back to contents 1 - satmagazine · satmagazine.com back to contents 3 september 2005 satnews...

TRANSCRIPT

2Back to Contents

September 2005 SATMAGAZINE.COM

Vol. 2 No. 7, September 2005

TABLE OF CONTENTSClick on the title to go

directly to the story

COVER STORYCOVER STORYCOVER STORYCOVER STORYCOVER STORY FEAFEAFEAFEAFEATURESTURETURETURETURE

“European broadcasting hasnever been in better shape.”Or “It’s a real challengemaking any money.” Thesetwo comments from seniorsuits at major Europeanbroadcasting companies sumup the current state of play.

.

REGULAR DEPREGULAR DEPREGULAR DEPREGULAR DEPREGULAR DEPARTMENTARTMENTARTMENTARTMENTARTMENTSSSSS

By Chris Forrester By Dan Freyer

Recent tests of its newlylaunched XTAR satellitefar exceeded performanceobjectives and validatedthe confidence of its twopartners in this excitingnew satellite business.

Despite growing competitionfrom terrestrial wireless andfiber optic systems, the newIP environment provides manyopportunities for growth ofVSAT networks.

18 / Glass Half Full, or Glass Half Empty?

23 / US Programmers:Still FranchisingVia Satellite inEurope

32 / A Unique SatelliteSystem Aces ItsDemonstrationTests

35/ Data Communi-cations throughSatellites–Opportunitiesfor VSATs

CCCCCASE STUDASE STUDASE STUDASE STUDASE STUDYYYYY

With over 211 million TVhomes with a hugeappetite for USprogramming Europe is ahuge market for USbroadcasters.

by Cor Westerhoff

by Bruce Elbert

3 / Notes from the Editor4 / Calendar of Events5 / Featured Event:

SATCON 20056 / Industry News

SatMagazine Managing EditorVirgil Labrador spoke withGlobeCast CEO Christian Pinon onthe European market and otherissues.

40/ Inteview with GlobeCast CEO

Christian Pinon

10 / Executive Moves14 / New Products and Services43 / Market Intelligence46 / Advertisers’ Index/

Stock Quotes

EXECUTIVE SPOTLIGHTEXECUTIVE SPOTLIGHTEXECUTIVE SPOTLIGHTEXECUTIVE SPOTLIGHTEXECUTIVE SPOTLIGHT

29 / Integrated DigitalTV and theDigital Home

by Laurent Jabiol

Integrated Digital TV(iDTV) technologies aremaking the concept of atruly digital home areality.

VIEWPOINTVIEWPOINTVIEWPOINTVIEWPOINTVIEWPOINT

FEAFEAFEA E

SATMAGAZINE.COM

3Back to Contents

September 2005

Satnews Publishers is the leadingprovider of information on theworldwide satellite industry. Foremore information, go towww.satnews.com

Cover Design by: Simon Payne

Published monthly bySatnews Publishers800 Siesta Way,Sonoma, CA 95476 USAPhone (707) 939-9306Fax (707) 939-9235E-mail: [email protected]: www.satmagazine.com

Baden WoodfordContributing Writer, Africa

Jill Durfee([email protected])Advertising Sales

Joyce Schneider([email protected])Advertising Sales

Copyright © 2005Satnews PublishersAll rights reserved.

EDITORIALSilvano PaynePublisher

Virgil LabradorManaging Editorand Editor, North America

Chris ForresterEditor, Europe, Middle Eastand Africa

Bernardo SchneidermanEditor, Latin America

Peter GalaceEditor, Asia-Pacific

John Puetz, Bruce ElbertDan Freyer, Howard GreenfieldContributing Writers,The Americas

David Hartshorn, Martin JarroldContributing Writers, Europe

NOTE FROM THE EDITOR

Industry Consolidation Continues

As we went to press, the second largest satellite operator, Intelsat, announced that it its purchasingthe third largest satellite operator, PanAmSat for $3.2Billion. The deal, if approved by regulators would createthe largest satellite company in the world, surpassing thecurrent largest operator, SES Global both in terms ofrevenue and number of satellites. The new mergedcompany which will retain the Intelsat name, will have a

fleet of 53 operating satellites worldwide and projected annual revenues of$1.9 Billion.

Just a few weeks before the announcement, PanAmSat purchased anotheroperator, Europe*Star and announced a joint-venture with Japaneseoperator JSAT for a Ku-band satellite. The Wall Street Journal alsoreported a week before the announcement that Intelsat was in talks of apossible merger with Netherlands-based operator, News Skies Satellites.The merged company will have a lot of complementary synergies withIntelsat’s traditional strength in the telecommunications market andPanAmSat in the video market. During the press conference announcingthe merger, Intelsat acknowledged that it has had continuing talks withother operators, but did not specify which ones.

Surely more consolidation is in the offing. Transponder utilization rates arestill well below capacity (it’s 63% for Intelsat and 74% for PanAmSat) andthere’s increased competition from fiber and other carriers. The deal wasfacilitated by investment firms Deutsche Bank, Credit Swiss First Bostonand Lehman Bros. Both Intelsat and PanAmSat wer purchased previouslyby a consortium of private investment firms as with other leading satellitecompanies. The merger is expected to close in 6-12 months, pendingshareholder and regulatory approvals. Both Intelsat and PanAmSat areemphasizing that the two companies are “complimentary in customer,geographic and product focus,” anticipating possible anti-trust or anti-competitive issues that may be raised by the merger.

How things have changed. Before SES was even founded in 1984,PanAmSat was the first private international satellite operator to challengethe Intelsat virtual monolpoy in international satellite transmissions. Sincethen, due mainly to the pressures from private companies like PanAmSat,Intelsat has been fully privatized and now has become once again the topglobal satellite operator.

The face of the satellite industry is continuously changing. We’ll keepyou apprised of developments.. Stay tuned...

4Back to Contents

September 2005 SATMAGAZINE.COM

September 5-8, Paris, FranceWorld Satellite Business Week 2005Linda Zaiche Tel: +33 1 49 23 75 17 Fax: +33 1 48 05 54 39E-mail: [email protected]: www.satellite-business.com

September 8-12, Amsterdam, The NetherlandsIBC 2005Tel: +44 (0)20 7831 6909 / Fax: +44 (0)20 7242 8907Email: [email protected] /Website: http://www.ibc.org/

September 13-16, The Waldorf Hilton Hotel, London, England7th Annual VSAT 2005 ConfereceMaria Batet SoleTel: +44-1727-832-288 / Fax: +44-1727-810-194Email: [email protected]: www.comsys.co.uk/vc05_mn.htm

September 20-22, Hotel Grand Ashoka, Bangalore, IndiaSatellite Users Interference Reduction Group(SUIRG) 2005 Annual MeetingTel: +1-941-575-1277 / Fax: +1-941-575-7048Email: [email protected] / Website: www.suirg.org

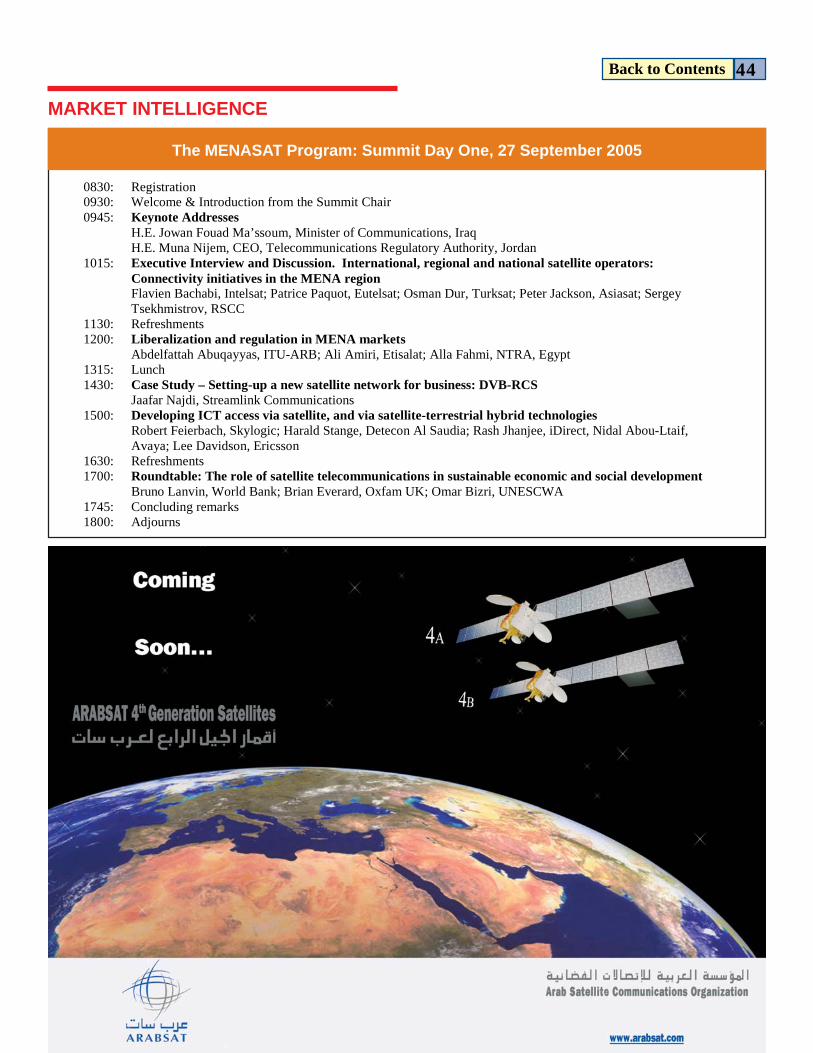

September 27-28, Dubai, United ArabEmiratesMENASAT 2005 Satellite Summit to serveas private and public sector forumJustin BambridgeTel: +44(0)207 0894200 / Fax: +44(0)207 0894201Email: [email protected]: www.thecwcgroup.com

