bank of baroda

TRANSCRIPT

1

INTRODUCTION 1.1 EVOLUTION OF BANK OF BARODA

Bank of Baroda (BoB) is an Indian state-owned banking and financial

services company headquartered in Vadodara (earlier known as Baroda) in

Gujarat, India. It is the second-largest bank in India, after Bank of Baroda, and

offers a range of banking products and financial services to corporate and retail

customers through its branches and through its specialized subsidiaries and

affiliates.

The bank was founded by the Maratha, maharaja of Baroda, H. H. Sir Sayajirao

Gaekwad iii on 20 July 1908 in the princely state of Baroda, in Gujarat. The bank,

along with 13 other major commercial banks of India, was nationalized on 19 July

1969, by the government of India and has been designated as a profit-making

public sector undertaking (PSU).Bank of Baroda is one of the big four banks of

India, along with Bank of Baroda, ICICI bank and Punjab.

HISTORY

1908 to 1959

In 1908, Maharaja Sayajirao Gaekwad III, one of the knights of the Maratha

Kingdom, set up the Bank of Baroda (BoB), with other stalwarts of industry such

as Sampatrao Gaekwad, Ralph Whitenack, Vithaldas thakersey, Tulsidas

kilachand and NM Chokshi. Two years later, BOB established its first branch

in Ahmedabad.

1960’s to 1970’s

In 1961, BOB merged in new citizen bank ofIndia. This merger helped it increase

its branch network in Maharashtra. BoB also opened a branch in Fiji. The next

year it opened a branch in Mauritius. Bank of Baroda in 1963, BoB acquired Surat

banking corporation in Surat, Gujarat. The next year BoB acquired two banks:

Umbergaon people’s bank in southern Gujarat and Tamil Nadu central bank

in Tamil Nadu state.Bank of Barodaacquired bank ofIndia's operations in Uganda.

After two years later, Bank of Barodaopened a branch in Dubai and Abu

2

Dhabi.Back in India, in 1975, Bank of Barodaacquired the majority shareholding

and management control in UttarPradesh. Later on, Nainital bank has expanded

to Uttarakhand state.

1980’s to 1990’s

In this period, Bank of Barodaopened a branch in Bahrain and a representative

office in Sydney, Australia. In HongKong IUB international finance, a licensed

deposit taker was established by Bank of Baroda, union bank ofIndiaand Indian

bank in which each bank took an equal share. Back in India, in 1988, Bank of

Barodaacquired trader’s bank, which had a network of 34 branches in Delhi.Bank

of Barodaincorporated its operations in Kenya into a local subsidiary with a small

group of shares quoted on the Nairobi stock exchange. This bank also entered in

the capital market with an initial public offering (IPO). The government ofIndiais

still the largest shareholder, owning 66% of the bank equity.

2000’s to 2010’s

2005: Bank of Barodabuilt a global data center(dc) in Mumbai for running

its centralized banking solution (CBS) and other applications in more than

1,900 branches across Indiaand 20 other counties where the bank operates.

Bank of Barodaalso opened a representative office in Thailand.

2006: Bank of Barodaestablished an offshore banking unit (OBU) in

Singapore.

2007: in its centenary year, Bank of Baroda’s total business crossed

2.09 trillion (short scale), its branches crossed 2000, and its global customer

base 29 million people.

2008: Bank of Barodaopened a branch in Guangzhou, china (02/08/2008)

and in Kenton, harrowsUnited Kingdom. Bank of Barodaopened a joint

venture life insurance company with Andhra bankand legal and

general (UK) called India first life insurance company.

In period Malaysia awarded a commercial banking license to a locally

incorporated bank to be jointly owned by Bank of Baroda. Bank of Baroda opened

an electronic banking service unit (EBSU) was opened at Hamriya free zone,

3

Sharjah (UAE). It also opened four new branches in existing operations in Uganda,

Kenya (2), and Guyana.

1.2 OBJECTIVE

1) To study products and services provided by Bank of Baroda.

2) To do the financial analysis ofBank of Barodafor the year ended 31stmarch

2010, 2011, 2012, 2013and 2014.

1.3 METHODOLOGY

We have adopted following methodology as regards collection, analysis and

presentation of the data

A. Collection of data: required data have been collected from the secondary

sources such as annual reports textbooks, websites etc.

B. Analysis and presentation: data is analyzed using comparative and ratio

analysis method and is printed in the form of tables and graphs.

1.4 SCOPE OF STUDY

The scope of study has been restricted only to the study of products and services

offered by Bank of Barodaand its financial analysis for the years 2010, 2011, 2012,

2013, 2014.

1.5 LIMITATIONS

1) The project is based only on the information provided by annual reports which

are themselves subjected to serious limitations. Ratio also suffers from some

limitations and hence the same limitations may reflect in the project.

2) The project has been done by taking into consideration the annual reports of

only five years.

3) Capital adequacy ratio not calculated because of lack of information.

4

PRODUCTS AND SERVICES

Personal banking

Personal banking is a form of investment where the products and services a bank

is offering are customized to meet the needs of the customers.Personal banking

offered by Bank of Barodato its customers encompasses a range of products and

services. The two main categories of personal are deposits and advances.

Deposits

The type of deposits offered the banks are of two types:

1. Demand deposits

2. Term deposits

Demand deposits:-

A) Current account

B) Savings account

Term deposits:-

The various schemes offered by Bank of Baroda for term deposits are as follows:

A) CAPITAL GAIN ACCOUNT SCHEME, 1988

B) SPECIAL TERM DEPOSITS

C) RECURRING DEPOSITS

5

Advances

A. HOME LOANS

B. CAR LOANS

C. EDUCATIONAL LOANS

D. GOLD LOANS

NRI services

BOBoffer a red carpet welcome to all NRI to bank with us. As a premier

nationalized bank in India, with comprehensive banking experience world-wide,

and by virtue of our consistent track record of profit making since 1908, BOB are

confident of meeting all your banking requirements.

BOB’s wide network of foreign branches, offices and correspondent relations at

convenient business locations all round the world, which is the largest among any

bank in India, will ensure a smooth and safe banking experience.

BOB continue to cherish our rich ethnic traditional values and culture, during our

personal interface. Yet BoB are speedily repositioning us in the e-millennium era

of banking in India, to take care of your changing needs and expectations. BOB’s

information technology strategies are directed towards enabling us to provide

you with a state of the art customer convenience, thereby facilitating a global

banking experience.

Internet banking

The internet banking portal ofBank of Baroda enables its retail banking customers

to operate their accounts for anywhere anytime, removing the restrictions

imposed by geography and time. It is a platform that enables the customers to

carry out their banking activities from their desktop, aided by the power and

6

convenience of the internet. Internet banking enables the customers to carry out

his online bank transaction.

Mobile banking

Mobile banking is a service provided by Bank of Baroda through which a customer

can carry out limited banking transactions from anywhere and at any time. For

example do the balance inquiriesof the accounts, transfer funds within and

outside the bank, top up or recharge etc. These facilities can be availed by the

customer by using the Bank of Baroda app on their mobile phone.

ATM services

Bank of Baroda offers theircustomer’s convenience of over 26,000 ATM’s in India,

the largest network in the country and continuing to expand fast! This means that

one can transact free of cost at the ATM’s of state bank group and wholly on

subsidiary viz. Bank of Baroda commercial and international bank ltd. Using the

BOB ATM-cum-debit (cash plus )card. ATM service allows the customers to

withdraw cash from Bank of BarodaATM’s wherever they go. The minimum

amount of cash that can be withdrawn is rs.100/- and maximum is rs.40, 000/- per

day. Also the customer can get their balance inquiry and the mini statement of

their accounts, transfer funds to ATM to ATM, etc.

Locker services

Lockers are available for safe deposits of valuable as per the requirement of the

customer. Lockers of three sizes are available, small, medium and large twelve

visited in a year to the locker are free. For additional visit charge ofrs.50/- per visit

is levied.

7

FINANCIAL ANALYSIS

3.1Capital adequacy

Capital adequacy is the capital expected to maintain balance with the risks

exposure of the financial institution such as credit risk, market risk and

operational risk, in order to absorb the potential losses and protect the financial

institution’s debt holder. “Meeting statutory minimum capital requirement is the

key factor in deciding the capital adequacy and maintaining an adequate level of

capital is a critical element.

