bankcard 101. agenda company overview credit card history evolution of processing process flow...

TRANSCRIPT

Bankcard 101

AgendaCompany OverviewCredit Card History Evolution of ProcessingProcess FlowMerchant Services 101Merchant Processing ExpenseMarketing/Prospecting Statement ReviewBack Office Procedures

Welcome! Netcom PaySystem

Thank you for your interest in becoming a Netcom PaySystem Regional Sales Agent.

Our company has been in the electronic payments industry since 1987 and our portfolio consists of over 4,000 merchants. We are a newly formed public company out of a new IPO with United eSystems. We have a wide variety of products to offer our merchants to make a progressive package at competitive pricing.

Where are we!

980 Canton StreetSuite D

Roswell, Georgia 30075

Phone: 800-875-6680Fax: 770-649-1370

www.netcompaysystem.com

Your Team and Operations

Mike Plummer- PresidentAmy Plummer – Finance Coordinator Amy will help out with statement analysis as needed.Sam Spiezio- Vice President of Sales

Development Contact Sam for sales development and marketing

questions.Scott Wegert and Robert O’Brien- Accounts

ManagersContact Scott and Robert for all day-to-day operations and

application management.

Products and ServicesAt Netcom PaySystem we constantly monitor changes in the Point of

Sale industry with an emphasis on improved service to our Clients.

Credit/Debit Processing ACH Retail or Internet Recurring Billing Check Services including; Check21 ECC Check by Phone Check by Web Free Check Recovery InStor BillPay Services Including: SameDay BillPay Load all Debit Load all Wireless International Wire Transfer Gift and Loyalty Programs Merchant Advance Age and ID Verify or MSB’s ROAMpay Wireless

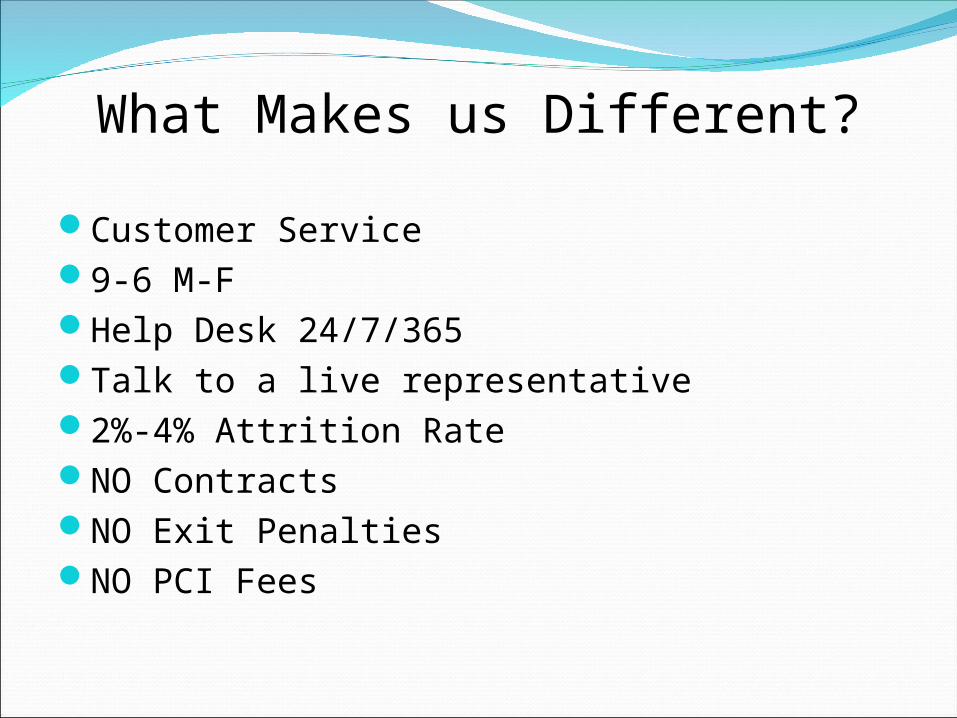

What Makes us Different?

