axa · moody's investors service financial institutions 3 5 december 2016 axa: update...

TRANSCRIPT

FINANCIAL INSTITUTIONS

CREDIT OPINION5 December 2016

Update

RATINGS

AXADomicile Paris, France

Long Term Rating A2

Type Senior Unsecured -Dom Curr

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Analyst Contacts

Dominic Simpson 44-20-7772-1647VP-Sr Credit [email protected]

Brandan Holmes 44-20-7772-1605VP-Senior [email protected]

Alexandra Aspioti 44-20-7772-5315Associate [email protected]

Antonello Aquino 44-20-7772-1582Associate [email protected]

AXAUpdate incorporating consolidated scorecard

Summary Rating RationaleMoody’s rates AXA SA A2 for senior debt, and its main operating subsidiaries Aa3 forinsurance financial strength – all rated entities have a stable outlook. The ratings reflectthe AXA Group’s (“AXA” or “Group”) very strong franchise and business and geographicdiversification, resilient and relatively stable operating performance, strong asset/liabilitymanagement, and prudent reserving practices. Less positively, AXA faces the challenges ofprotecting the investment margin within its life business particularly in markets like Germanyand Switzerland which are the most affected by the very low interest rate environment.Furthermore, we view the Group’s economic capitalisation as lower than some of its Aa ratedpeers, and its level of goodwill and intangible assets remains high.

AXA SA is the ultimate holding company of the Group and is listed on Euronext. Its life andnon-life insurance subsidiaries have leading positions in several major insurance markets.AXA is market leader in France, where AXA France IARD (Aa3 insurance financial strengthrating) is number two in P&C and AXA France Vie (Aa3 IFSR) is number three in life, inSwitzerland (AXA Versicherungen AG, Aa3 IFSR, and AXA Leben AG) and in Belgium (AXABelgium, Aa3 IFSR). The Group also holds strong market positions in Germany (AXA Konzern,Aa3 IFSR for the main operating entities), in the life market in the United States (AXAEquitable Life Insurance Company, Aa3 IFSR, MONY Life Insurance Company of America, A1IFSR), in the UK and Irish P&C market (AXA Insurance UK plc, Aa3 IFSR, AXA Insurance Ltd,A1 IFSR), in Japan and in Central and Eastern Europe.

AXA's senior debt is rated two notches below the IFSR of its main operating subsidiaries,which is narrower than the standard three notches. This notching primarily reflects the highlevel of geographic and business diversification of the Group, as well as the strong liquidity atthe holding company level, thanks to centralised treasury management, stand-by revolvingloan facilities from several banks and a liquidity contingency plan.

On 9 September 2016, Moody’s affirmed AXA’s ratings with a stable outlook.

Credit Profile of Significant SubsidiariesThe Aa3 IFSRs of AXA's main subsidiaries in France, Switzerland, the US, Germany, Belgiumand the UK benefit from one or two notches of implicit support, reflecting their strongcontribution to AXA's revenues and profits and their strategic relevance to the group.

The A1 IFSR of AXA Insurance Ltd, AXA's Irish subsidiary, benefits from implicit support fromthe AXA Group. Although relatively small, AXA Insurance Ltd is a leading and profitable P&Cinsurer in its market and fits well within the strategy of the AXA Group.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 5 December 2016 AXA: Update incorporating consolidated scorecard

For more information on the credit profiles of: 1) AXA France IARD and AXA France Vie; 2) AXA Versicherungen AG, and AXA LebenAG; 3) AXA Lebensversicherung AG, AXA Versicherung AG, AXA Krankenversicherung AG which are the most important operatingentities of AXA Konzern AG; 4) AXA Equitable Life Insurance Company, please refer to our separate Credit Opinions on these entities.

