bain & company western union remittance strategy … morningstar, business essentials 6 western...

TRANSCRIPT

Bain & Company Western Union Remittance Strategy Fall 2016

Bain & Company SIBC Analysts

Daniel Murphy Junior

Mech Engineering & ACMS

Riverside, IL

Jose Fernandez Trevino

Sophomore Pol. Science &

Economics Monterrey, Mex

Roberto Elosua Gomez

Sophomore Finance & Stats Monterrey, Mex

Blair Yiyang Hu Sophomore

Pol. Science & Economics

Shanghai, China

Regina Zavala Rangel

Freshman Economics

Monterrey, Mex

Yiling Zhou Sophomore Finance & Economics

Shanghai, China

Miles Wood Freshman

Business & ACMS Kansas City, MO

Connor Murphy Sophomore

Pol. Science & Economics

Portland, OR

2

Meredith Henry Sophomore

Liberal Studies & Film/Television

Harrison, NY

Bernadette Grant Sophomore Undecided Business

Chappaqua, NY

Executive Summary

Client Western Union is global financial services company specializing in payments. 80% of its revenue comes from remittances, or C2C international payments.

Situation

Western Union’s relatively large remittance market share is declining, though the overall industry is growing. Western Union is mainly struggling with problems of reach and costs.

Solution

Western Union should integrate brick-and-mortar partnerships with a new digital platform to target underbanked populations in developing countries and reduce transaction costs.

3

Western Union should integrate new physical partnerships with a reengineered digital platform

Oasis

Objectives

Oxxo / Safaricom Locations Leverage WU Connect Stellar Mobile Platform

Impact

Greater Reach Greater Profitability Lower Transaction Costs

4

Physical Partnerships Digital Platform

$ WU Partner with companies with large reach as withdrawal points

Leverage WU Connect’s reliability and interface to streamline development

Partner with Stellar to create blockchain–based mobile payments platform

Expand Market Share by targeting mobile users in developing countries

Revenue Stellar’s blockchain technology can reduce transaction costs by 25% Costs