Customer Service9-6 M-FHelp Desk 24/7/365Talk to a live representative2%-4% Attrition RateNO ContractsNO Exit PenaltiesNO PCI Fees

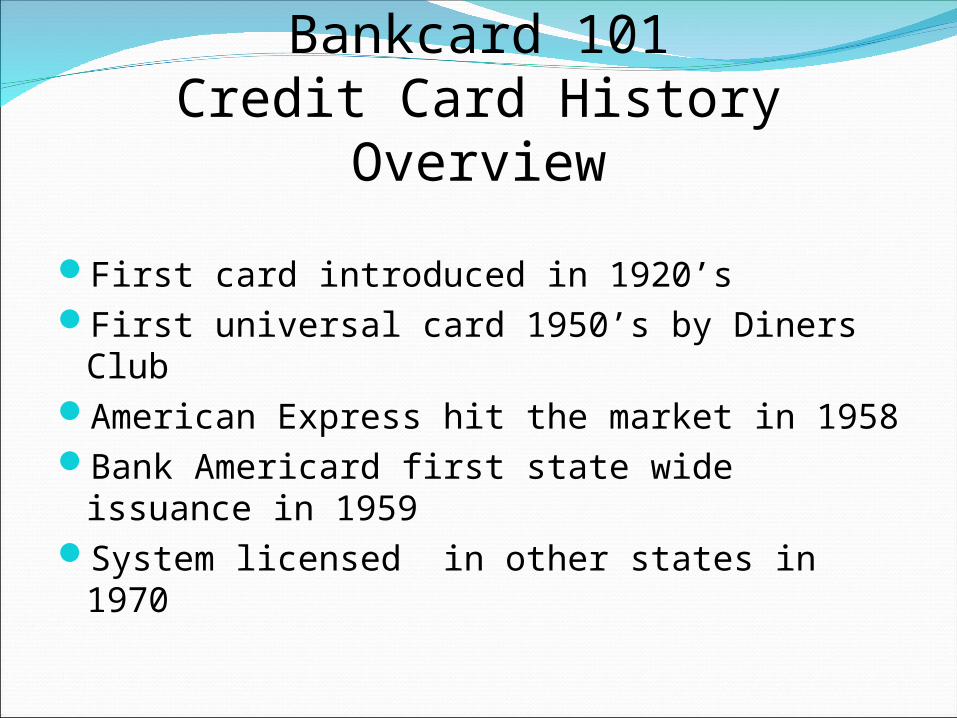

Bankcard 101Credit Card History Overview

First card introduced in 1920’sFirst universal card 1950’s by Diners ClubAmerican Express hit the market in 1958Bank Americard first state wide issuance in

1959System licensed in other states in 1970

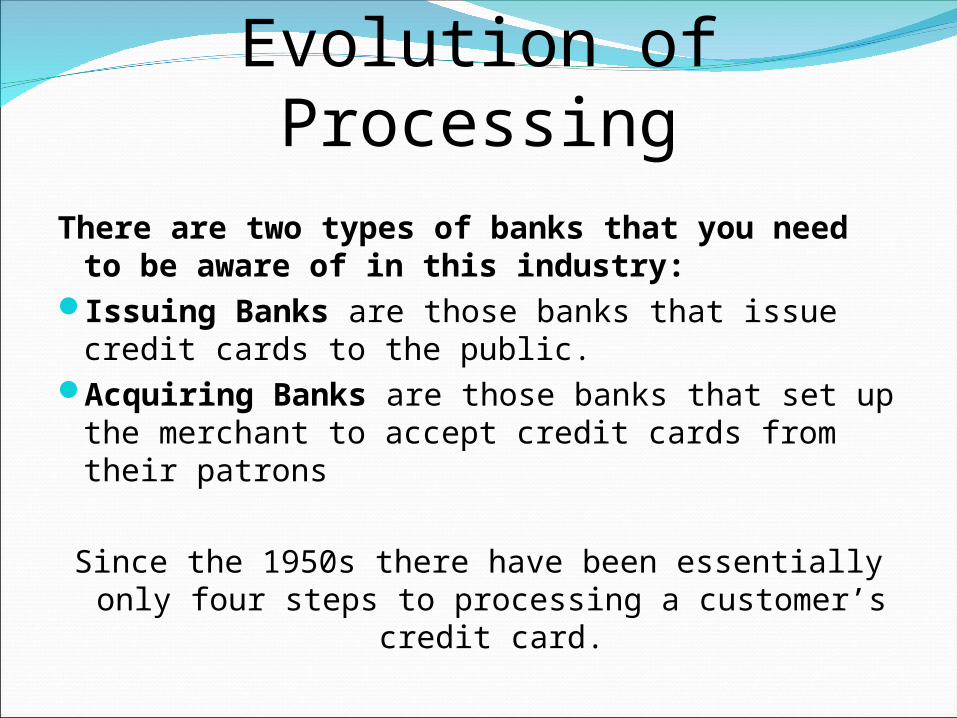

Evolution of ProcessingThere are two types of banks that you need to

be aware of in this industry:Issuing Banks are those banks that issue credit

cards to the public.Acquiring Banks are those banks that set up

the merchant to accept credit cards from their patrons

Since the 1950s there have been essentially only four steps to processing a customer’s credit

card.