3.1.1Capital adequacy ratio (CAR)

Capital adequacy ratio is propounded to ensure that banks can take up a

reasonable level of losses arising from operational losses. The higher the car ratio,

indicates stronger the bank and the more will be the protection to investors.The

banks are required to maintain 9% capital adequacy ratio as per latest RBI norms.

Car = (tire –i capital + tire-ii capital)

Tire 1 capital (core capital) is shareholders equity capital. Tire 2capital

(supplementary capital) are the bank’s loan loss reserves plus subordinated debt

which consist of bonds sold to raise funds. Risk –weighted assets are the weighted

total of each class of assets and off –balance sheet asset exposures with weights

related to the risk associated with each type of assets.

Year 2010 2011 2012 2013 2014 Capital adequacy ratio

12.84% 13.02% 12.95% 12.09% 11.66%

8

In the above table and graph, we see that the capital adequacy ratio has been

fluctuating. Theratio was the highest at 13.02 in the year 2011. In 2010 the ratio

was 12.84, which increased in year 2011 to 13.02, in 2012 the ratio was 12.95, in

2013 the ratio was 12.09, in 2014 the ratio is11.66, however the ratio is above 9%

in each of the year.

10.5

11

11.5

12

12.5

13

13.5

2010 20112012

20132014

Capital adequacy ratio (IN %)

Capital adequacy ratio (IN %)

9

3.1.2Debt equity ratio

The debt to equity ratio is a financial ratio indicating the relative proportion

ofshareholders equity and debt used to finance co. Assets. The ratio is also known

as risk, gearing or leverage. The 2 components are often taken from banks

balance sheet of statement of financial position, but the ratio may also be

calculated using market values for both, if the co. Debt and equity publicly traded,

or using a combination of book value for debt and market value for equity

financial.

Value in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014

Debt 134042707 223783296 235980584 265529425 369763007

Shareholders net worth

157245900 285163033 218265720 271774219 221081700

Debt to equity ratio= Total borrowings

Shareholders net worth

Year 2010 2011 2012 2013 2014

Debt to equity ratio

0.85 0.78 1.08 0.97 1.67

10

In the above table and graph, we see that the debt to equity ratio has been

fluctuating. The ratio was the highest at 1.67 in the year2014. In 2010 the ratio

was 0.85. In year 2011 the ratio was 0.78, in 2012 the ratio was 1.08, in 2013 the

ratio was 0.97and in 2014 the ratio is 1.67.

Favorably the ratio should be less than 1, which means for every 1 rupee of equity

there is less than 1 rupee of debt. In the year 2010, 2011, 2013 the ratio is 0.85,

0.78 and 0.97 respectively which is a good sign, it means that for every 1 rupee of

owners fund there is less than 1 rupee of outside fund. On the contrary in the

year 2012 and 2014 the ratio is 1.08 and 1.67 which is not a good sign, it means

that for every 1 rupee of owners fund there is more than 1 rupee of outside fund.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

20102011

20122013

2014

DEBT TO EQIUTY

DEBT TO EQIUTY

11

3.1.3Advances to assets ratio

This ratio indicates the relationship between the total advances and total assets.

This ratio indicates bank aggressiveness in lending which ultimately produces

better profitability. Higher ratio is preferred than a lower one.

Values in crores: 000‘s are omitted

Year 2010 2011 2012 2013 2014

Advances 1777118975 2320851112 2920771369 3336251972 4037153727 Assets 2842767651 3662137657 4574120058 5593883319 6761141057

Advances to assets ratio = Total advances x 100

Total assets

Year 2010 2011 2012 2013 2014 Advances to assets ratio

62.51% 63.37% 63.85% 59.64% 59.71%

12

In the above table and graph, we see that the advance to assets ratio has been

fluctuating. The ratio was the highest at 63.85% in the year 2012. In 2010 the

ratio was 62.51%, in year 2011 the ratio was 63.37%, in 2012 the ratio was

63.85%, in 2013 the ratio was 59.64% and in 2014 the ratio is 59.71%.

This ratio should be maximum as possible because the main function of the bank

is to give out advances. If there is more lending more will be the income from its

operations. There is no use of having idol assets.

In the years 2010, 2011 and 2012 the percentage of advances had been increasing

but in the year 2013 and 2014 the percentage of advances has reduced in

comparison. The bank should see that the ratio should be high so they can yield

maximum profits from interest on lending.

57

58

59

60

61

62

63

64

20102011

20122013

2014

Advances to assets ratio (in %)

ADVANCES TO ASSETS (IN%)

13

3.1.4Government securities to total investment ratio

This ratio reflects the risk involved in a bank investment. It is calculated by

dividing the amount invested in government securities by total investments. Since

government securities are risk free, higher the proportion of government

securities in total investment, lower will be the risk involved in bank investment

and vice-versa.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014 Government securities

526801503 631317455 733574682 1067594785 1015115501

Total investment

631632703 741544187 866970036 1256170527 1221128639

Government securities to total investment ratio= Government securities x 100

Total investment

Year 2010 2011 2012 2013 2014

Government securities to total investmentratio

83.40% 85.13% 84.61% 84.98% 83.12%

14

In the above table and graph, we see that the government security to total

investment has been fluctuating. The ratio was the highest at 85.13% in the year

2011. In 2010 the ratio was 83.40%, in year 2011 the ratio was 85.13%, in 2012

the ratio was 84.61%, in 2013 the ratio was 84.98% and in 2014 the ratio is

83.12%.

Government securities are the most secured investments that a bank can have. In

the above graph we can see that the investments in government securities are

always above 80% which is good, it ensures constant rate of returns to the bank.

All investments cannot be made up of government securities because they tend

to have a low rate of return. There should be a balance between government

securities and other investments.

82

82.5

83

83.5

84

84.5

85

85.5

2010 2011 20122013

2014

Government securities to total investment ratio(in %)

GOVERNMENT SECURITIES TOTOTAL INVESTMENT (IN %)

15

3.2Assets quality

Assets quality is related to the left hand side of the bank balance sheet. Bank

manager are concerned with the quality of their loans since that provides earning

for the bank. Loan quality and asset quality are two terms with basically the same

meaning. A bad quality loan has higher probability ofbecoming nonperforming

assets (NPA’s) with no return.