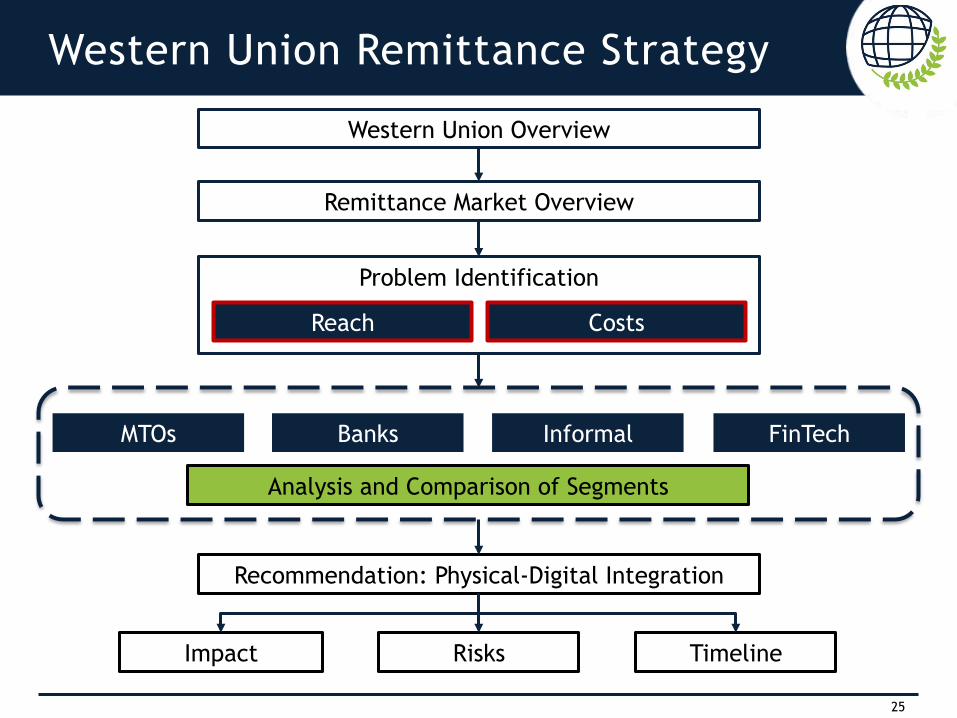

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

5

Remittance Market Overview

Informal

Reach Costs

6 Sources: Morningstar, Business Essentials

Western Union’s remittance-dependent business model is under pressure

Background

• Founded in 1851 • Provides money movement and

payment services world-wide

Business Segments

Consumer to Consumer

• Allows people to quickly send or receive money anywhere around the world

• 80% of revenue and 90% of profits

Consumer to Business

• Singular or recurring payments to businesses

• International B2B cross-border, cross-currency payment services

Business Solutions

• Facilitates payments for small and medium enterprises across borders and currencies

Gross Profit Margin Decline Revenue Stagnation and Decline

500,000 agent

locations worldwide

100,000 ATM Locations

0

2

4

6

8

10

12

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Reve

nue

(in

billi

ons

of d

olla

rs)

Year

37 38 39 40 41 42 43 44 45 46 47

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Gro

ss P

rofi

t M

argi

n (%

)

Year

CAGR: -1.3%

7 Source: Save

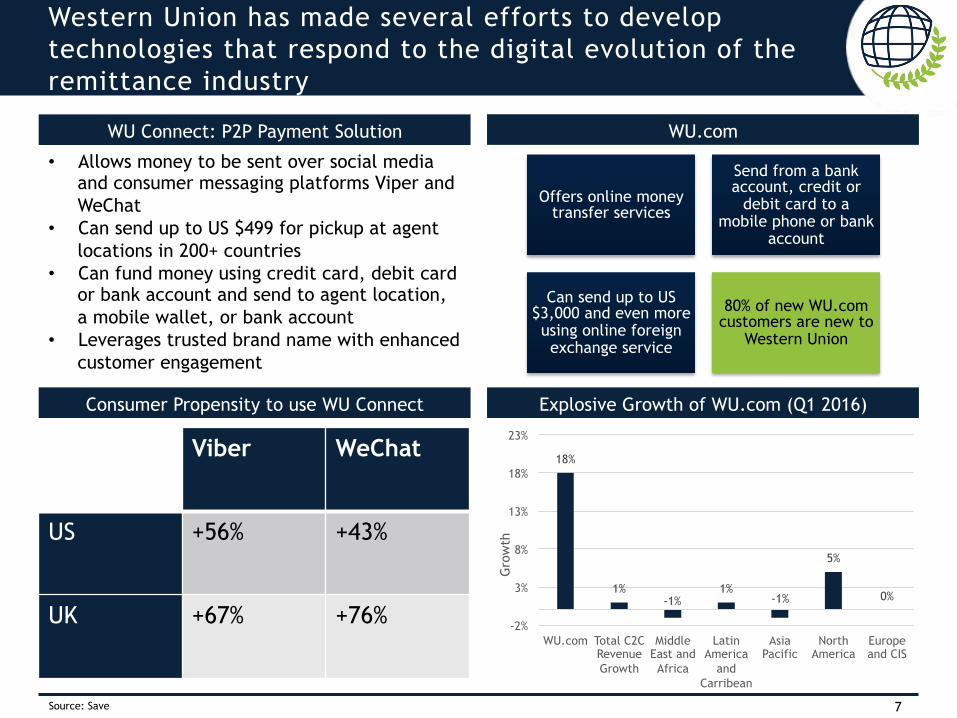

Western Union has made several efforts to develop technologies that respond to the digital evolution of the remittance industry

WU Connect: P2P Payment Solution WU.com

Consumer Propensity to use WU Connect Explosive Growth of WU.com (Q1 2016)

• Allows money to be sent over social media and consumer messaging platforms Viper and WeChat

• Can send up to US $499 for pickup at agent locations in 200+ countries

• Can fund money using credit card, debit card or bank account and send to agent location, a mobile wallet, or bank account