AXA Insurance Group UK

Moody's Aa3 IFSR of AXA's UK P&C business reflects both the benefits of ownership by AXA and the particular characteristics of thesebusiness units. AXA's non-life insurance franchise in the UK is good, as evidenced by its top five market position. AXA has made severaladd-on acquisitions in the UK since 2006 to get better access to the broker and direct sales distribution channels, although the Grouphas announced the disposal of Bluefin, its UK P&C commercial broker, which is expected to finalised in Q1 2017. The Group writes bothcommercial and personal lines with a particular focus on the SME sector. The Group continues to focus on operational improvements,although P&C profitability in individual lines remains one of the credit weaknesses of AXA in the UK. Going forward, the Group’s UKbusiness is focused on Property & Casualty, Health and Asset Management.

In Life, the Group has recently sold its UK (non-platform) investment and pensions business and its direct protection business(“Sunlife”) to Phoenix Group Holdings, which follows the earlier sale of its UK offshore investment bonds business (“AXA Isle of Man”)to Life Company Consolidation Group, and sale of the wrap platform business (“Elevate”) to Standard Life.

Credit Strengths

» Very strong franchise with leading positions in several major insurance markets

» High degree of business and geographic diversification

» Resilient and relatively stable operating performance

» Strong asset/liability management, and prudent reserving practices

» Sound liquidity position, reflecting the conservative debt management, the existence of significant alternative sources of liquidityand the benefit of its centralized treasury management

Credit Challenges

» Protecting the investment margin within its life business within the very low interest rate environment

» Lower economic capitalisation than some its Aa-rated peers

» High level of goodwill and intangible assets

» Potential losses from legacy VA business

Rating OutlookThe outlook is stable.

What to watch for:

» Underlying profitability development in key mature markets and in emerging countries

» Solvency II ratio level and volatility

» Evolution of investment portfolio in light of low interest rate environment

» Impact of significant number of recent senior management appointments, including appointment of Thomas Buberl as Group CEO,and new CEO appointments in Belgium, France, Germany, Japan, UK, Global P&C, Global Life & Health, and Emerging Markets

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

3 5 December 2016 AXA: Update incorporating consolidated scorecard

» Progress in achieving financial objectives including adjusted return on equity between 12% and 14% over the period 2016E-2020E,Solvency II ratio target range between 170% and 230%, Euro 2.1 billion pre-tax cost savings by 2020E, Property & Casualty all yearcombined ratio at 94-95% by 2020E, Euro 350 million additional Life and Savings underlying earnings from in-force initiatives by2020E

» Turkish non-life operating performance

What Could Change the Rating - DownDownward pressure would develop on AXA’s ratings in case of: 1) a sustained rise in adjusted financial leverage beyond 30% and/or; 2)deterioration in profitability as evidenced by a Return on Capital (Moody’s definition) consistently below 5% and fixed charge coverageconsistently below 5x and/or; 3) Group Solvency II ratio falling below 170% and/or; 4) a deterioration in asset quality.

What Could Change the Rating - UpUpward pressure would develop in case of: 1) a sustainable reduction in adjusted financial leverage to nearer 20% and/or; 2) asustainable improvement in the Group's capitalisation level and quality and/or; 3) improvements in profitability as evidenced by aReturn on Capital consistently above 8% and fixed charge coverage consistently above 8x across the underwriting cycle.

Any downgrade/upgrade of AXA’s ratings would place downward/upward pressure on those subsidiaries which receive support fromAXA.

Key Indicators

Exhibit 1

[1] Information based on IFRS financial statements as of Fiscal YE December 31[2] Certain items may have been relabeled and/or reclassified for global consistency

DETAILED RATING CONSIDERATIONSMoody’s assigns IFSRs to insurance operating companies which are analyzed at an “analytic unit” level. For some complex insurancegroups which comprise more than one analytic unit, Moody’s supports its analysis by also preparing a Moody's insurance financialstrength rating scorecard using consolidated group financial information. The consolidated scorecard facilitates a holistic view of thegroup and improves transparency of key credit strengths and weaknesses. The scorecard, shown and discussed below, produces anotional group IFSR which may differ from ratings assigned to any particular operating companies in the group.The Aa3 notional groupIFSR for AXA is in line with the adjusted rating indicated by the Moody's insurance financial strength rating scorecard below.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

4 5 December 2016 AXA: Update incorporating consolidated scorecard

MARKET POSITION: Aa - VERY STRONG GLOBAL FRANCHISE WITH LEADING POSITIONS IN SEVERAL LIFE AND NON-LIFEMARKETS

AXA has a very strong global footprint, with leading positions in several major life and non-life insurance markets and global brandrecognition. AXA is the largest European insurer in terms of gross written premium (EUR92bn), and its very strong franchise, whichMoody’s expects AXA to maintain, includes leading market positions in France, Switzerland, Belgium, the UK and Ireland. Furthermore,the Group is active in 10 Asian countries with strong market positions in China, Indonesia, Hong Kong and Thailand. In addition, AXA isa leading global health player.

