-end deployment of service vendors. The services

provided by the ATM industry includes ATM site sourcing, site

development, electronic journal (EJ) and switch management services,

managed services, maintenance services, installation services and cash

management. The notification of 06.04.2018 by RBI requiring banks to

put in place certain minimum standards in their arrangements with

service providers by March 2019, it is feared, will result in closing down

of many ATMs.

In this backdrop, the research paper examines the present status

of ATMs and the reason behind the notification of RBI 06.04.2018. The

authors analyze its impact on the banking industries and on the

customers.

Assistant Professor, VIT School of Law, VIT Chennai. 4th Year, BA LLB (Hons.), VIT School of Law, VIT Chennai.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 14

EVOLUTION OF ATM:

The birth of ATM took place to satisfy the customer’s need after

the banking hours. The first ATM which resembled the modern day

ATM, though did not function, was the Bankograph. This Bankograph

was installed in the year 1961 in New York by the Citi Bank. It did not

give out money but accepted the same without any representatives from

the bank. This was not that popular but left a huge impact on the

public.

The first money dispending ATM was installed on 27th June, 1967

by Barclays Bank in Enfield Town, London. It is known by the name De

La Rue Automatic Cash System. Users would insert cheques into the

machines and the machines would return the appropriate amount. The

cheques were called tokens and they were treated with an isotope of

carbon that the machine could read and interpret securely. The tokens

were mailed back to users after the transactions were processed.

Though not ideal by today’s security standards, this system was quite

popular at the time and would eventually inspire the use of plastic bank

cards in ATMs1.

The ATM that resembles the present day modern ATM was first

installed on 2nd September 1969 by the Chemical Bank in New York.

This ATM was the first to dispense cash using bank-issued cards that

worked in combination with security keys like what we call now as PIN

numbers. After the establishment of the ATMs around the world, the

next concern was to go in accordance with the advancement in

technology. At the advent of internet in 1990s, the next goal was to

connect ATMs to the internet so that they could update automatically

and quickly. ATMs have not stopped evolving since they were invented.

ATM IN INDIA:

The advent of ATMs in India took place in 1990s by the foreign

banks due to the high expenses incurred for the installation of ATM and

its technologies. The first Indian Bank that started introducing ATM

was Indian Bank in the year 1988. The HSBC - Hongkong and

1 Bronwyn Watt, “How the ATM machine has evolved over the years”, available at http://paycorp.co.za/news-views/how-

the-atm-machine-has-evolved-over-the-years/, accessed on 01.12.2018.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 15

Shanghai Banking Corporation was the first foreign bank to introduce

the ATM concept in India way back in 1987 at Sahar Road Branch,

Andheri, Mumbai.

Originally, ATM facilities were limited to the high net worth and

wealthier customers. But later when Citibank came up with the

Suvidha Programme, other banks started to provide this service to all

its customers without any limitation. In the first stage, banks that put

up ATMs restricted their use to their own customers. A little later, some

banks joined hands to run the machines and expand these services. In

that phase, with its teething problems, the regulator addressed

concerns relating to safety and security, especially at “offsite” ATMs,

which were not attached to branches of banks.

Private Banks started to expand their networks, giving a big push

to ATMs. Some of the banks started to offer free ATM cards to all

customers. At that stage, banks had to still obtain approvals from the

Reserve Bank of India to get around the provisions of the Banking

Regulation Act that specified activities that could be carried out from

the premises of a bank.

Complaints started to reach the regulator and Reserve Bank of

India found that charges varied from bank to bank. RBI then set up a

working group to formulate a scheme for ensuring reasonable charges,

and to incorporate it in the Fair Practices Code. After completing its

analysis, the RBI made all ATM transactions free, along the lines of the

UK, Germany, France, among other countries.

Subsequently, however, the power to price these services returned

to banks after the regulator eased its stance. But by then, the regional

spread of ATMs had changed, as also the range of banking services they

offered. From being just cash dispensing machines, they had started to

offer payment and many other services, including for loan products,

helping millions of customers reduce their visits to bank branches2.