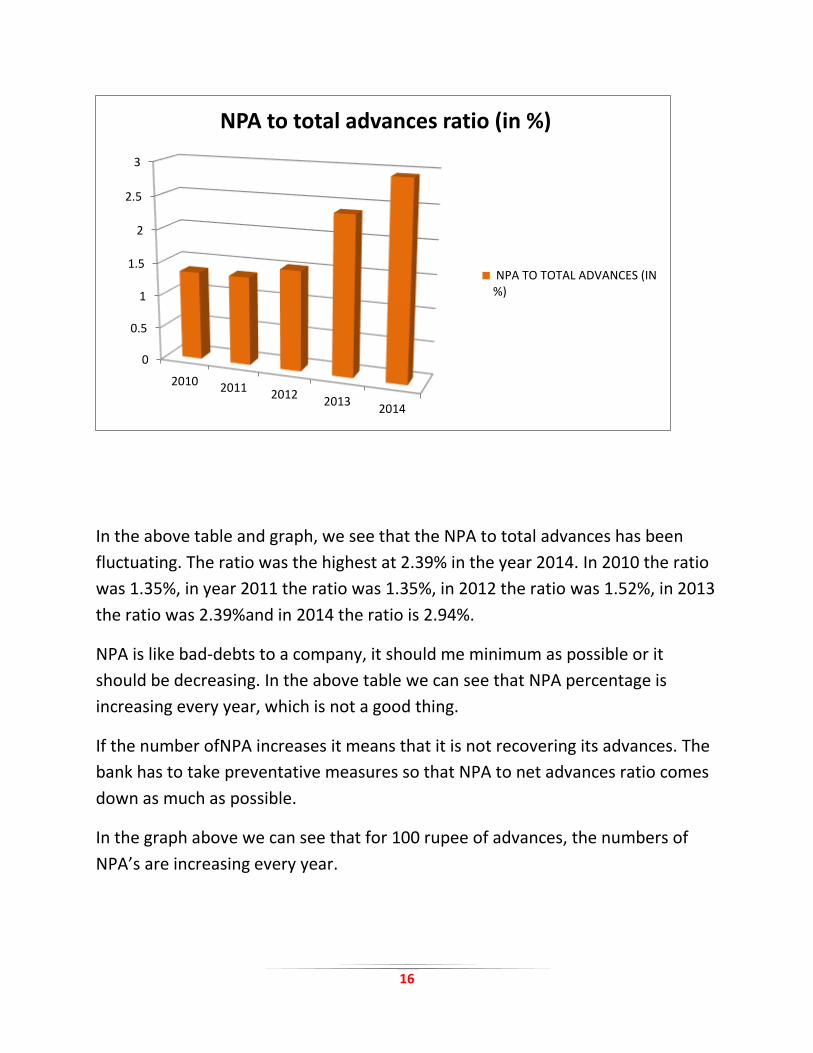

3.2.1 NPA to total advances ratio

It is the most standard measure to judge the assets quality, measuring the net

non-performing assets as a percentage of total advances.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014 Non-performing assets

24006900 31525000 44647500 79825800 118759000

Total advances

1777118975 232085112 2920771369 3336251972 4037153727

NPA to total advances ratio = Nonperforming assets x 100

Total advances

Year 2010 2011 2012 2013 2014

NPA to total advancesratio

1.35% 1.35% 1.52% 2.39% 2.94%

16

In the above table and graph, we see that the NPA to total advances has been

fluctuating. The ratio was the highest at 2.39% in the year 2014. In 2010 the ratio

was 1.35%, in year 2011 the ratio was 1.35%, in 2012 the ratio was 1.52%, in 2013

the ratio was 2.39%and in 2014 the ratio is 2.94%.

NPA is like bad-debts to a company, it should me minimum as possible or it

should be decreasing. In the above table we can see that NPA percentage is

increasing every year, which is not a good thing.

If the number ofNPA increases it means that it is not recovering its advances. The

bank has to take preventative measures so that NPA to net advances ratio comes

down as much as possible.

In the graph above we can see that for 100 rupee of advances, the numbers of

NPA’s are increasing every year.

0

0.5

1

1.5

2

2.5

3

2010 20112012

20132014

NPA to total advances ratio (in %)

NPA TO TOTAL ADVANCES (IN%)

17

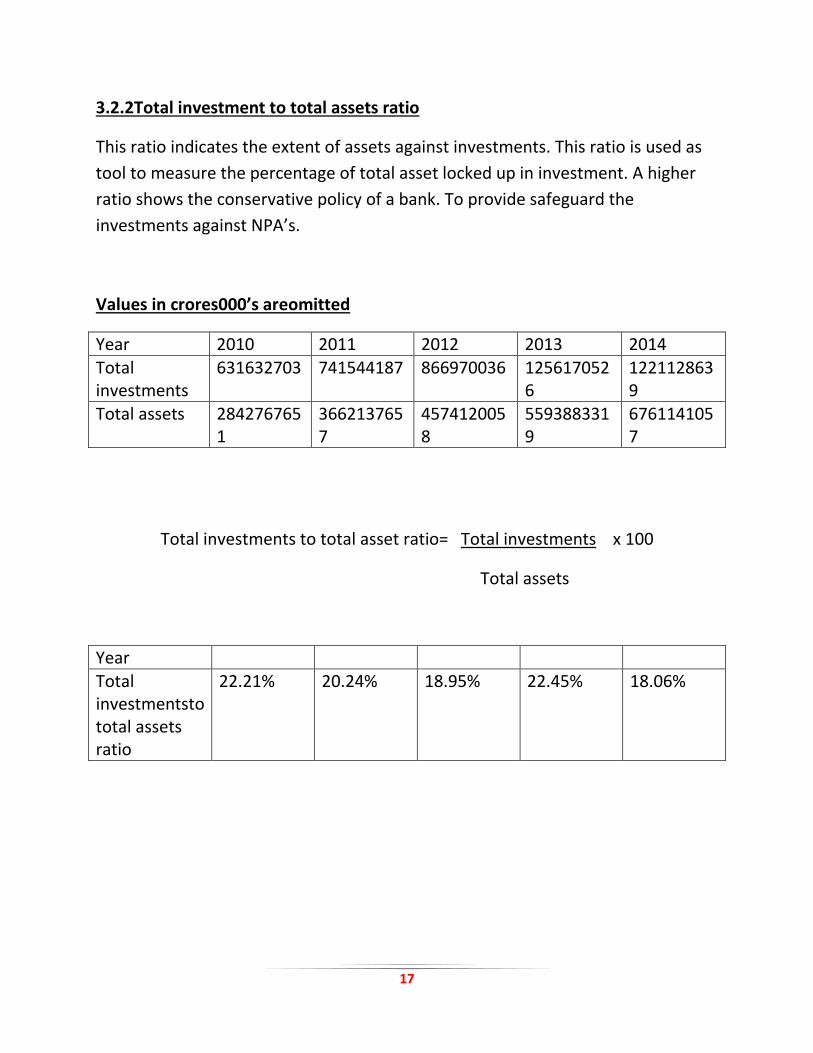

3.2.2Total investment to total assets ratio

This ratio indicates the extent of assets against investments. This ratio is used as

tool to measure the percentage of total asset locked up in investment. A higher

ratio shows the conservative policy of a bank. To provide safeguard the

investments against NPA’s.

Values in crores000’s areomitted

Year 2010 2011 2012 2013 2014

Total investments

631632703 741544187 866970036 1256170526

1221128639

Total assets 2842767651

3662137657

4574120058

5593883319

6761141057

Total investments to total asset ratio= Total investments x 100

Total assets

Year

Total investmentsto total assets ratio

22.21% 20.24% 18.95% 22.45% 18.06%

18

In the above table and graph, we see that the total investments total assets ratio

has been fluctuating. The ratio was the highest at 22.45% in the year 2013. In

2010 the ratio was 22.21%, in year 2011 the ratio was 20.24%, in 2012 the ratio

was 18.95%, in 2013 the ratio was 22.45% and in 2014 the ratio is 18.06%.

In the above graph we can see that on average the ratio is about 20% every year.

This shows us that the bank has 20% of its assets locked up as investments. This

ensures provision for any NPA’s which may occur.

0

5

10

15

20

25

2010 20112012

20132014

Total investments to total asset ratio (in %)

NPA TO TOTAL ADVANCES (IN%)