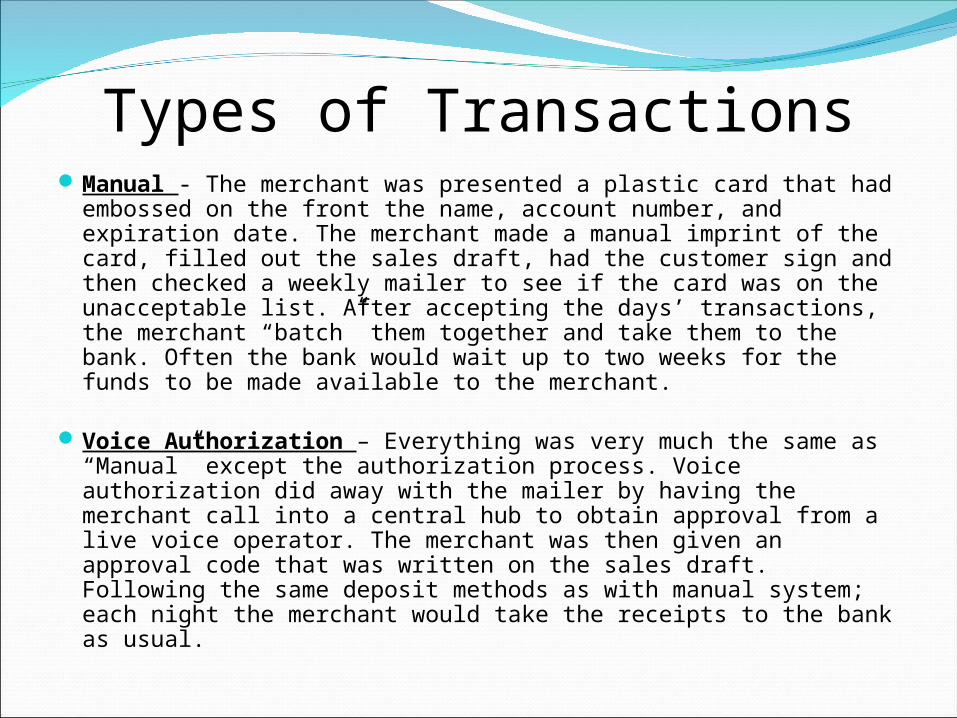

Types of TransactionsManual - The merchant was presented a plastic card that had

embossed on the front the name, account number, and expiration date. The merchant made a manual imprint of the card, filled out the sales draft, had the customer sign and then checked a weekly mailer to see if the card was on the unacceptable list. After accepting the days’ transactions, the merchant “batch” them together and take them to the bank. Often the bank would wait up to two weeks for the funds to be made available to the merchant.

Voice Authorization – Everything was very much the same as “Manual” except the authorization process. Voice authorization did away with the mailer by having the merchant call into a central hub to obtain approval from a live voice operator. The merchant was then given an approval code that was written on the sales draft. Following the same deposit methods as with manual system; each night the merchant would take the receipts to the bank as usual.

Types of Transactions (Cont.)Point of Sale Authorization – This was the first time the

magnetic strip on the back of the cards came into play. The magnetic stripes are with the cardholders account and bank routing number information. By swiping the card thru the terminal the merchant sends the information via the telephone lines to a central system that authorizes payment. The merchant then batches as usual and takes the drafts to the bank for deposit.

EDC (Electronic Data Capture) - This is the process that we use today. By swiping the card the merchant gets the P.O.S. authorization; however the merchant does not have to make a physical bank deposit. At the end of the day, the merchant electronically batches the information held within the terminal and the deposits are made automatically to the merchant’s checking account within 2 business days.

Types of Transactions (Cont.)Note: With the EDC system there are two kinds of

processing:

Host Capture – the transaction is authorized automatically by the processor. This is used for all types of business where the transaction is completed and nothing is left open.

Terminal Capture – is a type of EDC that allows a transaction to stay open, such as needed in the hotel and restaurant industries. An amount of money is entered into the terminal in order to capture this money from the cardholder’s line of credit. The hotel then closes out the transaction at check out and the exact amount is entered into the terminal. The transaction then gets batched and the company receives their funds within two business days.

Process Flow

Authorization ProcessCardholder presents credit card to pay for purchaseMerchant swipes card, enters the dollar amount, and

transmits an authorization request to the merchant bank.

Merchant bank automatically sends authorization request to the Processor (or other platform)

Platform routes the request to cardholder issuerIssuer approves or declines the transaction.The Processor forwards the Issuer’s response to the

Merchant.Merchant Bank forwards the response to the

Merchant.Merchant receives the authorization response and

completes the transaction accordingly.