September 29 - October 1, Vicenza, ItalySAT EXPO 2005Rosalia D’ApranoTel: +39 0444 543133Email: [email protected]: http://www.satexpo.it/en

October 17-20, Atlantic City, NJMILCOM 2005Steve WalleyTel: +1-408-213-3000 / Fax: +1-408-213-3001Website: http://www.milcom.org

October 25-27, Mumbai, IndiaSATELLITE & CABLE TV INDIA TRADE SHOW 2005Mr. Dinyar ContractorTel: +91 - 22 - 24948280 / 2498 4273 / Email: [email protected]: www.scatindia.com

CCCCCALENDALENDALENDALENDALENDAR OF AR OF AR OF AR OF AR OF EEEEEVENTSVENTSVENTSVENTSVENTSSEPTEMBER

OCTOBEROctober 3-6, Salvador da Bahia, BrazilITU Telecom Americas 2005John Jacobs Tel: +41 22 730 5401 / Email: [email protected]: itu.int/AMERICAS2005/index.html

October 26 - 27, New York, NYSATCON - Satellite Applications and ContentDelivery Conference & ExpoMichael Driscol lTel: +1-203 371 6322 / Email:[email protected]:www.satconexpo.com

Oct. 31 -Nov. 1, Marriot Grand Hotel, Moscow, Russia2nd Russia and CIS Broadband Summit andMITEL 2005 ExhibitionElena Peredelskaia / Tel: +44 (0)20 7596 5205 / 5000Fax: +44 (0)20 7596 5208 (direct line)Email: [email protected]: http://www.broadband-conference.com ; http://www.ite-exhibitions.com

November 1-4, Houston, TexasOffshore Communications 2005Inger PetersonTel: +1-772-221-7720 ext. 112 / Fax: +1-772-221-7715Email: [email protected]: www.offshorecoms.com

November 2-4, Beijing New Century Hotel Beijing, ChinaChina Satellite 2005Richard Theodor (Wozniak) Kusiolek / Tel: +1-650-428-1872Mobile: +1-650-504-2978 / Email: [email protected]: www.transglobalnet.com/

5Back to Contents

September 2005 SATMAGAZINE.COM

FEATURED EVENTS

October 26-27, 2005Javits Convention Center,New York City

SATCON, the Satellite Applica-

tion and Content Delivery Conferenceand Expo, now on it’s fourth year willbe focusing on “Satellite Applications,Content Management and ContentDelivery Solutions” in its 2005 editionto be held in New York from October26-27.

”This year’s SATCON will focusonce again on the users’ perspective ofthe industry — from the three primary customer groups: media andentertainment, military and government and the enterprise sector,” saidSusan Irwin, President of Irwin Communications and Conference Chair. “The changes in the technology, applications and structure of theindustry will be discussed by an extraordinarily high level of speakers,including senior executives from the largest corporations using satelliteservices, senior government and military officials and CEO’s of themajor satellite firms,” she added.

SATCON is one of the fastest growing shows in the satelliteindustry averaging 50 percent growth every year since it’s inception in2001. SATCON has expanded its focus this year to include contentdelivery and content management in addition to satellite applications. It will also feature over 110 exhibitors, 25 sessions and over 100speakers.

The conference will feature three tracks of sessions including :Military, Federal, State & Local Government, Homeland

Security, Relief Agencies, and NGO’s ·Broadcast, Media & Entertainment·Enterprise Applications for industries such as:

Retail, Hospitality, Food Service, Banking and Financial,Telecom& ISP’s, Healthcare, Oil & Gas, Maritime, Shipping, Transpor-tation & Fleet Management, Energy & Utilities, Manufacturing, Mining& Natural Resources, Service Industries, Distribution, and more.

Two Keynote Sessions will be highlighting the conference. Thefirst on “The Satellite Industry Emerges: New Ownership, New Life,New Management” features speakers such as:

Pradman Kaul, CEO, Hughes Network Systems,David McGlade, CEO, Intelsat,Joseph Wright, CEO of PanAmSat and

Armand Mussey, President of NearEarth, Ltd. The second keynote sessionwill focus on the military’s defenserequirements and will feature

Major General Dennis C Moran,Joint Staff Vice Director for Command,Control, Communications & ComputerSystems, Dept. of Defense.

According to organizers ofSATCON, the show features more end-user speakers and end-user attendees thanany other satellite show and is regardedby many as “the most interesting satellite

show” in terms of session content. ”We are pleased the industry and the end-user communities have

embraced SATCON and made it such a popular event to attend. Themilitary, broadcasters and enterprise firms support SATCON in a bigway, and that shows us we are doing the right things as wecontinually develop and improve the event each year,” said MichaelDriscoll, SATCON Event Director.

”It’s been extremely gratifying to me to see SATCON evolve intoa user-focused conference and trade show, having been attendingindustry conferences for so many years in which the primary activityhas been vendors talking to vendors,” said Conference Chair Irwin.“SATCON has singlemindedly focused on the end user and trulyproviding the customers’ perspective. Any enterprise, government orbroadcast executive who is looking at communications solutions, canbenefit from the experiences of those who have done it—what worksand what doesn’t. SATCON provides the ideal forum for thisexchange,” she added.

To encourage more users of satellite services to attend theconference, A limited number of complimentary full-conference passesare being offered by the organizers for “end-users,” defined as “acurrent employee from a broadcast/media & entertainment firm,military, government or a private sector company that uses informationand communications technology (ICT) but does not sell ICT services,equipment, integration or consulting."

”Major satellite companies are sponsoring SATCON includingIntelsat, Hughes, Artel, GlobeComm, New Skies, Thrane and Thrane,iDirect, Flextronics and Viasat, among others.

For more information on SATCON’s program, registration orexhibition and sponsorship opportunities go to www.satconexpo.com or phone 203-371-6322 e-mail : [email protected]

SATCON Conference & Expo to Focus on Satellite, Content Management, Distributionand Delivery Solutions

SM

6Back to Contents

September 2005 SATMAGAZINE.COM

Ariane 5 Successfully LaunchesThailand’s iPSTAR Broadband Satellite

After an almost two-year delay,Thailand’s iPSTAR broadbandsatellite is finally launched onThursday from Kourou, FrenchGuiana. (CNES/ESA/Arianespace photo)

Starsem’s Soyuz-Fregatsoars to space success-fully orbiting PanAmSat’sGalaxy 14 satellite in anearly Sunday morningmission from BaikonurCosmodrome. (PanAmSatphoto)

KOUROU, FrenchGuiana —Arianespace’s lAriane 5 launcher successfully launched on August 11 Thaicom 4(iPSTAR) during anearly-morning missionfrom the Spaceport inFrench Guiana. Thepayload is the heaviestcommercial satelliteever delivered togeosynchronous orbit. Thaicom 4 is a high-power broadbandsatellite built by SpaceSystems/Loral (SS/L)for Shin Satellite Plc of

Thailand designed to provide broadband services to bothenterprises and consumers throughout 14 countries in the Asia-Pacific region. The satellite had a launch weight of 14,300 pounds(6486 kilograms). The satellite has a massive total data throughput capacity of over45 Gbps. It is designed to provide users with data speeds of upto four Mbps on the forward link and two Mbps on the returnlink. Thaicom 4 will use its seven on-board antennas to create 112spot and regional beams in the Ku and Ka frequency bands. Thesatellite will generate 14 kW of electrical power throughout itsplanned 12-year service life. Shin Satellite, aprovides C- and Ku-bandtransponder leasing, teleport and other value-added andengineering services to users in Asia, Africa, Europe andAustralia. Shin Satellite owns and operates Thaicom 1A, Thaicom2 and Thaicom 3. The satellites carry a total of 47 C-band and 20Ku-band transponders offering over 100 channels. Thaicom isthe hot-bird for Indochina, an emerging platform of choice fortranscontinental satellite television broadcasts from Europe toAustralia. The company is hoping that its efforts to develop new technology to make Internet via satellite more

efficient would pay off with the launch of iPSTAR.

Once in operational service, Thaicom 4 will generate 14 kW ofelectrical power during its planned 12-year mission life, providingInternet access and broadband services to businesses andconsumers through 84 spot beams, three shaped beams andseven regional broadcast beams. Galaxy 14 Orbited; Satellite to ExpandPanAmSat’s US Cable TV Fleet

BAIKONURCOSMODROME,Kazakhstan — Starsem’sSoyuz-Fregat launchersuccessfully orbited onSunday PanAmSat’s Galaxy14 satellite in an earlymorning mission fromBaikonur Cosmodrome. The Soyuz-Fregat launcherlifted off from BaikonurCosmodrome on schedule at5:28 a.m., August 14, localtime and climbed out on thepower of its four first-stageboosters and central coresecond stage.