19

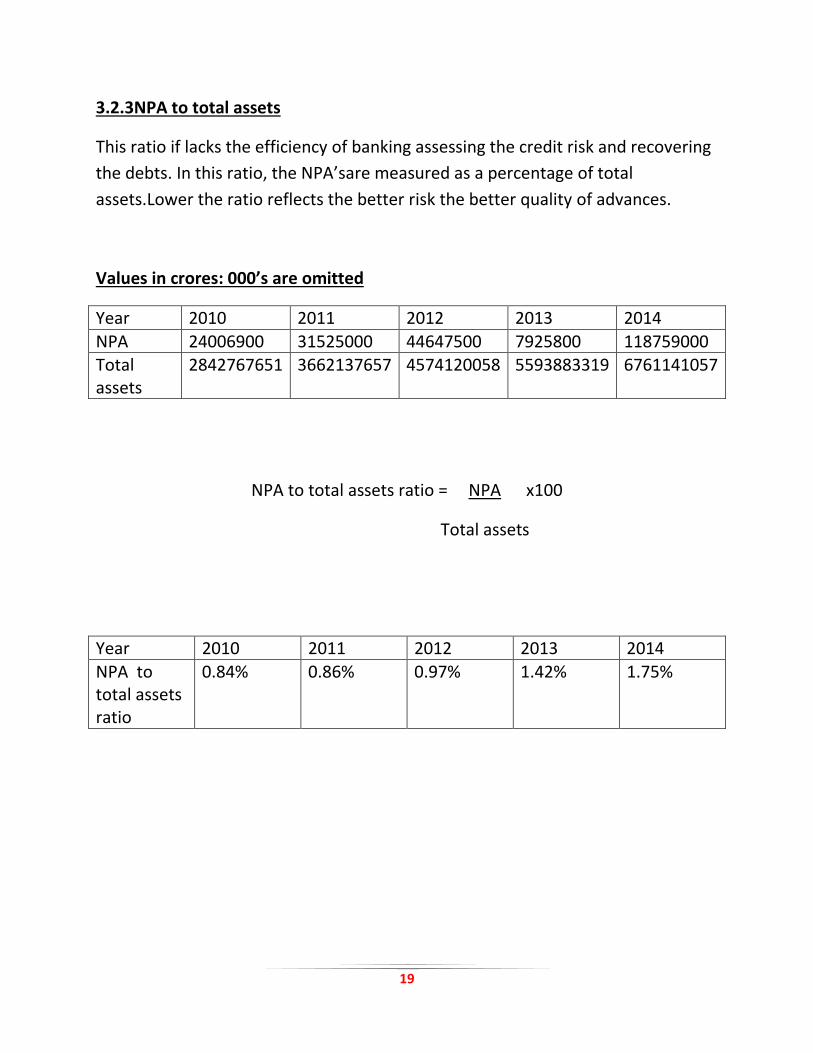

3.2.3NPA to total assets

This ratio if lacks the efficiency of banking assessing the credit risk and recovering

the debts. In this ratio, the NPA’sare measured as a percentage of total

assets.Lower the ratio reflects the better risk the better quality of advances.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014

NPA 24006900 31525000 44647500 7925800 118759000 Total assets

2842767651 3662137657 4574120058 5593883319 6761141057

NPA to total assets ratio = NPA x100

Total assets

Year 2010 2011 2012 2013 2014

NPA to total assets ratio

0.84% 0.86% 0.97% 1.42% 1.75%

20

In the above table and graph, we see that the NPA total asset has been

fluctuating. The ratio was the highest at 1.75% in the year 2014. In 2010 the ratio

was 0.84%, in year 2011 the ratio was 0.86%, in 2012 the ratio was 0.97%, in 2013

the ratio was 1.47%and in 2014 the ratio is 1.75%.

NPA means bad debts to a company, the bank should see that the NPA levels are

kept minimum as possible. If NPA is low the returns on the asset is of high quality.

In the above table we can see that the NPA figure is increasing, which is not good.

The bank has to take measures to reduce the level ofNPA. If the NPA levels

increase the income or returns on their investments/advances will reduce.

In the graph above we can see that for every 100 rupee of asset the number of

NPA’s is increasing every year. The bank has to take measures to correct its NPA’s.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2010 20112012

20132014

NPA to total assets ratio (in %)

NPA TO TOTAL ASSETS RATIO(IN %)

21

3.3Management efficiency

Ratios that are typically used to analyze how well a bank uses its assets and

liabilities internally.Efficiency ratio can calculate the turnover of receivables, the

replacement of liabilities, the quality and usage of equity and the general use of

inventory and machinery.

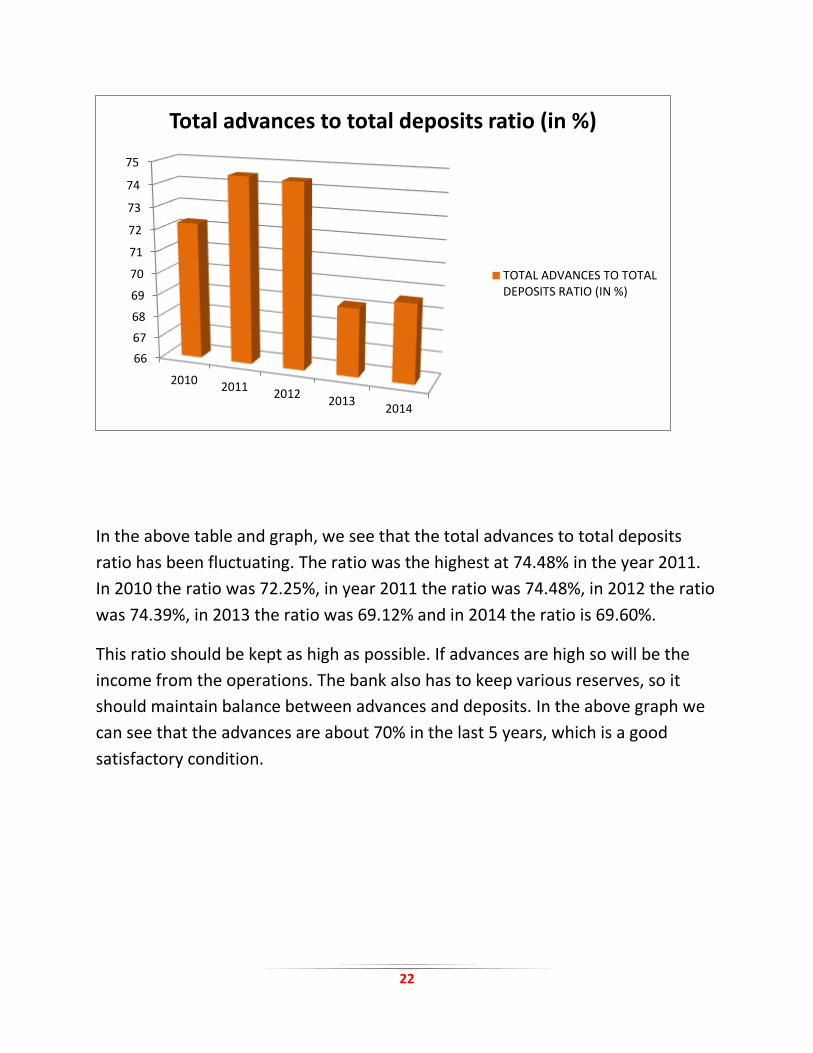

3.3.1Total advances to total deposits ratio

This ratio evaluate the efficiency and capabilities of the banks management in

applying the deposits (including the receivables) available excluding the other

funds viz. Equity capital etc. Into reach earning advances.

Value in crores: 000’sare omitted

Year 2010 2011 2012 2013 2014 Total advances

1777118975 2320851112 2920771369 3336251972 4037153727

Total deposits

2459511455 3116032489 3926159450 4826388930 5799970560

Total advances to total deposits ratio = Total advances X 100

Total deposits

Year 2010 2011 2012 2013 2014 Total advances to total deposits ratio

72.25% 74.48% 74.39% 69.12% 69.60%

22

In the above table and graph, we see that the total advances to total deposits

ratio has been fluctuating. The ratio was the highest at 74.48% in the year 2011.

In 2010 the ratio was 72.25%, in year 2011 the ratio was 74.48%, in 2012 the ratio

was 74.39%, in 2013 the ratio was 69.12% and in 2014 the ratio is 69.60%.

This ratio should be kept as high as possible. If advances are high so will be the

income from the operations. The bank also has to keep various reserves, so it

should maintain balance between advances and deposits. In the above graph we

can see that the advances are about 70% in the last 5 years, which is a good

satisfactory condition.

66

67

68

69

70

71

72

73

74

75

20102011

20122013

2014

Total advances to total deposits ratio (in %)

TOTAL ADVANCES TO TOTALDEPOSITS RATIO (IN %)

23

3.3.2Returns on equity

It is a measure of the profitability of the bank. In calculation of this ratio, profit

after tax is expressed as a percentage of equity.

Year 2010 2011 2012 2013 2014

Net profit (000’s are omitted)

32498728 45159105 53872358 49829573 52819205

Number of equity share

365527700 392807300 412384600 422517500 430676300

Returns on equity= Net profitx 100

No. of equity share

Year 2010 2011 2012 2013 2014 Returns on equity

8.89% 11.49% 13.06% 11.79% 12.26%

24

In the above table and graph, we see that the return on equity has been

fluctuating. The ratio was the highest at 13.06% in the year 2012. In 2010 the

ratio was 8.89%, in year 2011 the ratio was 11.49%, in 2012 the ratio was 13.06%,

in 2013 the ratio was 11.79% and in 2014 the ratio is 12.26%.

