bac2664 audit planning

TRANSCRIPT

TRIMESTER II, 2015/2016 SESSION

BAC 2664 Auditing

Report:

Audit Planning for PN-17 Company

Study Case: Petrol One Resources Bhd.

Competitor: Carimin Petroleum Bhd.

Prepared by: Ana Ululiyatul Al-bab 1132702479

Lee Sin Yee 1141326955

Leong Jun Rong 1121115871

Submission Date: 1st of February 2016

Lecturer : Mdm. Sunita

Session : B01

ii

Table of Contents 1. Introduction ........................................................................................................................ 1

1.1 Background Information ............................................................................................. 1

1.2 Purpose of Audit Planning .......................................................................................... 1

1.3 Steps of Audit Planning............................................................................................... 2

1.4 Potential Client’s Profile ............................................................................................. 2

1.4.1 Potential Customer Due Diligence Procedure ..................................................... 2

1.4.2 About PN17 ......................................................................................................... 2

1.4.3 About Potential Client’s Company: Petrol One Resources Bhd. ......................... 3

1.5 Potential Client’s Competitor ...................................................................................... 5

1.6 Industry Insight: Trends, Problems and Challenges.................................................... 5

2. Accepting Client ................................................................................................................ 7

3. Understanding Client’s Business Risk ............................................................................. 10

4. Performing Analytical Procedures ................................................................................... 11

4.1 Horizontal Analysis ................................................................................................... 11

4.2 Vertical Analysis ....................................................................................................... 14

4.3 Ratio Analysis of Petrol One Resources Berhad (PORB) and Carimin Petroleum

Berhad (CPB) ....................................................................................................................... 17

4.3.1 Profitability Ratios ............................................................................................. 17

4.3.2 Liquidity Ratio ................................................................................................... 20

4.3.3 Risk Ratio........................................................................................................... 21

4.4 Industry Analysis....................................................................................................... 23

4.5 Credit Analysis .......................................................................................................... 24

5. Setting Materiality and Assess Acceptable Audit Risk and Inherent Risk ...................... 24

5.1 Setting Materiality Level ........................................................................................... 24

5.2 Assessing Acceptable Audit Risk ............................................................................. 25

5.3 Assessing Inherent Risk ............................................................................................ 25

6. Internal Control ................................................................................................................ 26

iii

6.1 Control Environment ................................................................................................. 26

6.2 Information System and Communication ................................................................. 28

6.3 Monitoring ................................................................................................................. 28

6.4 Control Activities ...................................................................................................... 29

6.5 Other Control Activities ............................................................................................ 29

6.6 Corporate’s Structure ................................................................................................ 31

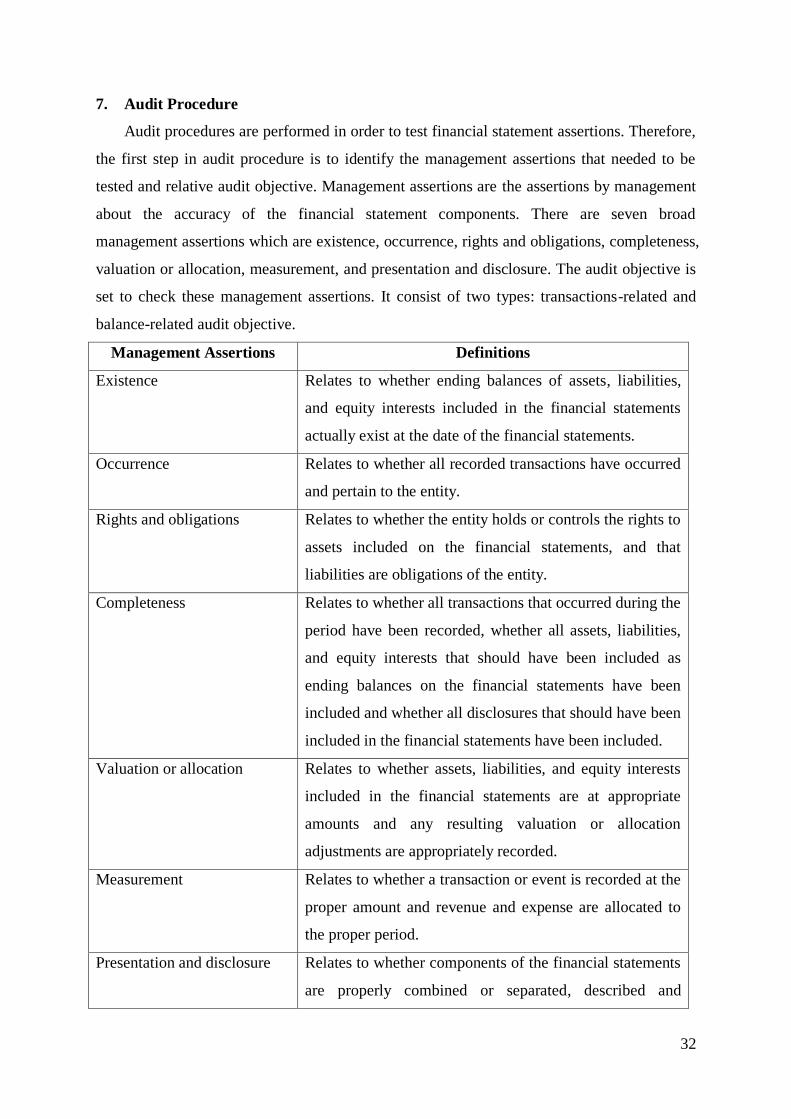

7. Audit Procedure ............................................................................................................... 32

7.1 Management Assertions for Liabilities and Owner’s Equity .................................... 33

7.2 Management Assertions for Sales and Cost of Sales ................................................ 34

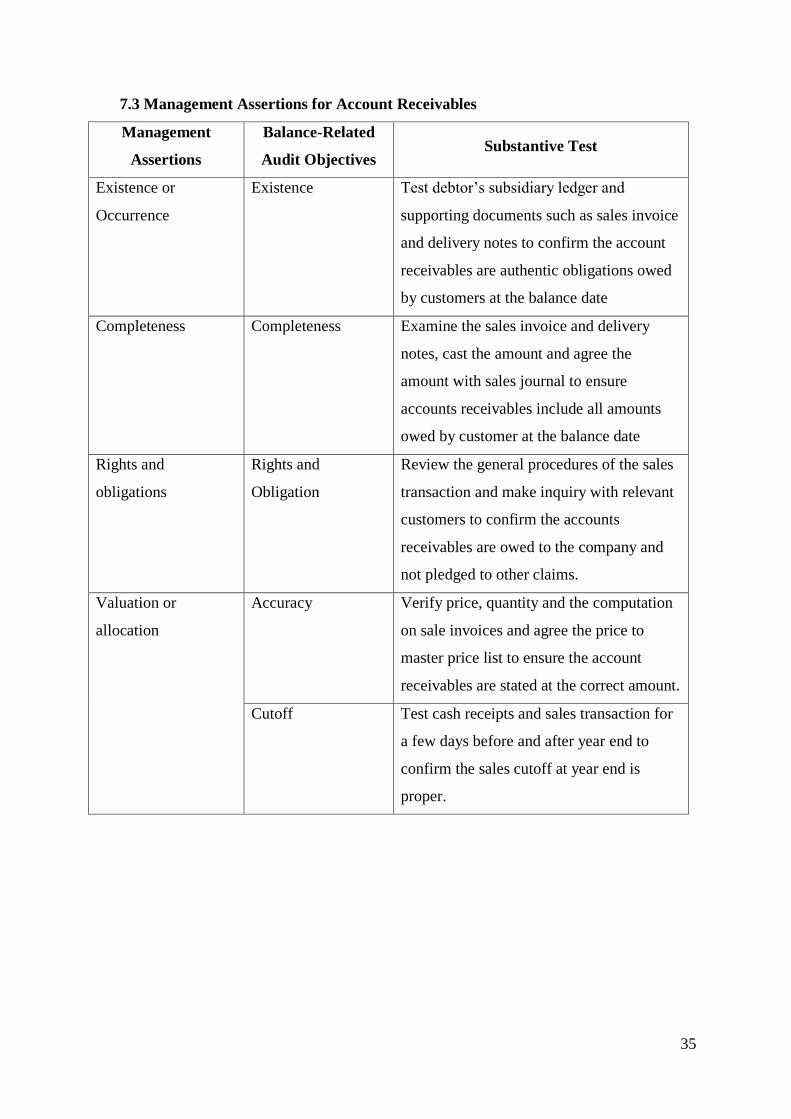

7.3 Management Assertions for Account Receivables.................................................... 35

8. Overall Audit Plan ........................................................................................................... 36

9. Conclusion ....................................................................................................................... 38

References ................................................................................................................................ 39

1

1. Introduction

1.1 Background Information

Since its introduction, the need for companies to be audited by an independent

external auditor has been a key element of confidence and trust in corporate world. It

builds the bridges to prevent agency problem, where different interests might arise

between the ones managing the company and those who own the company. It also

provides assurance that management has presented a ‘true and fair’ view of company’s

financial performance and position, hence the users would be able to fully rely on the

information provided to make an economical decision.

In general, an audit consists of evaluation of a subject matter with a view to express

an opinion on whether the subject matter is fairly presented (PwC, 2013). In order to do

so, ISA 300 states that a proper audit plan has to be made beforehand to ensure that the

overall audit process is efficiently conducted in reasonably low level of audit risk (Burke,

2016).

In this report, we will only focus on the planning stage of audit which is the first step

out of three to be conducted once the engagement with the client has been accepted.

1.2 Purpose of Audit Planning

The following are the purpose of creating an audit plan according to ISA 300 Para

A1-A3 (Alvin A. Arens, 2014):

It will enable the auditor to identify, obtain sufficient evidence and pay more

attention to important and risky areas of the audit.

It assists the auditor to identify and resolve potential problems effectively and

efficiently on a timely basis

It is useful in choosing the right engagement team members with appropriate

levels of capabilities and competence to respond to anticipated risks being

assessed and suitable job assignment to them.

It facilitates to direct, coordinate and supervise the engagement team members

and review their work.

It helps to keep audit costs to be paid by the client at a reasonable level, as

well as to avoid misunderstandings with the client.

2

1.3 Steps of Audit Planning

The following are the steps to be taken in planning an audit and designing an audit

approach, which also serves as guide for us to compose our own audit plan for this report.

You may refer to which section is referring to which step of our audit plan progress.

Accept client and perform initial audit planning: (2) and (1.4.1, 1.4.2, 1.4.3)

Understand the client’s business and industry: (1.5, 1.6)

Assess client business risk : (3)

Perform preliminary analytical procedures (4.1, 4.2, 4.3, 4.4, 4.5)

Set materiality level and assess acceptable audit risk and inherent risk (5.1,

5.2, 5.3)

Understand internal control and assess control risk (6.1, 6.2, 6.3, 6.4, 6.5, 6.6)

Gather information to assess fraud risks (5)

Develop overall audit plan and audit program (7 and 8)

(Alvin A. Arens, 2014)

1.4 Potential Client’s Profile

1.4.1 Potential Customer Due Diligence Procedure

As stated in IFAC’s Code of Ethics for Professional Accountants, we have to

investigate our potential client, its owners and business activities they conduct in order

to evaluate whether taking them in as the new client would expose us into integrity

issues which lead into unacceptable risk (ACCA, 2015). Normally known as ‘customer

due diligence’ procedures, we are performing this procedure towards Petrol One

Resources Bhd. as they approach us, so that we have a better understanding of what

they do.