The flight was performed by Starsem as part of the cooperationwith its Arianespace affiliate company, which allows the twolaunch service providers to best respond to their clients’ needs.Galaxy 14 originally had been planned for launch on anArianespace Ariane 5, and subsequently was switched toStarsem’s Soyuz-Fregat to meet PanAmSat’s operational require-ments. Galaxy 14 is the 24th satellite in PanAmSat’s fleet. The satellite, tobe co-located with Galaxy 12 at 125 degrees west longitude, willenable PanAmSat to have two in-orbit spares for its U.S. fleet,allowing the company to continue to provide the highest fleetredundancy and reliability in the FSS industry. Although designated a back-up satellite, the powerful all C-bandspacecraft is designed to deliver digital video programming,high-definition television (HDTV), VOD and IPTV servicethroughout the continental U.S.EU Clears United LaunchAlliance,

INDUSTRY NEWS

7Back to Contents

September 2005 SATMAGAZINE.COM

INDUSTRY NEWS

Space Launch Joint Venture ofLockheed Martin and Boeing BRUSSELS — The European Commission has cleared thecreation of United Launch Alliance (ULA), a space launchservices joint venture, between Lockheed Martin and Boeing. The EU said the approval was made under the EU MergerRegulation. EU concluded the proposed transaction will notsignificantly impede effective competition in the European Union. Both Boeing and Lockheed provide space launch services togovernmental and commercial customers. Lockheed is active onthe market with its Atlas family of launch vehicles as well as withProton, a launcher produced in a joint venture with Russianpartners. Boeing offers the Delta launch vehicles as well as

launchers produced by SeaLaunch, also a joint venture withRussian partners. Both Boeingand Lockheed also produce andmarket satellites. ULA, structured as a 50-50 jointventure, will combine the produc-tion, engineering, test and launchoperations associated with U.S.government launches of Boeing’sDelta and Lockheed’s Atlasrockets. ULA is exclusivelyintended to serve the US govern-

ment market for launch services.

8Back to Contents

September 2005 SATMAGAZINE.COM

INDUSTRY NEWS

Global Lease Revenues forCommercial Satellite Capacity to Hit$7.3-B in 2010, Says Northern SkyResearch ORLANDO, Fla. — Northern Sky Research (NSR) saiddemand for commercial C- and Ku-band capacity is growing atan average annual rate of 3.1%, and the total number of leasedtransponders should exceed 4,950 in 2010, up from 4,125 as ofthe end of 2004. According to NSR’s newest market survey and forecast report“Global Assessment of Satellite Demand: A Demand-Driven,Region-Specific Analysis of the Commercial GeostationarySatellite Transponder Market for 2004-2010,” demand for C-band capacity is flat to declining in half of the regional marketsinvestigated in detail, and the real engine for growth in mostmarkets will be the lease of commercial Ku-band capacity forvideo distribution, Direct-to-Home (DTH) and emerging satellitebroadband services. To reach this conclusion, NSR structured the study such that inexcess of 100 individual demand forecasts were performed inorder to provide the detailed wealth of information the commer-cial satellite industry requires to successfully grow within anever more competitive marketplace. Separate regional C- andKu-band demand forecasts were performed for each of the majorsatellite applications investigated in the study. These applications included the three cited above, in addition tovideo contribution & OUTV, telephony & carrier, narrowbandVSAT and a group of other niche satellite services. NSRprimarily utilized a bottom-up approach to build its marketassessment for each of the following regional markets: NorthAmerica, Central America & Caribbean, South America, theAtlantic Ocean Region, Western Europe, Central & EasternEurope, the Middle East & North Africa, Sub-Saharan Africa,East Asia, South Asia, Southeast Asia, and the Pacific OceanRegion. Stratos to Acquire Xantic for $191-M BETHESDA, MD — Stratos Global Corp. announced on Aug. 15the signing of a letter of intent to purchase the shares of XanticB.V. According to Stratos, the transaction will create the world’sleading provider of advanced remote communications solutions,with a significantly expanded geographic presence and customerbase in the Americas, Europe and the Asia-Pacific region.

Under the terms of the agreement, Stratos will acquire 100 percentof Xantic, jointly owned by KPN N.V. (65 percent) and TelstraCorp. Ltd. (35 percent), for approximately US$191 million. But theprice is subject to adjustment based upon audited EBITDA forthe 12 months immediately preceding closing and specifiedworking capital levels. Xantic, with 2004 revenue of approximately $172 million, employs270 people worldwide and operates two Inmarsat Land EarthStations in Burum, Netherlands, and Perth, Australia. In addition,Xantic has been selected by Inmarsat to host the new SatelliteAccess Station for the next-generation Inmarsat BGAN (Broad-band Global Area Network) service, slated for commercial launchlater this year. The combination of Stratos’ presence in theGovernment and Military, Energy and Leasing sectors, combinedwith Xantic’s position as a provider to themaritime and carrier sectors, gives the combined business akey presence in the key markets for mobile satelliteservices, said Stratos. J.D. Power and Associates Reports:Satellite TV Penetration IncreasesSignificantly

WESTLAKE VILLAGE, Calif.— The number of householdssubscribing to satellite TVservice has increased dramati-cally over the past year, evenas cable narrows the gap incustomer satisfaction ratings,according to a J.D. Power andAssociates newly releasedstudy.

Satellite TV service continues to erode cable’s market share,increasing every year for the past 10 years and making its mostsignificant leap this year, the study said. Currently, 27 percent ofU.S. households only subscribe to satellite service — up from 19percent in 2004 and 12 percent in 2000. Sixty percent of house-holds only subscribe to cable service — down from 62 percent in2004 and 66 percent in 2000. “Although satellite providers continue to gain market share,overall customer satisfaction among satellite subscribers hasdeclined while satisfaction among cable subscribers is up,” saidSteve Kirkeby, senior director of telecommunication research for

9Back to Contents

September 2005 SATMAGAZINE.COM

INDUSTRY NEWS

J.D. Power. “Overall, satellite customers are still more satisfied with theirservice than cable subscribers, but if satellite providers want to continueto attract subscribers away from cable, customer satisfaction is a criticalarea where they can’t afford to lose ground.” J.D. Power said for the first time since 2001, a cable service provider —WOW! (WideOpenWest) — holds the top carrier position in the customersatisfaction rankings. WOW!, which operates in major markets in Michi-gan, Illinois and Ohio, ranks highest among 14 of the nation’s largestcable/satellite companies with an index score of 717 (on a 1,000-pointscale).

Space and Satellite Market Tops $103-B,Seen at $158-B by 2010

BETHESDA, Md. — The International SpaceBusiness Council has released its 2005 State ofthe Space Industry report, which shows worldturnover generated from commercial services andgovernment programs reached $103 billion in 2004and is predicted to exceed $158 billion in 2010. First released in 1997, the report was developed toprovide industry, government, and financiers with

an independent assessment of the trends and issues affecting the indus-try. The report concluded “now is a good time to be involved in the space andsatellite industry,” saying government funding for space is on the rise,commercial orders for satellites and launches have rebounded andstabilized, new exploration initiatives are being pursued, and entrepreneur-ial efforts related to radio, broadband, and space tourism are generatingexcitement. It said, whatever one’s focus — on military, civil government, or commer-cial activities — is not necessary as there are numerous opportunities. The report described U.S. export regulations under ITAR “the industry’smost serious issue” and states, “what initially was a nuisance to busi-nesses has evolved into a serious problem for U.S. industry.” Other highlights of the ‘2005 State ofthe Space Industry’ include:

More than $18 billion is spent annually on the development of spacesystems. U.S. Defense spending on space has grown from around $15billion in 2000 to more than $22 billion today and is forecast to reach $28billion by 2010. India and China have joined the U.S., Europe, Russia, andJapan as having fully independent capabilities. SM

10Back to Contents

September 2005 SATMAGAZINE.COM

EXECUTIVE MOVES

WildBlue Names David Leonardas CEO

Denver, CO — WildBlue Communications, Inc. announced onTuesday David Leonard will be joining the company on Septem-ber 1 as its Chief Executive Officer. Leonard comes to WildBluefrom Liberty Global Inc., where he served as president of theLatin America Division.

Tom Moore, WildBlue’s co-founder and current CEO, will relinquishday-to-day operating responsibility. He will, however, stayactively involved with the company as a shareholder and boardmember.

“WildBlue now needs a world-class operating CEO to drive thecompany to the next level of success - Dave has those incredibletalents and I am really looking forward to seeing what he is ableto accomplish,” says Moore,

Leonard brings more than 25 years experience in media andtelecommunications to WildBlue. Most recently, Leonard hasbeen working with Liberty Global (LGI, formerly Liberty MediaInternational) overseeing operations in Argentina, Chile andPuerto Rico. Prior to LGI, Leonard was founder and CEO atVeloCom Inc. which established the largest competitive localexchange carrier in Latin America.

He has served as either CEO or Board Member of several foreignand domestic entities including VTR (Chile); Cablevision(Argentina); Metrocall Wireless (USA); United InternationalHoldings; Kabelvision (Sweden), and United Cable of Colorado(a subsidiary of United Cable Television Corporation). Leonardwas named Ernst & Young’s “Entrepreneur of the Year” in 2000.

An always-on broadband Internet connection, WildBlue’sservice provides two-way wireless high-speed Internet access.