• Leverages trusted brand name with enhanced customer engagement

Offers online money transfer services

Send from a bank account, credit or

debit card to a mobile phone or bank

account

Can send up to US$3,000 and even more using online foreign exchange service

80% of new WU.com customers are new to

Western Union

Viber WeChat

US +56% +43%

UK +67% +76%

18%

1% -1%

1% -1%

5%

0%

-2%

3%

8%

13%

18%

23%

WU.com Total C2C Revenue Growth

Middle East and Africa

Latin America

and Carribean

Asia Pacific

North America

Europe and CIS

Gro

wth

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

8

Remittance Market Overview

Informal

Reach Costs

9 2016 10K, SaveOnSend, Infosys, Pew Research Center

The worldwide remittance market is experiencing growth driven by developing nations

Basic Overview

Geographical Overview

Segments Market Share

$586B Industry in 2015

$436B to developing countries

Remittances have steadily climbed

since 1970

Expected $636B Industry by 2017

Top Remittance Senders

United States ($133B)

Saudi Arabia ($46B)

United Arab Emirates ($30B)

Germany ($23B)

Russia ($16B)

Top Remittance Recipients

India ($69B)

China ($64B)

Philippines ($28B)

Mexico ($25B)

Nigeria ($21B)

41%

16%

21%

22% MTOs

Banks

Digital

Hawala/Informal

Takeaways

• 3.5% growth projected from 2015 to 2017 Growth

• 74% of remittances sent to developing world

• Majority of growth comes from developing markets

Developing World

10 Infosys, World Bank

Digitization has disrupted the remittance industry, creating downward pressure on fees and necessitating responses from established players

Technological Shift

Consolidation in the Industry

Decreasing Remittance Fees in All Segments

Exploration of Alternate Platforms

Social Media

Platform

Money Transfer Service

Increased Accesibility

90% of money transfer between friends and family

Facebook and WeChat have

extensive international

consumer base

Traditional agent-based business models are diversifying into new revenue streams

Innovative money transfer players looking to become generic money management players

Example: PayPal acquired Xoom for US$890m in 2015

Digital services account for 53% of the industry

Proliferation of smartphones among remittance senders and receivers

Average digital money transfer fee of 5.32% in 2015

2011 • 9.30%

2012 • 9.00%

2013 • 8.93%

2014 • 7.96%

2015 • 7.37%

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

11

Remittance Market Overview

Informal

Reach Costs

Infoysys, World Bank, McKinsey & Company, GSMA, Pew Research Center, SaveOnSend 12

10%

11%

12%

13%

14%

15%

16%

Costs

Mobile money based remittances are fastest growing remittances product by transactions

volumes with a rate of +52%

Reach

Western Union Global Market Share

Decreasing Remittance Fees

Downward Margin Pressure

Key Trend: Digitization

Despite growth in the remittance industry, Western Union’s market share is decreasing due to fee pressure and digitization, creating a problem of reach and costs

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

13

Remittance Market Overview

Informal

Reach Costs

14 World Bank, S&P Capital IQ, MoneyGram, Ria Financial Services

MTOs, although they comprise the largest segment, are facing decreasing market share and margins

Major Players

Services Overview Methods of Money Transfer

Quantitative Analysis

Money Transfer

Currency Exchange

Bill Payment

Prepaid Debit Cards

Check Cashing

Money Orders

Send money online

Send money in person

Send money directly to bank accounts

Send money to a mobile wallet

Send money to an inmate

Market Share 41%

Margins 25%

Average Transaction

Size $200 9.3%

Fee

13%

4%

5%

15 S&P Capital IQ, Ria Financial Services, Interview with Tim Fanning (Former COO of Ria Financial Services)

Company Overview

Interview with Former COO Ria and 7-Eleven Partnership

Fee Structure

Average Intl. Transfer: $300

Estimated Average Intl. Fee: ~7-8%

Founded: 1987 Headquarters: London, England Company Description: Operates the Money Transfer segment of Euronet Worldwide, Inc. As the third largest money transfer company in the world, Ria has a global agent network of over 316,000 locations in 150 countries worldwide. In addition to money transfer services, the company offers bill payment, mobile top ups, prepaid debit cards, check cashing, and money orders.