1.4.2 About PN17

After exercising the due diligence procedure, we found out that Petrol One

Resources Bhd. is classified as PN 17 in Bursa Malaysia for the past 4 financial years.

PN 17 stands for Practice Note, and any listed company in the Malaysian Stock

Exchange that fall within PN17 normally face financial difficulties and poor

managements (Bursa Malaysia, 2015). The list itself serves as a warning to the potential

investors and stakeholders that the companies within the list are under scrutiny due to

their poor performance.

3

As of 29 December 2015, there are 17 companies listed in Malaysian Stock

Exchange classified as PN17. To be classified as one of the PN17 companies, the

company needs to meet at least one of these criteria as follow:

Shareholders' equity is 25% or less of the total paid-up capital and such

shareholders' equity is less than RM40 million;

Receivers or managers have been appointed to take control of at least 50% of

the total assets employed;

Winding up of a subsidiary or associate company;

The auditors have expressed adverse or disclaimer opinion to the company;

default in loan interest and principal repayments;

The companies have suspended or ceased their operations;

And companies do not have any significant businesses or operations.

(Bursa Malaysia, 2015)

The main reason why Petrol One Resources Bhd. is classified under PN17 is

because the result of the shareholders’ equity of the Group on a consolidated basis was

less than 25% of its issued and paid-up capital (excluding treasury shares) and it was

less than RM40,000,000 (Petrol One Resources Bhd, 2015). Additionally, it is being

listed as PN17 for the reason that the auditors, KPMG Malaysia, has issued three times

of disclaimer opinions for their financial statements for the year 2012-2014 (Yuan,

2015).

1.4.3 About Potential Client’s Company: Petrol One Resources Bhd.

As the result of our initial investigation about our prospective client, basically

Petrol One Resources Berhad is a Malaysia-based investment holding company.

Incorporated in 1995 and based in Kuala Lumpur, the company is engaged in the oil

and gas refining, and marketing industry. Through its subsidiaries, i.e Arus Dermaga

Sdn. Bhd., Petrol One Storage Sdn. Bhd., Petrol One Offshore Sdn. Bhd. and One

Petroleum Ltd; Petrol One Resources Bhd operates their businesses.

The company mainly operates in three major activities, which are: support

activities for mining, support activities for transportation, and warehousing and storage.

In general, they offer services in shipping and forwarding, floating storage and

offloading, offshore support services, bunker and ship management which are broken

down further in the figure 1 below.

4

In each major activities we have mentioned earlier, the company has different

strong competitors. In terms of doing support activities for mining, Kim Yuan Amang

Factory Sdn. Bhd is the closest competitors for Petrol One Resources. Meanwhile, Nyk

Line (Malaysia) Sdn. Bhd. is a fast growing and potential competitor for activities of

support activities for transportation, and Kic Oil Terminals Sdn. Bhd.is a strong

competitor for activities of warehousing and storage.

Having said that oil and gas is the lifeblood of Malaysia's economy and

accounted for approximately 30 percent of GDP, the company which is doing support

services and providing related equipment related to oil and gas is operating in relatively

competitive and mature market although the number of competitors have been

declining (Manac, 2015).

In terms of business partner, Petrol One Resources Bhd. has constantly done

business together with its two major customers, Coastal Oil Limited Private Limited

and Noble Clean Fuels Limited since they have signed fuel storage contract with Petrol

One eversince 2009.

Figure 1: The Product Line that Petrol One Resources Bhd. Offers (Petrol One Resources Bhd., 2011)

5

1.5 Potential Client’s Competitor

We have mentioned earlier that Kim Yuan Amang Factory Sdn. Bhd, Nyk Line

(Malaysia) Sdn. Bhd., and Kic Oil Terminals Sdn. Carimin Petroleum Berhad are among

the closest and strongest competitors for our potential client, Petrol One Resources Bhd.

However, due to the fact that none of the end-date of the fiscal year is the same with

Petrol One Resources Bhd., we have decided to choose other company as the comparison

for us to proceed with analytical procedures later on. Comparing companies with different

starting and ending date of fiscal year can distort the analysis. The time included may

vary and seasonal factors may become skewed. Additionally, the extra day in leap years

may distort comparisons too.

With that in mind, we choose Carimin Petroleum Berhad instead. Carimin Petroleum

Berhad is an investment holding company that has been established since 1989 and

headquartered in Kuala Lumpur, Malaysia. It principally involves in providing technical

support services in the offshore oil and gas industry in Malaysia. It mainly engages in the

provision oilfield inspections services, manpower, commissioning of onshore or offshore,

and quality assurance services and related contract works for Oil and Gas support

industry.

In terms of long-term business relationship, Carimin has established some good

relationship with top players in oil and gas industry, such as: Petronas, Carigali, Shell,

Murphy Oil, Talisman, Exxon Mobil, Nippon Oil, New Field, Petrofac, and Hess.

Furthermore, marine support services is one of the major activities of Carimin

Petroleum Berhad. This service involves of chartering and maintenance, offshore

transportation and support vessels which are similar to the major activities of offshore

support services offered by Petrol One Resources Berhad. Hence, Carimin Petroleum

Berhad is considered as a strong competitor to Petrol One Resources Berhad in this area.

1.6 Industry Insight: Trends, Problems and Challenges

Over the last few months, we have witnessed the series of economics events has been

hitting energy industry hard. With global economy turmoil i.e slower economic growth in

China and continuing financial distress in Europe resulting in weakening global energy

demand, oil price drops below $28 per barrel reaching its 12-year low (down more than

60% from their high in the Summer 2014) (Viren Doshi, 2016), and Iran recently being

lifted from the sanction enabling them to export more oil to the already oversupplied-

market; oil and gas industry has a wide range of challenges to face across its sectors in the

6

months to come, including in the downstream and oilfield services sectors which our

potential client is currently operating at.

While many analysts have been predicting that it is not going to get better anytime

soon, and the oil price is not expected to rebound until at least the end of 2016 (Ngai,

2016); the challenge for top managers and business leaders has prevailed. How are they

going to navigate their company in the oversupplied-market where the market outlook

hints that 2016 is going to be arduous? Especially in Malaysian market where our

prospective client has its operation, where it is evident that oil companies and

governments that rely on the price of crude oil for their living are in trouble. 30% of lay

off happened in 2015 alone is from oil and gas companies, amounting to nearly 2000

people losing their jobs (Sidhu, 2015).

Furthermore, as our prospective client – Petrol One Resources Bhd. is not only doing

oil refinery1 but also offering support services for other oil and gas companies; another

challenge that they are going to face is that their customers are expected to negotiate for

10 to 30 percent discounts from oil-field services that Petrol One provides in the attempt

to lower their operating cost, leading into potential reduction in revenues (Viren Doshi,

2016).

Additionally, the fact that a major concern about climate change is being raised, and

the effort to reduce CO2 emissions and minimize fossil fuels has been in the top priority

worldwide; being in the industry where it does otherwise sets another challenge for our

prospective client on how to successfully do business in oil and gas industry in an

increasingly carbon-constrained world.

1 Oil refinery refers to an industrial plant that refines crude oil into petroleum products such as diesel, gasoline

and heating oils (Investopedia, 2016)

7

2. Accepting Client

After thoroughly understand the nature of business, the way our prospective client run

their business, and the intended use of the statements as well as who are the likely users; we

have decided to accept Petrol One Resources Bhd. as our client, and sent an engagement

letter to define the professional and engagement relationship between our auditing firm and

our client. Enclosed in the following page is the copy of our audit engagement letter that we

sent to our client, Petrol One Resources Bhd.

We are appointing Ms. Lee Sin Yee as the main auditor for this engagement as to meet

the first general standard of the Generally Accepted Auditing Standards relating to adequate

technical training and proficiency. Considering that she is a Chartered Accountant with

previous experiences and adequate expertise in auditing oil and gas company, we believe that

she will be the best suit for the job.

8

Audit Engagement Letter

ANA, JR AND SY, CAs

CYBERJAYA, MALAYSIA

January 2, 2015

MR. LIM KIAN BOON, Executive Chairman

PETROL ONE RESOURCES BERHAD

Regus, Level 8, Tower 8, Avenue 5

The Horizon Phase 2,

59200 Kuala Lumpur Wilayah Persekutuan,

Malaysia.

DEAR MR. LIM KIAN BOON,

We are pleased to accept the instruction to act as auditor for your company of the

financial statement of PETROL ONE RESOURCES BERHAD for the year ending June 30,

2015. The purpose of this letter, together with the attached terms and conditions, is to clarify

our terms for carrying out the work and make our respective responsibilities clear. We are

bound by the ethical guidelines of accepted accounting standards, and accept instructions to

act for you on the basis that we will act in accordance with those ethical guidelines.

Our audit will be conducted in accordance of Auditing Standards which issued by the

Malaysian Institute of Accountants. Those standards require that we obtain reasonable, rather

than absolute, assurance that the financial statements are free of material misstatement,

whether caused by error or fraud. It will include such tests of transactions and of the

existence, ownership and valuation of assets and liabilities as we consider necessary. We also

shall obtain an understanding of the accounting systems and internal control systems in order

to assess their adequacy as a basis for the preparation of the accounts and to establish whether

proper books of accounts have been maintained. We shall expect to obtain such appropriate

evidence and explanation as we consider sufficient to enable us to draw reasonable

conclusions there from.

In addition, an audit is not designed to detect immaterial misstatements or violations of

laws or governmental regulations that do not have a direct and material effect on the financial

statements or major programs. Therefore, the audit will not necessarily detect misstatements

less than this materiality level that might exist because of error, fraudulent financial

9

reporting, or misappropriation of assets. If, for any reason, we are unable to complete the

audit or are unable to form or have not formed an opinion, we may decline to express an

opinion or decline to issue a report as a result of the engagement. However, if during the

course of our audit we become aware of such errors, fraud, or illegal acts, we will bring them

to your attention.

The financial statements are the responsibility of the company’s management.

Management is also responsibility for:

1. establishing and maintaining effective internal controls over financial report, and also

including monitoring on-going activities

2. responsible for making all financial records and related information available to us

3. responsible for the design and implementation of programs and controls to prevent

and detect fraud, and for informing us about all known or suspected fraud or illegal

acts affecting the government involving

4. Providing the conclusion of the engagement a representation letter that, among other

things, will confirm management’s responsibility for the preparation of the financial

statement in conformity with accounting principles generally accepted in Malaysia.