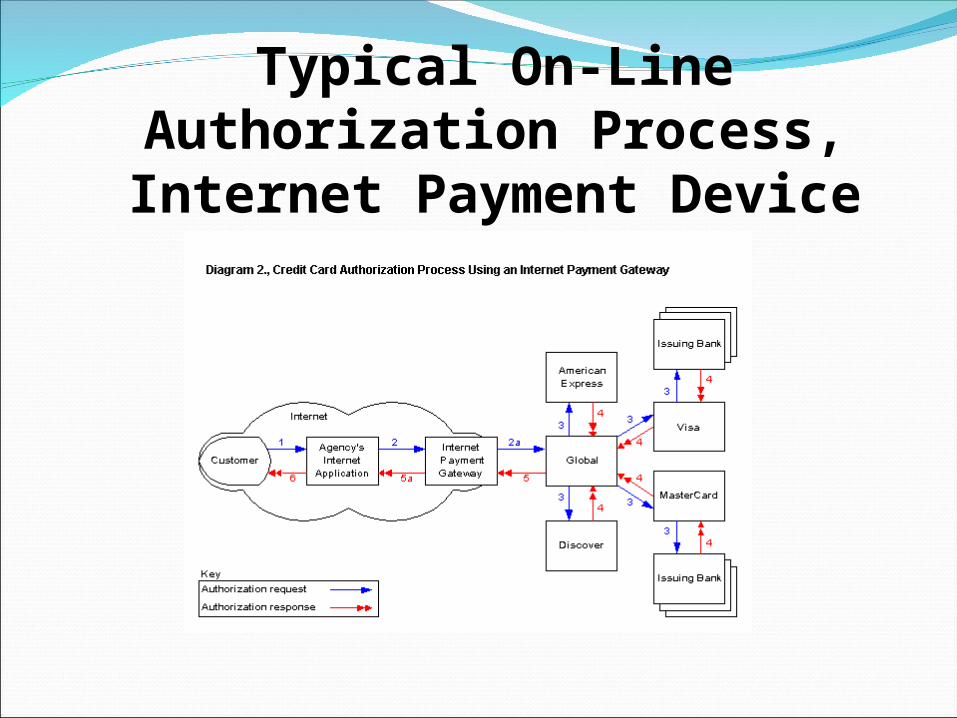

Typical On-Line Authorization Process, Internet Payment Device

Authorization through an Internet Application

Card information (e.g., card type, account number, expiration date) is entered into the Internet application by the cardholder in a secure environment using Secure Socket Layer (SSL) technology

The agency's Internet application, which automatically links to an Internet payment gateway, transmits the encrypted information to the selected gateway.

The gateway accepts the encrypted data via the Internet, decrypts the information, reformats the information to Processor's specifications and transmits it to Processor’s over a leased-line.

The Processor's system recognizes the authorization request as being for a Visa, MasterCard, American Express or Discover card. In the case of Visa or MasterCard, the request is transmitted to the appropriate association, which, in turn, routes the request to the member bank which issued the card. If the authorization request is for an American Express or Discover card, the Processor transmits the request to American Express or Discover respectively.

Authorization through an Internet Application (Cont.)

The card issuer (a Visa or MasterCard issuing bank or American Express or Discover) verifies that the cardholder's account is valid, and that the amount of the transaction is less than their remaining credit limit (if such a credit limit exists). The approval (with authorization number) or declination is transmitted directly back to the Processor for American Express and Discover transactions and indirectly back to the Processor through an association for Visa and MasterCard transactions.

The Processor sends the authorization response over the leased-line to the gateway.

The gateway encrypts the authorization response and forwards the response over the Internet to the agency's Internet application.

The cardholder is made aware of the response, and, if approved, is typically provided a confirmation number. If declined, customers are typically afforded the opportunity to use another card.

Valid Credit Card TransactionsThere are 3 components to every credit card transaction that

must be present in order for a transaction to be valid. If any of these three components is missing, then the cardholder has the opportunity to contest the transaction.

1.Proof the card was presented at the time of the transaction. There are only two forms of proof that the card is present.A manual imprint of the card orCard swiped in Point-of-Sale terminal

2.Signature on the Sales Draft. Every draft must be signed by the cardholder in order to be valid.

3. Promised goods and services must have been delivered at the time of the sale. In other words the cardholder must have received the services or goods that they were promised.

How do the Issuers/Processor’s make their money?

Pricing: There are many different aspects of pricing in our industry. This section will

focus on the basic pricing structures. This is the ongoing cost associated with processing cards for the merchant.

Discount Rate: For the vast majority of merchant, this is the single most important element to their pricing structure. The discount rate is a percentage of money the processor keeps out of every transaction. These monies are distributed to all of the entities involved in processing the transaction. Naturally, all merchant should be concerned that they have competitive discount rate.