2 Shaji Vikraman, “In ATM’s 50th year, recalling its growth-and peak- in India”, available at

https://indianexpress.com/article/explained/in-bank-atm-50th-year-recalling-its-growth-and-peak-in-india-4855156/, accessed on 10.12.2018.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 16

A Pune based technology company has developed Bio-ATM, a

biometric based automated teller machine for banks and financial

institutions which leverages sophisticated biometric technology to allow

secure ATM transactions. This is the first time that any Indian company

has developed such an ATM machine. The Bio ATM provides alternative

to the regular card and pin based ATM transaction systems. In order to

access accounts users need to give their biometric to the machine that

will verify and authenticate it with the biometric records available in the

database. The machine uses fingerprints for the verification purpose

and hence customers will need to register their fingerprint with the

bank3.

The number of ATMs in the year 1999, i.e. 12 years after their

birth were only around 800 ATMs in India. But the number increased

from 80,117 in the year 2011 to 2,22,653 in the 20174. The industry of

ATM outsourcing has been growing exponentially in India, since the

ATM industry continues to move from bank’s managed services to end-

to-end deployment of service vendors.

RBI GUIDELINES ON ATM MANAGEMENT:

The RBI’s Statement on Developmental and Regulatory Policies

dated 05th April, 2018 sets out various developmental and regulatory

policy measures for strengthening regulation and supervision;

broadening and deepening financial markets; improving currency

management; promoting financial inclusion and literacy; and,

facilitating data management. In para 11 of the above statement, RBI

stated that in view of the increasing reliance of the banks on outsourced

service providers and their sub-contractors in cash management

logistics, certain minimum standards will be prescribed for the service

provider/sub-contractors who are engaged by the banks for this

purpose within a period of 30 days5. Accordingly, RBI came up with a

notification on “Cash Management activities of the banks - Standards

for engaging the Service Provider and its sub-contractor” dated 06th

April, 2018 wherein it has been decided that the banks shall put in

place certain minimum standards in their arrangements with the

3 Refer http://shodhganga.inflibnet.ac.in/bitstream/10603/40299/5/chapter%204.pdf, accessed on 01.12.2018. 4 Source from RBI. 5 Refer https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=43574.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 17

service providers for cash management related activities. Banks have

been advised to review their existing outsourcing arrangements and

bring them in line with these instructions within 90 days from the 06th

April, 2018. The notification further stated that as the cash held with

the service providers and their sub-contractors continue to remain the

property of the banks and the banks are liable for all associated risks,

the banks shall put in place appropriate Business Continuity Plan

approved by their boards to deal with any related contingencies6.

According to Bloomberg report, these guidelines need to be

implemented by the industry and time had been given till April 2021 to

transition to these rules in phases. It wants operators and banks to

implement these measures by March 20197. The standards prescribed

by the notification are as follows8-

• Minimum net worth requirement of Rs.1 billion should be

maintained at all times by service providers and their sub-

contractors handling cash management logistics on behalf of

banks.

• Minimum fleet size of 300 specifically fabricated cash vans

(owned/leased).

• Cash should be transported only in the owned/leased security

cash vans of the Service Provider or its first level sub-contractors.

Each cash van should be a specially designed and fabricated

Light Commercial Vehicle (LCV) having separate passenger and

cash compartments, with a CCTV covering both compartments.

• The passenger compartment should accommodate two custodians

and two armed security guards (gunmen) besides the driver.

• No cash van should move without armed guards. The gunmen

must carry their weapons in a functional condition along with

6 Refer https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=11245&Mode=0 7Why they say half of ATMs will shut down by March next year, available at

//economictimes.indiatimes.com/articleshow/66770631.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst, accessed on 11.12.2018.

8 Supra note 6, Annex.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 18

valid gun licenses. The Service Provider or its first level sub-

contractor should also furnish the list of its employed gunmen to

the police authorities concerned.

• Each cash van should be GPS enabled and monitored live with

geo-fencing mapping with the additional indication of the nearest

police station in the corridor for emergency.

• Each cash van should have tubeless tyres, wireless (mobile)

communication and hooters. The vans should not follow the same

route and timing repeatedly so as to become predictable.

Predictable movement on regular routes must be discouraged.

Staff should be rotated and assigned only on the day of the trip.