Our fees for all services are related to our standard hourly rates in effect at the time

services are performed. Our standard hourly rates vary according to the degree of

responsibility involved and the experience level of the personnel assigned to your engagement.

Our fee for this engagement will be RM 9000 from which 50% will be paid upon March 1,

2015 and other 50% upon June 1, 2015.

Once it has been agreed, this letter will remain effective, from one audit appointment to

another, until it is replaced arising from changes in audit scope or other circumstances. We

shall be grateful if you could confirm in writing your agreement to these terms by signing and

returning the enclosed copy of this letter, or let us know if they are not in accordance with

your understanding of our terms of engagement.

Accepted: Yours very truly:

By: Lee Sin Yee

Date : PARTNER

10

3. Understanding Client’s Business Risk

Each company will have to face a certain risk, but different industries will have to face a

different risk that maybe. The following is the biggest risks that oil and gas companies face:

Political risk, risk that an investment's returns could suffer as a result of political

changes or instability in a country. Instability affecting investment returns could stem

from a change in government, legislative bodies, other foreign policy makers, or

military control. For example, political decisions by governmental leaders about taxes,

currency valuation, trade tariffs or barriers, investment, wage levels, labor laws,

environmental regulations and development priorities, can affect the business

conditions and profitability. Similarly, non-economic factors can affect a business.

For example, political disruptions such as terrorism, riots, coups, civil wars,

international wars, and even political elections that may change the ruling government,

can dramatically affect businesses’ ability to operate.

Geological Risk refers to both the difficulty of extraction and the possibility that the

accessible reserves in any deposit will be smaller than estimated. For example,

exploration has moved on to areas that involve drilling in less friendly environments

like on a platform in the middle of an undulating ocean, they normally use the terms

"proven," "probable" and "possible" before reserve estimates, to express their level of

confidence in the findings. Because they have no proper ways and method to estimate

the resource.

Price risk is the primary risk and unavoidable. Basically, the higher the geological

barriers to easy extraction, the more price risk a given project faces. This is because

unconventional extraction usually costs more than a vertical drill down to a deposit.

This doesn't mean that oil and gas companies automatically mothball a project that

becomes unprofitable due to a price dip. Often, these projects can't be quickly shut

down and then restarted.

Supply and Demand Risks, a real risk for oil and gas companies. As mentioned,

operations take a lot of capital and time to get going, and they are not easy to mothball

when prices go south, or ramp up when they go north. The uneven nature of

production is part of what makes the price of oil and gas so volatile. Other economic

factors also play into this, as financial crises and macroeconomic factors can dry up

capital or otherwise affect the industry independently of the usual price risks.

11

Cost risk. Cost focuses on operational factors and an extraction project can

commonly exceed capital invested based on regulations, global production and

drilling in unfamiliar areas. A major risk is not being able to find qualified workers

due to many who are retiring which also add to the increasing operational cost. A risk

for companies is also dealing with stakeholders who feel like they can cut cost and

still have healthy growth while incurring more costs through spending on new

technology for a more efficient extraction.

4. Performing Analytical Procedures

Following ISA 520, we are conducting analytical procedures in our planning stage to

assist us in gaining better understanding of the client’s business and in assessing client’s

business risk. We might not be aware of that risk, but performing analytical procedures will

assist us in finding any unusual or unexpected relationships that may highlight where the

risks exist. In order for us to do so, we will perform 5 sets of analysis: horizontal analysis,

vertical analysis, ratio analysis, and industry analysis, and credit analysis.

4.1 Horizontal Analysis

Horizontal analysis is the comparison of historical financial information within the

company over a series of reporting periods (Accounting Tools, 2016). We are using this

method on their income statement as well as balance sheet for the year 2014 and 2015. By

doing so, we would like to see if any numbers are unusually high or low within the period

of time, which may then can be our base to conduct a further and detailed investigation

pertaining the area with the highlighted risks.

PETROL ONE RESOURCES BERHAD

Comparative Income Statement

For Years Ended 30 June, 2014 and 2015

2015

2014

Increase or Decrease

(RM'000)

(RM'000)

Amount Percent(%)

Net Sales

11811

5404

6407 119%

Other Revenues

165

1027

(862) -84%

Total Revenues

11976

6431

5545 86%

Costs of Goods &

Services / Total

Expenses

(4909)

(522)

(4387) -840%

Operating Income

7067

5909

1158 20%

12

Selling, general &

administrative costs

(3385)

(7125)

3740 52%

Earnings Before Interest,

Tax & Depreciation

3682

(1216)

4898 403%

Total Depreciation, Depletion &

Amortization

(343) (303)

(40) -13%

Earnings Before Interest

& Tax

3339

(1519)

4858 320%

Interest Expense

(2199)

(4226)

2027 48%

Other Financial Income

& Expenses

3333

(236)

3569 1512%

Earnings Before Tax

4473

(5981)

10454 175%

Income Taxes

(19)

4

(23) -575%

Net Profit

4454

(5977)

10431 175% The figures of income statements are extracted from Petrol One Resources Sdn Bhd Annual Report: 2014 and 2015

The overall trend in 2015 has shown a significant increase and improvement from the

previous year, including the rise in the revenue as well as the net profit. However, we have

found out that there are areas with unusually high change which we believe we need to

investigate further as it might contain the risk of misstatement or the existence of fraud.

In cost of sales part, it drops by -840% for the year 2015 while the revenue increased

by 86%. Normally cost of sales has a positive correlation with the increase in the revenue.

The increase in the efficiency might happen which could lead to reduce the cost, but we

find it odd enough that the reduction reach the percentage above 800%.

PETROL ONE RESOURCES BERHAD

Comparative Balance Sheet

30 June, 2014 and 2015

2015

2014

Increase or decrease

(RM'000)

(RM'000)

Amount Percent(%)

Assets

Non-current assets

Plant and equipment

3,169

3,106

63 2%

Current assets

Cash & Bank

80.00

24.00

56 233%

Accounts Receivable

8,371

2,897

5474 189%

Prepayments & Advances

0

340

(340) -100%

Other Current Assets

1,246

1,022

224 22%

13

Total Assets

12,866

7,389

5477 74%

Liabilities

Non-current liabilities

Loans and borrowings

126

136

(10) -7%

Current liabilities

Loans and borrowings

52,215

48,569

3646 8%

Trade and other payables

59,377

48,426

10951 23%

Provision for taxation

40

20

20 100%

Total liabilities

111,758

97,151

14607 15%

Equity

Share capital

50,805

50,805

0 0%

Share premium

12,669

12,669

0 0%

Reserves

(162,366)

(153,236)

(9130) -6%

Total equity

(98,892)

(89,762)

(9130) -10%

Total equity and liabilities

12,866

7,389

5477 74%

The figures of balance sheet are extracted from Petrol One Resources Sdn Bhd Annual Report: 2014 and 2015

The overall trend of the balance sheet comparison for the year 2014 to 2015 shows

some unusual figures and changes which we believe we need to investigate further as it

might contain the risk of misstatement or the existence of fraud.

First of all, despite the issue that the company has issues in settling their debt

obligation for the year 2014 (Lynn, 2014), the company was still taking more short term

loans and borrowings to cover their operations for the year 2015. It poses the risk in the

going concern of the company.

Secondly, a sudden rise of 189% in account receivables put a question into how

effective their credit collection policy is. There is also a risk of misstatements in this area

which we need to investigate further to figure out how it correlates with the sales.

Thirdly, we noticed that there is a negative equity in both reporting years and it

increased too. As a measure, shareholder equity reveals what the owners of a company

(stockholders) would be left with if all assets were sold and all debts were paid, as asset –

liabilities = stockholders equity. In the case it shows a negative answer, theoretically the

stockholders would owe money, although the structure of publicly listed corporations like

Petrol One Resources Bhd. would prevents common stockholders from facing actual

liability. While knowing that it is already negative for the year 2014, we believe that it is

probable that the risk of mismanagement or even fraud exist when the company decided to

14

further leverage its borrowing and causes even higher negative equity, instead of trying to

improve it.

Fourthly, we have came to know that there is a substantial increase in cash and bank

amounting 223% that came into our attention. We need to further investigate to figure out

how this happened and where is the source of the money came from.

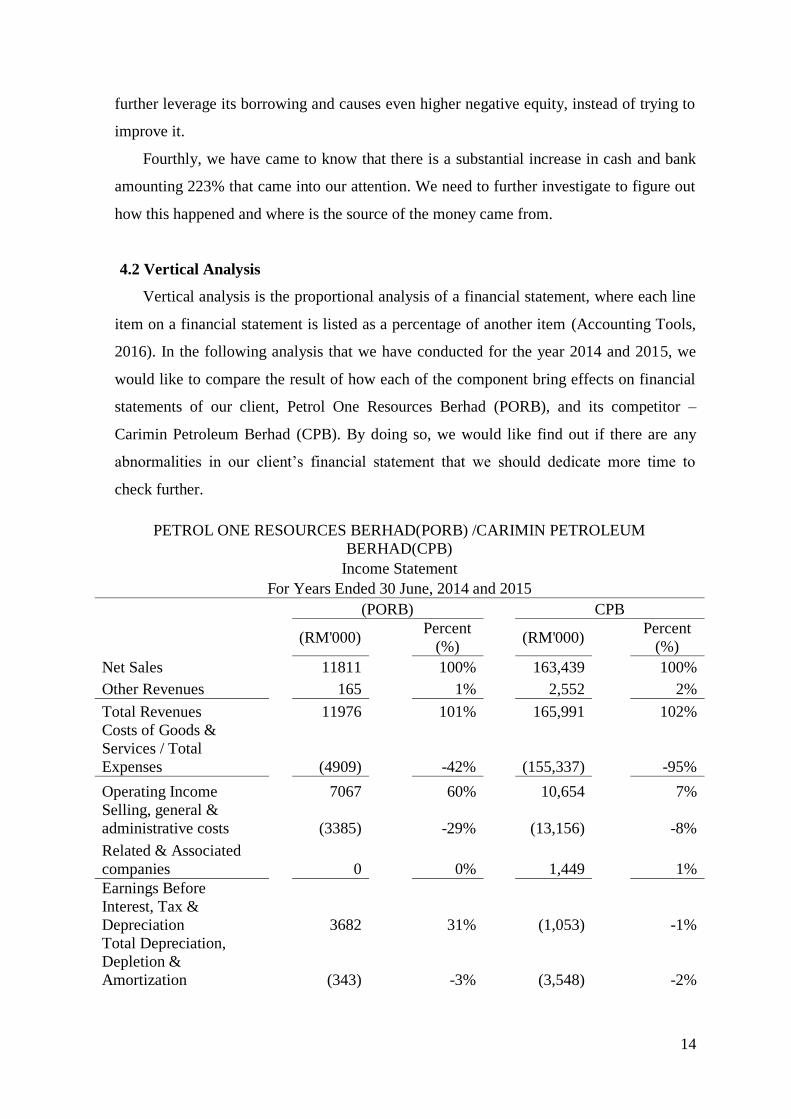

4.2 Vertical Analysis

Vertical analysis is the proportional analysis of a financial statement, where each line

item on a financial statement is listed as a percentage of another item (Accounting Tools,

2016). In the following analysis that we have conducted for the year 2014 and 2015, we

would like to compare the result of how each of the component bring effects on financial

statements of our client, Petrol One Resources Berhad (PORB), and its competitor –

Carimin Petroleum Berhad (CPB). By doing so, we would like find out if there are any

abnormalities in our client’s financial statement that we should dedicate more time to

check further.