Example: If a merchant is being charged a 2% discount rate based on a $100.00 ticket; the cost on this particular sales would be $2.00. Merchant would keep $98.00 for that sale. In addition to any other fees that may be associated with the transaction.

How do the Issuers/Processor’s make their money? (Cont.)

Generally speaking the processor will give the merchant one of two choices as to when they want the charges to be debited to their account.

Month End Discount : Monies are deposited into merchant’s

account within 24-48 hours from the time they batch out. Then at the end of the month, all fees are collected and debited from merchants account. Primary benefit to the merchant is having access to more of their money longer.

Daily Discount : Monies are deposited into merchants account within 24-48 hours as with month-end-discounts; however, instead of the fees being taken out at the end of the month. The fees are debited before being deposited.

To eliminate bookkeeping nightmares on the part of the processors, it is suggested that the emphasis be on “Month End Discounting”

How do the Issuers/Processor’s make their money? (Cont.)

Swiped Transaction: This type of transaction is for the merchant who business is primarily face-to-face; having the ability to swipe the card present through his processing terminal. This method is the most secured way of accepting the transactions, greatly reducing the risk for fraud; therefore, the merchant receives the lowest possible discount rate available for his type business.

Keyed Transaction: This rate is for transactions that do not have the card

present at the time of sale. Or perhaps the merchant’s processing terminal is unable to read the magnetic strip on the back of the card (which holds all of your information). Therefore, there is a need to “key in” the credit card number, expiration date, and with the new Address Verification System (AVS), you will also be prompt to enter in billing address and zip code.

Due to the card and customer not being present at the time of sale, the rates are

higher to cover the increased risk of fraud. In order for them to qualify as a swiped account, they must accept at least 80% of their sales face-to-face, with only 20% keyed. The reverse is true for keyed accounts.

How do the Issuers/Processor’s make their money? (Cont.)

Mid-Qualified Transaction: This is when a merchant who is set up as a swiped account, accepts a keyed transaction. Or a card not present transaction, which includes the billing address being passed for an authorization or sale transaction. The discount rate for this transaction is higher than the discount rate for a Qualified transaction. For the increased risk of a keyed transaction, typical industry price can average anywhere from .65% to 1.5% of the keyed transaction, higher than is charged for a swiped transaction.

Non-Qualified Transaction: This is a charge that applies to transactions that carry the most risk. Typical reasons are: International Cards, Failure to close out a batch in a timely manor (24 hours), commercial cards, and lack of information about a transaction. Most of the time it is lacking the billing address information from a keyed transaction.

However, with today’s technology and proper processing, the merchant can avoid some of these charges. With newer updated equipment that prompts your merchant for this information; the cost of upgrading can many times pay for itself, in addition to reducing the risk of fraud.

How do the Issuers/Processor’s make their money? (Cont.)

Transaction Fee: In addition to the discount fee, there is a cost per transaction for processing credit cards. Depending on the processor this fee can be called many different things and be located in several different locations within the body of their monthly billing statement.

Authorization Fees Watts Fees Per Item Fees Transaction Fees

The set range for this fee is anywhere from $0.00 (due to much higher discount rates), to as much as $!.00 per transaction. The industry average is $.20 to $.40 per transaction. As with discount rates, typically speaking, the per transaction fee for keyed transactions accounts is higher than swiped. Again, this is due to higher risk.

Example: If each transaction cost the merchant $.20 and they performed 400

transactions per month, their transaction fee cost would be $80.00, in addition to the discount rate and any other fees that may apply.

How do the Issuers/Processor’s make their money? (Cont.)

Statement / Service fee: Similar to most financial services, this is a monthly fee for receiving the statement summary of the account, as well as the service the 24 hrs / 365 days a year, service that the merchant receives. This is an area where in some cases you’ll find hidden fees being charged to the merchant.

Industry average is from $5 to $20, although $10.00 is what’s typically

seen on most merchant statements.

Monthly Minimum: This is the monthly total processing cost. The merchant will be billed whichever is greater, the sum total of discount rate and transaction fees, or the minimum, whichever, is greater.

How do the Issuers/Processor’s make their money? (Cont.)

Batch – A collection of credit card transactions saved for

submitting at one time. Usually each day. Batch fees are charged to encourage a merchant to submit his or her transactions at one time, rather than throughout the day.

Batch Settlement – An electronic bookkeeping procedure that causes all

funds from captured transactions to be routed to the merchants acquiring bank for deposit.