With regard to security, additional regulations/guidelines as

prescribed by Private Security Agencies (Regulation) Act, 2005,

the Government of India and the State Governments from time to

time must be adhered to.

• Night movement of cash vans should be discouraged. All cash

movements should be carried out during daylight. There can be

some relaxation in metro and urban areas though depending on

the law and order situation specific to the place or the guidelines

issued by the local police. If the cash van has to make a night

halt, it necessarily has to be in a police station. In case of inter-

state movement, changeover of security personnel at the border

crossing must be pre-arranged.

• Proper documentation including a letter from the remitting bank

should be carried invariably in the cash van, at all times,

particularly for inter-state movement of currency.

• ATM operations should be carried out only by certified personnel

who have completed minimum hours of classroom learning and

training. The content of such training may be certified by a Self-

Regulatory Organisation (SRO) of Cash-in-Transit (CIT)

Companies/Cash Replenishment Agencies (CRAs) who may tie up

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 19

with agencies like National Skill Development Corporation for

delivery of the courses.

• The staff associated with cash handling should be adequately

trained and duly certified through an accreditation process.

Certification could be carried out through the SRO or other

designated agencies.

• Character and antecedent verification of all crew members

associated with cash van movement, should be done

meticulously. Strict background check of the employees should

include police verification of at least the last two addresses. Such

verification should be updated periodically and shared on a

common database at industry level. The SRO can play a proactive

role in creating a common data base for the industry. In case of

dismissal of an employee, the CIT/CRA concerned should

immediately inform the police with details.

• Safe and secure premises of adequate size for cash

processing/handling and vaulting. The premises should be under

electronic surveillance and monitoring round the clock. Technical

specifications of the vault should not be inferior to the minimum

standards for Chests prescribed by the Reserve Bank. The vault

should be operated only in joint custody and should have colour

coded bins for easier storage and retrieval of different types of

contents.

• All fire safety gadgets should be available and working in the

vault which should also be equipped with other standard security

systems live CCTV monitoring with recording for at least 90 days,

emergency alarm, burglar alarm, hotline with the nearest police

station, lighting power backup and interlocking vault entry doors.

• Work area should be separate from the cash area. The premises

should be under the security of armed guards whose number

should have reference to the scale of operations specific to the

location but not less than five in any case.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 20

• Critical information like customer account data should be kept

highly secure. Access to the switch server should be restricted to

banks. Interfaces where a bank gives access to the service

provider or its sub-contractor to the bank’s internal server should

be limited to relevant information and secured.

Adding further RBI asked banks to ensure that the computer

systems in ATMs were BIOS password protected and carried supported

versions of the operating system by its notification dated 21st June,

2018.

IMPACT OF ATM MANAGEMENT GUIDELINES:

The impact of the above guidelines prescribed by the Central

Bank can be studied under two heads. One, their impact on the ATM

industry and second, on the customers.

ATM industry:

Due to demonetization in November, 2016, the calibration of

ATMs had to be changed. There were various restrictions on amount of

withdrawals that can be done by account holders. This itself was a great

hindrance to the ATM industry and in addition to demonetization came

the above guidelines from the RBI.

The first guideline that minimum net worth requirement of Rs.1

billion should be maintained at all times by service providers and their

sub-contractors handling cash management logistics on behalf of banks

will create a situation where there would be very few players in the

market and those would not be able to cater to the requirements of

banks, even as it creates a monopoly. Of the dozens of major cash

logistic companies in the county, only three namely CMS, AGS, and

Checkmate, currently have net worth of Rs1 billion.

On the issue of additional armed guards, it is hard to get gun

licences and increasing the number of security personnel will be

difficult. Especially during elections, armed guards are in short supply.

It is also impractical that loaded cash vans be parked at police stations

after sundown.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 21

As per estimates, each ATM will require three sets of five cassettes

– one set in the ATM, one in transit, and another at branch/CIT

company (ready for loading next day). The cost of each cassette is

about Rs.20,000. So, the one-time cost of additional cassettes for over

two lakh ATMs could be close to Rs.6,000 crore. Further, to comply

with the minimum cash management standards, including the

requirement of specially designed and fabricated Light Commercial

Vehicles having separate passenger and cash compartments with CCTV

covering both compartments, and two armed security guards (gunmen),

prescribed by the RBI, the cost per month per ATM will increase

by Rs.4,0009. To implement all these security, software-hardware

directive would entail an additional cost of minimum Rs.150,000 per

ATM per month10.