This ratio gives us the earning per share issued. The returns should be kept at a

constant/increasing rate which is also very attractive. In the above graph we can

see that the average returns are about 11.5% of the net earnings of the bank. The

rate is very good. A return on equity has increased every year, which has yielded

more return to the shareholders.

0

2

4

6

8

10

12

14

20102011

20122013

2014

RETURNS ON EQUITY (IN %)

RETURNS ON EQUITY (IN %)

25

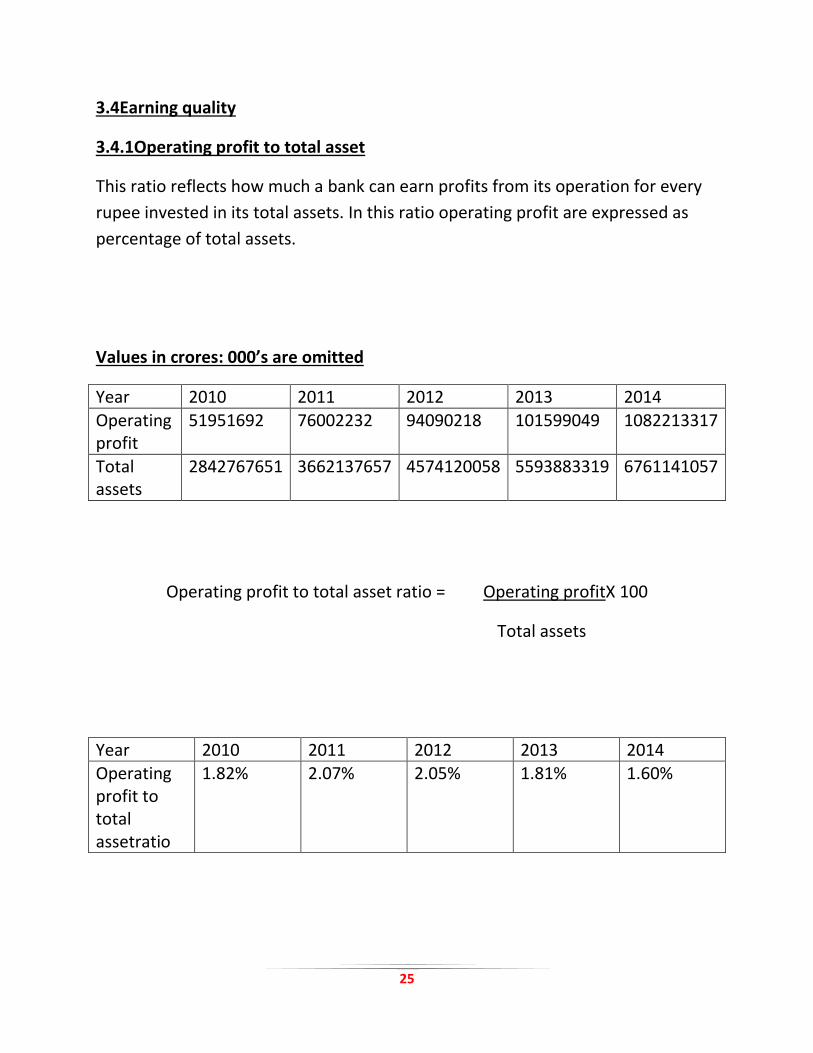

3.4Earning quality

3.4.1Operating profit to total asset

This ratio reflects how much a bank can earn profits from its operation for every

rupee invested in its total assets. In this ratio operating profit are expressed as

percentage of total assets.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014

Operating profit

51951692 76002232 94090218 101599049 1082213317

Total assets

2842767651 3662137657 4574120058 5593883319 6761141057

Operating profit to total asset ratio = Operating profitX 100

Total assets

Year 2010 2011 2012 2013 2014 Operating profit to total assetratio

1.82% 2.07% 2.05% 1.81% 1.60%

26

In the above table and graph, we see that the operating profit to total asset has

been fluctuating. The ratio was the highest at 2.07% in the year 2011. In 2010 the

ratio was 1.82%, in year 2011 the ratio was 2.07%, in 2012 the ratio was 2.05%, in

2013 the ratio was 1.81% and in 2014 the ratio is 1.60%.

In the above graph we can see that the ratio is always above 1.5% which is good,

it means that for every 100 rupees invested the bank can get 1.5% increase in the

returns it will give. For example if we invest Rs.100 than at the end of the year we

will get rs101.5 as our returns.

0

0.5

1

1.5

2

2.5

2010 20112012

20132014

Operating profit to total asset ratio (in %)

OPERATING PROFIT TO TOTALASSET RATIO (IN %)

27

3.4.2Net profit to total assets

This ratio reflects the return in assets employed or the efficiency in utilization of

assets. It is calculated by dividing the net profits with the total assets of the bank.

Higher ratio reflects better earning potential of a bank in the future.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014

Net profit 32498728 45159105 53872358 49829573 52819205 Total assets

2842767651 3662137657 4574120058 5593883319 6761141057

Net profit to total assets ratio = Net profit X 100

Total assets

Year 2010 2011 2012 2013 2014

Net profit to total assets ratio

1.14% 1.23% 1.17% 0.89% 0.78%

28

In the above table and graph, we see that the net profit to total asset ratio has

been fluctuating. The ratio was the highest at 1.23% in the year 2011. In 2010 the

ratio was 1.14%, in year 2011 the ratio was 1.23%, in 2012 the ratio was 1.17%, in

2013 the ratio was 0.89% and in 2014 the ratio is 0.78%.

In the above graph we can see that the ratio is on an average 1% every year. It

means that for every 100 rupees invested the bank can get 1% increase in the

returns it will give. For example if we invest Rs.100 than at the end of the year we

will get rs101 as our returns. An increase in this ratio means higher amounts of

net profit i.e.Income from investment.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

2010 20112012

20132014

NET PROFIT TO TOTAL ASSETS RATIO (IN %)

NET PROFIT TO TOTAL ASSETSRATIO (IN %)

29

3.4.3Interest income to total income ratio

Interest income is considered as prime source of revenue for bank. The interest

income to total income reflects the capability of the bank in generating income

from its lending business.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014

Interest income

172348186 225133054 304884936 364420574 404628927

Total income

202001151 258004056 345889102 409526805 460180460

Interest income to total income ratio = Interest incomeX 100

Total income

Year 2010 2011 2012 2013 2014 Interest income to total income ratio

85.32% 87.25% 88.14% 88.98% 87.92%

30

In the above table and graph, we see that the interest income to total income

ratio has been fluctuating. The ratio was the highest at 88.98% in the year 2013.

In 2010 the ratio was 85.32%, in year 2011 the ratio was 87.25%, in 2012 the ratio

was 88.14%, in 2013 the ratio was 88.98%and in 2014 the ratio is 87.92%.

This ratio shows the income from the operations of the bank. High ratio will

indicate the performance of the bank from its operations. Interestearned should

be as high as possible, as the major function of the bank is lending of funds to the

customers.

In the above graph we can see that the ratio is always above 85%. This means that

the income is generated from the operations of the business.The bank has to see

that the ratio is maintained at high levels.

83

84

85

86

87

88

89

2010 20112012

20132014

INTEREST INCOME TO TOTAL INCOME (IN %)

INTEREST INCOME TO TOTALINCOME (IN %)

31

3.5Liquidity

Risk of liquidity can have an effect on the image of bank. Liquidity is a crucial

aspect which reflects banks’ ability to meet its financial obligation. An adequate

liquidity position means a situation, where organization can obtain sufficient

liquid fund, either by increasing liabilities or by converting its assets into cash.

3.5.1Liquid assets to total assets ratio

This ratio measures the overall liquidity position of the bank. The liquid asset

include cash in hand, money at call and short notice, balance with reserve bank

ofIndia and balance with banks (India and abroad).total asset include the

revaluation of all the assets.