Card Validation Code (CVC) or Card Validation Value (CVV or CVV2) – Tool used by MasterCard or Visa to prevent fraud. It

requires that a number usually located on the back of the card above the mag-stripe be entered in to verify the card is the present and authentic. When the card is not present at time of sale.

How do the Issuers/Processor’s make their money? (Cont.)

Chargebacks If goods and services are unsatisfactory delivered or preformed

and the cardholder notifies the bank within a specific period of time after the transaction, the merchant might receive a chargeback, which means the money is taken from their account and returned to the cardholder. The steps for the chargeback are as follows:

Customer notifies their issuing bank to refund a transaction. Issuing bank notifies the acquiring bank to provide proof the

card was present.Acquiring bank notifies merchant to provide proof. (a) if merchant can’t provide proof, the checking account is

debited. (b) if merchant provides the proof, the case then may go to

arbitration.

Dealing with Interchange Fees

What's the reason for the interchange fee? Interchange compensates card issuing institutions for their risk and the expenses they incur to process transactions.

The conditions under which you accept credit cards and process transactions all affect how high the fee will be.

The interchange fee is determined by the nature of your business and the processing procedures you follow.

Hence the interchange fee for a face-to-face transaction will be less

While MOTO or ecommerce transaction will be higher

For example, a customer makes a $200 purchase, using a Visa card, at a retail store. The interchange category for this Visa transaction is CPS Retail. The discount rate is 1.95 percent. If all procedures are followed -- if the card is swiped, electronic authorization procured and transaction settled within two days -- there are no additional charges, and the fee is $3.90 to the merchant. However, if the card is hand-keyed instead of swiped, there's a 1.00% percent penalty, making your bill $5.90 instead.

What is a Basis Point?

Investopedia explains Basis Point - BPSThe relationship between percentage changes and basis points can be summarized as follows: 1% change = 100 basis points, and 0.01% = 1 basis point.

So, a bond whose yield increases from 5% to 5.5% is said to increase by 50 basis points; or interest rates that have risen 1% are said to have increased by 100 basis points.

On-line vs. Off-line debit

Online (Pin-based): When the customer enters pin number at time of sale,

the transactions are subject to only a set transaction fee regardless of the size of the ticket. The merchant has no liability for a fraud based charge back. Normally .55-.85 per transaction

Off-Line (Signature based): Transactions are processed as credit cards and subject

to discount rates, transactions fees. The transactions are subject to the same rules and regulations of credit cards.

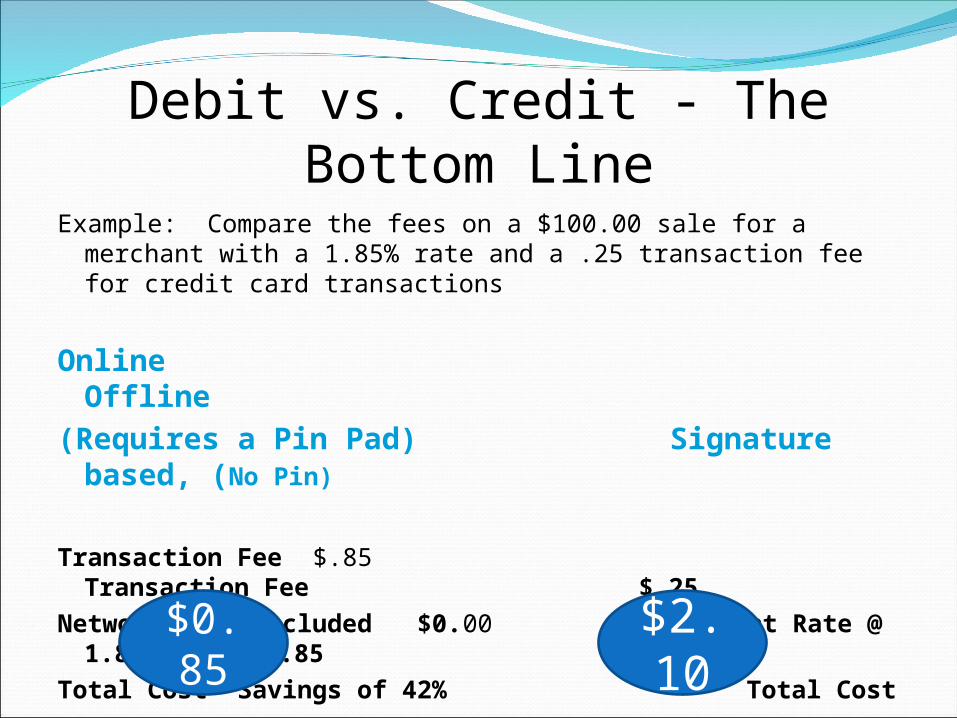

Debit vs. Credit - The Bottom LineExample: Compare the fees on a $100.00 sale for a merchant

with a 1.85% rate and a .25 transaction fee for credit card transactions

Online Offline

(Requires a Pin Pad) Signature based, (No Pin)