Lockheed Names James B. ComeyGeneral Counsel BETHESDA, Md. — Lockheed Martin has named James B.Comey, 44 as successor of Frank H. Menaker, Jr., 65, thecorporation’s senior vice president and general counsel, effectiveOctober 1, 2005. Menaker, who has served as general counselsince March 1995, will retire at the end of January 2006. Comey joins Lockheed Martin from the U.S. Department of

Justice, where he has served as Deputy Attorney General sinceDecember 2003. In this position, he oversaw many importantgovernment cases, including terrorism and securities fraudprosecutions. Previously, he served as United States Attorney for the SouthernDistrict of New York, where he had earlier been an assistant U.S.Attorney and lead prosecutor in the highly publicized UnitedStates v. John Gambino racketeering and murder trial. From 1996through 2001, he was Managing Assistant U.S. Attorney incharge of the Richmond Division of the U.S. Attorney’s office forthe Eastern District of Virginia. TerreStar Appoints Robert Brumleyas President and CEO; Wharton B.Rivers, Jr. Joins Board asVice Chairman MCLEAN, Va. — TerreStar Networks has appointed Robert H.Brumley as the company’s new president and chief executiveofficer. Brumley joins TerreStar from Pegasus Global, an interna-tional firm specializing in telecommunications/technology,infrastructure development and aerospace/defense. Brumley’s extensive experience and background includes seniorexecutive positions with global communications firms such asDeutsche Telekom and Bell Atlantic International where Brumleywas responsible for Bell Atlantic’s international telecommunica-tions transactions worldwide, including its participation inConstellation Communications, Inc., a low earth orbit satelliteventure. Brumley also served as a Presidential appointee of the ReaganAdministration, as General Counsel of the U.S. Department ofCommerce, where he was chief legal officer of the Departmentand senior policy advisor to the Secretary. Brumley served onsenior-level working groups of the National Security, Domesticand Economic Policy Councils. Brumley also chaired the ReaganAdministration policy group that privatized commercial spacetransportation and removed NASA from the burden of launchingcommercial satellite payloads on the Space Shuttle (STS).

Measat Appoints New VP, Sales &Marketing KUALA LUMPUR — Measat Satellite Systems Sdn. Bhd.(formerly known as Binariang Satellite Systems Sdn. Bhd.) has

11Back to Contents

September 2005 SATMAGAZINE.COM

EXECUTIVE MOVES

appointed Diego Sutachan as vicepresident of Sales & Marketing. Measat said Diego will oversee all ofthe company’s key sales functions,including identifying new salesopportunities for the upcomingMEASAT-3 satellite (due for launchlater in 2005). Diego comes to Measat fromTeleglobe, where he held the

position of executive director, Asia Pacific Region, for 4 years.Prior to Teleglobe, Diego held various engineering, sales andmarketing positions in Telecommunications and IT industryacross Asia Pacific with companies such as Fujitsu, ComTechand AAPT Sat-Tel (now New Skies Satellite)

Scott Schneider Joins New SkiesSatellites as Director The Hague, The Netherlands — New Skies Satellites HoldingsLtd. has taken in Scott Schneider as a member of its boardbringing the total number of directors to eight. Schneider, whoseappointment takes effect on August 7, 2005, will also serve as amember of the company’s Audit Committee. New Skies said Schneider will serve as “independent” directorunder the rules of the New York Stock Exchange and thecompany’s Corporate Governance Guidelines. He will serve as aClass II director. Schneider is currently a member of the board of directors ofCitizens Communications. He was previously vice chairman,president and CEO of Citizens from 2002 to 2004 and has heldvarious executive positions at Citizens since 2000. Prior to joiningCitizens, Schneider was chief financial officer and a member of

Diego Sutachan

12Back to Contents

September 2005 SATMAGAZINE.COM

EXECUTIVE MOVES

the board of directors of Century Communications, where he worked from1982 to 1999. Schneider also served as chief financial officer, senior VP andtreasurer and a member of the board of directors of Centennial from 1991 to1999.

ILC Appoints New Directors for ProductDevelopment and Federal SystemsATLANTA, GA- Network control software provider ILC has appointed twonew directors for product development and federal systems. KimHarrington was appointed director for product development and RobertHuggins, director of Federal Systems.

Huggins comes to ILC from Harris Corp.'s Network Support Divisionwhere he directed the Government Sales Team towards $4.5 million inannual sales of network management products and services.

Huggins started at Harris as a systems engineer and later became amanager of business development, during which time he ranked as a topperformer, securing and providing engineering support for multi-million-dollar orders. Previously, Huggins was section head of TRW’s FederalSystems Group where he led the design and development of operationssystems for programs such as the Anti-Submarine Warfare OperationsCenter (ASWOC) C3 Upgrade. Experienced in end-to-end management of software lifecycles,Harrington will lead ILC's product development organization to handleincreasingly complex demands as the company pursues both new andexisting markets for its network management software.

Prior to ILC, Harrington was executive program manager at a major U.S.telecom service provider (RBOC) where he oversaw the execution of anextensive product portfolio including network management and provision-ing technology. At telecom interconnect company Expanets, Harringtondirected product strategy, implementation, market introduction and lifecyclefor Internet telephony converged voice and data solutions, as the companygrew from a start-up to a billion dollars in revenue.

NSG Datacom Appoints Bill GrantVP of Sales

NSGDatacom has appointed William (Bill) Grant to the position of VicePresident, Sales.

Bill will report to Rich Yalen, Chief Executive Officer. Yalen said, “WithBill’s background, NSG Datacom’s product portfolio and new productsbeing launched in the near future, I am excited about our ability to con-tinue to grow the business profitably.”

Grant said, “I am confident in NSG Datacom’s commitment to offer our

13Back to Contents

September 2005 SATMAGAZINE.COM

EXECUTIVE MOVES

Officials and Association of Procurement Technical AssistantCenters.

Den Hartog’s expertise includes sales, marketing and businessdevelopment management. Den Hartog previously served as theDirector of Sales and Marketing/Director of Business Develop-ment for the global R.C. Smith Company of Burnsville, Minne-sota. He produced 20 to 35 percent of growth annually ongovernment sales, reaching a record level for the company andexpanded business into the United Kingdom, the Middle Eastand U.S. overseas military facilities. Den Hartog has also heldsales and marketing positions in the medical arena includingsurgical and rehabilitation products, and founded the Savage,Minn. Chapter of Rotary International.

WCC has been working with numerousgovernment agencies. The company was awarded a five-yearU.S. General Services Administration (GSA) contract as anapproved supplier of Iridium satellite phones services andaccessories to all U.S. federal government agencies. Additionally,WCC helps supply the U.S. government in their efforts in Kuwait,Iraq and Afghanistan. A sampling of U.S. government agenciesthat WCC has worked with include: The U.S Coast Guard,Department of Homeland Security, The Marine Corps, NASA andthe Environmental Protection Agency. WCC is also the soleprovider of backup communications for the Oahu Civil Defenseoffice in Honolulu, Hawaii.

Futron Corporation Names BernardoSchneiderman as BusinessDevelopment &Technical Director

Bethesda, MD — Futron Corporation hasappointed Bernardo Schneiderman asBusiness Development and TechnicalDirector of the Space and Telecommuni-cations Division, responsible for expand-ing corporate activities on the WestCoast and in international markets.

Mr. Schneiderman, who will be based inIrvine, California, has spent 30 years inthe satellite and telecommunicationsindustry. He has extensive experience inproject management, business develop-ment, sales and marketing for satellite

operators, telecommunications companies, VOIP carriers andequipment manufacturers in the U.S. and international markets.

Robert C. DenHartog

John D. Kilian

BernardoSchneiderman

SM

customers a compelling value proposition based on real worldsolutions for the satellite, government, military, financial, lotteryand wireless markets.” Grant has over 25 years of sales andexecutive sales management experience with established andstart-up vendors of networking and communications equipment,selling to large enterprises and service providers worldwide.

WCC Expands Government Division

Chandler, Ariz., –World Communica-tion Center (WCC), aprovider of globalsatellite voice anddata communications,announced theexpansion of itsGovernment Divisionwith the addition of

two industry veterans, John D. Kilian and Robert C. Den Hartog.Kilian and Den Hartog will supercharge WCC’s governmentinitiatives to provide reliable satellite communications disasterrecovery initiatives, backup communication systems, militarydocking systems, and more to government entities worldwide.

Welcoming Kilian and Den Hartog, WCC CEO, Weldon Knape,says, “Our solutions deliver critical satellite voice and dataservices at all levels: subterranean, on-ground, within buildingsand above-ground – as well as 24x7 live customer support – tousers in areas that would normally be deemed inaccessible forcommunications. Our solutions are ideal for government entitiesand we are confident that Kilian and Den Hartog’s in-depthexperience in this sector will help us maximize business expan-sion.”