WU experiencing price pressure from third parties

People want to go to a branch, hand money to a person, and let the recipient collect it in person

Cash isn’t exiting the market because of its ease of use and anonymity

Money Transfer services available in 7-Eleven

Card-based, telephone originated remittance

Failed due to lack of personal interaction

Fee

Send/Pick-up Methods

Destination

Send Location

Money Amount

Ria’s comparable business model reveals the risk of specific expansion strategies

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

16

Remittance Market Overview

Informal

Reach Costs

17

Segment Overview

Receive 70% of volume globally.

Top 4 US banks are responsible for half of all banks remittance volume.

Banks retreating from money transfer industry due to high regulations.

61 52

69

57 48

40

59

40 32 33

51

11

0 10 20 30 40 50 60 70 80

All Unbanked Underbanked Banked

%

I trust traditional banks more than I do online banks

Using a peer-to-peer lender is riskier than getting a loan from a traditional bank or credit union I would consider using banking services from a nonbank (i.e. Walmart)

Trust in Traditional Banks

Segment Response to Technology

More people trust traditional banks over online platforms.

The underbanked sector would rather get a loan from a traditional bank.

Trust in traditional banks rises with household income, but so does demand for other alternatives.

Increasing e-commerce and electronic payment

technology will bring revenue growth

Majority of revenue comes from data processing and

transaction fees from credit/debit purchases.

Ratio of electronic payments to cash payments

has increased.

Transaction volumes for processors in industry have

gone up.

People tend to trust traditional banks over other money-transferring alternatives

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

18

Remittance Market Overview

Informal

Reach Costs

Business Structure

19

Worker in Country 1

Family in Country 2

Broker in Country 1

Broker in Country 2

$ $

Call / Fax / Email

Definition: An alternative, informal remittance system that works by transferring money without actually moving it. It usually involves a hawaladar (broker) delivering money from his cash reserve or account at the request of a counterpart hawaladar in another country who is serving a client

Remittance Code

Remittance Code

Balancing Methods: Hawaladars usually well-

connected business owners

Illegal: Smuggling of currency, commodities or invoice

manipulation

Legal: Money transfers using

conventional bank routes, postal money orders and

goods swaps

Chief Organizer, UN, IMF, Global Development Research Center, William and Mary, WAIFEM, Regalii

Informal money transfers through legal and illegal channels rely on the personal networks of brokers

120 Days

7 Days

65% 53%

20

Pros • System is self-regulating, it is rare for hawaladars to defraud one another or their clients

• Very small operating costs and ensures anonymity for clients

• Cash based without any need of formal banking (ideal for unbanked clients)

Cons • Moderate barriers to entry (must know a trusted hawaladar to participate)

• Due to its obscure and informal nature, extremely hard to regulate (illegal in some countries)

• Money laundering and other criminal activities rampant in system

Market Share ~22%

Margins 2%

Average Transaction

Size $200 .25% to

1.25% Fee

Quantitative Analysis

• The UN estimated that $100-$300 billion moved through informal money transfer systems

• Margins are expected to stay at around 2% for the foreseeable future

• Very little overhead compared to other formal transfer channels

• Enables hawaladars to charge much lower rates than alternative official channels

Evaluation of Hawala System

Chief Organizer, UN, IMF, Global Development Research Center, William and Mary, WAIFEM, Regalii