These requirements were never anticipated by the industry

participants at the time of signing contracts with the banks. Many of

these agreements were inked four to five years ago11.

Almost 50 per cent of the 2.22 lakh ATMs may have to be closed

by March 2019 on account of non-viability of operations brought about

by recent regulatory guidelines for ATM hardware and software

upgrades, recent mandates on cash management standards, and the

cassette swap method of loading cash.

Customers:

It is obvious that such move of the Central Bank is for protecting

the interest of the general public and the customers in particular. But,

if the guideline lead to the closure of ATMs then that would have a

negative impact on the customers for whom the banking industry is

existing.

Consumers would first face the difficulties of using the normal

banking system again by going back to banks and to wait in long queue

to get their banking works to be done. As not everyone would adopt 9 See https://www.thehindubusinessline.com/money-and-banking/catmi-tells-rbi-to-constitute-task-force-on- pricing-

to-prevent-closure-of-atms/article25579967.ece, accessed on 05.12.2018. 10 See https://www.ndtv.com/india-news/atm-shutdown-50-atms-in-india-may-shut-down-by-march-next-year-says-

report-1951093, accessed on 09.12.2018. 11See https://www.livemint.com/Politics/pc0J8nfD5m9Ze1mnHWYLaL/50-of-existing-ATMs-across-India-to-shut-

down-by-March-2019.html, accessed on 02.12.2018.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 22

themselves to the concept of internet banking for various reasons like,

few may not know how to use such technology; some may not utilize

such facilities. It may also happen that individuals, who are able to

utilize them, step back because of the high number of online fraud and

wrong transactions that might happen.

The enhanced charges will increase by 30-40 per cent for security

alone. The per-transaction charge might increase by Rs.6 to Rs.10. This

might increase interchange fee, currently capped at Rs.15 per

transaction12. Services such as the doorstep cash-delivery and pick-up,

offered to senior citizens and small businesses, would also be affected.

Cash loading will be affected.

Closure of ATM would impact on jobs of many individuals and

also the financial inclusion efforts of the government. There would be a

negative impact on the financial inclusion programme where the

beneficiaries under the scheme withdraw their cash subsidies from

ATMs. Thousands of families many lose their jobs and this will result in

huge unemployment, from the security guards to many officials

authorities. It would be like hitting hard both urban and rural

population, and dealing a blow to the digitization policy.

Using internet banking as a result of shut downs of ATM’s would

pave way for crime crimes. Fraudulent money transfer would begin and

many new regulations and new method of transaction may have to be

passed on it to reduce and govern on the transaction online.

CONCLUSION:

Closing half the ATMs in the country would mean another

demonetisation-like situation where people struggle to get hold of cash.

Shutting down of ATM’s would be detrimental to financial services in

the economy as a whole. 30% of the account holders in bank are

regular users of ATM’s, now this would also disturb the customers of

those banks. ATM’s are known to be the financial connectivity among

people, only after the setting ups of ATM’s financial transactions,

12 Raghu Mohan, RBI's new cash logistics norms might disrupt functioning of ATMs: IBA, available at

https://smartinvestor.business-standard.com/market/story-542593-storydet-RBIs_new_cash_logistics_norms_ might_disrupt_functioning_of_ATMs_IBA.htm#.XBktuzAzbIU, accessed on 12.12.2018.

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

CECLJ - TNDALU Page 23

withdrawals and deposits of cash was made easier and simple for the

customers.

Despite the growth of cards and other payment systems, the

market for cash, and ATMs to dispense it, does seem likely to remain

strong in India. As a business historian and expert on cash economies,

Batiz-Lazo pointed out the ratio of ATMs to population in India is still

way below global norms, leaving plenty of scope to expand. Once you

leave the metros, ATMs still seem far too few and remote13. A report by

Hexa research suggests that the worldwide ATM market is projected to

garner more than 26 billion US$ by 2024, growing at around 9.8%

CAGR in the forecast period (2016-2024). It had a value of 12.5 billion

US$ in 2015. Technological breakthroughs and innovative security

standards amid growing wireless devices should propel the market in

the near future. This can reduce fraud and lead to safe financial

transactions14.