Values in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014 Liquid asset

365694792 514237272 658103467 877020666 1343556680

Total asset

2842767651 3662137657 4574120058 5593883319 6761141057

Liquid assets to total assets= liquid assetsX 100

Total assets

Years 2010 2011 2012 2013 2014 Liquid assets to total assets ratio

12.86% 14.04% 14.38% 15.67% 19.87%

32

In the above table and graph, we see that the liquid assets to total assets ratio has

been fluctuating. The ratio was the highest at 19.87% in the year 2014. In 2010

the ratio was 12.86%, inyear 2011 the ratio was 14.04%, in 2012 the ratio was

14.38%, in 2013 the ratio was 15.67% and in 2014 the ratio is 19.87%.

This ratio shows the assets kept as liquid form or can be liquidated as easily and

as fast as possible. The ratio should be kept at a balanced rate. Lending and

liquidity have to be kept balanced.

In the above graph we can see that the ratio is increasing and is above 12%. This

ratio ensures that the bank will have enough liquid assets in order to cope-up

with sudden demand for withdrawals.

0

2

4

6

8

10

12

14

16

18

20

20102011

20122013

2014

LIQUID ASSETS TO TOTAL ASSETS (IN %)

LIQUID ASSETS TO TOTALASSETS (IN %)

33

3.5.2Liquid asset to total depositsratio

This ratio measures the liquidity available to the depositor of a bank. It is

calculated by dividing the liquid asset with total deposits.

Value in crores: 000’s are omitted

Year 2010 2011 2012 2013 2014

Liquid assets

365694792 514237272 568103467 877020666 1343556680

Total deposits

2459511455 3116032489 3926159450 4826388930 5799970560

Liquid assets to total deposits ratio = Liquid assets x 100

Total deposit

Year 2010 2011 2012 2013 2014 Liquid assets to total deposits ratio

14.86% 16.50% 16.76% 18.17% 23.16%

34

In the above table and graph, we see that the liquid assets to total deposits ratio

has been fluctuating. The ratio was the highest at 23.16% in the year 2014. In

2010 the ratio was 14.86%, in year 2011 the ratio was 16.50%, in 2012 the ratio

was 16.76%, in 2013 the ratio was 18.17% and in 2014 the ratio is 23.16%.

This ratio shows the percentage of liquid assets /investment in comparison to the

total deposits available in the bank .the bank should maintain balance between

the liquid assets and its advances in order to ensure constant flow of withdrawals

to the customer.

In the above graph we can see that the ratio is increasing every year which is a

sign showing that the bank is maintaining a proper balance.

0

5

10

15

20

25

20102011

20122013

2014

Liquid assets to total deposits (in %)

LIQUID ASSETS TO TOTALDEPOSITS (IN %)

35

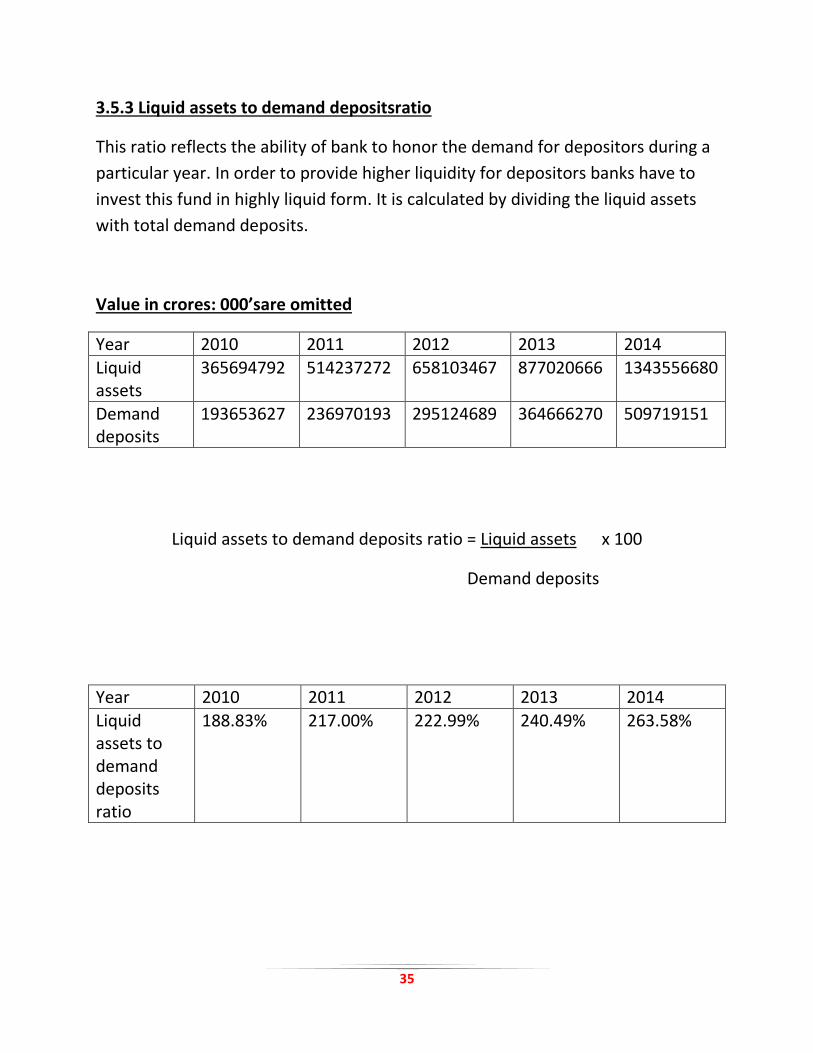

3.5.3 Liquid assets to demand depositsratio

This ratio reflects the ability of bank to honor the demand for depositors during a

particular year. In order to provide higher liquidity for depositors banks have to

invest this fund in highly liquid form. It is calculated by dividing the liquid assets

with total demand deposits.

Value in crores: 000’sare omitted

Year 2010 2011 2012 2013 2014

Liquid assets

365694792 514237272 658103467 877020666 1343556680

Demand deposits

193653627 236970193 295124689 364666270 509719151

Liquid assets to demand deposits ratio = Liquid assets x 100

Demand deposits

Year 2010 2011 2012 2013 2014

Liquid assets to demand deposits ratio

188.83% 217.00% 222.99% 240.49% 263.58%

36

In the above table and graph, we see that the liquid assets to demand deposits

ratio have been fluctuating. The ratio was the highest at 260.58% in the year

2014. In 2010 the ratio was 188.83%, in year 2011 the ratio was 217%, in 2012 the

ratio was 222.99%, in 2013 the ratio was 240.49% and in 2014 the ratio is

263.58%.

This ratio shows the percentage of liquid assets /investment in comparison to the

total deposits available in the bank. The bank should maintain balance between

the liquid assets and its advances in order to ensure constant flow of withdrawals

to the customer.

In the above graph we can see that the ratio is increasing every year which is a

sign showing that the bank is maintaining a proper balance.

0

50

100

150

200

250

300

2010 20112012

20132014

Liquid assets to demand deposits(In %)

LIQUID ASSETS TO DEMANDDEPOSITS RATIO (IN %)

