bangladesh accounting standard (bas-1)

DESCRIPTION

Bangladesh Accounting Standard (BAS)BAS 1 Objectives This standard prescribes the basis for presentation of general purpose financial statements to ensure comparability both with the entity’s financial statements of previous periods and with the financial statements of other entities. It sets out overall requirements for the presentation of financial statements, guidelines for their structure and minimum requirements for their content.10. Complete set of financial statements A complete set ofTRANSCRIPT

Bangladesh Accounting Standard (BAS)Bangladesh Accounting Standard (BAS)Bangladesh Accounting Standard (BAS)Bangladesh Accounting Standard (BAS)

BAS 1

Objectives

This standard prescribes the basis for presentation of general purpose financial statements to

ensure comparability both with the entity’s financial statements of previous periods and with the

financial statements of other entities. It sets out overall requirements for the presentation of

financial statements, guidelines for their structure and minimum requirements for their content.

10. Complete set of financial statements

A complete set of financial statements comprises:

a) A statement of financial position as at the end of the period;

b) A statement of comprehensive income for the period;

c) A statement of changes in equity for the period;

d) A statement of cash flows for the period;

e) Notes, comprising a summary of significant accounting policies and

other explanatory information; and

f) A statement of financial position as at the beginning of the earliest

comparative period when an entity applies an accounting policy

retrospectively or makes a retrospective restatement of items in its

financial statements, or when it reclassifies items in its financial

statements.

� Both the companies (Beximco Pharmaceuticals Ltd. & Square Pharmaceuticals Ltd.)

have shown the complete set of financial statements including a statement of financial

position, a statement of comprehensive income, a statement of changes in equity, a

statement of cash flows and notes for the period according to the BAS 1(10). The

document is attached at the end of the report.

51. An entity shall clearly identify each financial statement and the notes. In

addition, an entity shall display the following information prominently, and repeat

it when necessary for the information presented to be understandable:

a) The name of the reporting entity or other means of identification, and

any change in that information from the end of the preceding

reporting period;

b) Whether the financial statements are of an individual entity or a

group of entities;

c) The date of the

the set of financ

�

The name of the reporting

Beximco Pharmaceuticals

It is also clear that both of

reporting period are covere

d) The presentatio

e) The level of rou

statements.

Foreign currencies are translated into

accordance with BAS-21 "The Effect

currency for retention quota account h

ruling on that date and gain/(loss) hav

Statement.

There is no rounding figure in the

he end of the reporting period or the period

ancial statements or notes;

rting entity or other means of identification are follow

ticals Limited and Square Pharmaceuticals Limited.

oth of them are individual entities. The dates of the en

covered by the set of financial statements or notes.

tion currency, as defined in BAS 21;

ounding used in presenting amounts in the

d into taka at the exchange rates ruling on the date of trans

Effects of Changes in Foreign Exchange Rates". Bank dep

count has been translated into taka at the year end at the ra

ss) have been accounted for as other income/(loss) in the I

in the statements. The amounts are shown in full figur

iod covered by

followed by

the end of the

he financial

f transactions in

nk deposit in foreign

the rate of exchange

n the Income

l figure.

54. Statement of financial po

Information to be presented

As a minimum, the statemen

present the following amoun

a) Property, plant and eq

b) Investment property;

c) Intangible assets;

d) Financial assets(exclu

e) Investments accounted

f) Biological assets;

g) Inventories;

h) Trade and other receiv

i) Cash and cash equivale

j) The total of assets clas

groups classified as he

Assets Held for Sale an

k) Trade and other payab

position

ed in the statement of financial position

ent of financial position shall include line it

unts:

equipment;

y;

luding amounts shown under (c), (h) & (i))

ted for using the equity method;

eivables;

alents;

lassified as held for sale and assets included

held for sale in accordance with BFRS 5 Non

and Discontinued Operations;

ables;

items that

i));

ed in disposal

on-current

l) Provisions;

m) Financial liabilities [excluding amounts shown under (k) and (l)];

n) Liabilities and assets for current tax, as defined in BAS 12 Income Taxes;

o) Deferred tax liabilities and deferred tax assets, as defined in BAS 12;

p) Liabilities included in disposal groups classified as held for sale in accordance

with BFRS 5;

q) Non-controlling interests, presented within equity; and

r) Issued capital and reserves attributable to owners of the parent.

=> Both companies followed the BAS-1 (54) in completing financial position statement. But

some of the elements are absent.

83. An entity shall disclose the following items in the statement of comprehensive

income as allocations of profit or loss for the period:

a) Profit or loss for the period attributable to:

i. Non-controlling interests, and

ii. Owners of the parent.

b) Total comprehensive income for the period attributable to:

i. Non-controlling interests, and

ii. Owners of the parent.

=> Both of companies followed BAS- 1 (83) requirements.

84. An entity may present in a separate income statement (see paragraph 81) the

line items in paragraph 82 (a)-(f) and the disclosures in paragraph 83(a).

=> Both companies have followed the format of comprehensive income statement according to

the BAS-1(81, 82, and 83).

97. When items of income or expense are material, an entity shall disclose their

nature and amount separately.

=> Items of income or expense are shown separately both in the statements and notes.