The Confederation of ATM Industry has called upon the Reserve

Bank of India (RBI) to constitute a task force to transparently discover

pricing related to implementing cassette swap for replenishing cash and

adhering to minimum standards for cash-management activities. The

only way to salvage the situation for the industry is if banks step in to

bear the load of the additional cost of compliance. Also the RBI should

relax net worth and security rules to prevent interchange costs from

shooting up.

13 “Here's the story of ATMs over the years”, available at https://economictimes.indiatimes.com/slideshows/nation-

world/heres-the-story-of-atms-over-the-years/miles-to-go/slideshow/55511202.cms, accessed on 03.12.2018. 14 See https://www.hexaresearch.com/research-report/atm-market.

CECLJ - TNDALU Page 24

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

ANALYSIS OF NEW TRENDS IN BANK: CUSTOMER

RELATIONSHIP

VIGNESHWARAN.R &

RAJPRIYA.R

ABSTRACT

Indian economic environment is witnessing path breaking reform

measures. Today the banking industry is stronger and capable of

withstanding the pressures of competition. We are having a fairly

well developed banking system with different classes of banks, both

old and new generation, with the Reserve Bank of India as the

fountain Head of the system. In the banking field, there has been an

unprecedented growth and diversification of banking industry has

been so stupendous that it has no parallel in the annals of banking

anywhere in the world. In general, banks have had a track record of

innovation, growth and value creation. However this process of

banking development needs to be taken forward to serve the larger

need of financial inclusion through expansion of banking services,

given their low penetration as compared to other markets. Now-a-

days we are hearing about e-governance, e-mail, e-commerce, e-

tail etc. In the same manner, a new technology is being developed in

US for introduction of e-cheque, which will eventually replace

the conventional paper cheque. Our Indian banks have developed

new trends for the growth of their banks, as to attract the customers.

This paper deals with the new trends of banks and relation between

the bank and customers and its backdrops.

INTRODUCTION

During the last 41 years since 1969, tremendous changes have

taken place in the banking industry. The banks have shed their

traditional methods, improving and coming out with new types of

services to cater to the emerging needs of their customers. Today, we

are having a fairly well developed banking system with different

classes of banks – public sector banks, foreign banks, private sector

banks – both old and new generation, regional rural banks and co-

operative banks with the Reserve Bank of India as the fountain Head

of the system. Some of them have engaged in the areas of consumer

DR. Ambedkar Global Law Institute, Tirupathi – AP.

CECLJ - TNDALU Page 25

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

credit, credit cards, merchant banking, leasing, mutual funds etc. A

few banks have already set up subsidiaries for merchant banking,

leasing and mutual funds and many more are in the process of doing

so. The banking system in India is significantly different from other

Asian nations because of the country’s unique geographic, social,

and economic characteristics. Today, Indian banking industry is one

of the largest in the world. Customer Relationship Management

(CRM) in the banking sector is of strategic importance. CRM is a

holistic process of acquiring, retaining, and growing customers. CRM

is used to define the process of creating and maintaining

relationships with business or customers.

1. TO UNDERSTAND THE RECENT TRENDS IN “CRM”

• CRM IN BANKING SECTOR

Good customer service is brand investor of any bank. The idea of

CRM is that it helps banks use technology and human resources to

evaluate the perception of customers and the value of those

customers. Customer Relationship Management is very important for

the growth and profitability of banks in the present technological

age. The definition of CRM given as “the market place of the future”

is undergoing a “technology-driven metamorphosis”. It is emphasized

that customer relationship management based on social exchange

and equity significantly assists the firm in developing collaborative,

cooperative and profitable long-term relationships. CRM is

instrumental in identifying and capturing the most customers of the

bank. It combines technology with human resources in order to

create new strategies to acquire new customers and retain the

existing ones. The long-term business relationships provide many

potential benefits for banks and clients.