37

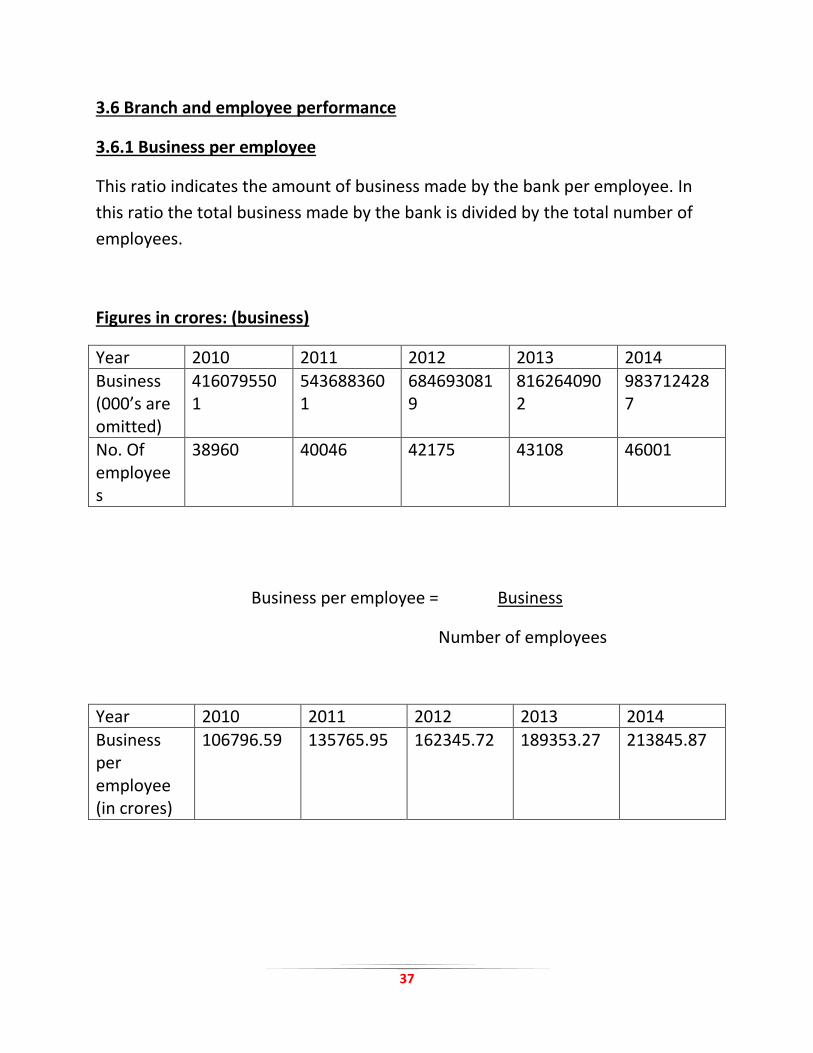

3.6 Branch and employee performance

3.6.1 Business per employee

This ratio indicates the amount of business made by the bank per employee. In

this ratio the total business made by the bank is divided by the total number of

employees.

Figures in crores: (business)

Year 2010 2011 2012 2013 2014

Business (000’s are omitted)

4160795501

5436883601

6846930819

8162640902

9837124287

No. Of employees

38960 40046 42175 43108 46001

Business per employee = Business

Number of employees

Year 2010 2011 2012 2013 2014

Business per employee (in crores)

106796.59 135765.95 162345.72 189353.27 213845.87

38

In the above table and graph, we see that the business per employee has been

steadily increasing. Thebusiness was the highest at Rs.213845.87crores per

employee in the year 2014. In 2010 the business was Rs.106796.59 crores per

employee, in year 2011 the business was Rs.135765.95 crores per employee , in

2012 the business was Rs.162345.72 crores per employee, in 2013 the business

was Rs.189353.27crores per employee, in 2014 the ratio is Rs.213845.87crores

per employee.

This ratio shows the efficiency levels of the employees to generate business to the

bank. More the ratio more is the efficiency level of the banks employees.

In the above graph we can see that business per employee is constantly

increasing.

0

50000

100000

150000

200000

250000

2010 20112012

20132014

BUSINESS PER EMPLOYEE

BUSINESS PER EMPLOYEE

39

3.6.2 Net profit per employee

This ratio indicates the amount of net profit made by the bank per employee. In

this ratio the total net profit made by the bank is divided by the total number of

employees.

Figures in crores: (business)

Year 2010 2011 2012 2013 2014

Net profit (000’s are omitted)

32498728 45159105 53872358 49829573 52819205

No. Of employees

38960 40046 42175 43108 46001

Net profit per employees = Net profit

Number of employees

Year 2010 2011 2012 2013 2014

Business per employees (in crores)

834.14 1127.68 1277.35 1155.92 1148.21

40

In the above table and graph, we see that the net profit per employee has been

fluctuating. The business was the highest at Rs. 1277.35 crores per employee in

the year 2012. In 2010 the business was Rs. 834.14crores per employee, in year

2011 the business was Rs. 1127.68crores per employee , in 2012 the business was

Rs. 1277.35 crores per employee, in 2013 the business was Rs. 1155.92 crores per

employee, in 2014 the ratio is Rs. 1148.21crores per employee.

This ratio shows the efficiency levels of the employees to generate business to the

bank. More the ratio more is the efficiency level of the banks employees.

In the above graph we can see that net profit per employee is growing at an

acceptable rate.

0

200

400

600

800

1000

1200

1400

2010 20112012

20132014

NET PROFIT PER EMPLOYEES

NET PROFIT PER EMPLOYEES

41

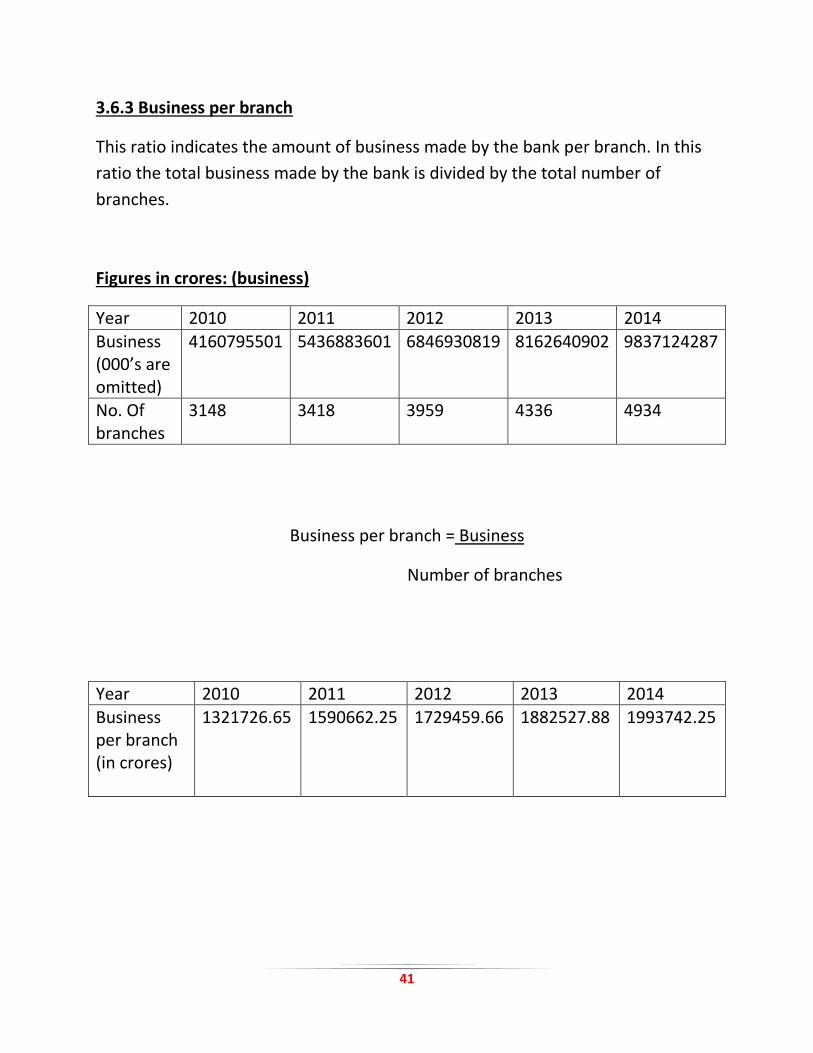

3.6.3 Business per branch

This ratio indicates the amount of business made by the bank per branch. In this

ratio the total business made by the bank is divided by the total number of

branches.

Figures in crores: (business)

Year 2010 2011 2012 2013 2014

Business (000’s are omitted)

4160795501 5436883601 6846930819 8162640902 9837124287

No. Of branches

3148 3418 3959 4336 4934

Business per branch = Business

Number of branches

Year 2010 2011 2012 2013 2014

Business per branch (in crores)

1321726.65 1590662.25 1729459.66 1882527.88 1993742.25

42

In the above table and graph, we see that the business per branch has been

steadily increasing. The business was the highest at Rs.1993742.25 crores per

branch in the year 2014. In 2010 the business was Rs.1321726.65 crores per

branch, in year 2011 the business was Rs.1590662.25 crores per branch, in 2012

the business was Rs.1729459.66 crores per branch, in 2013 the business was

Rs.1882527.88 crores per branch and in 2014 the ratio is Rs. 1993742.25 crores

per employee.