PETROL ONE RESOURCES BERHAD(PORB) /CARIMIN PETROLEUM

BERHAD(CPB)

Income Statement

For Years Ended 30 June, 2014 and 2015

(PORB)

CPB

(RM'000)

Percent

(%) (RM'000)

Percent

(%)

Net Sales

11811

100%

163,439

100%

Other Revenues

165

1%

2,552

2%

Total Revenues

11976

101%

165,991

102%

Costs of Goods &

Services / Total

Expenses

(4909)

-42%

(155,337)

-95%

Operating Income

7067

60%

10,654

7%

Selling, general &

administrative costs

(3385)

-29%

(13,156)

-8%

Related & Associated

companies

0

0%

1,449

1%

Earnings Before

Interest, Tax &

Depreciation

3682

31%

(1,053)

-1%

Total Depreciation,

Depletion &

Amortization

(343)

-3%

(3,548)

-2%

15

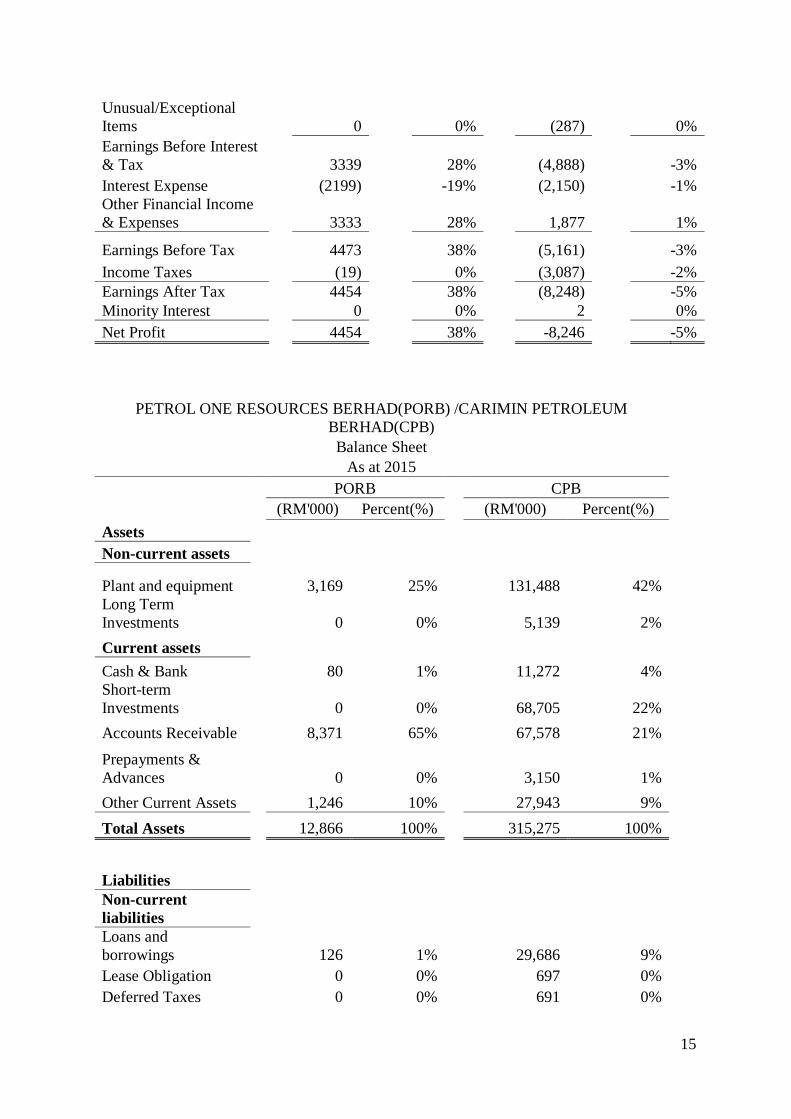

Unusual/Exceptional

Items

0

0%

(287)

0%

Earnings Before Interest

& Tax

3339

28%

(4,888)

-3%

Interest Expense

(2199)

-19%

(2,150)

-1%

Other Financial Income

& Expenses

3333

28%

1,877

1%

Earnings Before Tax

4473

38%

(5,161)

-3%

Income Taxes

(19)

0%

(3,087)

-2%

Earnings After Tax

4454

38%

(8,248)

-5%

Minority Interest

0

0%

2

0%

Net Profit

4454

38%

-8,246

-5%

PETROL ONE RESOURCES BERHAD(PORB) /CARIMIN PETROLEUM

BERHAD(CPB)

Balance Sheet

As at 2015

PORB

CPB

(RM'000) Percent(%)

(RM'000) Percent(%)

Assets

Non-current assets

Plant and equipment

3,169 25%

131,488 42%

Long Term

Investments

0 0%

5,139 2%

Current assets

Cash & Bank

80 1%

11,272 4%

Short-term

Investments

0 0%

68,705 22%

Accounts Receivable

8,371 65%

67,578 21%

Prepayments &

Advances

0 0%

3,150 1%

Other Current Assets

1,246 10%

27,943 9%

Total Assets

12,866 100%

315,275 100%

Liabilities

Non-current

liabilities

Loans and

borrowings

126 1%

29,686 9%

Lease Obligation

0 0%

697 0%

Deferred Taxes

0 0%

691 0%

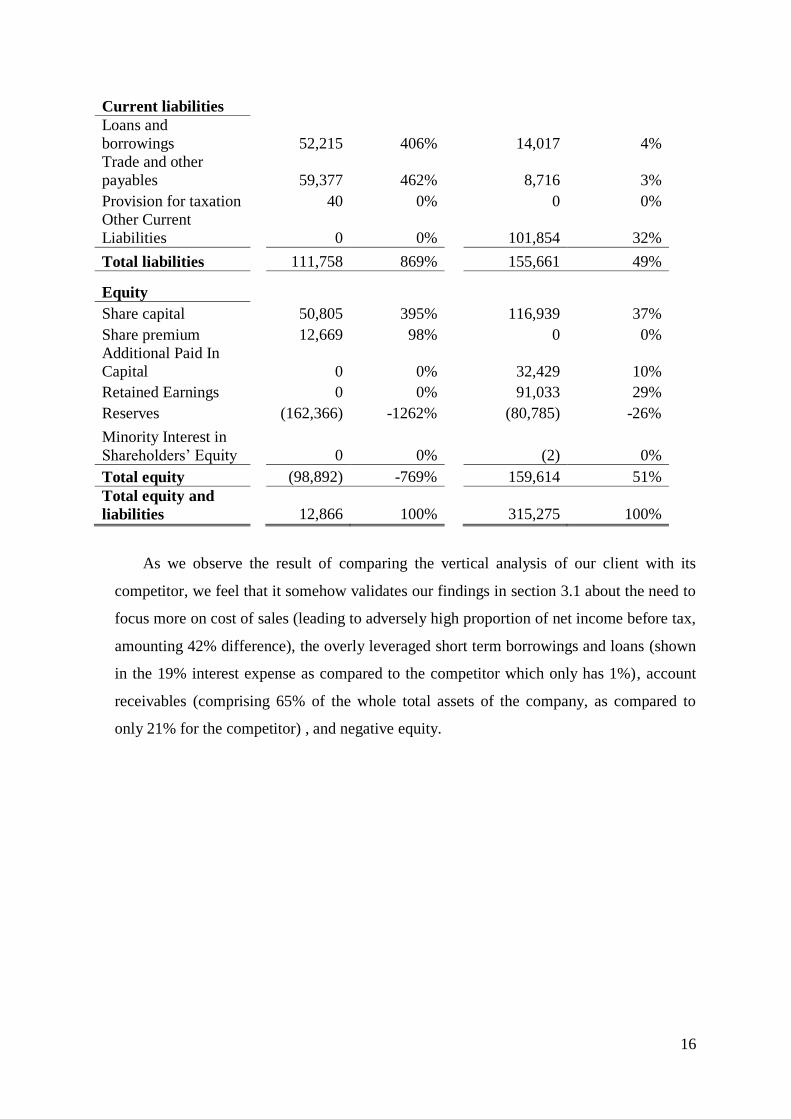

16

Current liabilities

Loans and

borrowings

52,215 406%

14,017 4%

Trade and other

payables

59,377 462%

8,716 3%

Provision for taxation

40 0%

0 0%

Other Current

Liabilities

0 0%

101,854 32%

Total liabilities

111,758 869%

155,661 49%

Equity

Share capital

50,805 395%

116,939 37%

Share premium

12,669 98%

0 0%

Additional Paid In

Capital

0 0%

32,429 10%

Retained Earnings

0 0%

91,033 29%

Reserves

(162,366) -1262%

(80,785) -26%

Minority Interest in

Shareholders’ Equity

0 0%

(2) 0%

Total equity

(98,892) -769%

159,614 51%

Total equity and

liabilities

12,866 100%

315,275 100%

As we observe the result of comparing the vertical analysis of our client with its

competitor, we feel that it somehow validates our findings in section 3.1 about the need to

focus more on cost of sales (leading to adversely high proportion of net income before tax,

amounting 42% difference), the overly leveraged short term borrowings and loans (shown

in the 19% interest expense as compared to the competitor which only has 1%), account

receivables (comprising 65% of the whole total assets of the company, as compared to

only 21% for the competitor) , and negative equity.

17

4.3 Ratio Analysis of Petrol One Resources Berhad (PORB) and Carimin Petroleum Berhad (CPB)

4.3.1 Profitability Ratios

Gross profit percentage = 𝐺𝑅𝑂𝑆𝑆 𝑃𝑅𝑂𝐹𝐼𝑇

𝑆𝐴𝐿𝐸𝑆 𝑅𝐸𝑉𝑈𝑁𝑈𝐸 𝑥 100

Net profit percentage = 𝑂𝑃𝐸𝑅𝐴𝑇𝐼𝑁𝐺 𝑃𝑅𝑂𝐹𝐼𝑇

𝑆𝐴𝐿𝐸𝑆 𝑅𝐸𝑉𝑈𝑁𝑈𝐸 𝑥 100

Year (PORB) (CPB) Comments

2014 4,578,996

5,404,077 x 100 =84.73 %

44,108

245,575 𝑥 100 = 17.96%

A high gross profit margin is an indication that PORB is in good financial health, although there is a substantial reduction

in the ratio for the year 2015 that we need to find the reason

why. It means that it has more than enough money left from

revenues after accounting for the cost of goods sold.

However, as we compared to the competitor, CPB, it has significant difference which makes it probable that the risk of

misstatement, sales errors or fraud within PORB exist.