Transaction Fee $.85 Transaction Fee $.25

Network fee. Included $0.00 Discount Rate @ 1.85% = $1.85

Total Cost Savings of 42% Total Cost $0.8

5$2.10

Making the ChoiceBoth forms of debit acceptance let merchants offer

payment flexibility to their customers, which in turn can capture impulse buying, generate higher-ticket purchases and improve customer loyalty. But PIN-based debit transactions offer added advantages, such as:

The option to provide cash back to customers, which increases store traffic.

A fast way to move shoppers through the checkout line.

Virtual elimination of chargebacks and fraud. Higher transaction approval rates. Potential for additional revenues from surcharges.

Prospecting

Cold CallsPhone SolicitationNetworking SocialsAssociationsLead/Referral SourcesObservational

Cold Calls/Tele-Sales

Know who you are calling on and why!Get past “The Gatekeeper”! Establish Trust! Be prepared!Stop thinking like a salesperson!Start thinking like a customer service rep!Remove any expectations.HAVE FUN!

Example – Cold Calling(ask for the owner by name if possible)Hi my name is __________. I work as a Merchant Advisor and am tasked with the responsibility to talk to each of the Merchant’s in this area

with regards to PCI regulation, the erroneous fees being charged by

processor, and how it effects your business.

I do not have time now, as I have an appointment with Jim down the

street. However, I was running early and out of consideration for your time. I wanted to schedule a few minutes for me to review your current situation and show you how you can eliminate the fees, become compliant and stay

compliant at NO CHARGE TO YOU.

Does that make sense?

Set the appointment!

Note: If they hesitate, assure them you are not there to sell them any, but rather make suggestion based on your findings.

Be very a matter of fact, and non threatening.

Example - Tele-Sales

(ask for owner by name if possible) Hi my name is __________. I do not mean to bother you,

but I’m making a customer service call. Is now a good time to talk? I work as a Merchant Advisor and am tasked with the responsibility to talk to each of the Merchant’s in this area with regards to PCI regulation, the erroneous fees, being charged by processor, and how it effects your business.

I wanted to schedule a time, when it’s convenient for you, so that I may review your current situation and show you how you can eliminate the fees, become compliant and stay compliant at NO CHARGE TO YOU.

There is NO Charge for our service, and shouldn’t take up too much of your time whatsoever.

SET APPOINTMENT!

Networking Socials

BNI – Business Network International 1. Professional Marketing Organization that

helps members build business via word of mouth referrals.

2. Only one person from each professional specialty is permitted to join.

3. Because giving referrals is the cornerstone of membership, everyone becomes a virtual sales team for the members.

4. Increased exposure to many people and business, because the relationships are built on trust. You not only meet other members, you gain access to their contacts as well.

Networking Socials

Local Chamber of Commerce 1. Integrity – Positive perception by local

members, as well as a positive impact on the community.

2. Networking Functions a. Luncheons for Women b. Business after 5 meetings c. Industry Luncheons d. Golf Tournaments e. Home Shows 3. Marketing Opportunities a. Monthly News Letters b. Radio Advertizing c. Hot links to our website via business

directories

Associations

Trade Association 1. Integrity – Positive perception by local members,

as well as a positive impact on the community. 2. Referral Opportunities a. Work with other like operators/

business owners with similar interest b. Develop a reputation

c. Have them calling you 3. Marketing Opportunities a. Monthly or quarterly trade