Kilian brings over 26 years of government procurement andcontacting management expertise. From 1999 to 2003, Kilianserved as Area Manager for the Procurement Technical Assis-tance Center of Minnesota Project Innovation (MPI).where he collaborated with over 150 area local companies tosecure business from federal, state and local governments. From1994 to 1999 he was responsible for strategic development,standardization and management of government procurementprocesses for Northeast Computer Supply, Inc. He also workedfor Motorola and Control Data Corporation. Kilian earned aBachelor of Science degree from the University of Wisconsin-Stout and is an active member in the National Contract Manage-ment Association, National Association of State Procurement

14Back to Contents

September 2005 SATMAGAZINE.COM

NEW PRODUCTS

Gilat Ships 30 SkyEdge Hubs, 10,000VSATs; Unveils SkyEdge Basic Hubfor Small Networks

PETAH TIKVA, Israel— Gilat SatelliteNetworks Ltd. hasshipped more than 30SkyEdge commercialhubs and more than10,000 SkyEdge VSATsworldwide. Gilat’s SkyEdge systemis based on the conceptof a single scalable hub

that serves a variety of market segments. The SkyEdge hub isavailable in various configurations to support a wide range ofnetworks, from small networks, consisting of a few tens of sites,to large networks that include tens of thousands of sites. Thesenetworks can be operated in either a dedicated or a shared hubenvironment, according to Gilat. The SkyEdge hub supports a family of VSATs tailored for variousapplications such as broadband, VoIP, video, trunking andothers. In addition, the SkyEdge platform supports both Star andMesh topologies. This single hub allows the operator to simulta-neously serve various customers, while providing security,Quality of Service (QoS) and management for each, as well astrue network segregation. According to Gilat, SkyEdge’s unique system architectureenables network operators to provide specific services todifferent end customers from a single hub. FAA OKs Digital Angel’s New SatelliteTransceiver - CommPoint 3 (CP3) SO. ST. PAUL, Minn. — Digital Angel Corp. said its OuterLinksubsidiary has been approved by the Federal Aviation Adminis-tration (FAA) for its new satellite radio transceiver. Called the CommPoint 3 (CP3) Satcom Data Terminal, the devicecan track a wide variety of international commercial, militaryaircraft and ground vehicles in any weather condition, even whenother traditional communication modes are disrupted. The CP3 issmaller, lighter and easier to install than its predecessor, the CP2,

and, with models to be introduced in the fall, will allow OuterLinkfor the first time to address the international tracking marketplace. “The FAA regulatory approval allows us to offer this product toboth international commercial and military customers andutilizes advanced components to track vital equipment inlocations and circumstances such as heavy storms or whereaircraft are not trackable by radar,” said Digital Angel CEOKevin McGrath. The CP3, although similar and compatible with the CP2, incorpo-rates features that enable it to operate with communicationsatellites on a global basis. This capability will facilitate expan-sion of communication coverage from the existing North Ameri-can service area to transoceanic and other continents, eventuallyproviding global capability which is essential for providing real-time mobile asset management capabilities for the U.S. Depart-ment of Homeland Security and military markets. Blue Sky Offers Online Global SatelliteTracking System for TransportationAsset Management LA JOLLA, Calif. — Blue Sky Network, a global logisticssolution for two-way linking and managing remote transporta-tion assets via satellite, has released SkyRouter, an interactiveWeb portal with detailed mapping for tracking transportationassets anywhere on earth. Blue Sky claims it is the first satellite tracking company toprovide global tracking and event management (take-off, landingand inactive/active asset updates) on the Internet, allowingdispatchers and logistics managers to view their transportationassets anywhere, anytime. Blue Sky said its SkyRouter system is reliable and completelysecure, giving customers peace-of-mind when running theirsystems. Blue Sky Network customers can login to their onlineaccount and quickly locate all of their transportation assets(aircraft, vessels, land-based) across the globe in near real-time. After a recent SkyRouter demonstration, Tom Bondurant,logistics coordinator for Unocal said we finally have a servicethat can monitor aircraft, boats and land transportation, with asingle application. “Blue Sky Network provides the informationcustomers need when and where they need it, and because theycan be integrated with logistics as well as financial management

15Back to Contents

September 2005 SATMAGAZINE.COM

NEW PRODUCTS

applications, customers will be able to use their data in a real-timeformat to execute their business processes.” MDU Installs Single Wire SolutionFrom DirecTV TOTOWA, N.J. — MDU Communications International, Inc., aprovider of DirecTV digital satellite television programming saidcondo, co-op owners and apartment renters now have unlimitedaccess to the full DirecTV television experience after DirecTV hasdramatically simplified the process of delivering its programmingand services to customers living in multi-family housing. MDU said a new advanced multi-satellite distribution systemdeveloped by DirecTV, and first installed by MDU Communica-tions in a new luxury apartment complex in New York City, is nowavailable to the MDU market nationwide.

Developed by DirecTV, thisnew technology is capable ofreceiving and distributingprogramming - more than 225channels of sports, news andfamily entertainment - fromeach of DirecTV’s existingsatellites via a single wire tothe MDU customer’s home.This system more efficiently

supports the use of multiple receivers, and has the ability todeliver other national, local and high-definition programmingservices. The system was designed to work with a building’sexisting wiring and also support older DirecTV receivers that arestill in use. A new 274-unit luxury rental property in lower Manhattan is thefirst building in the nation to have the new DirecTV single wire

16Back to Contents

September 2005 SATMAGAZINE.COM

NEW PRODUCTS

distribution system in operation.MDU Communications was the firstDirecTV MDU dealer to install andutilize the new technology. Qualcomm,Connexion by BoeingTest In-FlightMobile PhoneCommunications SEATTLE — Qualcomm Incorpo-rated and Connexion by Boeing areworking together to test and demon-strate in-flight wireless communica-tions aboard Connexion One, aspecially equipped Boeing 737-400aircraft. The companies said they haveperformed a series of test flights thatsuccessfully demonstrated thesimultaneous use of CDMA andGSM mobile phone technology overan on-board network with infrastruc-ture and integration support fromUTStarcom, Inc. Using standardcellular communications, a small in-cabin CDMA2000 and GSM“picocell,” or small cellular basestation, is connected to the world-wide terrestrial network by an air-to-ground satellite link provided by theConnexion by Boeing high-speedairborne network. Passengers on the test flight wereable to use BREW-based dataapplications via Qualcomm’s BREWsolution. The BREW solutionenables users to download businessapplications, 3D games, informationand communication applicationssuch as email and instant messengerwirelessly, over the air. Passengersalso downloaded and watched videoclips and made phone calls on avariety of mobile devices including3G mobile phones.

17Back to Contents

September 2005 SATMAGAZINE.COM

NEW PRODUCTS

Audiovox and XM Unveil XpressRadio, Thinnest Radio

HAUPPAUGE, N.Y. — AudiovoxCorp. and XM Satellite Radio haveunveiled the Xpress radio, a all-newXM plug-and-play receiver fromAudiovox. The Xpress is beingbilled as the smallest satellite radioreceiver to offer a five-line displayscreen. Tom Malone, senior vice president

of sales for Audiovox, said the Xpress offers brand new conve-nience features in a compact design, providing consumers with asleek, functional device to access XM’s amazing service. The Xpress combines compact design and a five-line displayscreen, allows the user to search XM’s 150-plus channels ofcommercial-free music and premier sports, talk, news, andentertainment programming with just one knob, and comes with aremote control so that other passengers can control the program-ming. The Xpress can be self-installed quickly and easily in thecar or home. BBC Radio 1 Launched on Sirius NEW YORK — Sirius Satellite Radio launched on Aug. 10 BBCmusic channel Radio 1 in America during the channel’s ChrisMoyles Breakfast Show. Sirius’ broadcast of BBC Radio 1 will bring its subscribers theirfirst opportunity to listen to the music channel from the UK. BBC Radio 1 will provide Sirius subscribers with a cutting-edgemix of pop, rock, R&B and hip-hop music. Radio 1 is alsointernationally recognized for its support of up-and-comingBritish artists, its unique in-studio performances and interviews,its extensive coverage of the international music scene, and itsengaging and informative hosts and entertainment information.

Telenor to Offer Inmarsat SatelliteService in Brazil OSLO, Norway — Telenor Satellite Services has receivedapproval from the Brazilian government to begin offeringInmarsat satellite services directly to service providers and theircustomers throughout Brazil. SM

The official announcement appeared in the Diário Oficial daUnião, the official government record publication of the Braziliangovernment on July 25, according to Telenor.

The negotiations process for the service began in 2002 withInmarsat, Embratel, and the Brazilian government to authorizeTelenor to sell directly to service providers and their customers inBrazil. Prior to the approval, Telenor Satellite Services was able tosell Inmarsat service in country only through state-sponsoredservice provider Embratel.

Tore Hilde, chief executive officer of Telenor Satellite Services,said Telenor can now offer its complete portfolio of ‘on demand’Inmarsat satellite services to service providers in Brazil and theircustomers needing reliable communications on land, at sea, andwhile in flight.

Germany’s Teles skyDSL SatelliteService Expands to the UKBERLIN — Germany’s broadband via satellite provider, TelesWireless Broadband Internet GmbH, is expanding to the UK viaits new subsidiary Teles skyDSL UK Ltd. based in Birmingham.

“The British market is attractive to us as satellite services alreadyhave a large established customer base,” says Klaas Imgenberg,managing director of Teles Wireless Broadband Internet GmbH.“Hence we anticipate a particularly quick acceptance by themarket of using broadband internet access via satellite.”

skyDSL was developed by IT company Teles AG from Berlin. Ithas been successfully established in Germany with several tenthousands customers gained in the past years. Imgenberg saidskyDSL is aimed at all British internet users.

MSV Introduces the MSAT-G2 MobileSatellite Radio

DENVER — Mobile Satellite Ventures will unveil this month itsnew MSAT-G2 Mobile Satellite Radio. MSV said this new two-way radio was developed to address the increasing needs anddemands of public safety and emergency response personnel,which include: interoperability with Land Mobile Radio systems;access to multiple agencies and talk groups; as well as GPS,which enables emergency management coordinators to know theexact location of their people.