DISTRIBUTION: Aa - GOOD DIVERSITY, GOOD CONTROL

AXA’s distribution is viewed as strong, with access to a diversified number of distribution channels and a high weight of proprietarychannels in its distribution mix. The group has strong agent networks in continental Europe and a high presence in the brokeragechannel. AXA also utilises several other channels to distribute its products including bancassurance agreements (including the largestbancassurance deal worldwide with ICBC in China), salaried sales-force, and direct. AXA also has overall a balanced mix betweencontrolled and non-controlled distribution channels, and we believe that the group has generally preferred positions with brokers andother partners (eg exclusive distribution agreements with banks).

PRODUCT FOCUS AND DIVERSIFICATION: Aa - VERY STRONG BUSINESS AND GEOGRAPHIC DIVERSIFICATION, BUT SOME RISKVIA LIFE LEGACY BOOK

AXA benefits from very strong business diversification. In 2015, the Group’s underlying earnings were well balanced between nonlife(39%), savings and asset management (36%), and protection & health (25%). AXA’s geographic diversification is also very strongbenefiting from meaningful amounts of revenue via France (its largest market which represents around 25% of premiums), the US,Germany, Switzerland, UK and Asia.

AXA’s main product risk is in its in-force traditional general account savings business which has relatively high guarantees in some of itsmarkets. However, the Group has no meaningful concentration risk to countries where investment spreads are low, notably Germany,where the spread between the average in-force average guarantee of 3.5% and the investment yield had reduced to zero at H1 16, andSwitzerland.

AXA also has a legacy portfolio of US variable annuities (~8% of total life reserves) with guaranteed benefits which has inherentcomplexity and volatility that can affect earnings and capital materially despite the use of hedging. However, over the past few years,AXA Equitable has lowered the risk profile of its VA business.

Going forward, we expect AXA’s life & savings risk profile to improve as the Group continues to focus on increasing the proportion ofcapital light products at the expense of its traditional general account products. The P&C risk profile, which currently benefits from theorientation towards personal lines, may increase as the Group seeks to increase commercial business.

ASSET QUALITY: A - OVERALL GOOD, BUT HIGH LEVEL OF INTANGIBLE ASSETS

AXA’s invested asset quality is good, including 42% of government and related bonds, 33% corporate bonds, 5% real estate and 3%listed equities as at H1 16. The quality of the fixed income securities also remains good with the average ratings of government/relatedand corporates bonds maintained at AA and A respectively. The Group has exposure to peripheral (mainly Italy and Spain) countrygovernment & related bonds but it is not excessive at around 8% of invested assets or 57% of total equity at H1 16, and the gross bookvalue has been relatively stable. The high risk assets as a % of shareholders’ equity ratio (which includes equities, investment property,and below investment grade/unrated debt securities) is relatively high (148% at YE15) but this is mitigated to some extent by theGroup’s ability to share losses with policyholders by managing its crediting rates, and also by hedging.

Going forward, we do not expect significant changes in AXA’s asset mix, although we expect the Group, like many of its peers, togradually increase more illiquid/riskier assets to counter the very low interest rates.