The Hawala system is low-cost but presents serious regulatory issues

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

21

Remittance Market Overview

Informal

Reach Costs

22

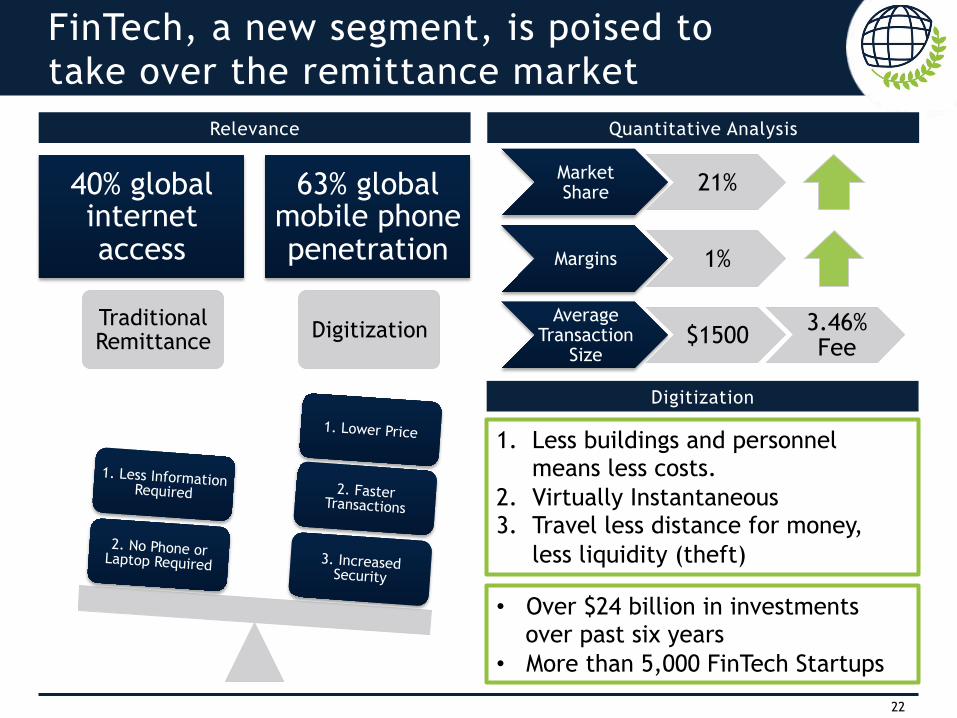

FinTech, a new segment, is poised to take over the remittance market

Traditional Remittance Digitization

3. Increased Security

2. Faster Transactions

1. Lower Price

2. No Phone or Laptop Required

1. Less Information Required

1. Less buildings and personnel means less costs.

2. Virtually Instantaneous 3. Travel less distance for money,

less liquidity (theft)

