banking and bank runs we are going to learn a bit about what a bank does and why it leads to the...

Post on 20-Dec-2015

213 views

TRANSCRIPT

Banking and Bank Runs

• We are going to learn a bit about what a bank does and why it leads to the possibility of bank runs.– We will start out today with

a couple of movie clips.– Then discuss a theoretical

model of a bank.

Mary Poppins

• Two things to notice.– Bank Run was caused by panic w/o financial

reasons. The bank was fully solvent.– The bank closed its doors: stopped payment.

It’s a Wonderful Life

• It was a systemic panic.• There may have been a justification for the bank

run.• A bank takes money and invests it in long-term

assets (mortgages). • The bank can’t easily liquidate these assets.• The bank did not fully suspend payments. Doing

so would hurt depositors. • There was a degree of negotiation on who gets

what.

Diamond Dybvig Model (1983)

• Captures elements of what a bank does.

• Shows that there is a basic problem of bank runs.

• The model consists of two parties.– Depositors – Banks

• The model has three time periods: yesterday, today and tomorrow.

Depositors

• Depositors placed money (say £1000) in a bank (yesterday) before learning when they need the money.

• Depositors either need their money today (impatient) or tomorrow (patient). There is a 50% chance of being either type.

• The ones that need their money tomorrow can always take the money today and hold onto it.

• The ones that need money today get relatively very little utility for the money tomorrow.

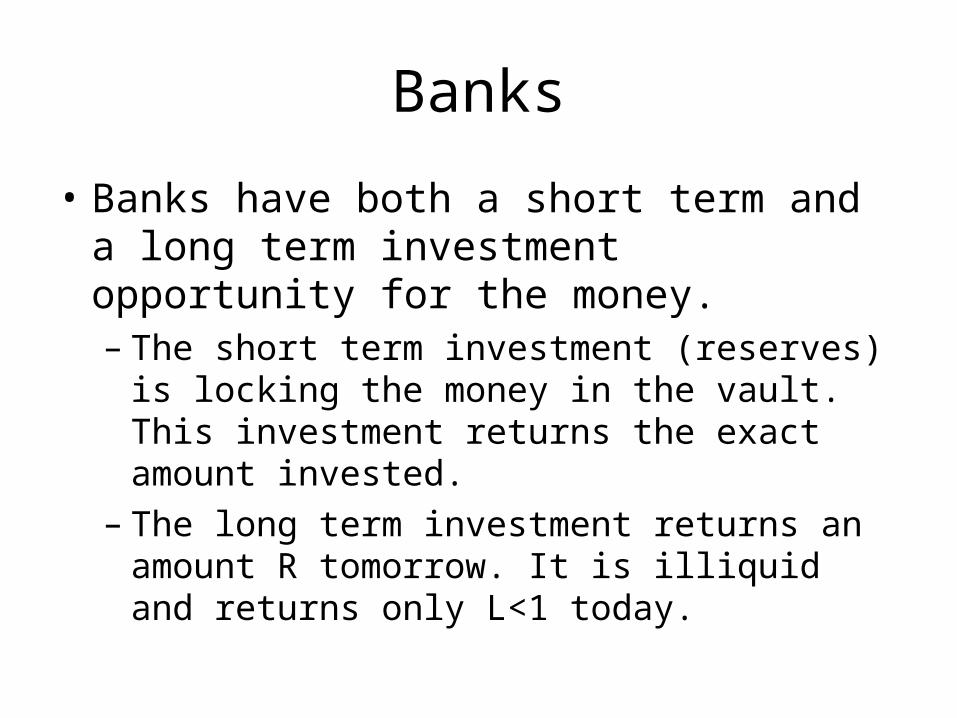

Banks

• Banks have both a short term and a long term investment opportunity for the money.– The short term investment (reserves) is

locking the money in the vault. This investment returns the exact amount invested.

– The long term investment returns an amount R tomorrow. It is illiquid and returns only L<1 today.