AXA’s goodwill and intangibles to adjusted equity remains high at 73% at YE15 (YE14: 70%), although this includes a significantproportion of deferred acquisition costs, and reduces to 53% if adjusted for URF, URR, Minority Interests, PB & tax.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

5 5 December 2016 AXA: Update incorporating consolidated scorecard

CAPITAL ADEQUACY: A - GOOD AND RELATIVELY STABLE, ALTHOUGH SOLVENCY II RATIO SIGNIFICANTLY INFLATED BY USE OFEQUIVALENCE

AXA’s capitalisation strengthened during 2015, illustrated by an improvement in its Solvency II ratio to 205% (YE14: 201%) which iscomfortably within the group’s target range of 170-230%, and by the 7% increase in total equity (which includes €9.5bn of perpetualdebt) to €72.6bn. The Group’s Solvency II / previously reported economic solvency ratio has been relatively stable in recent years(eg: YE13: 206%, YE12: 199%). At 9m 2016, the ratio dropped to 191%, negatively impacted by the fall in interest rates as well as thechange in EIOPA’s reference portfolio with regard to the Volatility Adjuster, but the reported figure compares well to peers. However,we view the Group’s economic capitalisation as lower than some of its Aa-rated peers, as the public ratio is significantly inflated by theuse of equivalence for the Group’s US business.

Going forward, we expect AXA’s capitalisation to remain good, but like many of its peers, the Group’s solvency ratio is sensitive tofinancial market movements as seen during 9m 16.

PROFITABILITY: A - RESILIENT AND RELATIVELY STABLE OPERATING PERFORMANCE, NOTWITHSTANDING LOW INTEREST RATEHEADWIND

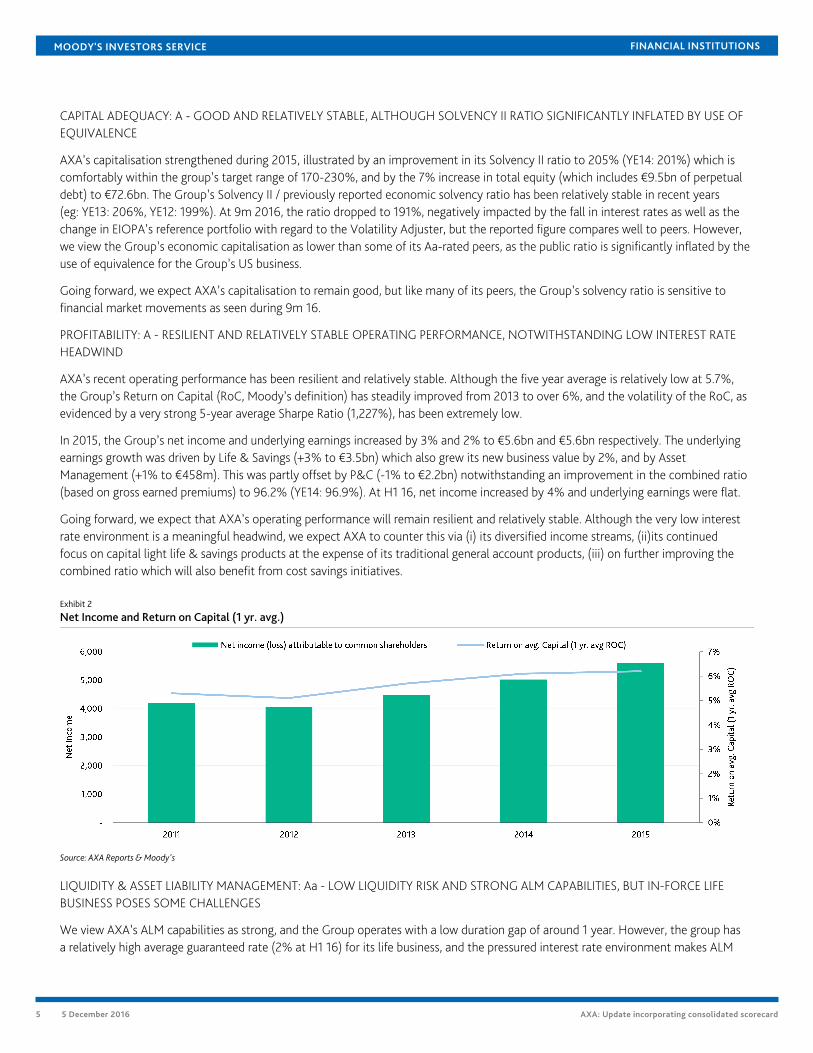

AXA’s recent operating performance has been resilient and relatively stable. Although the five year average is relatively low at 5.7%,the Group’s Return on Capital (RoC, Moody’s definition) has steadily improved from 2013 to over 6%, and the volatility of the RoC, asevidenced by a very strong 5-year average Sharpe Ratio (1,227%), has been extremely low.