• Over $24 billion in investments over past six years

• More than 5,000 FinTech Startups

Quantitative Analysis

Market Share 21%

Margins 1%

Average Transaction

Size $1500 3.46%

Fee

Relevance

40% global internet access

63% global mobile phone penetration

Digitization

23 Source: Forbes, The Economist

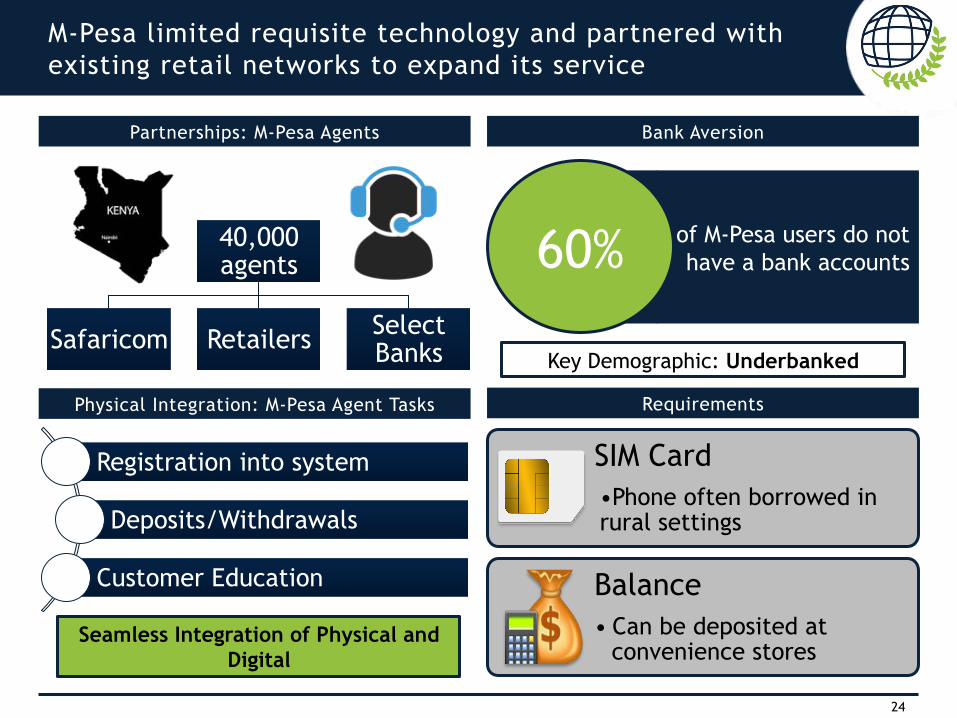

M-Pesa offers a blueprint on how to successfully integrate digital and physical payment systems

Diverse Partnership in Creation • M-Pesa was created by a joint venture between UK’s

department for International Development and Safaricom (Vodafone).

Volume of Transactions • Over 43% of the value of GDP in Kenya in 2013 flowed

through M-Pesa • 237 million person to person transactions in that year.

Inclusiveness • Extended financial inclusion for 20 million Kenyans. • By 2011 more than 72% of the people in Kenya living

under $1.25 a day used M-Pesa

Expansion • M-Pesa later evolved from only a payment facilitator to

a provider of loans and savings products. • M-Pesa can also be used to pay salaries and bills.

Critical Success Factors

Effects

Household income increased by 5-30% due to M-Pesa’s efforts

Decrease in time spent going to bank, standing in line, etc.

• Experienced troubles in expansion

Trouble replicating

• Weak law enforcement in target areas

Corruption and Money

Laundering

• 255 services in 89 countries Severe

International Competition

Challenges

24

SIM Card • Phone often borrowed in rural settings

Balance • Can be deposited at

convenience stores

of M-Pesa users do not have a bank accounts

40,000 agents

Safaricom Retailers Select Banks

Bank Aversion

Requirements

Partnerships: M-Pesa Agents

Physical Integration: M-Pesa Agent Tasks

60%

Key Demographic: Underbanked

Registration into system

Deposits/Withdrawals

Customer Education

Seamless Integration of Physical and Digital

M-Pesa limited requisite technology and partnered with existing retail networks to expand its service

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

25

Remittance Market Overview

Informal

Reach Costs

WesternUnion.com, TransferWise.com, Infosys, World Bank, Reuters, SaveOnSend

26

Consequences of Fee Pressure

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

$50 $100 $150 $200

MTO

Mobile w/ Cash

Mobile w/out Cash

Average Remittance Costs

Industry Responses

Reach Costs

FinTech companies are creating downward fee pressure, straining traditional players with respect to reach and costs

• Share of FinTech segment devoted to payments

35%

• P2P payments growth $174

billion

The FinTech segment offers the most upside potential in the future of the remittance market

Segment Mkt. Share

Share Trends Margins Margin

Trends Avg. Fee Barriers To Entry Regulation Overall

MTOs 41 % Negative 25 % Negative 9.63 % N / A Medium

Banks 16 % Neutral 12 % Negative 11.18 % High High

Informal 22 % Neutral 2 % Neutral 1.00 % High Medium

FinTech 21 % Positive 1 % Positive 3.46 % Low Low

Summary of Analysis of Remittance Market Segmentations

Factors Supporting an Entry Into The FinTech Segment

Mkt. Share Trends

• Only FinTech segment has positive growth

Customer Type

• Underbanked • Represents 75% of overall market

Success of Startups

• M-Pesa handles 43% of the value of Kenya's GDP

Efficient Solution

• Best area for solution given constraints: time, budget, feasibility

27

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

28

Remittance Market Overview

Informal

Reach Costs

Western Union can alleviate its reach and costs problems by adapting the M-Pesa model

Days

65%

29

Solution: Expand M–Pesa Model

Reach: Falling Market Share Costs: Falling Remittance Fees

Problem: FinTech Player Entering Remittance Market

Partnerships Physical-Digital Integration

Physical: Convenience Stores Digital: Stellar Partnership Flexibility in Partnerships by