Designed for the MSAT Network, the MSAT-G2 supportscontinent-wide satellite Push-to-Talk (PTT) Dispatch Radio andCircuit Switched Voice communications.

18Back to Contents

September 2005 SATMAGAZINE.COM

COVER STORY

“European broadcasting has never been in better shape.” Or “It’s a real challenge making

any money”. These two comments fromsenior suits at major European broadcast-ing companies sum up the current state ofplay. The “Glass half full” point-of-viewhas much merit behind it. In one recentmid-summer day (August 22) we had newsthat BSkyB had announced its first 6 high-def channels, on top of declaring recordsales for its direct-to-home pay-TVoffering, and that the company waspreparing to buy back more of its stockand was even on the expansion trail.

On the same day Private Equityoutfits Permira and Kohlberg KravisRoberts agreed to buy Amsterdam-basedSBS Broadcasting (not to be confused

Glass Half Full, or Glass Half Empty?By Chris Forrester

European TV:

with SBS Comm’s) for a thumping $2.1bnin cash, and making a nice return oninvestment for chairman Harry EvansSloan and main backer Liberty Media(21.9%). Sloan, and CEO MarkusTellenbach stay on in executive positions.SBS is an absolute ‘rags to riches’television story that we’ll return to in amoment.

BSkyB’s CEO is James Murdoch,and is now heir-apparent (if not CrownPrince) of Rupert’s News Corp empire.However, he told journalists that he wasin London at Sky for the long haul. “Ifully intend to be here for the long term.I’m engaged by the business, the teamand I are working hard on the business.That’s my comment,” he stressed.

In all fairness, rising son Murdochdelivered a robust and upbeat financialpresentation, all-embracing in his visionand confidence of Sky’s ability to hit 10mby the end of calendar year 2010. Some 18months ago, while some newspapers weredescribing his performance as “fidgety”,he announced Sky’s “investing forgrowth” strategy, which now is paying

dividends, he said. He argued that there’splenty of upside to come, including HDTV(“early 2006”), a neat wireless audio‘sender’ gadget called “Gnome” (dis-played sitting in a faux-garden settingcomplete with deck chair, sun parasol andopened bottle of beer), and stunninglygood sales of its Sky+ PVR units (to888,000 or 11% of its 7.8m subscriberbase). “We’ll pass 1m in a few weeks,”

Murdoch told his audience, high-lighting the increased revenueposition (up 11% to $7.5bn), muchimproved operating margin of 20%(profit before goodwill andexceptionals up 34% to $1.5bn) andprofit after tax up 32% to $750m. Heoutlined that revenues from on-screen gambling will soon be thebroadcaster’s second-largest incomestream (after subscriptions) beatingwholesale and advertising income.He added that ARPU was up in Q4.

James Murdoch

Harry Evans Sloan

19Back to Contents

September 2005 SATMAGAZINE.COM

COVER STORY

“We’ve never been stronger,” he said, “and “the business is in tremendoushealth.” Unsaid might have been histhought ‘What more can I do?’

He’s right. Since August 26 UKviewers have been able to sign up toBSkyB’s high-def offering. Early orderswere being taken at consumer electronicsstores, even though Sky has not yetindicated its pricing structure for the first6 channels announced. The channelsthemselves are hardly surprising. How-ever, in some regards what Sky has leftout of its initial announcement is perhapsmore surprising than what’s included.

Not present – yet - is either of the

20Back to Contents

September 2005 SATMAGAZINE.COM

COVER STORY

much-anticipated ‘documentary services’.National Geographic’s already confirmed(by Nat-Geo) high-def version is missingfrom the list. Nor is Discovery HD Theatrepresent, suggesting that Sky might wiselybe keeping its powder dry for its SecondBurst of marketing later this year. Sky saysit is in “advanced discussions” with otherchannels interested in offering HFservices on digital satellite, “which will beannounced in the coming months”.

Also answered on Aug 22 is thewhole question of how BSkyB would treatits flagship channel, Sky One, where mostof its American imports sit along with itsown high-profile drama series like ‘Hex’,captured in high-def. Sky say there will bea simple “simulcast” of the standard andhigh-definition channels.

In other words, BSkyB will orches-trate its usual hype and promotion to theestimated 2m flat-panel owners already inthe UK (out of a total TV universe of some25m homes). Next year it will launch high-

def and – in their view – reap the rewardsfor what James Murdoch promises to be“the most exciting thing to have happenedto television – ever.”

Other countries that are equallyenthusiastic towards high-def are Ger-many (Premiere), most of the Scandinaviannations (Canal+) and France (Canal+ andTPS). Italy (Sky Italia) and Spain (Canal+)have yet to show their hand, but mostexpect announcements soon.

Indeed, most of these markets havenot only buoyant pay-TV businesses inoperation, but also a growing digitalterrestrial multichannel market. While theUK’s ‘Freeview’ offering now reaches wellover 5m homes, it now has imitators justabout everywhere. It’s early days yet, andnobody has even got close to the UK’ssuccess, but that very success hasgenerated plenty of digital terrestrialinterest. ‘Freeview’ has even forced thestruggling ITV Network to wake up andsmell the coffee. ITV, the UK’s primary

commercial network, has been languishingin the doldrums. Advertising income isdown, viewer ratings are suffering whichfurther drains away precious ad-income.Last year, and some 17 years after BSkyBstarted, ITV launched its second channelin an attempt to win a greater slice ofmultichannel shelf-space. It has sincelaunched a third, and in August promisedit would launch its own Kids Channel (ontop of the 20 or so kids service nowavailable) and a channel for “men’currently dubbed ITV4. It has consistentlymissed the multichannel boat and onlynow is it playing an aggressive game ofcatch up.

The decision is not a moment toosoon. ITV has drifted in 5 short years frombeing Britain’s most important commercialchannel with an audience market sharethat exceeded the BBC’s, to today’s share(in multichannel homes) of just 16.4%.That’s still a big number, but the overallmix is helped by ITV2’s 2.1% share, andITV3’s 1.2%. Neither is costing much tocreate being, by and large, channels thatare full of repeats.

Just as a reality check, BSkyB’sroster of channels, when combined,deliver a typical 8% share while the BBC’snon-network channels (that is their newmultichannel offerings), deliver a useful4.1%. In other words ITV, thanks to itsnew-found policy, is already doing well.

It’s much the same in mainlandEurope, which takes us back to SBSBroadcasting and their recent takeover byPermira/KKR. SBS only started in Europein 1990 by buying up a couple of strug-gling local TV stations in Scandinavia.Since then chairman Harry Sloan hasturned a $25m initial investment intotoday’s $2bn operation. It has expandedand now serves more than 100m viewersin 9 Western and Central Europeanmarkets, and can now justifiably bedescribed as Europe’s second-largest

21Back to Contents

September 2005 SATMAGAZINE.COM

COVER STORY

European Digital Satellite Platforms

WESTERN EUROPE Jun-05 Dec-04 Jun-04

ScandinaviaDenmark Canal Digital NA 127,000 NAFinland Canal Digital NA 54,000 NANorway Canal Digital NA 712,000 NASweden Canal Digital NA 585,000 NATotal Canal Digital 853,000 824,000 782,000Viasat 519,000 475,000 436,000France CanalSat 3,200,000 2,990,000 2,800,000TPS 1,352,000 1,354,244 1,270,000AB Sat NA 65,000 NAGermany Premiere 3,313,140 3,247,172 2,893,405Italy Sky Italia 3,300,000 3,100,000 2,700,000Netherlands Canal Digitaal 550,000 525,000 500,000Portugal TV Cabo Sat 378,000 350,000 315,000Spain Digital+ 1,776,000 1,652,573 1,815,000Turkey Digiturk NA 868,000 NAUK Sky Digital 7,787,000 7,609,000 7,355,000Sky+ 888,000 642,000 397,000Multiroom 645,000 473,000 293,000Ireland 363,000 347,000 332,000EASTERN EUROPEBulgaria Bulsatcom NA NA NAHungary UPC Direct 150,000 140,400 121,800Czech Republic UPC Direct 91,000 90,100 75,200Poland Cyfrowy Polsat 500,000 450,000 400,000Cyfra+ 700,000 650,000 650,000Romania FocusSat NA NA NADigital TV Group NA NA NAMax TV NA NA NASlovakia UPC Direct 15,000 14,600 12,200Baltic Viasat 24,000 15,000 2,000

Source: Company Data/New Television Insider Research

multichannel player. It either ownsor controls 10 top-tier stations, in 7markets, and has recently launcheda clutch of music channels rivallingMTV. Revenue has grown steadily,from •510m in 2002, to almost •700mlast year and its share price reflectsthat performance, and a reversal ofthe collapse of a few years agowhen media stocks suffered duringthe dot-com fall out.

The buyout firms said theywere attracted to SBS because of itsgrowth potential. “The key pointhere being that central and easternEurope and Scandinavia haveabove-average growth prospectscompared to Europe,” said GotzMauser, a partner at Permira, notingthe faster economic growth in thoseregions as they race to catch upwith western Europe.

SBS has been quick to expandits reach to include multiplebroadcasting outlets, including payTV and interactive services overmobile phones and video ondemand. The proceeds of the salewill be distributed to shareholdersin November. They will receiveabout •46, or $56, per share, a 16%premium to where they were tradingon Aug. 12 before a report firstsurfaced about a possible sale ofthe company.