2015 6,588,554

11,810,645 x 100 = 55.78 %

4,616

163,439 𝑥 100 = 2.82%

Year (PORB) (CPB) Comments

2014 5909

6431 x 100 = 91.88%

47,710

245,575 x 100 = 19.43%

Reasonably good cost control has been maintained by PORB despite the substantial decrease in sales for the year 2015.

On the other hand, it has a substantial difference as we

compared the ratio with the CPB as the competitor. The high

gap between the two makes it probable that there is a risk of

misstatement in cost of sales, sales cost errors, missing

transaction unrecorded, understatement of cost or even fraud

within PORB. To test this, it is worth comparing the

commercial and administrative costs to sales.

2015 7067

11,976 x 100 = 59.01 %

10,654

163,439 𝑥 100 = 6.52 %

18

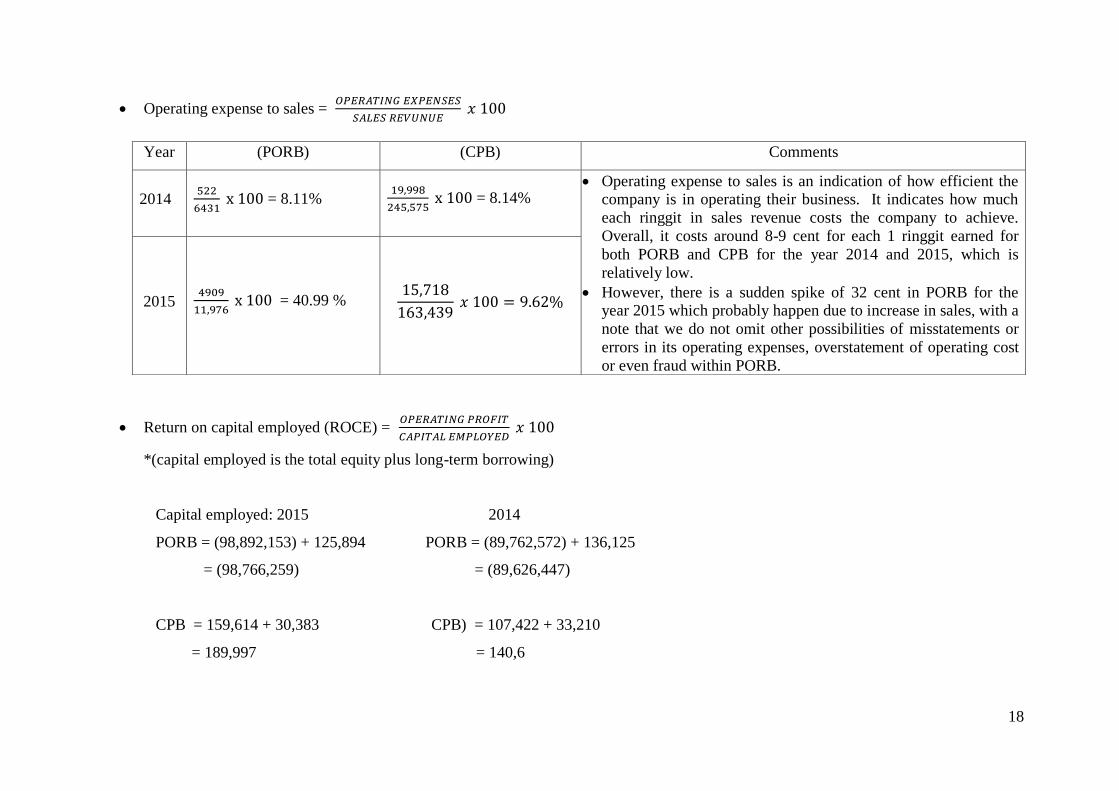

Operating expense to sales = 𝑂𝑃𝐸𝑅𝐴𝑇𝐼𝑁𝐺 𝐸𝑋𝑃𝐸𝑁𝑆𝐸𝑆

𝑆𝐴𝐿𝐸𝑆 𝑅𝐸𝑉𝑈𝑁𝑈𝐸 𝑥 100

Return on capital employed (ROCE) = 𝑂𝑃𝐸𝑅𝐴𝑇𝐼𝑁𝐺 𝑃𝑅𝑂𝐹𝐼𝑇

𝐶𝐴𝑃𝐼𝑇𝐴𝐿 𝐸𝑀𝑃𝐿𝑂𝑌𝐸𝐷 𝑥 100

*(capital employed is the total equity plus long-term borrowing)

Capital employed: 2015 2014

PORB = (98,892,153) + 125,894 PORB = (89,762,572) + 136,125

= (98,766,259) = (89,626,447)

CPB = 159,614 + 30,383 CPB) = 107,422 + 33,210

= 189,997 = 140,6

Year (PORB) (CPB) Comments

2014 522

6431 x 100 = 8.11%

19,998

245,575 x 100 = 8.14%

Operating expense to sales is an indication of how efficient the company is in operating their business. It indicates how much

each ringgit in sales revenue costs the company to achieve.

Overall, it costs around 8-9 cent for each 1 ringgit earned for

both PORB and CPB for the year 2014 and 2015, which is

relatively low.

However, there is a sudden spike of 32 cent in PORB for the year 2015 which probably happen due to increase in sales, with a

note that we do not omit other possibilities of misstatements or

errors in its operating expenses, overstatement of operating cost

or even fraud within PORB.

2015 4909

11,976 x 100 = 40.99 %

15,718

163,439 𝑥 100 = 9.62%

19

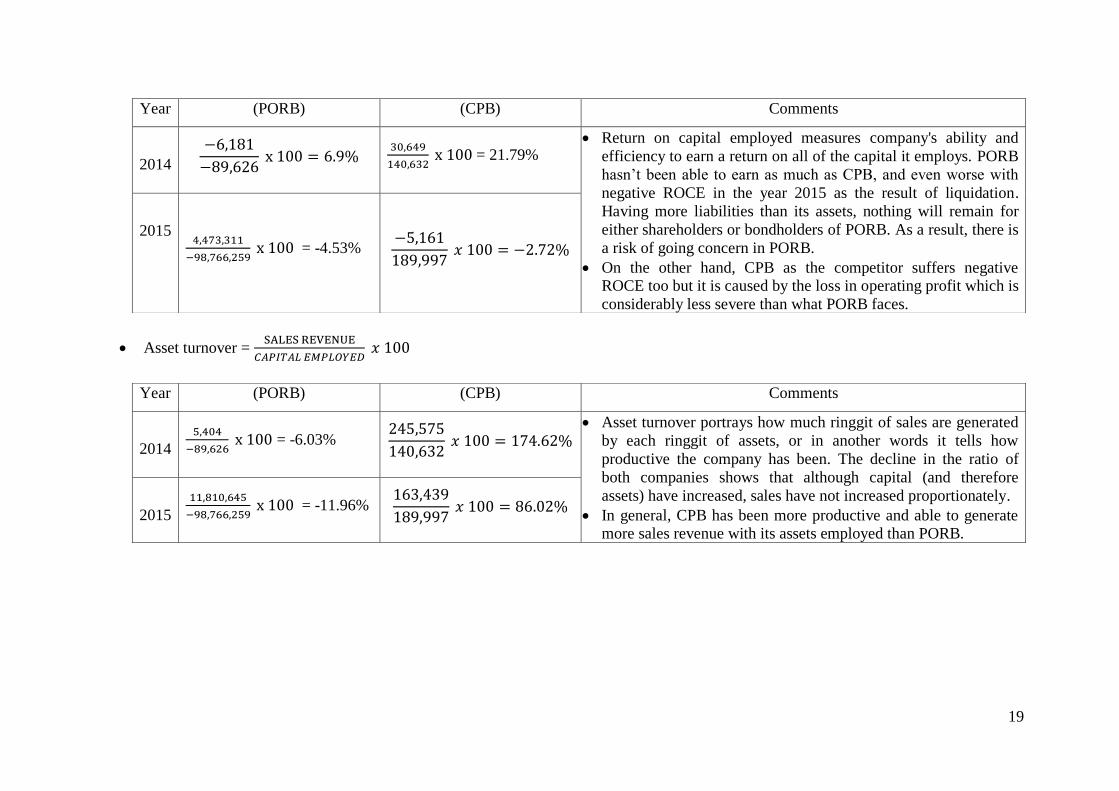

Asset turnover = SALES REVENUE

𝐶𝐴𝑃𝐼𝑇𝐴𝐿 𝐸𝑀𝑃𝐿𝑂𝑌𝐸𝐷 𝑥 100

Year (PORB) (CPB) Comments

2014

−6,181

−89,626 x 100 = 6.9%

30,649

140,632 x 100 = 21.79%

Return on capital employed measures company's ability and

efficiency to earn a return on all of the capital it employs. PORB

hasn’t been able to earn as much as CPB, and even worse with

negative ROCE in the year 2015 as the result of liquidation.

Having more liabilities than its assets, nothing will remain for

either shareholders or bondholders of PORB. As a result, there is

a risk of going concern in PORB.

On the other hand, CPB as the competitor suffers negative ROCE too but it is caused by the loss in operating profit which is

considerably less severe than what PORB faces.

2015 4,473,311

−98,766,259 x 100 = -4.53%

−5,161

189,997 𝑥 100 = −2.72%

Year (PORB) (CPB) Comments

2014

5,404

−89,626 x 100 = -6.03%

245,575

140,632 𝑥 100 = 174.62%

Asset turnover portrays how much ringgit of sales are generated

by each ringgit of assets, or in another words it tells how

productive the company has been. The decline in the ratio of

both companies shows that although capital (and therefore

assets) have increased, sales have not increased proportionately.

In general, CPB has been more productive and able to generate more sales revenue with its assets employed than PORB.