In 2015, the Group’s net income and underlying earnings increased by 3% and 2% to €5.6bn and €5.6bn respectively. The underlyingearnings growth was driven by Life & Savings (+3% to €3.5bn) which also grew its new business value by 2%, and by AssetManagement (+1% to €458m). This was partly offset by P&C (-1% to €2.2bn) notwithstanding an improvement in the combined ratio(based on gross earned premiums) to 96.2% (YE14: 96.9%). At H1 16, net income increased by 4% and underlying earnings were flat.

Going forward, we expect that AXA’s operating performance will remain resilient and relatively stable. Although the very low interestrate environment is a meaningful headwind, we expect AXA to counter this via (i) its diversified income streams, (ii)its continuedfocus on capital light life & savings products at the expense of its traditional general account products, (iii) on further improving thecombined ratio which will also benefit from cost savings initiatives.

Exhibit 2

Net Income and Return on Capital (1 yr. avg.)

Source: AXA Reports & Moody's

LIQUIDITY & ASSET LIABILITY MANAGEMENT: Aa - LOW LIQUIDITY RISK AND STRONG ALM CAPABILITIES, BUT IN-FORCE LIFEBUSINESS POSES SOME CHALLENGES

We view AXA’s ALM capabilities as strong, and the Group operates with a low duration gap of around 1 year. However, the group hasa relatively high average guaranteed rate (2% at H1 16) for its life business, and the pressured interest rate environment makes ALM

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

6 5 December 2016 AXA: Update incorporating consolidated scorecard

more challenging. This is especially the case in Germany where the average guaranteed rate is 3.5%. The sensitivity of the Group’ssolvency II ratio (-5% point reduction in scenario of a decrease in interest rates by 50bps) illustrates this risk, although AXA’s interestrate sensitivity is less than some of its peers. The liquidity of the group is viewed as very strong.

RESERVE ADEQUACY: Aa - CONSISTENTLY FAVOURABLE RESERVE DEVELOPMENT

The overall reserve adequacy of AXA, which has consistently released reserves, is considered strong. Over the last twelve years, theGroup’s prior year releases have benefited its combined ratio by an average of around 2% points. During 2015, the prior year releaseincreased slightly to 1% of gross earned premium (YE14: 0.6%) with positive developments in mature markets offsetting €179m ofdeterioration in Turkey following evolution in regulation/jurisprudence on bodily injury and material claims for MTPL. AXA’s reservingrisk benefits from its diverse book of business and orientation towards personal lines, and going forward we expect the Group tocontinue to report reserve releases.

FINANCIAL FLEXIBILITY: A - IMPROVED METRICS, WITH ADJUSTED FINANCIAL LEVERAGE BELOW 30%, ALTHOUGH EARNINGSCOVERAGE STILL RELATIVELY LOW FOR THE Aa RATING CATEGORY

The Group's financial leverage reduced again slightly to 26.9% (on Moody's basis, including adjustments for pensions and operatingleases) in 2015 (YE14: 27.3%) benefiting from the 7% increase in reported equity (excluding perpetual subordinated debt)notwithstanding a higher level of debt. 2014 was the first time in many years that AXA’s adjusted financial leverage had been below30%, and it remains at a level which is in line with Moody’s expectation for AXA’s rating level. Total leverage also reduced slightly to32.4% (YE14: 32.9%) which remains somewhat elevated but below historic levels of around 40%.At year-end 2015, double leverage atAXA SA increased to 148% (143%) (excluding the perpetual subordinated debt from the shareholders' equity).