Use - Case / Country

• Physical locations serve: • to reach customers • as withdraw points

• REACHES more customers

• Stellar partnership serves: • to reduce costs • to digitize use

• Reduces COSTS

• Flexibility in integration • target large physical

partners by country • utilize local

infrastructure

Impact Risks Implementation

Reduced costs and greater market share will produce $204- $957 MM in profits

With Stellar, Oxxo, and WU Connect, this strategy can be implemented by late 2017

2017 $ Security, regulatory, and brand confidence risks have been addressed

30 Stellar, Western Union

Western Union and other remittance companies have pursued comparable partnerships

Stellar Overview WU - Oxxo Partnership

• Nonprofit that connects people to low-cost financial services

The Organization

• Made up of servers that contain a shared database of all accounts on the network The Network

• Entities that connect to the stellar network and lets incompatible organizations interact efficiently

Gateways

• Developed at the local level Users and Services

Partnership with Deloitte and Tempo

Deloitte Partnership

Reduce cost of transfers by up

to 40%

Transactions completed in 5

seconds

Tempo Partnership

600,000 transactions for

$.01

Increase transparency and reduce

remittance fees

• Partnership with Mexico’s largest convenience store chain with 14,000 locations

• Flexibility: three modes of payout • Doubles retail network in Mexico

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

31

Remittance Market Overview

Informal

Reach Costs

Western Union can cut variable costs to lower its remittance fees and win market share

32

Demand Curve Logistic Concave Convex

Shape S(P)

Pros Diminishing returns to raising and lowering fees

Diminishing returns as fees approach 0

Traditional approach, data-driven elasticity

Cons Assumes higher market share at high fees

Diminishing decreases not present as fee grows

Monolithic elasticity unrealistic

In order to calculate the effect of lowering remittance fees on the overall market share, we need to assume a demand curve that accurately portrays the remittance market.

Profit Revenue

Market Size Market Share

S(P) Price per

Remittance

Costs

Fixed Costs Variable Cost

C(P)

Profitability Optimization Model

0%

10%

20%

30%

40%

50%

60%

70%

Mar

ket

Shar

e S(

P)

Fee

Market Share vs. Fee

WU 10K

Successful implementation of the solution greatly increases both market share and profit

33

Logistic Demand Model

($2.0)

($1.5)

($1.0)

($0.5)

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

Prof

it (

in b

illio

ns)

Fee

Profit vs. Fee

Scenario Base Case Worst Case Best Case

Description Current WU Situation

Failure to increase market share

Grow share and maximize profit

Fee 9.3% 8.1% 8.1%

Market Share 13% 13% 19.9%

Profit (Net Profit) $1.04bn ($0) $1.31bn (+$265 MM) $2.0bn (+$957 MM)

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

34

Remittance Market Overview

Informal

Reach Costs

35 Source: Western Union 10K�

In a competitive, dynamic environment, successful implementation is challenged by a number of risks

• Price reductions reduce margins and adversely affect financial results in both short term and long term if transaction volumes do not increase sufficiently.

Reduction in Margins

• Poor performance of third-party businesses may impair their ability to provide services to Western Union and have a potential impact on Western Union’s own business. �

Third-Party Business Performances�

• Insufficient professional qualifications, knowledge or skills in money transfer services of third-party agents may damage the reputation of Western Union and confidence in brand�

Customer Confidence in Brand�

• Third-party locations that have low security protection such as 7-Eleven and Starbucks may be more vulnerable to thefts, robberies and other criminal activities

Physical Security of Third-Party Locations

• Additional regulations such as customer identification, agent due diligence requirements, enhanced recordkeeping or transaction monitoring may be difficult to comply with

New and Increasing Regulations

• Stellar’s virtual system and its own digital currency lumens are at risk from hackers, malware and operational glitches that could result in huge losses

Stellar’s Cybersecurity

Problem Identification

Western Union Overview

Banks MTOs

Western Union Remittance Strategy

FinTech

Analysis and Comparison of Segments

Recommendation: Physical-Digital Integration

Risks Impact Timeline

36

Remittance Market Overview

Informal

Reach Costs

By leveraging Western Union’s current resources, this strategy can be implemented by the end of 2017