2015

11,810,645

−98,766,259 x 100 = -11.96%

163,439

189,997 𝑥 100 = 86.02%

20

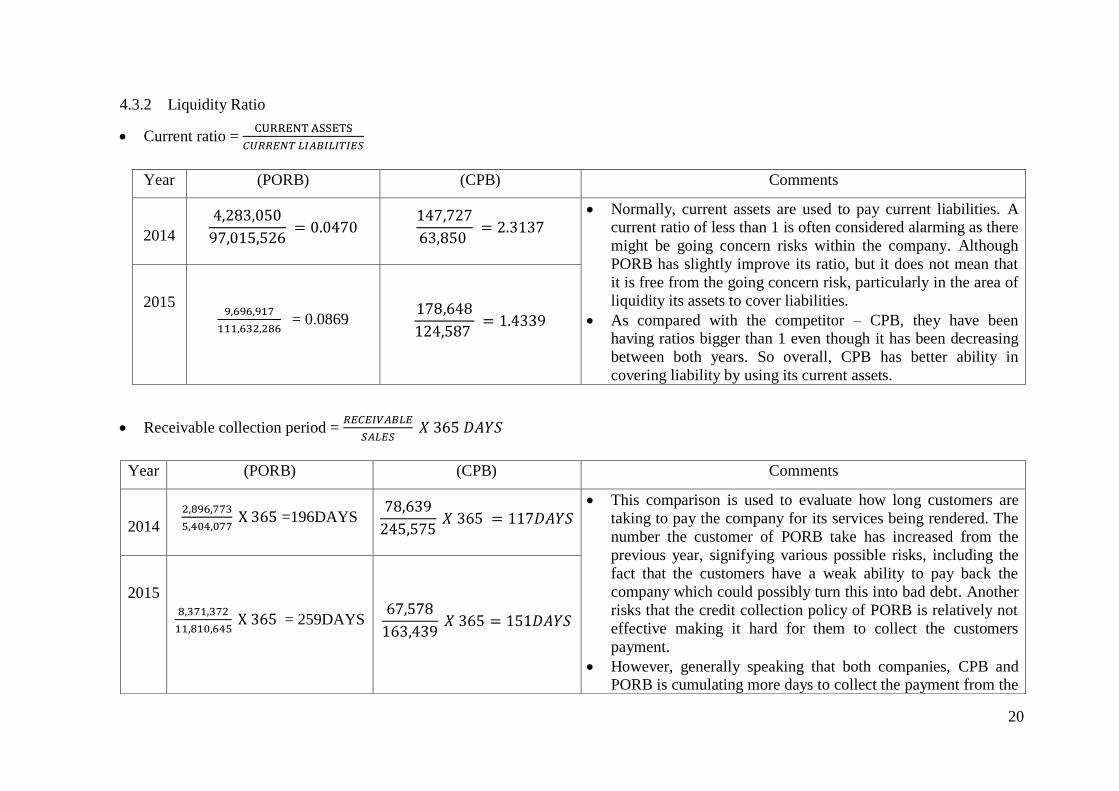

4.3.2 Liquidity Ratio

Current ratio = CURRENT ASSETS

𝐶𝑈𝑅𝑅𝐸𝑁𝑇 𝐿𝐼𝐴𝐵𝐼𝐿𝐼𝑇𝐼𝐸𝑆

Receivable collection period = 𝑅𝐸𝐶𝐸𝐼𝑉𝐴𝐵𝐿𝐸

𝑆𝐴𝐿𝐸𝑆 𝑋 365 𝐷𝐴𝑌𝑆

Year (PORB) (CPB) Comments

2014

4,283,050

97,015,526 = 0.0470

147,727

63,850 = 2.3137

Normally, current assets are used to pay current liabilities. A current ratio of less than 1 is often considered alarming as there

might be going concern risks within the company. Although

PORB has slightly improve its ratio, but it does not mean that

it is free from the going concern risk, particularly in the area of

liquidity its assets to cover liabilities.

As compared with the competitor – CPB, they have been having ratios bigger than 1 even though it has been decreasing

between both years. So overall, CPB has better ability in

covering liability by using its current assets.

2015 9,696,917

111,632,286 = 0.0869

178,648

124,587 = 1.4339

Year (PORB) (CPB) Comments

2014

2,896,773

5,404,077 X 365 =196DAYS

78,639

245,575 𝑋 365 = 117𝐷𝐴𝑌𝑆

This comparison is used to evaluate how long customers are

taking to pay the company for its services being rendered. The

number the customer of PORB take has increased from the

previous year, signifying various possible risks, including the

fact that the customers have a weak ability to pay back the

company which could possibly turn this into bad debt. Another

risks that the credit collection policy of PORB is relatively not

effective making it hard for them to collect the customers

payment.

However, generally speaking that both companies, CPB and PORB is cumulating more days to collect the payment from the

2015 8,371,372

11,810,645 X 365 = 259DAYS

67,578

163,439 𝑋 365 = 151𝐷𝐴𝑌𝑆

21

Payables Payment period = 𝐴𝐶𝐶𝑂𝑈𝑁𝑇 𝑃𝐴𝑌𝐴𝐵𝐿𝐸𝑆

𝐶𝑂𝑆𝑇 𝑂𝐹 𝑆𝐴𝐿𝐸𝑆 𝑋 365𝐷𝐴𝑌𝑆

4.3.3 Risk Ratio

The gearing ratio 𝐿𝑂𝑁𝐺 𝑇𝐸𝑅𝑀 𝐿𝑂𝐴𝑁 𝐹𝐼𝑁𝐴𝑁𝐶𝐸

𝐸𝑄𝑈𝐼𝑇𝑌 𝐹𝐼𝑁𝐴𝑁𝐶𝐸 𝑋 100%

customer, highlighting the fact that it could be collective problem that the whole industry is currently facing though

PORB has it worse than its competitor, CPB.

Year (PORB) (CPB) Comments

2014

9,962,688

825,081 𝑋 365

= 4407𝐷𝐴𝑌𝑆

11,778

201,467 𝑋 365 = 21𝐷𝐴𝑌𝑆

Payables payment period ratio tells how long it takes for company to pay its invoices from trade creditors, such as

suppliers and its business partners. In the previous fiscal years,

Petrol One and its subsidiary were unable to meet their loan

obligations since January 2011 and March 2010, respectively

(Lynn, 2014). So it does make sense that PORB was having a

huge number of days count to pay its payables as the

obligations from the previous fiscal years were carried forward.

However, they have shown a good improvement as PORB has

successfully reduced the days to 16% of previous year’s day

count.

On the other hand, its competitor, CPB has shown a constantly

healthy and reasonable period of payment in meeting its

obligation to pay its payables having it less than 30 days, as

compared with PORB which has a long way to go before it can

be considered healthy.

2015

10,897,955

5,252,091 X 365 =

757DAYS

8,716

158,823 𝑋 365 = 20𝐷𝐴𝑌𝑆

22

Interest cover = 𝑂𝑃𝐸𝑅𝐴𝑇𝐼𝑁𝐺 𝑃𝑅𝑂𝐹𝐼𝑇 𝐵𝐸𝐹𝑂𝑅𝐸 𝐼𝑁𝑇𝐸𝑅𝐸𝑆𝑇

𝐼𝑁𝑇𝐸𝑅𝐸𝑆𝑇

Year (PORB) (CPB) Comments

2014

136,125

(89,762,572) X 100 = −0.16%

33,210

107,422 𝑋 100 = 30.92%

The gearing ratio is defined in a way of comparing long-

term loan finance to total finance. As gearing ratio

decreases, so does the possibility of more interest can not

be paid. However, it is difficult to define a ‘safe’ level of

gearing. Reduction of gearing ratio would mean a greater

financial stability, and hence it is recommended for oil and

gas companies to keep it low as it is operating in volatile

market full of uncertainties. Yet, PORB has still long plan

to settle their equity finance problem.

As compared with CPB, both of the company has shown a slight improvement in its gearing ratio, reducing its

possibility of not being able to pay the interest of its loans.

2015

125,894

(98,892,153) X 100 = -0.13%

31,074

159,614 𝑋 100 = 19.47%

Year (PORB) (CPB) Comments

2014

(1,519)

4,266= −0.36

30,393

246 = 123.55

Interest cover shows how many times interest can be paid out of earnings. Neither

of these ratios would give cause for concern. The interest amounts would have to be

tested to see that they were reasonable, given interest rates and when the additional

borrowings were made. Besides that, because in the 2014, the company was making

loses so PORB was not able to pay its interest and hence it gets the negative figure.

However, as we compared with CPB as the competitor which has sudden drop in its ability to pay interest out of its earnings, it has significant difference which shows

that PORB was operating slightly well as compared to CPB.

2015 3,339

2,199 = 1.52

(4,888)

2,150 = -2.27

23

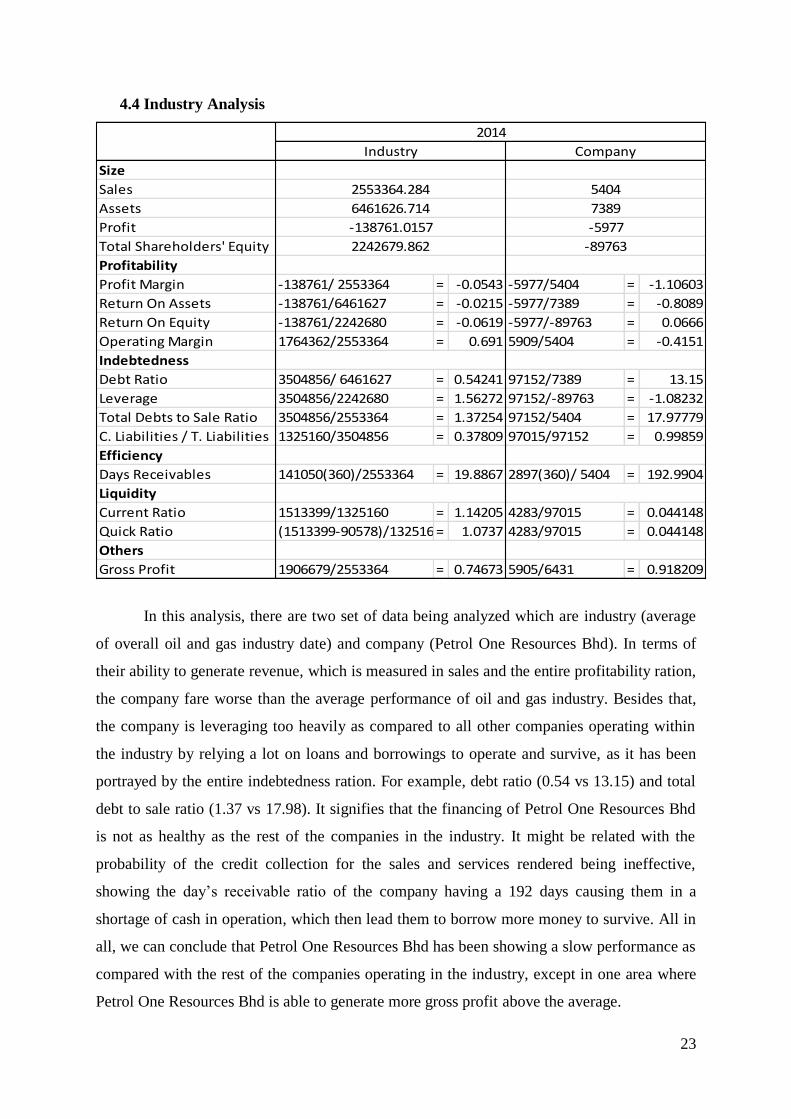

4.4 Industry Analysis

Size

Sales

Assets

Profit

Total Shareholders' Equity

Profitability

Profit Margin -138761/ 2553364 = -0.0543 -5977/5404 = -1.10603

Return On Assets -138761/6461627 = -0.0215 -5977/7389 = -0.8089

Return On Equity -138761/2242680 = -0.0619 -5977/-89763 = 0.0666

Operating Margin 1764362/2553364 = 0.691 5909/5404 = -0.4151

Indebtedness

Debt Ratio 3504856/ 6461627 = 0.54241 97152/7389 = 13.15

Leverage 3504856/2242680 = 1.56272 97152/-89763 = -1.08232

Total Debts to Sale Ratio 3504856/2553364 = 1.37254 97152/5404 = 17.97779

C. Liabilities / T. Liabilities 1325160/3504856 = 0.37809 97015/97152 = 0.99859

Efficiency

Days Receivables 141050(360)/2553364 = 19.8867 2897(360)/ 5404 = 192.9904

Liquidity

Current Ratio 1513399/1325160 = 1.14205 4283/97015 = 0.044148

Quick Ratio (1513399-90578)/1325160= 1.0737 4283/97015 = 0.044148

Others

Gross Profit 1906679/2553364 = 0.74673 5905/6431 = 0.918209

-138761.0157

2242679.862

2014

CompanyIndustry

5404

7389

-5977

-89763

2553364.284

6461626.714

In this analysis, there are two set of data being analyzed which are industry (average