Both SBS and the equity firmssaid they are not interested inbreaking up the company and

Skyâ•™s HDTV set-top Box

22Back to Contents

September 2005 SATMAGAZINE.COM

COVER STORY

SM

selling channels to local rivals, a route some analysts havesuggested could fetch higher prices. “These stations worktogether,” said Harry Sloan, in an interview. “The morechannels that we’re buying programming for from Hollywood,the more buying power we have, and the more opportunitythere is to have the channels work together.” SBS once reliedalmost entirely on advertising revenue. Itis now about two-thirds ad-based, and infive years, CEO Markus Tellenbach said itshould be about half as the companybranches into new pay-based services.

SBS is not alone. Germany’sProSiebenSAT1 production unitSevenSenses has just applied to theregional media authorities in Berlin-Brandenburg for four pay-TV licences. Thechannels in question will be called Com-edy-Kanal, Lifestyle, Current Movies andClassic Movies and initially distributed viathe Kabel Deutschland digital platform.ProSiebenSAT1 plans to source revenuesfrom a combination of traditional advertis-ing, interactive value added services andcarriage fees in order to finance thechannels. The channels are part pf adiversification section headed by MarcusEnglert, and according to industry sourcesthe main aim is to strike a deal with KabelDeutschland.

The overall strategy is meanwhile toincreasingly diversify revenue andgenerate new income sources besidestraditional TV advertising. Only 7% ofProSiebenSAT1’s turnover was notgenerated from advertising in 2004, and thecompany would like to double the figureby 2007/8.

This is the trend. Broadcasters aremoving away from ad-supported ‘free toview’ television, and putting more empha-sis on pay television. Nobody yet sug-gests the major networks are dying – yet.But they are having to re-invent theircommercial models in order to survive.

23Back to Contents

September 2005 SATMAGAZINE.COM

FEATURE

US Programmers: Still FranchisingVia Satellite in Europe by Daniel Freyer

Eutelsat’s Hot Bird 1 satellite

With over 2641 million TVhomes, 75 million of whichare cable and over 51

million satellite DTH homes, it is easy tounderstand why Europe has attracted somany American broadcasters to ventureacross the pond. To put this in context,the US has 73 million cable subscribersand just over 26 million satellite homes. Inaddition to the size of the market, Europehas the appetite – Europeans are hugeconsumers of US content and have anappreciation for American programming.Many American broadcasters who havesuccessfully made the transatlantic hopwith multiple European channels includeTurner Networks, QVC, Bloomberg,Viacom’s MTV, VH1 and Nickelodeonnetworks, Discovery Networks, Playboy,and Hallmark Channel to name a few.Furthermore, as the costs of channeluplink and satellite distribution have fallenwith digital compression, the reducedbarriers to entry have allowed many newnetworks to launch in Europe in recentyears.

Open Skies and Local Skies

Unlike the US today, where aprogrammer needs to negotiate carriagewith an EchoStar (11.5 million subscribers)or DIRECTV (14.7 million subscribers) inorder to reach mainstream DTH viewers, inEurope it’s possible for a new channel tosimply lease uplink and satellite transmis-sion services and directly access asubstantial home viewer audience. Butit’s an audience spread across thirtycountries, each with its unique viewertastes, market and regulations. In addi-

tion, desirable satellite subscribers areaggregated in key countries on specificdomestic DTH platforms, or “bouquets”,like Sky (BSkyB) in the UK, Digital Plus inSpain, Sky Italia in Italy, France’s TPS andCanal Plus, and so on.

Hot Birds

Top satellite options for Pan Euro-pean signals are the Eutelsat Hot Bird fleetof co-located spacecraft at 13° East, andSES-Astra’s Astra fleet co-located at 19.2°East and 28.2° East. Both orbital loca-tions are geared to making it easy formillions of DTH antennas across Europeto receive hundreds of radio & TVchannels via a single rooftop dish.

Hot Bird at 13° East and EuroBird 1at 28.5° East reach 120 million homesacross Europe, North Africa and theMiddle East, boasting a community ofover 1500 TV and 800 Radio channels. For Europe alone, around 1500 TV and radio

services reached a measuredaudience of 68 millioncable homes and 45million DTH homes andmore than 2 million hotelrooms for 2004, accord-ing to the company.Launching a newchannel on this locationoffers access to 80% of cable and satellitehomes in Western,Central and EasternEurope, and 99% cablehead-end penetration2.

The Astra 19.2° East locationcombined with Astra (28.2° East location)offers an attractive reach of over 102.68million European cable and satellitehomes, or 82% penetration of that totalmarket. It hits 76% of satellite homes andaccesses 87% of cable subscribers.

A Who’s Who of American brandchannels can be found as digital primarydistribution signals at these orbitallocations. Numerous “primary” feedsignals are used by these programmers toreach Europe’s cable systems, as well asthe broadcast centers of national DTHbouquets like Canal Satellite and TPS inFrance, Sky Italia, Digital Plus and others.

For instance, Turner Networks’ CNNInternational is uplinked to Hot Bird-6 in adigital multiplex operated and uplinkedfrom outside of London by GlobeCast.This particular GlobeCast multiplex servicecarries the major European news channels,including CNN International’s Europe

24Back to Contents

September 2005 SATMAGAZINE.COM

FEATURES

feed, BBC World and Euronews reachingvirtually every cable headend in Europe.Bloomberg TV also uses Hot Bird-6,broadcasting a five-channel multiplex ofchannels for European cable and DTHplatforms while Viacom renewed itscontract earlier this year for uplink of allits European feeds on Hot Bird-6.

While they may be the best, Hot Birdat 13° East and Astra 19.2° East locationsare not the only distribution options. Forexample, Viacom, Inc, distributes the UKMTV and VH1 channels for the Skyplatform on its transponder on theAstra2A satellite at 28.2° East, also usinga GlobeCast uplink from London. In

addition, although Discovery Channelfeeds to European cable markets from itsplayout facilities in the UK, its cablesignals are uplinked by GlobeCast to theSirius-1 spacecraft, which offered lowerrates on transponders when it firstlaunched.

DTH Platforms: The UK is FirstPort of Call

With no language barrier and strongcultural ties, it’s perhaps not surprisingthat American TV fare has a strongfoothold in the UK. How strong? In arecent sample of UK TV channels trackedby BARB for an August 2005 week, a sub-

a substantial amount of non-BSkyB-owned channels were American brands( See Table 1). These “American”channels captured over 10% of total weekly viewing share, or the equivalent of 24% of the total cable and satellite-viewing share. As such, the UK’s SkyDTH is a key distribution platform formany American-brand channels.

The UK market is somewhat straight-forward in that there’s a single provider ofsatellite DTH services – BSkyB. The SkyDigital bouquet reaches 7.7 millionsubscribers and BSkyB aims to raise thisto 10 million by 2010. Many of thechannels on the Sky platform also havecarriage with the two UK cable operators

SATMAGAZINE.COM

25Back to Contents

September 2005

FEATURES

– NTL and Telewest – which have 4.5million subscribers between them. Inaddition, there is one Digital TerrestrialTelevision operator – Freeview – whichreaches 5 million homes. All channels onthe Sky platform are digitally encryptedfor reception only via Sky’s set topreceivers, including the Free-To-Airchannels in Sky’s basic package forsubscribers. All of the major NorthAmerican programmers in the UK are onthe Sky platform.

Becoming part of the Sky bouquetdoesn’t mean that as a channel you needto buy satellite capacity and uplink fromBSkyB. Programmers can choose from anumber of UK-based satellite and uplinkcompanies that offer digital services onthe Astra 28.2° and Eurobird 28.5° Eastsatellites.

The Astra 2A, 2B and 2D satellites co-located at 28.2° East formed the firstsatellite fleet used by Sky until four yearsago when the new Eutelsat Eurobirdsatellite was co-located at the same orbitalslot, providing more transponder capacityfor new Sky channels — all receivable bythe same DTH dishes. Transponderspace on Astra at 28.2° degrees East hadbeen very expensive but the launch ofEurobird opened the marketplace up byintroducing competition, new spaceinventory and more affordable rates.Soon a large number of new channels runby smaller companies joined the Skylineup.

However, being available on the satelliteis useless if viewers can’t find yourchannel. Broadcasters can arrange for alisting on the Sky Electronic ProgramGuide (EPG) as a separate transactionwith BSkyB, even if they are not beinguplinked by BSkyB. The Sky systemprovides an EPG listing for each channel,which is based on programming genrecategories, e.g. general entertainment,sports, specialist etc. EPG listings areregulated by the government, as is the

tariff for being listed. It runs at some£75,000 per year for Free-To-Airchannels. Pay-Per-View channels paymore, plus £1.50 per subscriber. Paychannels can either use Sky’ssubscription management and consumercall center for authorizations, activationsand billing, or they can outsource thatfunction to other companies, whotypically charge a per-subscriber monthlyfee for the service.

Satellite service providers can assist anew programmer in managing orfacilitating the technical arrangements fordelivery of EPG materials to the BSkyBorigination center.

For example, GlobeCast has been thecontractor of choice for a number ofchannels in the Sky package to provideuplink and space segment. In order toinclude the EPG data in its uplinkmultiplex at the GlobeCast Brookman’sPark Teleport, GlobeCast houses a SkyAdaptation Hub there that is remotely

operated by BSkyB. This system outputsa video program stream with the EPG andsubscription authorization informationadapted to a single transport stream,which feeds GlobeCast’s multiplex uplink

All broadcasters need a license from therelevant issuing authority, for exampleOfcom in the UK and CSA in France.