At year-end 2015, the Group’s 5-year average earnings coverage improved again to 5.5x (YE14: 4.9x) benefiting from the 1 yearcoverage in 2015 improving to 6.7x (YE14: 6.2x). Although the 5-year average figure includes some exceptional items related to salesof subsidiaries, and Moody's considers the earnings coverage on an underlying basis to be resilient at above 5x, the ratio is still belowMoody's expectations for Aa companies. Going forward, whilst expecting further improvements in the 5-year average, we believe thatAXA's fixed charge coverage will remain somewhat constrained in the next few years, with meaningful improvements unlikely withouta reduction of the gross debt level.

Exhibit 3

Financial Flexibility

Source: AXA Reports & Moody's

AXA SA issues or guarantees most of the financial debt outstanding in the Group. As of 31 December 2015, the Group had aroundEUR20 billion (YE14: c.€19bn) of debt (excluding related derivatives and AXA Bank debt) outstanding, of which 87% was issued directlyby the holding company, 5% by AXA Financial, the remaining 8% by other subsidiaries (including bank overdrafts).

At year-end 2015, the debt mix was around 4% senior and 96% subordinated debt (excluding commercial paper and bank overdraft).The Group's debt repayment profile is sound, with an average maturity of 7.9 years as of 31 December 2015, assuming all early

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

7 5 December 2016 AXA: Update incorporating consolidated scorecard

redemption options are exercised (and excluding EUR2.7 billion of perpetual debts with no redemption options). Most of AXA's debt islong-dated.

Around EUR5.6 billion of debt (around 28%) is maturing between 2016 and 2020 (assuming the first call date as the de facto maturitydate), with the maturity profile benefiting from AXA issuing (i) GBP724 million and EUR984 million undated deeply subordinateddebts in November 2014 in connection with an exchange offer for four outstanding undated deeply subordinated debts with call datesbetween 2016 and 2019; (ii) EUR 1.0billion in May 2014 for refinancing of EUR1.5billion of senior debt which matured in January 2015;(iii) EUR 1.5 billion dated subordinated notes in March 2016 and (iv) USD 850 million undated subordinated notes in September 2016to refinance, in advance, part of AXA’s outstanding debt. As a result Moody’s believes the refinancing risk to be low.

Liquidity Profile

AXA SA's primary source of cash-flow is the dividend capacity of its insurance operations. In 2015, AXA SA received a lower EUR2,552million in dividends from its subsidiaries (2014: EUR3,342 million), whereas AXA SA incurred EUR1,094 million of interest expense(2014: EUR1,128 million) and the dividend paid in 2015 for 2014 was a higher EUR2,317 million (while the dividend paid in 2014 for2013 was EUR1,960 million).

Although the Group historically has not maintained a significant amount of cash and investments at the holding company level, cashand cash equivalents have been higher recently on AXA SA's balance sheet (EUR 2.8 billion and EUR 3.0 billion at year-end 2014and 2013), although the balance reduced a little to EUR2.6 billion at YE15. Cash is mostly invested in highly liquid money marketinstruments. AXA's liquidity is much stronger than the liquid resources held at the AXA SA level would suggest, thanks to a centralisedtreasury management, banking arrangements and a liquidity contingency plan. The Group has a centralized treasury management forsome of its European operations (including AXA France and the Group holding company AXA SA). AXA also has banking arrangements(either bilateral or syndicated) providing committed credit facilities of around EUR13 billion, undrawn at 31 December 2015.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

8 5 December 2016 AXA: Update incorporating consolidated scorecard

Rating Methodology and Scorecard Factors

Exhibit 4

AXA Group scorecard as at YE2015

[1] Information based on IFRS financial statements as of Fiscal YE December 31[2] The Scorecard rating is an important component of the company's published rating, reflecting the stand-alone financial strength before other considerations (discussed above) areincorporated into the analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

9 5 December 2016 AXA: Update incorporating consolidated scorecard

Ratings

Exhibit 5Category Moody's RatingAXA

Rating Outlook STASenior Unsecured A2Senior Unsecured MTN (P)A2Subordinate A3 (hyb)Junior Subordinate A3 (hyb)Junior Subordinate Baa1 (hyb)Commercial Paper P-1

Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

10 5 December 2016 AXA: Update incorporating consolidated scorecard

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1051512