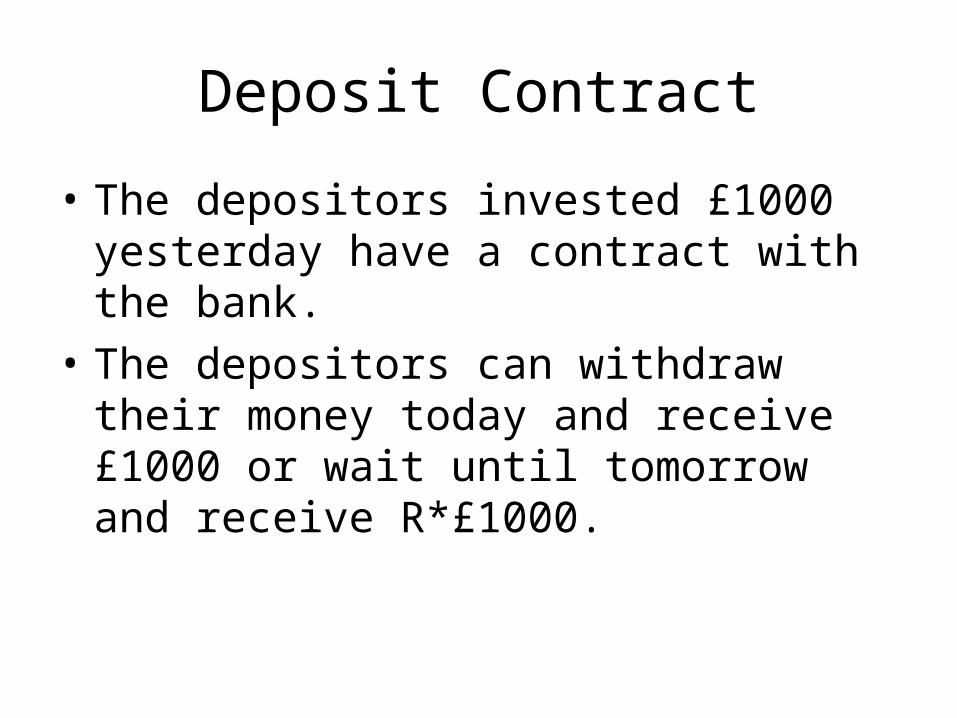

Deposit Contract

• The depositors invested £1000 yesterday have a contract with the bank.

• The depositors can withdraw their money today and receive £1000 or wait until tomorrow and receive R*£1000.

Bank’s decision

• How can the bank meet this contract?– The bank can divide into two parts.

• Take half and keep it as reserves.

• Take the other half and put it in the long term investment.

• Say there are 10 depositors: 5 patient and 5 impatient. The bank puts £5000 in the vault and invests £5000.

• Demands today are 5*1000, and 5*R*1000. The bank has 5000 and R*5000 tomorrow.

• Thus, a bank makes zero profit.

Danger!

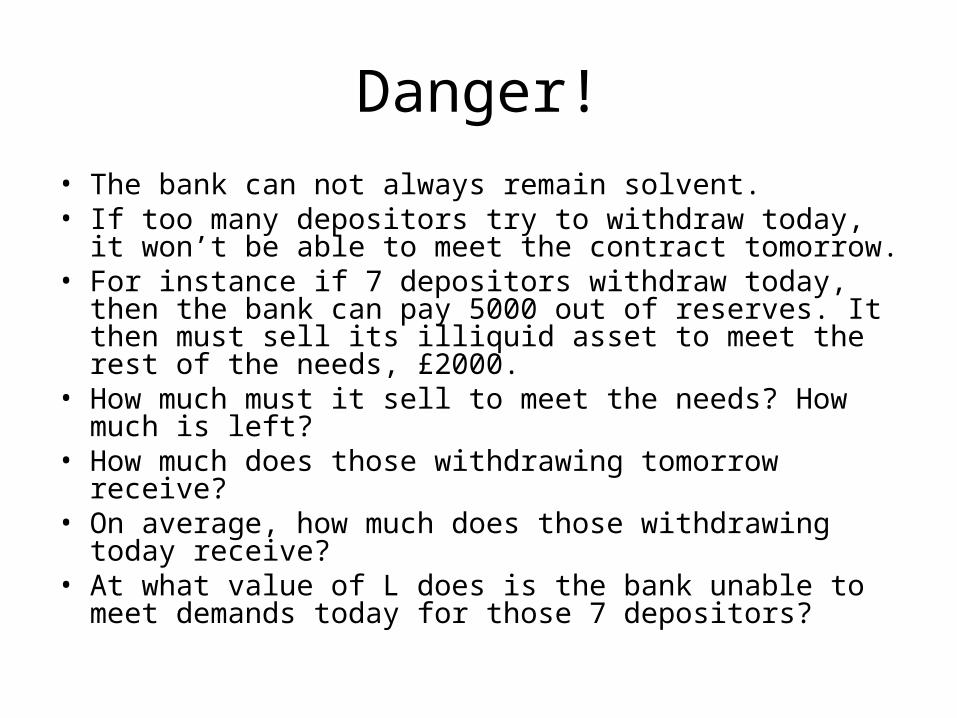

• The bank can not always remain solvent.• If too many depositors try to withdraw today, it won’t be

able to meet the contract tomorrow.• For instance if 7 depositors withdraw today, then the

bank can pay 5000 out of reserves. It then must sell its illiquid asset to meet the rest of the needs, £2000.

• How much must it sell to meet the needs? How much is left?

• How much does those withdrawing tomorrow receive?• On average, how much does those withdrawing today

receive?• At what value of L does is the bank unable to meet

demands today for those 7 depositors?