In the above graph we can see that business of the bank per branch has increased

every year, which is a good sign for the bank.

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

2000000

2010 20112012

20132014

BUSINESS PER BRANCH

BUSINESS PER BRANCH

43

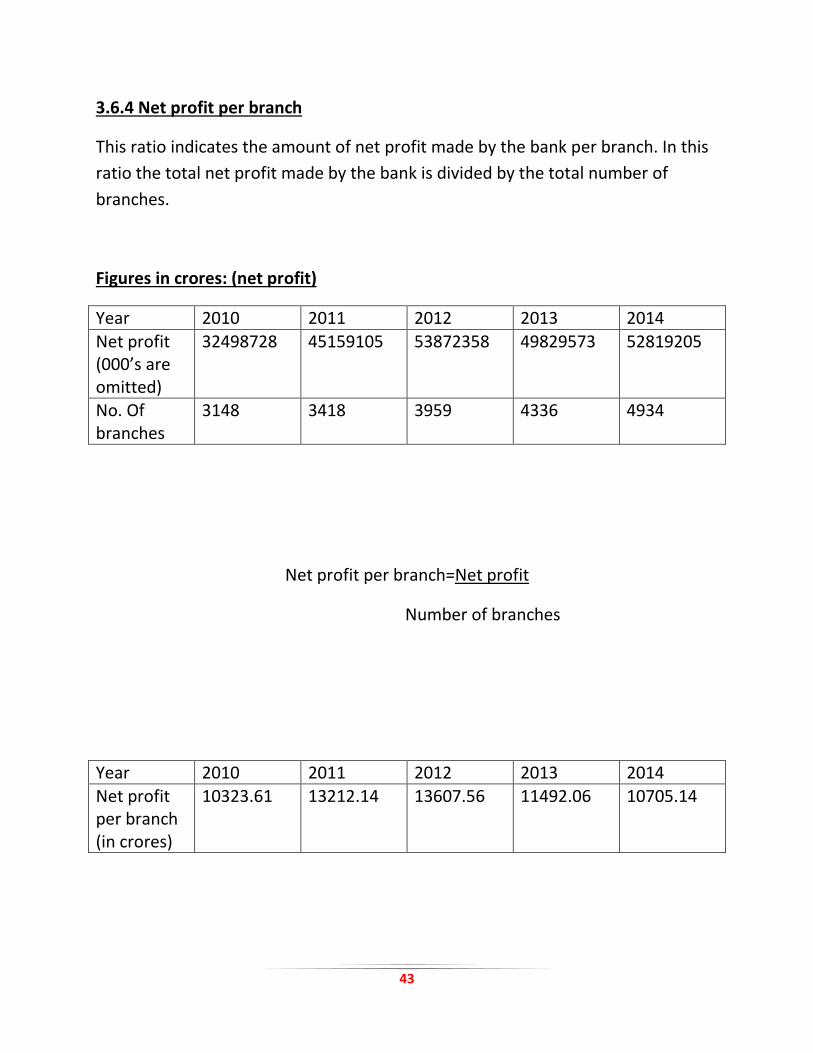

3.6.4 Net profit per branch

This ratio indicates the amount of net profit made by the bank per branch. In this

ratio the total net profit made by the bank is divided by the total number of

branches.

Figures in crores: (net profit)

Year 2010 2011 2012 2013 2014

Net profit (000’s are omitted)

32498728 45159105 53872358 49829573 52819205

No. Of branches

3148 3418 3959 4336 4934

Net profit per branch=Net profit

Number of branches

Year 2010 2011 2012 2013 2014

Net profit per branch (in crores)

10323.61 13212.14 13607.56 11492.06 10705.14

44

In the above table and graph, we see that the net profit per branch has been

fluctuating. The net profit was the highest at Rs.13607.56 crores per branch in the

year 2012. In 2010 the net profit was Rs.10323.61 crores per branch, in year 2011

the net profit was Rs.13212.14 crores per branch, in 2012 the net profit was

Rs.13607.56 crores per branch, in 2013 the net profit wasRs.11492.06 crores per

branch and in 2014 the ratio is Rs.10705.14 crores per branch.

Till 2012 net profit earned per branch has increased. However from 2013 onwards

it reduced. The reduction in net profit indicates inefficiency to manage their

branches.

0

2000

4000

6000

8000

10000

12000

14000

2010 20112012

20132014

Net profit per branch

NET PROFIT PER BRANCH

45

SUMMARY

Ratio 2010 2011 2012 2013 2014 Capital adequacy

Capital adequacy

12.84% 13.03% 12.95% 12.09% 11.66%

Debt to equity

0.85 0.78 1.08 0.97 1.67

Advances to total assets

62.51% 63.37% 63.85% 59.64% 59.71%

Govt. Securities to total investments

83.40% 85.13% 84.61% 84.98% 83.12%

Asset quality NPA to total advances

1.35% 1.35% 1.52% 2.39% 2.94%

Investments to total assets

22.21% 20.24% 18.95% 22.45% 18.06%

NPA to total assets

0.84% 0.86% 0.87% 1.42% 1.75%

MANAGERIAL EFFICIENCY Advances to total deposits

72.25% 74.48% 74.39% 69.12% 69.60%

Returns on equity

8.89% 11.49% 13.06% 11.79% 12.26%

Earning quality Operating profit to total assets

1.82% 2.07% 2.05% 1.81% 1.60%

Net profit to total assets

1.14% 1.23% 1.17% 0.89% 0.78%

Interest income to total income

85.32% 87.25% 88.14% 88.98% 87.92%

**Next page**

46

LIQUIDITY

Liquid assets to total assets

12.86% 14.04% 14.38% 15.67% 19.87%

Liquid assets to total deposits

14.86% 16.50% 16.76% 18.17% 23.16%

Liquid assets to demand deposits

188.83% 217.00% 222.99% 240.49% 263.58%

Branch and employee performance (in crores)

Business per employee

106796.59 135765.95 162345.72 189353.27 213845.87

Net profit per employee

834.14 1127.68 1277.35 1155.92 1148.21

Business per branch

1321726.65 15906620.25 1729459.66 1882527.88 1993742.25

Net profit per branch

10323.61 13212.44 13607.56 11492.06 10705.14

47

CONCLUSION

During the process of analysis done on Bank of Barodafor the 5 financial years

using camel model we conclude that:

Capital adequacy-

In our study, we found that BOB has grown into wider business unit each year.

The capital adequacy parameter is satisfactory in terms of percentage from the

year 2010 to 2014. The percentage is always above 9%.

Capital adequacy consists of capital adequacy ratio, debt-equity ratio, advance to

assets, government securities to total investment ratios. The capital adequacy

ratio of the bank stands at 11.66% for the year 2014, against RBI stipulated of9%

with tier i capital at8.22 % and tier ii capital at 5.16%. In the year 2014, BOB has

the highest debt-equity ratio compared to other years.The advance to asset ratio

is at a good level in 2014. BOBhas invested sufficient amount in government

securities in every year.

Asset Quality-

In terms of asset quality, the performance ofBOB in net NPA to net advances was

not very good in 2014 as compared to other years;NPA’s in 2014 were the highest

in 2014. Total investment to total assets ratio has decreased in 2014. The possible

reason was that, there was increase in total investments compared to other years

but proportionate increase was not there compared to previous year’s total

assets. NPA to total asset ratio increasing every year, in 2014 it was the highest at

1.75%.

48

Managerial efficiency-

Under management efficiency parameter it was observed that the efficiency has

acceptable from 2010 to 2014. Total advances to total deposits ratio has

decreased by 2.65%in 2014 when we compare it with 2010. Shareholders enjoyed

better return on equity in 2014as compared to other years.

Earning Quality-

In terms of earning quality parameter, BOB has had a stable period of 5 years

where its earning quality was quite similar. Interest income to total income was

has been increasing at a stable rate in the last 5 years, in the year 2014 the ratio is

87.92%.

Liquidity-

This is a parameter where BOB has done outstandingly well. All the three aspects

i.e. Liquid asset to total deposit, liquid asset to time deposits & liquid asset to

demand deposit have done well. All three ratios have shown a positive

movement.