Licensing Issues

Broadcasters now also need to complywith European industry regulations. Inthe current political climate, newEuropean directives are compellingplayers in the broadcast arena to be morecautious of what is made available ontheir airwaves and authorities are morestrenuously enforcing existing legislation.Most satellite operators will no longercarry a channel that is not licensed asthey could now be subject to fines andcould even be considered an accompliceor accessory to

Discovery WingsDisney ChannelDisney PlayhouseDisney ToonsE! EntertainmentFox NewsFox KidsHallmarkHistory ChannelMTV ClassicMTV HitsMTV2MTVNational GeographicNickelodeon

Animal PlanetBravoBoomerangCartoon NetworkBiography ChannelBloomberg TVCNBCCNN InternationalDiscovery CivilizationsDiscovery HealthDiscovery Home & LeisureDiscovery KidsDiscovery ScienceDiscovery Real TimeDiscovery Travel & Adventure

Table no. 1Selected American Channels in Europe

UK Satellite Channels

Nick JuniorNick ToonsNickelodeonNick ToonsParamount ComedyParamount 2Playboy TVQVCSci Fi ChannelThe BoxThe Golf ChannelThe Travel ChannelTurner Classic MoviesVH1, VH2, Classic

26Back to Contents

September 2005 SATMAGAZINE.COM

FEATURES

a programmer’s actions whose contentwas deemed illegal or criminal. Therefore,appropriate licenses must now be ob-tained to launch operations in Europe andbroadcast service providers with expertiseon regional legislation can help navigatethis otherwise daunting and unfamiliarpath.

The good news is that a licensegranted by any country within theEuropean Union is valid for all the membercountries, as well as all associated statesand it is not necessary to apply forindividual licenses in every country wherethe programming will be broadcast.

While they cannot provide legalcounsel, some broadcast transmissionservice providers, like GlobeCast, canexplain the rules and provide an outline ofthe steps that need to be taken to complywith current regulations – everything fromwhere to apply, to submission procedures,to license renewals. In fact, legal counselis rarely necessary at all as the regulatoryauthorities generally insist on having arelationship directly with the broadcastersand will often not enter into a discussionwith a third party. Some local authoritieshave even taken measures to improvetheir user-friendliness for Americancompanies by adding English-speakingstaff.

Applying for a License

The application must either besubmitted in the country where thebroadcaster maintains its flagship Euro-pean office (i.e. where decisions are madewith regard to editorial content and wheretop regional management is based), or inthe country where the satellite operator isregistered. The four major satelliteoperators in Europe are Astra (Luxem-bourg); Eutelsat (France); Hispasat(Spain); and NSS (Netherlands).

In France, and a number of other

countries, there is no fee for a license andwhere payment is required the cost istypically nominal. Information requiredfor the application usually includes theapplicant company’s bylaws and adescription of its content.

Since it can take up to two months

for an application to be approved, it iswise to apply for a license in the earlyplanning stages. Depending on the natureof the channel, the process can be fasterbut uplinking can not take place without avalid license.

Once the license is approved it is

SATMAGAZINE.COM

27Back to Contents

September 2005

FEATURES

is valid for a term of five years atthe end of which an application forrenewal must be submitted.Renewal is usually a rather swiftprocess requiring no more than anupdated programming schedule.

When in Roma….

Negotiation of local DTH carriageterms, fees, EPG placement andtechnical integration to meet therequirements of a specific DTHbouquet can be complex, time-consuming and perplexing for aUS-based business with limitedEuropean presence.Programmers should look for in-Europe satellite transmissionpartners that offer in-countryoffices, with strong local contactsand experience to facilitatenegotiations for distribution onspecific DTH bouquets andplatforms in the UK, Spain, Italy,France, Germany and elsewhere,depending on the programmer’starget markets.

This edge gained by working withthe right satellite service providerswho offer experience, marketconnections and relationships canbe a big benefit to your successfullaunch and distribution in Europe.

Setting up Shop

For American programmersconsidering European channelexpansion, it’s obviously critical tounderstand unique viewer tastes.What may work in the UK, withoutany language conversion, could befar from the mark in France. Withtransatlantic fiber rates between Londonor Paris, and New York or Los Angeles aslow as domestic US cross-country rates,US-based networks can cost-effectivelyoriginate European feeds in the US and

then deliver them via fiber to Europeanuplinks. This is the case for instance withLos Angeles-based E! Entertainment,which sends two feeds to Europe.European interstitials, time-delays and

spots can be inserted via remotelycontrolled or monitored automationsystems. As the European revenuestream builds, increased local presencemay be warranted.

Source: Lyngsat.com

SATMAGAZINE.COM

28Back to Contents

September 2005

Customizing Feeds with Advanced

Content Management

Using the latest in ingest, file storage,technologies, programmers can now evenremotely control their playlistmanagement, reducing the technical costof creating new channels “in-country”.For example, GlobeCast has introducedit’s Store & Broadcast ContentManagement Delivery System whichallows international channels to distributemultiple program streams with separatelanguage tracks and subtitling without thecost of creating and delivering sixseparate linear feeds. This new kind ofservice allows the programmer to controltransmission parameters, cue tones,associated subtitling, animated and fixedlogos, as well as audio streams, The resultis a central platform that reduces the cost,logistics and infrastructure associatedwith more traditional tape-basedorigination solutions.

The UK has been a popular place forAmericans to base initial Europeanoperations, with no language barriers,good infrastructure and a competitivemarket for satellite, uplink and playoutfacilities readily available in or aroundLondon. For example, Middle East Pay-TV operator Showtime has selectedGlobeCast to deliver a bouquet of 12leading Western television channels viaLondon to the DTH provider’s digitalplatform on Nilesat 102 covering the

Middle East and North Africa. Bloombergdecided to operate its own playout andorigination facilities in England, where itcreates unique channels for France, Italy,Germany and of course the UK.Bloomberg’s playout is fed to theGlobeCast uplink in London. Viacomuplinks its MTV networks from justoutside London, as do Discovery andTurner networks. Turner launched aFrench language version of children’schannel Boomerang on the French TPSpackage but, given its existing UKoperations, elected to originate the signalin the UK, relying on GlobeCast to fiberthe signal to Paris for uplink to its jointplatform with TPS on Hot Bird.

Obviously there are exceptions tolocating in the UK, whether forregulatory, programming-specific or otherbusiness reasons. A case in point isreligious programmer TrinityBroadcasting Network (TBN). For theIberian market, TBN has a feed on theSpanish DTH platform uplinked fromGlobeCast in Spain to a Hispasat

spacecraft multiplex. Meanwhile, TBNrelies on GlobeCast to uplink its SkyDigital signal for the UK on Eurobird.GlobeCast also operates a digital multiplexfor TBN on Hot Bird for Europeandistribution of six channels.

Regardless of where operations arebased, Europe offers opportunities – notonly for subscription and pay channeldistribution but also in emerging revenueopportunities like interactive services.Although satellite distribution andtechnical infrastructure decisions do playa part in a channel’s success,programming to meet the needs ofspecific European viewer and marketsegments is obviously the critical successfactor. To help focus your resources onprogramming and marketing, Americanprogrammers planning European channelscan look for satellite service providerswho offer proven technical expertise,“one-stop-shopping” for prime Europeanand international satellite and uplink andfiber facilities, and service quality trackrecords. In-country contacts andexpertise, and the ability to help gain DTHplatform carriage in Europe should beoffered and available. Customer servicein both the US and Europe, anunderstanding of both the Europeanenvironment and your business“Stateside”, and facilities and assets tolink the two should be the standard youexpect in satellite service providers tohelp make your channel a success.

Notes:1 Eutelsat market study source2www.eutelsat.com/news/media_library/brochures/Facts_&Figures.pdf3:based on data from SES-Astra website.www.ses-astra.com/corporate/market-research/covmarket.shtml

Control Room monitoringsatellite packages overEurope with AmericanProgramming(Photo Courtesy ofGlobeCast)

Dan Freyer is Director of Marketing in America for GlobeCast, aglobal leader in satellite transmission services for professionalbroadcast, enterprise multimedia and Internet content delivery. He hashelped leading satellite companies like Intelsat, PanAmSat, Hughesand TRW grow their revenues and markets since 1989 in various sales,marketing and business development management positions. He hashelped numerous cable, broadcast, Internet and VSAT users deploysatellite networks in the US and overseas. He is President of theSociety of Satellite Professionals International in California and can be reached [email protected]

SM

29Back to Contents

September 2005 SATMAGAZINE.COM

FEATURE

For the first time on a global scale thedigital home is becoming a reality.Consumers are experiencing the

wide diffusion of Internet appliances, aswell as domestic multimedia peripherals(typically digital camcorders, cameras andmusic players such as the iPOD™). As theTV ecosystem switches towards thedigital age, this combination sets thefoundation for the upcoming PC-TVconvergence. In addition to this globaltrend, this year TV over IP will grow to thematurity stage, thus preparing thegroundwork for massive deployment.

First we will highlight the mainadvantages of the integrated digital TVsets. With more than one million unitsalready in use in Great Britain, of whichhalf of them were sold at the end of 2004,the innovative concept of IntegratedDigital TV ( iDTV) follows a growingpublic interest in the technology.

Sony just announced that all TV’sbigger than 26 inches, will be digital.Moreover, because it is also capable toreceive the analog over-the-air channels in