98. Circumstances that would give rise to the separate disclosure of items of income

and expense include:

a. Write downs of inventories to net realizable value or of property,

plant and equipment to recoverable amount, as well as reversals of

such write-downs;

b. Restructuring o

provisions for t

c. Disposals of item

d. Disposals of inv

e. Discontinued op

f. Litigation settle

g. Other reversals

=> Both of the companies have fol

g of the activities of an entity and reversals

r the costs of restructuring;

tems of property, plant and equipment;

nvestments;

operations;

tlements and

als provisions.

ave followed BAS-1(98) for above elements.

als of any

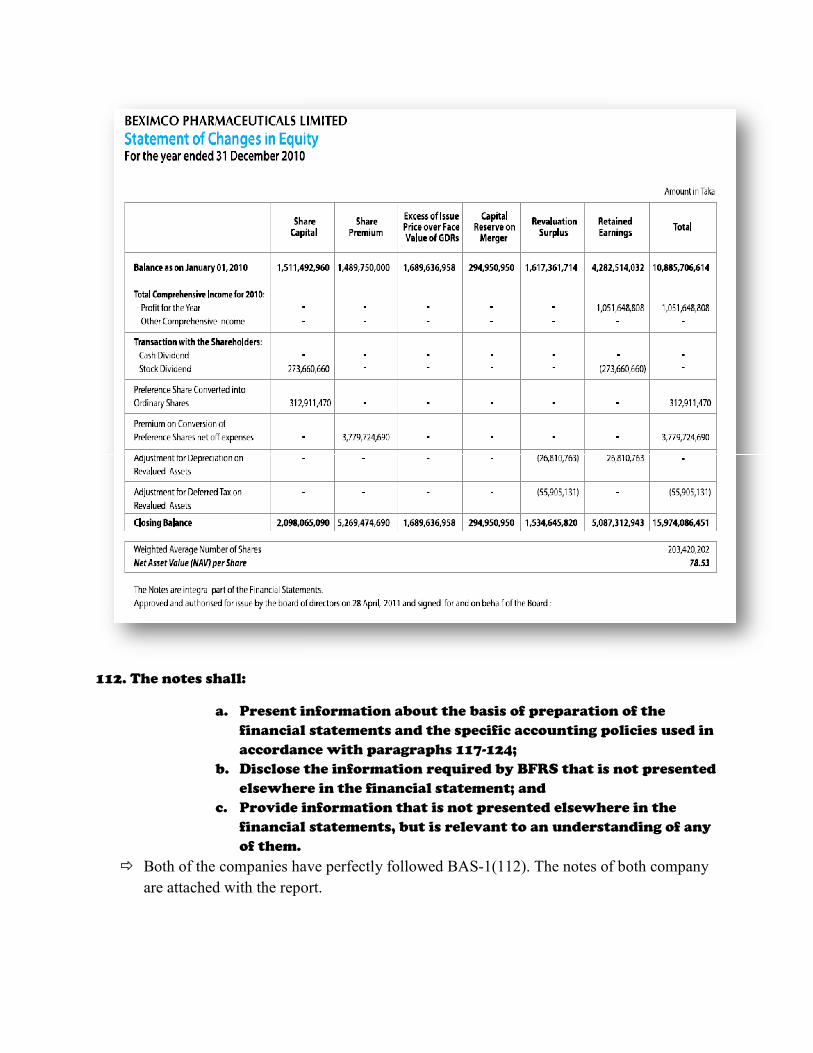

106. An entity shall present a

statement:

a. Total comprehe

total amounts a

controlling inte

b. For each compo

or retrospective

and

c. For each compo

amount at the b

disclosing chang

i. Profit or

ii. Each item

iii. Transacti

separatel

changes i

in a loss o

� Both of the companies have f

t a statement of change in equity showing i

hensive income for the period, showing sep

s attributable to owners of the parent and t

terests;

ponent of equity, the effect of retrospective

ive restatement recognized in accordance w

ponent of equity, a reconciliation between t

e beginning and the end of the period, separ

anges resulting from;

or loss;

em of other comprehensive income; and

ction with owners in their capacity as owne

tely contributions by and distributions to ow

s in ownership interests in subsidiaries tha

s of control.

have followed the above rules of BAS-1(106). See the figu

g in the

eparately the

d to non-

ive application

with BAS 8;

n the carrying

arately

ners, showing

owners and

hat do not result

he figures,

112. The notes shall:

a. Present in

financial

accordan

b. Disclose t

elsewher

c. Provide in

financial

of them.

� Both of the companies hav

are attached with the repor

t information about the basis of preparation

ial statements and the specific accounting po

ance with paragraphs 117-124;

e the information required by BFRS that is

ere in the financial statement; and

e information that is not presented elsewhe

ial statements, but is relevant to an understa

es have perfectly followed BAS-1(112). The notes of

report.

ion of the

policies used in

is not presented

here in the

standing of any

tes of both company

117. An entity shall disclose in the summary of significant accounting policies:

a. The measurement basis (or bases) used in preparing the financial

statement, and

b. The other accounting policies used that are relevant to an

understanding of the financial statements.

� Both of them followed the related accounting policies.