of overall oil and gas industry date) and company (Petrol One Resources Bhd). In terms of

their ability to generate revenue, which is measured in sales and the entire profitability ration,

the company fare worse than the average performance of oil and gas industry. Besides that,

the company is leveraging too heavily as compared to all other companies operating within

the industry by relying a lot on loans and borrowings to operate and survive, as it has been

portrayed by the entire indebtedness ration. For example, debt ratio (0.54 vs 13.15) and total

debt to sale ratio (1.37 vs 17.98). It signifies that the financing of Petrol One Resources Bhd

is not as healthy as the rest of the companies in the industry. It might be related with the

probability of the credit collection for the sales and services rendered being ineffective,

showing the day’s receivable ratio of the company having a 192 days causing them in a

shortage of cash in operation, which then lead them to borrow more money to survive. All in

all, we can conclude that Petrol One Resources Bhd has been showing a slow performance as

compared with the rest of the companies operating in the industry, except in one area where

Petrol One Resources Bhd is able to generate more gross profit above the average.

24

4.5 Credit Analysis

Focusing more of our attention towards the credit of its company due to its high

amount of loans and borrowings to the point it is exceeding its asset, we do think that

presenting the result analysis would be a good complementary towards other analysis we

have performed earlier.

Referring to the credit analysis on Petrol One Resources Berhad on International

Emerging Market, this company is scored higher than only 26.19% of companies in the

industry, which equates to D - High Risk on the Business Scale (EMIS, 2016). The

relative weakness stated is sales, sales growth and net income. EMIS was issuing

disclaimer on this, which we should take into consideration as it has been a primary go-to

source for investors an business leaders in making decisions.

5. Setting Materiality and Assess Acceptable Audit Risk and Inherent Risk

5.1 Setting Materiality Level

In deciding the level of materiality that we are going to use in determining whether

the omission of certain part would significantly alter the economic decision being made

by the users, we will take some matters into our consideration.

First and foremost, we are considering the disclaimer opinion for the year 2012 until

2014 for Petrol One Resources Bhd being expressed by KPMG Malaysia as the

company’s former auditor. The disclaimer opinions serve as precaution for us as the

appointed auditor to do a more thorough checking and review when we are auditing the

company.

Secondly, we have found inconsistencies between the figures posted in the annual

report and the audited figures of financial statements available in EMIS, an institutional

investment website for investors and analysts. This serves as another cautionary for us as

the risk of the misstatement are evident.

Thirdly, as the result of credit analysts put Petrol One Resources Bhd in D list (High

Risk on the Business Scale); we will hence need to take the risks into account too.

Fourthly, considering the company is having liquidity problem with its liabilities

exceeding its assets and the current outlook of the industry is in high volatility and not

very well either; it will not only mean that a lot more stakeholders will rely on our audit

report, but it will also mean that a little mistake might bring a fatal blow to the company

which is relatively unhealthy in terms of its financial condition. Hence, a careful and

25

thorough checking and review would be factored in deciding the level of materiality

which is not only economically and time efficient for auditor and its client, but also it is

highly reliable with its reasonable assurance for the users to rely on.

Fifthly, figuring out the fact that there are 3 major areas in high risk category which

are: account receivables, liabilities and stockholders’ equity, as well as sales and cost of

sales; a thorough audit and review shall be necessary in ensuring that it is reasonably

reliable.

Hence, after taking the aforementioned factors into consideration and the nature of the

company being risk taker; our auditing company has decided to set 5% materiality level –

strict enough to not miss any material misstatements but economically wise enough to not

put our client in deeper financial difficulty.

5.2 Assessing Acceptable Audit Risk

Acceptable audit risk or normally referred as audit assurance is a measure of how

willing are we as an auditor to accept that the financial statements might be materially

misstated after the audit is done and an unqualified opinion has been issued. Considering

our client’s company size with its less than 50 employees, the degree of the external users

might rely on our audit report especially those creditors that our client has been

borrowing the money from, and the likelihood that the financial difficulties that our client

are facing might be getting severe; we have decided to set the acceptable audit risk to 3%

- which is fine to contain material statement but not powerful enough to bring adverse

effects towards our client and the stakeholders in general.

5.3 Assessing Inherent Risk

Inherent risk measure the auditor’s assessment of the tendency that there are material

misstatement due to error or fraud in a segment before considering the effectiveness of

internal control (Alvin A. Arens, 2014). As the auditor, we have conclude that the area of

sales and its cost of sales is assessed as high inherent risk, while receivables, liabilities

and stockholders’ equity are assessed as lower inherent risk based on our findings from

the analytical procedures we conducted in the earlier section. In addition to the increasing

high inherent risk, we would appoint more experienced staff in performing further

investigations and extensive tests to the sales and cost of sales in regards of achieving

reasonable assurance.

26

6. Internal Control

6.1 Control Environment

The control environment consist of policy, procedures and action that reflect the

attitude of the top management towards the internal control in the organization.

One of the subcomponent under control environment is communication and

enforcement of integrity and ethical value. This include the management’s actions to

remove or reduce the intention of employees to do unethical actions. The most effective

way to implement achieve this is implementation of whistleblowing policy.

Whistleblowing means employees reporting about suspected misconduct, illegal acts or

failure to act within the company. The objective of this policy is to encourage employees

and others to raise their concern about wrong doing and come forward to voice those

concerns to management.

Normally, the first to realize that there may be something seriously wrong within the

organization are employees. After detailed observation and analysis on Petrol One

Resources Berhad, we found that this company is not implementing whistle blowing

policy. Without whistleblowing policy, the unethical action within the company is

difficult to detect. This will increase the risk of fraud and error and deeply affect the

organization’s efficiency and long-term success.

Another subcomponent in control environment is commitment to competence. Petrol

One Resources Berhad is a small company with only 1 to 50 employees. Qualified and

motivated employees are the precondition for each successful oil and gas company.

However, Petrol One Resources is not focusing and high concern on employees’

competence since there are no any written policies and procedures relating to areas of

competence such as recruitment, hiring, training exist and communicated to all the

employees. Without continuous improvement of skills and knowledge, the employees in

the company most probably could not catch up with the changes and the growth in oil and

gas industry.

Besides, the significant subcomponent of control environment that Petrol One

Resources Berhad fail to achieve is participation of board of director or audit committee.

This failure is significant shown through the turnover of the director in fiscal year of 2015.

In the year end of 2015, there are seven Directors on the board, comprising two Executive

directors and five Non-Executive Directors. The composition of the Board is well-

balanced and represents a good mix of skills, knowledge and experience. However, the

27

turnover of directors is high within this year. There are 2 directors resigned from the

group and 3 directors were appointed during the financial year.

Name of director Date of resigned and appointed

Azlan Shairi Bin Asidin

Appointed as an Executive Director cum Chief

Executive Officer w.e.f. 11 November 2014

Ahmad Nainy Bin Mokhtar

Appointed as an Independent Non-Executive

Director w.e.f. 6 February 2015

Chris Lim Su Heng

Appointed as an Independent Non-Executive

Director w.e.f. 2 March 2015

Lim Kian Boon

Resigned as the Managing Director w.e.f. 11

November 2014

Wisun Soon

Resigned as an Independent Non-Executive

Director w.e.f.11 November 2014

(Petrol One Resources Bhd, p.19, 2015)

The turnover of director will result in the poor communication among Directors.

There will be a time gap for every new directors appointed to the board to understand the

board responsibilities and management. This may result in the inactiveness of the Board

and reduce their efficiency of action and effectiveness to internal control implementation.

Moreover, we recognize Petrol One Resources Berhad is a risk taker in its

management philosophy and operating style. In 2014, the current ratio of the company has

decrease to 0.04 from 0.32 from 2012. The decrease in current ratio give a very significant

view that the ability of the company to pay their short term debt is decreasing. However,

Petrol One Resources Berhad keeps getting more loan from financial institution without

considering their ability to pay for the short- term and long-term obligation. The risk of

Petrol One Resources Berhad unable to pay for its debt is very high and this has arisen the

substantial doubt about going concern of the company.

28

6.2 Information System and Communication

Information system and communication is one of the components of internal control.

It is establishment of an information system to manage and communicate the

organization’s activities and prepare financial statements. Information system and

communication is enabling to supports understanding and execution of organizational

objectives and individual responsibilities at all levels of the organization. Communication

can flow down, up, and across all levels of an organization to effective. This includes not

only emails, office memorandums, and staff meetings; but also more formal

communications like position descriptions, employee evaluations, and agency and

statewide policy and procedures. It is critical that employees understand organizational

objectives, including internal control objectives, and their specific role in achieving them.

In the group, the Senior Management adopt‘ open-door’ and ‘hands-on’ approach in

the daily operational activities to improve the workflow throughout the Group and to

enhance overall communication effectiveness. (Petrol One Resources Bhd, p.18, 2015)

6.3 Monitoring

Third is monitoring, the Board recognizes and think to increasing of maintaining a

risk management and internal control system and affirms its ultimate responsibility for the

Group’s risk management and internal control that covers the determination of the risk

profiles, appetite and level of tolerance, the implementation of appropriate processes and

control actions to manage the significant risks, and the periodical review and monitoring

of the effectiveness of the system to ensure its adequacy and integrity to enable the Group

to achieve its goals and objectives as well as to safeguard the shareholders’ investments

and the Group’s assets. The Management, which comprises Directors with executive

function, is assigned to implement the Board’s policies and practices on risk and control.

Besides that, the Group’s risk management and system of internal controls are designed to

manage rather than eliminate the risks that may impede the achievement of its corporate

objectives.

Other than that, the Group’s risk management and internal control extends to all

aspects of its activities. The Board is dedicated to ensure that the Group’s corporate

strategies are set in congruence with its risk profile and degree of tolerance. The risk

management structure and control mechanism for financial, operational, environmental

and compliance matters with Board’s participation, is put in place and embedded

throughout the Group during the financial year under review and up to the date of

29

approval of this Statement, so as to manage the significant risks that may affect the

Group’s business objectives on a continuous basis and they also allow any new

significant risk identified being subsequently evaluated and managed.