GLOBAL BANKING DEVELOPMENTS

The year 2010-11 was a difficult period for the global banking

system, with challenges arising from the global financial system as

well as the emerging fiscal and economic growth scenarios across

countries. Global banks exhibited some improvements in capital

adequacy but were beleaguered by weak credit growth, high leverage

and poor asset quality. In contrast, in major emerging economies,

credit growth remained at relatively high levels, which was regarded

as a cause of concern given the increasing inflationary pressures and

CECLJ - TNDALU Page 26

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

capital inflows in these economies. In the advanced economies, credit

availability remained particularly constrained for small and medium

enterprises and the usage of banking services also stood at a low,

signalling financial exclusion of the population in the post-crisis

period. On the positive side, both advanced and emerging economies,

individually, and multi-laterally, moved forward towards effective

systemic risk management involving initiatives for improving the

macro-prudential regulatory framework and reforms related to

systemically important financial institutions.

RECENT TRENDS IN BANKING

Through the years, the CRM industry relied heavily on

technology and software developments. CRM has evolved over the

decades. The term became popular in the early '90s, when it began to

be used to refer to front-office applications. Banks can develop

innovative and creative customer solutions to attain growth and

profitability along with sound risk-management practices. The CRM

industry relied heavily on technology and software developments.

CRM trends in the coming months - and years - are bound to change

how businesses deal with customers. Cloud CRM and social CRM are

used recently to deal with customers. CRM products such as Sales

force, Microsoft Dynamics CRM, Exact Target, Markets, Silver Pop,

Oracle and SAP are available in the market. Public sector banks

must use these CRM techniques to remain in competition. The

following are some of the latest e-CRM techniques used by banks in

offering new products and services to its customers.

1) Electronic Payment Services ( E Cheques )

2) Real Time Gross Settlement (RTGS)

3) Electronic Funds Transfer (EFT)

4) Electronic clearing services (ECS)

5) Automatic Teller Machine (ATM)

6) Point of Sale Terminal

7) Tele Banking

8) Electronic Data Interchange (EDI)

9) Mobile banking

10) Chip card

1) Electronic Payment Services – e- Cheques

CECLJ - TNDALU Page 27

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

A new technology is being developed in US for introduction of

e-cheque, which will eventually replace the conventional paper

cheque. India, as harbinger to the introduction of e-cheque, the

Negotiable Instruments Act has already been amended to include;

truncated cheque and e-cheque instruments.

2) Real Time Gross Settlement (RTGS)

Real Time Gross Settlement system, introduced in India since

March 2004, is a system through which electronic instructions can

be given by banks to transfer funds from their account to the

account of another bank. The RTGS system is maintained and

operated by the RBI and provides a means of efficient and faster

funds transfer among banks facilitating their financial operations. As

the name suggests, funds transfer between banks takes place on a

‘Real Time' basis. Therefore, money can reach the beneficiary

instantaneously and the beneficiary's bank has the responsibility to

credit the beneficiary's account within two hours.

3) Electronic Funds Transfer (EFT)

Electronic Funds Transfer (EFT) is a system whereby anyone

who wants to make payment to another person/company etc. can do

so by giving complete details such as the receiver's name, bank

account number, account type (savings or current account), bank

name, city, branch name etc.

4) Electronic Clearing Service (ECS)

Electronic Clearing Service is a retail payment system that can

be used to make bulk payments/receipts of a similar nature

especially where each individual payment is of a repetitive nature

and of relatively smaller amount. This facility is meant for companies

and government departments to make/receive large volumes of

payments rather than for funds transfers by individuals.

5) Automatic Teller Machine (ATM)

1. ATM is a step in improvement in customer service.

2. ATM facility is available to the customer 24 hours a day. The

customer is issued an ATM card.

3. This is a plastic card, which bears the customer’s name. This

card is magnetically coded and can be read by this machine.

CECLJ - TNDALU Page 28

BANKING SERVICES: PROBLEMS AND PERSPECTIVES

4. After the card is a recognized by the machine, the customer

enters his personal identification number.

5. When the transaction is completed, the ATM ejects the

customer’s card.

6) Point of Sale Terminal

During a transaction, the customer's account is debited and

the retailer's account is credited by the computer for the amount of

purchase.

7) Tele Banking

Tele Banking facilitates the customer to do entire non-cash

related banking on telephone. Under this devise Automatic Voice

Recorder is used for simpler queries and transactions. For