publications b. Local events

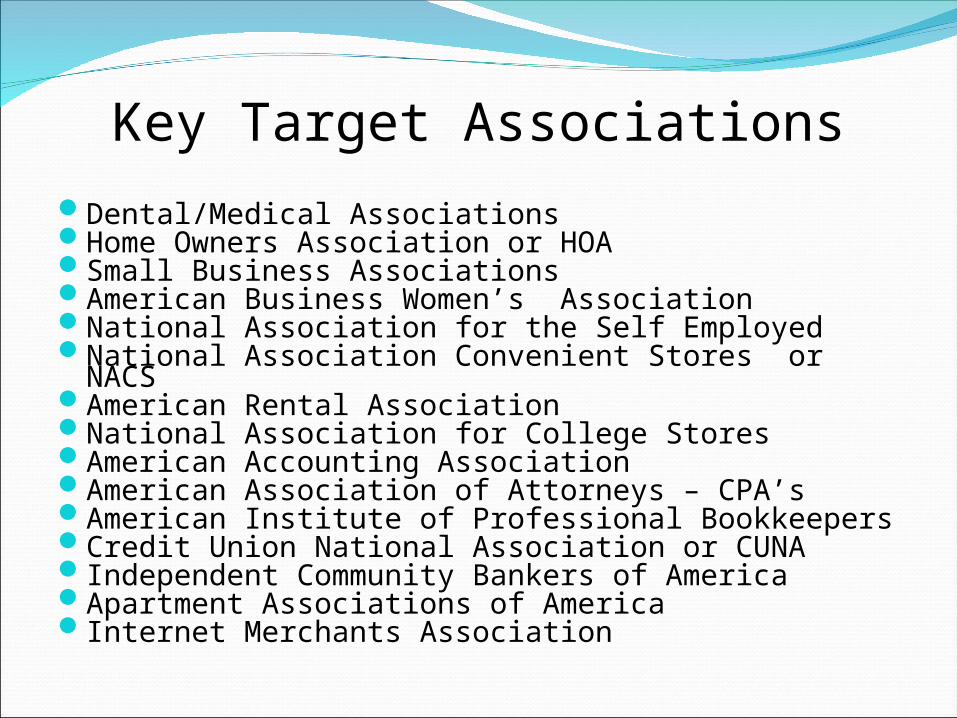

Key Target AssociationsDental/Medical AssociationsHome Owners Association or HOASmall Business AssociationsAmerican Business Women’s AssociationNational Association for the Self EmployedNational Association Convenient Stores or NACSAmerican Rental AssociationNational Association for College StoresAmerican Accounting AssociationAmerican Association of Attorneys – CPA’sAmerican Institute of Professional BookkeepersCredit Union National Association or CUNAIndependent Community Bankers of America Apartment Associations of AmericaInternet Merchants Association

Lead/Referral Sources

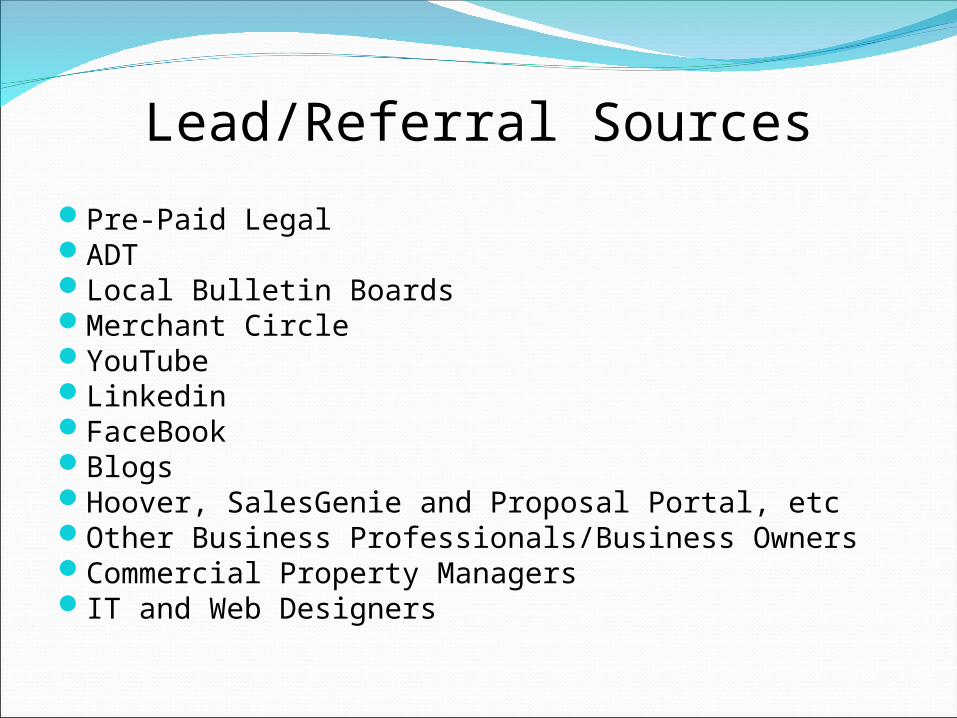

Pre-Paid LegalADTLocal Bulletin BoardsMerchant CircleYouTube LinkedinFaceBookBlogsHoover, SalesGenie and Proposal Portal, etcOther Business Professionals/Business OwnersCommercial Property ManagersIT and Web Designers

Observational

Sales opportunities are everywhere, if you look for them. Even when you are at lunch, at a traffic light or just driving down the street. Keep a digital recorder with you at all times.

Coming SoonNew construction – strip malls and office parksNew locationLocal auto repair shopsLocal eateries a. Electricians b. Plummer’s c. Any other mobile service vehicles