Multiple equilibria

• This leads to multiple (Nash) equilibria.

• It is inherent in banking.

• Here is an example with 2 patient depositors (and 2 impatient depositors).

• This forms a 2x2 game between the patient depositors.

• R=1.5 and L=.5

Game between patient depositorsDepositor 1

Depositor 2

Today

Today

Tomorrow

Tomorrow

3/2

3/2

R=1.5, L=.5

0

0

1

13/4

3/4

Experiment

• We then went to the lab and had 3 treatments with 9 patient and 9 impatient.

• Credit Crunch: R=1.1, L=.11

• Normal Conditions: R=2, L=.7

• Credit Crunch with 90% deposit insurance.

• How many other patient depositors need to withdraw today for you to want to withdraw today?

Credit crunch

Normal Conditions Credit crunchw/ 90% deposit ins.

Hidden assumption

• Depositors withdraw sequentially: a bank cannot count the number of people wanting to withdraw today and then decide how much to pay them.

• Otherwise, they can just pay them 5000/N where N is the number withdrawing early (for the 10 depositor case). This would make suspension less painful.

What is not captured in the model• Uncertainty in depositor’s preferences.

– Too many actually need the money today.

• Riskiness in technology.– Riskiness in R: Perhaps there really isn’t enough to

meet demand tomorrow. • Implication: it will be worthwhile to withdraw money

independent of what others do. Sometimes a bank run will be the unique equilibrium.

– Riskiness in L: Perhaps one can’t really get L. Particularly if it is a systemic risk.

• With LTCM, prices went down on any asset that LTCM owned! Dual listed stocks arbitraged by LTCM diverged

Early Solutions to Bank Runs

• Put money in the windows

• Slow up payments.

Solutions.• Make sure R & L are not risky. Difficult & doesn’t stop multi. Equilibria.• Pay early withdrawers less than 1 or pay late withdrawers less than R (and keep

more reserves/Narrow Banking)– Problems: not best contract.

• Suspend payments/ Partial Suspension.– Problem when number needing money today is uncertain.

• Creditor Coordination.– Long Term Capital Management ran into trouble in 1998. – The NY FED organized a bailout with creditors.

• Lender of last resorts.– Central bank will stop in and loan the bank money to replace deposits.– This should work with depositors in the case of a problem with liquidity– In 1975,

• April 14th, Credit Suisse announced lost some money in one of its branches. It didn’t mention details.

• April 25th, The Swiss Central Bank announced it was willing to lend money.• This had the opposite result causing share price to tumble 20%.

• Combination Bailout.– 1907 Banking panic (JP Morgan and US treasury).

• Deposit Insurance.– This works well. Risk-Sharing between banks.

Insurance Problem: Moral hazard

• Todd buys theft insurance for his laptop.• Because he buys the insurance, he is

more likely to leave the laptop in his car.• Ideally, he would like to commit to not

leaving the computer in his car. • Sometimes, we can contract on it.• Other times, we can’t. • Do we have a moral hazard problem with

deposit insurance?

Answer: Yes.

• Marc is the manager of a Springfield S&L. • Marc pays higher interest than a bigger and safer bank

claiming his small size helps him cut costs.• Springfield has deposit insurance (100%).• Todd puts money in Springfield.• Springfield lends money to a dodgy lecturer at

Springfield State University at a higher rate.• When there is no default, everyone wins.• When there is a default, Todd still gets paid.• Without insurance, Todd wouldn’t invest if he sees

Springfield’s risky behavior.

Model of Moral Hazard.• The bank can choose any investment x, where 3>x=>1. • Any investment costs £.95 and is either successful and pays of x or

unsuccessful and pays £0. • The probability of the investment being successful is

P(X)=(3-x)/2. • Choosing x=1 is safe, choosing x close to 3 is unsafe.• Todd is close to risk neutral and wants to earn at least as much as

£1 (in expectation) which the other banks are offering as a risk free investment. He wants R where R*P(x)=1.

• Without insurance, the bank maximizes – P(X)*(X-R) where R=1/P(x)

• With insurance, Todd only needs R=1. So the bank maximizes– P(X)*(X-R) where R=1

Savings and Loans scandal

• In the 1980s about 1000 S&L’s went bankrupt. • They originally lent money out at fixed rates of

6% and paid deposits 3%.• With inflation, they had to pay deposits 14% and

lost money.• Took gambles to catch up, went to Vegas.• They were able to take high risk due to the

deposit insurance.• This cost US taxpayers $120 billion.

Solution to Moral Hazard

• One solution is for insurance to not be 100% (co-pay as in the UK).

• However, this requires the depositors to be savvy and this still keeps the multiple equilibrium problem.

• In the US, in 2006 Bush signed a law allowing the FDIC to charge premiums based upon risk.