37

Q1 2017 Reach Out and

Confirm Physical

Partnerships

Secure Partnership with Stellar

Review Regulatory Compliance

Q2 2017 Trial at

Selected Stores

Integrate WU/Stellar

Engineers

Beta Test Platform

Q4 2017 Marketing to

Target Countries

Offer Discounts to New / Loyal Customers

Record Data on Platform

Performance

2018 Beyond

Profit Optimization

Expand Into Rural Markets

Expand from C2C to B2B

Implementation Timeline

Long-Term Planning

Phase 1

Phase 2

Phase 3

Phase 4

Product Development

Official Launch of

New Strategy

Joint Venture Proposals

Successful Implementation Grow market share, reduce costs, and mitigate FinTech threat

38

Identified Problems In Western Union Remittance and Segment Analysis

Western Union Remittance Strategy: Objectives, Implementation, and Addressed Risks

Summary

! Western Union’s remittance business struggles in reach and cost ! The most attractive strategy involves entering the FinTech segment of the market

" The FinTech segment is the fastest growing segment, and has the lowest costs " Many consumers in developing countries only use digital platforms

! Western Union should integrate physical and digital partnerships " Partnership will stellar builds a digital platform, reducing costs by 25% " Partnerships with Oxxo and Safaricom give physical locations to withdraw cash

! Implementation of strategy is achievable by the end of 2017 ! Potential security, regulatory, and implementation risks have been addressed

“Western Union is the largest player in the international remittance business, but is

losing its market to FinTech players. To combat downward pressure on fees, Western

Union should integrate digital and physical partnerships to reach greater markets in

developing countries and decrease costs associated with sending money.”

Conclusion

APPENDIX

39

Appendix 1: Details and Assumptions for Recommendation Impact Calculations

40

WU 10K Data

Solution Calculations

Transaction Fees $3,221,000,000 For Ex $1,057,100,000 Other Revenues $65,800,000 Total Revenue $4,343,900,000

Operating Expenses $3,301,364,000.00 Operating Income $1,042,000,000 Operating Margin 24%Remittance Market $553,701,000,000 WU Market Share 13%WU Fee 9.30%

WU Remittance Volume Remittance Market * Market Share = $71,981,130,000 Realized Remittance Rate Revenue / WU Remittance Volume = 6.03%Realized to Fee Scaler Remittance Fee / Realized Remittance Fee = 1.5411 Total Remittance Fees WU Remittance Volume * Remittance Fee = $6,694,245,090 Realized Remittance Fees WU Remittance Volume * Realized Remittance Fee = $4,343,900,000

Realized Operating Income Operating Margin * Realized Remittance Fee = $1,042,536,000 Cost of Sending $1 Operating Expenses / Remittance Volume = $0.045864 Marginal Revenue/$1 Sent Realized Remittance Fee = $0.060348 Income/Dollar Sent Cost of Sending $1 – Marginal Revenue/$1 Sent = $0.014483 Income Income/Dollar Spent * WU Remittance Volume = $1,042,536,000

Cost Reduction Calculations

Calculated Data (WU Specific)

Costs Reduction (Assumed) 25%New Cost of Sending $1 (1-Cost Reduction) * Cost of Sending $1 = $0.034398 Desired Income per Dollar Spent Income/Dollar Sent = $0.014483

Target Marginal Revenue Cost of Sending $1 + Desired Income/Dollar = $0.048882 New Realized Remittance Rate Target Marginal Revenue = 4.89%New Remittance Fee Scalar * New Realized Remittance Rate = 7.53%

Fee Realized Fee S(P) Revenues Costs Profit Last Fee + (WU

Realized Remittance Fee – Min Fee) / 15 =

Fee * Realized to Fee Scalar =

1 / (1 + Exp(100 * (Fee – (Realized Remittance Fee * 100 – 1.734) / 100))) =

Remittance Market * S(P) * Fee =

Remittance Market * S(P) * Other Revenues = Revenues – Costs =

0.052538 0.08096494949 0.1990282167 $5,789,822,092.17 $3,790,757,247.98 $1,999,064,844.19