To strengthen the Group’s risk management processes of identifying, evaluating,

monitoring and managing significant risks faced by the Group, administrative and

operational functions of the Group are centralized to maintain consistency in the setting

and application of policies and procedures relating to these functions. The structure helps

to reduce duplication or overlapping of efforts, close the possible coverage gaps and

create synergies to the Group. The Executive Directors and the Management, who are

accountable for the conduct and performance of the Group, practiced ‘open-door’ and

‘hands-on’ approach in their management of the day-to-day affairs and business activities

of the Group.

6.4 Control Activities

The Group has two reportable segments and which are the Group’s strategic business

units. The strategic businesses units offer different services, and are managed separately

because they require different technology and marketing strategies. For each of the

strategic business units, the Group’s Executive Director reviews internal management

reports at least on a quarterly basis. There two of the Group’s reportable segments:

Segment assets

The total of segment asset is measured based on all assets of a segment, as

included in the internal management reports that are reviewed by the Group’s

Executive Director. Segment total asset is used to measure the return on assets

of each segment.

Segment liabilities

Segment liabilities information is neither included in the internal management

reports nor provided regularly to the Group’s Executive Director. Hence, no

disclosure is made on segment liability.

6.5 Other Control Activities

Proper documentations to define the duties and responsibilities of the Board

and each of its committees.

30

Key functional units are managed by experienced and dedicated team of

personnel.

Defined levels of authority for day-to-day business aspects of the Group

covering procurement, payments, capital expenditures, investments and

recruitment have been made known to all personnel.

Clear organization structure, comprising Business Operations and Finance, to

facilitate the implementation of risk management and control procedures.

The executive directors participate directly in the daily management of the

Group, and report to the Board on significant changes in business environment

as well as relevant corporate, legal, accounting and market developments

which might affect the business of the Group.

31

6.6 Corporate’s Structure

BOARD OF DIRECTOR AUDIT COMMITEE

PRESIDENT

GENERAL MANAGEMENT

Bunker

Offshore

Support

Services

Floating

Storage and

Offloading

Storage

Shipping and

Forwarding

INTERNAL

AUDIT

Ship

Management

32

7. Audit Procedure

Audit procedures are performed in order to test financial statement assertions. Therefore,

the first step in audit procedure is to identify the management assertions that needed to be

tested and relative audit objective. Management assertions are the assertions by management

about the accuracy of the financial statement components. There are seven broad

management assertions which are existence, occurrence, rights and obligations, completeness,

valuation or allocation, measurement, and presentation and disclosure. The audit objective is

set to check these management assertions. It consist of two types: transactions-related and

balance-related audit objective.

Management Assertions Definitions

Existence Relates to whether ending balances of assets, liabilities,

and equity interests included in the financial statements

actually exist at the date of the financial statements.

Occurrence Relates to whether all recorded transactions have occurred

and pertain to the entity.

Rights and obligations Relates to whether the entity holds or controls the rights to

assets included on the financial statements, and that

liabilities are obligations of the entity.

Completeness Relates to whether all transactions that occurred during the

period have been recorded, whether all assets, liabilities,

and equity interests that should have been included as

ending balances on the financial statements have been

included and whether all disclosures that should have been

included in the financial statements have been included.

Valuation or allocation Relates to whether assets, liabilities, and equity interests

included in the financial statements are at appropriate

amounts and any resulting valuation or allocation

adjustments are appropriately recorded.

Measurement Relates to whether a transaction or event is recorded at the

proper amount and revenue and expense are allocated to

the proper period.

Presentation and disclosure Relates to whether components of the financial statements

are properly combined or separated, described and

33

disclosed.

After running of risk assessment and the ratio analysis on Petrol One Resources Berhad,

we have decided to test these management assertions together with relative audit objectives

on the dubious, improbable, and high risk areas such as liabilities and owner’s equity, sales

and cost of sales, account receivables. Substantive procedures are performed to detect

whether there are any material misstatements in these areas.

7.1 Management Assertions for Liabilities and Owner’s Equity

Management

Assertions

Balances-Related

Audit Objective Substantive procedure

Existence Existence Trace a sample of trade payables to the

purchase invoices, to confirm the existence

of the transaction of purchasing goods.

Completeness Completeness Examine all loan and borrowings contracts,

cast the amount and agree the amount with

the balances amount on balance sheet to

confirm there all loan and borrowing exist

has been counted and included in the loan

summary.

Valuation or

allocation

Accuracy

Recheck the price of shares and the amount

of outstanding shares to ensure the price

used to value the shares are materially

correct and the extensions of prices times

the number of shares are correct and detail

are correctly added.

Cutoff Examine a sample of shipping documents

and purchase invoices for a few days before

and after year-end to confirm the purchase

cutoff at year-end is proper.

Classification Examine the account on the balance sheet

to confirm the equity items are properly

classified as to common stock(ordinary

34

shares), preference shares and reserves

Rights and obligation Rights and obligation Examine the loan contract to confirm entity

has legal title or obligation to the debts

shows on the balance sheet

7.2 Management Assertions for Sales and Cost of Sales

Management

Assertions

Transaction-

Related Audit

Objectives

Substantive Procedure

Existence or

occurrence

Existence Examine the profile of customer to confirm

the recorded sales are for shipments made

to non-fictitious customers.

Completeness Completeness Examine cost of goods sold in all sales

transaction and agree it with the beginning

inventory and ending inventory to ensure

all existing cost of goods sold is are

recorded and there is no any intentionally

omission of cost.

Valuation or

allocation

Accuracy Recheck the selling price and relative

quantity sold for sale transactions in

samples of sale invoice and general journal

to ensure recorded sales are for the amount

of goods shipped and are correctly billed

and recorded.

Timing Examine the dates of receiving the order,

shipment and payment to ensure the sales

are recorded on the correct dates.

Posting and

Summarization

Review the daily sales records updated on

computer accounting system and monthly

statement to ensure sales transactions are

properly included in the master file and are

correctly summarized.

35

7.3 Management Assertions for Account Receivables

Management

Assertions

Balance-Related

Audit Objectives Substantive Test

Existence or

Occurrence

Existence Test debtor’s subsidiary ledger and

supporting documents such as sales invoice

and delivery notes to confirm the account

receivables are authentic obligations owed

by customers at the balance date

Completeness Completeness Examine the sales invoice and delivery

notes, cast the amount and agree the

amount with sales journal to ensure

accounts receivables include all amounts

owed by customer at the balance date

Rights and

obligations

Rights and

Obligation

Review the general procedures of the sales

transaction and make inquiry with relevant

customers to confirm the accounts

receivables are owed to the company and

not pledged to other claims.

Valuation or

allocation

Accuracy Verify price, quantity and the computation

on sale invoices and agree the price to

master price list to ensure the account

receivables are stated at the correct amount.

Cutoff Test cash receipts and sales transaction for

a few days before and after year end to

confirm the sales cutoff at year end is

proper.

36

8. Overall Audit Plan

Auditor Contact

Details

Name: Ana, JR and SY, CAs

Address: 13, Jalan Multimedia, Persiaran Multimedia, 63000

Cyberjaya, Selangor Darul Ehsan.

Auditee Contact

Details

Address:

Regus, Level 8,

Tower 8, Avenue 5

The Horizon Phase 2,

59200 Kuala Lumpur Wilayah Persekutuan, Malaysia.

Telephone (m):

03-20849000

Audit Objective The objective of this audit was to determine whether Petrol One

Resources Berhad adequately enforced compliance with the

Company Acts, 1965.

Scope of Audit Standards complied:

Malaysia Accounting Standard Board (MASB)

Business size:

50 employees

Industry:

Refining and Marketing in Oil and Gas Industry

Type of services:

- Shipping and forwarding

- Floating storage and offloading

- Offshores support services

- Bunker

- Ship management

Business hour:

Regular hour, Monday- Friday

Type of audit:

Team Audit

Language:

English

37

High Risk Area:

Liabilities and owner’s equity

Account receivables

Sales and cost of sales

Materiality Level:

5%

Scheduled Time

and Proposed

Duration of Audit

The first payment of audit fees is expected to be made on 1st March

2016 and the second payment on 1st June 2016. The duration of audit

will start from the day both parties signed the engagement letter, or

latest by the day the client has made its first fees payment.

Auditor has rights to access any information and document of Petrol

One Resources Berhad at any reasonable time within the period for

completing the audit works. The audit work is expected to be

completed on 5th

June 2016 while the audit report is expected to be

prepared and sent to Petrol One Resources Berhad on 5th

June 2016.

Hence, the expected total duration of the audit is 3 months

considering the size and complexity of the company and industry as

we have been appointed as the sole auditor for the group.

38

9. Conclusion

As a closing remark, generally the need of a company being independently audited by

external audit firm has been playing a key roles of gaining the trust and confidence of the

stakeholders of the company is indeed true. In a turbulence economy with less certainty

of what is about to happen tomorrow in the market, auditing and its assurance services

come into the light bringing in-depth analysis and ensuring that the financial statements

and other statements they give their opinions at truly give a true and fair view of the

current economic condition, helping the users to make a sound economic decision.

While many steps have to be taken to achieve that goal, we came to realize that

planning an audit will lead us few steps closer to the success of an audit. Fail to plan an

audit means that we are planning to fail the audit itself. The eight components of audit

planning, starting from understanding the client to forming the overall audit plan, will

guide the auditor, each step at a time in building a comprehensive audit planning which

eventually will serve as a guideline of what to do and what not to do to complete the

whole process of audit.

These results lead to the conclusion that audit planning is a must skill to have for an

auditor considering its importance in conducting a successful audit. Having the hands on

experience on crafting an audit plan for Petrol One Resources Bhd. itself is truly an

enriching and learning journey for us to become the next auditor with integrity.

39

References

ACCA. (2015, August 18). Acceptance Decisions for Audit and Assurance Enggagement.

Retrieved from ACCA: http://www.accaglobal.com/ie/en/student/exam-support-

resources/professional-exams-study-resources/p7/technical-articles/acceptance-

decisions.html

Accounting Tools. (2016). Horizontal Analysis. Retrieved from Accounting Tools:

http://www.accountingtools.com/horizontal-analysis

Accounting Tools. (2016). Vertical Analysis. Retrieved from Accounting Tools:

http://www.accountingtools.com/vertical-analysis

AICPA. (2012). Planning an Audit. Retrieved from AICPA:

http://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/AU-

C-00300.pdf

Alvin A. Arens, R. J. (2014). The Audit Process. In A. A. Arens, R. J. Elder, M. S. Beasley,

N. A. Amran, R. Shafie, & M. Yusof, Auditing and Assurance Services in Malaysia

(pp. 194-195). Kuala Lumpur: Pearson Malaysia.

Burke, A. (2016). Introduction to Audit Planning. Retrieved from CPA Ireland:

http://www.cpaireland.ie/docs/default-source/Students/Study-Support/P1-

Auditing/introduction-to-audit-planning.pdf?sfvrsn=0

Bursa Malaysia. (2015, January 27). Main Listing Requirement: Criteria and Obligations of

PN 17 Issuers. Retrieved from Bursa Malaysia:

http://customer.bursamalaysia.com:8080/MainLR/Pages/MainPracticeNote17.aspx